Ultrasonic Scalpel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.91 Billion |

| Market Size (2031) | USD 4.23 Billion |

| Growth Rate (2026 - 2031) | 7.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrasonic Scalpel Market Analysis by Mordor Intelligence

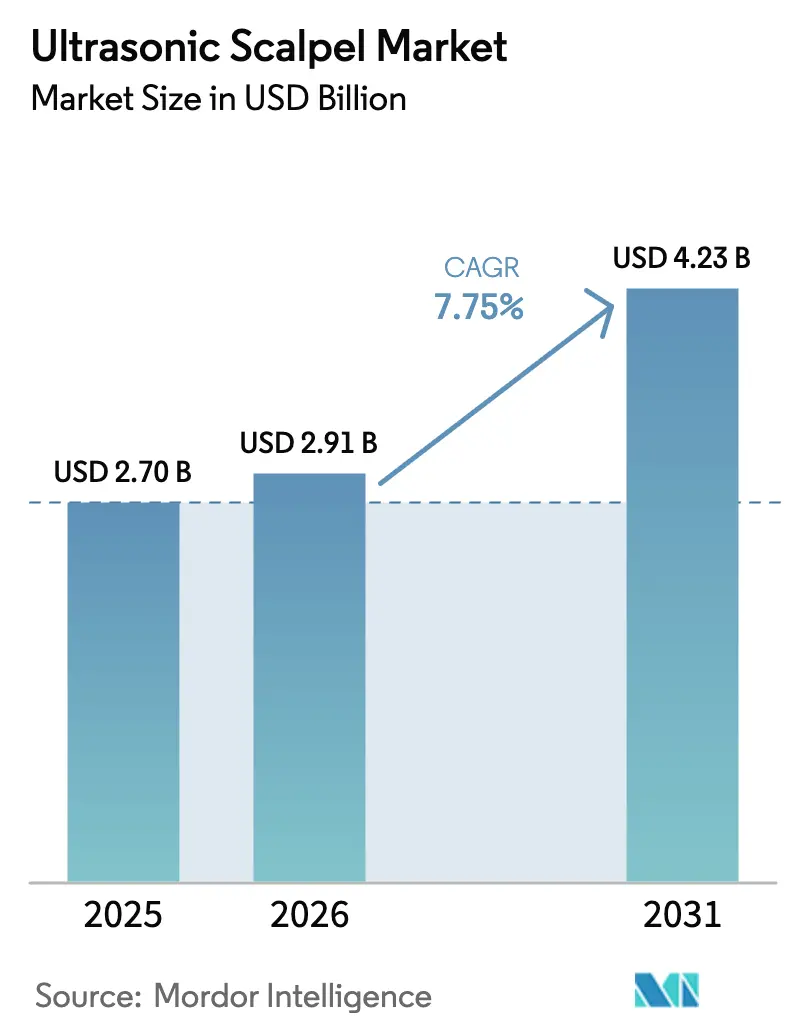

The Ultrasonic Scalpel Market size was valued at USD 2.70 billion in 2025 and is estimated to grow from USD 2.91 billion in 2026 to reach USD 4.23 billion by 2031, at a CAGR of 7.75% during the forecast period (2026-2031).

Rising adoption of robotic surgery, localization incentives in China and India, and value-based purchasing models that reward reloadable handpieces are accelerating procurement decisions across high-volume surgical centers. Fixed-frequency systems still dominate routine procedures, yet adaptive tissue-sensing and cordless platforms are redefining ergonomic and cost expectations. Tariffs on piezo-ceramic inputs, sustainability mandates favoring reusable instruments, and bundled payment pressures are reshaping total cost-of-ownership calculations, prompting hospitals to look beyond upfront capital pricing. Rapid regulatory clearances for hybrid generators that merge ultrasonic and bipolar modes are expanding the addressable ultrasonic scalpel market, particularly for complex oncology and cardiovascular cases that demand reliable vessel sealing.

Key Report Takeaways

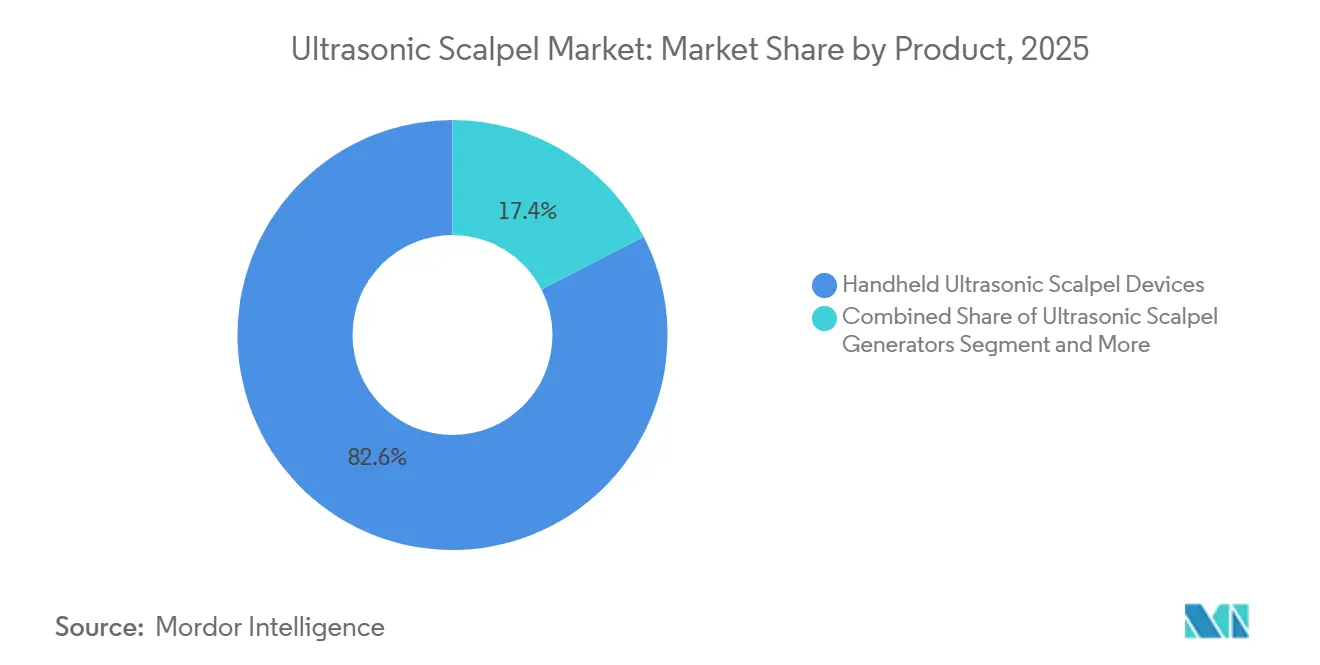

- By product, handheld ultrasonic devices led with 82.56% revenue share in 2025; generators are projected to post an 8.25% CAGR through 2031.

- By technology, fixed-frequency platforms captured 42.53% of 2025 revenue, while cordless battery systems are forecast to expand at a 10.85% CAGR to 2031.

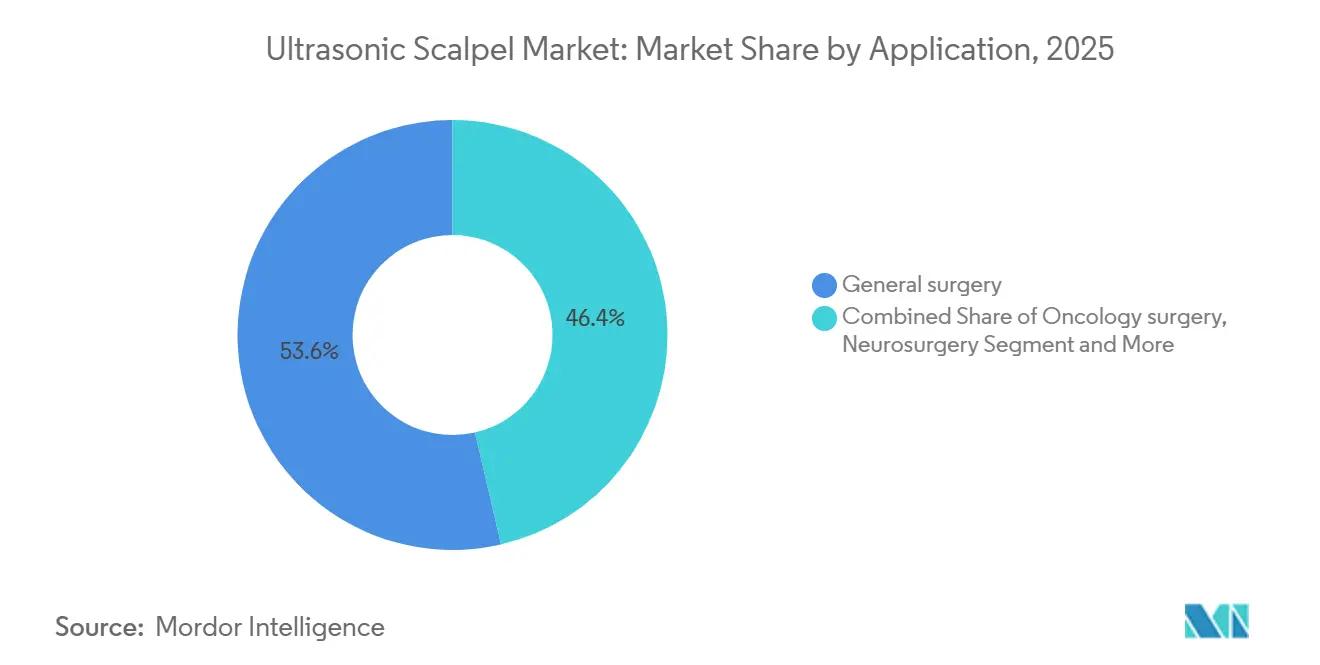

- By application, general surgery accounted for 53.63% of the ultrasonic scalpel market share in 2025 and neurosurgery is advancing at a 9.87% CAGR through 2031.

- By end-user, hospitals held 68.33% of 2025 spending; ambulatory surgical centers are growing at an 8.7% CAGR to 2031.

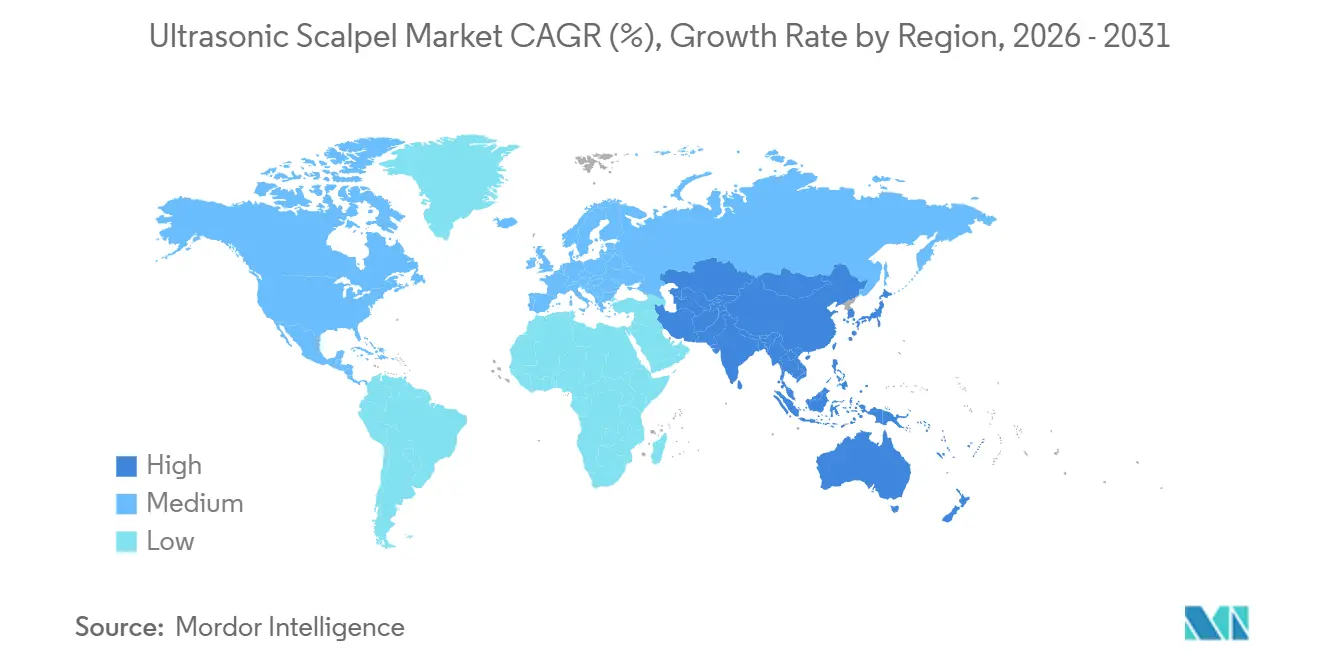

- By geography, North America retained 38.13% share in 2025, whereas Asia-Pacific is set to climb at a 9.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ultrasonic Scalpel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic diseases | +1.2% | Global, strongest in North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Increased demand for minimally invasive procedures | +1.5% | Global, led by North America and Western Europe, rising in Asia-Pacific | Medium term (2-4 years) |

| Rapid technology upgrades in ultrasonic energy platforms | +1.3% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Integration with robotic surgical systems accelerates adoption | +1.8% | North America, Europe, Japan, South Korea, Australia | Short term (≤ 2 years) |

| Value-based purchasing bundles boost reloadable handpiece uptake | +0.9% | North America, select European markets | Medium term (2-4 years) |

| China / India localization incentives lowering device costs | +1.1% | China, India, spill-over to Southeast Asia and Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases

Growing incidence of cancer, cardiovascular disease, and metabolic disorders is lifting surgical volumes worldwide. The World Health Organization projects that non-communicable diseases will account for 73% of global deaths by 2030[1]World Health Organization, “Noncommunicable Diseases,” WHO Fact Sheets, who.int. Rising case counts translate into more oncologic and bariatric procedures, both of which depend on energy devices that combine cutting and coagulation with minimal thermal spread. A 2024 systematic review showed that ultrasonic scalpels delivered higher lymph-node yields in thyroid and colorectal cancer cases than conventional electrosurgery. Higher nodal harvest improves staging accuracy, encouraging oncology departments to standardize on ultrasonic platforms. Demand is most pronounced in countries with robust screening programs that detect early-stage tumors amenable to curative surgery.

Increased Demand for Minimally Invasive Procedures

Patient preference for faster recovery drives the migration from open to laparoscopic and robotic approaches, boosting the ultrasonic scalpel market. These procedures require devices that seal vessels up to 7 mm within confined spaces. Ultrasonic platforms meet the threshold reliably while limiting collateral thermal damage. FDA clearance of Intuitive Surgical’s Vessel Sealer Curved in July 2025 demonstrates how robotic accessories tailor ultrasonic energy to unique dissection planes. Hospital buyers now bundle energy devices with multi-year robotic service contracts, locking manufacturers into long-tail consumable revenue.

Rapid Technology Upgrades in Ultrasonic Energy Platforms

Second-generation systems modulate power based on tissue impedance, improving efficiency. Olympus launched its THUNDERBEAT II in October 2025, enabling surgeons to toggle among ultrasonic, bipolar, and hybrid modes. Cordless handpieces such as Medtronic’s Sonicision remove cable clutter and simplify sterilization, key benefits for outpatient centers. Shorter instrument exchange times, estimated at 8–12 minutes per case, improve throughput in high-volume operating rooms.

Integration with Robotic Surgical Systems Accelerates Adoption

Robotic platforms are becoming essential for complex minimally invasive procedures. CMR Surgical’s Versius and Medtronic’s Hugo gained FDA clearance in late 2024, both allowing third-party ultrasonic devices. Hospitals favor open-architecture systems that avoid vendor lock-in and standardize energy sources across procedures. Early regulatory clearance and surgeon training programs give leading device makers a first-mover edge in high-throughput robotic suites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global regulatory pathways | -0.8% | U.S., China, Japan | Medium term (2-4 years) |

| High capital & consumable costs | -0.6% | Latin America, Southeast Asia, budget-constrained Europe | Long term (≥ 4 years) |

| New tariffs on piezo-ceramic crystals inflate BOM costs | -0.5% | North America, Europe | Short term (≤ 2 years) |

| Procedure-bundled payment cuts squeeze hospital budgets | -0.4% | North America, select Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Regulatory Pathways

FDA 510(k) clearances average 6–10 months when a suitable predicate exists, while De Novo routes can extend beyond 18 months. Ethicon’s Total Energy System, cleared in January 2025, illustrates the time and data requirements even for incremental upgrades. China’s NMPA adds another 18–24 months of local clinical trials for Class III devices, raising entry hurdles for smaller firms. Europe’s Medical Device Regulation imposes unannounced audits that have forced some legacy models off the market. These layered reviews delay product launches and inflate development budgets.

High Capital & Consumable Costs

Ultrasonic generators cost USD 25,000–60,000, reusable handpieces USD 3,000–8,000, and single-use devices USD 200–400 per procedure. Hospitals in Latin America and Southeast Asia often default to monopolar electrosurgery, requiring only a USD 5,000–10,000 generator. Reusable ultrasonic systems achieve cost parity at 300 cases per year, but many facilities lack sterilization capacity. As a result, adoption in emerging markets lags despite falling hardware prices, capping near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Reusable Handpieces Drive Sustainability Shift

The ultrasonic scalpel market size for handheld devices dominated with an 82.56% share in 2025, underscoring their central role in hemostasis across surgical specialties. Hospitals are pivoting toward reusable configurations, encouraged by lifecycle studies that report a 69% lower carbon footprint and six-digit cost savings after 200 uses. Single-use disposables remain prevalent in ambulatory centers lacking sterilization infrastructure, yet their slice of the ultrasonic scalpel market is narrowing as modular designs let users replace blades while retaining the core handpiece.

Ultrasonic generators are forecast to expand at an 8.25% CAGR through 2031, fueled by hybrid towers that combine ultrasonic and bipolar radiofrequency modes. These multipurpose consoles reduce operating-room clutter and simplify staff training. Accessories—blades, tips, irrigation tubing, and footswitches—sustain high-margin recurring revenue. Hospitals increasingly bundle these consumables within long-term capital contracts, guaranteeing supply continuity and predictable per-case economics.

By Technology: Cordless Systems Redefine Ergonomics

Fixed-frequency units still accounted for 42.53% of 2025 technology revenue, valued for predictable performance and lower capital costs. Adaptive tissue-sensing platforms, however, are carving share by automatically adjusting blade amplitude to tissue impedance, a feature prized in complex oncology resections. Cordless battery-powered devices, the fastest-growing subsegment at a 10.85% CAGR, are reshaping workflow expectations as surgeons demand cable-free ergonomics in laparoscopic and robotic settings[3]Medtronic, “Sonicision Cordless Ultrasonic Dissection Device,” medtronic.com.

Battery innovations now permit 60–80 activations per charge while keeping handpiece weight under 250 grams, satisfying outpatient case requirements. Limitations persist for marathon bariatric or hepatobiliary cases, yet iterative battery density upgrades are closing the gap. Premium adaptive platforms, priced up to 50% above fixed-frequency systems, justify their premium by shaving 8–12 minutes off average procedure durations, a critical benefit for high-turnover sites.

By Application: Neurosurgery Leads Growth Amid Robotic Integration

General surgery generated 53.63% of ultrasonic scalpel market revenue in 2025, reflecting high procedure volumes of cholecystectomy, hernia repair, and colorectal resection. Oncologic procedures rank second, buoyed by evidence that ultrasonic dissection improves lymph-node harvest and staging accuracy. Neurosurgery, though smaller in absolute value, is forecast to expand at a 9.87% CAGR through 2031, outpacing all other applications. The rise of robotic navigation paired with intraoperative ultrasound is broadening the use of ultrasonic aspirators for brain and spinal tumor debulking[2]Integra LifeSciences, “Integra LifeSciences Reports Third Quarter 2024 Financial Results,” integralife.com.

Bariatric surgery demand is climbing on the back of epidemic obesity and payer coverage expansion, pushing ultrasonic scalpels into sleeve gastrectomy workflows. Cardiovascular and thoracic applications, while niche, are growing steadily as minimally invasive valve repair and lobectomy techniques proliferate. Plastic, gynecologic, and urologic procedures complete the portfolio, each tracking overall surgical volume growth with a tilt toward outpatient settings that favor cordless devices.

By End-User: ASCs Capture Outpatient Migration

Hospitals represented 68.33% of 2025 spending, anchored by complex oncology, cardiovascular, and neurosurgical volumes that rely on sophisticated energy platforms. Budget pressure from bundled payments, however, is driving consignment models in which vendors retain generator ownership and charge per activation, mitigating capital outlay. Ambulatory surgical centers are projected to grow at an 8.7% CAGR as same-day bariatric, general, and gynecologic surgeries migrate from inpatient floors.

ASCs value equipment portability and intuitive user interfaces that shorten staff training curves, making cordless systems attractive. Specialty clinics, though the smallest segment, are rising as physicians capture facility fees by shifting procedures in-house. Single-use ultrasonic devices dominate in these settings to avoid sterilization investment, but their share may erode as compact tabletop sterilizers gain traction.

Geography Analysis

North America commanded 38.13% of 2025 revenue, propelled by widespread robotic surgery use and reimbursement models that reward reusable handpieces. Medicare’s BPCI-Advanced covers 32 surgical episodes, influencing hospital procurement toward devices that minimize consumable spending. Intuitive Surgical’s Vessel Sealer Curved clearance in July 2025 strengthened the pull-through effect for compatible ultrasonic consumables. Tariff-induced cost increases on rare-earth components have squeezed supplier margins, prompting accelerated qualification of Japanese and Vietnamese crystal vendors.

Europe’s share has flattened due to the June 2025 International Procurement Instrument, which limits China-origin devices to 50% of public tender value. Germany, the United Kingdom, and France lead adoption of reusable platforms that dovetail with sustainability targets. Olympus posted 9.8% revenue growth in its EMEA region for fiscal 2024 on the back of THUNDERBEAT rollouts. Central and Eastern European countries are upgrading from monopolar electrosurgery using EU structural funds, creating a two-step adoption path that begins with fixed-frequency units before migrating to adaptive systems.

Asia-Pacific is forecast to post a 9.51% CAGR, the highest of any region. China and India account for the bulk of demand, underpinned by localization incentives that compress device pricing by up to 30%. Medtronic recorded 8.8% revenue growth in China and 8.4% in wider emerging markets during fiscal 2025 Q2, illustrating the payoff of regional manufacturing. Japan, Australia, and South Korea continue to upgrade to adaptive, robot-compatible platforms, while Southeast Asia sees rising demand from medical tourism. Middle East & Africa and South America remain nascent but show pockets of acceleration in Gulf Cooperation Council states and Brazil, where private hospitals differentiate through advanced minimally invasive capabilities.

Competitive Landscape

The top suppliers, including Ethicon, Medtronic, Olympus, Stryker, and Integra LifeSciences, control a significant percentage of the global ultrasonic scalpel market revenue, indicating moderate market concentration. Ethicon’s Harmonic line remains the clinical standard, yet its tight coupling with the da Vinci ecosystem limits cross-platform reach and opens space for Medtronic’s Hugo and CMR Surgical’s Versius, both of which accept third-party handpieces. Smaller challengers such as Söring, BOWA, Lepu Medical, and Wuhan BBT compete on price, offering fixed-frequency systems at 30–40% discounts.

Innovation clusters around cordless architecture and hybrid energy towers. Ethicon’s recent patent covers jaw clamping pressures between 60 and 210 psi, creating formidable materials-science barriers for entrants. FDA’s Safety and Performance Based Pathway accelerates submissions that prove substantial equivalence, shaving 3–6 months off time-to-market. Tariff headwinds have spurred sourcing diversification, but validation timelines temper quick pivots. Meanwhile, sustainability agendas push vendors to emphasize reusable designs, shifting competition toward sterilization protocol robustness and service-contract economics rather than headline device price.

Emerging disruptors concentrate on ambulatory surgical center needs, marketing cordless ultrasonic scalpels with simplified user interfaces and disposable sheaths that eliminate reprocessing. Nami Surgical, for instance, opened a USD 10 million Series A round in August 2025 to commercialize a miniaturized ultrasonic scalpel tailored to robotic arms. Strategic alliances between robot manufacturers and energy-device specialists are likely as interoperability becomes a prime purchasing criterion.

Ultrasonic Scalpel Industry Leaders

Medtronic PLC

Olympus Corporation

Stryker Corporation

Ethicon (J&J)

Integra LifeSciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Glasgow-based Nami Surgical opened a USD 10 million Series A round to advance its miniaturized ultrasonic scalpel for robotic-assisted surgery.

- April 2025: IMPLANET highlighted OLEA, an ultrasonic osteotome that enables controlled bone removal while sparing soft tissue.

Global Ultrasonic Scalpel Market Report Scope

As per the scope of the report, ultrasonic scalpels, also known as harmonic scalpels, are surgical instruments that are used to simultaneously cut and cauterize tissue through the utilization of ultrasonic vibrations.

The segmentation for the ultrasonic scalpel market by product includes handheld ultrasonic scalpel devices, which are further categorized into reusable systems and single-use (disposable) devices. Ultrasonic scalpel generators are segmented into hybrid energy generators (ultrasonic + bipolar) and standalone ultrasonic generators. Accessories and consumables include blades/tips, irrigation and suction sets, and footswitches and cables. By technology, the market is segmented into fixed-frequency systems, adaptive tissue-sensing systems, and cordless battery-powered systems. By application, the segmentation includes general surgery, oncology surgery, cardiovascular and thoracic surgery, bariatric and metabolic surgery, neurosurgery, and other applications. By end-user, the market is segmented into hospitals, ambulatory surgical centers, and specialty clinics. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Handheld Ultrasonic Scalpel Devices | Reusable systems |

| Single-use (disposable) devices | |

| Ultrasonic Scalpel Generators | Hybrid energy generators (ultrasonic + bipolar) |

| Standalone ultrasonic generators | |

| Accessories & Consumables | Blades / tips |

| Irrigation & suction sets | |

| Footswitches & cables |

| Fixed-frequency systems |

| Adaptive tissue-sensing systems |

| Cordless battery-powered systems |

| General surgery |

| Oncology surgery |

| Cardiovascular & thoracic surgery |

| Bariatric & metabolic surgery |

| Neurosurgery |

| Other applications |

| Hospitals |

| Ambulatory surgical centres |

| Specialty clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Handheld Ultrasonic Scalpel Devices | Reusable systems |

| Single-use (disposable) devices | ||

| Ultrasonic Scalpel Generators | Hybrid energy generators (ultrasonic + bipolar) | |

| Standalone ultrasonic generators | ||

| Accessories & Consumables | Blades / tips | |

| Irrigation & suction sets | ||

| Footswitches & cables | ||

| By Technology | Fixed-frequency systems | |

| Adaptive tissue-sensing systems | ||

| Cordless battery-powered systems | ||

| By Application | General surgery | |

| Oncology surgery | ||

| Cardiovascular & thoracic surgery | ||

| Bariatric & metabolic surgery | ||

| Neurosurgery | ||

| Other applications | ||

| By End-User | Hospitals | |

| Ambulatory surgical centres | ||

| Specialty clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the ultrasonic scalpel market in 2026?

The ultrasonic scalpel market size stands at USD 2.91 billion in 2026.

What is the expected growth rate for ultrasonic scalpels through 2031?

The market is projected to expand at a 7.75% CAGR, reaching USD 4.23 billion by 2031.

Which product segment grows fastest over the forecast horizon?

Ultrasonic generators, enabled by hybrid energy platforms, are forecast to grow at an 8.25% CAGR.

Why are ambulatory surgical centers important for future demand?

ASCs are shifting same-day bariatric and general surgery volumes from hospitals, driving an 8.7% CAGR in ultrasonic scalpel spending among these facilities.

Which region exhibits the highest growth potential?

Asia-Pacific leads with a projected 9.51% CAGR, fueled by localization incentives in China and India.

Page last updated on: