Ultrasonic Tissue Ablation System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

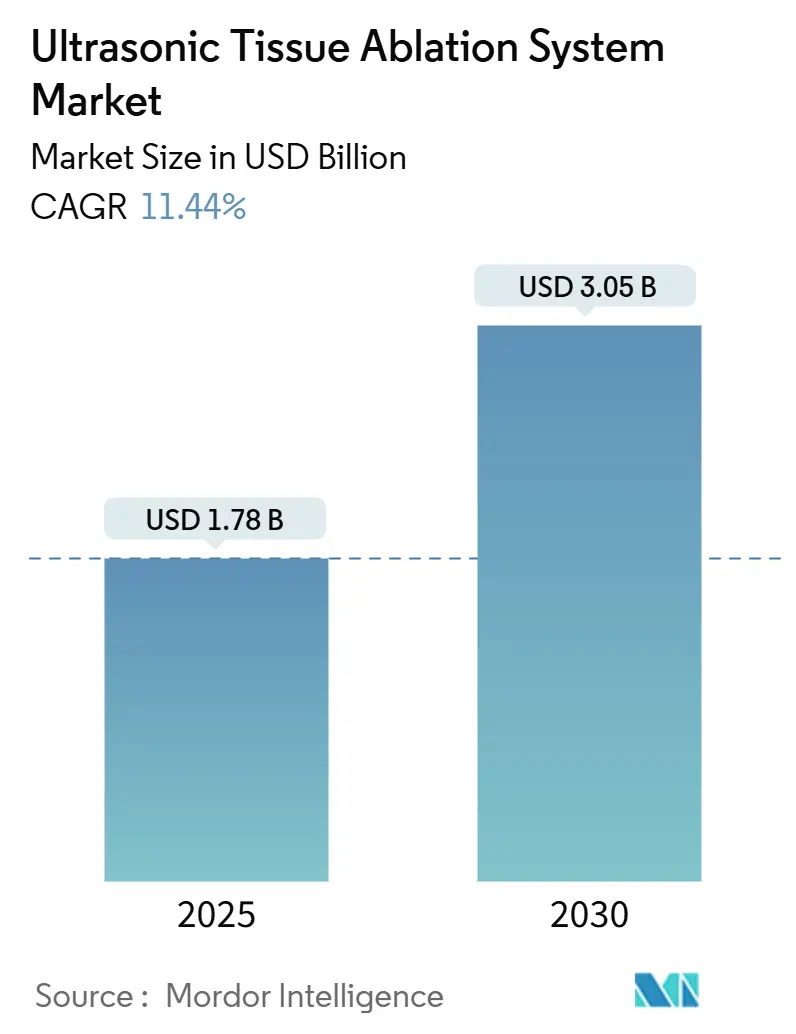

| Market Size (2025) | USD 1.78 Billion |

| Market Size (2030) | USD 3.05 Billion |

| Growth Rate (2025 - 2030) | 11.44% CAGR |

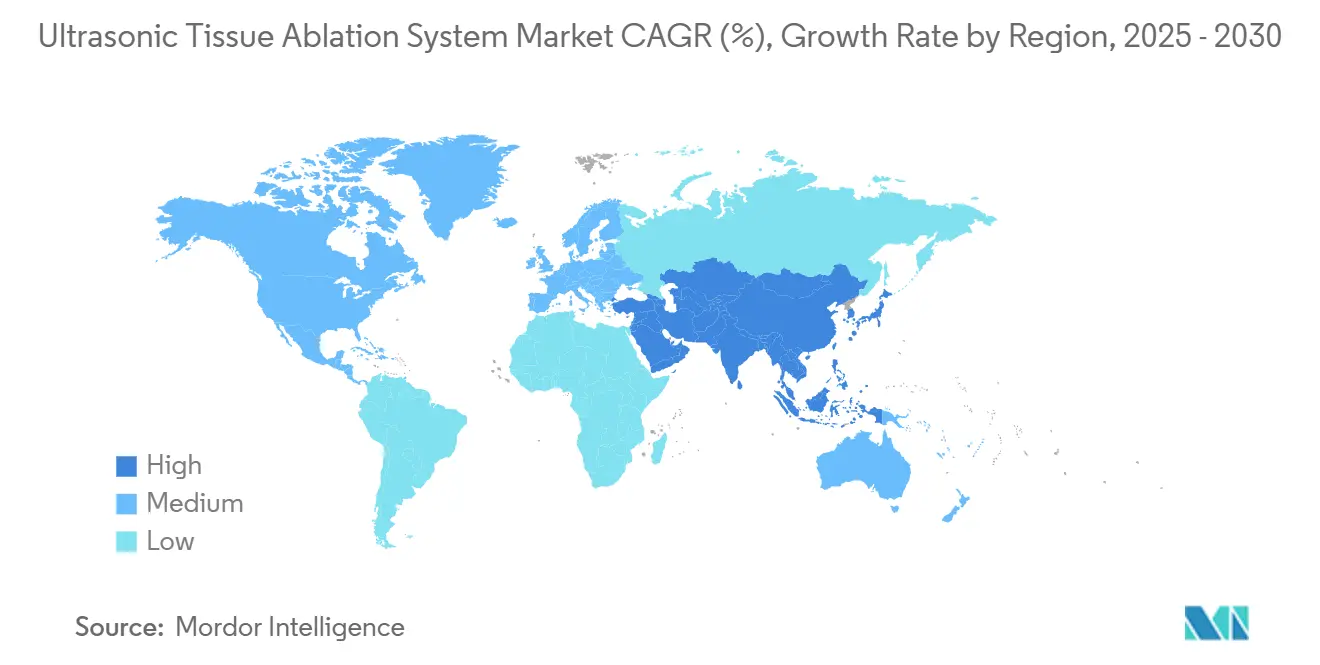

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrasonic Tissue Ablation System Market Analysis by Mordor Intelligence

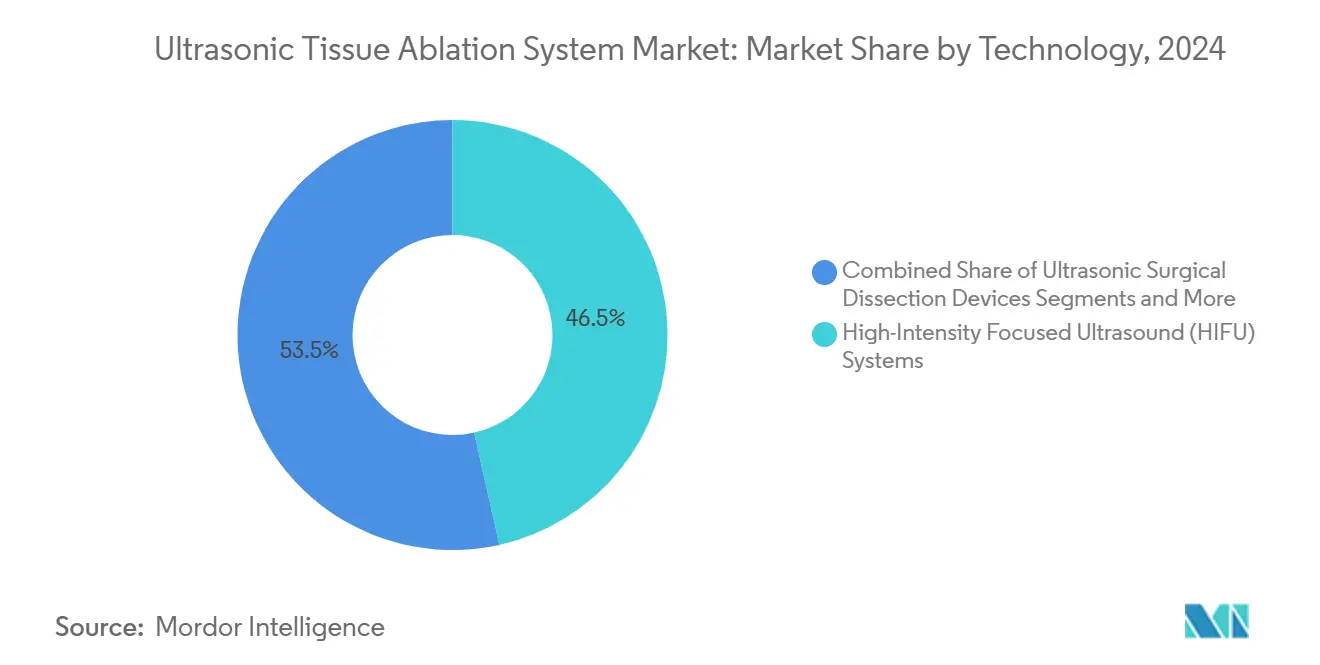

The ultrasonic tissue ablation system market size stands at USD 1.78 billion in 2025 and is forecast to reach USD 3.05 billion by 2030, advancing at an 11.44% CAGR. Robust growth is tied to histotripsy’s 2023 FDA breakthrough status for liver tumors, wider reimbursement for basivertebral nerve and essential-tremor procedures, and accelerated adoption of image-guided High-Intensity Focused Ultrasound (HIFU) across oncology, orthopedics, and pain management applications.[1]U.S. Food and Drug Administration, “Paradise Ultrasound Renal Denervation System – P220023,” FDA.gov North America remains the largest regional contributor, underpinned by Medicare coverage gains and strong academic expertise, while Asia-Pacific leads in pace with a 13.57% CAGR as infrastructure and regulatory harmonization improve. Technology dynamics show HIFU systems accounting for 46.52% of 2024 revenues, yet ultrasonic bone scalpels post the fastest segment CAGR at 15.77% on the back of shorter orthopedic operating times and lower blood-loss metrics. Oncology retains a 34.58% revenue share, although orthopedic and spine procedures expand most quickly (15.32% CAGR), mirroring surgery’s migration to ambulatory settings. M&A signals—such as HistoSonics’ potential USD 2.5 billion sale—underscore competitive pressure and the strategic value of mechanical tissue-fractionation platforms.

Key Report Takeaways

- By technology, High-Intensity Focused Ultrasound systems led with 46.52% of ultrasonic tissue ablation system market share in 2024; ultrasonic bone scalpels are projected to climb at a 15.77% CAGR through 2030.

- By application, oncology captured 34.58% of the ultrasonic tissue ablation system market size in 2024, while orthopedic and spine procedures are set to expand at 15.32% CAGR to 2030.

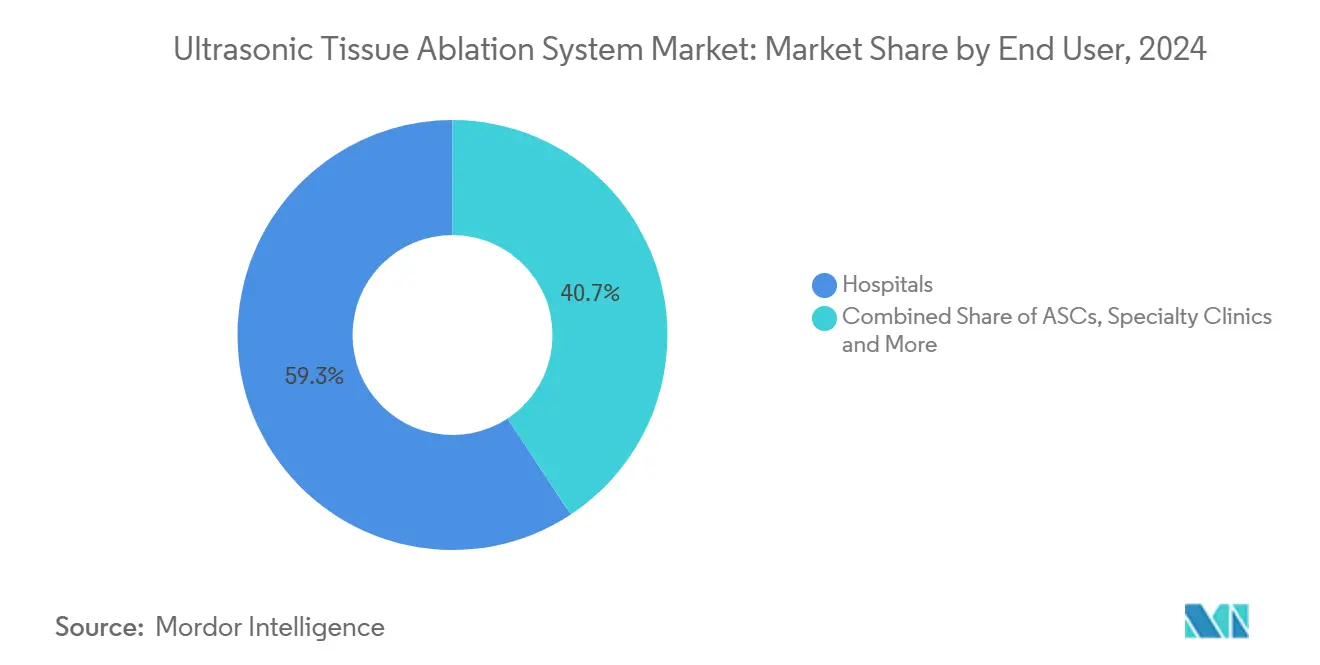

- By end user, hospitals held 59.27% revenue share in 2024; ambulatory surgical centers record the highest projected CAGR at 14.23% between 2025-2030.

- By product component, generators and consoles commanded 44.72% share of the ultrasonic tissue ablation system market size in 2024, with guidance and imaging modules advancing at a 13.68% CAGR to 2030.

- By geography, North America controlled 39.77% of 2024 revenues; Asia-Pacific is forecast to deliver the quickest 13.57% CAGR through 2030.

Global Ultrasonic Tissue Ablation System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cancer & chronic diseases | +2.8% | Global; aging markets in North America & Europe | Long term (≥ 4 years) |

| Technological advances in image-guided HIFU platforms | +2.1% | North America & EU leading; APAC accelerating | Medium term (2-4 years) |

| Transition to outpatient minimally-invasive surgery | +1.9% | North America & EU core; APAC urban centers | Short term (≤ 2 years) |

| Favorable reimbursement in US, EU & Japan | +1.7% | North America & EU established; Japan expanding | Medium term (2-4 years) |

| Veterinary oncology use-cases for focused ultrasound | +0.6% | North America leading; EU following | Long term (≥ 4 years) |

| Immuno-synergistic histotripsy trials in research hubs | +0.8% | North America & EU research centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Of Cancer & Chronic Diseases

Escalating global cancer incidence sustains demand for non-invasive ablation, especially where comorbid, elderly patients tolerate surgery poorly. Histotripsy’s October 2023 FDA clearance for hepatocellular carcinoma validated mechanical tissue destruction, with HOPE4LIVER trials reporting 95% technical success and 7% major-complication rates.[2]Timothy J. Ziemlewicz, “The #HOPE4LIVER Single-Arm Pivotal Trial for Histotripsy of Primary and Metastatic Liver Tumors,” Radiology, pubs.rsna.org Aging populations prefer minimally-invasive approaches that shorten recovery. Early evidence also shows histotripsy may stimulate systemic immune responses, supporting its future integration with checkpoint inhibitors. Veterinary oncology studies in canine osteosarcoma provide translational data for pediatric settings, accelerating clinical pipelines.

Technological Advances In Image-Guided HIFU Platforms

Real-time MRI now turns HIFU into a precision-targeted therapy. Johnson & Johnson’s VARIPULSE achieved 85% primary effectiveness in atrial-fibrillation ablation while minimizing fluoroscopy. Non-thermal histotripsy counters heat-sink limitations near vessels, and Sonire Therapeutics’ pancreatic program shows cavitation ultrasound’s reach into acoustically challenging organs. Integrated imaging reduces uncertainty, enhances surgeon confidence, and justifies premium pricing.

Transition To Outpatient Minimally-Invasive Surgery

ASC volumes rise as payers reward efficiency. Medicare documented 3.3 million ASC patients and USD 6.1 billion in 2024 spending.[3]Medicare Payment Advisory Commission, “Report to the Congress: Medicare Payment Policy,” MedPAC.gov HistoSonics’ Edison platform supports same-day liver tumor ablation without thermal-injury monitoring, aligning with bundled-payment incentives. Proven outpatient outcomes prompt further ASC investment, creating a virtuous adoption cycle.

Favorable Reimbursement In US, EU & Japan

Medicare’s basivertebral-nerve coverage and Humana’s essential-tremor approval illustrate payer confidence in focused ultrasound value. The FDA’s 2024 thermal-effects guidance provides regulatory clarity that further reassures insurers. Germany’s reimbursement expansion and Netherlands’ national coverage decision for MRgFUS underline parallel European momentum. Japanese payers have likewise broadened coverage, anchoring capital-equipment investment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance cost of HIFU consoles | -1.8% | Global; tighter budgets in emerging markets | Medium term (2-4 years) |

| Shortage of trained sonosurgeons & steep learning curve | -1.5% | Worldwide; acute in APAC & developing regions | Long term (≥ 4 years) |

| Regulatory uncertainty for non-thermal histotripsy devices | -0.9% | Global; differing regional frameworks | Short term (≤ 2 years) |

| Thermal-safety concerns in aesthetic contouring segment | -0.7% | North America & EU where aesthetics prevail | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Cost Of HIFU Consoles

Advanced MRI-guided platforms range from USD 1-3 million, with annual service contracts adding 10-15% of purchase price. Smaller hospitals and emerging-market centers struggle to finance these systems, concentrating capability in large academic hubs. Leasing models help but may cap procedure volumes and hinder ROI.

Shortage Of Trained Sonosurgeons & Steep Learning Curve

Focused ultrasound demands mastery of physics, targeting, and multidisciplinary care. AIUM guidelines recommend dedicated fellowships, yet programs remain sparse. Proficiency requires significant case numbers, fostering geographic disparities that slow uptake in resource-limited settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: HIFU Dominance Faces Mechanical Disruption

High-Intensity Focused Ultrasound accounted for 46.52% of 2024 revenues, reflecting decades of validation across prostate, uterine fibroid, and liver indications. The ultrasonic tissue ablation system market size for HIFU-led platforms is projected to expand steadily through 2030 as MRI guidance broadens anatomical reach. Histotripsy’s 95% technical success in liver tumors and ultrasonic bone scalpels’ 40% blood-loss reduction signal a pivot to mechanical modalities that address thermal limitations.

Ultrasonic bone scalpels’ 15.77% CAGR positions them as the technology frontier, especially in orthopedics where shorter operating times drive operating-room throughput. Hybrid energy consoles like Johnson & Johnson’s DUALTO leverage ultrasonic, RF, and pulsed-field energies to offer surgeons multi-modality flexibility. The ultrasonic tissue ablation system market share of disruptive mechanical platforms is expected to rise as outcome data accumulate.

By Application: Oncology Leadership Challenged by Orthopedic Growth

Oncology retained 34.58% revenue share in 2024, buoyed by prostate and liver programs. Segment sales are reinforced by payers recognizing non-invasive options that shorten stays and reduce complications. Orthopedics and spine interventions, however, exhibit the highest 15.32% CAGR as bone scalpels and basivertebral-nerve ablation spread across ASC networks. The ultrasonic tissue ablation system market size for orthopedic uses could narrow the gap with oncology by 2030 if reimbursement parity holds.

Cardiovascular growth stems from fluoroscopy-free atrial-fibrillation ablation, while pain management gains from Medicare-covered vertebrogenic-pain procedures. Neurology and gynecology sustain steady expansion through tremor and uterine-fibroid treatments, respectively, providing portfolio diversification.

By End User: Hospital Dominance Erodes to ASC Efficiency

Hospitals generated 59.27% of 2024 spending due to infrastructure requirements and complex case loads. Yet ambulatory surgical centers deliver a 14.23% CAGR, driven by payer incentives and patient preference for same-day discharge. The ultrasonic tissue ablation system market size accruing to ASCs continues to rise as compact consoles enter the field and histotripsy’s non-thermal profile obviates extended monitoring.

Specialty clinics serve focused indications like pain or women’s health, while veterinary hospitals constitute a niche but fast-modernizing channel capturing translational research dollars. The ultrasonic tissue ablation system market share of hospitals will likely fall below 50% beyond 2030 if ASC momentum persists.

By Product Component: Console Leadership Meets Imaging Acceleration

Generators and consoles generated 44.72% of 2024 revenue, giving them the highest ultrasonic tissue ablation system market share at the component level. Handpieces and probes provided steady recurring sales, but price competition limited margin growth. Disposable shears and accessories tracked procedure volume and supported predictable aftermarket revenue. Guidance and imaging modules posted the quickest 13.68% CAGR as providers demanded real-time monitoring for safety and accuracy. Service and software contracts expanded in parallel, driven by predictive maintenance and cloud analytics that streamline workflow. The shift toward integrated consoles with embedded AI boosted demand for premium models that bundle imaging and therapy in a single footprint.

The ultrasonic tissue ablation system market size attached to consoles will keep rising as hospitals and ambulatory centers upgrade to multi-modality platforms that handle HIFU, histotripsy, and pulsed-field applications in one unit. Imaging modules should continue to outpace the base market because real-time feedback reduces retreatment rates and supports favorable reimbursement. Vendors leverage software updates to extend hardware life cycles and lock in customers through subscription models. Probe designs move toward internally cooled tips that permit longer sonication times without thermal damage. Accessory standardization lowers per-case cost, yet differentiating features like RFID tracking help protect margin. Overall, component innovation centers on tighter integration between power delivery, imaging, and data analytics, ensuring every capital purchase yields both clinical impact and long-term service revenue.

Geography Analysis

North America captured 39.77% of 2024 revenues, benefiting from clear reimbursement pathways, concentrated clinical expertise, and a strong pipeline of domestic device innovators. The ultrasonic tissue ablation system market size in the region is supported by CPT codes for basivertebral-nerve ablation and Humana’s tremor-therapy coverage. Europe follows with robust adoption in Germany and the Netherlands, each expanding coverage for MR-guided focused ultrasound technologies. Research consortia in France and the United Kingdom further anchor clinical evidence generation.

Asia-Pacific posts the highest 13.57% CAGR thanks to infrastructure rollouts in China, Japan, and South Korea and rising chronic-disease incidence. Korean Liver Cancer Association guidelines now embed ultrasound-guided ablation, signaling mainstream acceptance. China’s increased local manufacturing capacity could lower system prices, broadening access and raising the ultrasonic tissue ablation system market share of indigenous suppliers.

Middle East and Africa show selective uptake, chiefly in private centers serving medical-tourism inflows. South America lags, curtailed by economic headwinds, though Brazil’s sizeable installed imaging base offers a foundation for longer-term growth. Government initiatives to incentivize minimally-invasive surgery could unlock latent demand across emerging regions during the forecast horizon.

Competitive Landscape

The field exhibits moderate concentration. Multinationals—Johnson & Johnson, Medtronic, Olympus—capitalize on broad portfolios and distribution muscle, while focused-ultrasound specialists—INSIGHTEC, HistoSonics—command premium pricing through technological distinctiveness. Intellectual-property positions around cavitation control and image guidance create temporary barriers that erode as patents expire.

Strategic moves underscore consolidation appetite. HistoSonics’ exploration of a USD 2.5 billion sale illustrates histotripsy’s perceived strategic value. Hologic’s USD 350 million acquisition of Gynesonics broadens women’s-health exposure. Partnerships such as Canon-Olympus leverage complementary competencies to accelerate product cycles. Competitive differentiators increasingly hinge on procedure workflow, AI-guided planning, and multi-modality consoles that rationalize capital budgets.

Small entrants target cost-effective systems for emerging markets or explore veterinary and immunotherapy adjacencies. Market participants also chase service revenue through cloud analytics and outcome-tracking platforms that can support reimbursement dossiers and foster customer lock-in.

Ultrasonic Tissue Ablation System Industry Leaders

Johnson & Johnson

Medtronic plc

Olympus Corporation

Stryker Corporation

Conmed Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HistoSonics explores a USD 2.5 billion sale to Medtronic, GE HealthCare, and Johnson & Johnson, spotlighting histotripsy’s strategic value.

- March 2025: Johnson & Johnson MedTech launches the DUALTO Energy System, integrating ultrasonic, RF, and pulsed-field energies in one console.

- February 2025: Johnson & Johnson resumes U.S. VARIPULSE cases with updated instructions after safety review affirmed device integrity.

Global Ultrasonic Tissue Ablation System Market Report Scope

| High-Intensity Focused Ultrasound (HIFU) Systems |

| Ultrasonic Surgical Dissection Devices |

| Ultrasonic Aspirators |

| Histotripsy Systems |

| Ultrasonic Bone Scalpels |

| Others |

| Oncology |

| Cardiovascular |

| Gynecology |

| Pain Management |

| Orthopedics & Spine |

| Urology |

| Other Clinical (Neurology, Aesthetics, Veterinary) |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Veterinary Hospitals & Clinics |

| Generators / Consoles |

| Handpieces & Probes |

| Disposable Shears & Accessories |

| Guidance & Imaging Modules |

| Service & Software |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | High-Intensity Focused Ultrasound (HIFU) Systems | |

| Ultrasonic Surgical Dissection Devices | ||

| Ultrasonic Aspirators | ||

| Histotripsy Systems | ||

| Ultrasonic Bone Scalpels | ||

| Others | ||

| By Application | Oncology | |

| Cardiovascular | ||

| Gynecology | ||

| Pain Management | ||

| Orthopedics & Spine | ||

| Urology | ||

| Other Clinical (Neurology, Aesthetics, Veterinary) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Veterinary Hospitals & Clinics | ||

| By Product Component | Generators / Consoles | |

| Handpieces & Probes | ||

| Disposable Shears & Accessories | ||

| Guidance & Imaging Modules | ||

| Service & Software | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the ultrasonic tissue ablation system market in 2025?

The market is valued at USD 1.78 billion in 2025 and is forecast to grow to USD 3.05 billion by 2030.

What CAGR is projected for ultrasonic tissue ablation systems through 2030?

The global CAGR is estimated at 11.44% for the 2025-2030 period.

Which technology holds the largest share today?

High-Intensity Focused Ultrasound systems account for 46.52% of 2024 revenues.

Which clinical area is expanding fastest?

Orthopedic and spine procedures lead with a 15.32% CAGR through 2030.

Which region shows the quickest growth momentum?

Asia-Pacific is expected to expand at a 13.57% CAGR, driven by rising infrastructure investment and regulatory alignment.

What trend underpins rising ASC adoption?

Outpatient minimally-invasive surgery supported by payer incentives is pushing ASC volumes, with ultrasonic platforms enabling same-day discharge.

Page last updated on: