Ultrasonic Aspirator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

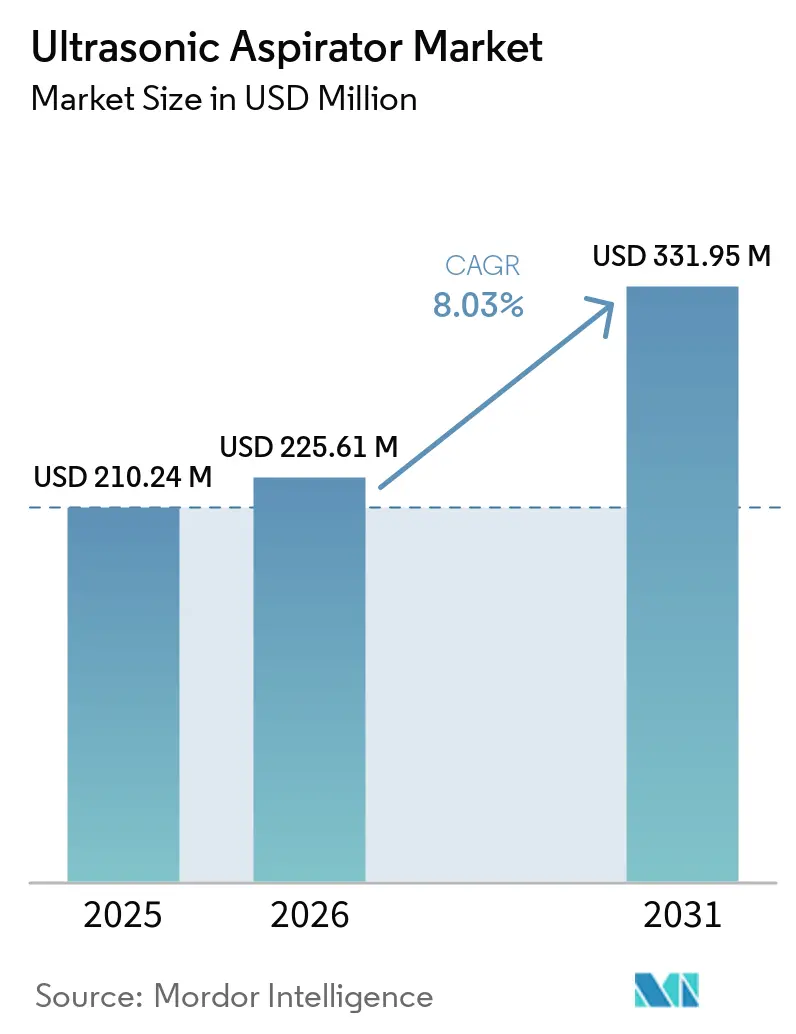

| Market Size (2026) | USD 225.61 Million |

| Market Size (2031) | USD 331.95 Million |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrasonic Aspirator Market Analysis by Mordor Intelligence

The Ultrasonic Aspirator Market size was valued at USD 210.24 million in 2025 and is estimated to grow from USD 225.61 million in 2026 to reach USD 331.95 million by 2031, at a CAGR of 8.03% during the forecast period (2026-2031).

The ultrasonic aspirator market is also benefiting from stronger clinical preference for precise soft-tissue fragmentation in areas where thermal spread and mechanical traction need to stay limited, and published 2025 clinical work continued to support that value in gynecological and spinal tumor procedures. The ultrasonic aspirator market is further supported by hospital and specialty center spending on high-acuity surgical equipment, especially where integrated consoles can serve several disciplines from one installed platform and reduce workflow friction inside the operating room. Competitive positioning in the ultrasonic aspirator market is increasingly shaped by installed base leverage, breadth of indication clearances, and navigation ecosystem fit, which gives larger suppliers a practical advantage when they expand within existing neurosurgery accounts. Even so, the ultrasonic aspirator market still faces slower adoption in some settings because capital budgets remain tight, training requirements stay high, and alternative energy and suction platforms continue to compete for the same procedural budgets.

Key Report Takeaways

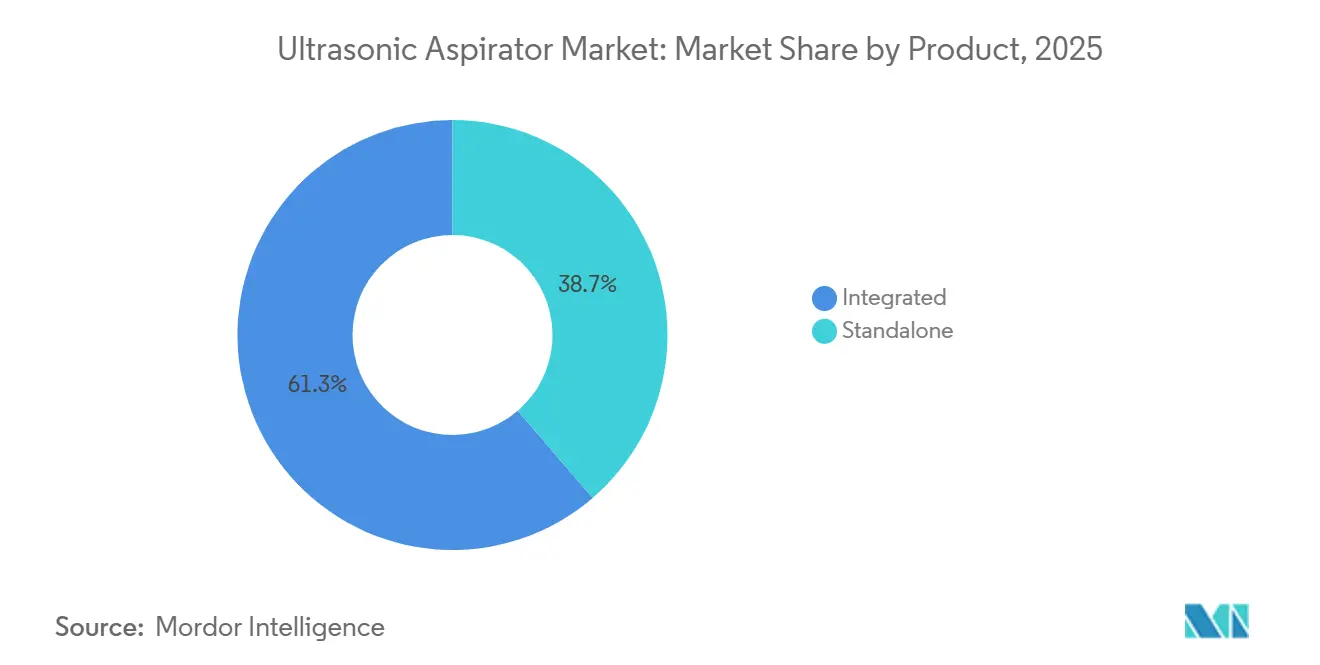

- By product, integrated systems led with 61.31% revenue share in 2025, and the same segment is forecast to grow at 8.68% CAGR through 2031 in the ultrasonic aspirator market.

- By application, neurosurgery held the largest 27.07% share in 2025, while cardiac surgery is projected to record the fastest 10.12% CAGR through 2031.

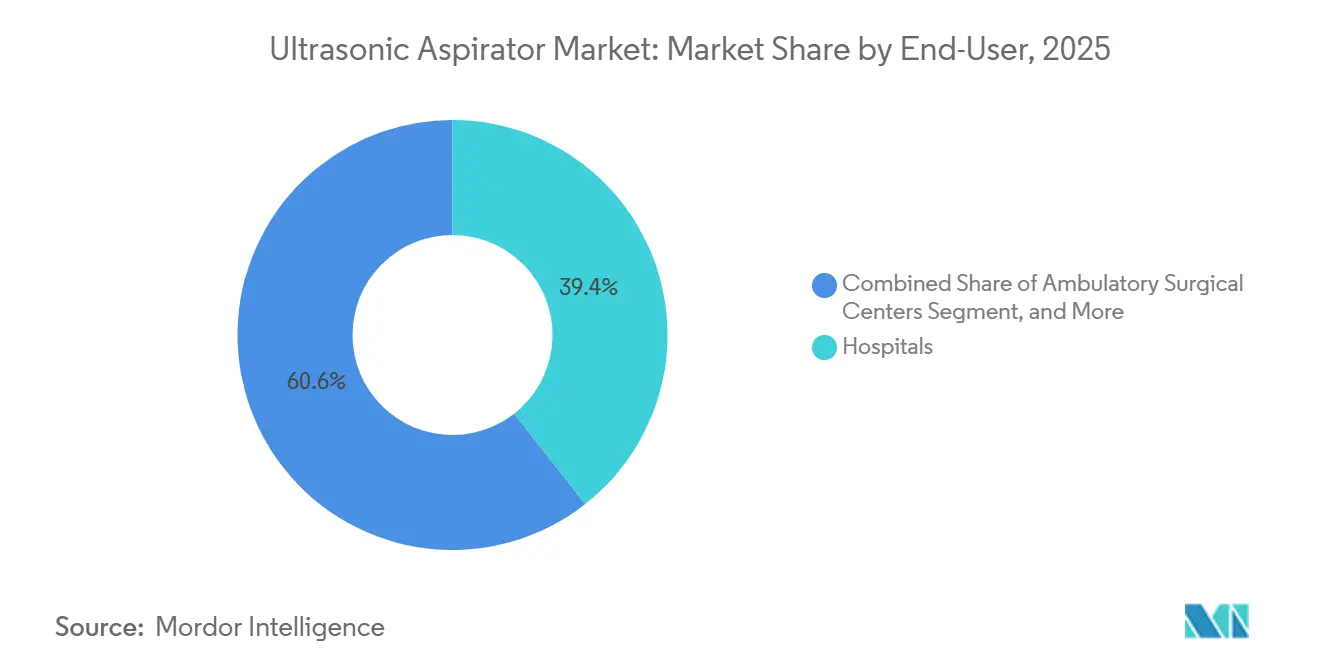

- By end-user, hospitals accounted for 39.36% share in 2025 in the ultrasonic aspirator market, while specialty clinics are expected to expand at the fastest 9.34% CAGR through 2031.

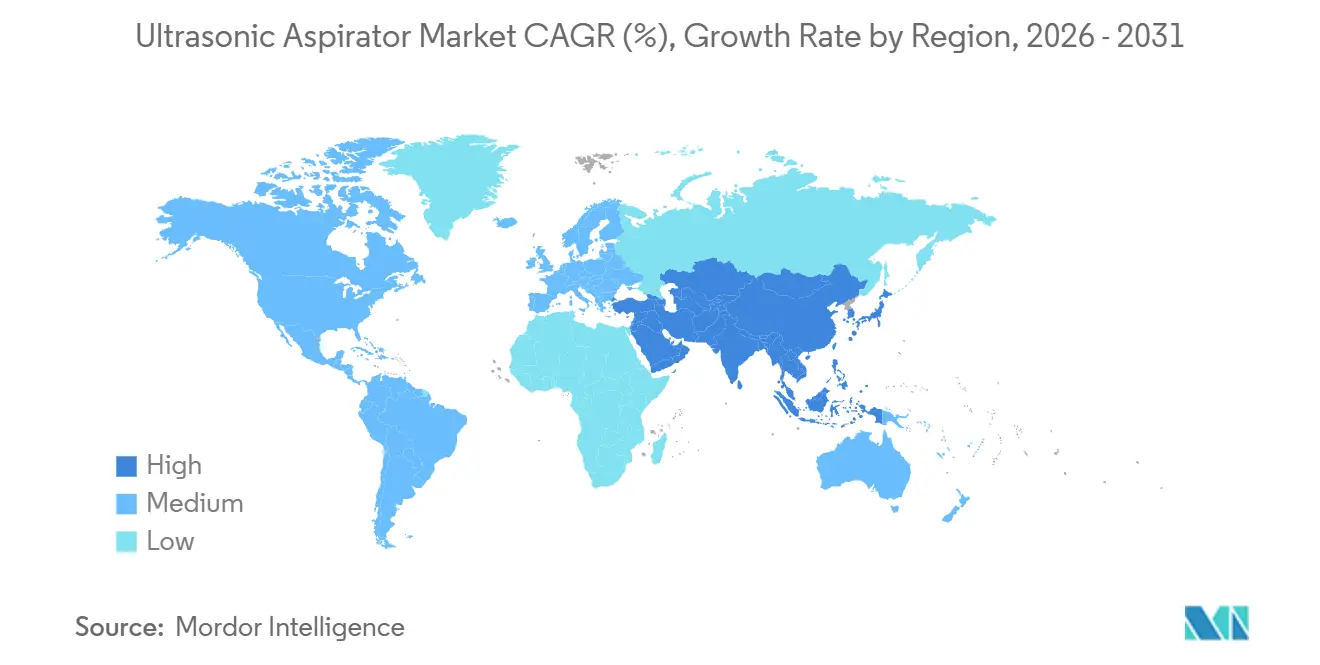

- By geography, North America held the largest 38.16% share in 2025, while Asia-Pacific is expected to post the fastest 9.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ultrasonic Aspirator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Neurological and Oncology Surgery Volumes | +1.8% | Global, with concentration in North America and Western Europe | Short term (≤ 2 years) |

| Shift Toward Precision-Based Minimally Invasive Surgery | +1.5% | Global, led by North America, Europe, and Japan | Medium term (2-4 years) |

| AI-Guided Surgical Workflow Integration | +1.1% | North America and Western Europe, with early adoption in Asia-Pacific | Medium term (2-4 years) |

| Expansion of Ambulatory and Day-Surgery Capacity | +1.0% | North America primarily, with spillover to Europe and Asia-Pacific | Short term (≤ 2 years) |

| Replacement Demand From Aging Ultrasonic Surgical Installed Base | +0.8% | North America and Europe | Medium term (2-4 years) |

| Budget Reallocation Toward High-Acuity Surgical Capital Equipment | +0.7% | North America, Europe, and core Asia-Pacific markets | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Neurological And Oncology Surgery Volumes

The ultrasonic aspirator market continues to draw durable support from rising neurological and oncology surgery volumes because the core use case remains tied to delicate tissue removal around critical neural structures. This demand is directly related to the growing disease burden, and global brain and central nervous system cancer prevalence reached 975,279 cases in 2021, with the age-standardized prevalence rate projected to increase from 12 to 13.5 per 100,000 by 2040.[1]Frontiers in Neurology Editorial Office, “The Global, Regional, and National Brain and Central Nervous System Cancer Burden and Trends From 1990 to 2021,” Frontiers in Neurology, frontiersin.orgThe ultrasonic aspirator market also benefits when complex tumor surgeries become more concentrated at tertiary centers, because those centers are more likely to purchase premium systems, maintain trained teams, and standardize workflows around established platforms. That concentration creates a smaller but more predictable customer base for the ultrasonic aspirator market, and it improves visibility for service contracts, disposable demand, and account expansion after the first console sale. It also raises the value of vendor-led training and clinical support, since hospitals that handle higher-acuity caseloads tend to expect stronger procedural coverage and faster troubleshooting. As a result, disease burden not only increases procedure counts in the ultrasonic aspirator market, but it also improves the commercial quality of demand inside the most important buying accounts.

Shift Toward Precision-Based Minimally Invasive Surgery

The ultrasonic aspirator market is also being lifted by the move toward precision-based minimally invasive surgery, where surgeons need selective tissue fragmentation in tighter spaces and near vulnerable vessels or nerves. The evidence for laparoscopic endometriosis excision, where investigators reported safe use of CUSA with limited thermal spread in fertility-preserving procedures. A separate 2025 simulation study also supported the safety profile of ultrasonic aspiration in intramedullary spinal cord tumor treatment by showing operating temperatures remained below the 46 °C tissue-necrosis threshold.[2]Editorial Team, “Ultrasonic Surgical Aspirator in Intramedullary Spinal Cord Tumours Treatment,” Bioengineering, mdpi.com That matters for the ultrasonic aspirator market because minimally invasive adoption does not simply shift existing case volume from one tool to another; it expands the number of procedures where aspirators can be justified on precision and tissue-preservation grounds. The ultrasonic aspirator market also gains from cross-specialty use, since one installed console can support neurosurgery, liver resection, gynecological surgery, thoracic surgery, and now selected cardiac procedures when the system holds the right clearances. This pattern strengthens platform economics for hospitals and reinforces the role of multifunction consoles in the ultrasonic aspirator market.

AI-Guided Surgical Workflow Integration

The ultrasonic aspirator market is gradually moving toward AI-guided and digitally integrated workflows, although the greatest change is occurring around navigation, visualization, and workflow control rather than inside the aspiration console alone. Stryker's Sonopet iQ received FDA 510(k) clearance in March 2025 with real-time frequency modulation and wireless foot control, which supports more fluid intraoperative adjustment without breaking the resection sequence.[3]U.S. Food and Drug Administration, “K243930, Sonopet iQ Ultrasonic Aspirator System,” FDA 510(k) Database, 510kdatabase.net The ultrasonic aspirator market is therefore starting to reward vendors that can fit into a wider surgical ecosystem, especially when surgeons expect imaging, navigation, robotic guidance, and aspiration to work as one coordinated workflow. Medtronic's 2025 10-K described a neurosurgery portfolio that combines navigation, robotic guidance, imaging, and adjacent tools, and that broad installed base gives the company a practical cross-selling advantage in the ultrasonic aspirator market. The strategic implication is that stand-alone aspirator vendors may find it harder to capture premium pricing if the value conversation shifts from one tool's performance to the efficiency of the entire surgical stack. Over time, the ultrasonic aspirator market is likely to reward suppliers that make aspiration part of an integrated digital surgery environment rather than a single-function console sale.

Expansion Of Ambulatory And Day-Surgery Capacity

The ultrasonic aspirator market is also being influenced by the gradual expansion of ambulatory and day-surgery capacity, particularly where complex procedures are moving out of large inpatient settings and into focused surgical environments. The ambulatory surgery centers and specialty settings are an emerging buyer pool that is asking for compact consoles, simpler logistics, and financing structures that fit lower-volume facilities. That changes the commercial model in the ultrasonic aspirator market because many independent centers do not buy equipment the same way academic hospitals do, and they often weigh setup time, disposables cost, and service simplicity more heavily. The ultrasonic aspirator market can therefore gain from the rise of this channel only if vendors adapt product configuration, training support, and commercial terms to that operating model. The specialty clinics segment is the fastest-growing end-user group, which supports the idea that focused care environments are becoming more important purchase points for the ultrasonic aspirator market. As this channel grows, suppliers that build outpatient-friendly offerings should be better positioned to capture new placements without depending only on large hospital capital budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Lifecycle Ownership Cost | -1.5% | Global, most acute in emerging Asia-Pacific markets and South America | Medium term (2-4 years) |

| Shortage of Surgeons and OR Staff Trained on Ultrasonic Tissue Fragmentation | -1.0% | Global, with acute shortfall in Middle East and Africa, South America, and smaller Asia-Pacific markets | Long term (≥ 4 years) |

| Competitive Substitution From Established Energy and Suction Platforms | -0.9% | Global, most intense in gynecological and gastrointestinal surgery segments | Medium term (2-4 years) |

| Lengthy Regulatory Approval and Hospital Procurement Cycles | -0.8% | Global, most pronounced in Europe and the United States | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital And Lifecycle Ownership Cost

High capital and lifecycle ownership costs remain one of the clearest limits on the ultrasonic aspirator market because the full expense reaches well beyond the base console purchase. The ownership includes service agreements, replacement handpieces and tips, consumables, and formal training, which makes the economic decision more difficult for smaller hospitals and focused outpatient centers. This issue matters across the ultrasonic aspirator market because adoption often depends on committee review, and committees tend to compare aspirators against other energy platforms that appear easier to justify on immediate utilization. Cost pressure is also more visible in channels where case volume is still building, since facilities may struggle to spread fixed service and training costs over enough procedures in the early years of adoption. In practical terms, the ultrasonic aspirator market expands faster when vendors offer flexible financing, refurbished platforms, longer warranties, or simpler recurring-cost models that reduce budget friction at the account level. Without that adaptation, some customers will continue to delay purchase decisions even when clinical demand is present.

Shortage Of Surgeons and or Staff Trained On Ultrasonic Tissue Fragmentation

The ultrasonic aspirator market is also restrained by the limited pool of surgeons and operating room staff who are fully trained in the ultrasonic tissue fragmentation technique. They stressed that effective use depends on setting selection, tip angle, tissue engagement pressure, and workflow familiarity, which means competency usually comes through structured mentoring rather than brief device orientation. This creates a practical bottleneck in the ultrasonic aspirator market because many of the facilities expected to grow fastest, including specialty clinics and ambulatory settings, are not the places where most advanced training currently takes place. The same gap affects scrub technicians and circulating nurses, since they also need device-specific knowledge for setup, handpiece connection, and troubleshooting during procedures. As a result, the ultrasonic aspirator market does not scale only through product placement; it also scales through simulation programs, proctorship, and digital onboarding that help new sites become clinically comfortable with the technology. Vendors that invest more heavily in those support structures can widen their usable market faster than vendors that compete on hardware specification alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Integration Consolidates The Platform Architecture

Integrated systems held 61.31% share of the ultrasonic aspirator market size in 2025, and they are also projected to expand at an 8.68% CAGR through 2031. This leadership reflects buyer preference for consolidated platforms that combine power delivery, aspiration, irrigation, and handpiece control inside a single console, which lowers compatibility risk and makes operating room setup more predictable. Integra's CUSA Clarity is a clear example of that model, and its indication expansion into cardiac surgery in November 2025 showed how one installed platform can keep adding procedural value over time. Stryker's Sonopet iQ also supports this integrated direction, since its 2025 clearance added real-time modulation and wireless foot control features that fit academic and high-precision settings. The ultrasonic aspirator market, therefore, favors integrated systems not only because they simplify console management, but also because they create a better base for multi-specialty use, training standardization, and hospital-wide service support.

Standalone systems remain relevant in the ultrasonic aspirator industry because they serve hospitals and specialist centers that want to upgrade handpieces or preserve existing infrastructure without replacing the full console. Growth in this part of the ultrasonic aspirator market is slower, but the slower pace reflects replacement timing rather than disappearing need. Mature sites in North America and Europe still operate legacy equipment, and that installed base preserves a practical role for stepwise upgrades instead of immediate conversion to a new integrated platform. The regulatory framework also keeps both product types active, because ultrasonic surgical devices under FDA product code LFL and 21 CFR Part 878 still need to demonstrate substantial equivalence through the 510(k) route, regardless of configuration. Over the medium term, the ultrasonic aspirator industry is likely to keep integrated systems in the lead while allowing standalone systems to hold a narrower but still durable replacement-oriented niche.

By Application: Neurosurgery Anchors Volume While Cardiac Broadens The Case Mix

Neurosurgery accounted for 27.07% share of the ultrasonic aspirator market size in 2025, while cardiac surgery is forecast to grow at the fastest 10.12% CAGR through 2031. Neurosurgery remains the anchor application because the clinical need for selective tissue removal is strongest in brain tumor resection and other procedures performed near critical neural structures. The application mix is widening, and Integra's November 2025 cardiac clearance opened a new procedural pool around valve replacement and repair that sits under different hospital teams and budgets. That development matters for the ultrasonic aspirator market because it reduces dependence on neurosurgery alone and gives suppliers a path into additional high-value departments without building a completely new platform. The ultrasonic aspirator market is therefore becoming broader in application while still relying on neurosurgery as its clinical and commercial foundation.

Gynecological and gastrointestinal procedures add steadier growth to the ultrasonic aspirator industry, supported by published evidence that selective tissue fragmentation can preserve surrounding structures and limit thermal spread in delicate laparoscopic work. Brain cancers, ischemic stroke, and traumatic brain injury remain tightly linked to the wider neurosurgery demand pool because they reflect overlapping drivers in complex neuro care and long-run disease burden. The orthodontic surgery as a niche area where precision around nerve bundles still creates a procedural role for ultrasonic aspiration. Other applications, including liver transplant and thoracic surgery, help extend the ultrasonic aspirator market into adjacent settings where multi-indication approvals can strengthen utilization rates across the installed base. Vendors that develop procedure-specific tip geometries and power settings are well placed in this part of the ultrasonic aspirator market because surgeons often judge performance through case-level control rather than through generic platform claims.

By End-User: Hospital Demand Stays Largest While Specialty Clinics Gain Pace

Hospitals held 39.36% share in 2025, which kept them as the largest end-user group in the ultrasonic aspirator market. Their lead remains tied to complex surgical volume, larger capital budgets, formal training structures, and the concentration of neuro-oncology, cardiac, and advanced liver procedures inside tertiary settings. The specialty clinics are set to grow at the fastest 9.34% CAGR through 2031, which signals a wider migration of selected procedures into focused care environments. That trend supports the ultrasonic aspirator market because specialist-led centers often value scheduling speed, dedicated case flow, and targeted equipment placement that matches a narrower set of procedures. At the same time, hospitals still anchor the ultrasonic aspirator market because they provide the broadest platform utilization across disciplines and remain the main sites for training and early adoption.

Ambulatory surgery centers and specialty clinics are changing how sales work in the ultrasonic aspirator market because these accounts usually ask for smaller footprints, simpler consumable planning, and faster staff onboarding. The buying influence is shifting within hospitals, where specialty divisions increasingly shape purchase decisions for AI-compatible and workflow-integrated systems rather than leaving those decisions only to central procurement. That shift raises the importance of clinical sales support in the ultrasonic aspirator market, since vendors now need to speak to surgeons, nurses, technicians, and administrators in the same account. Other end-users, including dental surgery institutes, research hospitals, and military care settings, remain smaller but meaningful because they are less saturated and often underserved by mainstream channel strategies. Overall, end-user change is broadening the ultrasonic aspirator market beyond the traditional hospital base without weakening the hospital sector's central role.

Geography Analysis

North America held 38.16% ultrasonic aspirator market share in 2025, which made it the largest regional contributor to the ultrasonic aspirator market. The region benefits from a dense concentration of academic neurosurgery centers, higher procedure intensity, and an FDA pathway that allows suppliers to expand indications and refresh product features with relatively consistent regulatory logic. The ultrasonic aspirator market in North America also gains from mature installed bases, because replacement demand from legacy systems can support recurring capital cycles even when first-time adoption moderates. Medtronic's broad neurosurgery platform presence strengthens this regional position further by giving the company a practical route to cross-sell aspiration tools into already established navigation and imaging accounts.

Europe remains a major pillar of the ultrasonic aspirator market because it combines long-standing academic neurosurgery capability with a high underlying disease burden in neuro-oncology. Western Europe recorded the world's highest brain and central nervous system cancer age-standardized incidence rate at 7.4 per 100,000, which supports a steady procedural need for ultrasonic aspiration. Germany stands out through both demand and device manufacturing depth, while the United Kingdom and France remain important treatment centers with established hospital networks. The ultrasonic aspirator market in Europe is therefore supported by clinical capability and structural demand, even though procurement and compliance processes can remain slower than in the United States.

Asia-Pacific is projected to expand at 9.96% CAGR through 2031, which makes it the fastest-growing regional portion of the ultrasonic aspirator market size. Japan contributes through a large neurosurgical need base, and the high-income Asia-Pacific cohort recorded a brain and central nervous system cancer age-standardized prevalence rate of 36.4 per 100,000. China adds a different growth pattern, with hospital modernization and device localization shaping how the ultrasonic aspirator market develops across large care networks. The Middle East and Africa and South America remain smaller parts of the ultrasonic aspirator market, with growth concentrated in better-funded health systems and major urban hospitals. These regions still offer room for expansion, but distributor dependence, training limitations, and longer approval pathways can slow the speed of adoption compared with North America, Europe, and advanced Asia-Pacific markets.

Competitive Landscape

The ultrasonic aspirator market shows moderate concentration rather than dominance by a single supplier. Stryker's position in the ultrasonic aspirator market is tied closely to product refresh and workflow usability, and the March 2025 FDA clearance for Sonopet iQ supported that direction with real-time frequency modulation and wireless foot control. Medtronic competes from a wider ecosystem position, since its neurosurgery portfolio includes navigation, robotic guidance, imaging, and adjacent tools that can reinforce account retention and cross-selling. Integra strengthens its standing in the ultrasonic aspirator market by expanding CUSA Clarity across more procedures, and its November 2025 cardiac clearance materially widened the addressable case mix beyond traditional neurosurgery.

Competition in the ultrasonic aspirator market is also shaped by how well a supplier can connect device performance with training, service, and clinical workflow support after installation. Integrated platforms have an advantage here because they can be standardized across departments, and that reduces friction when hospitals want broader use from one console base. The ultrasonic aspirator market also remains open to competition from alternative energy and suction platforms in gastrointestinal and gynecological surgery, where hospitals often compare a broader set of tools at the budget stage. That keeps the field from becoming overly concentrated across the full ultrasonic aspirator market, even if neurosurgery accounts are more tightly contested among a smaller group of established brands. As a result, competitive strength depends on more than installed share, it also depends on indication breadth, procedural proof, and the ability to keep the device relevant inside changing surgical workflows.

Olympus adds another competitive layer to the ultrasonic aspirator market through adjacent ultrasonic surgical capability, and the October 2025 FDA clearance for the USG-410 Ultrasonic Bipolar Generator showed continued movement in this direction. The broader field also included companies such as KARL STORZ, B. Braun, Söring, and other specialized participants, which suggests the ultrasonic aspirator market still has room for niche strategies even when the top names are strong. White-space opportunities remain visible around robotic compatibility, pediatric-scale tip design, and disposable kits better suited to fast-turnover outpatient settings, all of which can influence future share movement in the ultrasonic aspirator market. Overall, the ultrasonic aspirator market rewards suppliers that combine clinical credibility with ecosystem fit, while still leaving enough room for focused challengers in specific procedures or care settings.

Ultrasonic Aspirator Industry Leaders

B. Braun SE

Boston Scientific Corporation

Integra LifeSciences Corporation

Medtronic

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Trice Medical has announced the launch of its Tenex 2nd Generation Ultrasonic System, marking a significant advancement in minimally invasive treatment options for chronic tendon pain. This new system enhances precision and efficiency in ultrasonic therapy, expanding access to innovative solutions for patients suffering from long-term tendon conditions.

- November 2025: Integra LifeSciences received FDA 510(k) clearance (K251162) for the CUSA Clarity Ultrasonic Surgical Aspirator System in cardiac surgery, encompassing tissue debridement in valve replacement and repair procedures. This was the first formal cardiac indication for a CUSA-class device and it opened a new surgical department as a customer segment for ultrasonic aspiration technology.

- March 2025: Stryker Instruments received FDA 510(k) clearance (K243930) for the Sonopet iQ Ultrasonic Aspirator System, incorporating real-time frequency modulation and wireless foot control for surgical workflow refinement in high-precision settings.

Global Ultrasonic Aspirator Market Report Scope

The Ultrasonic Aspirator Market is defined as the global industry for surgical devices that use ultrasonic vibration to fragment, emulsify, and aspirate soft tissue during complex procedures such as neurosurgery, gynecology, gastrointestinal, and liver resections. These devices enable precise tissue removal while minimizing damage to surrounding healthy structures, making them essential in minimally invasive and high‑precision surgeries.

The Ultrasonic Aspirator Market is segmented by product, application, end‑user, and geography. By product, it includes Integrated and Standalone devices. By application, it covers Neurosurgery, Gynecological Surgery, Gastrointestinal Surgery, Cardiac Surgery, Orthodontic Surgery, Brain Cancers, Ischemic Stroke, Traumatic Brain Injury, and Other Applications. By end‑user, the market is segmented into Hospitals, Ambulatory Surgical Centers, Specialty Clinics, and Other End‑Users.

Geographically, it spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia‑Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle East and Africa), and South America (Brazil, Argentina, Rest of South America).

| Integrated |

| Standalone |

| Neurosurgery |

| Gynecological Surgery |

| Gastrointestinal Surgery |

| Cardiac Surgery |

| Orthodontic Surgery |

| Brain Cancers |

| Ischemic Stroke |

| Traumatic Brain Injury |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Integrated | |

| Standalone | ||

| By Application | Neurosurgery | |

| Gynecological Surgery | ||

| Gastrointestinal Surgery | ||

| Cardiac Surgery | ||

| Orthodontic Surgery | ||

| Brain Cancers | ||

| Ischemic Stroke | ||

| Traumatic Brain Injury | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current outlook for ultrasonic aspirator demand through 2031?

The ultrasonic aspirator market is expected to rise from USD 225.61 million in 2026 to USD 331.95 million by 2031 at an 8.03% CAGR, supported by growth in complex neurosurgery, oncology procedures, and broader use in precision surgical settings.

Which product type leads revenue generation?

Integrated systems lead the ultrasonic aspirator market, holding 61.31% share in 2025 and also posting the fastest product growth at 8.68% CAGR through 2031, which reflects buyer preference for unified consoles and simpler workflow management.

Why does neurosurgery remain the core use case?

Neurosurgery held 27.07% share in 2025 because ultrasonic aspiration remains highly valuable in tissue removal near critical neural structures, where precision, limited traction, and controlled thermal effect are especially important.

Which end-user group is growing fastest?

Specialty clinics are the fastest-growing end-user segment at 9.34% CAGR through 2031, although hospitals remained the largest segment in 2025 with 39.36% share because they still manage the highest-acuity procedures and most formal training pathways.

Which region offers the strongest near-term expansion opportunity?

Asia-Pacific is the fastest-growing regional segment at 9.96% CAGR through 2031, while North America remains the largest regional base with 38.16% share in 2025 due to stronger installed infrastructure and deep neurosurgery capacity.

What are the main barriers that can slow adoption?

The biggest constraints in the ultrasonic aspirator market are high full-lifecycle ownership costs, limited trained surgeon and operating room staff availability, and competition from other surgical energy or suction systems that target similar budgets.

Page last updated on: