Neurology Ultrasonic Aspirators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

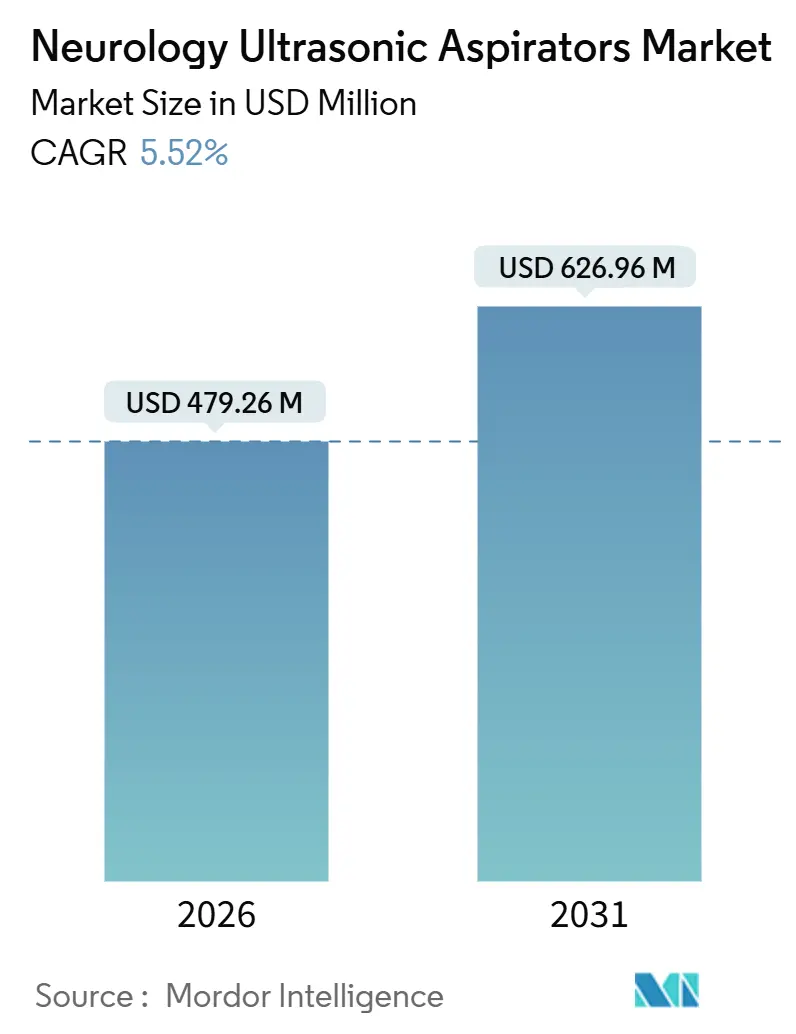

| Market Size (2026) | USD 479.26 Million |

| Market Size (2031) | USD 626.96 Million |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

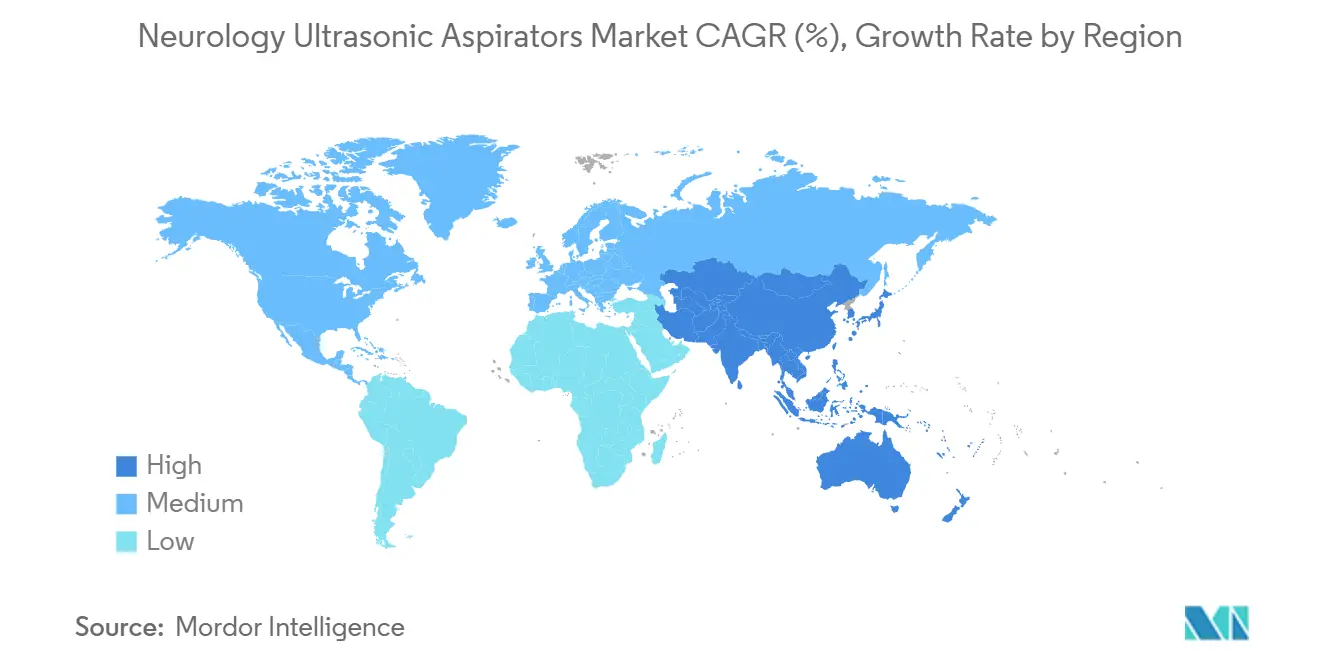

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

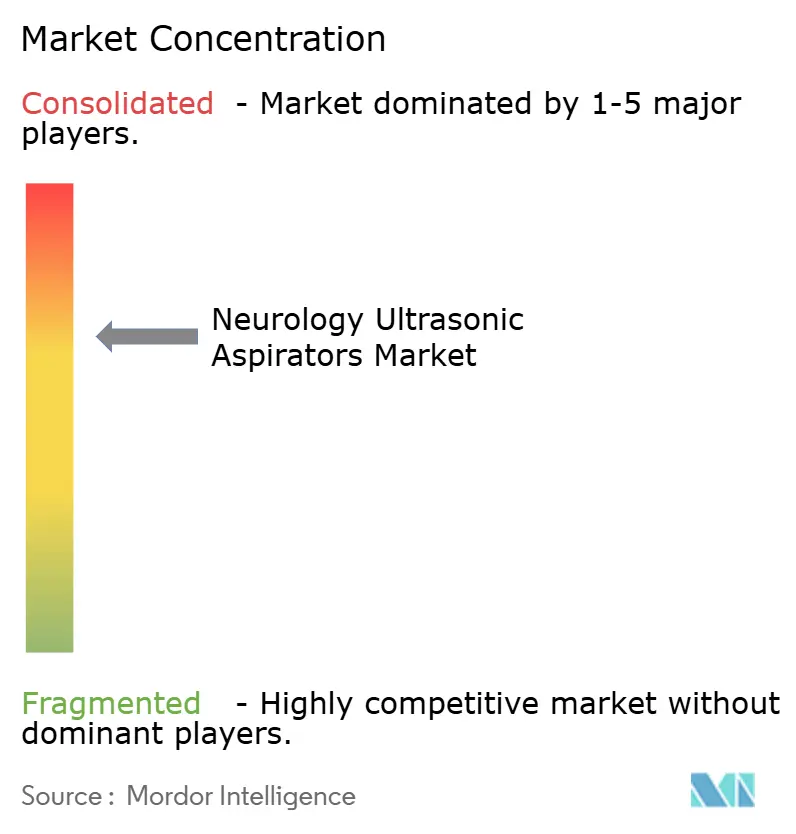

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurology Ultrasonic Aspirators Market Analysis by Mordor Intelligence

The Neurology Ultrasonic Aspirators Market size is estimated at USD 479.26 million in 2026, and is expected to reach USD 626.96 million by 2031, at a CAGR of 5.52% during the forecast period (2026-2031).

Hospital budgets remain tight, yet surgeons view ultrasonic fragmentation as a safety-critical technology for brain tumor and spinal decompression cases, which keeps replacement cycles active. Modular handpiece upgrades are attracting capital-constrained facilities because they deliver the latest tip geometries without forcing a full console purchase. A broader shift toward minimally invasive and outpatient neurosurgery is expanding the total addressable pool of procedures, while integration with imaging and navigation platforms encourages premium pricing. Competition remains moderate as three multinational suppliers bundle training and service contracts to secure long-term accounts.

Key Report Takeaways

- By product type, standalone consoles held 46.76% of the neurology ultrasonic aspirators market share in 2025; handpiece-only upgrades are forecast to grow at a 7.65% CAGR through 2031.

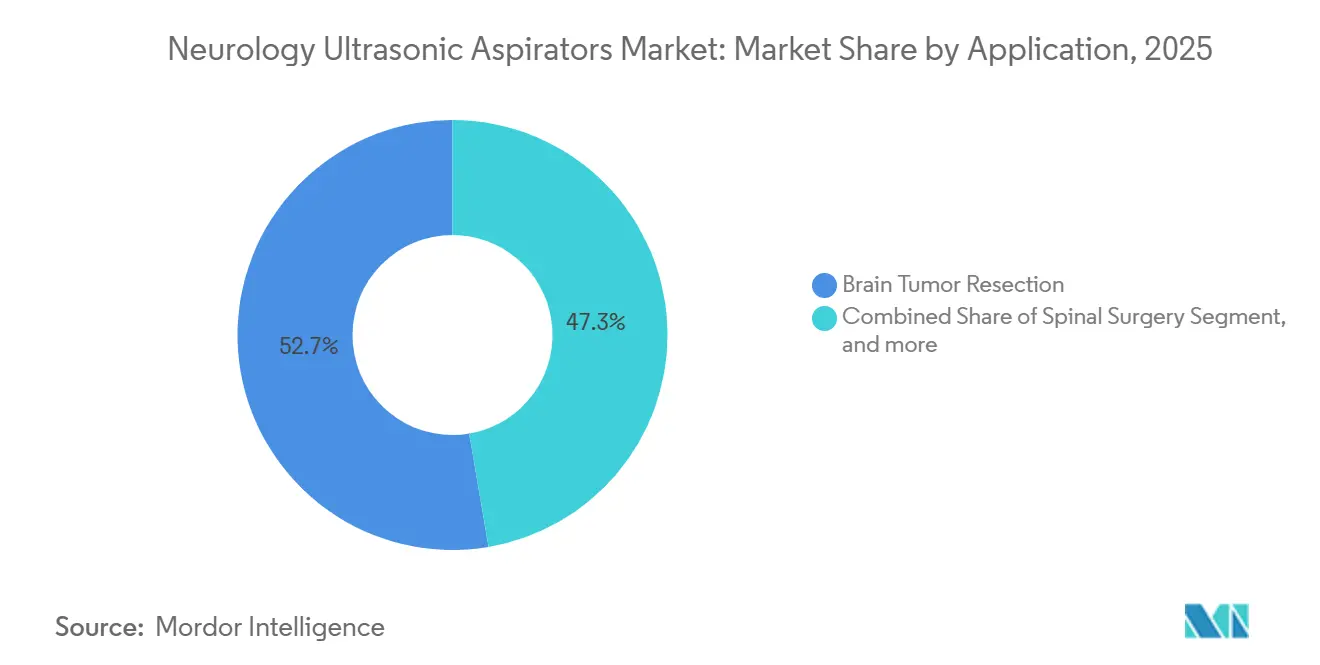

- By application, brain tumor resection accounted for 52.67% of the neurology ultrasonic aspirators market in 2025; epilepsy and functional neurosurgery are advancing at an 8.22% CAGR through 2031.

- By end user, hospitals captured 71.43% revenue in 2025, while ambulatory surgical centers are set to expand at an 8.43% CAGR through 2031.

- By geography, North America dominated with 42.67% revenue in 2025; Asia-Pacific is projected to post the fastest CAGR of 6.54% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Neurology Ultrasonic Aspirators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Neurological Disorders | +1.2% | Global, highest in Japan, Germany, United States | Long term (≥ 4 years) |

| Continuous Technological Innovation in Ultrasonic Aspiration Devices | +1.4% | North America and Europe for R&D, Asia-Pacific for adoption spill-over | Medium term (2-4 years) |

| Growing Adoption of Minimally Invasive Neurosurgical Techniques | +1.3% | United States, Germany, urban China | Medium term (2-4 years) |

| Expanding Healthcare Expenditure and Neuro-Specialty Infrastructure | +0.9% | China, India, South Korea, Middle East & Africa | Long term (≥ 4 years) |

| Integration With Advanced Intraoperative Imaging and Navigation | +1.1% | North America, Western Europe, Japan | Short term (≤ 2 years) |

| Emergence of Ambulatory Neurosurgery Settings in Developed Markets | +1.0% | United States, Canada, Germany, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Neurological Disorders

Primary brain tumor incidence rose to 321,731 new cases worldwide in 2022, pushing hospitals to replace legacy suction instruments with precision ultrasonic systems that spare the eloquent cortex[1]International Agency for Research on Cancer, “GLOBOCAN 2022 Brain Tumor Statistics,” iarc.fr. Epilepsy affects 50 million people, and one-third remain drug-resistant, creating a procedural backlog for resective and ablative surgery that routinely uses ultrasonic fragmentation. Aging populations in Japan and Germany elevate demand for spinal decompression and vascular malformation resections, both of which benefit from ultrasonic bone scalpels that limit thermal damage. The United States logs about 25,000 malignant brain tumor diagnoses each year, with sub-10% five-year survival in glioblastoma, sustaining the clinical push for maximal safe resection. These epidemiologic pressures ensure that the neurology ultrasonic aspirators market continues to receive budget priority despite capital constraints.

Continuous Technological Innovation in Ultrasonic Aspiration Devices

Integra expanded CUSA Clarity into cardiac surgery in 2025, creating a new USD 150 million addressable segment and shortening payback periods for hospitals that operate multi-specialty theaters. Stryker’s Sonopet iQ combines real-time tissue-impedance sensing with wireless foot control, allowing surgeons to adjust ultrasonic frequency mid-cut and reducing the risk of vascular injury during skull-base procedures. The U.S. FDA cleared 14 ultrasonic surgery devices in 2024, several of which feature articulating tips that improve reach to posterior fossa and foraminal targets. Medtronic embedded its aspirator handpieces within the StealthStation S8 workflow, overlaying MRI data so neurosurgeons can trim margins intraoperatively. Rapid feature gains are shortening replacement cycles to five-seven years, which lifts the neurology ultrasonic aspirators market even where procedure volumes are flat.

Growing Adoption of Minimally Invasive Neurosurgical Techniques

U.S. ambulatory surgery centers completed more than 28 million procedures in 2024, and neurosurgery is carving a bigger share as laser ablation for epilepsy and endoscopic decompression migrate out of inpatient wards. New CMS outpatient codes in 2024 reimburse minimally invasive cranial work, eliminating a reimbursement gap that once blocked ASC uptake. Germany’s insurers now cover endoscopic third ventriculostomy and transsphenoidal pituitary surgery, both of which use ultrasonic aspirators to debulk tissue through small corridors. Beijing’s Tiantan Hospital logged a 40% jump in minimally invasive spine cases between 2023 and 2025, prompting the procurement of compact handpiece systems with fast sterilization turnaround times. These operating-room shifts grow total unit demand and tilt purchases toward modular platforms priced for outpatient economics.

Expanding Healthcare Expenditure and Neuro-Specialty Infrastructure

China earmarked CNY 850 billion (USD 120 billion) for hospital expansion in 2024, with nearly one-third routed to neurosurgery and cardiovascular suites. India added six new AIIMS campuses between 2024 and 2025, each pre-equipped with MRI-guided neurosurgery theaters that specify ultrasonic fragmentation as standard. Saudi Arabia invested USD 12 billion in tertiary hospitals through 2025, including a major neuroscience wing in Riyadh that standardizes on ultrasonic debulking for tumor and vascular cases. South Korea raised reimbursement for complex cranial procedures by 15% in 2024, freeing budget for console upgrades. These policy moves create steady pipelines that lift the neurology ultrasonic aspirators market across the next decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Maintenance Costs of Ultrasonic Aspirator Systems | -0.8% | Emerging Asia-Pacific, Latin America, Sub-Saharan Africa | Short term (≤ 2 years) |

| Limited Reimbursement and Cost-Benefit Evidence in Certain Regions | -0.6% | Latin America, Middle East & Africa, rural Asia-Pacific | Medium term (2-4 years) |

| Shortage of Highly Trained Neurosurgeons in Emerging Markets | -0.7% | Sub-Saharan Africa, South Asia, parts of Latin America | Long term (≥ 4 years) |

| Stringent Regulatory Approval and Compliance Burdens | -0.5% | European Union, Japan, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs of Ultrasonic Aspirator Systems

A console lists for USD 80,000-150,000, and annual service contracts add USD 8,000-15,000, a heavy burden for hospitals operating under capitated payments. Handpieces that must be replaced every 50-100 cases cost USD 1,200-2,500, and that consumable line competes with implants and biologics during budget cycles. Public hospitals in Brazil and Argentina froze capital budgets at 2023 levels as currency depreciation increased import costs, forcing neurosurgery departments to run equipment past its intended lifespan[2]Brazilian Ministry of Health, “2025 Capital Budget Report,” saude.gov.br. Rural Indian and Indonesian centers lack biomedical engineers who can service generators, leading to downtime exceeding 20% and discouraging further investment. These issues steer buyers toward handpiece-only upgrades, restraining revenue growth in full-console categories of the neurology ultrasonic aspirators market.

Limited Reimbursement and Cost-Benefit Evidence in Certain Regions

Medicare trimmed 2024 physician fees for select cranial codes by 2-3%, tightening margins on technology-intensive surgery and delaying equipment refresh in community hospitals. Private insurers in Mexico and Colombia require pre-authorization for ultrasonic aspirator use, a paperwork hurdle that dampens adoption in ambulatory settings. NICE has not issued guidance on ultrasonic aspirators, leaving procurement to cash-strapped NHS trusts that already face elective-care backlogs[3]National Institute for Health and Care Excellence, “Medical Technologies Guidance Pipeline,” nice.org.uk. Donor-backed neurosurgery programs in South Africa and Kenya still favor basic instrumentation because cost-effectiveness data for ultrasonic devices remain scarce. Until local health technology assessments quantify the benefits of outcomes, the neurology ultrasonic aspirators market will advance more slowly in these territories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Modular Upgrades Gain Traction

Standalone consoles captured 46.76% of revenue in 2025 as high-volume academic hospitals valued integrated irrigation, suction, and programmable power settings for long skull-base cases. Handpiece-only kits are forecast to post a 7.65% CAGR to 2031, the fastest product-level pace in the neurology ultrasonic aspirators market, because they retrofit legacy generators at one-third the cost of new consoles. Integrated irrigation variants that combine saline infusion with aspiration are gaining traction in outpatient spine suites where every minute of turnover counts. FDA’s streamlined 510(k) path for accessory handpieces lets suppliers launch articulating tips and variable-frequency modules without full trials, accelerating innovation cycles.

Hospitals performing 200-plus cranial resections each year still favor console replacements because advanced user interfaces and multichannel suction improve ergonomics during six-hour operations. Community hospitals and ASCs that handle 50-100 procedures annually tend to favor handpiece upgrades that align with cash-flow constraints. Stryker’s Sonopet iQ wireless foot switch removes floor cables and reduces unintended activation, a popular ergonomic upgrade. Integra leverages CUSA Clarity’s cardiac approval to cross-book neurosurgery plus valve cases, lifting utilization and justifying capital spend. Quality-system certifications, such as ISO 13485, are now appearing in procurement tenders across Germany and Japan, giving compliance-ready vendors an edge.

By Application: Epilepsy Surgery Accelerates

Brain tumor resection accounted for 52.67% of the neurology ultrasonic aspirators market revenue in 2025, as glioblastoma and metastasis workflows demand ultrasonic debulking to protect the motor and language cortex. Epilepsy and functional neurosurgery are projected to advance at an 8.22% CAGR to 2031, the swiftest rise, driven by SEEG mapping and laser ablation protocols that rely on small-footprint aspirators compatible with stereotactic frames. Spinal laminectomy and foraminotomy volumes continue to expand as bone scalpels replace drills, reducing dura tear risk and operating time, and lifting sales of integrated irrigation tips. Neuro-trauma remains niche because volume swings with accident rates, and trauma surgeons often prefer manual debridement when budgets are tight.

SEER data show roughly 25,000 malignant brain tumor diagnoses each year in the United States, 45% of which are glioblastoma cases that call for maximal safe resection. U.S. epilepsy surgery rose 12% from 2023 to 2025 after payers broadened coverage for laser interstitial therapy. European centers report double-digit growth in functional neurosurgery for movement disorders, supporting cross-specialty use of ultrasonic debulkers. Japan’s aging society drives an 8% annual rise in spinal decompressions, giving spinal-tuned ultrasonic bone scalpels a clear runway. Regulatory equivalence rules on both sides of the Atlantic ensure a steady flow of new application clearances without long delays.

By End User: ASCs Capture Outpatient Shift

Hospitals accounted for 71.43% of 2025 revenue, as complex cranial cases still require MRI-guided theaters, which are mainly found in tertiary centers. Ambulatory surgical centers, however, are projected to grow at an 8.43% CAGR through 2031, making them the fastest-growing buyer group in the neurology ultrasonic aspirators market. Hospitals prefer fully featured consoles that integrate with StealthStation or BrainLab navigation and supply continuous irrigation for six-hour glioma resections. ASCs pick compact handpieces, focusing on low depreciation and 10-minute sterilization cycles.

European university hospitals build hybrid ORs that blend surgical and interventional radiology capabilities, so aspirators must interface with angiography systems. Indian private chains such as Apollo added 15% more neurosurgery capacity during 2024-2025 to capture medical tourism. Chinese and Korean hospitals request bundled service contracts because they face shortages of biomedical technicians. U.S. outpatient payment updates in 2024 finally reimbursed minimally invasive cranial codes, removing a financial barrier that long blocked ASC adoption.

Geography Analysis

North America accounted for 42.67% of 2025 revenue, driven by Medicare coverage for complex cranial work and the region’s dense network of intraoperative MRI suites. Nearly 6,000 ASCs and 5,000 hospitals in the United States create a substantial installed base that feeds console replacement demand. Canada adds capacity in Ontario and British Columbia to cut wait lists, while Mexico’s private hospitals invest to capture cross-border patients even as public facilities hold spending.

Asia-Pacific is poised for a 6.54% CAGR through 2031, the fastest regional growth rate in the neurology ultrasonic aspirators market. China’s USD 120 billion hospital program reserves 30% for neuro and cardiovascular theaters. Japan’s Ministry of Health expects neurosurgery volumes to rise 10% from 2025 to 2030 as its population ages. India’s six new AIIMS campuses anchor public demand, while South Korea’s 15% reimbursement bump accelerates console upgrades. Australia cut device review timelines to six months, enticing suppliers to launch regionally ahead of slower Asian jurisdictions.

Europe, the Middle East & Africa, and South America contribute smaller but strategic shares. Germany’s insurers now cover key endoscopic cranial procedures that need ultrasonic resection, sustaining steady console turnover. UK NHS budgetary constraints delay some refresh cycles, yet leading academic centers still adopt next-generation systems for research protocols. France reimburses at U.S.-equivalent rates, keeping demand consistent. Saudi Arabia’s USD 12 billion tertiary-care buildout includes a neuroscience hub with ultrasonic aspirators as standard kit. Brazil and Argentina face currency headwinds that are extending equipment lifespans, dampening new-unit demand until fiscal pressures ease.

Competitive Landscape

Stryker, Medtronic, and Integra LifeSciences together hold an estimated 60-65% share, illustrating moderate concentration in the neurology ultrasonic aspirators market. Stryker’s 2025 Sonopet iQ adds real-time frequency modulation and wireless foot control, features prized by academic centers handling eloquent cortex resections. Medtronic harnesses its vast StealthStation install base to cross-sell aspirator handpieces, giving it sticky account control. Integra diversified with cardiac clearance for CUSA Clarity, reducing reliance on neurosurgical volumes and broadening revenue avenues.

Smaller rivals such as Söring and Mectron gain share in spine surgery by pricing their consoles 20-30% below incumbents'. White-space plays include pediatric-scale handpieces and robotic compatibility, allowing aspirators to mount on surgical robots for remote resections. Disposable handpiece innovations target ASC turnover bottlenecks by eliminating the need for sterilization cycles. Patent filings climbed 18% from 2023 to 2025, focused on frequency algorithms and articulating geometries, underscoring a pipeline of incremental yet clinically meaningful upgrades. European tenders increasingly mandate ISO 13485 compliance, screening out suppliers without robust post-market surveillance.

Neurology Ultrasonic Aspirators Industry Leaders

Stryker

Integra LifeSciences

Olympus Corporation

Söring GmbH

B. Braun (Aesculap)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Insightec, one of the global healthcare innovators pioneering the use of focused ultrasound to transform patient care, spun out and launched Lotus Neuro, a new clinical-stage biotechnology company advancing the next generation of brain‑targeted therapeutics through precision, low-frequency focused ultrasound. This launch marks a pivotal evolution in brain medicine, bringing together Insightec’s world‑leading device technology and Lotus Neuro’s biotech innovation model to accelerate drug delivery across the blood‑brain barrier (BBB).

- November 2025: Integra LifeSciences gained U.S. Food and Drug Administration (FDA) 510(k) clearance for its CUSA Clarity ultrasonic surgical aspirator system for cardiac surgery. It is also indicated for surgical procedures requiring fragmentation, emulsification, and aspiration of soft and hard tissues, such as neurosurgery, plastic and reconstructive surgery, orthopedic surgery, thoracic surgery, laparoscopic surgery, gynecological surgery, and liver resection and transplant surgery.

Global Neurology Ultrasonic Aspirators Market Report Scope

As per the scope of the report, neurology ultrasonic aspirators are specialized surgical devices used to precisely remove brain or spinal cord tumors and lesions. They utilize high-frequency ultrasonic vibrations to selectively break down abnormal tissue while sparing healthy tissue. This technology enhances surgical accuracy and minimizes damage to surrounding neural structures.

The Neurology Ultrasonic Aspirators Market is Segmented by Product Type (Standalone Consoles, Integrated Ultrasonic-Irrigation Systems, and Handpiece-Only Upgrades), Application (Brain Tumor Resection, Spinal Surgery, Neuro-Trauma Debridement, Epilepsy & Functional Neurosurgery, and Cerebrovascular Surgery), End-User (Hospitals and Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Standalone Consoles |

| Integrated Ultrasonic-Irrigation Systems |

| Handpiece-Only Upgrades |

| Brain Tumor Resection |

| Spinal Surgery |

| Neuro-Trauma Debridement |

| Epilepsy & Functional Neurosurgery |

| Cerebrovascular Surgery |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product Type | Standalone Consoles | |

| Integrated Ultrasonic-Irrigation Systems | ||

| Handpiece-Only Upgrades | ||

| By Application | Brain Tumor Resection | |

| Spinal Surgery | ||

| Neuro-Trauma Debridement | ||

| Epilepsy & Functional Neurosurgery | ||

| Cerebrovascular Surgery | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the projected value of the neurology ultrasonic aspirators market in 2031?

The market is expected to reach USD 626.96 million by 2031.

Which product category is growing fastest?

Handpiece-only upgrades are forecast to post a 7.65% CAGR through 2031.

Which application segment is expanding most rapidly?

Epilepsy and functional neurosurgery procedures are advancing at an 8.22% CAGR through 2031.

What region is projected to show the highest growth rate?

Asia-Pacific is set to grow at a 6.54% CAGR over the forecast period.

Who are the leading companies in this space?

Stryker, Medtronic, and Integra LifeSciences collectively hold roughly two-thirds of global revenue.

How do high capital costs affect adoption in emerging markets?

Up-front console prices and annual service fees strain budgets, so hospitals often delay purchases or opt for handpiece upgrades instead.

Page last updated on: