Fencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 40.71 Billion |

| Market Size (2031) | USD 54.98 Billion |

| Growth Rate (2026 - 2031) | 6.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fencing Market Analysis by Mordor Intelligence

The Fencing Market size is expected to increase from USD 38.34 billion in 2025 to USD 40.71 billion in 2026 and reach USD 54.98 billion by 2031, growing at a CAGR of 6.19% over 2026-2031.

Rising perimeter-security standards across homes, businesses, and critical infrastructure, together with steady residential construction and remodeling, keep the demand curve moving upward. Material substitution toward vinyl, aluminum, and composite panels is trimming lifetime maintenance costs for property owners, while modular product design is shortening installation time for contractors. Government spending on transport, power, and public facilities in Asia-Pacific and the Middle East is adding long linear runs of specification-grade barrier systems. At the same time, elevated metal and resin prices and a tight global trades workforce are pushing the market toward do-it-yourself (DIY) kits and factory-finished components that minimize on-site labor.

Key Report Takeaways

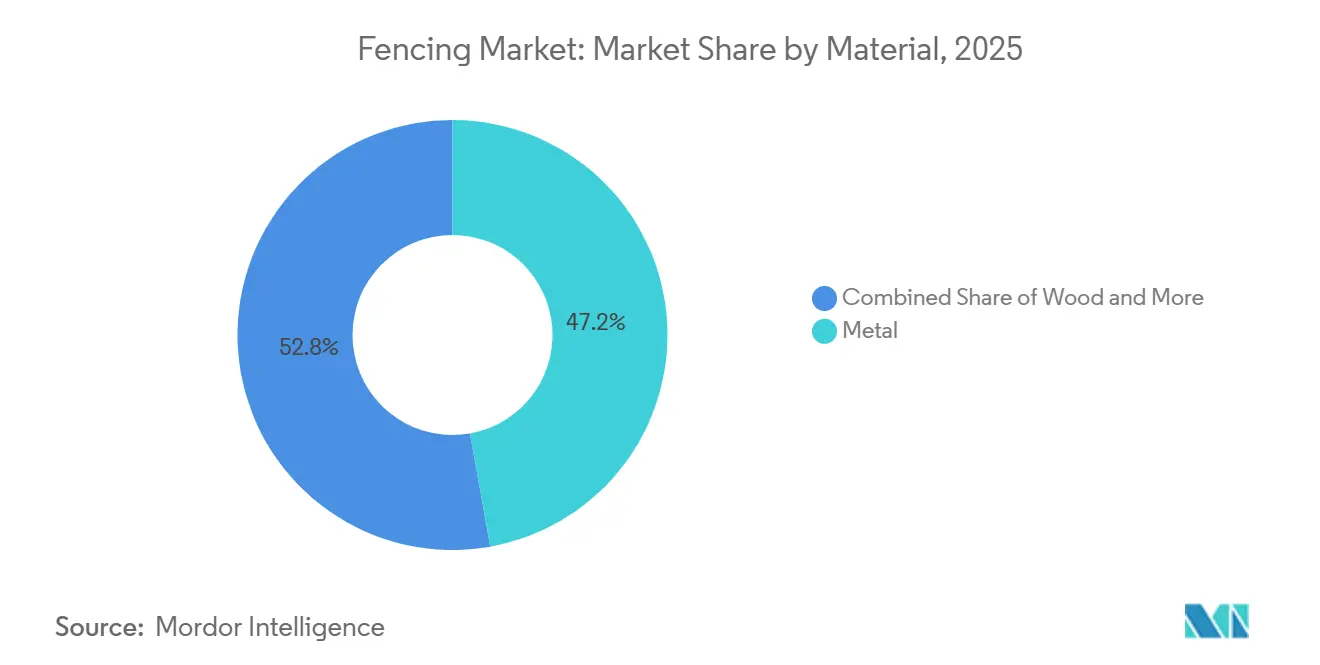

- By material, metal fencing held 47.2% of global revenue in 2025, while plastic and composite products are forecast to grow at a 6.81% CAGR through 2031.

- By end-user, residential applications captured 45.1% of 2025 demand, and the agricultural segment is projected to advance at a 7.16% CAGR over 2026-2031.

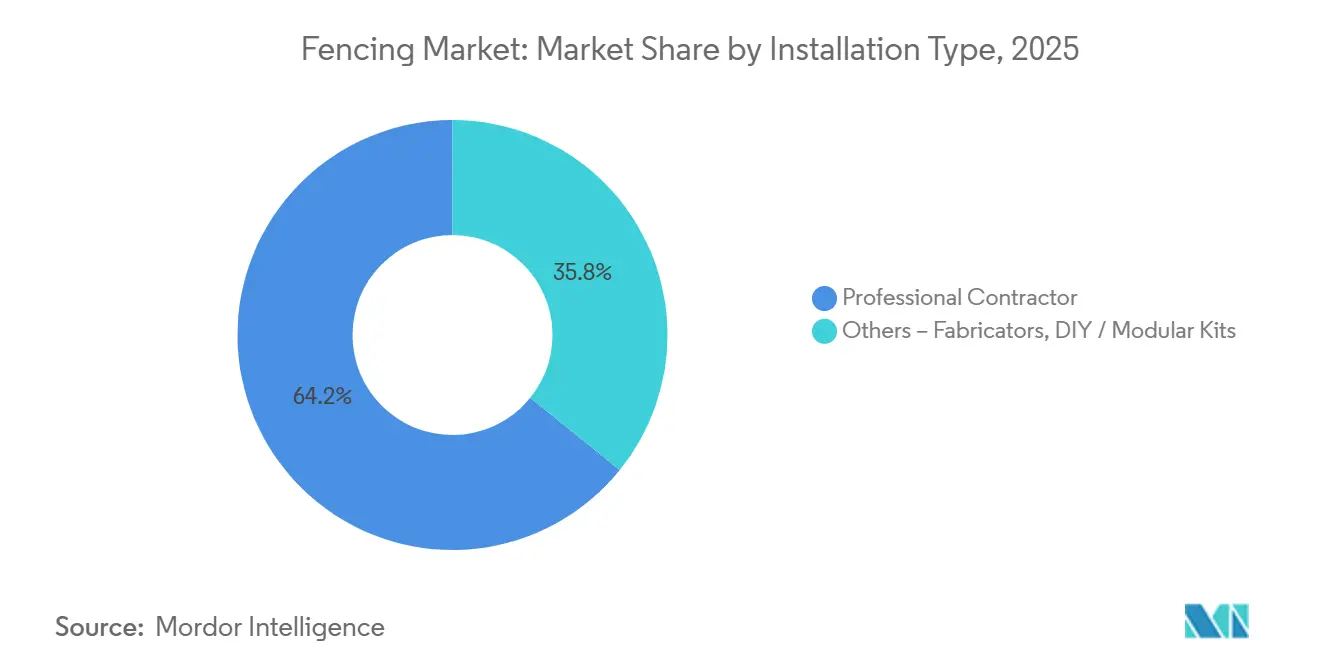

- By installation type, contractor-installed projects commanded 64.2% of sales in 2025, whereas DIY and modular kits are expected to rise at a 6.47% CAGR during 2026-2031.

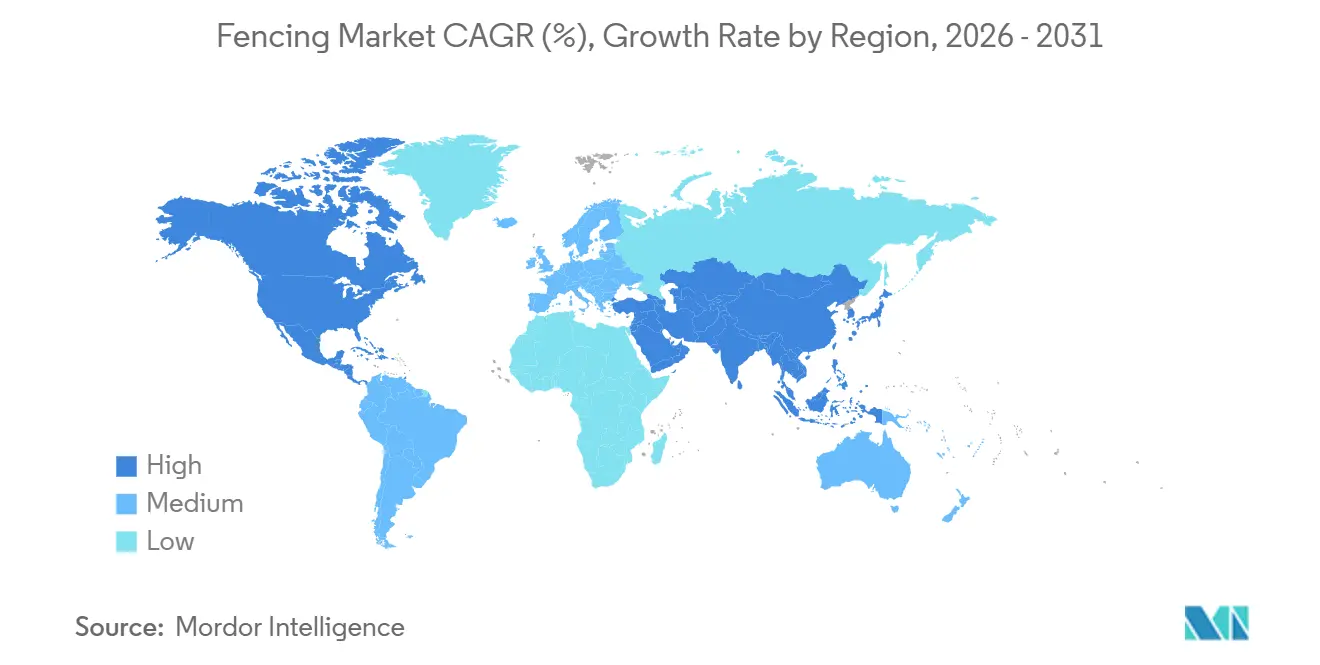

- By geography, Asia-Pacific led with a 33.8% share of 2025 revenue and is anticipated to expand at a 6.92% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fencing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for durable and low-maintenance materials | +1.2% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Growth in residential construction and remodeling | +1.1% | North America, Asia-Pacific, Europe | Short term (≤ 2 years) |

| Rising perimeter-security needs | +0.9% | Global | Short term (≤ 2 years) |

| Expansion of agricultural land protection | +0.8% | Americas, Asia-Pacific | Medium term (2–4 years) |

| Infrastructure and public-facility development | +0.7% | Asia-Pacific, Middle East, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Preference for Durable and Low-Maintenance Materials Boosting Metal, Vinyl, and Composite Fencing Adoption

Vinyl, aluminum, and wood-plastic composite lines are steadily replacing paint-intensive wood rails and galvanized panels. Homeowners value products that never need staining, while facility managers see lifecycle savings from corrosion-proof alloys. Oldcastle APG’s February 2025 purchase of EverStrong Profiles added two East Coast extrusion plants and lifted domestic PVC capacity to meet seasonal spikes in demand[1]CRH plc, “CRH Completes Acquisition of EverStrong Profiles,” crh.com . Aluminum sections, finished with durable powder coats, now dominate coastal builds where salt spray once shortened service life. Composite planks that pair recycled wood fiber with high-density polyethylene deliver wood-grain aesthetics without termite risk, a feature gaining traction in the humid U.S. Southeast. Manufacturers are sharpening vertical integration—complete with on-site resin mixing, in-line fabrication, and recycling streams—to stabilize raw-material inputs and speed customer deliveries.

Growth in Residential Construction and Remodeling Supporting New Fence Installations and Replacements

New-home starts and an aging North American housing stock continue to spur perimeter upgrades. The National Association of Home Builders Remodeling Market Index held at 64 in Q4 2025, signaling healthy backlogs for outdoor projects[2]National Association of Home Builders, “Remodeling Market Index Q4 2025,” nahb.org . Harvard’s Joint Center for Housing Studies counted USD 10.7 billion in fence-related spend across 2.85 million U.S. homeowner jobs. Similar momentum is visible in India, where the FY 2026-27 federal budget earmarks USD 145 billion for capital works, including new rail corridors that require property fencing. These pipelines translate directly into unit demand for posts, panels, and gates. In developed suburbs, replacement cycles are accelerating as aging wood stock succumbs to weather damage, prompting upgrades to composite or metal alternatives.

Rising Perimeter-Security Needs Increasing Demand Across Residential, Commercial, and Industrial Sites

Security codes are tightening worldwide. California’s 2025 Assembly Bills 2371 and 1622 formalize statewide rules for electrified security fences, clearing a regulatory path for higher-spec installations. The U.S. Department of Defense funded perimeter upgrades at Fort Cavazos and other major bases in 2025, highlighting federal appetite for anti-climb and sensor-ready systems. Energy utilities specify anti-ram barriers to satisfy Critical Infrastructure Protection guidelines, while logistics operators adopt tall welded-mesh panels around automated distribution centers. Insurance carriers are also pressuring commercial owners to add physical barriers alongside cameras and lighting to reduce claims risk, turning security fencing from optional to expected.

Expansion of Agricultural Land Protection Driving Demand for Boundary and Livestock Fencing

Farm and ranch operators are modernizing enclosures to improve herd rotation and wildlife stewardship. The U.S. Department of Agriculture Natural Resources Conservation Service (NRCS) shares installation costs for GPS-enabled virtual fencing, pushing adoption on large western ranches[3]U.S. Department of Agriculture, “NRCS Conservation Practice Standards,” usda.gov . South American soy and beef exporters in Brazil and Argentina are posting new woven-wire boundaries to secure high-value acreage amid expanding cultivated land. Wildlife-friendly layouts that reduce pronghorn and elk entanglement are gaining regulatory favor, especially in states that track migration corridors. Hybrid systems that pair physical perimeter fence with interior virtual paddocks balance capital outlay against operational flexibility and are drawing early adopters across Australia and the United States.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of steel, aluminum, and resin-based materials | -0.9% | Global, with acute impact in North America, Europe, the Middle East | Short term (≤ 2 years) |

| High installation and labor costs | -0.7% | North America, Europe, Australia | Medium term (2–4 years) |

| Zoning, permitting, and property-line compliance delays | -0.5% | North America (urban markets), Europe, Asia-Pacific (high-density cities) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Steel, Aluminum, and Resin-Based Materials Pressuring Margins

Commodity turbulence is tightening profits across the fencing supply chain. Aluminum traded at USD 3,333.50 per tonne in March 2026, up 25.07% year over year after Middle East supply disruptions reduced global output by roughly 10%. Steel coil shows similar volatility as tariffs shift and blast-furnace curtailments ripple through spot markets. Polyvinyl chloride and high-density polyethylene resin prices mirror crude-oil swings, making budget estimates for vinyl and composite kits a moving target. Contract bidders lock in prices months ahead, risking exposure when mill surcharges rise mid-project. Larger manufacturers partly hedge with long-term supply agreements and in-house recycling, yet small regional fabricators often absorb rising costs or cede contracts.

High Installation and Labor Costs Limiting Uptake in Price-Sensitive Projects

Qualified fence crews remain scarce. Median installer wages in the United States climbed 6.2% in 2025, outpacing overall construction labor gains. United Kingdom tender prices advanced 2.52% the same year, with industry trackers expecting another 3.5% lift in 2026. Higher bids push residential customers toward DIY systems, while commercial builders delay non-critical perimeter work. Manufacturers are responding with click-fit rails, pre-routed posts, and lightweight panels that two people can set without powered equipment. These innovations trim on-site person-hours, but until labor supply expands, installed costs will stay elevated and may cap demand in budget-constrained segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Composite and Vinyl Stretch Growth Potential

Metal products captured a 47.2% fencing market share in 2025 as steel and aluminum remained the default for high-security and industrial sites. Concrete sound walls and barrier slabs fill niche safety roles along highways and rail corridors. Conversely, vinyl and other plastic-composite formats are forecast to log a 6.81% CAGR through 2031, outpacing every other material class and enlarging the fencing market size for value-added, low-maintenance solutions. Homeowners in hurricane-prone Florida and humidity-high Southeast Asia are migrating toward PVC and wood-plastic composites that carry limited lifetime warranties and resist rot, insects, and salt spray. Oldcastle APG’s rolling acquisitions since 2022 have consolidated Bufftech, SimTek, and National Vinyl Products under one umbrella, giving the company national reach in extrusion, compounding, and post-consumer PVC reclamation.

Despite lower upfront cost, pressure-treated pine is losing share as end users weigh repaint cycles and replacement frequency against higher one-time material outlays. Meanwhile, recycled-content mandates in California and European Union markets are steering municipal buyers toward composite planks that integrate reclaimed PVC or polyethylene. Metal will retain primacy where structural rigidity and anti-ram ratings are non-negotiable, yet composite variants with steel-reinforced rails are closing the gap in light-commercial builds. Fast-cure powder-coat lines and value-engineered alloys also keep aluminum in pole position for decorative pool enclosures, particularly when local codes require non-corrosive framing.

By End-User: Agricultural Demand Breaks from the Pack

Residential projects accounted for 45.1% of global revenue in 2025, underpinning the day-to-day volume of the fencing market. Privacy screens, dog runs, and ornamental pickets dominate homeowner wish lists, and integrated solar-lighting post caps now bundle energy efficiency with curb appeal. The agricultural segment, however, is projected to register the fastest 7.16% CAGR through 2031, fueled by cost-share incentives for virtual fencing and expanding pasture acreage across Latin America. U.S. NRCS programs reimburse up to 75% of a rancher’s outlay for GPS-controlled collars, and Australian beef producers report 30% labor savings once rotational grazing routes are software-defined.

Military bases, utilities, and government parks provide predictable replacement cycles as legacy chain-link is swapped for anti-climb welded mesh with integrated fiber-optic intrusion lines. Mining and petrochemical complexes require heavy-gauge steel frameworks to pass OSHA (Occupational Safety and Health Administration) audits, while data-center operators are standardizing on dual-perimeter layouts that combine vehicle wedge barriers with micro-mesh inner partitions. These higher-spec installations carry premium margins and often bundle maintenance contracts, widening revenue per linear foot against commodity farm wire.

By Installation Type: DIY Channels Close the Distance to Pros

Contractor crews booked 64.2% of global revenue in 2025, reflecting the complexity of commercial projects and the value clients place on turnkey permitting and artistry warranties. Yet the DIY and modular-kit segment is on track for a 6.47% CAGR to 2031, driven by a shortfall of skilled installers and the prevalence of step-by-step video guidance distributed by retailers such as Home Depot and Lowe’s. Flat-packed aluminum screen rooms introduced under Oldcastle APG’s EncloSure label in 2024 can be erected over a weekend with basic power tools and comply with International Residential Code wind-load provisions.

Fabricator supply houses are bridging the gap between big-box kits and full custom builds by offering color-matched gates, lock sets, and variable-slope panels that adapt to uneven grades. Online configurators let homeowners draw lot lines on satellite images, auto-populate post counts, and receive delivered-to-door cut sheets, shrinking design lead times from weeks to hours. For small contractors, these digital tools translate into faster quotes and reduced jobsite waste, making the hybrid pro-DIY channel a rising share gainer inside the broader fencing market.

Geography Analysis

Asia-Pacific held 33.8% of the total 2025 revenue, and its 6.92% forecast CAGR secures the region’s spot as the chief accelerator of the fencing market. China’s manufacturing and transport build-out, underscored by 3,109 kilometers of rail laid in 2025, ensures that temporary safety barriers and permanent right-of-way fences are shipped by the trainload even while residential real-estate spending retracts. India’s USD 145 billion capital budget prioritizes seven high-speed rail corridors and industrial parks, creating continuous demand for boundary protection around depots and worker colonies. Urban upgrades in Indonesia, Vietnam, and the Philippines extend the runway for low-cost chain-link and PVC picket systems, as household formation and government housing schemes edge higher.

North America supplies depth and steady cash flow. U.S. housing starts remained firm through December 2025 despite high mortgage rates, pushing a pipeline of subdivision fences and homeowner associations’ board-approved privacy screens. The NAHB forecasts a 3% rise in remodeling outlays during 2026, further inflating replacement volume as weathered cedar pickets make way for composite slats. Canada adds incremental lift as immigration keeps new-home completions high, and Mexican border-zone industrial parks are fortifying perimeters to protect just-in-time inventories from theft.

Europe shows a more tempered but resilient pattern, with the Ifo Institute projecting 2.4% real construction growth in 2026. Germany’s EUR 500 billion Special Fund for Infrastructure and Climate is channeling up to EUR 210 billion toward public works, and civil-engineering allocations—mostly transport and grid upgrades—represent roughly 70% of that spend. Renovation now exceeds new-build value in both residential and non-residential segments, pulling through replacement fence orders that favor fast-install steel mesh and decorative aluminum over raw timber in densely populated urban blocks. The United Kingdom and Spain follow a similar retrofit track, although ongoing labor shortages have lengthened install lead times and nudged buyers toward factory-prefinished kits.

Note: Segments share of all individual segments available upon report purchase

Competitive Landscape

Market power is consolidating, yet still far from a monopoly. Oldcastle APG fused eight legacy labels into Catalyst Fence Solutions in January 2025, instantly scaling manufacturing in vinyl, molded-composite, aluminum, and steel lines across North America. With unified warranties and centralized customer care, the company is leveraging combined purchasing to blunt raw-material inflation and negotiate national retailer shelf space. Rival Beta fence, anchored in Belgium, courts critical-infrastructure clients with anti-ram mesh and integrated sensor grids, while its 2014 Secure USA buy-in gave it rapid entry to the U.S. vehicle-barrier business.

Product innovation is moving fast. Gregory Industries inaugurated a 90,000-square-foot, highly automated G-STRUT mill in Alabama in July 2025, trimming lead times for galvanized channels that double as fence posts and solar-array supports. Trex Company has extended its composite-decking fame to perimeter panels, marketing color-matched railing and picket kits that bundle with its core outdoor-living catalog. Smaller regional fabricators survive on custom scrollwork, rapid turnarounds, and permit-navigation services that the giants struggle to replicate across thousands of municipalities.

Technology is another front. Cloud-based configurators now calculate post spacing, gate swing clearances, and bill of materials in minutes, cutting design costs for pros and reducing errors for homeowners. Sensor manufacturers are embedding fiber optics into welded mesh, allowing real-time breach detection that links to site security dashboards. While smart-fence uptake remains under 5% of global footage, pilot installations at data centers and airports show premium pricing potential and recurring revenue via monitoring subscriptions, a field the industry’s largest players aim to cultivate.

Fencing Industry Leaders

CertainTeed

PLY Gem

Bekaert

BetaFence

Ameristar Perimeter Security

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Oldcastle APG acquired EverStrong Profiles, adding two vinyl extrusion plants on the U.S. East Coast and becoming the primary rail-and-fence supplier to Eastern Wholesale Fence.

- July 2024: Gregory Industries opened a 90,000-square-foot G-STRUT framing plant in Athens, Alabama, described as the most modern strut mill worldwide.

- March 2025: James Hardie agreed to buy The AZEK Company for USD 8.75 billion, expanding the combined North American exterior product TAM to USD 23 billion.

- January 2025: Oldcastle APG launched Catalyst Fence Solutions, bringing Barrette Outdoor Living, National Vinyl Products, Bufftech, and other brands under one banner with a transferable limited lifetime warranty.

Global Fencing Market Report Scope

| Metal | Steel |

| Aluminium | |

| Wood | |

| Plastic & Composite | |

| Concrete | |

| Other Materials |

| Residential |

| Agricultural |

| Military & Defense |

| Government |

| Mining |

| Petroleum & Chemicals |

| Energy & Power |

| Other End-Users |

| Professional Contractor |

| Others – Fabricators, DIY / Modular Kits |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific |

| By Material | Metal | Steel |

| Aluminium | ||

| Wood | ||

| Plastic & Composite | ||

| Concrete | ||

| Other Materials | ||

| By End-User | Residential | |

| Agricultural | ||

| Military & Defense | ||

| Government | ||

| Mining | ||

| Petroleum & Chemicals | ||

| Energy & Power | ||

| Other End-Users | ||

| By Installation Type | Professional Contractor | |

| Others – Fabricators, DIY / Modular Kits | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What CAGR is projected for the fencing market between 2026 and 2031?

The market is forecast to grow at a 6.19% CAGR over the 2026-2031 period.

Which material class is expected to post the fastest growth?

Plastic and composite systems are projected to register a 6.81% CAGR through 2031.

How large was the residential slice of global 2025 sales?

Residential projects generated 45.1% of worldwide revenue in 2025.

Why are DIY kits gaining popularity?

Labor shortages and higher installer wages are steering price-sensitive buyers toward modular, homeowner-friendly kits that reduce on-site hours.

Which region will add the most incremental demand by 2031?

Asia-Pacific, led by China and India, is expected to remain the fastest-expanding region with a 6.92% forecast CAGR.

What key risk could slow near-term growth?

Volatile steel, aluminum, and resin prices can squeeze margins and raise end-user costs, potentially delaying new projects.

Page last updated on: