Saudi Arabia Fencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

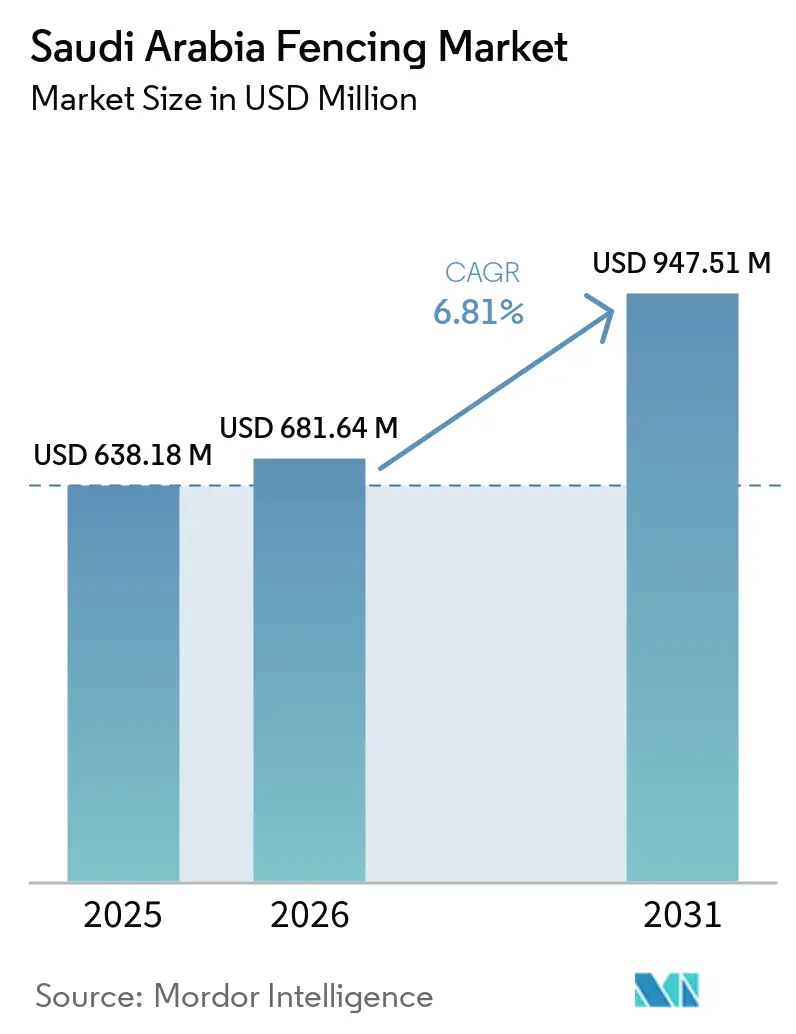

| Base Year Market Size (2025) | USD 638.18 Million |

| Market Size (2026) | USD 681.64 Million |

| Market Size (2031) | USD 947.51 Million |

| Growth Rate (2026 - 2031) | 6.81% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Fencing Market Analysis by Mordor Intelligence

The Saudi Arabia Fencing Market size is projected to expand from USD 638.18 million in 2025 and USD 681.64 million in 2026 to USD 947.51 million by 2031, registering a CAGR of 6.81% between 2026 to 2031.

The market is expanding because perimeter systems are now closely tied to infrastructure delivery, industrial security compliance, residential community planning, and protected-area management, rather than a single, narrow construction niche. Demand is also supported by the way large projects move from early land control and construction exclusion zones into utility boundaries, residential edges, access control points, and final permanent enclosures, which keeps procurement active across several project stages. Oil, gas, and utility sites continue to treat fencing as a required capital item because the High Commission for Industrial Security (HCIS) specifications define perimeter requirements for hydrocarbon facilities, providing the Saudi Arabia fencing market with a stable institutional base. The residential side adds a second layer of demand as planned communities, villa districts, and mixed-use schemes require plot boundaries, privacy fencing, and controlled entry systems. At the same time, conservation and border applications further broaden the end-use base. Competition remains moderate rather than highly concentrated because certified local suppliers have an advantage in regulated projects. Yet, input cost swings and execution delays still affect pricing discipline and delivery schedules across the Saudi Arabia fencing market.

Key Report Takeaways

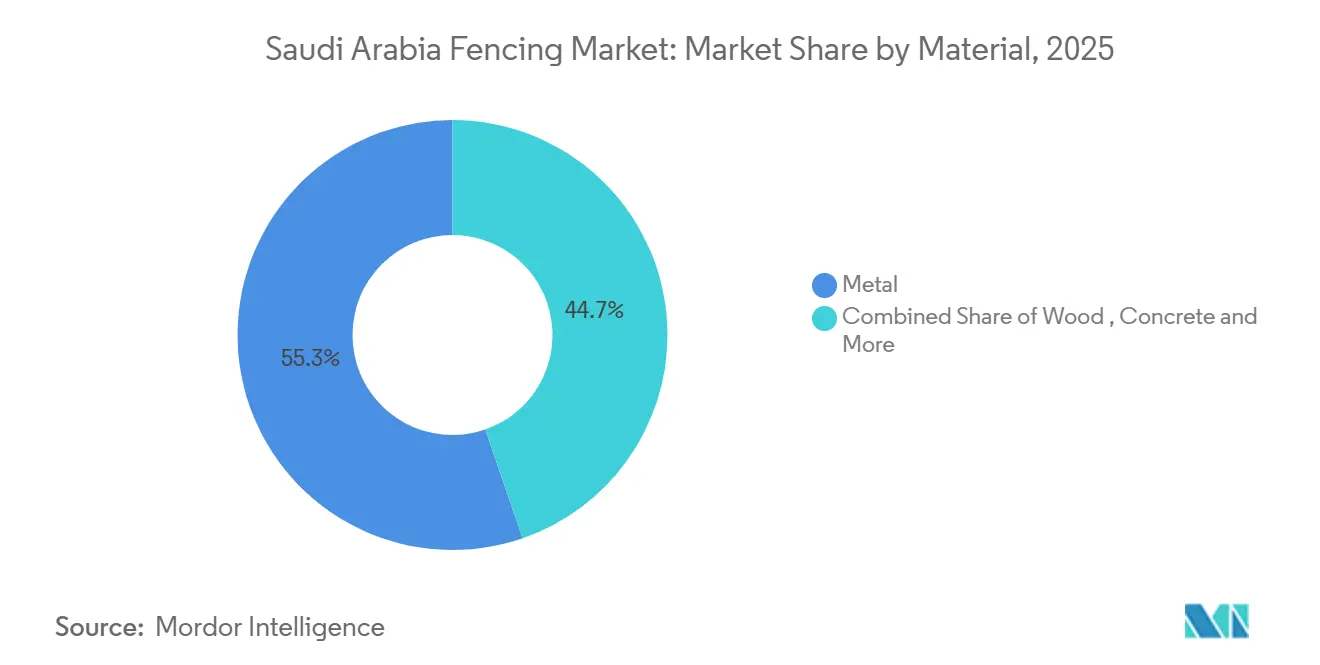

- By material, metal led with 55.3% of revenue in 2025, and metal is also forecast to expand at a 7.65% CAGR through 2031.

- By end-user, government held 22.1% of the Saudi Arabia fencing market share in 2025, while petroleum and chemicals recorded the highest projected CAGR at 7.91% through 2031.

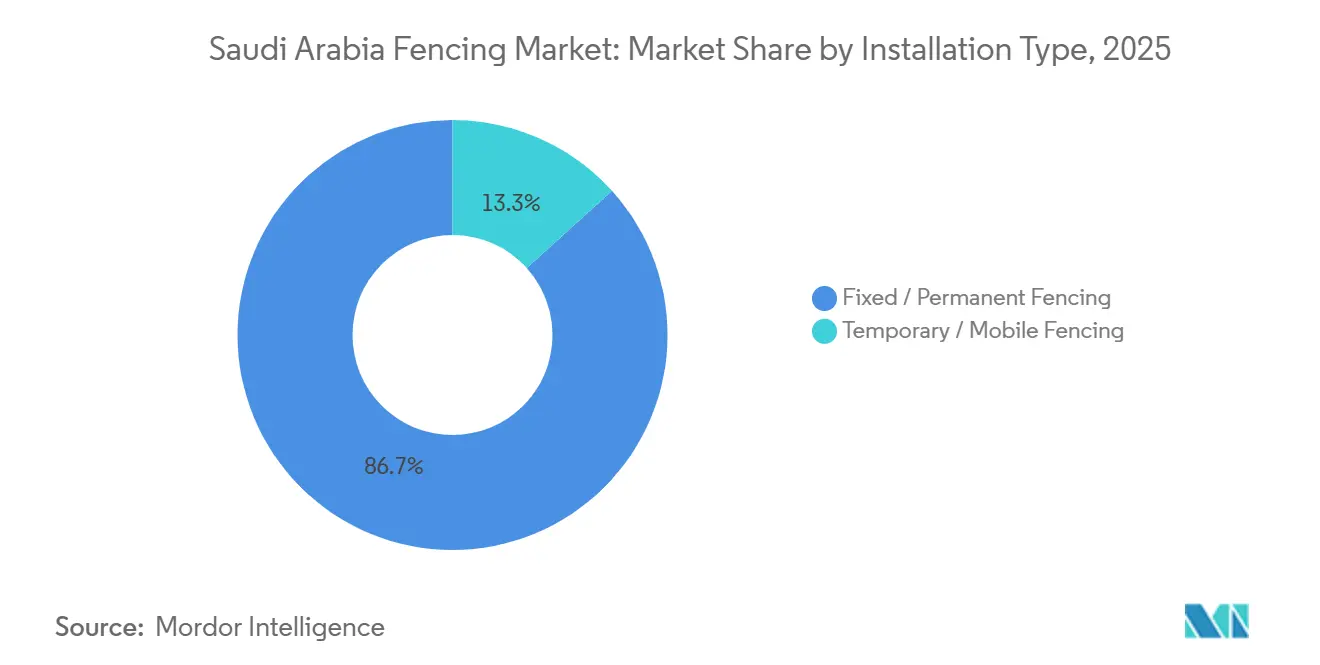

- By installation type, fixed or permanent systems accounted for 86.7% of the Saudi Arabia fencing market size in 2025, while temporary or mobile systems are advancing at a 7.33% CAGR through 2031.

- By installation channel, professional contractors captured 71.2% share in 2025, and the same channel is projected to grow at a 7.29% CAGR through 2031.

- By city, Riyadh held 39.8% share in 2025, while the Dammam Metropolitan Area is forecast to post the fastest growth at a 7.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Fencing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Mega Projects Driving Fencing Demand | +2.5% | National, including Riyadh, NEOM, Red Sea Corridor, Qiddiya, and Eastern Region | Medium term (2-4 years) |

| Oil, Gas, and Utility Infrastructure Supporting Perimeter Protection Adoption | +1.5% | Eastern Region, including Jubail, Dammam, and Al-Ahsa | Long term (≥ 4 years) |

| Border Security Infrastructure Increasing Demand for High-Security Systems | +1.2% | Northern and Southern borders | Long term (≥ 4 years) |

| Rising Residential Compounds and Gated Communities Increasing Privacy and Security Demand | +1.0% | National, including Riyadh, Jeddah, Makkah, and Dammam | Medium term (2-4 years) |

| Wildlife and Desert Conservation Initiatives Driving Protected-Area Fencing | +0.4% | AlUla, NEOM Reserve, Taif, and Eastern Region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Mega Projects: The Architectural Engine of Fencing Demand

Vision 2030 remains the broadest structural demand driver for the Saudi Arabia fencing market because the program spreads construction activity across new cities, tourism zones, logistics corridors, utility systems, and public assets rather than concentrating spending in one location. This matters because fencing demand is not limited to a single project milestone, and each major development typically requires early construction exclusion barriers, contractor safety partitions, utility boundary systems, access-control lines, and final permanent enclosures as the site matures. The same project can therefore generate repeat orders over many years, giving the Saudi Arabia fencing market greater continuity than categories tied only to finishing materials or short-cycle fit-out work. Large developments around Riyadh, NEOM, the Red Sea coast, Diriyah, and Qiddiya also increase the need for specialized products, including anti-climb systems, decorative urban barriers, acoustic-compatible boundary formats, and modular temporary solutions that can be relocated as work fronts move. This staged procurement pattern benefits both domestic manufacturers and contractor networks by spreading demand across fabrication, installation, maintenance, and replacement work rather than relying on a single one-time sale. It also creates room for suppliers that can serve both heavy-duty institutional perimeters and aesthetically controlled community fencing, broadening commercial opportunities in the Saudi Arabia fencing market.

Oil, Gas, and Utility Infrastructure: Compliance-Mandated Perimeter Investment

Oil, gas, and utility projects support the Saudi Arabia fencing market because perimeter protection at these sites is governed by HCIS rules, turning fencing from an optional purchase into a required part of capital spending[1]A-1 Fence Arabia, “Industrial Security Fence Solutions and HCIS Requirements,” A-1 Fence Arabia, a1fencearabia.com. The regulatory model is important because it defines perimeter layout, clear zones, and patrol access requirements, so project owners cannot easily defer this spending even when they delay other non-core works. This gives the Saudi Arabia fencing market a strong base in the Eastern Region, where hydrocarbon processing, support infrastructure, and industrial utility assets continue to drive demand for high-specification steel systems, secure gates, crash-rated components, and certified installation services. Saudi Aramco’s local supply chain spending reached 70% in 2025, and its 2030 target remains 75% under the In-Kingdom Total Value Add, or IKTVA, program, which strengthens the position of Saudi-registered manufacturers that can meet compliance and localization expectations. The King Salman Energy Park, or SPARK, between Dammam and Al-Ahsa, adds another industrial perimeter demand center, and it deepens the role of fencing in new energy, supply-chain, and support facilities linked to the broader industrial base[2]U.S. Department of State, “King Salman Energy Park Project Summary,” U.S. Department of State, state.gov. Because these projects need both heavy-duty perimeter structures and supporting contractor execution, oil, gas, and utility investment continues to anchor the upper-value end of the Saudi Arabia fencing market.

Border Security Infrastructure: From Physical Barriers to Integrated Detection Systems

Border security supports the Saudi Arabia fencing market through a procurement model that is more complex and higher value than standard commercial perimeter work. Frontier systems do not rely solely on fencing; they typically combine physical barriers with surveillance cables, sensors, monitoring equipment, and control infrastructure, thereby increasing the technical complexity and installation value of each secured stretch. This pushes demand toward suppliers that can either provide integrated systems directly or work alongside defense, security, and specialist engineering partners, thereby lowering entry barriers for smaller, unqualified fabricators. The operating environment also differs from that of standard private developments because border projects require high durability, controlled-access design, and dependable maintenance performance across remote terrain and harsh climate conditions. These factors make border applications one of the most specialized parts of the Saudi Arabia fencing market, and they keep demand concentrated in government and military-related channels even when civilian construction cycles soften. As a result, border security not only adds volume, but it also supports product upgrading and higher specification standards across the Saudi Arabia fencing market.

Residential Compounds: ESG-Linked Capital Fuelling Community Perimeter Demand

Residential compounds are becoming a steady demand source for the Saudi Arabia fencing market because planned communities use fencing at several levels, including site boundaries, internal plot divisions, landscaping protection, pedestrian routing, and entry control. This creates a repeatable procurement pattern, especially in new villa districts and mixed-use communities where perimeter design is part of the original master plan rather than an afterthought. ROSHN Group’s ALMANAR launch in Makkah during February 2025 shows the scale of integrated housing schemes now moving through the pipeline, with fencing embedded in community identity, security layout, and open-space management. The material mix in these projects is also widening, because developers increasingly balance security, maintenance, appearance, corrosion resistance, and installation speed when choosing between steel, aluminum, and composite systems. This supports a broader product range in the Saudi Arabia fencing market, where basic boundary products continue to sell. Still, more finished and visually controlled formats are gaining relevance in upper-middle- and premium-housing projects. Residential growth, therefore, adds not only unit demand, but also product diversification and stronger recurring work for local installers serving the Saudi Arabia fencing market.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Steel, Aluminum, and Polyvinyl Chloride Prices Increasing Product Costs | -0.8% | National | Medium term (2-4 years) |

| Rising Middle East War Tensions Impacting Investor Confidence and Project Timelines | -0.6% | Southern border and Red Sea corridor | Short term (≤ 2 years) |

| Extreme Desert Climate Increasing Maintenance and Durability Requirements | -0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Steel, Aluminum, and Polyvinyl Chloride Price Volatility: Margin Risk in Fixed-Price Contracts

Commodity price volatility remains the sharpest operating restraint for the Saudi Arabia fencing market because many suppliers bid on contracts before raw material conditions settle and then carry the pricing risk through delivery. The pressure is strongest in government, infrastructure, and institutional jobs where tender competition is tight and contract revisions are not always easy to negotiate after award. By February 2025, iron ore prices had fallen 18%, coking coal 44%, and scrap steel 19% year over year, while 81 antidumping investigations were launched by 19 governments in 2024, which shows that headline price declines did not remove policy-driven uncertainty from steel trade conditions[3]Organization for Economic Co-operation and Development, “Steel Outlook 2025,” OECD, oecd.org. Aluminum also remained elevated at USD 2,580 per metric ton in 2025 and is forecast to reach USD 2,600 per metric ton in 2026, which affects the cost base of residential, decorative, and corrosion-resistant product lines. This combination narrows margins for smaller fabricators, especially when they cannot hedge raw material exposure or pass through higher input costs to buyers with fixed budgets. Price swings, therefore, do not eliminate demand in the Saudi Arabia fencing market, but they do weaken profitability, delay quoting decisions, and favor larger suppliers with stronger procurement discipline.

Middle East War Tensions: A Geopolitical Overhang on Southern Corridor Execution

Regional tensions continue to weigh on the Saudi Arabia fencing market, as projects near the Yemeni frontier and the Red Sea corridor face greater schedule risk than those in inland urban centers. The effect is not uniform across the country. Still, it can influence investor confidence, site mobilization timing, insurance costs, logistics planning, and the availability of imported specialist components for higher-end perimeter systems. In practice, this means some projects move forward with added caution, longer lead-time assumptions, and more conservative contracting structures, especially when delivery depends on coordinated imports, cross-border shipping, or sensitive public infrastructure approvals. The restraint is therefore less about the long-run need for fencing and more about near-term execution pacing, because the same security backdrop can delay some investments while reinforcing demand for high-security installations in exposed areas. This creates an uneven pattern inside the Saudi Arabia fencing market, where civilian confidence may soften in certain corridors even as security-led procurement remains firm. The result is a mixed operating environment that requires suppliers to balance opportunities in defensive applications with slower decision-making in more commercially sensitive projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Metal Maintains Structural Dominance Across Security and Aesthetic Applications

Metal held 55.3% of the Saudi Arabia fencing market in 2025, leading across industrial, government, residential, and mixed-use applications. Its dominance reflects strength, availability, design flexibility, and familiarity among stakeholders, especially for projects requiring strict security or durability. Steel dominates due to its suitability for industrial corridors, utility assets, military sites, and regulated energy facilities. Aluminum is gaining traction for its corrosion resistance and cleaner finish, supporting gated communities, coastal developments, and urban boundaries. Metal is projected to grow fastest, with the segment expected to expand at a 7.65% CAGR from 2026 to 2031, solidifying its role in the current and future market.

Metal's strength in the Saudi Arabia fencing industry is supported by supplier capability and compliance-readiness. Hitech Fence has built its position through local manufacturing and compliance with HCIS and Saudi Aramco Inspection Services (SAIS) requirements, building buyer trust in regulated projects. End users in energy, infrastructure, and public works require assurance on fabrication standards, installation quality, and long-term performance. Wood remains limited to niche landscaping and hospitality uses, while plastic and composite systems are gaining traction where maintenance trade-offs outweigh structural strength. Concrete boundary walls serve sites prioritizing permanence and mass security but lack the versatility of fabricated metal systems. As environmental, social, and governance-linked real estate financing influences material choices, metal is expected to remain dominant, with higher-end aluminum and hybrid systems capturing a larger share of premium residential and urban design projects.

By End-User: Government Anchors Volume While Petroleum Sector Accelerates

Government buyers held 22.1% of the Saudi Arabia fencing market in 2025, making the public sector the largest end-user across municipalities, public institutions, utility facilities, and state-backed development sites. Government procurement involves large contracts, phased delivery, and specification-driven installations, ensuring stable order flow for approved suppliers. The public sector spans urban development, civic infrastructure, border management, and utility protection, broadening the market base. Petroleum and chemicals are the fastest-growing segment, with a 7.91% CAGR projected from 2026 to 2031, driven by the expansion of energy and industrial sites requiring high-security perimeters. Government anchors volume, while petroleum and chemicals drive high-specification demand.

This end-user mix benefits suppliers capable of working across public and industrial settings without altering compliance models. HCIS requirements ensure that fencing remains essential in hydrocarbon facilities, while Saudi Aramco’s IKTVA initiative strengthens domestic suppliers' compliance with standards. Military and defense projects, though smaller in volume, carry high contract values due to specialized security needs. Residential demand grows steadily in planned communities and villa developments, while agriculture, mining, and energy infrastructure add depth. The Saudi Arabia fencing market benefits from a diverse buyer base, reducing reliance on any single procurement channel. Over the forecast period, the balance between public infrastructure volume and industrial security intensity will define end-user demand.

By Installation Type: Permanent Systems Anchor the Market, Mobile Fencing Accelerates

Fixed or permanent fencing accounted for 86.7% of the Saudi Arabia fencing market in 2025, driven by its alignment with long-life infrastructure, industrial assets, public facilities, and established residential developments. Permanent systems meet the lifecycle needs of projects that require durability, greater protection, and minimal relocation. Government campuses, utility installations, and regulated industrial zones typically specify permanent fencing, keeping this segment dominant. Temporary fencing, however, is projected to grow at a 7.33% CAGR from 2026 to 2031, driven by giga-project construction that requires flexible site management during long build cycles. This dual demand supports both permanent and temporary fencing needs.

Suppliers are adapting to this shift. Hitech Fence’s focus on NEOM-related projects highlights the growing use of temporary fencing in industrial and renewable energy corridors. Temporary fencing now includes modular systems that can be reconfigured and maintained over extended schedules. Procurement is also shifting toward hire-or-lease models, introducing a service element beyond one-time sales. Over time, many temporary installations will transition into permanent demand as sites move from construction to operation, ensuring continuity between the two types.

By Installation Channel: Contractor Networks Dominate, Modular Formats Gain Relevance

Professional contractors held 71.2% of the Saudi Arabia fencing market share in 2025, making them the dominant installation channel for high-value projects. This dominance is tied to project complexity, as regulated industrial sites, public infrastructure, and large community developments require certified execution, site management, and documented quality. Contractors are also the fastest-growing channel, with a 7.29% CAGR projected through 2031, reflecting the market's shift toward larger, technically controlled projects. DIY activity remains common in smaller residential and light commercial cases but does not significantly impact the core value pool, leaving contractors central to converting product demand into installed revenue.

Other channels, including independent fabricators, small installers, and modular-kit assemblers, serve buyers with simpler needs or tighter budgets. A-1 Fence Arabia’s Unico Prima series, launched at Saudi Infrastructure 2025, highlights the development of modular systems for easier installation in municipal and residential applications. While standardization may lower installation barriers in some projects, the upper-value tiers of the market are likely to remain contractor-led due to compliance, warranty, and site complexity requirements. Over time, modular formats may add flexibility, but certified contractors are expected to retain control over the most valuable segments.

Geography Analysis

Riyadh accounted for 39.8% of the Saudi Arabia fencing market in 2025, maintaining leadership due to the concentration of government projects, planned communities, and major development corridors. The city benefits from a strong network of approved contractors, institutional buyers, and suppliers capable of delivering both security-grade perimeter systems and residential fencing solutions. Demand spans public infrastructure, utilities, gated housing, mixed-use developments, and construction enclosures, while the concentration of compliance-sensitive projects keeps certified vendors highly active. As a result, Riyadh strongly influences installation standards, procurement practices, and contractor participation across the market.

Jeddah represents a different but important demand center, driven by port infrastructure, coastal housing, tourism projects, and private urban developments. Demand is more closely linked to trade activity and urban expansion than to central government concentration. Visibility from projects such as Jeddah Tower strengthens supplier credibility in nearby commercial and infrastructure opportunities. Meanwhile, the Dammam Metropolitan Area is projected to be the fastest-growing city segment, with a 7.85% CAGR from 2026 to 2031, supported by industrial expansion, logistics activity, housing growth, and utility-linked development in the Eastern Region. Demand there comes from HCIS-compliant facilities, warehouses, transport hubs, and community developments, highlighting the diversified regional drivers of the Saudi Arabia fencing market.

The Rest of Saudi Arabia segment includes protected landscapes, mining zones, agricultural regions, border corridors, and NEOM-linked construction sites. Although these applications may appear fragmented individually, together they create a stable demand across multiple fencing formats. Conservation projects such as AlUla and the Sharaan Nature Reserve support environmental boundary requirements, while agricultural fencing, mining perimeters, and border security systems add further volume outside the major metros. NEOM-related developments also contribute significantly, with temporary construction barriers expected to evolve into permanent utility and community perimeters over time. This broader geographic spread creates multiple regional growth engines rather than reliance on Riyadh alone.

Competitive Landscape

The Saudi Arabia fencing market remains fragmented, with domestic manufacturers, security-focused fabricators, project contractors, and international technology partners competing across different niches. No single company dominates the market, and competitive advantage is driven more by certification capability, local manufacturing presence, installation execution, and access to approved vendor networks than by price alone. Companies such as Al Kuhaimi Metal Industries, A-1 Fence Arabia, and Hitech Fence are well-positioned in regulated institutional segments due to strong credibility with industrial, utility, and public-sector clients. This creates a two-tier structure where certified local players dominate high-value regulated projects. At the same time, smaller fabricators and import-led suppliers compete more actively in residential and light commercial applications.

Competition is also evolving through product specialization and localization strategies. A-1 Fence Arabia used Saudi Infrastructure 2025 to introduce the Unico Prima urban perimeter series, signaling expansion beyond industrial security into municipal and planned community projects. Hitech Fence showcased steel fencing systems, automation solutions, and sustainability-focused offerings at Big 5 Construct Saudi 2025, reflecting a strategy centered on technical breadth and project visibility. Meanwhile, Al Kuhaimi Group highlighted anti-personnel fences, crash-rated barriers, road blockers, and bullet-resistant systems at Intersec Saudi Arabia 2024, reinforcing its security-led positioning in defense, infrastructure, and energy sectors. These developments indicate that competition increasingly depends on system integration, product differentiation, and localized execution rather than fabrication capacity alone.

Localization policy is another major competitive driver. Saudi Aramco’s IKTVA program, which targets 75% local content by 2030, encourages procurement from suppliers able to demonstrate domestic value creation. This strengthens the position of local manufacturers and approved contractors on regulated, politically sensitive projects, where imported generic products face structural disadvantages despite lower upfront pricing. At the same time, opportunities remain in temporary fencing rental, modular community fencing, and integrated perimeter detection systems, where no clear market leader has emerged. However, rising certification expenses and raw material volatility may push smaller players toward subcontracting and partnership models. Overall, the market remains competitive enough to prevent dominance by a single supplier, while still rewarding certified local capability with a premium position.

Saudi Arabia Fencing Industry Leaders

BRC Industrial Limited

A-1 Fence Arabia Company

Hitech Fence and Steel Saudi Arabia

Golden Fence Mechanical Company

Desert Fence Company Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: A-1 Fence Arabia exhibited at Saudi Infrastructure 2025 at the Riyadh International Convention and Exhibition Center, from September 15 to 17, 2025, launching the Unico Prima urban perimeter series designed for Vision 2030-aligned residential and municipal developments.

- February 2025: Hitech Fence participated in Big 5 Construct Saudi Arabia 2025 at the Riyadh Front Exhibition Center, from February 15 to 18 and February 24 to 27, showcasing steel fencing systems, automation solutions, and sustainable materials, with the company active as a fencing supplier for the Jeddah Tower and UCC Saudi Arabia projects.

- January 2025: The National Center for Wildlife released 134 endangered species, including 100 Arabian oryxes, 20 Arabian gazelles, 8 Nubian ibexes, and 6 Idmi gazelles, into the NEOM Nature Reserve. This program depends on maintained boundary fencing to reduce livestock incursion across the reserve perimeter.

Saudi Arabia Fencing Market Report Scope

| Metal | Steel |

| Aluminium | |

| Wood | |

| Plastic & Composite | |

| Concrete | |

| Other Materials |

| Residential |

| Agricultural |

| Military & Defense |

| Government |

| Mining |

| Petroleum & Chemicals |

| Energy & Power |

| Other End-Users |

| Fixed / Permanent Fencing |

| Temporary / Mobile Fencing |

| Professional Contractor |

| Others – Fabricators, DIY / Modular Kits |

| Riyadh |

| Jeddah |

| DMA (Dammam Metropolitan Area) |

| Rest of Saudi Arabia |

| By Material | Metal | Steel |

| Aluminium | ||

| Wood | ||

| Plastic & Composite | ||

| Concrete | ||

| Other Materials | ||

| By End-User | Residential | |

| Agricultural | ||

| Military & Defense | ||

| Government | ||

| Mining | ||

| Petroleum & Chemicals | ||

| Energy & Power | ||

| Other End-Users | ||

| By Installation Type | Fixed / Permanent Fencing | |

| Temporary / Mobile Fencing | ||

| By Installation Channel | Professional Contractor | |

| Others – Fabricators, DIY / Modular Kits | ||

| By City | Riyadh | |

| Jeddah | ||

| DMA (Dammam Metropolitan Area) | ||

| Rest of Saudi Arabia |

Key Questions Answered in the Report

What is the projected value of the Saudi Arabia fencing market by 2031?

The Saudi Arabia fencing market is projected to reach USD 947.5 million by 2031, up from USD 681.6 million in 2026, at a 6.81% CAGR from 2026 to 2031.

Which material category leads the fencing demand in Saudi Arabia?

Metal leads the category with a 55.3% share in 2025, supported by steel demand in industrial security uses and growing aluminum use in residential and urban projects.

Why are petroleum and chemicals the fastest-growing end-user segment?

Petroleum and chemicals are projected to grow at a 7.91% CAGR, as fencing is required for perimeter compliance at hydrocarbon and downstream facilities under HCIS standards.

Why do professional contractors dominate installation activity?

Professional contractors held 71.2% share in 2025 because large projects often require certified execution, approved vendor status, and documented compliance for regulated sites.

Which city offers the strongest near-term growth opportunity?

Riyadh remains the largest city segment with 39.8% share in 2025, while the Dammam Metropolitan Area offers the fastest growth at a 7.85% CAGR through 2031.

What are the main risks affecting suppliers and installers?

The main risks are steel and aluminum price volatility, regional tension that can slow project timelines, and harsh desert conditions that raise maintenance and durability requirements.

Page last updated on: