Germany Fencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.16 Billion |

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 1.53 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

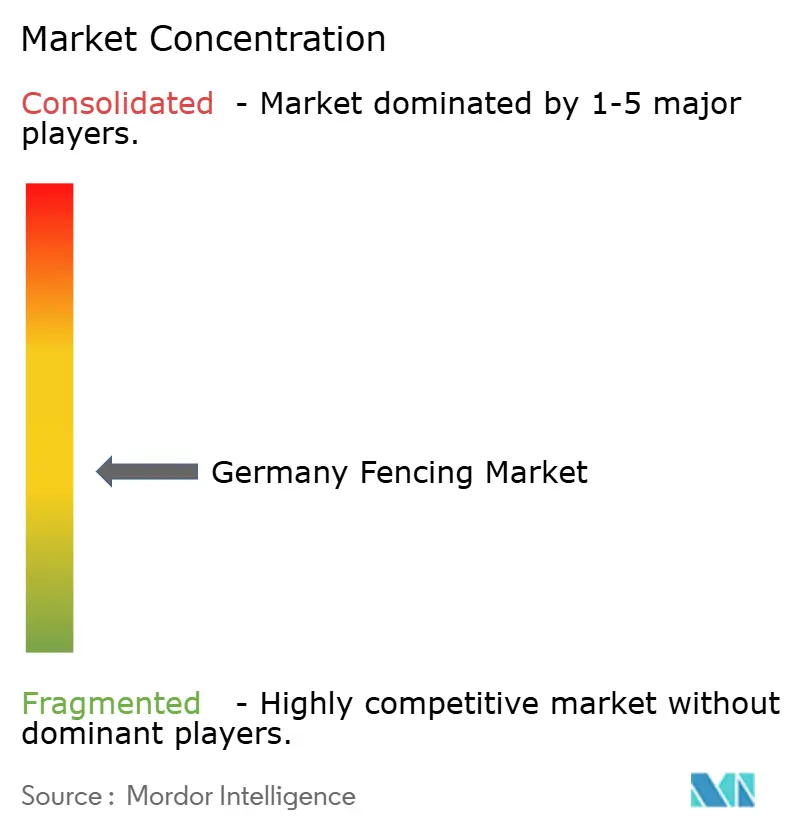

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Fencing Market Analysis by Mordor Intelligence

The Germany Fencing Market size is expected to grow from USD 1.16 billion in 2025 to USD 1.22 billion in 2026 and is forecast to reach USD 1.53 billion by 2031 at 4.63% CAGR over 2026-2031.

The Germany fencing market is benefiting from the return of growth in German construction during 2026, with civil engineering activity strengthening after a long period of contraction and with federal infrastructure spending lifting demand for site barriers, access control systems, and permanent perimeter solutions around transport and public works projects. Security-led procurement is also shaping the German fencing market, as the KRITIS framework now places perimeter protection within a formal resilience agenda for critical facilities, elevating the role of certified, specification-led products in energy, transport, and public administration projects. A second layer of demand is driven by the move toward technology-linked perimeter systems, where detection, monitoring, and high-security performance are becoming part of the value proposition rather than optional extras, thereby shifting spending toward higher-value, permanent installations. At the same time, the Germany fencing market still faces cost pressure from steel supply tightness in Europe and strong price competition from local unorganized suppliers in standard fencing categories, which keeps margin conditions uneven across the supplier base. The result is a market where growth is being supported by construction, compliance, and site security, while supplier strategies increasingly separate commodity products from more specialized perimeter systems.

Key Report Takeaways

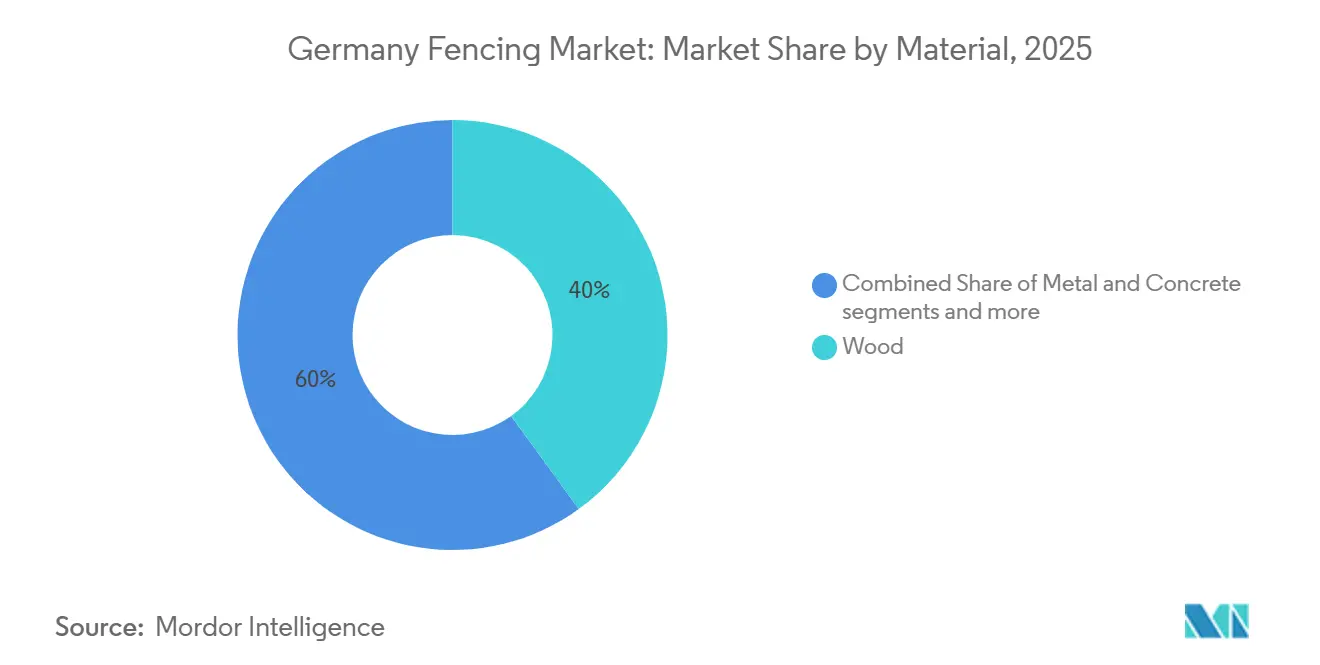

- By material, wood led with a 40% share in 2025, while metal is forecast to expand at a 5.6% CAGR through 2031 in the Germany fencing market.

- By end-user, residential held a 38% share of the Germany fencing market share in 2025, while energy and power recorded the highest projected CAGR at 6.3% through 2031.

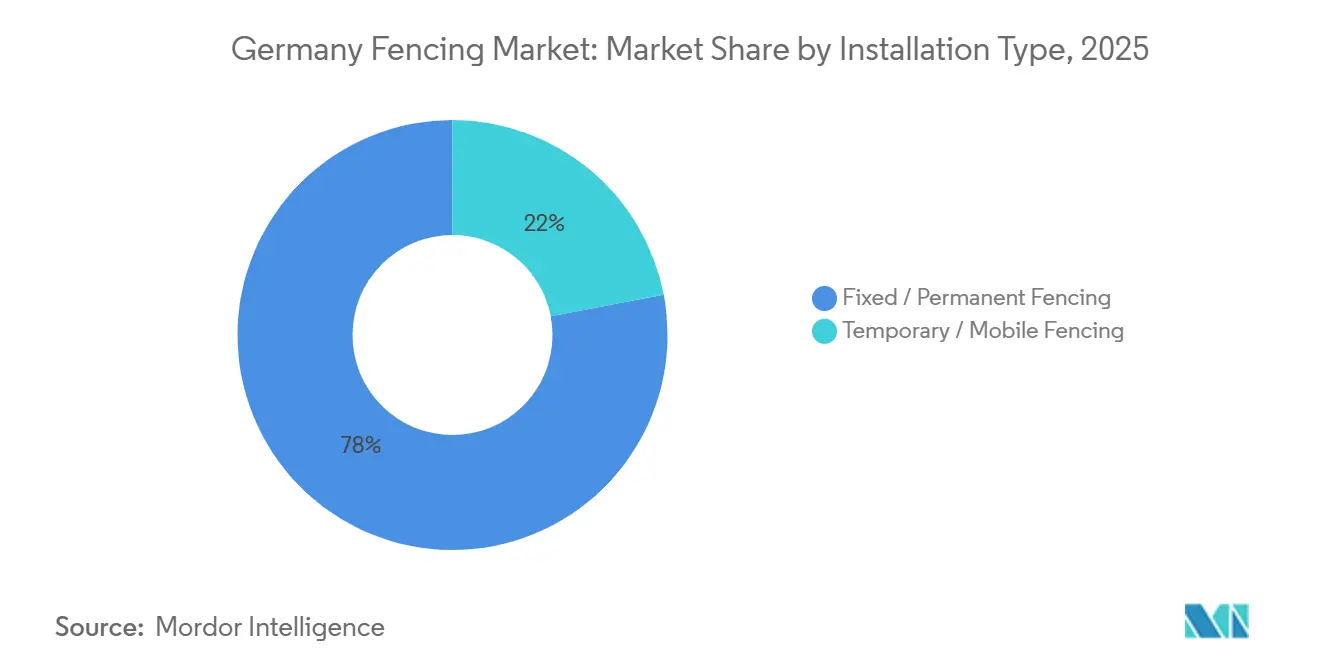

- By installation type, fixed / permanent fencing accounted for 78% share of the Germany fencing market size in 2025, while temporary / mobile fencing is advancing at a 5.9% CAGR through 2031.

- By installation channel, professional contractors held a 70% share in 2025, while others (fabricators, DIY / modular kits) are expected to grow at a 5.4% CAGR through 2031.

- By geography, Berlin held 25% of the Germany fencing market size in 2025, while Munich is projected to grow at a 5.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Fencing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Construction and Infrastructure Development | +1.4% | National, with early momentum in Berlin, Hamburg, Frankfurt, and Munich | Short term (≤ 2 years) |

| Rising Demand for Security and Perimeter Protection | +1.2% | Germany-wide, with stronger relevance in Berlin, Frankfurt, and Munich | Medium term (2-4 years) |

| Stringent Safety and Regulatory Standards | +0.8% | National, led by KRITIS and standards-led procurement | Medium term (2-4 years) |

| Increasing Adoption of Smart and Low-Maintenance Fencing Solutions | +0.7% | National, with stronger relevance in industrial and energy-linked regions | Medium term (2-4 years) |

| Increasing Agricultural Protection Needs Drive Demand for Farm and Livestock Fencing | +0.6% | Rural Bavaria, Lower Saxony, Baden-Württemberg, and Brandenburg | Long term (≥ 4 years) |

| Growing Preference for Sustainable and Recycled-Material Fencing | +0.3% | National, with earlier adoption in urban residential segments and publicly procured construction | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growth in Construction and Infrastructure Development

The Germany fencing market is closely tied to the construction cycle because every active project creates a need for temporary barriers during execution and permanent boundary systems at handover. German construction order intake grew 6.8% in real terms in 2025, which marked the first increase since 2021, and nominal orders reached EUR 113 billion (USD 129 billion), creating a broader base of live projects that require compliant fencing solutions. The German Institute for Economic Research (DIW Berlin) also expects overall construction volume to expand in 2026, with civil engineering showing the strongest momentum as infrastructure investment shifts to rail, road, and bridge work[1]Christian Danne, Martin Gornig, and Laura Pagenhardt, “Construction Industry Returns to Growth,” DIW Weekly Report, diw.de. Agricultural building permits also increased in the January to November 2025 period, which extends fencing demand into farm structures and rural perimeter projects alongside urban and commercial activity. The Germany fencing market benefits most where civil engineering and commercial work are improving faster than residential completions, because those project types carry larger and more specification-heavy perimeter needs.

Rising Demand for Security and Perimeter Protection

The Germany fencing market is seeing stronger demand from buyers that now treat perimeter protection as part of operational continuity rather than a simple boundary requirement. Germany’s security posture remained elevated after federal authorities extended border controls across all German land borders from September 2024, and the Bundespolizei recorded 83,572 unauthorized entries in 2024, which kept physical security a visible priority in public procurement and facility planning. This effect now extends beyond public facilities, as commercial users such as data centers and logistics operators are buying fencing systems with forced-entry resistance and vehicle-mitigation features rather than standard perimeter products. That shift improves pricing resilience in technical categories and supports vendors with certification depth, while basic mesh and low-spec products remain exposed to price competition. In the Germany fencing market, security demand is therefore widening the gap between performance-led suppliers and volume-led suppliers.

Stringent Safety and Regulatory Standards

The Germany fencing market is also being shaped by regulation because compliance now influences both product choice and installation practice across several end-user groups. The federal government’s KRITIS framework entered into force in March 2026 and identifies physical protection measures for designated critical facilities, which gives perimeter barriers a formal place in resilience planning for operators in energy, transport, healthcare, and related sectors. At the product level, German Institute for Standardization and European Norm (EN) standards continue to favor suppliers that can document material quality, coating performance, and safe use in both temporary and permanent applications, narrowing the room for uncertified, low-cost offers in complex tenders. This matters because large commercial and public buyers often need proof of specification compliance before installation begins, and that raises the role of professional contractors and accredited manufacturers. In the Germany fencing market, regulation is therefore acting less as a short-term shock and more as a structural filter that supports better-specified products over informal alternatives.

Increasing Adoption of Smart and Low-Maintenance Fencing Solutions

The Germany fencing market is moving toward systems that reduce maintenance needs and add detection or monitoring functions to the fence line. Fraunhofer FHR completed testing of its IDAS-PRO fence radar in June 2025 and is moving toward industrialization in 2026, indicating that perimeter infrastructure is increasingly linked to drone detection and broader site awareness for critical and industrial locations. On the product side, composite privacy infills, corrosion-resistant metal systems, and recycled-plastic mobile bases are gaining attention because buyers want longer service life and lower maintenance in labor-sensitive environments. This pattern matters because it changes procurement logic from upfront price to lifecycle performance, especially in commercial, public, and infrastructure settings. In the Germany fencing market, smart and low-maintenance options are therefore expanding the value pool even when overall volume growth stays moderate.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.5% | Global supply chains, with strong effect in Germany because of EU steel tightness | Medium term (2-4 years) |

| Competition from Unorganized Local Manufacturers is Affecting Pricing and Product Quality | -0.4% | Regional and semi-urban markets across Eastern and Southern Germany, particularly in cost-sensitive residential and agricultural fencing segments | Medium term (2–4 years) |

| Price Sensitivity among Rural and Small-Scale Buyers Limiting Premium Fencing Adoption | -0.3% | Rural Bavaria, Brandenburg, Mecklenburg-Vorpommern, and Saxony-Anhalt | Long term (≥ 4 years) |

| Shortage of Skilled Fencing Installation Labor | -0.1% | Urban and peri-urban construction zones in Berlin, Hamburg, Munich, and Frankfurt | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw Material Prices

The Germany fencing market remains exposed to input cost instability because steel wire products still sit at the center of many permanent security and industrial fencing systems. European Union (EU) steel supply conditions remained tight, with more than half of Europe’s primary steel production capacity idled since 2021, which kept upward pressure on prices and reduced manufacturers' flexibility in responding to cost-sensitive tenders[2]EUROMETAL, “Northern European Mills Keep Prices High for Steel Rebar, Wire Rod Amid Tight Supply,” EUROMETAL, eurometal.net . When input costs move higher, suppliers in mid-range categories are often unable to pass through the full increase without losing orders to smaller local competitors. That creates a difficult trade-off between margin protection and product quality, especially where buyers compare offers on upfront price rather than lifecycle performance. In the German fencing market, this restraint is most visible in welded mesh, basic agricultural systems, and standard metal products, where input inflation can quickly narrow already modest margins.

Competition from Unorganized Local Manufacturers is Affecting Pricing and Product Quality

Competition from unorganized local manufacturers continues to restrain growth in the Germany fencing market by intensifying price competition and limiting adoption of higher-value fencing solutions. Numerous small-scale regional fabricators and installers compete primarily on price, particularly in residential, agricultural, and small commercial projects where buyers are highly cost-sensitive. These players often offer basic wire mesh, chain-link, and metal fencing products at lower prices than organized manufacturers, reducing margins for established companies. The fragmented supplier base also creates inconsistencies in product quality, installation standards, and compliance with durability or security certifications. In several regional and semi-urban markets, end users prioritize upfront affordability over long-term performance, slowing penetration of premium fencing systems such as automated, high-security, corrosion-resistant, and aesthetically customized solutions. As a result, organized manufacturers face continued pressure on pricing and differentiation, especially in standard fencing categories over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Wood Leads While Metal Posts Superior Growth

Wood accounted for 40% of the Germany fencing market size in 2025, which kept it as the leading material category in the country. Its position rests on strong consumer acceptance in residential and agricultural settings, where buyers value familiar appearance, broad design choice, and ease of handling during installation. Germany also benefits from a large domestic timber base, which supports supply visibility and keeps wood relevant across garden fencing, paddock solutions, and farm boundaries.

In the Germany fencing market, that local supply advantage supports a wide mix of standard and premium products rather than a narrow low-cost niche. It also helps explain why wood remains established even as other materials gain share in higher-security or lower-maintenance uses. Species choice adds another layer to wood’s staying power, allowing buyers to choose between treated softwood and naturally durable hardwood options, depending on budget and service-life needs. Suppliers such as ROBINIO position Robinia-based products as offering long-term in-ground durability without chemical treatment, which aligns with a segment of German buyers who prefer a more natural specification. FSC-linked sourcing and sustainability messaging have also become more visible in garden and paddock procurement, which helps wood retain appeal where aesthetics and environmental criteria both matter. In the Germany fencing industry, wood therefore continues to serve as a practical and culturally familiar material rather than a declining legacy choice. The segment’s growth is slower than metal, but its installed base and broad use cases continue to anchor demand across the Germany fencing market.

Metal is the fastest-growing material segment, with the Germany fencing market size for metal projected to expand at a 5.6% CAGR between 2026 and 2031. Demand is strongest where sites require anti-climb performance, longer service life, or compatibility with access control and detection systems, making metal central to energy sites, transport facilities, critical infrastructure, and data center projects. Praesidiad and Betafence have expanded their portfolios to include certified high-security perimeter systems, reflecting this move toward performance-led procurement. Within the Germany fencing market, steel remains the main metal type because welded mesh, palisade formats, and rolled wire systems cover a wide range of industrial and public applications. Aluminum is also gaining ground in residential and light commercial applications, where lower weight and corrosion resistance support lifecycle value, even if the upfront cost is higher. Plastic and composite materials remain smaller than wood and metal, but they are building a firmer base in privacy fencing and modular residential systems. Composite infills and related systems appeal to buyers who want lower upkeep and a more uniform appearance across garden and boundary applications. Concrete remains a niche option for noise barriers and in selected infrastructure locations, while decorative materials play a limited but stable role in certain garden projects. The Germany fencing industry is therefore not shifting toward one replacement material, but toward a clearer material hierarchy shaped by aesthetics, upkeep, and security needs. That hierarchy keeps wood in the lead, but it gives metal the clearest path to outperformance through the forecast period in the Germany fencing market.

By End-User: Residential Anchors Demand While Energy & Power Accelerates

Residential held a 38% share of the Germany fencing market share in 2025, making it the largest end-user category. Germany’s large housing stock, strong preference for privacy in gardens and outdoor living areas, and broad retail access to fencing products all support this position. Housing-related activity also improved in parts of the pipeline in 2025, helping maintain demand for new boundary fencing, replacement panels, and modular privacy systems. In the Germany fencing market, residential demand is especially important because it spreads orders across material types, price points, and installation channels rather than concentrating demand in a few contract buyers. That makes the segment less dependent on a single project cycle and more tied to a broad base of household spending and small-contractor activity.

The segment also benefits from strong distribution coverage across home improvement and building supply channels, making product comparison and project planning easier for households. Hornbach and other retailers continue to expand natural wood and modular fencing options, which support replacement demand and the gradual move toward planned outdoor upgrades rather than purely functional boundary work. Residential buyers span both contractor-led and self-managed projects, which keeps volume flowing through multiple sales routes in the Germany fencing market. Even with uneven residential completions at the national level, the installed housing base keeps replacement and modernization demand active. This is why residential remains the structural anchor for the Germany fencing market even while faster growth is coming from other end-users.

Agricultural users form the next important demand layer because fencing is tied to livestock management, farm security, and land separation rather than purely visual boundaries. Veterinary and farm protection requirements continue to support multi-line installations and more complex layouts than earlier single-fence farm formats. That raises per-project meterage and makes fencing an operating need rather than a discretionary one. The Germany fencing market gains from this because farm orders often combine posts, mesh, gates, and electrified elements in a single purchase set. It also supports contractor demand in larger rural jobs where mechanized installation improves speed and consistency. The energy & power is the fastest-growing end-user segment at a 6.3% CAGR through 2031, which reflects the rising perimeter needs of renewable energy and utility sites in the Germany fencing market. These sites need protection for equipment, cable routes, transformer areas, and controlled access points, which increases the value of metal and high-security perimeter systems. Public-sector, military, and government facilities also provide a steady stream of specification-led projects as critical infrastructure resilience moves further into implementation. Mining, petroleum and chemicals, and other industrial buyers add baseline replacement demand, but the strongest acceleration is clearly within energy-linked projects. This mix means the Germany fencing market is no longer driven only by household and farm demand, because strategic infrastructure buyers are taking a larger role in the growth profile.

By Installation Type: Permanence Dominates, Mobility Gains Momentum

Fixed / permanent systems accounted for 78% of the Germany fencing market size in 2025, which shows how strongly the market is anchored in long-life installations. Residential garden fencing, permanent farm enclosures, industrial boundaries, and critical infrastructure perimeters all fall under this category, so its scale reflects both volume and a wide range of use cases. In the Germany fencing market, permanent systems also align with Germany’s planning culture because many installations need to meet local construction and property rules before work begins. That tends to favor formal specification, durable materials, and contractor involvement over improvised or short-life solutions. It also means that permanent fencing often captures the higher-value segment of the market, even as temporary fencing volumes rise during strong construction phases.

The security upgrade cycle further reinforces this pattern because fixed installations are the natural format for anti-climb mesh, palisade systems, integrated gates, and monitored perimeter layouts. Betafence’s portfolio focus on high-security permanent systems in 2026 fits this direction and shows where major suppliers see longer-term value in the Germany fencing market. Public infrastructure and critical facilities are especially important here because they need perimeter systems that combine intrusion delay, corrosion protection, and service reliability. For those buyers, temporary barriers may support a project phase, but permanent security remains the final procurement objective. This keeps fixed installations at the core of the Germany fencing market even as faster growth appears elsewhere.

Temporary / mobile fencing is the fastest-growing installation category and is projected to rise at a 5.9% CAGR through 2031. Construction order growth in 2025 widened the number of active sites that require compliant barriers for access control, public separation, and safe working areas, which directly supports mobile systems. Events, logistics yards, and temporary infrastructure work also support demand for easy-to-deploy perimeter products, especially where project timelines are short and reuse matters. In the Germany fencing market, this segment benefits from strong activity in commercial and civil engineering jobs rather than from long-term property investment alone. It also reflects a practical need for portable protection in an environment where work zones and public interface areas remain busy. Sustainability is becoming more visible in the temporary segment because contractors are paying closer attention to materials, handling efficiency, and emissions linked to site equipment. FenzFoot’s recycled plastic mobile fence bases had already been deployed across more than 18 million m² of German construction sites in 2026, which shows that reusable low-maintenance components are gaining a real installed base rather than staying a niche concept. That matters because large contractors increasingly want reusable products that are easier to transport and safer to manage on site. The Germany fencing market therefore shows an unusual split where permanent systems dominate total value, while mobile systems carry stronger growth momentum. This balance supports suppliers that can serve both short-cycle construction demand and longer-cycle perimeter security projects.

By Installation Channel: Professional Contractors Control the Market, Others (Fabricators, DIY / Modular Kits) Gain Traction

Professional contractors held 70% share of the Germany fencing market in 2025, which reflects the technical and procedural demands of many installations. Large agricultural layouts, permanent mesh systems, high-security perimeters, and most public-sector projects require proper site preparation, mechanized post setting, and documentation that household buyers or small fabricators typically do not provide. In the Germany fencing market, contractor strength also comes from procurement habits because municipalities, infrastructure buyers, and commercial operators often prefer approved installers with a known compliance record. This gives established regional contractors a durable role even when material supply is fragmented. It also means that labor capability remains as important as product availability in many higher-value jobs.

Contractors are especially central where projects involve coordination between fencing, gates, access points, and security hardware. KRITIS-linked projects and other critical-site installations reinforce this pattern because buyers need more than a fence line and often require a full perimeter package with traceable standards and performance claims. The Germany fencing industry therefore remains installation-led in much of its commercial and institutional business. Regional specialists retain an advantage through local service response and knowledge of municipal requirements, while multinationals rely on product depth and certification strength. This combination keeps the contractor channel dominant across the Germany fencing market.

Others (Fabricators, DIY / Modular Kits) is the fastest-growing channel, with a 5.4% CAGR expected through 2031, because residential and small-property buyers have better access to user-friendly systems than before. Retailers continue to widen the range of natural wood, modular privacy panels, and packaged installation formats that reduce the planning barrier for households. Digital tools are also making project design easier, which helps buyers visualize layouts before ordering and reduces reliance on a site visit for simple jobs. In the Germany fencing market, this does not remove the contractor role, but it does shift a larger share of smaller residential projects toward self-directed purchasing. The effect is strongest in privacy fencing, garden boundaries, and mid-tier replacement jobs where standardized kits are easier to install and compare. Fabricators and hybrid service models also support channel growth because many buyers want some planning help without handing over the full project to a contractor. That opens room for retail-linked installation partners and smaller workshops that can customize gates or panels while still using standardized system components. The Germany fencing market therefore shows a clear channel split between complex perimeter work that remains contractor-led and simpler home projects that are becoming easier to manage directly. Over time, this supports a broader customer base and more varied route-to-market models. It also helps explain why channel change in the Germany fencing market is gradual rather than disruptive.

Geography Analysis

Berlin held 25% share of the Germany fencing market in 2025, which made it the leading geographic segment. Its position reflects a dense urban base, a large concentration of government buildings, transport infrastructure, utilities, and commercial facilities that require both temporary and permanent perimeter systems. The city is also exposed to the near-term effects of KRITIS-linked compliance activity, as critical operators undertake registration and resilience planning steps that bring perimeter security into active procurement[3]Federal Government, “Critical Infrastructure Protection Strengthened,” Federal Government, bundesregierung.de. In the Germany fencing market, Berlin benefits from a mix of public-sector demand and urban development activity rather than from one dominant end-user alone. Frankfurt also holds an important position because its financial infrastructure, logistics footprint, and airport-linked facilities support steady demand for commercial and high-security fencing. Together, these two cities represent the part of the Germany fencing market where specification, security, and urban project density overlap most clearly.

Hamburg adds a different type of demand because its maritime and transport infrastructure supports ongoing perimeter requirements around port and logistics assets. These installations tend to favor durable metal systems, access-controlled boundaries, and contractor-led work because operating environments are more demanding than standard residential settings. The Germany fencing market also benefits in Hamburg from a steady base of industrial and utility-linked projects rather than sharp cyclical swings. That makes the city less dependent on one construction segment and more tied to long-running infrastructure and commercial operations. As a result, Hamburg remains a stable contributor to market demand even without leading national growth rates.

Munich is the fastest-growing geography and the Germany fencing market size in Munich is projected to expand at a 5.2% CAGR through 2031. Its growth comes from a strong commercial and residential pipeline, higher-value building activity in Bavaria, and continued demand from both urban and surrounding agricultural locations. In the Germany fencing market, Munich also benefits from the region’s broader economic base, which supports demand across homes, commercial premises, utilities, and farm operations rather than relying on one narrow project theme. This mix gives the city a broader growth foundation than a market that depends on only temporary construction fencing or only residential replacement. The result is faster expansion supported by multiple end-users and a regional economy that continues to favor planned property and infrastructure investment. Other regions such as North Rhine-Westphalia, Baden-Württemberg, Brandenburg, and Saxony-Anhalt account for the remaining share of the Germany fencing market. North Rhine-Westphalia is important for temporary fencing because it combines dense construction activity, large events, and a broad industrial base, while Baden-Württemberg adds a balanced mix of residential and industrial demand. Eastern states remain more price sensitive and continue to favor cost-effective agricultural and basic perimeter solutions over premium systems in many rural locations. This keeps regional growth patterns uneven, but it also shows that the Germany fencing market is not concentrated in one city cluster alone and still depends on a broad national base.

Competitive Landscape

Market concentration remains moderate in the Germany fencing market, as leading European manufacturers hold strong positions in premium, certified, and high-security fencing segments, while a large presence of domestic small and medium-sized enterprises (SMEs) and regional installers keeps the market fragmented across standard and price-sensitive applications. The German fencing market has a two-tier structure. Large European suppliers such as Betafence, Bekaert, and Heras compete through certification breadth, product range, and their ability to serve higher-value commercial and infrastructure projects, while German SMEs and regional installers compete through local service, shorter lead times, and price flexibility. This split is important because it shapes how value is distributed across the Germany fencing market, with multinational groups better placed in certified permanent systems and smaller firms more active in standard welded mesh, agricultural fencing, and local installation work. The competitive picture, therefore, mixes scale advantages at the top with fragmentation across the broader supplier base. That is why market behavior looks more concentrated in security-led categories than in volume-led standard fencing.

Recent strategic moves confirm that upper-tier suppliers are repositioning toward higher-value perimeter security. Garda Group completed the acquisition of Heras in April 2025, which strengthened its regional perimeter security presence and expanded cross-selling potential across Europe. Betafence discontinued its temporary and mobile fencing line in March 2026 and redirected attention to core perimeter security and permanent systems, which shows a deliberate move away from more standardized categories. Praesidiad also expanded its focus on critical infrastructure and data center solutions, which fits the wider move toward specification-led security offerings. In the Germany fencing market, these actions suggest that leading firms see the strongest value in integrated and certified perimeter systems rather than in high-volume basic products.

Technology is becoming a more visible competitive lever across the Germany fencing market. Fraunhofer FHR’s fence radar work points to a future where physical barriers and electronic detection are sold as part of one site protection concept rather than as separate layers. GRAEF Gruppe’s fence sensor launch shows that German providers are also bringing intrusion detection products into real project environments such as solar parks, logistics centers, and industrial sites. Certified high-security formats such as PALIFOR also strengthen supplier differentiation by setting a higher entry bar for tenders that need proven forced-entry performance. This means competition is no longer defined only by fence material and price per meter. It is increasingly shaped by compliance, system integration, service support, and the ability to serve critical sites in the Germany fencing market.

Germany Fencing Industry Leaders

Betafence

Heras

LEGI Group

Berlemann Torbau

BALU Tore GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The KRITIS-DachG, Critical Infrastructure Resilience Act, entered into force in Germany on March 12, 2026, requiring 1,700 critical facility operators across energy, transport, healthcare, and other sectors to implement physical security measures, explicitly including perimeter fencing, with registration by July 17, 2026, and compliance plans within 10 months of registration.

- March 2026: Betafence officially discontinued its temporary and mobile fencing product line, refocusing its German product offering on core perimeter security and permanent fencing systems, and naming ZND GmbH as a recommended alternative for temporary fencing needs.

- January 2026: The German Bundestag passed the KRITIS umbrella act on January 29, 2026, establishing the first nationwide cross-sector minimum standards for the physical protection of critical infrastructure, including structural barriers, detection systems, and access controls as mandatory resilience components.

- September 2025: Praesidiad appointed Benjamin Neumann as CEO, effective September 24, 2025, signaling a stronger strategic focus on energy, power, and critical infrastructure verticals for Betafence and Hesco globally.

Germany Fencing Market Report Scope

The Germany Fencing Market is Segmented by Material (Metal, Wood, Plastic & Composite, and more), End-User (Residential, Agricultural, Military & Defense, and more), Installation Type (Fixed / Permanent Fencing, Temporary / Mobile Fencing), Installation Channel (Professional Contractor and Others), and Geography (Berlin, Frankfurt, and more). The Market Forecasts are Provided in Terms of Value (USD).

| Metal | Steel |

| Aluminium | |

| Wood | |

| Plastic & Composite | |

| Concrete | |

| Other Materials |

| Residential |

| Agricultural |

| Military & Defense |

| Government |

| Mining |

| Petroleum & Chemicals |

| Energy & Power |

| Other End-Users |

| Fixed / Permanent Fencing |

| Temporary / Mobile Fencing |

| Professional Contractor |

| Others (Fabricators, DIY / Modular Kits) |

| Berlin |

| Frankfurt |

| Hamburg |

| Munich |

| Rest of Germany |

| By Material | Metal | Steel |

| Aluminium | ||

| Wood | ||

| Plastic & Composite | ||

| Concrete | ||

| Other Materials | ||

| By End-User | Residential | |

| Agricultural | ||

| Military & Defense | ||

| Government | ||

| Mining | ||

| Petroleum & Chemicals | ||

| Energy & Power | ||

| Other End-Users | ||

| By Installation Type | Fixed / Permanent Fencing | |

| Temporary / Mobile Fencing | ||

| By Installation Channel | Professional Contractor | |

| Others (Fabricators, DIY / Modular Kits) | ||

| By Geography | Berlin | |

| Frankfurt | ||

| Hamburg | ||

| Munich | ||

| Rest of Germany |

Key Questions Answered in the Report

What is the current value of the Germany fencing market?

The Germany fencing market was valued at USD 1.16 billion in 2025 and is forecast to reach USD 1.53 billion by 2031 at a 4.63% CAGR.

Which material leads fencing demand in Germany?

Wood led with a 40% share in 2025, supported by strong residential and agricultural use, while metal is growing faster at 5.6% CAGR through 2031.

Which end-user group is growing the fastest in Germany?

Energy & power is the fastest-growing end-user segment, with a projected 6.3% CAGR through 2031, driven by perimeter needs at utility and energy sites.

Why are permanent systems so dominant in Germany?

Fixed / permanent fencing accounted for 78% of demand in 2025 because residential, agricultural, industrial, and critical infrastructure sites all rely on long-life perimeter systems.

Page last updated on: