Surgical Mask And Respirators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

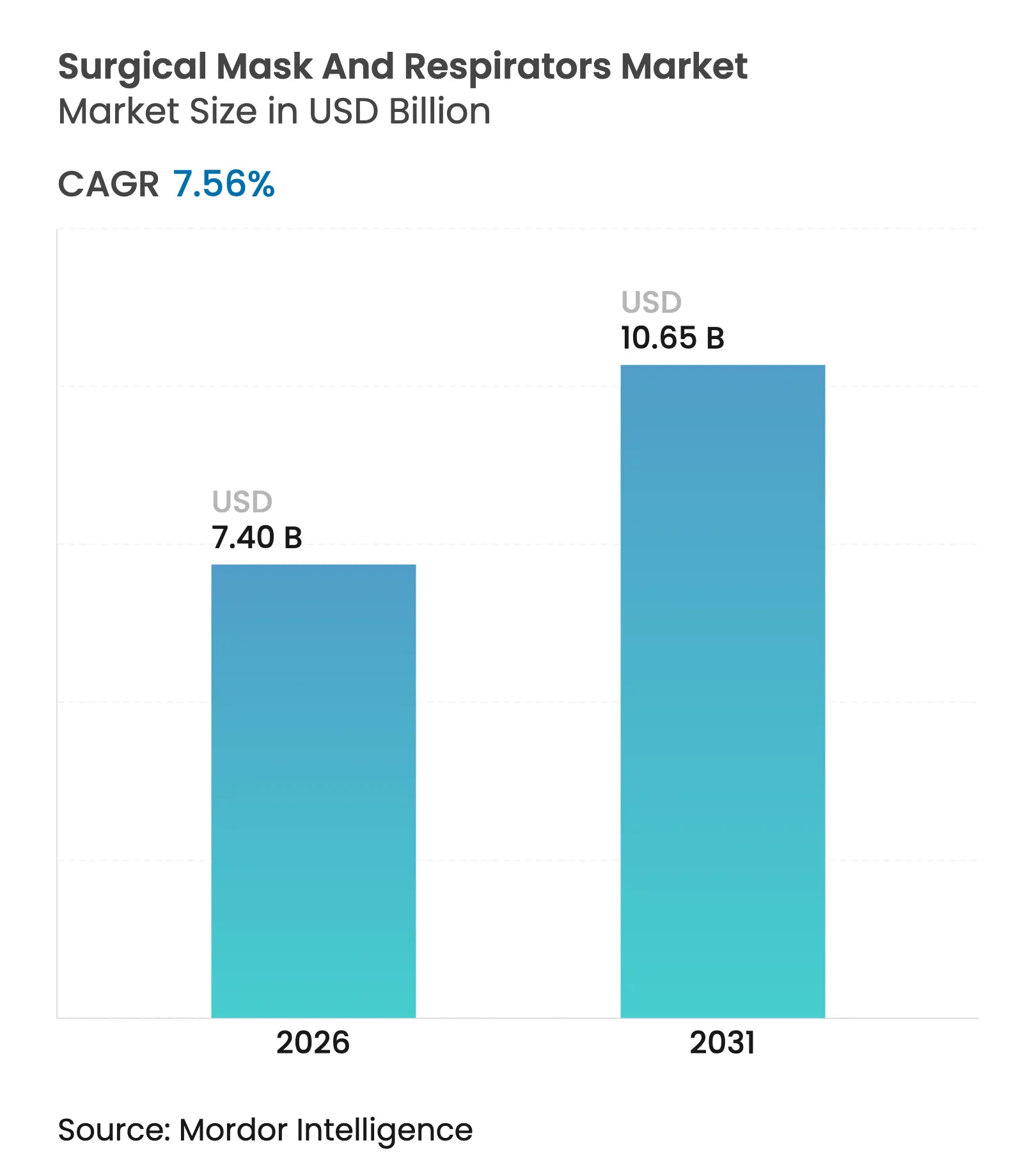

| Market Size (2026) | USD 7.4 Billion |

| Market Size (2031) | USD 10.65 Billion |

| Growth Rate (2026 - 2031) | 7.56 % CAGR |

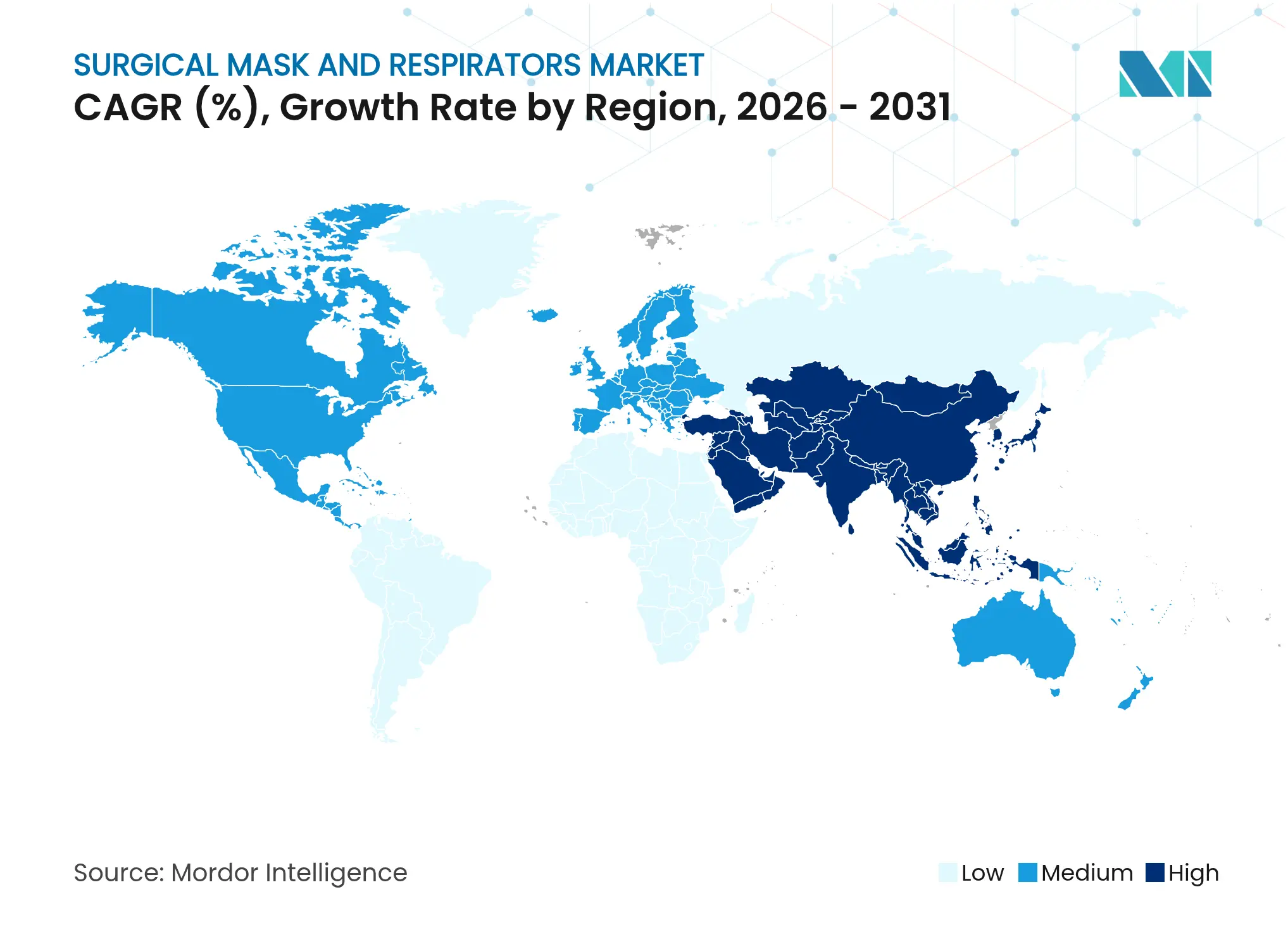

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

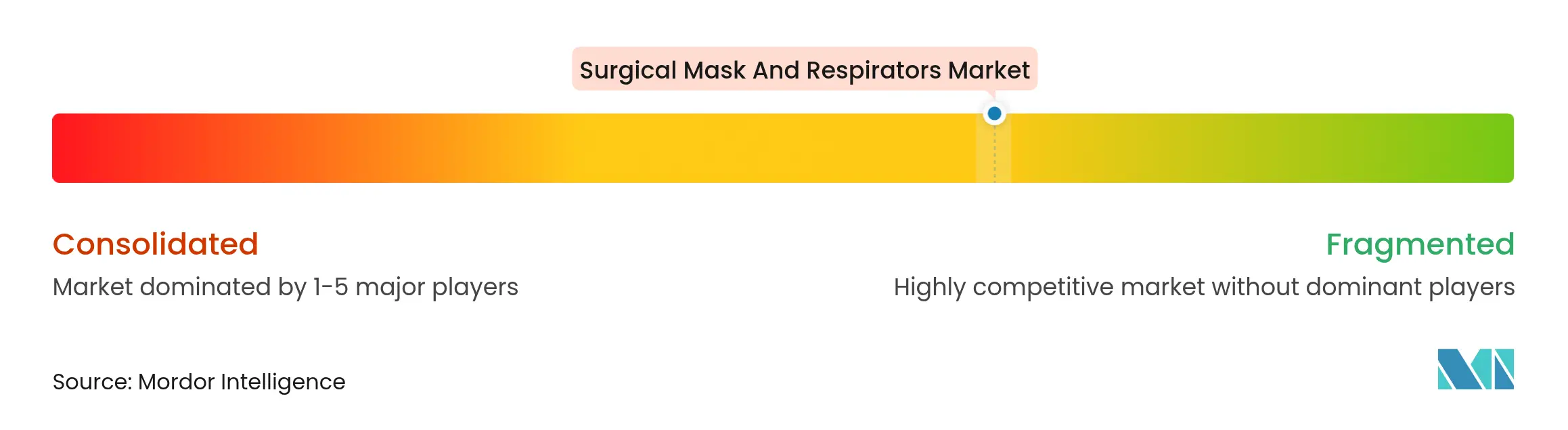

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Surgical Mask And Respirators Market Analysis by Mordor Intelligence

Surgical mask and respirators market size in 2026 is estimated at USD 7.4 billion, growing from 2025 value of USD 6.88 billion with 2031 projections showing USD 10.65 billion, growing at 7.56% CAGR over 2026-2031. Sustained demand arises as hospitals lock in higher baseline inventories, industrial employers comply with strengthened respiratory‐safety rules, and public authorities favor locally anchored supply chains. Infection-control protocols now cover outpatient wings and diagnostic units, lifting routine consumption a full tier above pre-2020 levels. Industrial workplaces add momentum as OSHA broadens audit scope and fines, making tight-fitting respirators the compliance default in many U.S. healthcare-adjacent facilities. Together, these trends encourage long-term contracts, multiyear capacity expansions, and accelerated R&D around lighter materials and better breathability. The market also reflects an incipient pivot toward reusable designs as waste‐management rules tighten and green procurement budgets climb, even while single-use products remain indispensable inside high-risk surgical fields.

Key Report Takeaways

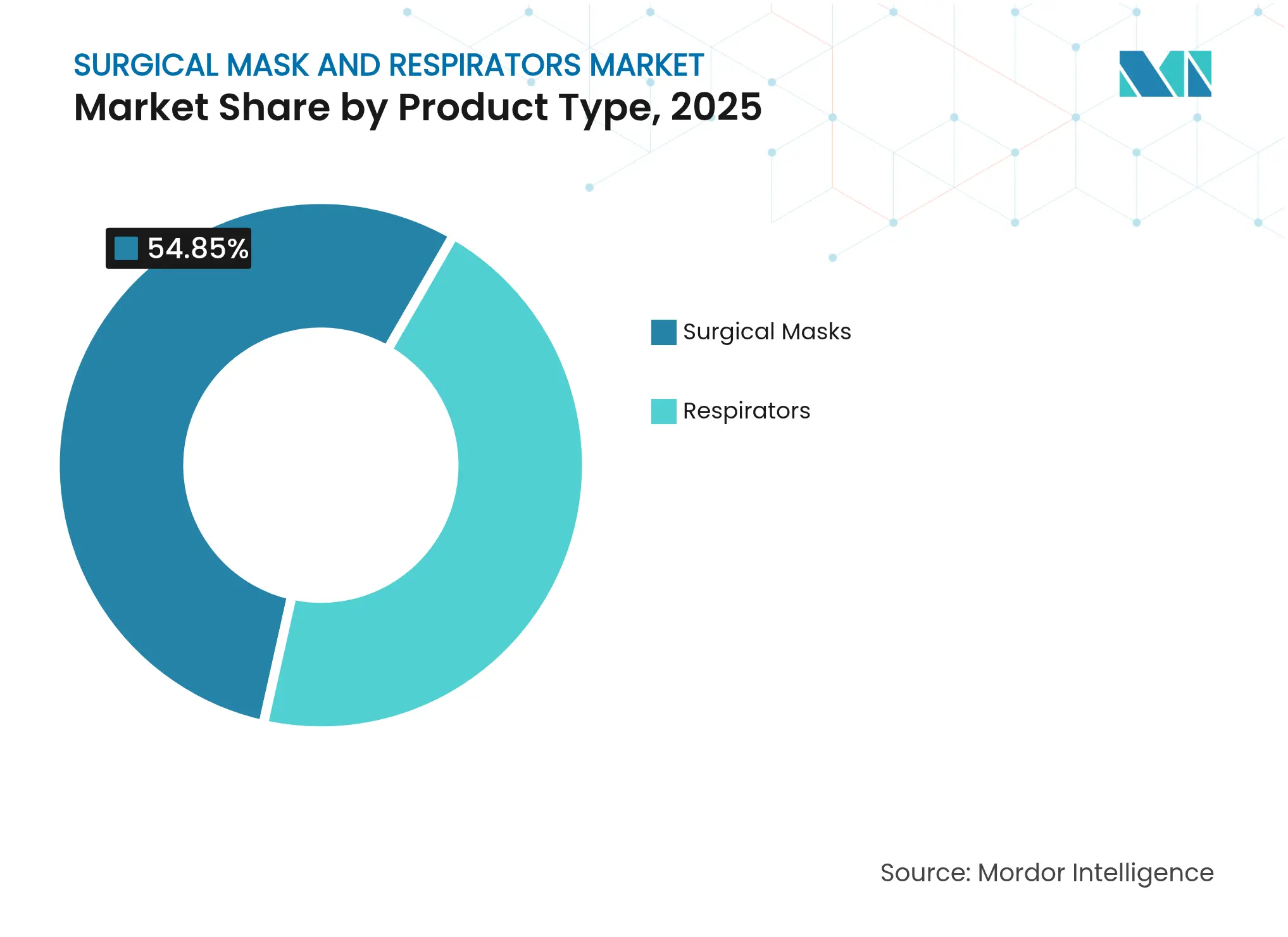

- By product type, surgical masks led with 54.85% of surgical mask and respirators market share in 2025; respirators are projected to post the fastest 7.92% CAGR through 2031.

- By usage, disposable variants captured 32.15% share of the surgical mask and respirators market size in 2025, while reusable solutions are projected to expand at a 6.88% CAGR between 2026 and 2031.

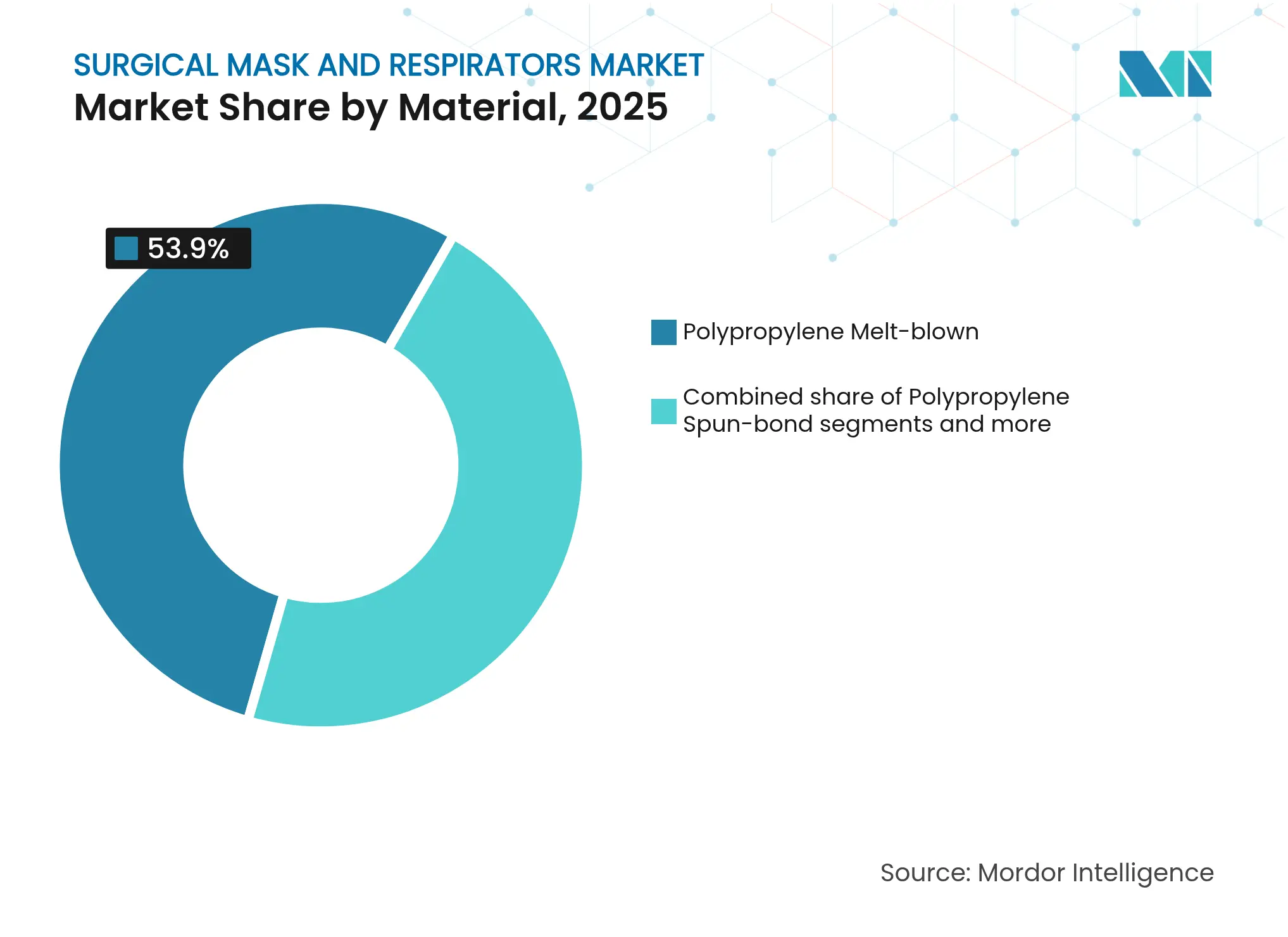

- By material, polypropylene melt-blown filters accounted for 53.90% of surgical mask and respirators market size in 2025; nanofiber media will advance at a brisk 10.25% CAGR through 2031.

- By distribution channel, hospital and surgical supply stores held 48.05% revenue share in 2025; online platforms register the highest forecast CAGR at 8.45% to 2031.

- By geography, Asia-Pacific commanded 37.75% of surgical mask and respirators market share in 2025, and the region is expected to expand at a 9.20% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Mask And Respirators Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent Infection-Control Protocols in Hospitals Stringent Infection-Control Protocols in Hospitals | +2.1% | Global, with higher impact in North America and Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:Global, with higher impact in North America and Europe | Impact Timeline:Medium term (2-4 years) |

OSHA-Mandated Respiratory Protection in U.S. Industrial Healthcare Settings OSHA-Mandated Respiratory Protection in U.S. Industrial Healthcare Settings | +1.7% | North America, with spillover effects in Europe | Short term (≤ 2 years) | |||

Rising Surgical Procedure Volume Rising Surgical Procedure Volume | +1.4% | Global, with concentration in Asia-Pacific and North America | Long term (≥ 4 years) | |||

Growing Burden of Allergies and Airborne Diseases Growing Burden of Allergies and Airborne Diseases | +1.9% | Global, with higher impact in urban centers across all regions | Medium term (2-4 years) | |||

Government-Backed Domestic Mask Production Incentives Government-Backed Domestic Mask Production Incentives | +0.5% | North America, Europe, and select Asia-Pacific countries | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Infection-Control Protocols in Hospitals

Hospitals have broadened mandates for personal protective equipment into outpatient clinics, imaging centers, and rehabilitation wards that rarely demanded surgical-grade barriers before 2024. The California Department of Public Health now requires surgical masks or higher filtration devices throughout every patient-care area, prompting facilities across other U.S. states to mirror the policy for risk-management parity. Average hospital inventory holdings stand 35-40% above pre-pandemic norms, locking in a persistent uplift in purchase volumes. Procurement contracts increasingly specify dual-purpose devices that combine ASTM Level 3 fluid resistance with N95 filtration to streamline stock-keeping units. Manufacturers respond with multi-layer composites that retain breathability even at high filtration ratings, a key differentiator for clinicians working extended shifts. These stricter rules reshape budgeting cycles: PPE now secures a dedicated capital line item rather than remaining an expendable line under consumables, stabilizing year-on-year demand peaks.

OSHA-Mandated Respiratory Protection in U.S. Industrial Healthcare Settings

OSHA's expanded enforcement of respiratory protection standards is transforming workplace safety compliance across U.S. healthcare facilities. The agency's focus has shifted from reactive inspections to proactive compliance verification, resulting in a 47% increase in respiratory protection standard citations since 2024. This regulatory pressure is compelling healthcare employers to implement comprehensive respiratory protection programs, including fit testing and training, which has increased demand for higher-grade respirators. The CDC's updated guidance for SARS-CoV-2 testing in point-of-care settings further reinforces this trend by specifying N95 respirators as essential PPE for personnel involved in testing procedures CDC, 2024[1]Centers for Disease Control and Prevention. "Guidance for SARS-CoV-2 Rapid Testing in Point-of-Care Settings." .

Rising Surgical Procedure Volume

Elective operations rebounded 12% in 2024 as waiting lists cleared, and aging demographics sustain this uplift into 2025. Ambulatory surgical centers gain share, widening the facility base that consumes masks because each operating room crew uses multiple units per case. Device shortages visible in early 2021 have disappeared; the FDA dropped surgical respirators from its shortage catalog in 2025, confirming availability. Higher throughput translates directly into greater per-diem demand, especially for fluid-resistant masks favored in orthopedic, cardiovascular, and transplant theaters. Growth remains most pronounced in Asia-Pacific, where procedure counts climb alongside new hospital construction and rising insurance coverage.

Growing Burden of Allergies and Airborne Diseases

Urban air quality issues and longer respiratory-virus seasons intensify everyday reliance on filtration, transforming surgical masks from episodic pandemic gear into year-round infection-control staples. Clinical protocols now oblige staff treating chronic respiratory patients to wear N95 or surgical masks during peak allergy periods, extending demand into months that historically saw lower usage. Public health advisories in Europe and North America urge higher-filtration respirators for clinicians whenever community transmission rates of influenza or RSV rise. Hospitals adjust by holding surge stockpiles calibrated for seasonal spikes, while industrial buyers implement standing purchase agreements to secure priority allocations in supply crunches[2]California Department of Public Health. "N95 Respirator Masks FAQs - CDPH - CA.gov." .

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Medical-Waste Disposal & Environmental Concerns for Single-Use PPE Medical-Waste Disposal & Environmental Concerns for Single-Use PPE | -0.8% | Global, with higher impact in Europe and North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.8% | Geographic Relevance:Global, with higher impact in Europe and North America | Impact Timeline:Medium term (2-4 years) |

End-User Compliance Issues Due to Fit-Factor Discomfort End-User Compliance Issues Due to Fit-Factor Discomfort | -0.6% | Global | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Medical-Waste Disposal & Environmental Concerns for Single-Use PPE

Disposable masks generate polypropylene waste that heightens landfill volumes and microplastic leakage, prompting environmental agencies to pressure hospitals to curtail single-use consumption. Lifecycle assessments indicate carbon-footprint reductions of up to 12% when facilities shift to reusable options. The European Union’s 2025 revision of EN 14683 links mask performance to sustainability metrics, encouraging procurement officers to experiment with washable or biodegradable variants. Waste-management costs also rise: several U.S. states introduced surcharges on regulated medical waste in 2024, nudging buyers to rethink reliance on disposables. Consequently, disposable volumes experience incremental substitution from reusable designs, tempering overall unit growth even as revenue expands.

End-User Compliance Issues Due to Fit-Factor Discomfort

Lengthy surgical sessions strain wearer tolerance. Surveys show mask re-wearing climbed as high as 40% post-pandemic, cutting into projected replacement volumes because staff attempt to mitigate discomfort. The drop in surgical tie-mask usage—from 87% pre-2020 to 71% in 2024—signals unresolved ergonomic gaps. Research teams now prototype 3D-printed frames that contour to individual faces, offering 95% filtration without traditional fit-tests. Adoption of such innovations will repair compliance over time, but near-term demand growth posts a modest drag as professionals stretch usage intervals.

Segment Analysis

By Product Type: Higher-Filtration Respirators Narrow the Lead of Traditional Masks

Surgical masks retained a 54.85% hold on the surgical mask and respirators market in 2025, yet respirators are forecast to capture outsized incremental value with an 7.92% CAGR across 2026-2031. The shift traces to rising awareness of aerosolized pathogens and OSHA’s push for fit-tested devices in clinical laboratories. Within respirators, N95 remains the workhorse thanks to a proven balance between filtration efficiency and breathability; powered air-purifying respirators carve a premium niche where heat stress or prolonged exposure warrants powered airflow. Phasing out emergency authorizations for non-NIOSH imports redirects demand toward certified domestic lines, solidifying pricing power for compliant suppliers.

Surgical masks evolve in parallel. Fluid-resistant variants gain share inside operating rooms as surgeons place a premium on splash protection and anti-fog coatings that maintain clear sightlines through loupes and shields. A sustained uptick in N95 usage inside theatres—from 4% pre-2020 to 13% by 2024—illustrates the blurring boundary between mask classes. Innovation focuses on softer inner liners and anti-fog nose bridges that mitigate lens fogging, boosting adoption among ophthalmic and orthopedic teams. The dual-use trend underpins stable revenue for incumbents while creating headroom for newcomers with differentiated design patents.

Note: Segment shares of all individual segments available upon report purchase

By Usage: Reusable Designs Challenge Disposable Dominance

Disposable units accounted for 32.15% of surgical mask and respirators market size in 2025, anchored by infection-control protocols that prioritize single-use barriers. Yet reusable formats ride a 6.88% CAGR as environmental metrics make headlines and hospitals reckon with escalating waste-haul fees. Early adopters quantify total cost of ownership and find that multi-cycle devices deliver savings once they surpass 25-30 reuse cycles, a threshold reachable under high-procedure workloads.

Manufacturers accelerate improvements in cleanability, creating masks that tolerate vapor-phase hydrogen peroxide or autoclave cycles without filtration loss. Georgia Tech’s custom-fit reusable design achieves 95% filtration while eliminating the expense of annual fit-tests, a compelling proposition for procurement managers. Reusable uptake also benefits from donor-funded sustainability targets: several European health systems now mandate that at least 25% of annual PPE spend go to low-environmental-impact products, a clause routinely satisfied with washable masks.

By Material: Nanofiber Technology Disrupts Conventional Melt-Blown Media

Polypropylene melt-blown substrates still dominate with 53.90% share because the installed base of high-output lines favors cost-efficient large-volume runs. However, nanofiber sheets exhibit a 10.25% CAGR to 2031 on the strength of higher filtration at lower pressure drops—a critical advantage as users seek breathable devices for long shifts. Comparative trials show nanofibers sustain 99% filtration even after ethanol cleaning, enabling reusable pathways that classical melt-blown cannot match.

Material scientists pursue bicomponent core-sheath structures that reduce airflow resistance 30-40%, expanding suitability for pediatric and geriatric care where breathing effort is critical. The U.S. National Nanotechnology Initiative’s record USD 2.2 billion 2025 budget underscores political will to accelerate such breakthroughs. Concurrently, biodegradable blends using polylactic acid allow composting within 28 days while retaining KF94-equivalent performance, answering regulators that tie public tenders to end-of-life credentials.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Online Platforms Capture Post-Crisis Momentum

Hospital and surgical supply stores retained 48.05% revenue share in 2025, supported by group purchasing contracts and integrated logistics footprints that guarantee just-in-time delivery. Yet online platforms exhibit an 8.45% CAGR as purchasing managers keep secondary relationships forged during 2020 supply crunches. Direct-to-institution portals compress procurement cycles, aggregate real-time inventory data, and bypass tiered distributors when emergency needs arise.

The channel map increasingly bifurcates. Primary wholesalers focus on high-volume, multi-SKU contracts bundled with sterilization wraps and gowns, while secondary distributors offer niche respirators, alternate sizes, and rapid-delivery guarantees to smaller clinics. Manufacturers hedge by operating brand-owned e-commerce portals to defend margins and collect end-user feedback, turning logistics proficiency into a competitive moat.

Geography Analysis

Asia-Pacific held 37.75% of surgical mask and respirators market share in 2025 and is projected to advance at a leading 9.20% CAGR through 2031. The region couples deep manufacturing clusters with expanding healthcare insurance coverage, especially in China, India, and Southeast Asia. Taiwan’s government-orchestrated scale-up from 1.8 million to 20 million masks daily during the pandemic proved regional agility and left a lasting surplus of automated lines ready for export quotas. Rising medical tourism in Thailand and accelerated hospital build-outs in India add downstream consumption, reinforcing internal demand loops.

North America remains innovation-driven. Tariffs on Chinese PPE rose from 7.5% to 25% in 2024 and will climb to 50% by 2026, redirecting orders to regional plants and joint ventures. Washington’s USD 95 million commitment to domestic capacity, plus OSHA’s hardened enforcement stance, ensures that higher-filtration respirators remain a baseline requirement nationwide. Canadian provinces likewise channel pandemic-era contingency funds into regional tooling, creating a North American buffer against global supply swings.

Europe differentiates on sustainability and harmonized standards. The revised EN 14683:2025 embeds environmental criteria, steering procurement teams toward reusable or biodegradable designs. Fragmented private investment—60% of exporting firms report barriers—led the European Investment Bank to expand public loan programs focused on green medical supplies. As a result, the region’s manufacturers emphasize closed-loop recycling schemes and low-carbon substrates as key brand pillars.

Competitive Landscape

Market Concentration

Industry concentration is moderate. 3M, Honeywell, and Kimberly-Clark leverage vertical integration, proprietary filtration media, and global distribution to anchor share. Each pivots toward higher-margin surgical respirators that blend ASTM Level 3 fluid protection with NIOSH filtration ratings. 3M’s planned spin-off of its Health Care unit will crystallize a dedicated personal-safety champion with sharpened R&D focus. Honeywell layers proprietary facial-mapping algorithms into its SmartFit line, aiming to remove manual fit-testing bottlenecks. Kimberly-Clark embeds transparent breathing chambers to improve intra-operative communication, a critical ergonomic differentiator.

Mid-tier players exploit supply-chain reshoring. Owens & Minor widens its respiratory catalog through acquisitions such as Rotech, seeking cross-selling into durable medical equipment channels. Cardinal Health positions antimicrobial silver-ion masks for high-infection wards, meeting hospitals’ multi-pathogen protocols. Quality oversight remains pivotal: FDA’s Class 2 recall of O&M Halyard masks in December 2024 highlights reputational stakes tied to bioburden compliance.

Start-ups focused on nanofiber and biodegradable substrates secure venture backing as health systems embed sustainability clauses. Several Asian contract manufacturers diversify into own-label exports as tariff walls erode the cost advantage of cross-Pacific shipping. Overall, competitive pressure intensifies around fit comfort, filtration durability, and eco-profile—factors that now inform tender scoring frameworks alongside unit price.

Surgical Mask And Respirators Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The European Union implemented the updated medical face mask standard (BS EN 14683:2025), introducing stricter microbial cleanliness tests, refined bacterial filtration efficiency methodologies, and new guidelines for transparent surgical masks to improve communication in operating rooms

- February 2025: The U.S. Department of Health and Human Services allocated USD 95 million in FY 2025 to expand domestic production of medical countermeasures, including surgical masks and respirators for healthcare facilities, and improve supply chain visibilit

Table of Contents for Surgical Mask And Respirators Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Stringent Infection-Control Protocols in OECD Hospitals

- 4.2.2Pandemic-Preparedness Stockpiling Initiatives across Asia

- 4.2.3OSHA-Mandated Respiratory Protection in U.S. Industrial Healthcare Settings

- 4.2.4Rising Surgical Procedure Volume in Middle-Income Economies

- 4.2.5Government-Backed Domestic Mask Production Incentives (e.g., U.S. DPA, EU IPCEI)

- 4.3Market Restraints

- 4.3.1Medical-Waste Disposal & Environmental Concerns for Single-Use PPE

- 4.3.2Polypropylene Price Volatility Impacting Margin Stability

- 4.3.3End-User Compliance Issues Due to Fit-Factor Discomfort

- 4.3.4Proliferation of Low-Cost Counterfeit Respirators Undermining Brand Equity

- 4.4Value/ Supply-Chain Analysis

- 4.5Regulatory Outlook

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Surgical Masks

- 5.1.1.1Basic Surgical Masks

- 5.1.1.2Anti-Fog Surgical Masks

- 5.1.1.3Fluid / Splash-Resistant Surgical Masks

- 5.1.2Respirators

- 5.1.2.1N95 Respirators

- 5.1.2.2N99 & N100 Respirators

- 5.1.2.3FFP1, FFP2, FFP3 Respirators

- 5.1.2.4Powered Air-Purifying Respirators (PAPRs)

- 5.2By Usage

- 5.2.1Disposable

- 5.2.2Reusable

- 5.3By Material

- 5.3.1Polypropylene Melt-blown

- 5.3.2Polypropylene Spun-bond

- 5.3.3Cotton & Polyester Blends

- 5.3.4Others (Activated Carbon, Nanofiber, etc.)

- 5.4By Distribution Channel

- 5.4.1Hospital & Surgical Supply Stores

- 5.4.2Retail Pharmacies & Drug Stores

- 5.4.3Online Platforms

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2France

- 5.5.2.3United Kingdom

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4South America

- 5.5.4.1Brazil

- 5.5.4.2Argentina

- 5.5.4.3Rest of South America

- 5.5.5Middle East and Africa

- 5.5.5.1GCC

- 5.5.5.2South Africa

- 5.5.5.3Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank / Share for key companies, Products & Services, and Recent Developments)

- 6.3.13M Company

- 6.3.2Honeywell International Inc.

- 6.3.3Kimberly-Clark Corporation

- 6.3.4Cardinal Health Inc.

- 6.3.5Medline Industries LP

- 6.3.6Owens & Minor Inc.

- 6.3.7Ansell Ltd.

- 6.3.8Halyard Health Inc.

- 6.3.9Alpha Pro Tech Ltd.

- 6.3.10Prestige Ameritech

- 6.3.11Moldex-Metric Inc.

- 6.3.12Shanghai Dasheng Health Products Mfg. Co., Ltd.

- 6.3.13Makrite Industries Inc.

- 6.3.14BYD Company Ltd

- 6.3.15Draeger Safety AG & Co. KGaA

- 6.3.16Teleflex Incorporated

- 6.3.17Ambu A/S

- 6.3.18Winner Medical Co. Ltd.

- 6.3.19DACH Schutzbekleidung GmbH & Co. KG

- 6.3.20Bullard

- 6.3.21Lakeland Industries Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Surgical Mask And Respirators Market Report Scope

As per the scope of the report, a surgical mask refers to a single-use filtration device made of fabric and worn over the nose and mouth of surgical staff to prevent contamination of the operative field and to protect the wearer from splashes and splatter whereas a respirator is an apparatus worn over the mouth and nose or the entire face to prevent the inhalation of dust, smoke, or other noxious substances. The Surgical Mask and Respirators Market is Segmented by Type (Masks and Respirators), Distribution Channel (Hospitals and Clinic, Drug Stores, and Online Stores), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.