United Kingdom Fencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.92 Billion |

| Market Size (2026) | USD 0.96 Billion |

| Market Size (2031) | USD 1.19 Billion |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

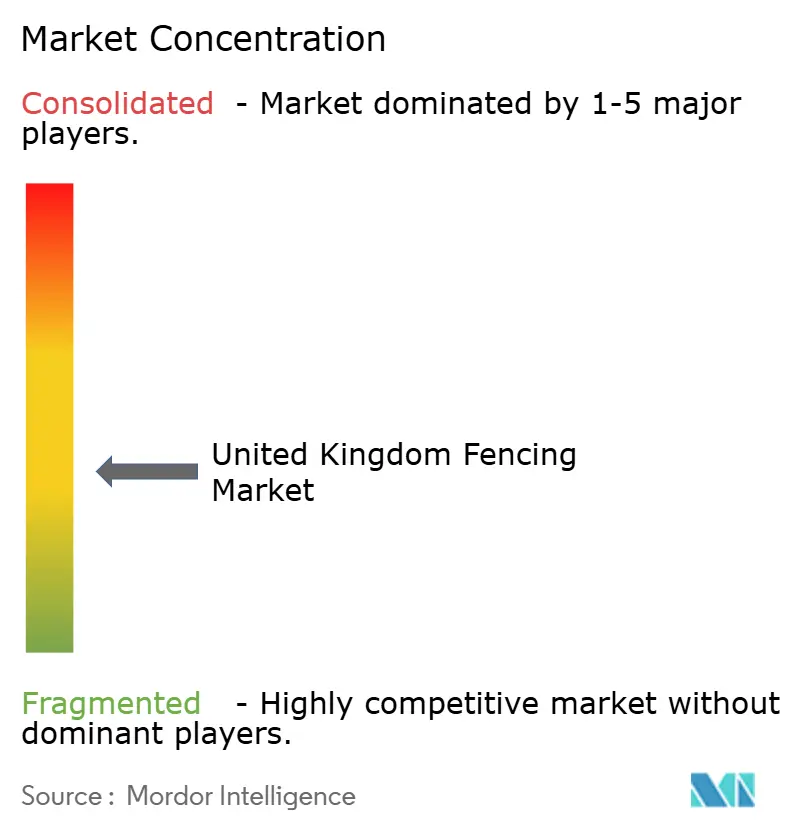

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Fencing Market Analysis by Mordor Intelligence

The United Kingdom Fencing Market size is expected to grow from USD 0.92 billion in 2025 to USD 0.96 billion in 2026 and is forecast to reach USD 1.19 billion by 2031 at 4.39% CAGR over 2026-2031.

The United Kingdom fencing market is supported by demand from housing upgrades, public infrastructure works, institutional security programs, and renewable energy projects, providing revenue streams with a broader base than many single-application construction product categories. Government funding for perimeter security, prison construction, and defense estate renewal is lifting demand for higher-specification systems, especially in projects that require tested security ratings and formal procurement compliance. The United Kingdom fencing market is also benefiting from refurbishment programs across transport and utilities, where recurring replacement cycles are less exposed to short-term swings in private construction activity. At the same time, renewable energy deployment is changing material choices and perimeter specifications, as utility-scale solar sites require durable boundary systems that meet safety, security, and site-management standards. The United Kingdom fencing market remains moderately fragmented. Still, consolidation is picking up in security-led and temporary fencing niches, which shows that scale, geographic coverage, and certified product portfolios are becoming more important in larger contracts.

Key Report Takeaways

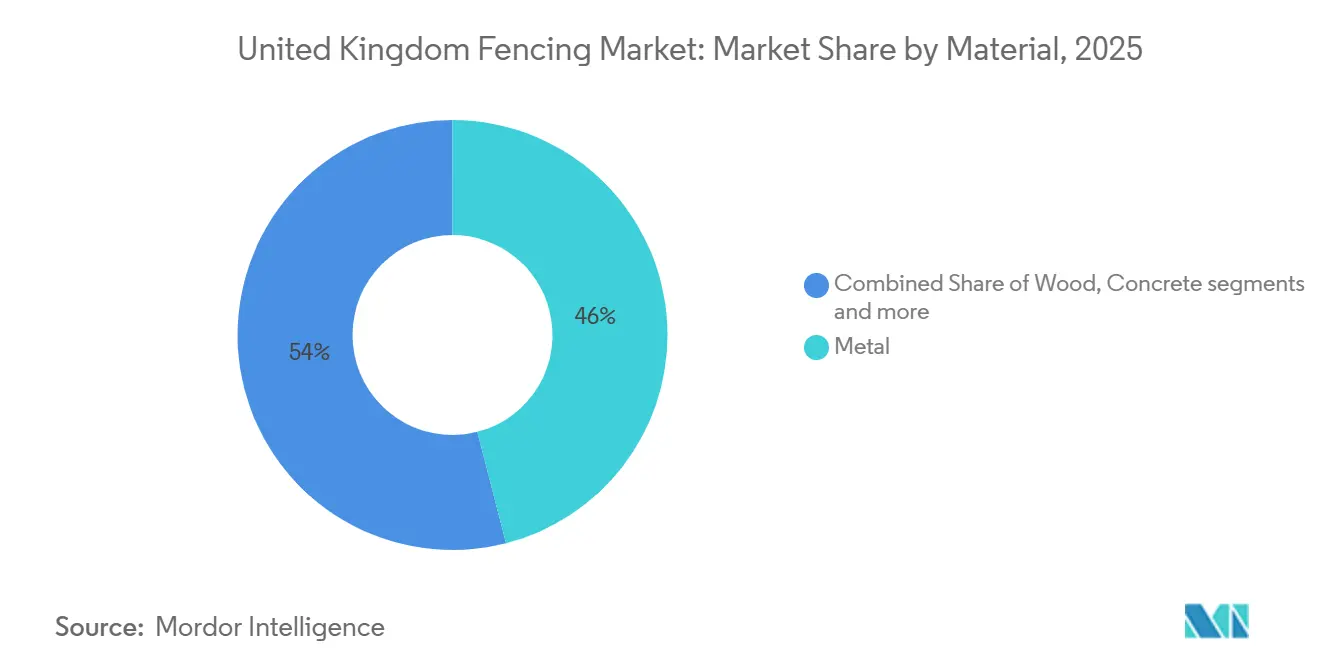

- By material, metal held 46% of revenue in 2025, while plastic & composite are forecast to expand at a 5.5% CAGR through 2031.

- By end-user, residential accounted for 38% of the United Kingdom fencing market size in 2025, while energy & power is projected to grow at a 6.2% CAGR through 2031.

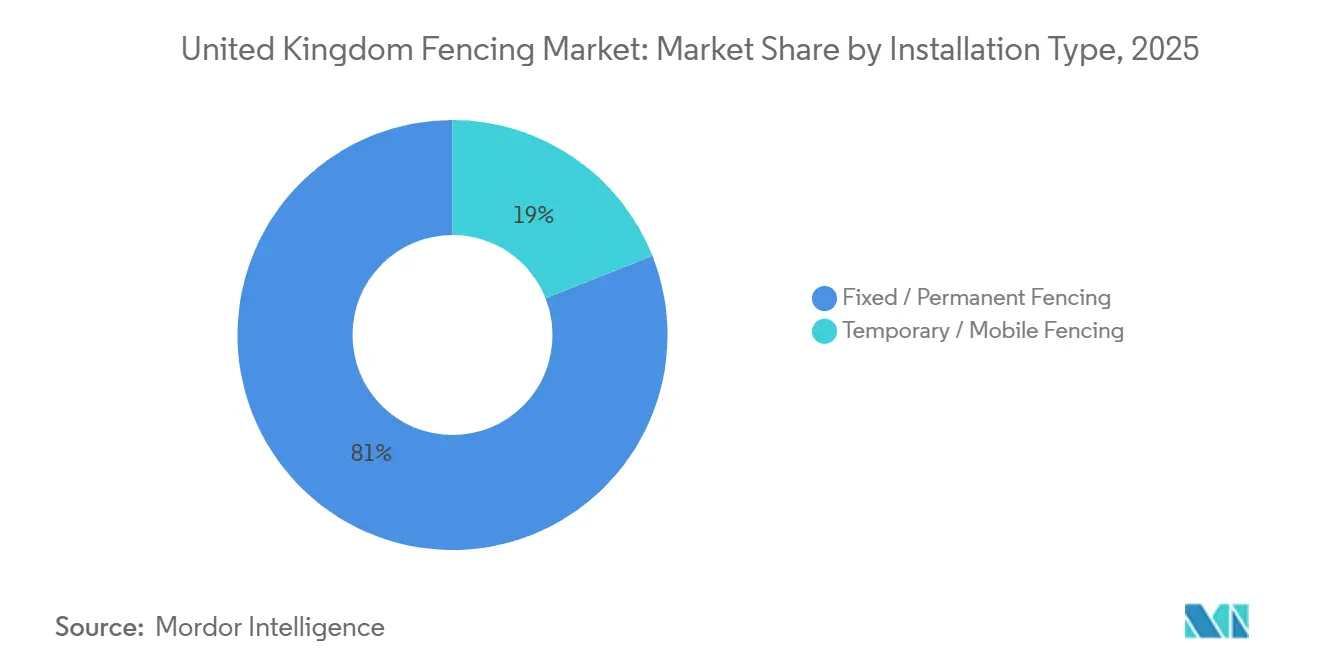

- By installation type, fixed / permanent fencing accounted for 81% of the United Kingdom fencing market share in 2025, while temporary/mobile fencing is expected to grow at a 5.9% CAGR through 2031.

- By installation channel, professional contractors held a 74% share of revenue in 2025, while DIY / modular kits are forecast to grow at a 5.4% CAGR through 2031.

- By geography, England held 64% of revenue in 2025, while Northern Ireland is projected to record the fastest regional growth at a 5.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Fencing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Funded Perimeter Security Upgrades Boost Fencing Demand at Critical Infrastructure Sites | +1.0% | National, with peak demand in England and Scotland near military, energy, and border installations | Long term (≥ 4 years) |

| Post-Pandemic Home Improvement Activity Increases Residential Fencing Installations | +0.8% | England, with strong activity in the South-East and Midlands, plus Wales and Scotland | Short term (≤ 2 years) |

| Infrastructure Refurbishment Projects Drive Replacement Demand for Aging Fencing Systems | +0.7% | England transport and utility corridors, with spillover to Scotland and Wales | Medium term (2-4 years) |

| Expansion of Solar Farms Increases Utility-Scale Fencing Installations | +0.6% | England and Scotland, including East Anglia and the Southern Uplands | Long term (≥ 4 years) |

| Demand for Eco-Friendly Composite Fencing Rises Across Residential and Commercial Sectors | +0.5% | England and Wales, with early commercial uptake nationally | Medium term (2-4 years) |

| Smart Sensor-Integrated Fencing Adoption Grows for Advanced Security Monitoring Applications | +0.4% | National, with concentration at critical infrastructure and data centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Funded Perimeter Security Upgrades Boost Fencing Demand at Critical Infrastructure Sites

The Spending Review 2025 committed at least GBP 100 million (USD 127 million) per year by 2028-2029 through the Integrated Security Fund and raised defense capital budgets from GBP 23.2 billion (USD 29.5 billion) in 2025-2026 to GBP 33.2 billion (USD 42.2 billion) by 2029-2030, while military accommodation renewal alone received GBP 7 billion (USD 8.9 billion)[1]UK HM Treasury, “Spending Review 2025,” GOV.UK, gov.uk. That spending base matters for the United Kingdom's fencing market because perimeter systems sit within defense, prison, transport, and critical infrastructure budgets rather than relying solely on stand-alone fence replacement cycles. The same review also allocated GBP 7 billion (USD 8.9 billion) for 14,000 new prison places by 2031, which supports multi-year demand for high-specification perimeter fencing and access control around custodial sites. The June 2025 National Security Strategy made protection of critical national infrastructure a formal priority, and that is pushing procurement toward rated systems rather than lower-end perimeter products. Hill & Smith stated in its 2025 full-year results that data center demand was an important driver of perimeter security revenue, which shows that digital infrastructure is becoming a major buyer of higher-value fencing systems. This is raising specification levels across the United Kingdom fencing market and shifting value toward suppliers that can meet premium security standards with tested products and approved installation capabilities.

Post-Pandemic Home Improvement Activity Increases Residential Fencing Installations

Private housing repair and maintenance activity strengthened during 2025 and continues to support demand in 2026, sustaining replacement and upgrade requirements for boundary products within the residential segment of the United Kingdom fencing market. Residential demand remains significant due to the country's large and aging housing stock, which drives recurring fence replacement needs even during periods of slower new housing construction. Demand growth is influenced not only by installation activity but also by homeowners increasingly favoring higher-quality, longer-warranty products over basic entry-level fencing solutions. This trend is reflected in supplier strategies, as manufacturers introduced extended-life timber and hybrid-composite product ranges during 2024 and 2025 to capture ongoing upgrade spending. As a result, revenue generated per project in the United Kingdom fencing market can increase even when overall installation volumes grow at a more moderate pace. The continued importance of the residential segment also underscores its role in shaping competitive positioning, despite the growing attention to institutional security and infrastructure-related fencing projects.

Infrastructure Refurbishment Projects Drive Replacement Demand for Aging Fencing Systems

The Institution of Civil Engineers said in its State of the Nation 2026 report that the United Kingdom faces a widening maintenance gap across transport and utility assets, which supports recurring replacement demand for perimeter systems around aging infrastructure. The government reinforced that direction in April 2026 when it opened the Structures Fund as part of a broader GBP 24 billion (USD 30.5 billion) roads and rail maintenance package for 2026-2027 to 2029-2030. These programs matter for the United Kingdom fencing market because fencing is tied to safety, access control, and boundary works in bridge, tunnel, motorway, and rail projects. London Underground's October 2025 tender for track fencing renewals showed that asset owners are increasingly using multi-year frameworks for survey, renewal, and replacement rather than one-off contracts. That makes refurbishment demand more stable than purely private construction demand and gives contractors a clearer backlog when housing activity weakens. It also favors suppliers that can serve long-duration maintenance programs with compliant products, installation capacity, and reliable delivery schedules.

Expansion of Solar Farms Increases Utility-Scale Fencing Installations

The United Kingdom added 2.6 GW of solar capacity in 2025, bringing installed capacity to 21.6 GW, while ground-mounted projects accounted for a larger share of new activity as developers moved further toward utility-scale sites. That matters because every utility-scale solar project needs perimeter fencing, and larger sites need systems that balance security, wildlife considerations, durability, and visual management. In the United Kingdom fencing market, this supports the faster growth of the energy & power segment, which is projected to expand at a 6.2% CAGR through 2031. Utility-scale energy projects also boost average selling prices because site fencing is usually engineered to higher standards than in basic agricultural applications. The effect is stronger in projects where developers and operators need certified, long-lasting systems that reduce maintenance over the site's operating life. As a result, the United Kingdom fencing market is seeing renewable energy demand add value as well as volume, especially for metal mesh and higher-performance perimeter designs.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Steel and Timber Prices Pressure Fencing Contractor Profit Margins | -0.5% | National, with stronger exposure for steel-dependent contractors in England and the Midlands | Short term (≤ 2 years) |

| Labor Shortages Across the United Kingdom Construction Sector Constrain Fencing Installation Capacity | -0.4% | National, with regional pressure in South-East England and urban Scotland | Medium term (2-4 years) |

| Strict Planning Permissions in Heritage and Conservation Zones Delay Fencing Projects | -0.3% | England, especially the South-East and historic city centers, plus Wales national park areas | Long term (≥ 4 years) |

| High Upfront Costs of Smart Fencing Limit Adoption Among SMEs | -0.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel and Timber Prices Pressure Fencing Contractor Profit Margins

Input-cost volatility remains a key restraint for the United Kingdom fencing market in 2026, as many projects are awarded under fixed-price contracts while material costs can fluctuate throughout the delivery period. During 2025, Timber Development UK (TDUK) reported significant timber price movements, with its timber price index rising from 107 at the beginning of 2025 to 130 by mid-2025, before easing to 125 in the third quarter of 2025 and recording a further 5% correction during the fourth quarter of 2025 as supply conditions improved. Although timber prices moderated toward the end of 2025, the volatility experienced throughout the year continues to influence purchasing and bidding decisions in 2026. This challenge is particularly relevant in the United Kingdom fencing market, where smaller contractors may be reluctant to participate in public tenders when future material costs are uncertain, reducing bidding depth and potentially delaying contract awards. Cost fluctuations also favor integrated manufacturers that can manage supply chains, maintain inventory, or diversify exposure across timber, steel, and composite fencing products. Over time, this dynamic may support market-share gains for larger operators, even as overall demand conditions remain healthy in 2026.

Labor Shortages Across the United Kingdom Construction Sector Constrain Fencing Installation Capacity

The Construction Industry Training Board (CITB) stated in June 2025 that the country would need around 239,000 additional construction workers over the forecast period, confirming that labor capacity remains tight across the installation base. The Federation of Master Builders and the Chartered Institute of Building (CIOB) reported in the second half of 2025 that 72% of construction small and medium-sized enterprises (SMEs) were affected by skilled trades shortages, with 49% seeing delayed job starts and 30% pausing expansion plans. For the United Kingdom fencing market, that does more than slow project delivery, because it also changes which products are easier to specify and install in a tight labor environment. Panel-based systems, modular kits, and pre-formed assemblies become more attractive when they reduce time on site and dependence on scarce skilled workers. Traditional timber formats that require more labor-intensive installation face a relative disadvantage under those conditions. This is why labor scarcity is shaping channel growth, product design, and procurement choices across the United Kingdom fencing market, rather than operating only as a short-term delivery issue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Metal Leads the Market While Plastic & Composite Records the Fastest Growth

Metal accounted for 46% of revenue in 2025, making it the largest material category in the United Kingdom fencing market. That leadership rested on its strong position in security, perimeter protection, transport, utilities, and other applications where rated mesh, steel palisade, and durable boundary systems are standard requirements. Steel held the larger share of the metal market, while aluminum gained ground in residential and commercial settings because it combines corrosion resistance with lower lifetime maintenance costs. Metal also retained a clear edge in projects where tested security performance and structural durability mattered more than visual style. In that sense, metal continued to anchor the core of the United Kingdom fencing market, even as other materials gained in appeal.

Plastics & composites are forecast to grow at a 5.5% CAGR through 2031, making it the fastest-growing material group. The segment is benefiting from stronger sustainability requirements and from demand for products that reduce ongoing maintenance in residential and commercial projects. Supplier documentation in 2025 showed recycled-content composite systems with 15- to 25-year warranties, sharpening the cost comparison with treated timber over the product life[2]EnviroBuild, “Composite Fencing Product Documentation,” EnviroBuild, envirobuild.com. Wood still holds an important place in residential and agricultural fencing, but it is under pressure from higher maintenance requirements and customer interest in longer-lasting alternatives. Concrete also plays a role in boundary walls and noise-barrier applications, especially near road and rail corridors undergoing refurbishment. The Forest Research Timber in Construction Roadmap still points to policy and procurement support for wood in broader building applications, which could help wood fencing volumes where local specifications remain favorable. Even so, the United Kingdom fencing market is seeing a material growth shift toward products that offer lower upkeep and stronger sustainability positioning.

By End-User: Residential Leads Demand While Energy & Power Records the Fastest Growth

Residential accounted for 38% of revenue in 2025, making it the largest end-user segment in the United Kingdom fencing market. That scale reflects the country's broad housing base and the continued need for fence replacement, repair, and garden upgrades across existing homes. Demand is spread across all 4 nations, so the segment is not tied to one capital spending cluster or a single institutional budget cycle. Agricultural demand remained another major driver of the United Kingdom fencing market, as rural land management and livestock containment continue to require regular boundary maintenance. Military, defense, and government demand also accelerated as public spending programs lifted perimeter upgrades at prisons, military sites, and other institutional locations.

Energy & power is projected to grow at a 6.2% CAGR through 2031, which makes it the fastest-growing end-user segment in the United Kingdom fencing market. The main driver is renewable energy, especially utility-scale solar, rather than new conventional power build-out. The Cleve Hill Solar Farm demonstrates that a single large-scale project can require several kilometers of perimeter fencing and a higher specification than is typical for agricultural applications. Mining, petroleum, and chemicals demand remains steadier because it depends more on existing asset maintenance than on a wave of new sites. Even when volume growth is modest, hazardous and high-security environments still support value because operators need rated perimeter solutions with integrated access control. This means the United Kingdom fencing industry is seeing some of its strongest value expansion where technical compliance matters more than simple volume. It also means the United Kingdom fencing industry is being pulled toward applications where installers need both product knowledge and tighter project execution standards.

By Installation Type: Fixed / Permanent Fencing Leads the Market While Temporary / Mobile Fencing Expands Faster

Fixed / permanent fencing represented 81% of revenue in 2025, which shows how much of the United Kingdom fencing market is still linked to long-life perimeter needs. Infrastructure, energy, residential, and public-sector projects all rely on installations that are expected to remain in place for many years, so procurement often happens through frameworks and planned supply agreements. That structure gives permanent systems a stable base and favors suppliers with durable product lines and dependable installation capacity. It also means revenue is concentrated in applications where warranty, compliance, and total life cost matter as much as initial price. Within the United Kingdom fencing market, permanent fencing still defines the largest pool of value.

Temporary / mobile fencing is forecast to grow at a 5.9% CAGR through 2031, well above the overall growth rate. This reflects demand from major construction compounds, phased infrastructure works, and event-related perimeter needs that require fast deployment and redeployment. CLD Fencing Systems' work on the HS2 East M42 to M6 Link Viaduct site showed that even temporary systems on major projects are now being specified at stronger anti-climb and security-led standards. The higher capital cost of better temporary systems is increasingly offset by redeployment benefits and by the ability to avoid some of the constraints that apply to permanent installations. Altrad Generation's February 2025 acquisition of Heras Mobile Fencing also showed that broad branch coverage and fast mobilization have become major competitive tools in this part of the market. As a result, the United Kingdom fencing market is seeing temporary fencing grow not only on construction volume but also on better product quality and stronger service expectations.

By Installation Channel: Professional Contractors Lead, DIY / Modular Kits Accelerates on Labor Scarcity

Professional contractors accounted for 74% of revenue in 2025, making them the leading force in the United Kingdom fencing market. That position is reinforced by specification complexity in commercial, public-sector, security, and energy projects where certification, warranty control, and procurement approvals are required. Contractors also dominate because larger clients need accredited partners for installation, compliance records, and post-installation support. In high-security work, approved products alone are not enough, because buyers also want installers who can handle restricted-site requirements and formal project documentation. These conditions keep the professional channel firmly in control of the largest and most demanding parts of the United Kingdom fencing market.

DIY / modular kits are forecast to grow at a 5.4% CAGR through 2031, making them the fastest-growing channel. Labor shortages are part of the reason, as easier-to-install systems help households, farms, landscape contractors, and small developers complete projects with less skilled labor. Product changes such as pre-formed clip systems, modular panels, downloadable guides, and easier assembly are supporting that shift, and manufacturers are clearly designing with installation simplicity in mind. The change is not just a consumer story; professionals also specify modular systems when labor is tight, and project timing is critical. Fabricators still play a useful middle role by supplying custom metalwork to contractors that do not make products in-house. That mix is why the United Kingdom fencing market is broadening by channel without removing the need for professional installation in more technical jobs.

Geography Analysis

England accounted for 64% of revenue in 2025, giving it the largest share of the United Kingdom fencing market. Its lead comes from the scale of housing activity, commercial development, transport corridors, utilities, and higher-value institutional contracts concentrated in the South-East and Midlands. The October 2025 London Underground framework for track fencing renewals showed how recurring public infrastructure procurement supports England's large installed base and replacement cycle[3]Transport for London, “Track Works and Resources Lot 3c Track Fencing Renewals,” Contracts Finder, find-tender.service.gov.uk. The June 2026 10-Year Infrastructure Strategy also reinforced this position by prioritizing maintenance and optimization and committing more than GBP 24 billion (USD 30.5 billion) for roads and rail capital between 2026-2027 and 2029-2030. In practical terms, England combines the broadest volume base with the highest concentration of projects that demand stronger specifications and higher per-site values.

Agricultural activity, renewable energy development, and increasing demand for high-security perimeter solutions support Scotland's fencing market. Its demand profile differs from England's, with rural applications and renewable energy projects accounting for a larger share of overall activity. Wales benefits from investment in the South Wales corridor and expanding renewable energy project pipelines that support utility-scale perimeter installations. Together, these regions contribute to the diversification of the United Kingdom fencing market by supporting demand across agricultural, energy, infrastructure, and security-related applications, while also creating opportunities for both standard and higher-specification fencing systems.

Northern Ireland is forecast to grow at a 5.1% CAGR through 2031, making it the fastest-growing regional segment in the United Kingdom fencing market. The Spending Review 2025 included GBP 137 million (USD 174 million) over 3 years for security-related programs in Northern Ireland, and part of that allocation supports institutional perimeter procurement. The region also benefits from cross-border infrastructure development, catch-up housing activity, and a large agricultural base that keeps field boundary investment relevant. Because they are smaller in absolute value, these overlapping demand sources lift growth faster than in larger regions. This is why Northern Ireland stands out in the United Kingdom fencing market, even though England remains far ahead in total revenue.

Competitive Landscape

The United Kingdom fencing market is moderately fragmented, with a clear two-tier structure. One tier includes larger multi-product manufacturers and pan-European platforms that compete in high-security, infrastructure, and energy-related work. The second tier includes regional specialists, agricultural suppliers, timber-focused businesses, and local contractors, all of which remain important in residential, horticultural, and farming applications. This balance keeps the United Kingdom fencing market open to regional players, but it also gives larger suppliers an advantage where certification, procurement scale, and product breadth are required. The result is a competitive setting where no single player controls the entire market, yet concentration is increasing in parts of the market with the highest technical barriers.

Several strategic moves in 2025 and 2026 show how quickly that higher-specification tier is consolidating. Garda Group completed its acquisition of Heras in April 2025, strengthening its perimeter security position across Europe and reinforcing Heras United Kingdom's position in permanent fencing and security systems. Altrad Generation acquired Heras Mobile Fencing in February 2025 and expanded its branch network to 38 locations in the United Kingdom, thereby improving its reach in temporary fencing and hoarding. Hill & Smith also expanded through 2026 deals tied to data center and engineered steel enclosure capabilities, which reflects the link between perimeter security and digital infrastructure construction. BRCK Group's June 2026 acquisition of Jacksons Fencing added premium timber, steel, acoustic barrier, and access control capabilities across several demand segments.

Technology and accreditation are also becoming sharper points of competition in the United Kingdom fencing market. Suppliers with approved and certified systems can charge higher prices and compete for projects closed to non-accredited rivals. Betafence's TriMax anti-personnel fence and Senstar's NPSA-certified perimeter intrusion systems show how product development is increasingly tied to market access rather than a simple product refresh cycle. White space still exists in renewable-specific perimeter solutions, integrated smart fencing, and circular-economy composite products. Still, these spaces are most likely to be captured by companies that can combine compliance, design capability, and national delivery coverage. That means the United Kingdom fencing market is still fragmented in broad terms, but its more profitable niches are becoming harder for undifferentiated suppliers to enter.

United Kingdom Fencing Industry Leaders

Bekaert

Betafence

Jacksons Fencing

CLD Fencing Systems

Hill & Smith Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: BRCK Group acquired H.S. Jackson & Son (Jacksons Fencing) for an initial GBP 15.0 million (USD 19.1 million), plus GBP 4.9 million (USD 6.2 million) for freehold land and property, with deferred consideration of up to GBP 11 million (USD 14.0 million) based on future performance. The transaction adds premium timber and steel fencing, acoustic barriers, perimeter security, and access control to BRCK's construction products portfolio, providing direct coverage across residential, commercial, public sector, and high-security segments. Jacksons generated GBP 40.9 million (USD 52.1 million) in revenue for the year ended September 2025.

- May 2026: Jacksons Fencing's Venetian Hit and Miss panels were specified at the RHS Chelsea Flower Show 2026, alongside Charlie Ovens' luxury outdoor cooking brand, positioning the manufacturer within the premium design-led residential and commercial fencing segment.

- March 2026: Hill & Smith PLC acquired 80% of Freeberg Industrial Fabrication (USA) for USD 36 million, with up to USD 50 million additional consideration for the remaining 20% based on future profitability. Freeberg designs custom steel enclosures for data centers, power generation, and infrastructure markets in North America, extending Hill & Smith's high-security perimeter capability into digital infrastructure. The deal is expected to be earnings-enhancing in 2026 and reflects the growing convergence of physical security fencing and data center infrastructure construction.

- August 2025: Hill & Smith initiated a GBP 100 million (USD 127 million) share buyback program, reflecting strong cash generation from its perimeter security and infrastructure products businesses, particularly the data center and high-security fencing pipelines.

United Kingdom Fencing Market Report Scope

The United Kingdom Fencing Market is Segmented by Material (Metal, Wood, Plastic & Composite, Concrete, and Other Materials), End-User (Residential, Agricultural, and More), Installation Type (Fixed / Permanent Fencing, Temporary / Mobile Fencing), Installation Channel (Professional Contractor and Others), and Geography (England, Scotland, Wales, and Northern Ireland). The Market Forecasts are Provided in Terms of Value (USD).

| Metal | Steel |

| Aluminium | |

| Wood | |

| Plastic & Composite | |

| Concrete | |

| Other Materials |

| Residential |

| Agricultural |

| Military & Defense |

| Government |

| Mining |

| Petroleum & Chemicals |

| Energy & Power |

| Other End-Users |

| Fixed / Permanent Fencing |

| Temporary / Mobile Fencing |

| Professional Contractor |

| Others – Fabricators, DIY / Modular Kits |

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Material | Metal | Steel |

| Aluminium | ||

| Wood | ||

| Plastic & Composite | ||

| Concrete | ||

| Other Materials | ||

| By End-User | Residential | |

| Agricultural | ||

| Military & Defense | ||

| Government | ||

| Mining | ||

| Petroleum & Chemicals | ||

| Energy & Power | ||

| Other End-Users | ||

| By Installation Type | Fixed / Permanent Fencing | |

| Temporary / Mobile Fencing | ||

| By Installation Channel | Professional Contractor | |

| Others – Fabricators, DIY / Modular Kits | ||

| By Geography | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland |

Key Questions Answered in the Report

What is the 2031 outlook for fencing demand in the United Kingdom?

The United Kingdom fencing market is projected to reach USD 1.19 billion by 2031 from USD 0.96 billion in 2026, growing at a 4.39% CAGR over 2026-2031.

Which region is growing fastest across the country?

Northern Ireland is expected to record the fastest regional growth at a 5.1% CAGR through 2031, supported by security spending, housing catch-up, and agricultural demand.

Which material category leads revenue today?

Metal remained the largest material segment with 46% share in 2025 because it is widely used in security, infrastructure, and industrial perimeter applications.

Why is the energy & power segment expanding faster than other end users?

Utility-scale solar development is lifting demand for higher-specification perimeter systems, which is why energy and power is projected to grow at a 6.2% CAGR through 2031.

Page last updated on: