India Fencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.34 Billion |

| Market Size (2026) | USD 2.51 Billion |

| Market Size (2031) | USD 3.55 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Fencing Market Analysis by Mordor Intelligence

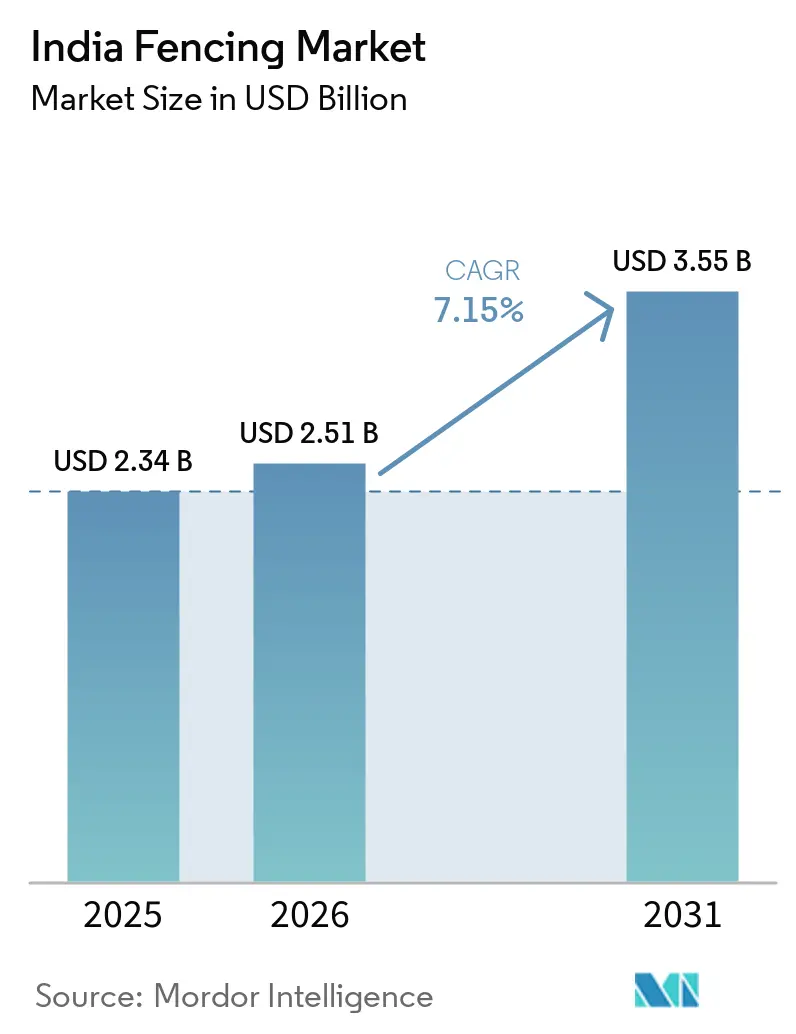

The India Fencing Market size is projected to be USD 2.34 billion in 2025, USD 2.51 billion in 2026, and reach USD 3.55 billion by 2031, growing at a CAGR of 7.15% from 2026 to 2031.

Public spending plays a more significant role than private real estate in shaping the market, providing a stable demand base compared to other building material categories. Key drivers include border infrastructure projects, roads, railways, utilities, and public compounds, which ensure strong order visibility for organized suppliers. For instance, the FY2026 border infrastructure allocation increased to USD 0.7 billion, and the India-Myanmar border fencing program was approved at USD 3.7 billion. Additionally, the market is supported by industrial park expansions, warehousing investments, and logistics corridor developments, which require formal perimeter systems and compliance documentation. Agricultural demand is also increasing due to rising wildlife conflicts, crop protection needs, and the adoption of solar electric fencing programs in rural areas across several states. However, margin pressure remains a key challenge, as input costs for steel, aluminum, and polymers fluctuate, while unorganized fabricators continue to dominate price-sensitive rural markets.

Key Report Takeaways

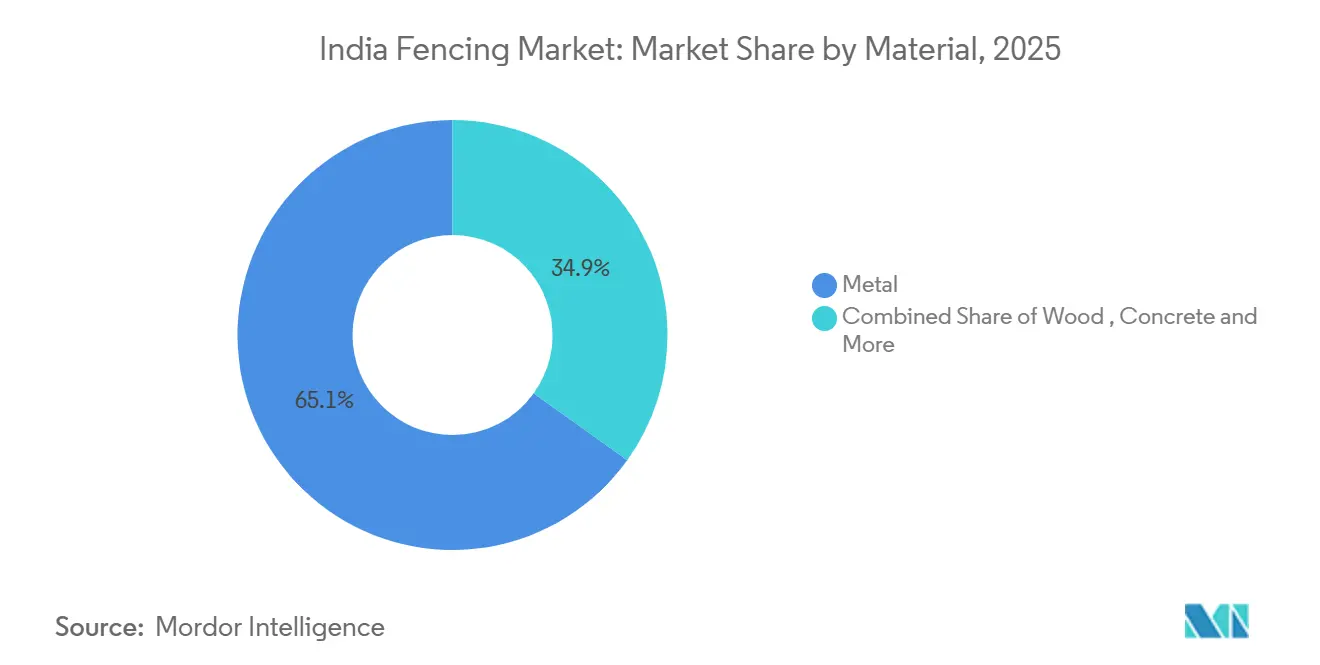

- By material, metal fencing led with 65.1% revenue share in 2025, while plastic and composite fencing are forecast to expand at a 7.91% CAGR through 2031.

- By end-user, government buyers accounted for 30.5% of the India fencing market in 2025, while agricultural fencing recorded the highest projected CAGR of 8.11% through 2031.

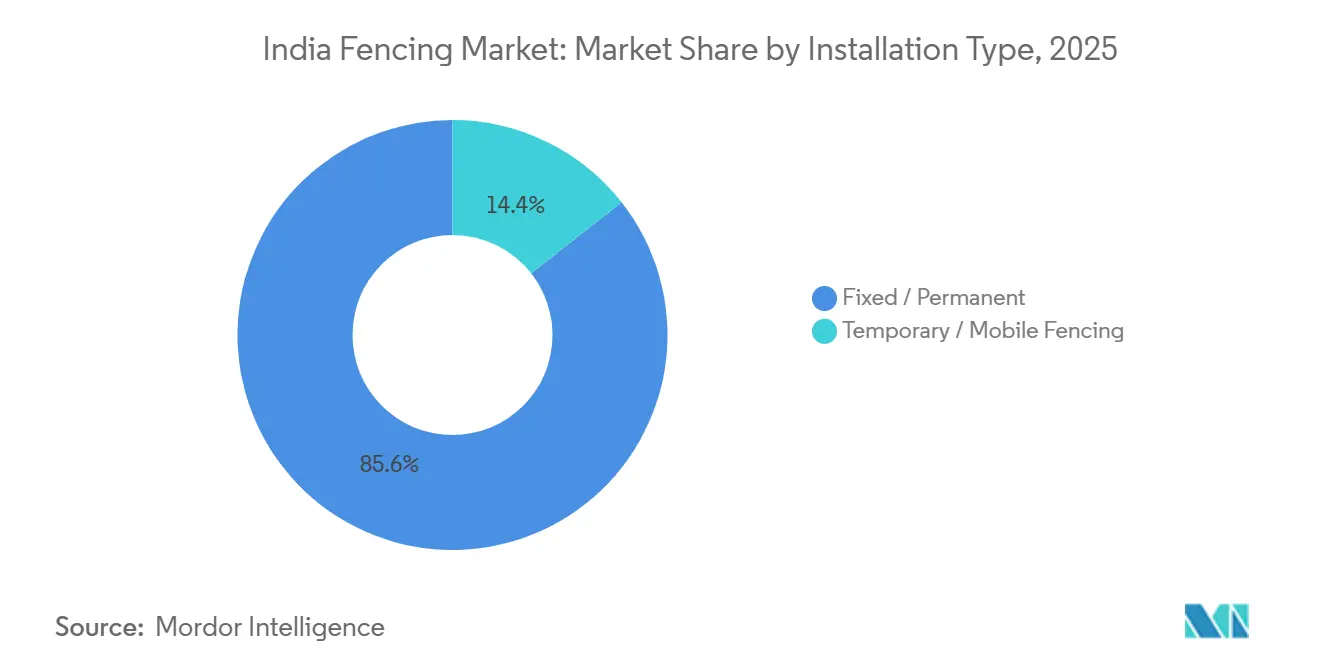

- By installation type, fixed and permanent fencing accounted for 85.6% of the India fencing market share in 2025, while temporary and mobile fencing is advancing at a 7.61% CAGR through 2031.

- By installation channel, professional contractors commanded 70.2% of revenues in 2025, while the DIY and modular kits channel is projected to grow at a 7.72% CAGR through 2031.

- By city, the Mumbai Metropolitan Region accounted for 16.3% of revenues in 2025, while Hyderabad is forecast to grow at a 8.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Fencing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government initiatives for border security and infrastructure projects | +1.5% | National, concentrated in Jammu and Kashmir, Punjab, Rajasthan, West Bengal, and northeast India. | Short term (≤ 2 years) |

| Government infrastructure development across roads, railways, and public facilities | +1.2% | National, with early gains in Bharatmala and PM GatiShakti corridors. | Medium term (2-4 years) |

| Growth in industrial parks, warehouses, and logistics hubs | +0.9% | Mumbai Metropolitan Region, Delhi National Capital Region, Pune, Bengaluru, and Hyderabad. | Medium term (2-4 years) |

| Increasing agricultural protection needs | +0.7% | Uttar Pradesh, Maharashtra, Madhya Pradesh, Odisha, Rajasthan, and Karnataka. | Short term (≤ 2 years) |

| Rising security concerns for institutional and industrial sites | +0.6% | National, concentrated in metro cities and industrial corridors. | Short term (≤ 2 years) |

| Wildlife protection and human-animal conflict mitigation | +0.4% | Assam, Uttar Pradesh, West Bengal, Odisha, Tamil Nadu, and Karnataka. | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Border Security: Sovereign Mandates Unlock Multi-Year Procurement

The India fencing market is seeing border work move from periodic buying to a long-cycle infrastructure program. India had already fenced 93.25% of its border with Pakistan and 79.08% of its border with Bangladesh. At the same time, the 1,643 km Myanmar frontier moved into a new execution phase after the USD 3.7 billion project was approved in 2024[1]Department for Promotion of Industry and Internal Trade, “PM GatiShakti National Master Plan Update,” Department for Promotion of Industry and Internal Trade, dpiit.gov.in. In May 2025, the Ministry of Home Affairs also cleared USD 0.2 billion to replace more than 500 km of aging fencing on the Pakistan border with modular, multi-layered barriers. The Comprehensive Integrated Border Management System, a smart-fencing model, is expanding the product mix by linking barriers with sensors, thermal imaging, and surveillance tools. This keeps the India fencing market less exposed to normal construction cycles and gives organized suppliers a visible project pipeline.

Industrial Parks and Logistics Hubs: Plug-And-Play Infrastructure Creates Structured Fencing Demand

The India fencing market is also gaining from the spread of planned industrial parks and warehouse campuses that buy perimeter systems through formal specifications. India’s warehousing sector drew USD 1.96 billion in institutional investment in 2024, while Grade A stock had expanded at a 21% CAGR over the prior five years. In March 2026, the Union Cabinet approved the BHAVYA scheme at USD 4.0 billion to develop 100 industrial parks with plug-and-play infrastructure, which makes perimeter fencing part of the base project scope rather than a later add-on. The Department for Promotion of Industry and Internal Trade stated that PM GatiShakti had mapped more than 600 projects, including industrial corridors and logistics parks, which support long-horizon site development[2]Government of India, “Entire Border With Myanmar to Be Fenced in Ten Years, Say Government Officials,” The Hindu, thehindu.com. This gives the India fencing market a stronger mix of repeatable project demand from industrial and logistics users.

Agricultural Fencing: Crop Losses and Wildlife Pressure Drive Rural Electrification Of Perimeters

Agricultural fencing is becoming one of the most active demand pockets in the India fencing market because crop loss and animal intrusion are pushing buyers toward stronger perimeter solutions. The Uttar Pradesh Forest and Wildlife Department installed nearly 272 km of fencing across 2023-24 and 2024-25, using both chain-link and solar systems to reduce conflict near farms and settlements. In Valparai, Tamil Nadu, the Forest Department deployed 1,300 solar units as part of a smart virtual fencing setup that cost USD 0.4 million and used infrared sensing and alerts in hard-to-patrol terrain. These examples show that state agencies and supported local programs are important channels for rural solar fencing adoption. That pattern matters because the India fencing market is getting farm demand through public and grant-backed spending, not only through hardware retail.

Rising Security Concerns: Industrial And Institutional Buyers Upgrade Perimeter Systems

The India fencing market is moving toward higher-specification products for energy, petroleum, and other critical sites, where passive barriers are no longer sufficient. Godrej Security Solutions reported 20% business growth in September 2025 and has been bundling electric fencing with closed-circuit television, access control, and solar backup into one perimeter package[3]Godrej Enterprises Group, “Premise Security,” Godrej Enterprises Group, godrejenterprises.com . Electric fencing for sensitive facilities is also tied to Indian Standard 302-2-76 safety rules for fence energizers, which raises the bar for suppliers and installers. Industry events in 2024 and 2025 also highlighted concertina wire, razor wire, and integrated perimeter formats that sit above simple per-meter pricing. This shift supports a steadier value mix in the India fencing market, especially in organized channels.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating steel, aluminum, and PVC prices | -0.7% | National, with higher exposure in regions dependent on imported PVC and aluminum | Short term (≤ 2 years) |

| Price sensitivity among rural and small-scale buyers | -0.5% | Rural India, especially Uttar Pradesh, Bihar, Madhya Pradesh, Rajasthan, and Odisha | Long term (≥ 4 years) |

| Competition from unorganized local manufacturers | -0.4% | Tier 2, Tier 3, and rural markets across India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Input Cost Volatility: Steel Softness and Polymer Spikes Create Asymmetric Margin Pressure

The India fencing market faces a difficult cost mix because steel, aluminum, and PVC are not moving in the same direction. Wire rod prices dropped to USD 451-455 per tonne in October 2025, while PVC costs rose by up to 30% and aluminum prices increased by 8-10% over the same broad period. This helps basic steel-heavy products but puts pressure on composite and PVC-coated fencing, which are seeing improving demand. Producers with mixed portfolios, therefore, face uneven margin performance across product lines. The India fencing market can still grow under these conditions, but cost swings are likely to slow full adoption in newer material categories.

Unorganized Competition: Fragmented Supply Base Restrains Quality Standardization

The India fencing market remains exposed to unorganized competition in agricultural, residential, and small commercial demand. Small local fabricators often win on lead time, flexible order sizes, and low upfront pricing, making it harder for certified brands to expand penetration in price-sensitive areas. This keeps a clear split in the market, with organized players stronger in government, defense, and Grade A industrial work. At the same time, informal suppliers stay active in rural and smaller cities. Bekaert’s decision to discontinue Steel Wire Solutions production in India in H1 2025 showed how hard it is for some commodity wire tiers to defend on cost. Until quality standards carry more weight in rural buying, this will remain a drag on the India fencing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Galvanised Steel Anchors Demand, Composites Gaining Velocity

Metal fencing accounted for 65.1% of market revenues in 2025, maintaining its position as the largest material category in the India fencing market. Galvanized mild steel wire mesh, barbed wire, and chain-link panels still lead volume because government tenders and border projects favor certified and proven products. Aluminum fencing serves a smaller premium niche in coastal and chemical settings where corrosion resistance matters more than cost. Concrete fencing continues to hold a role in highway barriers and utility compounds, while wood remains limited to decorative residential use.

Plastic and composite fencing is the fastest-growing segment, with a 7.9% CAGR for 2026-2031, and this part of the India fencing market is expanding in gated housing and landscaped campuses. Wood-plastic composite and high-density polyethylene panels are gaining acceptance where appearance, low maintenance, and termite resistance offset the higher initial cost. Karnataka’s Industrial Policy 2025-2030 supports investment in electronics, aerospace, and electric vehicle clusters, which aligns with demand for modular perimeter formats in cleaner industrial settings. Within the India fencing industry, this mix keeps metal dominant while giving composites a clearer growth lane.

By End-User: Government Procurement Dominates, Agriculture Outpacing All Others

Government end-users accounted for 30.5% of the India fencing market in 2025, making them the single largest demand group. Demand came from defense compounds, railway boundaries, national highways, border programs, and public utility sites. The BHAVYA scheme and the PM GatiShakti pipeline strengthen this position, as park, road, and logistics projects require perimeter systems early in the build cycle. Defense-linked orders also carry higher product specifications, which support better selling prices than basic enclosure work.

Agricultural fencing is the fastest-growing end-user segment, with a 8.1% CAGR for 2026-2031. Growth is strongest where crop losses, livestock movement, and wildlife conflict create a direct need for preventive fencing. Mining, petroleum and chemicals, and energy and power remain smaller in share, but they are important because they buy high-specification systems and are less tied to normal housing cycles. In the India fencing industry, residential demand is smaller today, but online sourcing and prefabricated kits are starting to expand access for urban homeowners.

By Installation Type: Permanent Fencing Commands The Market

Fixed and permanent fencing accounted for 85.6% of the India fencing market in 2025, reflecting the heavy weight of public, industrial, and farm installations. These projects usually require concrete-set posts, galvanized mesh or wire, and a long service life, so organized contractors are better placed to execute them. Border systems, industrial perimeters, and field boundaries all fit this model and reinforce the segment’s lead. The result is a market structure that favors durability and formal procurement over quick-turn temporary supply.

Temporary and mobile fencing is the fastest-growing installation type at a 7.6% CAGR for 2026-2031. Construction site enclosures, crowd management needs, and rapid-deployment barriers are the main demand drivers behind this rise. Border replacement programs are also introducing modular elements that enable faster repairs and section-level replacements in sensitive locations. Even so, the India fencing market will remain centered on permanent systems, as most core use cases require long-lasting installations.

By Installation Channel: Contractors Lead, Self-Install Channels Accelerating

Professional contractors commanded a 70.2% revenue share in 2025, which made them the leading installation channel in the India fencing market. Large public and industrial projects are routed through tender systems, bill of quantities documents, and compliance checks that favor traceable suppliers and experienced installers. This channel also supports post-installation service, warranty handling, and quality verification on larger sites. As a result, organized manufacturers are more protected in the highest-value project bands.

The DIY and modular kits channel is forecast to grow at a 7.7% CAGR for 2026-2031. Rural buyers and urban households are increasingly using digital procurement and online comparison tools to source standard panels and wire formats without hiring a full contractor. That change reduces buying friction for smaller orders and helps bring new customers into the India fencing market. It also puts pressure on distribution margins because product comparisons are becoming easier and pricing is more transparent.

Geography Analysis

Mumbai Metropolitan Region held 16.3% of the India fencing market in 2025, while Hyderabad is set to record the fastest city growth at 8.2% through 2031. Mumbai’s leadership comes from its large warehousing base, petrochemical exposure, and logistics assets around the Jawaharlal Nehru Port Authority corridor. The city absorbed 18.6 million sq ft of warehousing space in 2024, translating into visible perimeter demand for large, campus-style facilities. Delhi National Capital Region remains another major center for the India fencing market because public infrastructure, data centers, and logistics hubs generate steady institutional demand.

The government-approved Dadri Multi-Modal Logistics Hub in Greater Noida, valued at USD 0.7 billion, adds a long build cycle for perimeter systems in the Delhi National Capital Region. Kolkata is also gaining relevance because eastern supply routes are tied to border projects in West Bengal and the northeast. The Press Information Bureau stated in February 2025 that 3,240 km of the 4,097 km of the Bangladesh border had already been fenced, keeping procurement activity visible in the east. Hyderabad’s momentum comes from industrial redevelopment, logistics expansion, and road programs advancing simultaneously. Bengaluru is also strengthening its position in the India fencing market, as the state's policy targets USD 89.3 billion in new investments by 2030 and supports the development of more industrial areas.

Pune and Chennai remain dependable demand centers for the India fencing market because industrial logistics activity and port-linked infrastructure continue to require organized perimeter security. The rest of India segment is important for volume because agricultural and wildlife fencing programs are spreading into smaller cities and rural districts. Odisha, Assam, Uttar Pradesh, and Tamil Nadu show how state-led solar and wildlife fencing programs can create demand even where urban industrial channels are less developed. This keeps the India fencing market geographically broad, with high-value urban projects and high-volume rural applications growing simultaneously.

Competitive Landscape

The India fencing market remains structurally fragmented, with no single player holding more than 8-10% of national revenue. More than 3,000 organized and unorganized manufacturers operate across the supply chain, keeping the competitive landscape broad and crowded. The market has three visible layers. At the top are integrated perimeter security specialists that combine physical fencing with electric deterrence, artificial intelligence surveillance, and cloud monitoring for government, defense, and critical infrastructure projects. At the bottom, local fabricators, galvanizing shops, and wire traders continue to hold a large share of demand, which keeps pricing pressure high across the mass market.

The mid-tier comprises regional manufacturers with strong local reach and long-standing dealer relationships. Companies such as VBS Group continue to defend their position through deep distribution depth, especially in agricultural and semi-commercial applications, where buyer loyalty still matters. In the organized part of the market, compliance is becoming a stronger competitive filter as Bureau of Indian Standards certification under IS 278 and IS 4826 is enforced more closely in formal procurement. This is gradually limiting the role of informal suppliers in government-tendered work. Even so, the Micro, Small, and Medium Enterprise fringe still absorbs an estimated 40-45% of market value and continues to limit margin expansion for larger players.

Three strategic patterns are shaping the organized segment. Tech-integrated perimeter security firms are moving away from simple per-meter pricing by offering electric deterrence, artificial intelligence cameras, vibration sensors, anti-drone modules, and central monitoring software as part of a single system, and Godrej & Boyce's 20% growth in FY2025 shows how this model is helping companies win institutional premiums. Digital-first direct-to-consumer players such as JustFence are also changing distribution by using online configuration tools, multi-city fulfillment, and an expanding dealer program to reach more than 10,000 customers without relying fully on contractors. A third pattern is technical partnership leverage, where companies such as Static Systems Electronics use exclusive rights for compliant energizer systems to access prisons, solar power plants, and defense sites through product credentials rather than price. The clearest open space remains solar agricultural fencing, where forest departments and non-government organizations still shape procurement and where commercial firms have not yet built strong enough last-mile rural distribution.

India Fencing Industry Leaders

A-1 Fence Products

India Fence

Maa Vishla Industries (MV FENCE)

JustFence

Sharda Wires

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Union Cabinet approved the BHAVYA scheme (USD 4.0 billion) to build 100 plug-and-play industrial parks across India, ranging from 100 to 1,000 acres each, with NICDC as the implementing agency. Mandatory perimeter-security infrastructure in each park directly expands the procurement of structured fencing across multiple states.

- September 2025: Godrej Security Solutions reported 20% business growth, driven by an expanded channel-partner network, smart perimeter-security product integration, and increased uptake from institutional buyers. The company had previously unveiled its Pole Detector and electric fencing systems at IFSEC India 2024 in December 2024.

- June 2025: The Uttar Pradesh Forest and Wildlife Department completed installation of approximately 272 km of fencing (231 km chain-link and 41 km solar) across forest-fringe areas over 2023–24 and 2024–25 to mitigate human-animal conflict, marking one of the largest state-funded wildlife fencing programs in India.

- May 2025: The Center cleared an outlay of USD 0.2 billion to replace over 500 km of aging Pakistan-border fencing in Jammu & Kashmir, Punjab, and Rajasthan with modular, multi-layered, anti-cut barriers; the project also includes bulletproof sentry posts and improved BOB access roads, signaling a product-specification upgrade that benefits organized fencing manufacturers over informal contractors.

India Fencing Market Report Scope

| Metal | Steel |

| Aluminium | |

| Wood | |

| Plastic & Composite | |

| Concrete | |

| Other Materials |

| Residential |

| Agricultural |

| Military & Defense |

| Government |

| Mining |

| Petroleum & Chemicals |

| Energy & Power |

| Other End-Users |

| Fixed / Permanent Fencing |

| Temporary / Mobile Fencing |

| Professional Contractor |

| Others – Fabricators, DIY / Modular Kits |

| Mumbai Metropolitan Region |

| Delhi NCR |

| Pune |

| Bengaluru |

| Hyderabad |

| Chennai |

| Kolkata |

| Rest of India |

| By Material | Metal | Steel |

| Aluminium | ||

| Wood | ||

| Plastic & Composite | ||

| Concrete | ||

| Other Materials | ||

| By End-User | Residential | |

| Agricultural | ||

| Military & Defense | ||

| Government | ||

| Mining | ||

| Petroleum & Chemicals | ||

| Energy & Power | ||

| Other End-Users | ||

| By Installation Type | Fixed / Permanent Fencing | |

| Temporary / Mobile Fencing | ||

| By Installation Channel | Professional Contractor | |

| Others – Fabricators, DIY / Modular Kits | ||

| By City | Mumbai Metropolitan Region | |

| Delhi NCR | ||

| Pune | ||

| Bengaluru | ||

| Hyderabad | ||

| Chennai | ||

| Kolkata | ||

| Rest of India |

Key Questions Answered in the Report

What is the size outlook for the India fencing market through 2031?

The India fencing market is projected to move from USD 2.5 billion in 2026 to USD 3.6 billion by 2031 at a 7.15% CAGR.

What is driving demand the most in India right now?

Public spending is the main driver, especially for border works, roads, utilities, railways, and industrial parks. This makes demand more stable than in many construction-linked categories.

Which material category leads demand in India?

Metal fencing led with 65.1% revenue share in 2025 because it remains the standard choice for government, defense, industrial, and farm applications.

Which end-user group is growing the fastest?

Agricultural fencing is the fastest-growing end-user segment, with an 8.11% CAGR through 2031, supported by crop protection needs and wildlife conflict mitigation.

Which installation channel is most important for suppliers?

Professional contractors remain the largest channel, accounting for 70.2% of revenues in 2025, as large projects still rely on tendering, compliance checks, and formal installation.

Which city markets matter the most for growth?

Mumbai Metropolitan Region led the value share with 16.3% in 2025, while Hyderabad is expected to grow the fastest at a 8.22% CAGR through 2031.

Page last updated on: