Indonesia Fencing Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

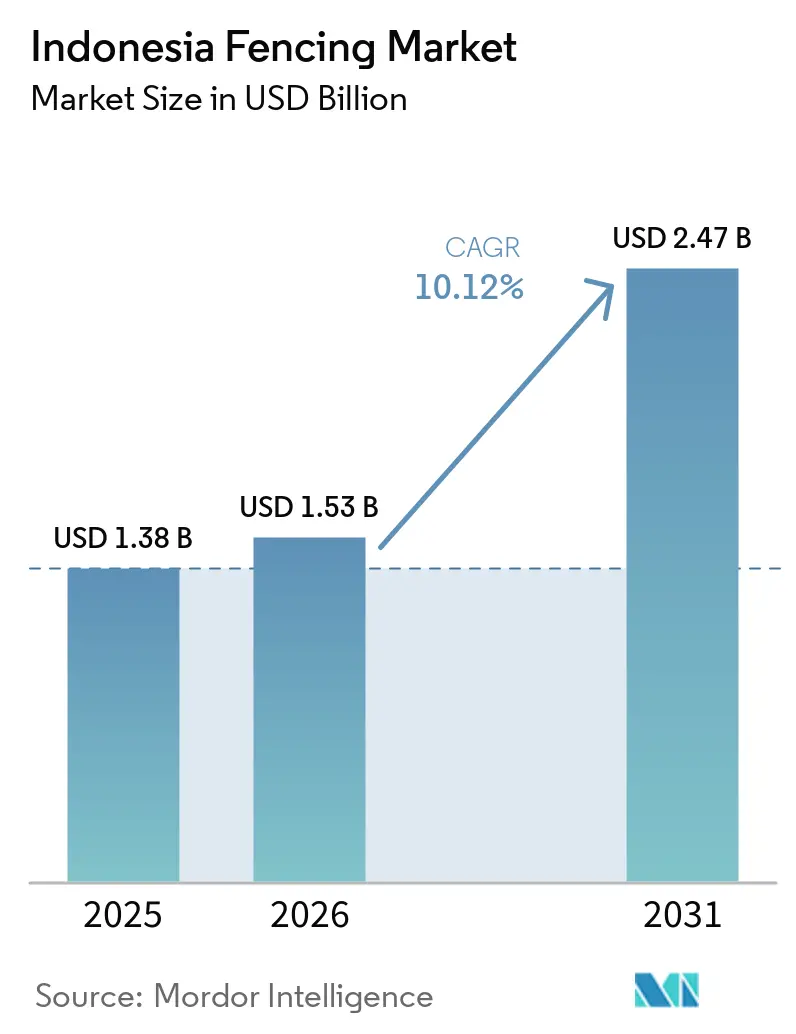

| Base Year Market Size (2025) | USD 1.38 Billion |

| Market Size (2026) | USD 1.53 Billion |

| Market Size (2031) | USD 2.47 Billion |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

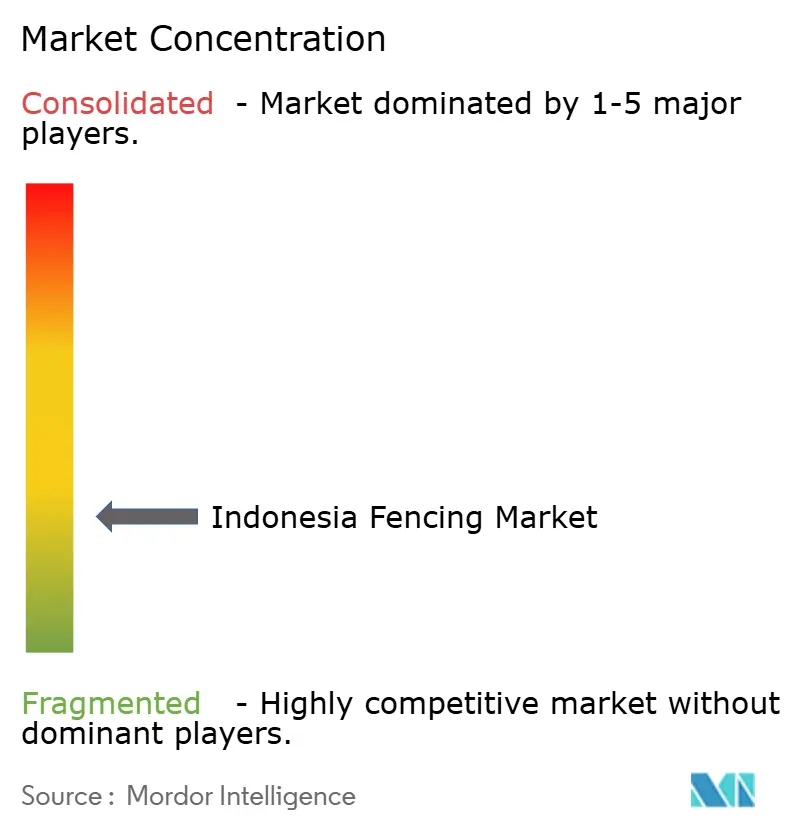

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Fencing Market Analysis by Mordor Intelligence

The Indonesia Fencing Market size is expected to increase from USD 1.38 billion in 2025 to USD 1.53 billion in 2026 and reach USD 2.47 billion by 2031, growing at a CAGR of 10.12% over 2026-2031. The Indonesia fencing market is expanding faster than the country’s nominal GDP because demand is being tied to residential construction, industrial estate build-out, border infrastructure, and plantation security needs rather than to short project cycles alone. Combined residential and industrial estate investment rose 19.2% year on year to IDR 75 trillion (USD 4.7 billion) in H1 2025, and that supports a deeper pipeline for perimeter security and land demarcation products across multiple provinces. Procurement standards are also becoming more formal, as TKDN and SNI-linked purchasing rules are lifting the importance of certified manufacturing capacity and platform visibility in public projects. Residential gated living, industrial estate expansion, border hardening, and plantation perimeter requirements are together widening the addressable demand base for the Indonesia fencing market, while suppliers with broader product lines are better placed to capture multi-specification orders. At the same time, steel and wire input swings still create margin pressure on fixed-price contracts, which means scale, compliance capability, and sourcing discipline remain central to long-term performance.

Key Report Takeaways

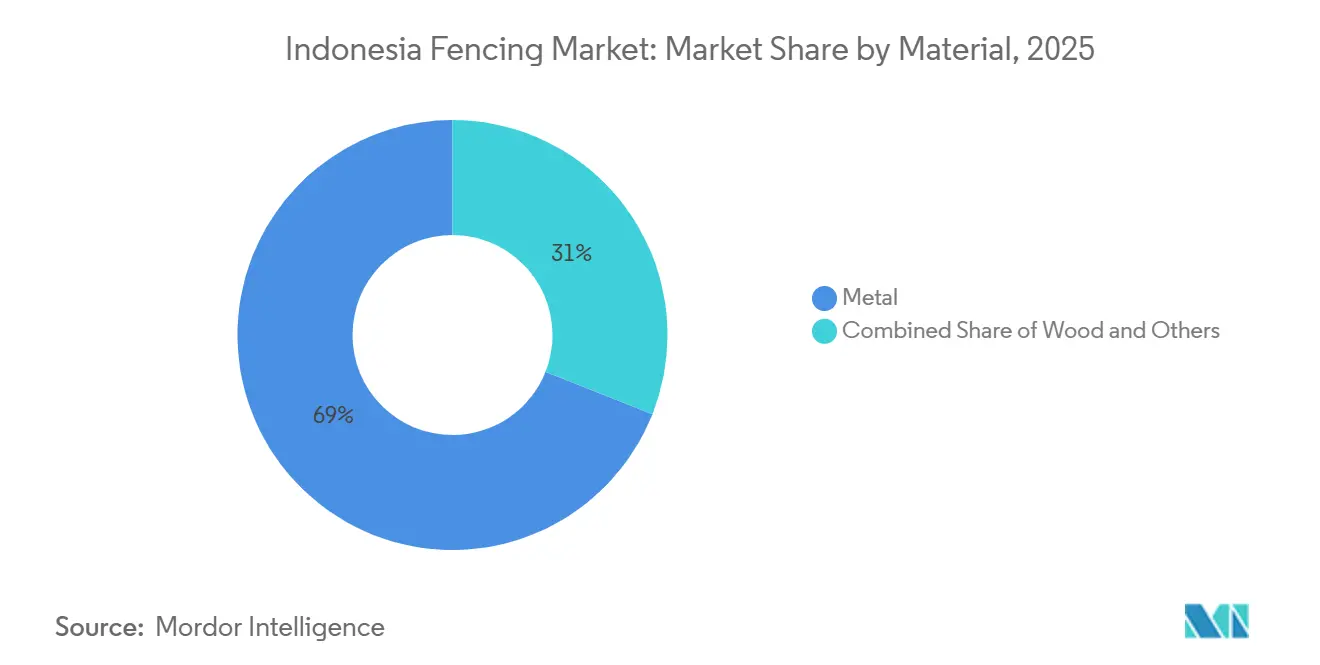

- By material, metal held 69% of Indonesia fencing market share in 2025, while plastic and composite is forecast to expand at 13% CAGR through 2031.

- By end-user, residential accounted for 24% of demand in 2025, while military and border security is projected to grow at 11.7% CAGR through 2031.

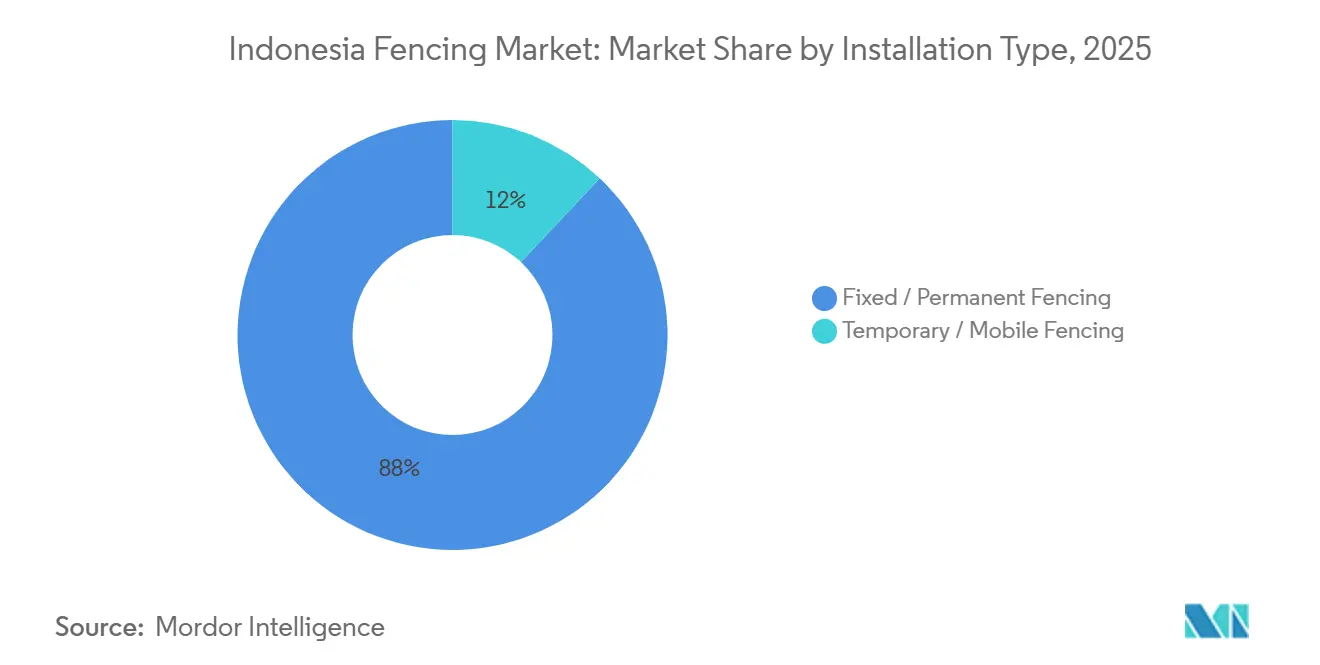

- By installation type, fixed and permanent fencing accounted for 88% share of the Indonesia fencing market size in 2025, while temporary and mobile fencing is forecast to expand at 13.6% CAGR through 2031.

- By installation channel, professional contractors held 70% share in 2025, while online and modular kit channels are projected to grow at 12% CAGR through 2031.

- By geography, Java accounted for 44% share of the Indonesia fencing market size in 2025, while Kalimantan is forecast to expand at 12.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Fencing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential and Gated-Community Security Demand | +3.0% | Java, Bali & Nusa Tenggara, Sumatra | Short term (≤ 2 years) |

| Industrial-Estate and Logistics-Park Expansion | +2.8% | Java, Riau Islands | Medium term (2-4 years) |

| Agriculture and Plantation Perimeter Protection | +1.5% | Sumatra, Kalimantan | Medium term (2-4 years) |

| Border-Post and Critical-Asset Security Upgrades | +1.2% | Kalimantan, Papua, East Nusa Tenggara | Long term (≥ 4 years) |

| SNI and TKDN Compliance Favoring Organized Suppliers | +0.9% | National, with early gains in Java and Riau Islands | Short term (≤ 2 years) |

| Human-Wildlife Conflict Mitigation Fencing | +0.6% | Sumatra, Kalimantan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Residential and Gated-Community Security Demand

Upper-middle and luxury housing expansion in Greater Jakarta kept residential perimeter demand active through 2025, and the landed housing sales rate shows that completed units were being absorbed rather than left idle. That matters because occupied communities usually move faster from basic boundary works to upgraded perimeter systems with gates, access control, and better finishes. The residential side of the market is also broadening beyond Jakarta into Surabaya, Medan, and Makassar corridors, which reduces dependence on one city for new orders. Developers are increasingly using different fencing specifications for outer and inner zones, and that creates larger order baskets for suppliers that can deliver several product grades in one contract. This pattern supports better pricing for organized manufacturers because design flexibility, coating quality, and installation support matter more when buyers are paying for long-term neighborhood security.

Industrial-Estate and Logistics-Park Expansion

Industrial estates remain one of the strongest project channels in the Indonesia fencing market because each site requires perimeter control, internal zoning, checkpoint separation, and recurring replacement over its operating life. Indonesia had 175 operational industrial estates at the end of 2025, with a cumulative investment of IDR 6,744.6 trillion (USD 419 billion), and estate investment growth of 9.3% year on year. The KITB complex in Batanghari is also committing IDR 22 trillion (USD 1.4 billion) toward a 4,300-hectare expansion, which widens the addressable scope for fencing well beyond initial perimeter works. Permenperin No. 26/2025 adds another layer, as higher estate accreditation depends heavily on infrastructure quality, giving developers a direct reason to upgrade fencing specifications rather than choosing the lowest-cost option. A large share of estates also remains outside OVNI designation, so perimeter hardening and security upgrades still represent an underserved pipeline across the industrial segment.

Agriculture and Plantation Perimeter Protection

Agriculture and plantation perimeter protection is emerging as a key growth driver for the fencing market, with the strongest demand concentrated in Sumatra and Kalimantan. Demand is supported by the scale of plantation activity, particularly in Sumatra, where palm oil cultivation reached 8.78 million hectares in 2025 and continues to require extensive boundary control and site-protection infrastructure. In these regions, fencing is used not only for land demarcation but also to reduce asset intrusion, crop loss, and operational disruption across large plantation estates.

The need for organized perimeter systems is also becoming more structured as plantation operators increasingly address human-wildlife conflict in sensitive cultivation zones. This was reflected in Aceh, where 82 kilometers of non-lethal electric fencing were deployed in April 2025 under the Sumatra Elephant Conservation Program, demonstrating a practical model that can support wider adoption across similar agricultural and conservation corridors.

Border-Post and Critical-Asset Security Upgrades

Border security is becoming a more specialized growth engine for the Indonesia fencing market because physical barriers are increasingly being paired with surveillance and monitoring systems. Indonesia had 15 operational land-border crossing points and 8 more in West Kalimantan and Papua were awaiting presidential instruction for Phase 3 deployment. BNPP’s Smart Border 2026 program links video analytics, drone monitoring, and satellite communications with fence infrastructure at priority crossings, thereby enhancing the value of sensor-ready, corrosion-resistant systems[1]Badan Nasional Pengelola Perbatasan, “Smart Border 2026 Programme Launch,” BNPP, bnpp.go.id. This changes fencing from a passive barrier into part of a wider security stack, and that supports better margins for suppliers that can meet higher technical specifications. The same procurement logic applies to energy and utility assets, where coastal humidity, salt exposure, and asset sensitivity make tested and compliant systems more important than low initial pricing.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel and Wire Price Volatility | -1.4% | National, most acute in outer islands | Short term (≤ 2 years) |

| Fragmented Local Competition and Price-Led Tendering | -1.1% | National, concentrated in Java and Sumatra | Medium term (2-4 years) |

| Archipelagic Freight and Installation-Cost Asymmetry | -0.9% | Maluku, Papua, Sulawesi, outer Kalimantan | Long term (≥ 4 years) |

| Coastal Permitting and Sensitive-Site Deployment Hurdles | -0.5% | Coastal Java, Bali & Nusa Tenggara, Papua coast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Steel and Wire Price Volatility

Steel input swings are a clear drag on the Indonesia fencing market because many suppliers still operate on fixed-price contracts while their material costs move with regional and global steel conditions. Wire rod FOB Indonesia moved from USD 480 per metric ton in September 2025 to USD 462 in November 2025, which looked softer on paper but did not remove underlying cost uncertainty for downstream buyers. In 2025, wire import volumes reached 143,662 metric tons, while national production capacity stood at 1,054,498 metric tons a year across 21 producers, showing that volume balance and pricing power do not always move together. Export volumes also fell sharply from 2021 to 2025, which suggests more supply was being redirected into the domestic market at prices still exposed to outside steel movements. Smaller manufacturers remain the most exposed because they usually lack long-term supply agreements and have less room to absorb cost spikes during tender execution.

Fragmented Local Competition and Price-Led Tendering

Price-led competition slows quality upgrading across the Indonesia fencing market because a large number of CV-level fabricators still compete mainly on low upfront pricing. In many tenders below strict TKDN thresholds, buyers continue to focus on unit price per linear meter rather than on lifecycle performance, gauge quality, or coating thickness. That makes it harder for organized suppliers with SNI systems and formal quality processes to defend higher prices, even when their products offer longer service life and lower maintenance needs. Specification ambiguity in e-procurement also remains a problem because lower-gauge steel or thinner coating can still enter bids when tender language is broad. The result is slower migration toward value-added perimeter systems, even though demand is clearly moving in that direction across residential, industrial, and security-linked applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Steel Dominates, Composites Gain Ground

Metal accounted for 69% of Indonesia fencing market share in 2025, making it the clear anchor material across residential, industrial, agricultural, and public infrastructure uses. Galvanized steel chain-link, BRC welded mesh, and barbed wire together formed the core of this volume because they are familiar to buyers, widely available, and easier to specify across standard project types. Within metal, steel remains the main volume driver, while aluminum serves narrower applications in coastal and high-humidity environments where corrosion risk makes the premium more acceptable. Wood remains present in rural boundary work, but its share is limited by maintenance needs and sustainability pressure. Concrete fencing stays relevant in privacy walls and highway-related installations, though it is a specialist rather than a broad-based category.

Upstream investment supports that metal-led structure. PT Beka Wire commissioned a new IDR 300 billion (USD 18.3 million) facility in Subang, targeting an output of 36,000 metric tons a year, demonstrating confidence in sustained domestic wire and mesh demand. At the same time, the material mix is not standing still. Plastic and composite materials are forecast to grow at a 13% CAGR through 2031 due to their low weight, salt-spray resistance, and ease of transport, which improve their fit for plantation zones and outer-island projects. UV-stabilized polyethylene mesh is starting to replace steel in uses where replacement cost and field life matter more than headline purchase price. The current standards framework still lacks a dedicated composite fencing product standard, and that creates short-term specification ambiguity while giving first movers room to shape future adoption.

By End-User: Residential Leads, Security Segments Accelerate

Residential users represented 24% of total demand in 2025, so the largest block of the Indonesia fencing market still comes from homes, clusters, and gated communities rather than from a single institutional buyer group. This reflects suburban growth and the cultural preference for secure enclosed living across major urban corridors. Agriculture and plantation demand also remains important because boundary fencing, site control, and wildlife-mitigation installations create large linear-meter requirements across broad land parcels. Government and public infrastructure projects add large contract visibility through formal tenders, while industrial and logistics sites continue to specify galvanized panels and electrified perimeter systems for operational security. Mining and energy projects are also adding demand for nickel processing and resource-linked zones, where asset protection is a procurement priority.

Military and border security is the fastest-growing end-user segment, with a 11.7% CAGR through 2031, reflecting the shift from simple barriers to security-integrated perimeter systems. BNPP’s Smart Border 2026 program is a major factor because it links physical fencing to monitoring architecture at priority border locations.Transportation infrastructure provides another recurring stream because airport and rail sites require repeated inspection, repair, and controlled boundary works as networks expand. Commercial and institutional demand is smaller in share, yet it is widening with the growth of logistics hubs and data-related infrastructure in secondary corridors. This broad end-user mix gives the market more resilience because weakness in one buyer group is less likely to stop total demand growth.

By Installation Type: Permanent Structures Anchor Revenue, Temporary Fencing Surges

Fixed and permanent fencing accounted for 88% share of the Indonesia fencing market size in 2025, which shows how deeply demand is still tied to long-life capital projects. Large industrial estates, government compounds, public infrastructure projects, and plantation boundaries usually specify systems that can be amortized over many years. That leads buyers toward galvanized welded mesh, chain-link panels, and cast concrete post systems that are designed for durability and low replacement frequency. It also supports long-duration supplier relationships because once a manufacturer is specified for an estate or public project, follow-on orders often continue through extensions, repairs, or adjacent phase work. This makes the permanent category structurally stable even when project-start timing shifts from one quarter to another.

Temporary and mobile fencing, however, is the fastest-growing installation type at 13.6% CAGR through 2031, and it is gaining strength from IKN construction, toll-road development, and rail expansion activity. Contractors are using site-boundary barriers, road-work delineation systems, and crowd-control products more frequently because project sequencing now depends more on phased site management and safety compliance. The purchase logic is different from permanent fencing because temporary units are treated more as recurring operational spend than as one-time capital assets. That change improves order frequency and helps niche manufacturers build steadier short-cycle demand. Lightweight modular steel panels and interlocking plastic barriers also suit outer-island deployment better because they are easier to move, store, and reinstall across changing project sites.

By Installation Channel: Contractors Hold Share, Digital Channels Erode It

Professional contractors dominated with 70% share in 2025, and that keeps the contractor route at the center of commercial activity in the Indonesia fencing market. The reason is straightforward because many industrial, government, and infrastructure buyers still prefer integrated supply-and-install contracts with one accountable counterparty. Contractors also support higher average order values by bundling engineering, installation, post-installation service, and warranty obligations into a single procurement package. This structure benefits certified manufacturers that already have preferred-supplier ties with large construction and engineering firms. It also makes the formal channel hard to displace in projects where technical scope, liability, and site coordination are complex.

Online and modular kit channels are still smaller, but they are forecast to grow at a 12% CAGR through 2031 and are starting to reshape demand for smaller residential and self-build projects. E-commerce platforms are making standardized mesh rolls, modular panels, and simple gate systems easier to compare and purchase in cities such as Medan, Semarang, and Banjarmasin. For buyers, that reduces search time and makes small-format fencing more accessible. For manufacturers, it creates a direct customer-acquisition route that complements contractor networks rather than replacing them. Informal fabricators still matter in rural and low-cost areas, yet digital listings, specification sheets, and installer referrals are gradually pulling part of this demand toward more visible branded offerings.

Geography Analysis

Java accounted for 44% of Indonesia fencing market share in 2025, and it remains the commercial center because it concentrates industrial estates, dense residential corridors, and government facilities in one geography. Investment in Java-based residential and industrial estate projects reached IDR 75 trillion (USD 4.7 billion) in H1 2025, maintaining near-term order visibility for both fabricators and installation partners. Premium gated-community developments in Banten, West Java, and East Java are pushing specifications upward from basic chain-link to powder-coated welded mesh and more integrated security layouts. Procurement in Java is also more formal than in most outer-island markets, so SNI and TKDN enforcement tends to be more consistent and that favors organized producers. Sumatra complements this profile because plantation boundary demand and wildlife-conflict corridors create long linear-meter volumes, while port and industrial nodes add more structured perimeter work.

Indonesia fencing market demand in Kalimantan is projected to grow at 12.3% CAGR through 2031, making it the fastest-growing geography in the report. This growth stems from two demand engines operating simultaneously: IKN Nusantara development and border-security expansion. As of May 2026, 26 of 28 Phase 2 IKN work packages were under contract, and the total Phase 2 construction value stood at IDR 20 trillion (USD 1.2 billion)[2]ANTARA News, “PLBN Phase 3 West Kalimantan and Papua,” ANTARA, antaranews.com. West Kalimantan is also receiving accelerated attention through BNPP’s Phase 3 border-crossing development, with Temajuk in Sambas highlighted for faster execution. Sulawesi is growing for a different reason because nickel-smelting and industrial estate activity in Morowali and Konawe keep demand tied to high-value operational asset protection.

Bali and Nusa Tenggara serve a more design-led niche where decorative and ornamental fencing for hospitality and resort properties supports better margins than pure commodity steel products. Maluku and Papua remain smaller in value, yet they carry strategic importance because border facilities, LNG assets, and agricultural expansion create highly targeted perimeter demand. Installed costs in these provinces are higher because freight, labor mobilization, and archipelagic logistics all raise the effective price of every fencing system delivered to site. BNPP allocated IDR 86 billion, which was USD 5.2 million, for border operations in 2026, and part of that supports perimeter-related works in eastern province. That means the smallest regional markets still matter for suppliers that can manage outer-island distribution and compliance-heavy security contracts.

Competitive Landscape

The Indonesia fencing market remains moderately fragmented because organized domestic manufacturers compete alongside a wide field of CV-level fabricators across Java and other established demand centers. Organized players have an edge in commercial and public projects because SNI-linked quality systems, TKDN alignment, and e-Katalog visibility raise the entry bar for informal operators. Smaller fabricators still stay active in residential and agricultural mid-market demand where price sensitivity is higher and product differentiation is lower. This split creates a two-track market structure, with certified suppliers strongest in specification-led tenders and informal players more visible in low-cost local jobs. Competitive intensity is therefore real, but consolidation pressure is rising as procurement channels become more formal.

The leading strategy pattern in the Indonesia fencing market is moving beyond commodity chain-link toward broader system portfolios, deeper compliance positioning, and expansion into outer-island security work. PT Bevananda Mustika is a strong example because it holds 26 brand patents and 3 product patents, opened a new Cikarang factory in 2025, and completed the installation of a corrosion-resistant sensor-ready BEVA Chainlink system at Pertamina Hulu Rokan in January 2026[3]PT Bevananda Mustika, “BEVA Minideploy Pilot With Polri,” Bevananda, bevananda.com. PT Bevananda also piloted the BEVA Minideploy rapid-deployment modular barrier with the National Police in September 2025, which shows how suppliers are linking physical fencing to tactical and security-response use cases. PT Halarag Baja Utama follows a different but related path through certification-led positioning, using SNI, TKDN, and ISO 9001:2015 credentials to improve tender readiness. These moves show that product range, certification status, and project references now matter more than simple volume presence.

White-space opportunities remain strongest in smart perimeter systems, composite and polymer fencing for coastal and plantation settings, and rapid-deployment modular barriers for construction, emergency response, and law-enforcement use. Platform-enabled direct-to-consumer kits are another area to watch because self-build buyers in secondary cities are becoming easier to reach through e-commerce and installer networks. Technology is now a practical differentiator rather than a marketing layer because buyers in industrial and border settings increasingly want fencing that can work with video, sensors, and real-time monitoring. As procurement rules tighten and technical requirements rise, organized producers with manufacturing depth and documented compliance are likely to capture a larger share of the higher-value portion of demand.

Indonesia Fencing Industry Leaders

PT Bevananda Mustika

PT Halarag Baja Utama

PT Sidokumpul Raya

PT Givro Multi Teknik Perkasa

PT Utama Pagar Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Indonesia's basic metal sector attracted IDR 64.9 trillion (approximately USD 4 billion) in investment during Q1 2026, reflecting upstream confidence in sustained demand from construction, fencing, and structural steel applications across the country's infrastructure pipeline.

- April 2026: The Indonesian government allocated IDR 4 trillion (approximately USD 244 million) toward safety upgrades at 1,800 railway level-crossings, a programme that incorporates trackside and right-of-way fencing across Java, Sumatra, and Kalimantan rail networks and generates multi-year fencing procurement contracts for compliant suppliers.

- April 2026: Land clearing commenced for the 3.2-hectare Nusantara Police Complex at IKN, initiating perimeter security and fencing procurement for one of the capital relocation project's key law-enforcement facilities and signaling the transition from civil works to operational infrastructure phasing at IKN.

- March 2026: BNPP accelerated development of the Temajuk PLBN in Sambas, West Kalimantan, the most remote land-border crossing on the Kalimantan-Malaysia frontier, with physical perimeter and security fencing forming an integral component of the facility's Phase 3 completion timeline.

Indonesia Fencing Market Report Scope

The Indonesia Fencing Market is Segmented by Material (Metal, Wood, Plastic & Composite, Concrete), End-User (Residential, Agriculture & Plantation, and More), Installation Type (Fixed / Permanent Fencing, Temporary / Mobile Fencing), Installation Channel (Professional Contractor, Others – Fabricators, DIY / Modular Kits), and Region (Java, Sumatra, Kalimantan, Sulawesi, and More). Market Forecasts are in Value (USD).

| Metal | Steel |

| Aluminum | |

| Wood | |

| Plastic & Composite | |

| Concrete |

| Residential |

| Agriculture & Plantation |

| Government & Public Infrastructure |

| Military & Border Security |

| Industrial & Logistics |

| Mining & Energy |

| Transportation Infrastructure |

| Commercial & Institutional |

| Fixed / Permanent Fencing |

| Temporary / Mobile Fencing |

| Professional Contractor |

| Others – Fabricators, DIY / Modular Kits |

| Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Bali & Nusa Tenggara |

| Maluku & Papua |

| By Material | Metal | Steel |

| Aluminum | ||

| Wood | ||

| Plastic & Composite | ||

| Concrete | ||

| By End-User | Residential | |

| Agriculture & Plantation | ||

| Government & Public Infrastructure | ||

| Military & Border Security | ||

| Industrial & Logistics | ||

| Mining & Energy | ||

| Transportation Infrastructure | ||

| Commercial & Institutional | ||

| By Installation Type | Fixed / Permanent Fencing | |

| Temporary / Mobile Fencing | ||

| By Installation Channel | Professional Contractor | |

| Others – Fabricators, DIY / Modular Kits | ||

| By Region | Java | |

| Sumatra | ||

| Kalimantan | ||

| Sulawesi | ||

| Bali & Nusa Tenggara | ||

| Maluku & Papua |

Key Questions Answered in the Report

What is the current outlook for fencing demand in Indonesia?

The Indonesia fencing market stands at USD 1.53 billion in 2026 and is projected to reach USD 2.47 billion by 2031 at a 10.1% CAGR, supported by residential, industrial, and border-security demand.

Which material category leads sales in this space?

Metal led with 69% share in 2025 because galvanized steel chain-link, welded mesh, and barbed wire remain the standard choice across most residential, industrial, and agricultural uses.

Which end-user group is expanding the fastest?

Military and border security is projected to grow at 11.7% CAGR through 2031, helped by PLBN expansion and the Smart Border 2026 program.

Why is Kalimantan the fastest-growing region?

Kalimantan is projected to grow at 12.3% CAGR through 2031 because IKN Nusantara development and border-crossing expansion are creating a multi-year project pipeline in the same geography.

Page last updated on: