Brazil Fencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

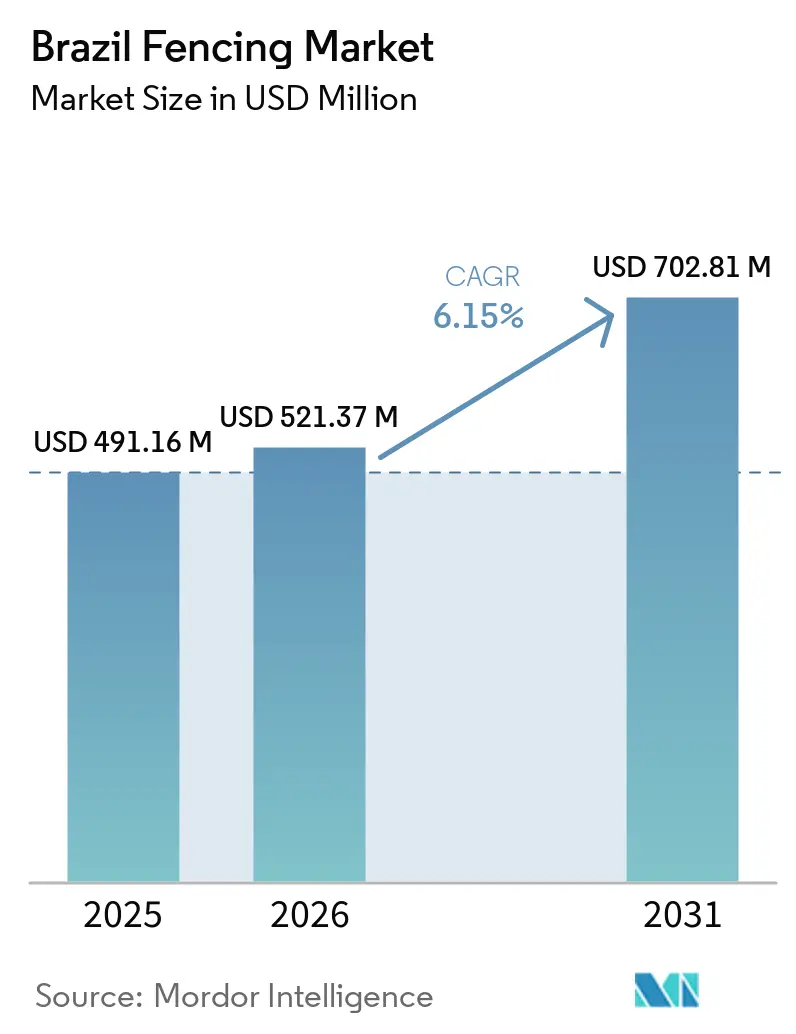

| Base Year Market Size (2025) | USD 491.16 Million |

| Market Size (2026) | USD 521.37 Million |

| Market Size (2031) | USD 702.81 Million |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

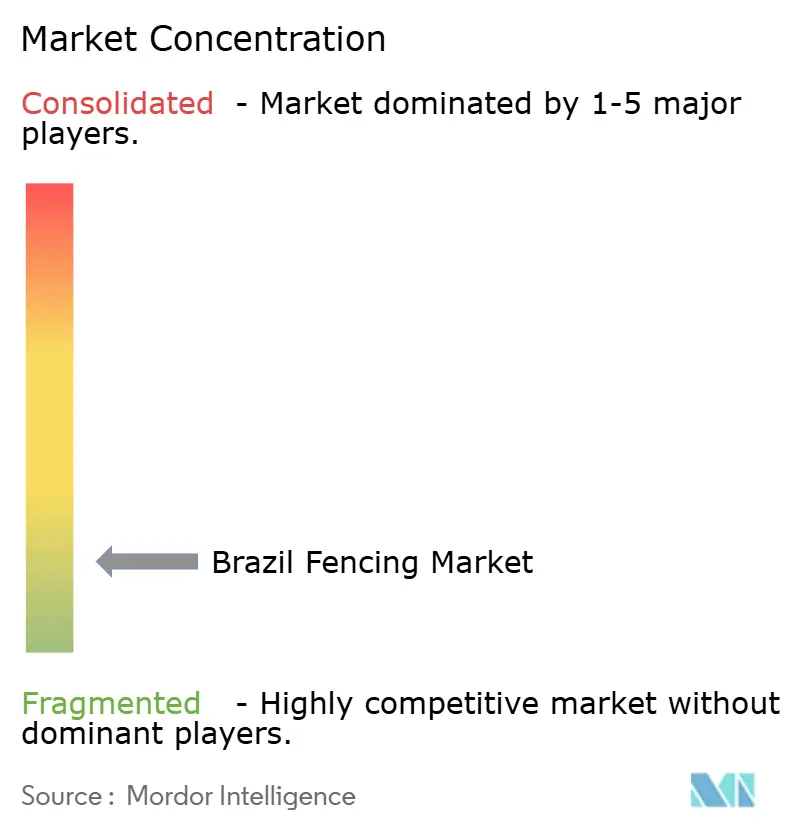

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Fencing Market Analysis by Mordor Intelligence

The Brazil Fencing Market size was valued at USD 491.16 million in 2025 and is estimated to grow from USD 521.37 million in 2026 to reach USD 702.81 million by 2031, at a CAGR of 6.15% during the forecast period (2026-2031).

Market growth is being supported by expanding agricultural activity, infrastructure development, and residential construction, creating demand across multiple end-use sectors. The growing adoption of livestock confinement systems is driving demand for structured land management and perimeter fencing solutions in the agricultural sector. At the same time, ongoing government investments in transport, energy, and housing projects are supporting demand for temporary and permanent fencing installations. Residential development, particularly gated communities and condominium projects, is further contributing to market expansion as security and privacy remain key priorities. However, fluctuations in raw material prices, particularly steel and PVC, along with competition from informal manufacturers, continue to pressure profitability across the market.

Key Report Takeaways

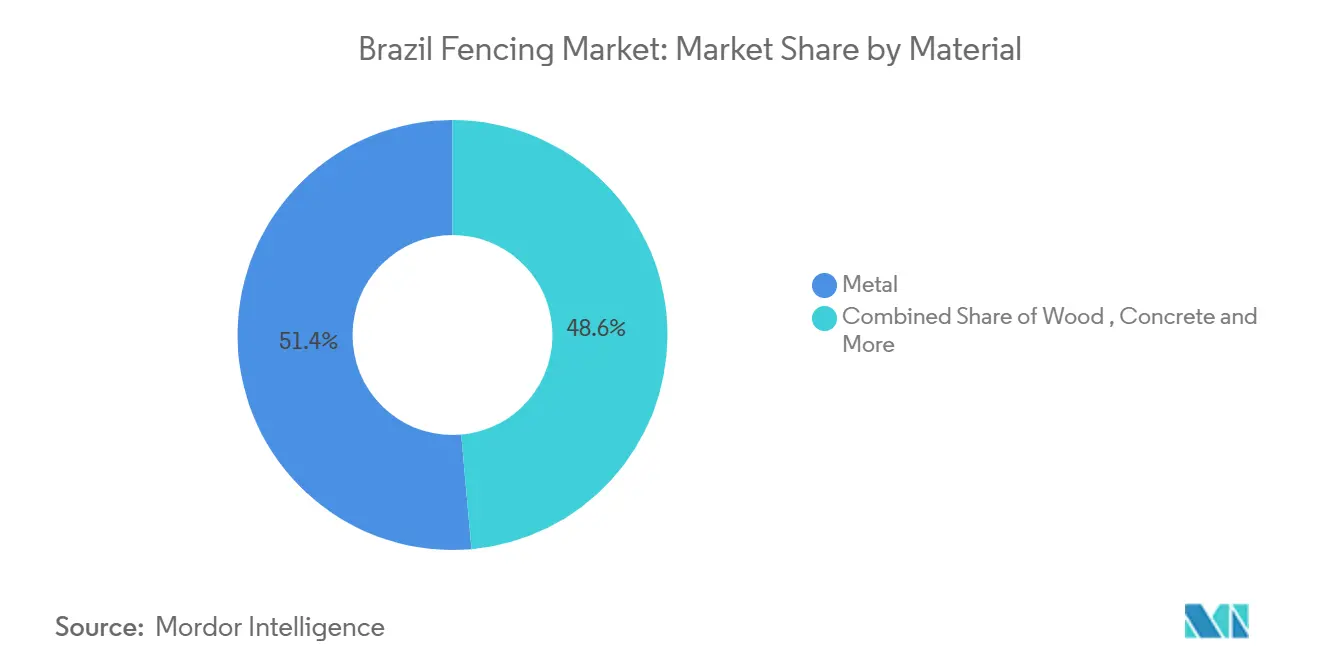

- By material, metal fencing held 51.4% of the Brazil fencing market share in 2025, while plastic and composite fencing are forecast to grow at 7.10% CAGR through 2031.

- By end-user, residential applications accounted for 30.6% of total demand in 2025, while Energy and Power is forecast to expand at 6.89% CAGR through 2031.

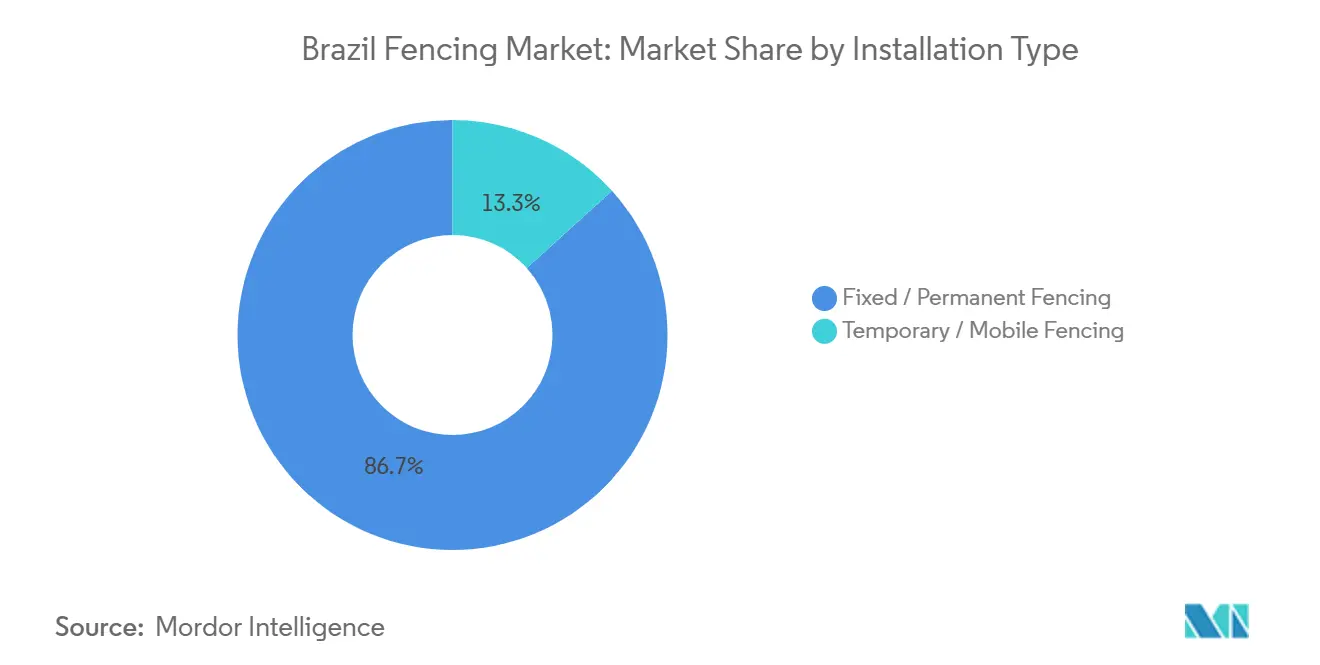

- By installation type, fixed and permanent fencing accounted for 86.7% of total demand in 2025, and this category is projected to grow at a 6.44% CAGR through 2031.

- By installation channel, professional contractors captured 72.3% of demand in 2025, while fabricators, do-it-yourself kits, and modular systems are forecast to grow at 6.37% CAGR from 2026 to 2031.

- By city grouping, the Rest of Brazil accounted for 41.7% of total demand in 2025 and is forecast to grow at a 6.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Fencing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Agricultural And Livestock Farming Activities | +1.4% | Mato Grosso, Goiás, Mato Grosso do Sul, São Paulo (Agribusiness Belt) | Long term (≥ 4 years) |

| Expansion Of Logistics Hubs, Warehouses, And Industrial Parks | +1.2% | São Paulo Metro, Espírito Santo, Rio de Janeiro | Medium term (2-4 years) |

| Growing Residential Gated Communities | +1.0% | São Paulo, Rio de Janeiro, Salvador, and major secondary cities | Medium term (2-4 years) |

| Infrastructure Development Across Highways, Railways, And Public Facilities | +0.9% | National, with early gains in São Paulo, Minas Gerais, Bahia, and Paraná concession corridors | Medium term (2-4 years) |

| Wildlife Protection And Road Safety Initiatives | +0.6% | São Paulo, Minas Gerais, BR-116 corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Agricultural and Livestock Farming Activities

Agricultural intensification is one of the strongest supports for the Brazil fencing market. Brazil’s grain output reached 350.2 million metric tonnes in the 2024 to 2025 harvest season, while beef production totaled 12.3 million metric tonnes in 2025, which kept commercial farm investment active across the main producing states[1]dsm-firmenich, “Confinement Census 2025,” dsm-firmenich, dsm-firmenich.com. The cattle confinement sector expanded to 9.25 million heads in 2025, up 16%, spread across 2,445 properties and 1,095 municipalities, indicating demand came from a broad operating base rather than a narrow cluster. As farms move from open-range systems to more intensive layouts, they need more permanent boundaries, paddock divisions, and machine-protection barriers around working areas. This driver matters because it provides the Brazil fencing market with a durable rural demand stream linked to changes in farm operations, rather than just short seasonal purchases.

Expansion of Logistics Hubs, Warehouses, and Industrial Parks

The logistics and industrial base are adding a more urban layer of demand to the Brazil fencing market. New warehouse complexes, industrial parks, and distribution sites require perimeter security, access control boundaries, and internal yard separation, which extends the installed fencing beyond the building line. This demand tends to favor better-specified products because operators want site security, controlled movement, and longer service life in high-use assets. The effect is especially visible around major business corridors and metro-linked industrial areas where land development remains active. This trend strengthens the Brazil fencing market by supporting higher-value perimeter systems and reducing dependence on purely commodity rural wire demand.

Growing Residential Gated Communities Supporting Demand for Privacy and Security Fencing

Residential activity remains a major driver of volume in the Brazil fencing market. Brazil recorded 453,005 housing launches in 2025, up 10.6%, while the Minha Casa, Minha Vida program supported 224,842 launched units, up 13.5%, which sustained enclosure demand across condominium and mass housing formats[2]Câmara Brasileira da Indústria da Construção, “Residential Launches in 2025,” CBIC, cbic.org.br . The launch value reached USD 54.2 billion in 2025, which shows that developers continued to commit capital despite a tighter financing backdrop. Boundary fencing in these projects is no longer limited to basic separation, as many developments use it as a first line of security, along with cameras and gated access. This shift supports the Brazil fencing market by increasing the value of installed systems and sustaining replacement demand in older residential areas.

Infrastructure Development across Highways, Railways, and Public Facilities

Infrastructure construction continues to create direct, long-line demand for the Brazil fencing market. Brazil’s federal transport concession portfolio for 2025 is projected at USD 29.8 billion across 8,449 km of highways, while the broader transport envelope under the New Growth Acceleration Program stands at USD 51.9 billion, including USD 34.4 billion for roads and USD 17.4 billion for rail[3]Casa Civil, “Transport Concessions and PAC Investment Portfolio,” Governo Federal, gov.br. By December 2025, cumulative execution across all sectors had reached USD 175.2 billion, equal to 70.8% of the USD 241.1 billion committed for 2023 to 2026, which confirms that the project pipeline was moving into delivery. Every new or upgraded corridor creates demand for side barriers, cattle guards, wildlife fencing, and secured perimeters around related assets and service areas. This provides the Brazil fencing market with a stable stream of public and concession-backed demand that is less exposed to short-term consumer sentiment.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Steel, Polyvinyl Chloride, And Wood Prices | -1.2% | National (most acute in Southeast steel-consuming regions) | Short term (≤ 2 years) |

| High Installation And Maintenance Costs | -0.9% | Rural Northeast, North, and peri-urban low-income areas | Long term (≥ 4 years) |

| Competition From Unorganized Local Manufacturers | -0.7% | National, with intensity in Interior São Paulo, Paraná, and Minas Gerais | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Steel, Polyvinyl Chloride, and Wood Prices

Input cost instability remains one of the clearest restraints on the Brazil fencing market. Wire rod prices, which directly affect fencing production, rose 12% to 17% between May 2024 and January 2025, narrowing fabricator margins and making forward pricing more difficult. The effect is strongest in metal products because metal still accounts for the bulk of total market demand, and many contracts are quoted before material costs are fully locked in. Polyvinyl chloride adds a second cost variable to coated wire and plastic-heavy systems, creating more uncertainty for producers working across multiple material families. This restraint matters because the Brazil fencing market can keep growing in volume while still facing uneven profitability at the manufacturer and fabricator level.

High Installation and Maintenance Costs Limiting Adoption in Price-Sensitive Areas

Installation costs remain a practical barrier in several parts of the Brazil fencing market. The construction sector employment base grew only 0.5% in 2025, which was not enough to fully absorb backlogs in inland regions where skilled work, such as welding, post-setting, and structural alignment, is harder to source. Large rural perimeters also raise mobilization costs because crews, equipment, and materials often have to travel long distances before installation even begins. Maintenance creates another issue because harsh exposure in humid, high-ultraviolet environments can shorten coating life and accelerate repair cycles. This slows the Brazil fencing market in price-sensitive areas because some buyers phase installation or defer replacement even when fencing needs are clear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Metal's Dominance Faces Composite Disruption

Metal fencing accounted for 51.4% of the Brazil fencing market in 2025, making it the largest material category by a clear margin. Galvanized steel wire, welded mesh panels, and chain-link structures remain the main products because they can serve agricultural, industrial, infrastructure, and standard residential applications without major changes in installation practice. This broad use keeps metal at the center of the Brazil fencing market, especially where buyers prioritize scale, familiar handling, and wide contractor availability. It also benefits from Brazil’s established wire-rod and fabricated wire base, which supports supply continuity across a wide range of end users.

Metal’s lead does not remove the pressure building from alternative materials. Wire rod price increases of 12% to 17% between May 2024 and January 2025 narrowed fabricators' margins and made buyers more attentive to lifecycle costs rather than only first cost. Plastic and composite fencing is forecast to grow at a 7.10% CAGR through 2031, making it the fastest-growing material category as coastal and high-humidity installations seek lower corrosion risk. Aluminum is also gaining traction in residential and commercial uses because it offers corrosion resistance and a cleaner visual finish, even though it remains more expensive than galvanized steel for budget-driven projects. The Brazil fencing industry is therefore still metal-led, but the value mix is slowly shifting toward materials that require less maintenance and perform better in exposed environments.

By End-User: Residential Scale Meets Energy Sector Dynamism

Residential applications accounted for 30.6% of total demand in 2025, making them the largest end-user group in the Brazil fencing market. The segment drew support from 453,005 housing launches in 2025 and from the continued role of the Minha Casa, Minha Vida program in supporting apartment, condominium, and planned-community development. Residential demand spans simple boundary systems for mass housing and more decorative or anti-climb products for mid-market and premium gated communities. This breadth provides the market with steady order flow, spread across many sites rather than concentrated in a few very large projects.

Energy and Power is the fastest-growing end-user segment, with 6.89% CAGR projected through 2031. Cumulative solar investment in Brazil surpassed USD 53.4 billion in 2026, while installed solar capacity reached 68.6 gigawatts, which increased demand for secure perimeter fencing around remote generation sites. Utility-scale solar and wind assets require long runs of galvanized boundary systems because theft of copper cable and panels can disrupt operations and increase project losses. Agricultural demand remains another major pillar of the Brazil fencing market, supported by the continued expansion of confinement and more intensive farm layouts. The Brazil fencing market, tied to energy and agricultural users, is therefore becoming increasingly important as the country expands both renewable generation and high-output livestock operations.

By Installation Type: Permanence as the Market Baseline

Fixed and permanent fencing accounted for 86.7% of the Brazil fencing market share in 2025, indicating that demand is closely tied to long-life assets rather than temporary site control. Farms, energy parks, highways, railways, and residential compounds all require boundaries that can remain in service for many years with limited intervention. This makes permanent systems the baseline product across the Brazil fencing market and raises the importance of coating quality, post strength, and installation standards. It also explains why buyers often evaluate durability and maintenance exposure more closely than headline unit price when the fenced asset has a long operating life.

The same category is also forecast to expand at a 6.44% CAGR through 2031, keeping it both the largest and fastest-growing installation type. The public transport and rail pipeline supports this pattern because new and upgraded corridors require durable perimeter solutions that meet concession and engineering specifications. Permanent systems also better fit large residential and energy projects because they reduce the need for repeat labor mobilization later. Temporary and mobile fencing still serves construction sites, event perimeters, and some mining applications where site layouts change over time. Even so, the Brazil fencing market remains structurally permanent because most of its end uses depend on stable boundary control rather than short-duration enclosure.

By Installation Channel: Contractors Lead but Modular Systems Accelerate

Professional contractors accounted for 72.3% of the installation channel value in 2025, making them the leading route to market in the Brazil fencing market. Their position is strongest in technically demanding work such as industrial perimeter systems, highway projects, energy park enclosures, and higher-spec residential installations. These jobs often require engineering input, site supervision, and compliance documentation, which gives professional teams an advantage over informal labor. It also keeps contractors central to public and concession-backed work where certification and inspection matter throughout project delivery.

Fabricators, do-it-yourself systems, and modular kits are forecast to grow at a 6.37% CAGR from 2026 to 2031, making them the fastest-growing installation channel. This shift reflects cost pressure among small and mid-sized buyers who want to reduce labor dependence and shorten installation time. Pre-engineered post-and-panel systems are helping rural and peri-urban customers build workable enclosures without relying on full contractor teams in locations where skilled labor is scarce. Local fabricators also remain relevant in secondary urban markets because they can deliver custom gates and panels quickly from purchased wire inputs. The Brazil fencing market is therefore keeping its contractor-led structure while opening more room for lower-labor and modular channel formats.

Geography Analysis

The rest of Brazil accounted for 41.7% of total demand in 2025 and is projected to expand at a 6.94% CAGR through 2031, confirming that the interior remains the main volume engine of the Brazil fencing market. The strongest support comes from agribusiness-heavy states where land-use intensification, confinement, and commodity farming require more permanent boundaries and internal divisions. Brazil’s confined cattle base reached 9.25 million heads across 1,095 municipalities in 2025, and this wide footprint gives the market a broad rural demand base rather than a narrow local one. Renewable energy projects in interior and semi-arid regions add a second layer of growth because utility-scale assets need long, secure perimeters to protect equipment and manage access. This combination keeps the Brazil fencing market closely tied to the country’s expanding interior economy.

São Paulo remains the most specification-intensive geography in the Brazil fencing market, even though the Rest of Brazil leads by volume. The state combines residential demand, industrial activity, public infrastructure projects, and wildlife-fencing programs into a single market, creating a broader range of product requirements than most other regions. Residential development remained active in 2025, which supported demand for condominium boundary systems and ornamental enclosure products. São Paulo also stands out because concession packages now require wildlife protection fences that guide animals toward crossing corridors rather than simply blocking movement.

Rio de Janeiro contributes industrial and urban perimeter demand through logistics-linked and site-security applications. At the same time, its dense built form often pushes buyers toward anti-climb formats and tighter boundary control. Salvador and the wider Bahia corridor add demand from housing, petrochemicals, and energy infrastructure, broadening the Brazil fencing market's urban base beyond the Southeast. Coastal exposure in El Salvador also increases the appeal of polyvinyl chloride-coated wire, aluminum, and composite materials because corrosion risk is higher than in many inland cities. This supports material change in some local projects even while metal remains the national leader. The Brazil fencing market size in metropolitan areas is therefore shaped more by specification depth, while the interior remains the larger source of installed volume.

Competitive Landscape

The Brazil fencing market is fragmented, and Belgo Arames remains the clearest formal-sector leader due to its scale, broad portfolio, and brand reach. The company operates 8 industrial plants across Bahia, Minas Gerais, and São Paulo, and sells products across agricultural wire, urban fencing, industrial safety grids, and wildlife boundary systems. This range gives Belgo Arames a stronger formal-market position than most regional competitors, especially in projects that require product consistency and recognized quality. Its role is most visible when customers value a full-system offer rather than a low-cost wire product. That makes Belgo Arames important to the structure of the Brazil fencing market, even though the overall field remains widely fragmented.

One of the clearest strategic moves came in October 2024, when Belgo Arames announced a USD 3.92 million investment to double fence-panel production capacity at its Contagem plant. The investment included Brazil’s first dedicated fence-panel production machine and lower electricity consumption, which shows a strategy focused on efficiency and scale in an otherwise price-sensitive market. The company also highlighted Belgo Strada in 2025, a product aimed at highway and railway wildlife boundary applications, suggesting a deliberate move into a more technical niche. These actions show how leading formal players are defending their positions through capacity, specialization, and manufacturing improvements rather than solely through direct price competition. This is a notable pattern in the Brazil fencing market, as it separates formal strategy from the tactics used in lower-cost commodity segments.

Outside the formal leadership group, the market includes many regional wire and mesh fabricators such as Morlan, Sitela Soluções em Fechamentos, Gradisa, Total Telas, and Lagotela. These firms compete strongly in subregional markets where fast delivery, custom fabrication, and direct customer relationships can matter more than national brand scale. The unorganized sector intensifies competition by offering lower-priced standard products without carrying the same compliance and certification burden as formal manufacturers. That creates a market with clear quality tiers and persistent pricing pressure, which is why the Brazil fencing market remains fragmented rather than consolidated as an industrial segment.

Brazil Fencing Industry Leaders

Belgo Arames

Morlan

Sitela Soluções em Fechamentos

Total Telas

Trade Fence

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Cumulative solar investment in Brazil surpassed USD 53.4 billion, with installed solar capacity reaching 68.6 gigawatts and the sector representing 25.3% of national electricity generation. The continued expansion of utility-scale solar farms, particularly in the Northeast semi-arid region, sustained large-volume demand for galvanized steel perimeter fencing at isolated rural sites where theft and vandalism remain operational risks.

- January 2026: Brazil’s New Growth Acceleration Program achieved 100% budget execution for 2025, disbursing the full annual allocation and reaching a total investment impact of USD 64.9 billion for the year. The transport and energy transition sectors, both important for end-use categories, moved at full pace and sustained project-level demand for perimeter and boundary fencing across concession corridors and generation assets.

- April 2025: The Government of the State of São Paulo announced mandatory wildlife crossings and protective perimeter fencing on 916 km of concession highways in the Circuito das Águas and Rota Mogiana lots, as part of a USD 2.9 billion concession investment. Future concessionaires were required to conduct annual roadkill hotspot surveys and install ecologically engineered perimeter fences designed to guide animals to crossing corridors, creating a new, specification-driven vertical of fencing demand with enforceable concession-contract obligations.

Brazil Fencing Market Report Scope

| Metal | Steel |

| Aluminium | |

| Wood | |

| Plastic & Composite | |

| Concrete | |

| Other Materials |

| Residential |

| Agricultural |

| Military & Defense |

| Government |

| Mining |

| Petroleum & Chemicals |

| Energy & Power |

| Other End-Users |

| Fixed / Permanent Fencing |

| Temporary / Mobile Fencing |

| Professional Contractor |

| Others – Fabricators, DIY / Modular Kits |

| São Paulo |

| Rio de Janeiro |

| Salvador |

| Rest of Brazil |

| By Material | Metal | Steel |

| Aluminium | ||

| Wood | ||

| Plastic & Composite | ||

| Concrete | ||

| Other Materials | ||

| By End-User | Residential | |

| Agricultural | ||

| Military & Defense | ||

| Government | ||

| Mining | ||

| Petroleum & Chemicals | ||

| Energy & Power | ||

| Other End-Users | ||

| By Installation Type | Fixed / Permanent Fencing | |

| Temporary / Mobile Fencing | ||

| By Installation Channel | Professional Contractor | |

| Others – Fabricators, DIY / Modular Kits | ||

| By City | São Paulo | |

| Rio de Janeiro | ||

| Salvador | ||

| Rest of Brazil |

Key Questions Answered in the Report

What is the current outlook for fencing demand in Brazil?

The Brazil fencing market is expected to increase from USD 521.37 million in 2026 to USD 702.81 million by 2031 at a CAGR of 6.15%. Demand is being supported by agriculture, infrastructure, housing, and renewable energy simultaneously.

Which material segment leads fencing demand in Brazil?

Metal fencing led with 51.4% of total demand in 2025. Its lead comes from broad use in farms, infrastructure, industrial sites, and standard residential applications

Which end-user group is growing fastest?

Energy and Power is the fastest-growing end-user segment, with a forecast CAGR of 6.89% through 2031. Solar and wind assets require long, secure perimeters because they are often located in remote areas.

Why does the rest of Brazil lead the total demand?

The rest of Brazil accounted for 41.7% of total demand in 2025 and is forecast to grow at a 6.94% CAGR through 2031. Interior states are poised for more agribusiness expansion, renewable energy projects, and land-intensive infrastructure than the main metro markets.

What are the biggest challenges for suppliers?

The biggest challenges are input cost volatility, high installation and maintenance costs in remote areas, and strong price competition from informal producers. These factors can compress margins even while total demand grows.

How are leading companies responding to competition?

Leading formal players are expanding capacity, improving manufacturing efficiency, and moving into specialized niches such as wildlife fencing and certified safety systems. This helps them compete on quality and specifications rather than only on price.

Page last updated on: