Ultrasound Probe Cover Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

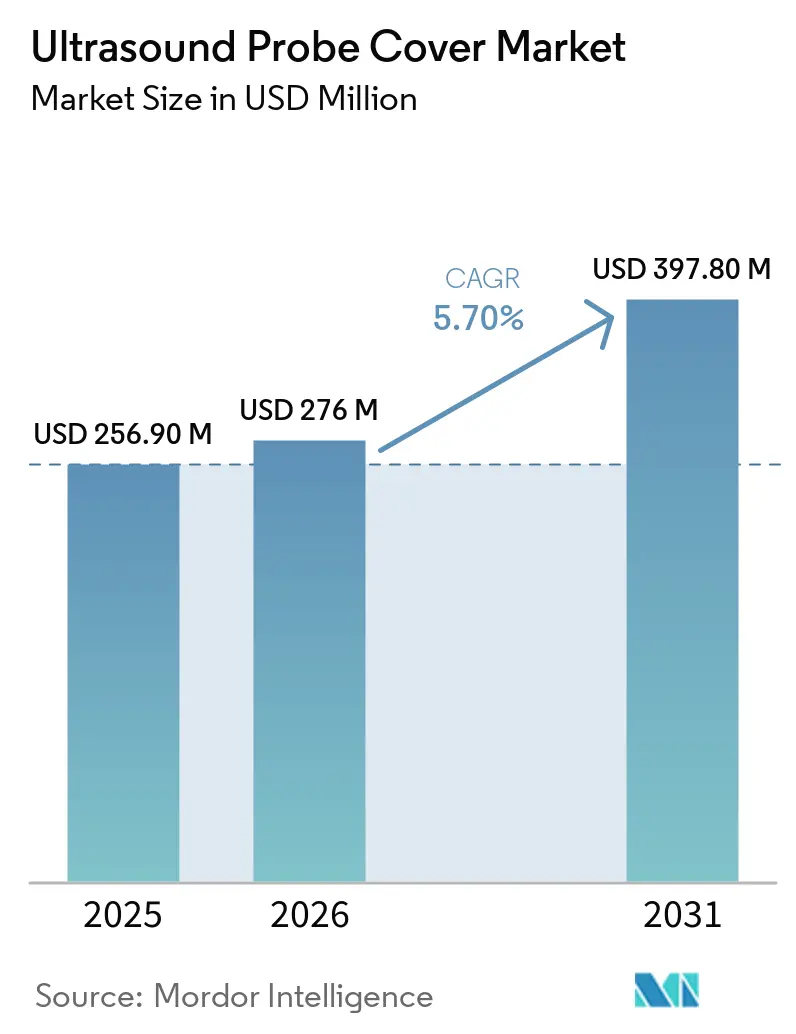

| Market Size (2026) | USD 276 Million |

| Market Size (2031) | USD 397.80 Million |

| Growth Rate (2026 - 2031) | 5.70% CAGR |

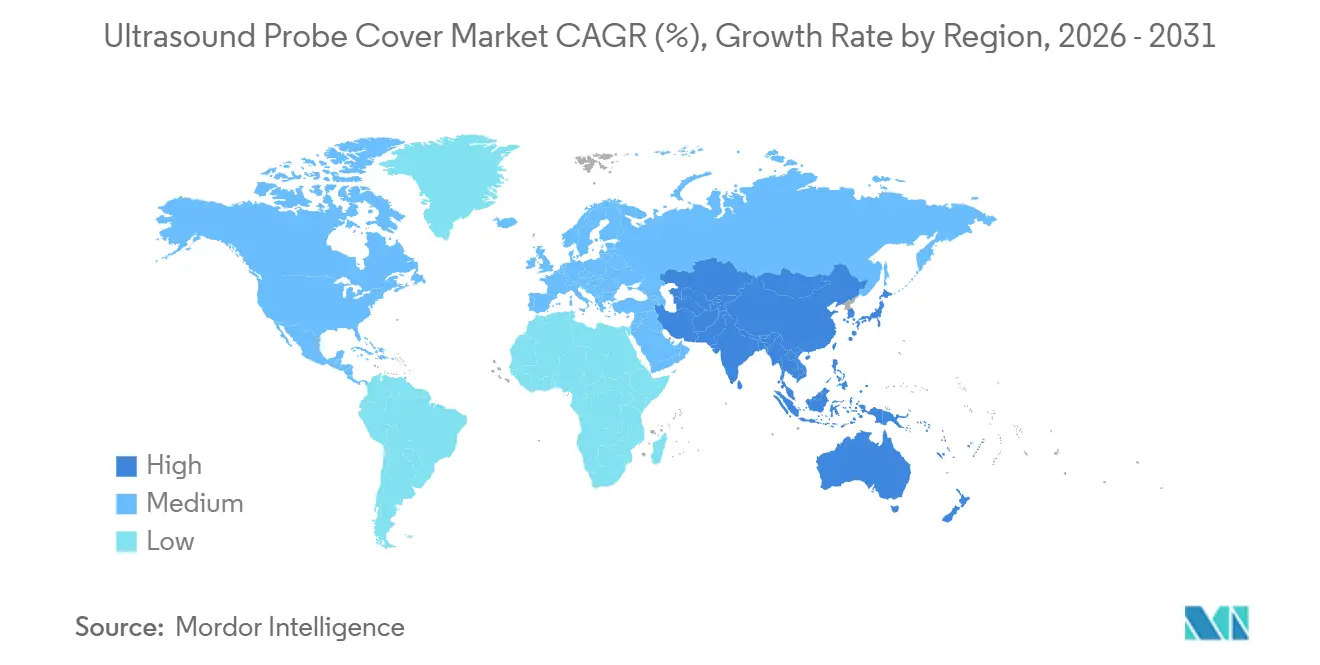

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

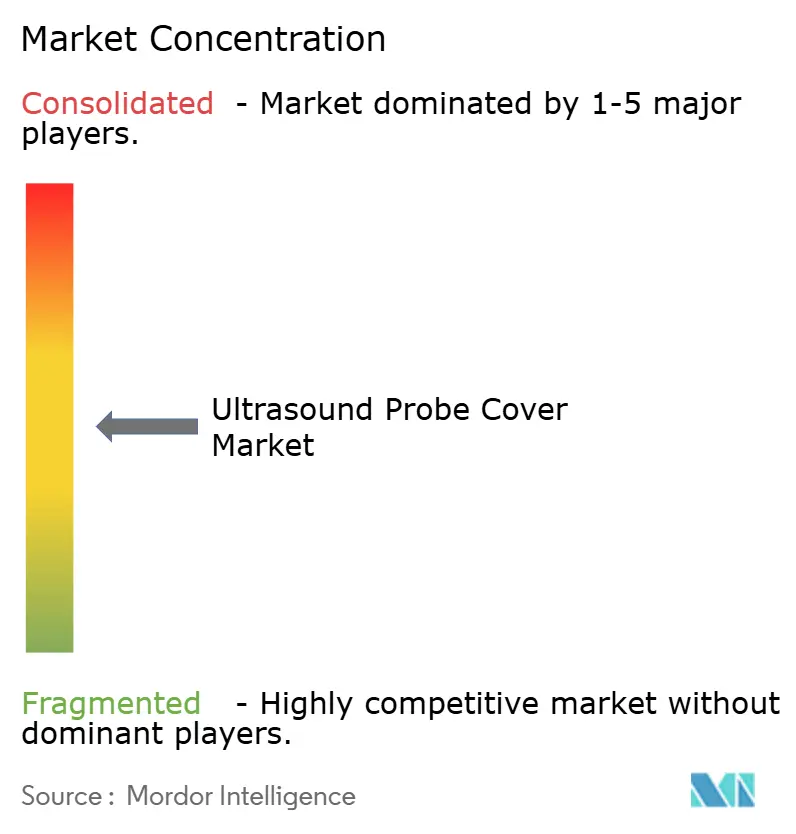

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrasound Probe Cover Market Analysis by Mordor Intelligence

The Ultrasound Probe Cover Market size is projected to be USD 256.90 million in 2025, USD 276 million in 2026, and reach USD 397.80 million by 2031, growing at a CAGR of 5.70% from 2026 to 2031.

Increased focus on hospital infection-control audits, the growing adoption of point-of-care ultrasound, and labor shortages in sterile processing are collectively driving demand for single-use barriers that enhance workflow efficiency. Disposable covers, which already dominate the ultrasound probe cover market, continue to expand their market share as decision-makers prioritize the mitigation of healthcare-associated infection risks over the relatively small additional cost of sterile sheaths. Latex-free options, particularly nitrile and polyisoprene, are experiencing the fastest growth as healthcare facilities phase out known allergens and comply with staff safety regulations. Advanced features such as antimicrobial coatings, RFID-enabled lot tracking, and vendor-managed inventory platforms are further strengthening the value proposition by integrating consumables with digital supply-chain analytics. This integration enables procurement teams to optimize reorder points and monitor usage patterns in real time.

Key Report Takeaways

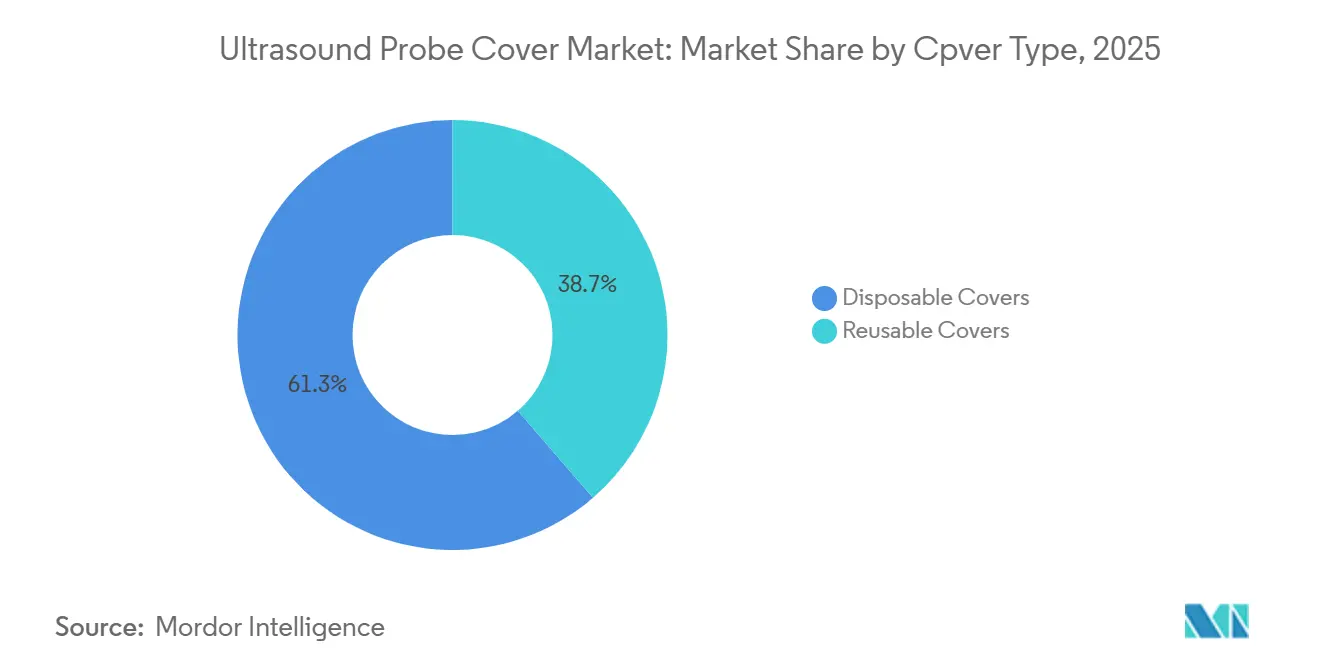

- By cover type, disposable products controlled 61.34% of revenue in 2025 while also delivering a 5.95% CAGR through 2031, reflecting the strongest growth across the ultrasound probe cover market.

- By material, latex-free variants accounted for 43.25% of revenue but are on pace to expand at a 6.03% CAGR, the fastest in their segment across the ultrasound probe cover market.

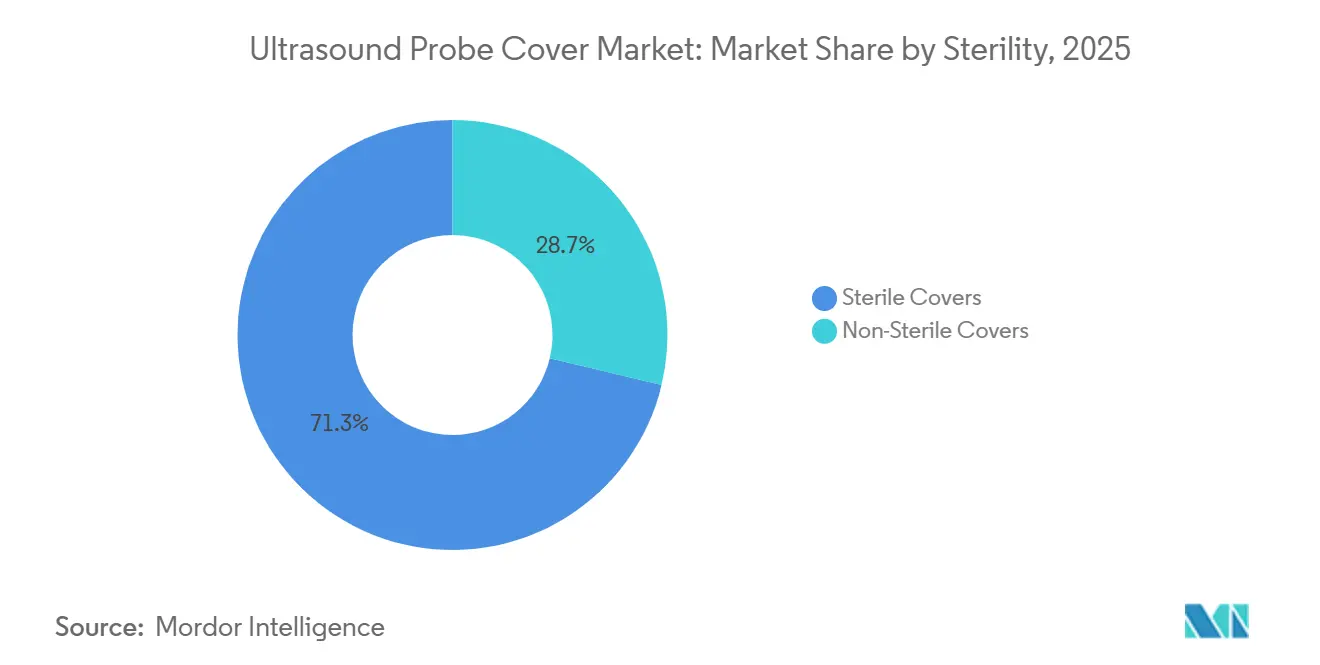

- By sterility, sterile barriers captured 71.26% of shipments in 2025 and are advancing at a 6.03% CAGR, driven by expanding minimally invasive surgery volumes.

- By probe application, endocavitary probes held 53.26% of the ultrasound probe cover market share in 2025 and continue to rise at a 5.91% CAGR under stricter semi-critical device guidance.

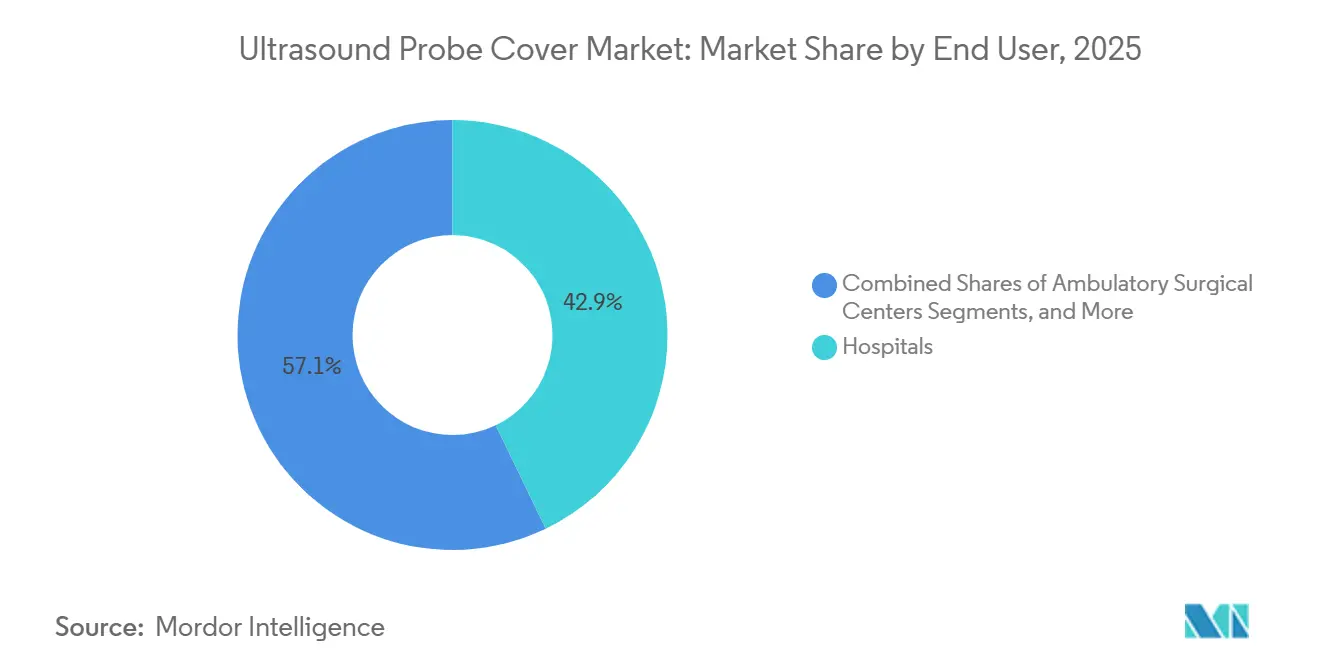

- By end-user, ambulatory surgical centers posted the steepest 5.95% CAGR, outpacing hospitals for the first time in the ultrasound probe cover market.

- North America captured 38.96% of 2025 revenue, yet Asia-Pacific is the fastest-growing region at a 6.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ultrasound Probe Cover Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising ultrasound procedure volumes | +0.9% | Global, with strongest gains in Asia-Pacific (China, India) and Middle East (UAE, Saudi Arabia) | Medium term (2–4 years) |

| Stricter infection-control regulations | +1.1% | North America & Europe, spillover to APAC hospital chains seeking JCI accreditation | Short term (≤ 2 years) |

| Shift to disposable covers | +0.8% | Global, led by North America and Western Europe; slower adoption in Latin America and Africa | Medium term (2–4 years) |

| Growth of point-of-care ultrasound | +1.0% | North America, Europe, Australia; expanding into urban centers in Brazil, Mexico, South Africa | Medium term (2–4 years) |

| Antimicrobial & smart-sensor covers adoption | +0.6% | North America, Western Europe, select APAC markets (Japan, South Korea, Singapore) | Long term (≥ 4 years) |

| Growth of auto-replenishment solutions in e-commerce | +0.5% | North America, Europe; pilot programs in GCC and urban India | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Ultrasound Procedure Volumes

Clinical imaging workloads are increasing as aging populations face chronic disease screenings and obstetric monitoring requirements. Countries such as Japan, South Korea, and several in Western Europe are experiencing double-digit growth in outpatient ultrasound visits. Similarly, China's township clinics have reported a rise in ultrasound procedures following increased equipment allocations under the "Healthy China 2030" initiative.[1]National Health Commission of China, “Healthy China 2030 Initiative,” nhc.gov.cn Each additional scan necessitates the use of at least one new cover or a high-level disinfection cycle. Hospitals without automated processors often rely on single-use barriers to maintain operational efficiency. The relationship is straightforward: more scans result in a higher number of probes in circulation daily. Administrators have effectively translated radiology booking data into forward orders for covers through materials-management software. Consequently, the growth in diagnostic procedures directly drives the ultrasound probe cover market, offering suppliers clear demand signals and predictable volume growth.

Stricter Infection-Control Regulations

Infection-control regulations classify transvaginal and transrectal transducers as semi-critical devices that require either high-level disinfection or the use of sterile, single-use covers between patients. Accreditation bodies now audit probe-cover inventory logs and penalize hospitals unable to link every endocavitary scan to a documented barrier or reprocessing record. Similar regulatory vigilance is enforced in Europe, and leading hospital chains in the Asia-Pacific region are adopting these standards to secure certifications critical for medical tourism. The risk of reputational damage and potential malpractice litigation has prompted administrators to prioritize sterile covers over reusable sheaths, even when the latter remains legally permissible. This regulatory environment continues to expand the ultrasound probe cover market as facilities adopt risk-averse practices and shift toward disposable solutions.

Shift to Disposable Covers

Reusable latex sheaths require meticulous rinsing, drying, and chemical disinfection, which strain limited sterile-processing resources and increase the risk of human error. Studies have shown that a significant percentage of reprocessed covers retain residual organic soil, reinforcing concerns about the reliability of manual workflows in ensuring sterility. Disposable polyethylene or nitrile barriers address these challenges by eliminating labor-intensive processes, reducing turnaround times, and transferring liability to manufacturers operating under stringent quality standards. While latex covers remain prevalent in resource-constrained markets, even cost-sensitive facilities are exploring latex-free options to mitigate allergy-related risks. Rising nursing wages and insurer incentives for documented infection-prevention protocols are accelerating the adoption of disposable covers, further solidifying their long-term impact on the ultrasound probe cover market.

Growth of Point-of-Care Ultrasound

Handheld ultrasound devices have become increasingly common in emergency wards and ambulances, enabling non-radiologists to perform focused cardiac or trauma assessments at the bedside. Each decentralized scanner requires its own stock of probe covers, leading to fragmented demand across departments that previously relied on centralized disinfection suites. The adoption of these devices by pre-hospital emergency medical services in regions such as the United Kingdom and Australia has further expanded consumption beyond traditional hospital settings. To meet this growing demand, distributors have implemented barcode scanning and RFID tagging systems that integrate with auto-replenishment dashboards, ensuring uninterrupted supply for mobile teams. This diffusion of point-of-care ultrasound devices has created additional touchpoints for suppliers, driving sustained growth in the ultrasound probe cover market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Single-use plastic sustainability concerns | -0.4% | Europe (EU Plastics Directive), California, select Canadian provinces | Medium term (2–4 years) |

| Cost pressure in low-resource settings | -0.5% | Sub-Saharan Africa, rural India, parts of Latin America (Bolivia, Paraguay) | Short term (≤ 2 years) |

| Resin additive supply-chain risks | -0.3% | Global, with acute impact during petrochemical plant outages in Gulf Coast (U.S.), Middle East | Short term (≤ 2 years) |

| Probe-dimension standardization gaps | -0.2% | Global, affecting all markets but most visible in multi-vendor hospital systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Single-Use Plastic Sustainability Concerns

The EU's Single-Use Plastics Directive enforces extended producer responsibility programs, holding manufacturers accountable for downstream waste management. Similarly, California's recycling regulations impose stringent targets, while advocacy groups evaluate hospitals' plastic usage through annual assessments. In response, industry leaders are piloting polylactic acid films that biodegrade in industrial composting environments while maintaining sterility standards. However, high costs, limited resin availability, and inadequate end-of-life infrastructure restrict broader adoption. Until bio-based polymers achieve comparable performance in barrier integrity and cost-effectiveness, environmental regulations are likely to impact the growth trajectory of the ultrasound probe cover market.

Cost Pressure in Low-Resource Settings

The cost of a sterile endocavitary cover, ranging from USD 2–5, represents a significant financial burden for clinics in regions with per-capita health expenditures below USD 100. In rural areas of India and Sub-Saharan Africa, facilities often reuse single-use products across multiple patients or rely on non-sterile polyethylene wraps, increasing infection risks and suppressing legitimate demand. Local manufacturers offer basic latex covers at significantly lower prices compared to multinational companies, intensifying competition and reducing profit margins. Without initiatives such as donor-funded procurement programs or tiered pricing strategies to improve affordability, cost constraints will continue to limit the penetration of ultrasound probe covers in developing markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cover Type: Disposables Fortify Workflow Efficiency

In 2025, disposable solutions contributed 61.34% of revenue and are projected to grow at a 5.95% CAGR, outperforming reusable sheaths across all monitored regions. This dominance is primarily driven by the labor-intensive requirements of sterile processing, as each reusable sleeve necessitates rinsing, leak testing, disinfection, drying, and documentation. Staffing shortages exacerbate these challenges, making disposables a reliable solution to mitigate human error and avoid compliance issues. Manufacturers have enhanced single-use items by incorporating antimicrobial coatings and RFID chips, further differentiating them from reusable alternatives. While reusable covers remain a tactical choice in budget-constrained scenarios, global health organizations increasingly allocate funding to disposables to ensure barrier integrity. Consequently, disposables are driving both volume and innovation in the ultrasound probe cover market.

By Material: Allergy-Safe, Latex-Free Uptake Accelerates

In 2025, latex accounted for 56.75% of units shipped, largely due to the availability and cost-effectiveness of natural rubber in Southeast Asia. However, materials such as nitrile, polyisoprene, and polyethylene are growing at a 6.03% CAGR, the fastest among material categories. Clinical data indicating that up to 17% of healthcare workers experience latex sensitivities has prompted risk assessments and led procurement teams to eliminate latex from institutional inventories. Synthetic elastomers have nearly matched natural rubber in tensile strength and elasticity, resulting in only a slight cost premium. Hospitals that previously maintained separate inventories for latex and non-latex products now default to latex-free options, simplifying inventory management and protecting staff from hypersensitivity risks.

By Sterility: Aseptic Assurance Drives Premium Growth

Sterile barriers represented 71.26% of global shipments in 2025 and are projected to grow at a 6.03% CAGR, significantly outpacing the non-sterile segment. Regulatory requirements classify transvaginal, transrectal, and intraoperative probes as semi-critical, necessitating high-level disinfection or sterile covers. Hospitals, aiming to avoid compliance risks, increasingly use sterile covers even for external probes when scanning immunocompromised patients. Suppliers have capitalized on this demand by offering individually pouched, gamma-irradiated covers that can be placed directly onto sterile fields, reducing touch points and improving room turnover efficiency. Non-sterile items remain prevalent in high-volume obstetric and musculoskeletal clinics, where intact skin contact allows for less stringent barriers, but reimbursement policies favor sterile protocols, further shifting the market balance.

By Probe Application: Endocavitary Dominance Endures

Endocavitary probes accounted for 53.26% of revenue in 2025 and are expected to grow at a 5.91% CAGR. Fertility clinics, urology centers, and women's health providers are increasingly standardizing disposable covers for every scan. These probes, which interact with mucous membranes, pose a higher risk of microbial transmission, necessitating the use of higher-cost sterile barriers. A 2024 investigation linked multiple bloodstream infections to a reprocessed transvaginal transducer, prompting the clinic to switch to single-use sheaths and report savings from reduced procedure downtime. Such cases strengthen the purchasing rationale for healthcare administrators globally.

By End-User: ASCs Surge as Procedures Decamp from Hospitals

Hospitals accounted for 42.87% of purchasing volume in 2025, but ambulatory surgical centers (ASCs) are experiencing the fastest growth, with a 5.95% CAGR. The expansion of ASC-payable procedures, including total joint arthroplasty, has driven demand for intraoperative ultrasound, which is used for nerve block guidance and implant placement. ASCs, operating with lean staffing models, require next-day replenishment, prompting distributors to offer tailored case sizes and subscription pricing. Diagnostic imaging centers face reimbursement pressures, while urgent-care clinics and physician offices are rapidly adopting handheld ultrasound devices. However, their smaller purchase volumes add complexity to supplier logistics.

Geography Analysis

In 2025, North America accounted for 38.96% of global revenue, driven by U.S. hospitals' adherence to stringent infection-control protocols and the adoption of automated high-level disinfection units. In Canada, bulk purchasing by provincial consortia boosts demand, while private healthcare chains in Mexico import premium antimicrobial covers to attract medical tourists. Despite market saturation and reimbursement challenges, the region's ultrasound probe cover market continues to grow steadily, supported by the shift toward outpatient surgery and point-of-care imaging.

Asia-Pacific is the fastest-growing region, with a 6.10% CAGR. In China, government initiatives are equipping township clinics with ultrasound units, driving demand for cost-effective barriers, while urban centers are adopting premium, latex-free products to meet international standards. In India, rising diagnostic volumes under national healthcare programs are offset by affordability challenges in public hospitals, slowing the adoption of premium products. Japan and South Korea lead in per-capita usage, driven by aging populations and early adoption of advanced covers. Australia aligns with North American standards, while Thailand and Singapore invest in robust supply chains to strengthen their medical tourism sectors.

Europe occupies a middle ground, with Germany, France, and the UK driving volume. However, the EU's Single-Use Plastics Directive is prompting suppliers to invest in biodegradable solutions and account for recycling costs. Southern European countries grow moderately, with public tenders emphasizing cost, leading to intense price competition. In the Middle East, Saudi Arabia and the UAE are channeling investments into advanced healthcare infrastructure, increasing demand for sterile covers. In Africa, donor-funded programs dominate, but urban private hospitals in countries like Kenya and Nigeria are beginning to adopt premium products, signaling potential growth as economic conditions improve.

Competitive Landscape

The ultrasound probe cover market comprises specialized manufacturers. Cardinal Health, McKesson, and Medline utilize extensive logistics networks and bundled contracts to integrate their SKUs into hospital enterprise resource planning systems. Their vendor-managed inventory algorithms significantly reduce emergency orders by over 90%, offering a strong value proposition for cost-conscious materials managers. CIVCO Medical Solutions and Parker Laboratories differentiate themselves with silver nanoparticle coatings that achieve 4-log microbial reductions within two hours, enabling them to command a 20-30% price premium from infection-prevention committees. Nanosonics, known for its expertise in probe disinfection, drives demand for covers by ensuring its automated cycles seamlessly integrate with specific disposable-sheath formats, creating a bundled ecosystem that secures repeat purchases.

Emerging competitors in India and China are leveraging vertical integration, including latex plantations, compounding, and extrusion, to reduce costs by 40-50%, thereby increasing competition in price-sensitive markets. Digital-native entrants are introducing subscription-based bundles that combine covers, disinfectants, and IoT trackers into a per-procedure fee, appealing to Ambulatory Surgical Centers (ASCs) that prioritize predictable operating expenses. Patent filings are increasingly focused on RFID antenna designs, antimicrobial additive dispersion, and biodegradable multilayer films, indicating key areas of future competition. Environmental certifications, such as ISO 14001, are now frequently included in tender requirements, pushing suppliers to validate their carbon footprints and implement closed-loop recycling programs. Overall, while competitive intensity remains moderate, companies that combine infection-prevention performance with advanced digital supply-chain visibility are better positioned to succeed.

Ultrasound Probe Cover Industry Leaders

Ecolab

CIVCO Medical Solutions

Sheathing Technologies

Parker Laboratories

Medline Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: B. Braun introduced the EZCOVER Probe Cover Set in the United States, a sterile kit aimed at peripheral nerve block procedures. It reduces cross-contamination risk while streamlining workflow in regional anesthesia suites.

- February 2025: CS Medical renewed its Strategic Partner Collaborator status with APIC, extending educational programs on automated probe reprocessing for infection-control professionals.

Global Ultrasound Probe Cover Market Report Scope

As per the scope of the report, ultrasound probe covers are protective sheaths, typically manufactured from materials such as latex, polyurethane, or polyethylene. These covers, available in both sterile and non-sterile options, can be disposable or reusable. They function as a sanitary barrier between the transducer and the patient, minimizing the risk of cross-contamination during imaging procedures. Their use is particularly critical in applications such as internal cavity scans, biopsies, and surgical procedures.

The segmentation of the ultrasound probe cover market is segmented by cover type, material, sterility, probe application, end user, and geography. By cover type, the market is segmented into disposable covers and reusable covers. By material, the market is segmented into latex-free covers and latex covers. By sterility, the market is segmented into sterile covers and non-sterile covers. By probe application, the market is segmented into endocavitary probes, external surface probes, intraoperative probes, and other applications. By end user, the market is segmented into hospitals, ambulatory surgical centers, diagnostic imaging centers, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| Disposable Covers |

| Reusable Covers |

| Latex-Free Covers |

| Latex Covers |

| Sterile Covers |

| Non-Sterile Covers |

| Endocavitary Probes |

| External Surface Probes |

| Intraoperative Probes |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Diagnostic Imaging Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Cover Type | Disposable Covers | |

| Reusable Covers | ||

| By Material | Latex-Free Covers | |

| Latex Covers | ||

| By Sterility | Sterile Covers | |

| Non-Sterile Covers | ||

| By Probe Application | Endocavitary Probes | |

| External Surface Probes | ||

| Intraoperative Probes | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Diagnostic Imaging Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the ultrasound probe cover market be in 2031?

The sector is forecast to reach USD 397.8 million by 2031, expanding from USD 276.0 million in 2026 at a 5.7% CAGR.

Which cover type generates the most revenue?

Disposable sterile barriers contribute more than 60% of global sales thanks to easier workflows and lower infection-control risk.

Why are latex-free probe covers gaining traction?

Rising staff allergies and OSHA recommendations push hospitals toward nitrile and polyisoprene alternatives that remove latex exposure without sacrificing performance.

Which end-user is growing fastest?

Ambulatory surgical centers post the steepest 5.95% CAGR as reimbursement reforms shift inpatient procedures to outpatient sites.

What regional market shows the highest growth?

Asia-Pacific leads with a 6.10% CAGR, propelled by universal coverage programs in China and India and rising medical tourism in Southeast Asia.

How are sustainability regulations affecting suppliers?

EU and California directives on single-use plastics are forcing manufacturers to invest in biodegradable films and extended producer responsibility programs, adding cost but opening green-product niches.

Page last updated on: