U.S. Beef Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 63.97 Billion |

| Market Size (2026) | USD 65.34 Billion |

| Market Size (2031) | USD 72.64 Billion |

| Growth Rate (2026 - 2031) | 2.14% CAGR |

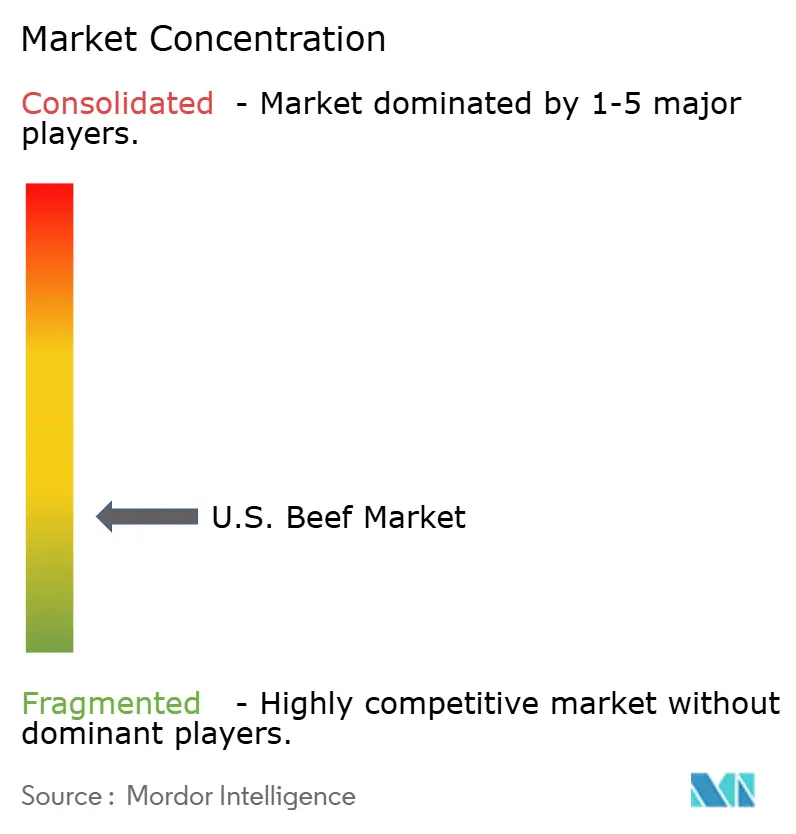

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Beef Market Analysis by Mordor Intelligence

In 2025, the U.S. beef market was valued at USD 63.97 billion, with projections to reach USD 72.64 billion by 2031, growing at a CAGR of 2.1% from 2026 to 2031. Domestic beef production dropped to 25.95 billion pounds in 2025, while the national cattle inventory fell to 86.2 million head, the lowest in 75 years. Despite high prices, per capita beef disappearance remained steady at 59.3 retail pounds, reflecting strong consumer demand. Off-trade channels led sales, but more volume shifted to supercenters, club stores, and online platforms. Buyers now prioritize traceability, verified claims, and premium products. Limited cattle supply and trade issues are driving processors and brands to focus on throughput, product mix, and premium programs in the U.S. beef market.

Key Report Takeaways

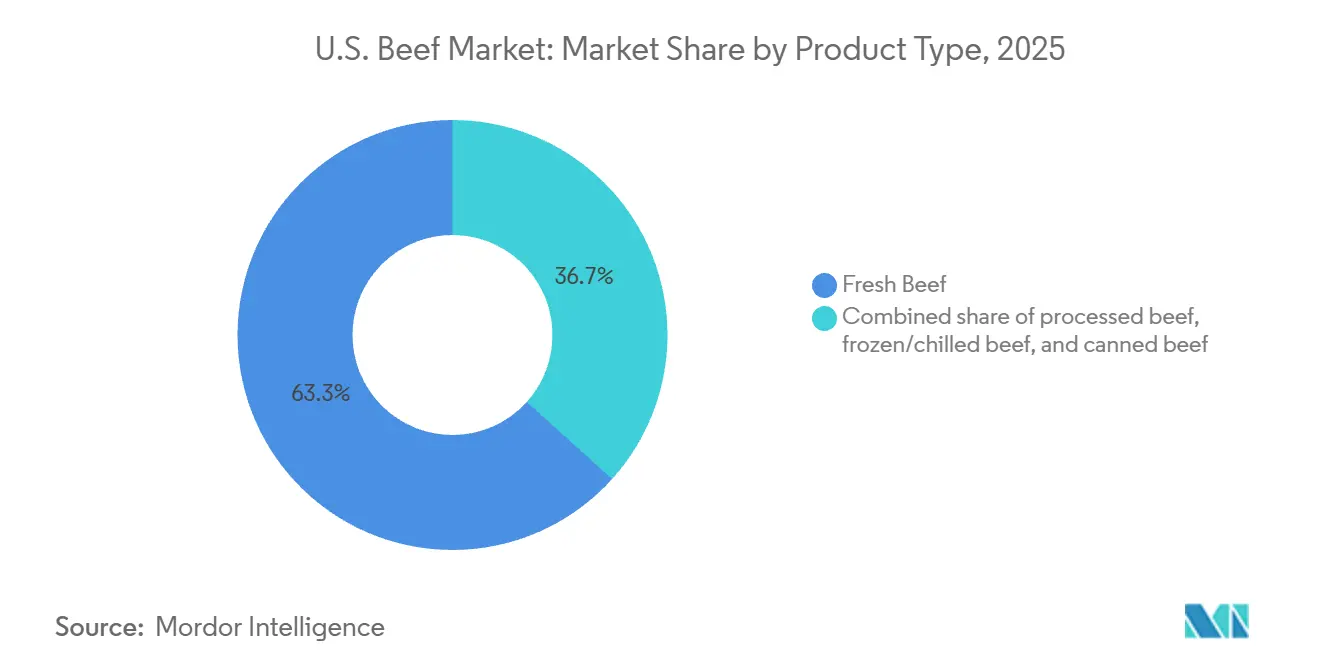

- By product type, fresh beef led with 63.32% of the United States beef market share in 2025, while frozen/chilled beef is projected to grow at a 2.35% CAGR through 2031.

- By nature, conventional beef held 95.34% share in 2025, while specialty beef is forecast to expand at a 3.52% CAGR through 2031.

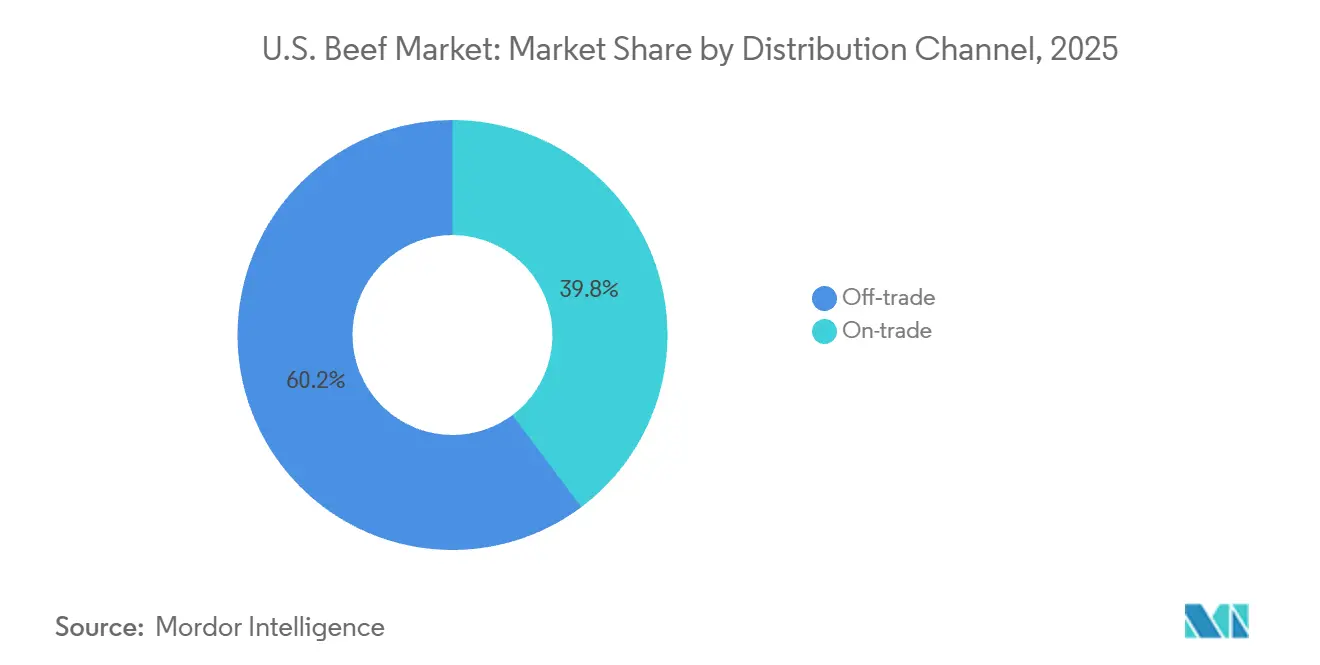

- By distribution channel, off-trade accounted for 60.23% of the United States beef market size in 2025, while on-trade is projected to advance at a 3.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Beef Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer dietary preferences and protein trends | +0.5% | National, with above-average pull in coastal metros and Sun Belt growth markets | Medium term (2–4 years) |

| Supply-chain traceability and transparency | +0.3% | National; technology uptake strongest in Midwest and Plains cattle-production states | Medium term (2–4 years) |

| Rising demand for shelf-stable beef snacks (jerky, biltong) in convenience channels | +0.4% | National, concentrated in South and West convenience-store corridors | Short term (≤ 2 years) |

| Premiumization via grass-fed and antibiotic-free processed beef claims | +0.4% | National, with premiums highest in Northeast and West Coast retail markets | Medium term (2–4 years) |

| Cultural and lifestyle associations with beef | +0.3% | National; strongest in Midwest, South, and Mountain West where beef culture is embedded | Long term (≥ 4 years) |

| Technology and production-system innovations | +0.2% | National; feedlot-heavy states — Iowa, Nebraska, Kansas, Texas — are early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer Dietary Preferences and Protein Trends

Despite ongoing price hikes, beef firmly retains its status as a dietary staple. In 2025, per capita retail beef disappearance stood at 59.3 pounds, a slight uptick from 59.1 pounds in 2024. This stability comes even as ground beef prices surged to USD 6.32 per pound and beef steaks climbed to USD 12.22 per pound, marking year-on-year jumps of 12.8% and 16.6%, respectively, as reported by the US Department of Labor in August 2025[1]Source: U.S. Department of Agriculture Economic Research Service, “Livestock, Dairy, and Poultry Outlook, December 2025”, ers.usda.gov. In 2024, over 90% of US consumers viewed beef positively or neutrally, with more than 70% recognizing meat and poultry as "nutrient powerhouses." Furthermore, 90% of consumers acknowledged the nutritional importance of protein. A less-discussed aspect is beef's cost advantage over chicken when considering protein value per gram. This advantage bolsters beef's central role in meals, even amidst rising retail prices. Additionally, the growing adoption of GLP-1 medications, which generally curtail caloric intake, has spurred a heightened demand for nutrient-dense, high-protein meals. This trend inherently favors beef over its lower-protein processed counterparts.

Rising Demand for Shelf-Stable Beef Snacks in Convenience Channels

The meat snack segment is expanding rapidly within processed beef, driven by high-protein diets and busy lifestyles. In 2024, millennials made up 62% of new meat product unit sales, while 53% of consumers combined scratch-cooked and semi-prepared items, boosting demand for convenience-format beef[2]Source: Food Marketing Institute, “The Power of Meat 2025”, fmi.org. At Expo West 2025, brands like Chomps, Archer, and Think Jerky showcased beef sticks and jerky as portable protein, aligning with mainstream retailers. As traditional grocery stores lose share to supercenters and online platforms, shelf-stable beef snacks are gaining popularity. Convenience-store operators, seeking higher-margin impulse items, are increasing their ambient beef snack offerings. Hormel Foods is capitalizing on this trend, with Q1 fiscal 2026 investments in an ambient meat snack facility in Jiaxing, China, and the May 2026 launch of the SPAM® Dog for roller grills and convenience-store channels.

Premiumization via Grass-Fed and Antibiotic-Free Processed Beef Claims

In 2025, the U.S. premium beef market saw strong growth, driven by increasing consumer demand for transparency, animal welfare, and health benefits. Grass-fed beef sales rose significantly, while organic meat continued its double-digit growth, showing consumers' willingness to pay more for unique products. USDA Agricultural Marketing Service data from May 2025 highlighted the pricing power of verified claims: a grass-fed ribeye steak sold for USD 38.28 per pound, a 172% premium over the commodity equivalent at USD 14.09. A key development, often overlooked, is USDA's August 2024 guideline update, which found antibiotic residues in 20% of samples from the "Raised Without Antibiotics" segment. This is pushing brands toward mandatory third-party certification, creating compliance challenges for smaller or unverified producers and concentrating premium pricing power among those with credible, auditable supply chains.

Supply-Chain Traceability and Transparency

Starting November 5, 2024, USDA's Animal and Plant Health Inspection Service (APHIS) will require electronic identification (EID) eartags for cattle and bison in interstate movement. These tags must be both visually and electronically readable. Electronic records enable state agencies to trace animals to their origin in under an hour, a significant improvement over the days or weeks needed with paper systems. In October 2024, USDA approved CattleProof's "Verified" as the first blockchain-based Process Verified Program (PVP) for cattle. This program allows ranchers to earn up to 150% premiums for certified animals and provides consumers real-time QR-code access to individual animal data. During an April 2025 congressional testimony, it was highlighted that the US beef supply chain had remained largely unchanged for 150 years. Blockchain-based digitisation is now addressing fraud risks, cash-flow delays, and export verification gaps. Traceability is shifting from a compliance requirement to a commercial advantage, with verified-origin beef commanding higher retail prices and improving export access, particularly in the EU and premium foodservice markets.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shifting dietary trends toward plant-based and alternative proteins | -0.3% | National, with stronger headwind in coastal metros among Gen Z and Millennial demographics | Medium term (2–4 years) |

| Animal-welfare and ethical-consumption pressures | -0.2% | National; particularly relevant in states with ballot-initiative animal welfare legislation | Long term (≥ 4 years) |

| Strict sanitary/phytosanitary and trade barriers | -0.3% | National trade policy, with disproportionate impact on export-oriented processing clusters in Midwest and Plains | Short term (≤ 2 years) |

| Environmental and climate-change regulations | -0.2% | National, with feedlot-intensive states — Iowa, Nebraska, Kansas, Texas — facing highest regulatory exposure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shifting Dietary Trends Toward Plant-Based and Alternative Proteins

Plant-based meats pose a long-term challenge to beef but remain a limited immediate threat. Between 2021 and 2024, weekly consumption of meat alternatives in the U.S. fell from 31% to 24%, while the share of Americans on a plant-based diet dropped from 6% to 3%. A September 2025 survey of 2,200 U.S. adults showed 60% reduced or avoided beef due to high prices, rising to 72% if prices increased further. Additionally, 35% considered non-meat alternatives for cost reasons, climbing to 53% among Gen Z. Research published in May 2026 in Applied Economic Perspectives and Policy, analyzing data from 136,553 U.S. households, found plant-based alternatives substituted some beef categories but complemented others. Consumers were more price-sensitive to plant-based products than beef, limiting substitution at current price gaps. This indicates plant-based alternatives impact beef most when beef prices are high, a trend likely to persist during the current cattle cycle.

Strict Sanitary/Phytosanitary and Trade Barriers

In 2025, US beef exports faced major setbacks due to trade-access disruptions. Export volumes fell 12% to 1.14 million metric tons, while export value dropped 11% to USD 9.33 billion[3]Source: U.S. Meat Export Federation, “Pork Exports Just Short of 2024 Record, Beef Feels Pinch of China Lockout, Strong Year for Lamb Exports”, usmef.org. Excluding China, the volume decline was just 3%, underscoring the significant impact of market-access issues with China. Chinese retaliatory duties on US beef peaked at 147% in April 2025, halting exports. Although duties were reduced to 22% by November 2025, export registration barriers persisted. Additionally, the USDA reinstated a live-cattle import ban from Mexico on July 9, 2025, following a New World Screwworm detection in Veracruz. This ban cut off 1.2–1.5 million feeder cattle annually, vital for the southern US feeding sector. Losing a key export market and live-cattle source squeezed profit margins for the four leading beef processors, leading to capacity closures and a DOJ antitrust investigation. The US–Korea FTA provided some relief, as US beef achieved zero-duty status in Korea for 2026. Korea remained the top-value export market, with USD 2.23 billion in 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fresh Beef Leads but Frozen Growth Reshapes Supply Mix

In 2025, Fresh Beef held a 63.32% share of the US beef market, highlighting its dominance in the retail and foodservice sectors. Beef appeared on 88% of US menus, and in 2024, 48% of consumers ate a beef burger at a restaurant within the past week. Ground beef led fresh retail volume. Retail fresh beef prices averaged USD 8.01 per pound in 2024, up from USD 7.60 in 2023, due to tight cattle supplies and high carcass values. On July 4, 2025, boxed beef prices hit a record USD 388.64 per hundredweight. Processed and Canned Beef cater to niche markets, with products like deli roast beef and corned beef hash gaining popularity in convenience stores and home meal prep. Hormel relaunched its NATURAL CHOICE Deli Roast Beef line in April 2024, and MARY KITCHEN introduced Skillet extensions in January 2026. These segments benefit from consumers seeking affordable prepared beef options.

Frozen/Chilled Beef is the fastest-growing segment, with a CAGR of 2.35% from 2026 to 2031, driven by rising imports reshaping the US beef supply. Between 2020 and 2024, the US frozen beef import value rose by 82.6%. In 2024, the US became the largest global importer of fresh and chilled beef, accounting for 18.1% of global import value. By April 25, 2026, US imports of fresh and frozen beef reached 637,648 metric tons, a 16.1% year-on-year increase. South American shipments from Brazil, Argentina, Paraguay, and Uruguay in Q1 2026 surged to 194,564 metric tons, 130% higher than two years earlier. This import surge, driven by domestic supply shortages, is expected to sustain Frozen/Chilled Beef growth through the cattle cycle recovery, likely extending to 2028-2029.

By Nature: Conventional Beef Dominates, but Specialty Commands the Growth Premium

By 2025, conventional beef dominated the US market, holding a commanding 95.34% share. This dominance underscores the vast scale of commodity cattle production, especially when juxtaposed with certified or specialty programs. As cattle prices surged and supplies tightened, the conventional segment wielded increased pricing power. This shift translated into heightened revenues for producers, even as processors grappled with margin pressures. In the foodservice arena, beef continues to reign as the highest-value protein. This is largely due to consumers' enduring preference for beef-centric menu items, bolstering the market's sustained growth.

Specialty Beef, which includes Wagyu, grass-fed, organic, and verified antibiotic-free programs, is emerging as the fastest-growing segment in the Nature category, boasting a CAGR of 3.52% from 2026 to 2031. The robust sales of grass-fed and organic beef highlight consumers' readiness to pay a premium, driven by perceived benefits in health, sustainability, and animal welfare. The Wagyu segment is also witnessing a surge, fueled by a growing appetite for luxury beef. Yet, challenges loom: tightening import quotas and tariffs on Japanese Wagyu are inadvertently benefiting American Wagyu producers. With diminished competition from imports, these domestic producers are well-positioned to tap into the premium demand. Moreover, as domestic suppliers invest in cutting-edge processing technologies and expand their capacities, the specialty beef segment is poised for further growth and value enhancement in the coming years.

By Distribution Channel: Off-Trade Anchors Volume, On-Trade Drives Value Growth

In 2025, Off-Trade channels dominated the US beef market, capturing 60.23% share. This was bolstered by the meat department achieving a record USD 105 billion in retail sales in 2024. Notably, ground beef emerged as the leading subcategory in absolute dollar growth, outpacing 85,000 other center-store and perishable categories. Meanwhile, online beef retailing is carving out a significant niche. For instance, Hormel's Black Label Oven Ready Bacon saw a remarkable 60% of its sales come from e-commerce in early 2026, setting a precedent for premium-branded beef products. Specialty Stores play a pivotal role for premium and certification-focused products. Consumers in search of grass-fed, Wagyu, and organic beef often transition from mainstream channels to these specialty grocery stores, seeking verified claims.

On-Trade is witnessing the fastest growth among distribution segments, boasting a CAGR of 3.04% from 2026 to 2031. This surge mirrors the structural recovery of the foodservice sector, which is notably leaning towards premiumisation. Restaurants command a significant 64% share of the foodservice beef market. Projections indicate a positive growth trajectory for foodservice beef sales by 2031. A key, yet often overlooked, factor driving this growth is the concentration of premium beef consumption within foodservice. Here, operators adeptly manage higher input costs through strategic menu pricing and portion control. This gives the On-Trade segment a structural advantage, insulating it from the price elasticity challenges faced by retail. The rise of upscale burger chains, steakhouse formats, and Japanese yakiniku restaurants, which are capitalizing on both US-produced and Japanese Wagyu cuts, is broadening the premium beef experience beyond just fine dining. All federally inspected beef establishments must adhere to compliance factors in the foodservice beef supply, including USDA FSIS food safety inspection standards and Hazard Analysis Critical Control Point (HACCP) requirements.

Geography Analysis

As of 2025, the United States remains the largest global beef consumer and ranks second in production. USDA data cited by CNN Brasil shows Brazil surpassed the U.S. in 2025, producing 12.35 million tonnes compared to the U.S.'s 11.8 million tonnes. Four states dominate U.S. beef production: Iowa (16.6%), Nebraska (14.4%), Kansas (10.4%), and Texas (8%), collectively contributing nearly half of the nation's red meat output. In 2025, Texas added 9 new federally inspected plants, bringing its total to 78, reflecting continued investment in the cattle-rich Southern Plains corridor. However, geographic vulnerabilities persist. In Q4 2024, drought conditions in Texas affected 62% of U.S. cattle in drought zones, the highest since December 2022. Additionally, the Southern U.S. feeding sector, reliant on 1.2–1.5 million head of Mexican feeder cattle annually, faced challenges due to the New World Screwworm's closure of the Mexico border for live cattle imports since July 2025.

Coastal markets, especially in the Northeast and West Coast, show strong premiumisation trends in beef consumption. USDA AMS data from May 2025 indicates grass-fed ribeye prices in these regions exceeded USD 40 per pound, compared to USD 35 in the Central region. Wagyu consumption is also concentrated in cities like Los Angeles, San Francisco, and New York, driven by population size, income levels, and high-end restaurants. JETRO's 2025 report identified these cities as key Wagyu hubs, with expansion efforts targeting Chicago, Philadelphia, and Houston. Demand for USDA Prime beef rose from 5.4% of the graded supply in 2015 to 9.5% in 2023, aligning with income growth in coastal metros.

The Midwest remains central to the U.S. beef value chain, serving as a production hub and a demand center for commodity beef. States like Nebraska, Kansas, and Texas see higher per capita beef consumption due to cultural ties, lower prices for local beef, and proximity to processing facilities. However, rural markets are shifting. The NCBA's 2025 Consumer Beef Tracker found 66% of consumers had no concerns about cattle raising practices, but among the 34% who did, 27% cited Animal Welfare, followed by Hormones, Antibiotics, and Vaccines at 23%. The Midwest's large-scale feedlot and processing infrastructure faces increased regulatory scrutiny under the EPA's greenhouse gas reporting rules, which require methane and nitrous oxide reporting for large livestock facilities under 40 CFR Part 98 Subpart JJ.

Competitive Landscape

The U.S. beef market is highly fragmented, comprising a mix of large integrated meat processors, regional packing companies, specialty beef producers, and numerous independent cattle ranchers. While major companies such as Tyson Foods, JBS USA, Cargill, and National Beef Packing Company dominate beef processing and distribution, thousands of cattle operations contribute to the supply base, creating a competitive and decentralized production landscape. Large processors benefit from scale, extensive procurement networks, and established relationships with retail and foodservice customers.

Competition is increasingly shifting beyond volume and price toward product differentiation and value-added offerings. Producers are expanding premium portfolios that include grass-fed, organic, Wagyu, Angus-certified, and antibiotic-free beef to capture growing consumer demand for quality, traceability, and sustainability. Companies are also investing in branded beef programs, advanced processing capabilities, and supply chain transparency to strengthen customer loyalty and secure higher margins in both retail and foodservice channels.

The market is also witnessing rising investment in operational efficiency, automation, and direct-to-consumer strategies. Leading processors are enhancing production capacity and adopting digital technologies to improve yield, consistency, and labor productivity, while specialty producers are leveraging e-commerce platforms and premium branding to reach niche consumer segments. As demand for premium and differentiated beef products continues to grow, competition is expected to intensify across both conventional and specialty categories, with innovation, supply chain control, and brand credibility emerging as key competitive factors.

U.S. Beef Industry Leaders

Tyson Foods, Inc.

Cargill Incorporated

JBS N.V.

National Beef Packing Company, LLC

Marfrig Global Foods S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: JBS USA invested USD 150 million, as a part of its expansion at its Cactus, Texas beef production facility, adding a new fabrication floor and expanded ground-beef room with completion targeted for early 2027. The Cactus facility purchases approximately USD 3.3 billion in livestock annually and employs over 3,600.

- January 2026: Hormel Foods launched two HORMEL® MARY KITCHEN® Skillet varieties, including a Southwest Style beef and pork skillet, expanding into convenience-driven, protein-rich meal solutions at select retailers nationwide. The brand extension directly targets consumers seeking semi-prepared beef formats.

- December 2025: Creekstone Farms implemented AI-powered processing technology in partnership with Marble Technologies at its Arkansas City, Kansas, facility. The Pack-Off and Box Verification systems were fully operational by September 2025, resulting in a 75% decrease in customer claims and improved on-time delivery rates.

U.S. Beef Market Report Scope

| Fresh Beef |

| Processed Beef |

| Frozen/Chilled Beef |

| Canned Beef |

| Conventional |

| Specialty Beef |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retailers | |

| Others |

| By Product Type | Fresh Beef | |

| Processed Beef | ||

| Frozen/Chilled Beef | ||

| Canned Beef | ||

| By Nature | Conventional | |

| Specialty Beef | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retailers | ||

| Others | ||

Key Questions Answered in the Report

What is the current outlook for the United States beef market?

The United States beef market was valued at USD 63.97 billion in 2025 and is projected to reach USD 72.64 billion by 2031 at a 2.1% CAGR, with growth supported by resilient demand and premium product expansion.

Which product category leads US beef sales?

Fresh beef led with 63.32% share in 2025, supported by strong menu penetration and continued household demand for burgers, steaks, and roasts.

Why is specialty beef growing faster than conventional beef in the United States?

Specialty beef is forecast to grow at a 3.52% CAGR because grass-fed and organic lines are expanding faster, and verified claims can command much higher retail pricing than commodity beef.

Which sales channel is growing fastest for beef in the United States?

On-trade is growing fastest at a 3.04% CAGR through 2031 because restaurants remain the main outlet for premium beef and can manage higher costs through menu pricing and portion control.

Page last updated on: