Ultrasound Transducer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.24 Billion |

| Market Size (2031) | USD 5.06 Billion |

| Growth Rate (2026 - 2031) | 3.59% CAGR |

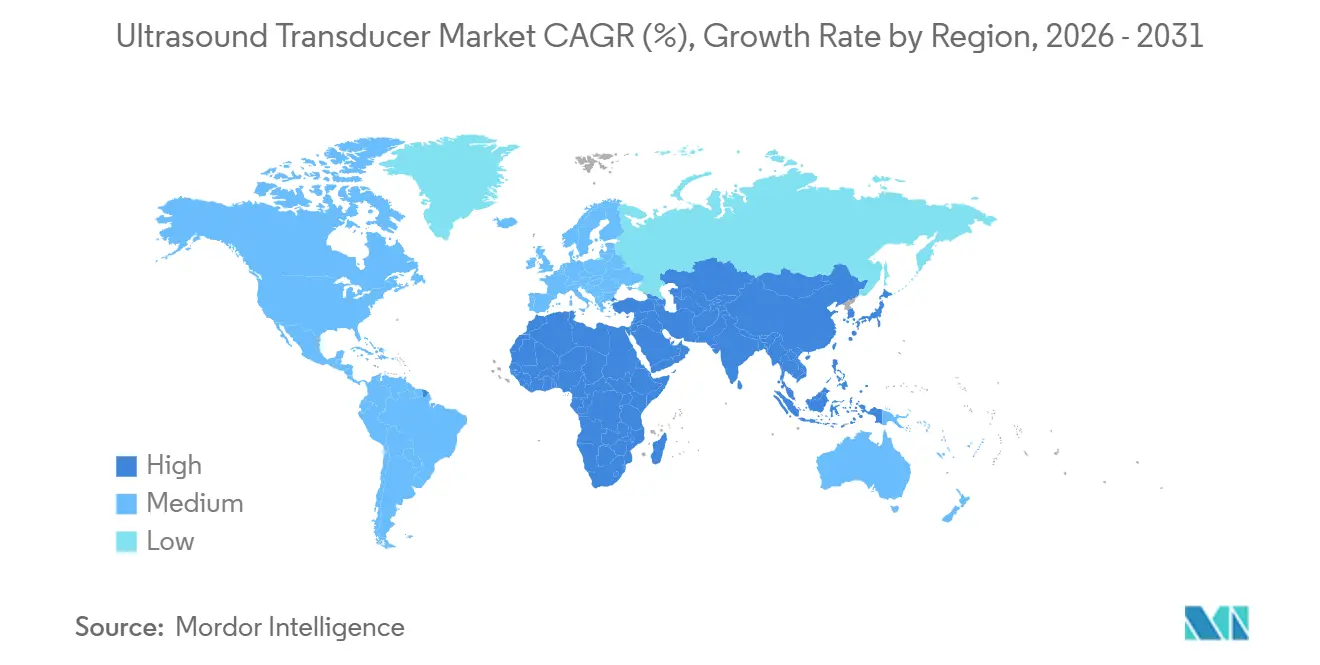

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrasound Transducer Market Analysis by Mordor Intelligence

The Ultrasound Transducer Market size is expected to increase from USD 4.15 billion in 2025 to USD 4.24 billion in 2026 and reach USD 5.06 billion by 2031, growing at a CAGR of 3.59% over 2026-2031.

The market's steady expansion conceals a structural shift from piezoelectric hospital consoles toward silicon-based arrays that power handheld, AI-enabled devices for bedside and home imaging. Demand is migrating from bulky, console-based platforms toward silicon-etched arrays that power pocket-sized, AI-enabled scanners. Semiconductor scale is lowering costs and enabling lead-free designs, while regulatory shifts such as the EU’s RoHS directive and China’s 2024 device-registration overhaul are accelerating adoption of next-generation architectures. Providers in emergency and critical-care settings are embedding handheld ultrasound into triage, and cloud-connected ecosystems now link home-health agencies with supervising clinicians. National manufacturing incentives in India, China, and Germany are localizing supply chains for piezoelectric wafers and CMUT chips, easing bottlenecks exposed during the semiconductor crunch.

Key Report Takeaways

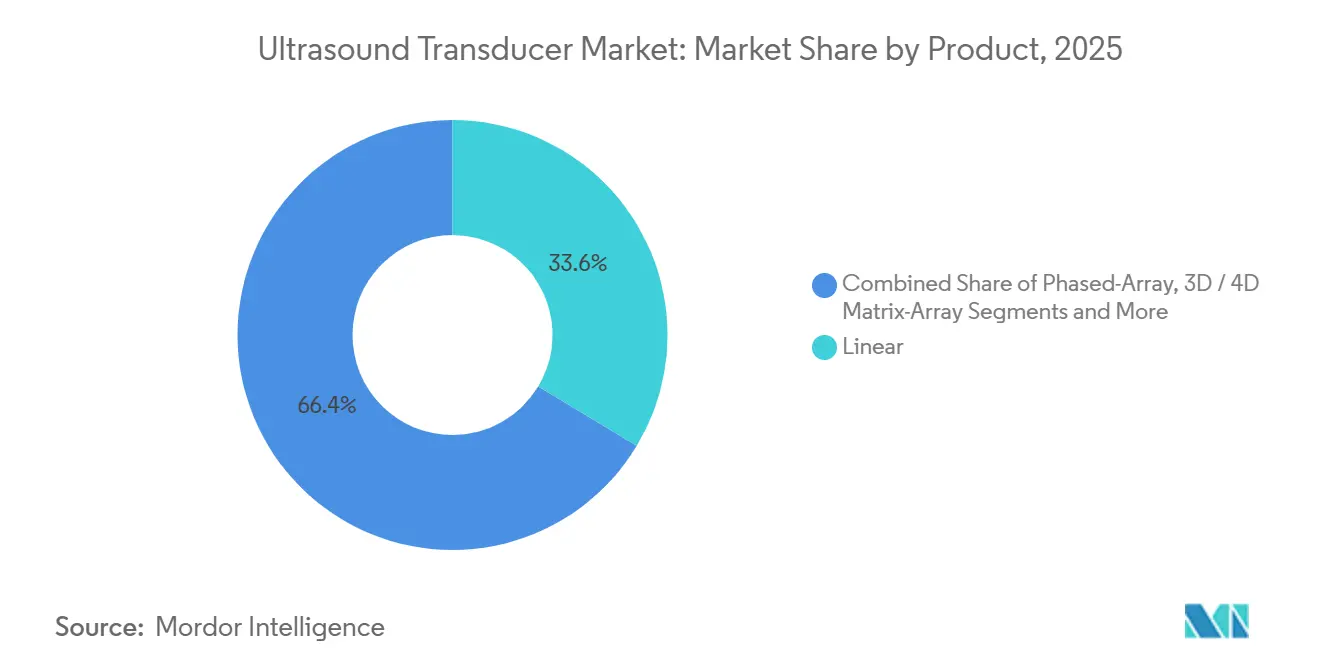

- By product category, linear probes led with 33.62% revenue share in 2025; 3D/4D matrix-array probes are on track to register a 7.25% CAGR through 2031.

- By technology, piezoelectric crystal designs captured 62.73% of the ultrasound transducer market share in 2025, whereas CMUT architectures are forecast to expand at a 6.14% CAGR to 2031.

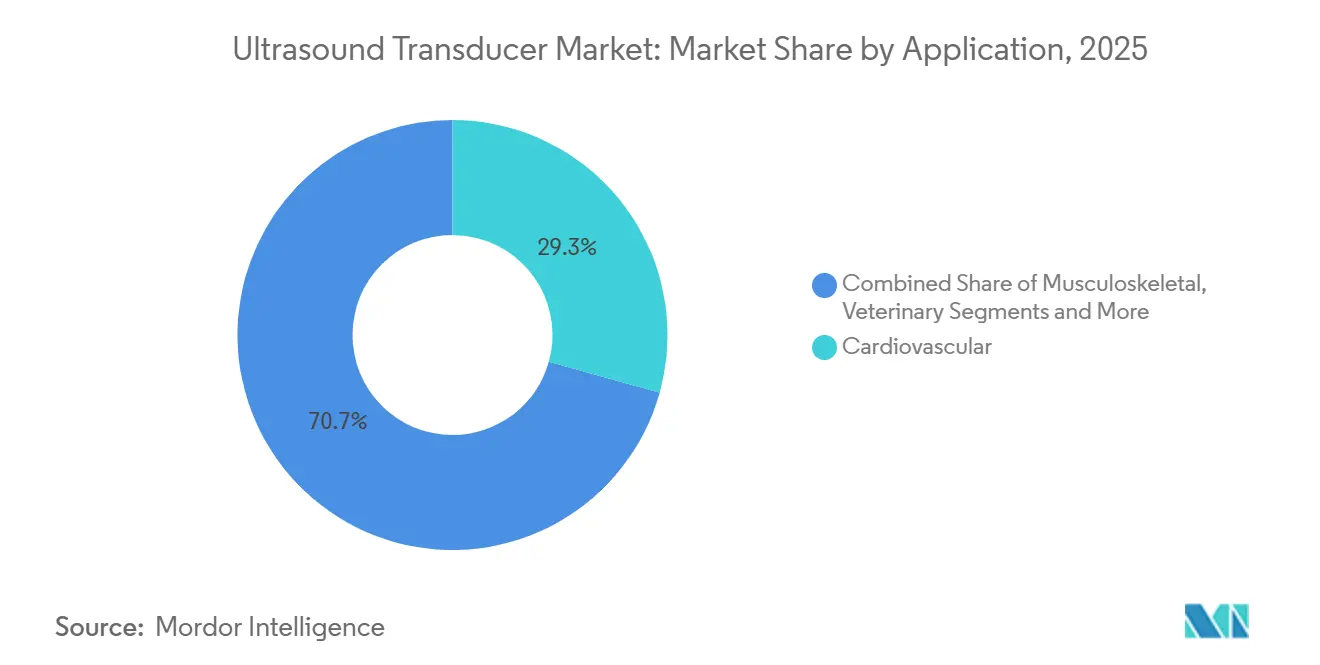

- By application, cardiovascular imaging held 29.32% of the ultrasound transducer market size in 2025 and point-of-care use cases are growing at a 6.25% CAGR during the outlook period.

- By end user, hospitals commanded 54.73% of 2025 revenue; home-healthcare settings represent the fastest trajectory with a 7.84% CAGR through 2031.

- By geography, Asia-Pacific generated 32.68% of 2025 revenue and is expected to post a 6.74% CAGR, the highest among regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ultrasound Transducer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid migration toward minimally invasive & image-guided interventions | 0.8% | Global, with concentration in North America & EU advanced surgical centers | Medium term (2-4 years) |

| Growing prevalence of cardiovascular & abdominal disorders | 0.7% | Global, highest burden in Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| Expanding obstetric screening in emerging economies | 0.5% | Asia-Pacific core (India, Southeast Asia), spill-over to Sub-Saharan Africa | Medium term (2-4 years) |

| Increasing average maternal age in developed regions | 0.4% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Surge in AI-assisted point-of-care (POC) ultrasound adoption | 0.9% | North America & EU early adopters, rapid diffusion to Asia-Pacific urban centers | Short term (≤ 2 years) |

| Supply-chain localization for piezoelectric crystals amid trade tensions | 0.3% | National initiatives in Germany, India, China; spillover to allied manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Migration Toward Minimally Invasive & Image-Guided Interventions

Interventional teams are dropping fluoroscopy in favor of real-time ultrasound for biopsies, ablations, and catheter navigation, reducing radiation exposure and shortening case times. Olympus obtained FDA clearance for the EU-ME3 ultrasound endoscope in 2025, enabling simultaneous imaging and tissue sampling of pancreatic lesions without external probes.[1]Olympus Corporation, “EU-ME3 Ultrasound Endoscopy System,” olympus-global.com Robotic platforms have begun integrating small-footprint transducers on articulating arms, letting surgeons delineate tumor margins during partial nephrectomies. These workflows push demand for high-frequency (≥20 MHz), sterilizable, or single-use probes that withstand autoclave cycles. Adoption is most pronounced in North America and Western Europe, where ambulatory centers compete on throughput and radiation-free protocols.

Growing Prevalence of Cardiovascular & Abdominal Disorders

Ischemic heart disease caused 9 million deaths in 2021, while 193 million disability-adjusted life years were lost to cardiovascular ailments worldwide. Echocardiography remains the first-line modality, sustaining demand for phased-array and CW Doppler probes. Ultromics secured FDA clearance for its EchoGo Heart Failure algorithm, which autonomously measures ejection fraction and detects HFpEF from routine views, widening access to cardiac diagnostics. Emerging economies face the greatest disease burden, spurring government tenders for portable echo systems.

Expanding Obstetric Screening in Emerging Economies

WHO’s 2024 antenatal guidelines recommend at least two ultrasound scans per pregnancy, prompting mobile programs across India, Indonesia, and Nigeria. Mindray’s Nuewa R9 Platinum, registered in the Philippines in 2025, links village health workers to remote radiologists via the MiCo+ cloud, raising probe volumes where durability and low cost trump advanced features.

Increasing Average Maternal Age in Developed Regions

In 2024, first-time mothers at Allegheny Health Network's (AHN) labor and delivery units in the U.S. averaged 31.1 years, surpassing the national average by over three years, as reported by the 14-hospital system.[2]Press Release, “Average Age of First-Time Mothers at AHN Labor and Delivery Units Climbs to 31 Years in 2024, Higher Than National Average,” PR Newswire, prnewswire.com Another national report highlighted that in 2023, the average age for first-time mothers nationwide in the United States was 27.5 years, with large metropolitan counties seeing an average of 28.5 years.[3]Andrea D. Brown, “Trends in Mean Age of Mothers: United States, 2016–2023,” National Vital Statistics Reports, cdc.gov Advanced maternal age drives additional ultrasounds for anomaly, Doppler, and nuchal translucency exams. Japan and South Korea report even higher averages, sustaining demand for high-frequency linear and 3D/4D matrix-array probes capable of resolving 2-millimeter fetal structures. Philips and GE bundle automated biometry and AI anomaly detection to convert demographic trends into recurring software revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of premium ultrasound platforms | -0.6% | Global, most acute in price-sensitive Asia-Pacific and Sub-Saharan Africa markets | Short term (≤ 2 years) |

| Reimbursement gaps for outpatient ultrasound procedures | -0.5% | North America, with spillover to private-payer markets in Latin America and Middle East | Medium term (2-4 years) |

| Shortage of trained sonographers, especially in rural settings | -0.4% | Global, highest impact in rural North America, Sub-Saharan Africa, and South Asia | Long term (≥ 4 years) |

| Limited global capacity for single-crystal piezoelectric materials | -0.3% | Global supply-chain constraint affecting premium transducer production | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Premium Ultrasound Platforms

Budgets at community hospitals remain tight, discouraging replacement of legacy consoles that have reached end-of-service life. Premium systems with matrix-array probes, elastography, and AI can top USD 200,000. Butterfly’s iQ3, introduced in 2024 at under USD 2,500, shows how CMUT designs can collapse costs, but handheld units sacrifice penetration depth for obese patients. Lease and pay-per-scan models ease barriers in high-income regions but lag in markets where credit is scarce.

Reimbursement Gaps for Outpatient Ultrasound Procedures

CMS cut the Medicare conversion factor by 2.8% in 2025 and applied a 2.5% efficiency adjustment to work RVUs in the 2026 final rule, crimping margins for office-based echocardiography and vascular studies. Private payers in Latin America and the Gulf typically follow CMS changes with a delay, signaling sustained pressure through 2028. Providers are shifting to higher-acuity procedures that pay better, concentrating demand on specialized probes and leaving general imaging exposed to volume declines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Matrix Arrays Drive Volumetric Imaging

3D/4D matrix-array probes are growing at 7.25%, the fastest across product categories, as obstetricians demand volumetric fetal screening and cardiologists quantify real-time valve regurgitation. Linear probes maintained a 33.62% share in 2025, favored for musculoskeletal and vascular imaging. Convex arrays dominate abdominal and obstetric work, while phased-array probes underpin cardiac imaging. Intracardiac and intravascular catheters command premium prices above USD 1,000 per case, critical to electrophysiology and coronary interventions. CMUT-based handhelds, powered by Infineon’s one-chip solution, streamline manufacturing and meet RoHS lead-free mandates. Veterinary and HIFU applications extend product diversity, and disposable probes gain traction where reprocessing costs approach USD 40 per cycle.

By Technology: CMUT Challenges Piezoelectric Dominance

Piezoelectric crystal designs still account for 62.73% of 2025 revenue, yet CMUT architectures are rising 6.14% yearly by leveraging semiconductor lithography and eliminating toxic lead. Butterfly’s Ultrasound-on-Chip exemplifies monolithic integration and RoHS compliance. PMUT designs blend thin-film piezo layers with silicon substrates for dermatology and ophthalmology applications demanding sub-50-micron resolution. Disposable and MRI-compatible probes carve out infection-control and interventional niches, broadening the technology palette.

By Application: Point-of-Care Outpaces Traditional Radiology

Point-of-care workflows grow at 6.25%, fueled by handheld devices and FDA-cleared AI aids. Cardiovascular work still leads with a 29.32% revenue share. Musculoskeletal imaging penetrates sports medicine and pain clinics with high-frequency probes, while WHO antenatal guidelines lock in baseline obstetric demand. Urology benefits from AI-guided transrectal biopsies, and oncology expands through HIFU guidance. Veterinary usage widens the application scope, especially in large-animal reproduction.

By End User: Home Healthcare Disrupts Hospital Hegemony

Hospitals commanded 54.73% of 2025 revenue, but home-healthcare programs are advancing at 7.84% as remote monitoring pairs handheld ultrasound with cloud analytics. Diagnostics centers and ambulatory surgical centers capture share with shorter wait times. Philips Lumify and Exo Iris empower caregivers to capture diagnostic-grade images in patient homes, a model further enabled by CMS’ virtual direct supervision policy.

Geography Analysis

Asia-Pacific generated 32.68% of 2025 revenue and is poised for a 6.74% CAGR through 2031. India’s Production-Linked Incentive program triggered 19 greenfield projects, including Siemens Healthineers’ INR 91.9 crore (USD 11 million) ultrasound plant announced in May 2025, while Medtronic earmarked USD 350 million to enlarge its Hyderabad campus in March 2024, reinforcing confidence in local supply chains. China’s 2024 device-regulation revision accelerated Fujifilm’s USD 120 million Suzhou expansion and cleared Olympus to register an advanced gastroscope with an integrated transducer in August 2025. Samsung Medison unveiled the R20 premium scanner at RSNA 2025, highlighting Seoul’s push for AI-centric imaging exports. Japan’s AMED continues to fund elastography and photoacoustic prototypes, ensuring a pipeline of high-frequency transducer innovations. Australia’s Therapeutic Goods Administration aligns with EU MDR pathways, preserving streamlined entry for systems already cleared in Europe. Collectively, the region blends domestic manufacturing incentives, regulatory reform, and chronic-disease demand to sustain above-average growth.

North America and Europe remain major revenue pools but advance at below-trend rates as reimbursement pressure curbs capital budgets. CMS cut the Medicare conversion factor by 2.8% in 2025 and applied a 2.5% efficiency adjustment in the 2026 fee schedule, dampening outpatient upgrade cycles. Philips partnered with Mass General Brigham in February 2025 to harvest de-identified echo and vascular data for AI training, illustrating how software ecosystems offset hardware margin compression. Germany’s EUR 700 million microelectronics plan, announced in October 2025, seeks local piezoelectric wafer capacity and less reliance on Asian suppliers.

Middle East & Africa and South America post the sharpest epidemiologic shifts yet wrestle with funding gaps and regulatory complexity. Gulf Cooperation Council hospitals are importing premium consoles under broader diversification agendas, while refurbished units dominate procurement in Sub-Saharan clinics. Brazil’s ANVISA shortened approval timelines to nine months, encouraging distributors to stock newer probes that meet ISO 13485 requirements. Argentina’s currency volatility steers buyers toward extended service contracts, and South Africa’s SAHPRA alignment with WHO prequalification facilitates faster entry for FDA-cleared handhelds, positioning distributed imaging as a solution for rural access constraints.

Competitive Landscape

The ultrasound transducer market shows moderate fragmentation. Philips forged interoperability deals with ventilator and anesthesia vendors in July 2025, embedding ultrasound data into broader care ecosystems. GE Healthcare’s Venue R6, launched in September 2025, ships with Verisound AI, tapping its 500,000-unit installed base for recurring software income. Mindray pushes into premium tiers via the Nuewa R9 Platinum cloud-connected system. New entrants leverage chip economics and AI: Infineon’s one-chip CMUT shrinks bill-of-materials by 30%, and Exo pairs SweepAI with Samsung Medison manufacturing scale. Veterinary and HIFU segments remain open for niche innovators.

Ultrasound Transducer Industry Leaders

Koninklijke Philips N.V

Siemens Healthineers

Canon Medical Systems

GE Healthcare

Fujifilm Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Samsung Medison introduced the R20 ultrasound system at RSNA 2025, offering AI-driven diagnostics and validated ergonomic updates.

- October 2025: Germany allocated EUR 700 million to expand microelectronics capacity for piezoelectric materials, strengthening regional supply resilience.

- June 2025: Verasonics added new configurations and an Acquisition SDK to its Vantage NXT research platform.

Global Ultrasound Transducer Market Report Scope

As per the scope of the report, an ultrasound transducer is a probe that produces sound waves and makes echoes. The device is used in surgical, diagnostic, and non-invasive procedures.

The ultrasound transducer market is segmented by product, technology, application, end user, and geography. By product, the market is segmented into Convex, Linear, Endocavitary, Phased-Array, CW Doppler, High-Frequency Linear, 3D/4D Matrix-Array, ICE/IVUS, CMUT, and Others. By Technology, the market is segmented into Piezoelectric Crystal, CMUT, PMUT, Single-Use, and MRI-Compatible. By Application, the market is segmented into Cardiovascular, Musculoskeletal, OB/GYN, General Imaging, Point-of-Care, Urology, Oncology, Veterinary, and Others. By End User, the market is segmented into Hospitals, Diagnostic Centers, ASCs, Home Healthcare, Veterinary Clinics, and Others. By Geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Convex (Curvilinear) |

| Linear |

| Endocavitary (Transvaginal & Transrectal) |

| Phased-Array |

| Continuous-Wave (CW) Doppler |

| High-Frequency Linear (≥20 MHz) |

| 3D / 4D Matrix-Array |

| Intracardiac & Intravascular (ICE/IVUS) |

| Capacitive Micromachined Ultrasonic Transducers (CMUT) |

| Others |

| Piezoelectric Crystal |

| CMUT |

| PMUT |

| Single-Use / Disposable |

| MRI-Compatible |

| Cardiovascular |

| Musculoskeletal |

| OB/GYN & Prenatal |

| General Imaging |

| Point-of-Care & Emergency Medicine |

| Urology & Prostate |

| Oncology |

| Veterinary |

| Others |

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Home Healthcare Settings |

| Veterinary Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Convex (Curvilinear) | |

| Linear | ||

| Endocavitary (Transvaginal & Transrectal) | ||

| Phased-Array | ||

| Continuous-Wave (CW) Doppler | ||

| High-Frequency Linear (≥20 MHz) | ||

| 3D / 4D Matrix-Array | ||

| Intracardiac & Intravascular (ICE/IVUS) | ||

| Capacitive Micromachined Ultrasonic Transducers (CMUT) | ||

| Others | ||

| By Technology | Piezoelectric Crystal | |

| CMUT | ||

| PMUT | ||

| Single-Use / Disposable | ||

| MRI-Compatible | ||

| By Application | Cardiovascular | |

| Musculoskeletal | ||

| OB/GYN & Prenatal | ||

| General Imaging | ||

| Point-of-Care & Emergency Medicine | ||

| Urology & Prostate | ||

| Oncology | ||

| Veterinary | ||

| Others | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Home Healthcare Settings | ||

| Veterinary Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the ultrasound transducer market in 2026?

The ultrasound transducer market size reached USD 4.24 billion in 2026 and is projected to rise to USD 5.06 billion by 2031.

Which product type leads revenue?

Linear probes led with 33.62% of 2025 revenue, but 3D/4D matrix-array probes are the fastest growing.

What region is expanding the fastest?

Asia-Pacific is forecast to grow at a 6.74% CAGR through 2031, buoyed by local manufacturing incentives.

Who are the major players?

GE Healthcare, Philips, Siemens Healthineers, Canon Medical Systems, and Mindray together hold about 45% of revenue.

How is AI influencing adoption?

More than 30 FDA-cleared AI algorithms now automate image interpretation, lowering skill barriers and accelerating point-of-care use.

What hampers wider uptake?

High upfront costs, reimbursement cuts, a sonographer shortage, and limited supply of single-crystal piezo materials restrain growth.

Page last updated on: