Ultrasonic Electrosurgery Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

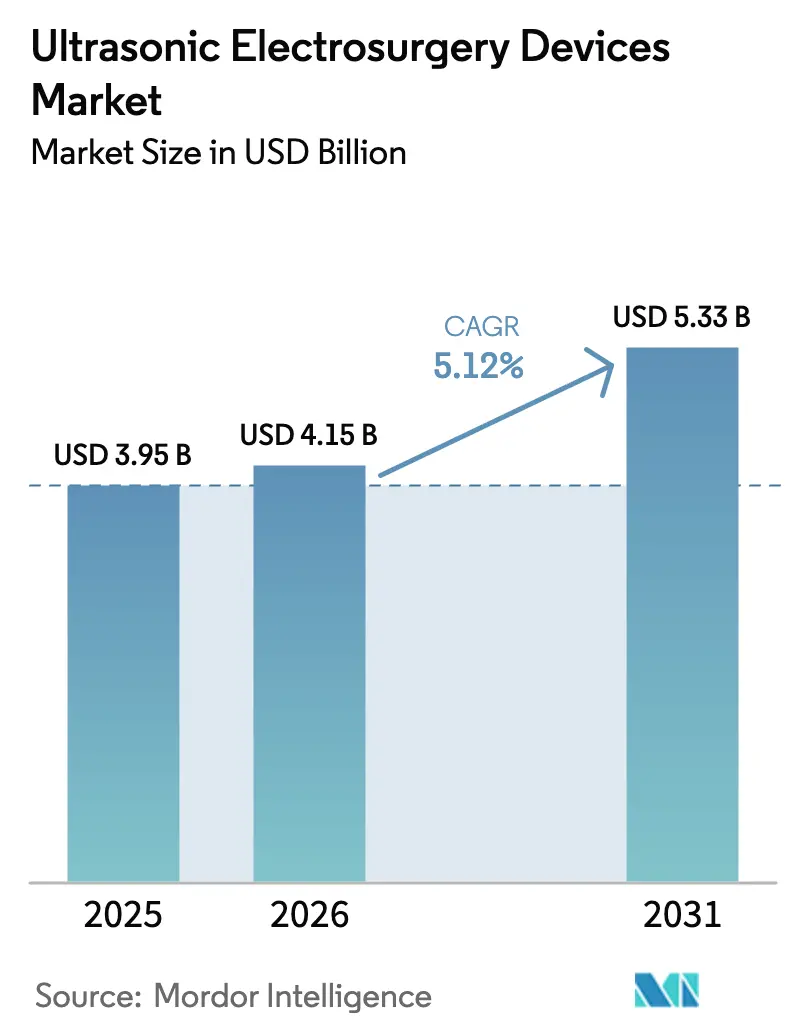

| Market Size (2026) | USD 4.15 Billion |

| Market Size (2031) | USD 5.33 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrasonic Electrosurgery Devices Market Analysis by Mordor Intelligence

The Ultrasonic Electrosurgery Devices Market size is expected to increase from USD 3.95 billion in 2025 to USD 4.15 billion in 2026 and reach USD 5.33 billion by 2031, growing at a CAGR of 5.12% over 2026-2031.

Demand grows as hospitals upgrade to multi-energy platforms, ambulatory centers chase higher-margin outpatient cases, and payers reward opioid-sparing technologies. Robot-assisted surgery expands procedure throughput and pushes device makers to engineer articulated ultrasonic tips that fit robotic wrists. Regional reimbursement changes, such as the United States CY2025 separate payments for non-opioid devices, directly accelerate capital purchases. Platform refinements that lower residual heat and extend pad life sustain premium pricing as surgeons and risk managers track thermal-spread incident reports. Niche players focusing on ENT microsurgery and orthopedic debridement widen product choice, yet the largest four suppliers still command the bulk of revenue.

Key Report Takeaways

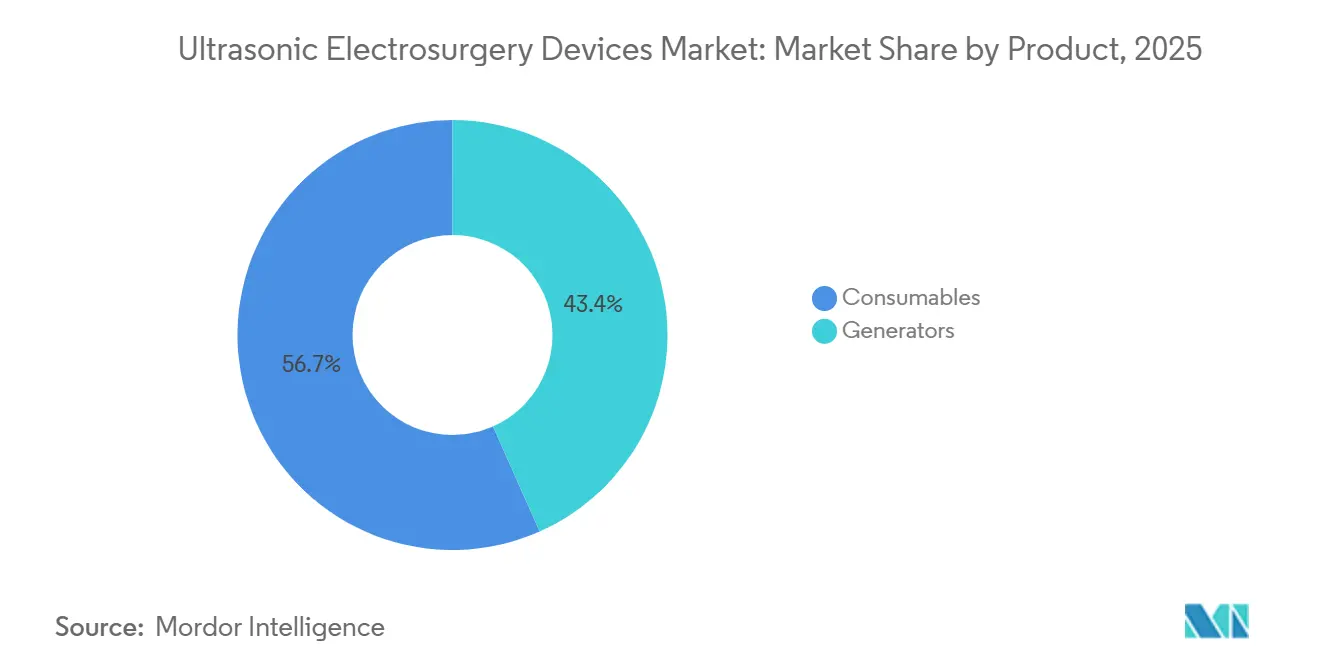

- By product type, consumables led with 56.65% of the ultrasonic electrosurgery devices market share in 2025, while generators recorded the fastest 7.54% CAGR through 2031.

- By procedure, minimally invasive surgery accounted for 63.21% of the ultrasonic electrosurgery devices market in 2025, and robot-assisted workflows are advancing at a 7.86% CAGR through 2031.

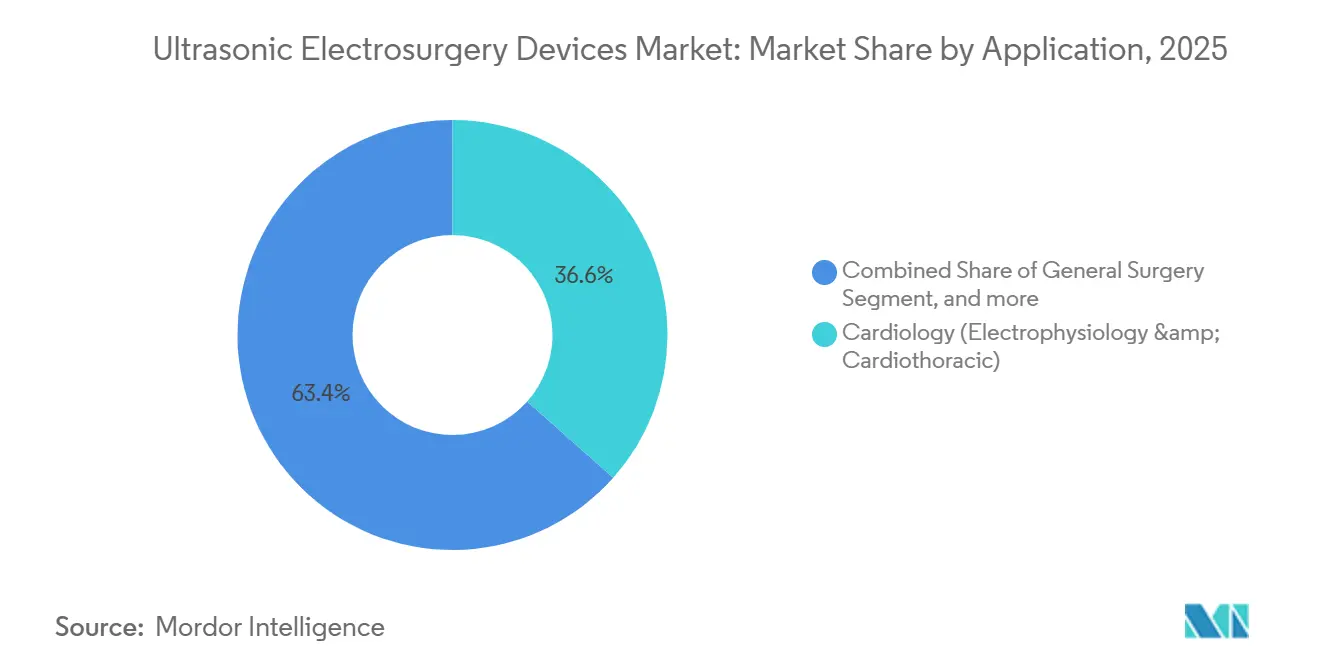

- By application, cardiology accounted for 36.56% of the ultrasonic electrosurgery devices market in 2025, and gynecology is expanding at an 8.55% CAGR through 2031.

- By type, HIFU ablators secured a 42.2% share in 2025, and ultrasonic surgical ablation systems are forecast to rise at a 7.45% CAGR to 2031.

- By end user, ambulatory surgical centers accounted for 58.24% of revenue in 2025, yet hospitals posted the highest 8.32% CAGR through 2031 as they replace legacy energy platforms.

- By geography, North America captured 40.43% share in 2025, whereas Asia-Pacific is projected to grow at a 6.54% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ultrasonic Electrosurgery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Surgical Procedure Volume | +1.2% | Global with focus on Asia-Pacific and North America | Medium term (2-4 years) |

| Growing Preference for Minimally Invasive Surgery | +1.5% | Global led by North America and Europe | Short term (≤ 2 years) |

| Technological Advancements in Ultrasonic Energy Platforms | +0.9% | Global with hubs in North America, Europe, Japan | Long term (≥ 4 years) |

| Expanding Ambulatory Surgical Center Footprint Worldwide | +0.8% | North America and emerging Asia-Pacific and South America | Medium term (2-4 years) |

| Integration with Robotic and AI-Guided Surgical Systems | +0.7% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Increasing Geriatric Population and Chronic Disease Incidence | +0.6% | Global, acute in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Surgical Procedure Volume

Hospitals performed almost 599 000 bariatric operations in 2021, up from 508 000 in 2020, while sleeve gastrectomy accounted for about 70% of cases and robot assistance reached 30% of United States procedures by 2022. Swedish registries also logged steady growth in atrial fibrillation ablations, confirming broader procedural expansion that directly lifts ultrasonic dissection demand. Meta-analysis shows these systems save an average 19.78 minutes of operative time and 45.25 mL of blood loss compared with conventional electrosurgery[1]National Evidence-based Healthcare Collaborating Agency, “Comparative Effectiveness of Vessel Sealing Systems,” neca.kr. The sharpest rise appears in Asia-Pacific where aging populations and chronic diseases fuel operating room volumes, prompting hospitals to invest in platforms that process more cases per theater.

Growing Preference for Minimally Invasive Surgery

Minimally invasive techniques captured 63.21% of 2025 revenue, supported by persistent shifts from inpatient to outpatient settings documented in United States Healthcare Cost and Utilization Project data. In a 265-patient trial completed December 2024, Ethicon Harmonic 1100 achieved 99% hemostasis, reinforcing its alignment with laparoscopic workflows. A 2024 study from Iran found higher postoperative hemoglobin and fewer complications when harmonic instruments replaced monopolar tools during hysterectomy. CMS separate payments for non-opioid devices effective January 2025 create a direct reimbursement tailwind for ultrasonic solutions that curb opioid use.

Technological Advancements in Ultrasonic Energy Platforms

Olympus launched THUNDERBEAT II in October 2025, adding a distal thermal shield that lowers probe temperature by 26.9% and three selectable energy modes, therefore limiting instrument exchanges during complex cases. Ethicon’s Harmonic 700 preclinical release in May 2024 showed 24-fold longer pad life and faster transection than its predecessor, addressing durability complaints seen in FDA MAUDE reports. InSightec Exablate continues to win multiyear FDA approvals for new ablation indications, blending high-intensity focused ultrasound with MR imaging for real-time verification. Hospitals reward these innovations with generator upgrades, explaining the 7.54% CAGR expected for capital equipment through 2031.

Expanding Ambulatory Surgical Center Footprint Worldwide

CMS granted a 2.9% payment increase for about 6 100 United States ASCs in its CY2025 rule and opened pass-through code C8000 for novel energy devices in October 2024. ASC revenue already topped 58.24% in 2025 and is tracking an 8.32% CAGR as operators target profitable outpatient volumes and payers approve broader procedure lists. Device offset policies introduced in January 2024 deduct high consumable costs from payments, making bundled pricing and reprocessed handpieces critical for suppliers that court this channel. Rapid ASC deployments in Singapore, South Korea, and Australia mirror the United States model, giving manufacturers additional high-growth arenas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Consumable Costs of Ultrasonic Systems | -0.6% | Global, acute in cost-sensitive Asia-Pacific and MEA | Short term (≤ 2 years) |

| Stringent Multiregional Regulatory Approval Processes | -0.4% | Global with delays in Asia-Pacific and EU | Medium term (2-4 years) |

| Limited Availability of Ultrasonically Trained Surgeons | -0.5% | Global, most severe in emerging Asia-Pacific and MEA | Medium term (2-4 years) |

| Competition from Alternative Energy-Based Surgical Modalities | -0.3% | Global, intense in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Consumable Costs of Ultrasonic Systems

Generator platforms cost USD 15 000 to USD 40 000 and single-use handpieces run USD 200 to USD 600, straining ASC budgets even after the CMS 2.9% payment bump. January 2024 device offset rules further deduct consumable expenses from payments, tightening margins unless centers negotiate bundle discounts. Stryker won July 2024 clearance to sell reprocessed Harmonic shears at 30% to 50% discounts, offering an immediate workaround for budget-pressed providers. Tiered product portfolios that keep entry pricing low without cannibalizing premium hospital lines have become a must-have for vendors.

Stringent Multiregional Regulatory Approval Processes

China upgraded ultrasonic soft-tissue devices to Class III in August 2023, adding clinical trial mandates that can stretch approvals by up to two years[2]National Medical Products Administration, “Notice on Adjustment of Classification Catalogue,” nmpa.gov.cn. Japan’s PMDA demands JIS T 0601 electrical safety conformity and local labeling, often requiring an extra year for clearance. Europe’s MDR, enforced since May 2021, leaves only 30 notified bodies available for Class IIb and III assessments, bottlenecking launches. Smaller firms therefore stage entries, focusing first on home markets until revenue can fund broader compliance programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Generators Expand Margin While Consumables Drive Volume

Consumables controlled 56.65% revenue in 2025, powered by per-procedure demand for active blades, shears, and handpieces, yet generators deliver higher gross margin and will grow at 7.54% CAGR through 2031. Hospitals invest because multi-energy consoles eliminate the need to dock separate ultrasonic and bipolar units. Olympus THUNDERBEAT II adds a standalone ultrasonic mode that surgeons toggle without exchanging tools, proving the premium generator case. The ultrasonic electrosurgery devices market size for generators is set to climb steadily as facilities retire single-energy consoles.

Active blades remain the largest consumable sub-segment because they are mandatory in laparoscopy, gynecology, and oncology. Reprocessed options threaten new-unit sales, evidenced by Stryker’s July 2024 FDA clearance that lets ASCs cut costs by half. Vendors respond with durability claims such as the Harmonic 700’s 24-fold longer pad life. Accessory bundles, including footswitches and cables, secure the ultrasonic electrosurgery devices market share of incumbents by locking buyers into proprietary connectors.

By Type: HIFU Dominates Share While Surgical Ablation Systems Lead Growth

HIFU ablators captured 42.2% share in 2025 on the back of InSightec Exablate approvals for essential tremor, uterine fibroids, and bone metastases. These systems integrate MR imaging that guides real-time energy deposition which helps avoid collateral damage. Ultrasonic surgical ablation platforms will accelerate at 7.45% CAGR as oncology and orthopedic surgeons adopt probes that blend cutting, coagulation, and cavitation. The ultrasonic electrosurgery devices market size for these applications gains from AI-driven planning that tailors pulse sequences to tissue impedance.

Shock wave therapy stays niche because reimbursement often runs flat, but orthopedic debridement devices from Bioventus and BOWA cut an opening in ENT micro-surgery niches. Chinese regulators now classify surgical ultrasound as Class III, delaying entry yet affirming state confidence in high-risk use. Vendors that clear that barrier stand to tap vast procedure volumes in China’s tertiary hospitals.

By Procedure: Robot-Assisted Workflows Accelerate Past Laparoscopic Base

Minimally invasive surgery owned 63.21% of 2025 revenue, backed by clear data on faster recovery and reduced pain. Robot-assisted workflows will post the quickest 7.86% CAGR due to expanding da Vinci installations and new entrants such as KARL STORZ LUNA. Ultrasonic device makers must therefore design articulated tips compatible with robotic wrists or seek partnerships. The ultrasonic electrosurgery devices market share for open surgery slips steadily but remains relevant for trauma and tumor debulking where tactile control matters.

Clinical evidence keeps stacking up. The December 2024 Harmonic 1100 trial reported 99% intraoperative hemostasis, underscoring suitability for laparoscopy. Robotic suits currently rely on bipolar sealers, leaving a white space that generators with end-effector intelligence can occupy. Medtronic’s cordless Sonicision 7 platform signals this pivot although no formal robotic tie-ins exist yet.

By Application: Cardiology Still Leads While Gynecology Races Ahead

Cardiology retained 36.56% of 2025 demand, fueled by atrial fibrillation ablation growth and ultrasonic tools that limit myocardial collateral injury. Gynecology will sprint at an 8.55% CAGR as outpatient hysterectomies migrate to ASC settings and evidence mounts that ultrasonic dissection cuts blood loss. The ultrasonic electrosurgery devices market size for oncology also accelerates because MR-guided focused ultrasound avoids open resection in select liver and kidney tumors.

Bariatric surgery in the United States reached 280 000 cases in 2022, with robotic shares growing, and each sleeve gastrectomy typically consumes one or two ultrasonic shears. ENT microsurgery benefits from low thermal spread that protects cranial nerves. Orthopedic bone cutting uses a smaller but steady volume, aided by osteotomy precision in spine fusion procedures.

By End User: Hospitals Maintain Revenue Peak, ASCs Drive Incremental Growth

Hospitals produced 58.24% of revenue in 2025 thanks to complex oncology and cardiothoracic caseloads that demand full-featured generators. Yet ambulatory surgical centers will lift revenue fastest at 8.32% CAGR as CMS widens ASC-approved CPT codes and grants pass-through payments for novel devices. The ultrasonic electrosurgery devices industry adapts with compact generators and lower-cost handpiece packs tailored to space-constrained centers.

Specialty clinics focusing on urology or gynecology hold about 12% share and often serve self-pay patients who favor same-day discharge. Academic institutes drive early adoption of MR-guided focused ultrasound installations that exceed USD 2 million per room, funneling first-in-human data back to regulators and payers.

Geography Analysis

North America accounted for 40.43% of 2025 global revenue because Medicare’s 2.9% payment lift and the separate non-opioid device pathway directly reward ultrasonic adoption. Canada and Mexico add smaller totals, with Mexican private hospitals marketing bariatric and cosmetic bundles to inbound medical tourists. FDA de novo clearances for Exablate show regulator openness to non-invasive ablation, a factor that keeps capital pipelines healthy.

Asia-Pacific is on track for a 6.54% CAGR through 2031. Japan anchors regional revenue with Olympus Therapeutic Solutions sales above JPY 360 billion in FY2025 and local launches of THUNDERBEAT II. China’s Class III designation in August 2023 raises barriers but also signals official endorsement, prompting provincial hospitals to budget for high-risk soft-tissue systems. India, Australia, and South Korea follow with procedure growth tied to aging populations and expanding private insurance.

Europe holds about 28% of global takings. Germany, the United Kingdom, and France make up 60% of regional demand, yet MDR bottlenecks slow new platform rollouts. Olympus introduced THUNDERBEAT II across EU markets in October 2025, emphasizing lower probe temperature to satisfy surgeon safety concerns. Italy and Spain emphasize consumable-first procurement under austerity rules. South America and Middle East & Africa contribute the remainder, with Gulf Cooperation Council hospitals spending on energy upgrades and Brazilian importers offsetting tariffs through local assembly deals.

Regulatory Landscape

In the United States, ultrasonic electrosurgery devices typically route through the FDA 510(k) pathway (substantial equivalence) under surgical device regulations, with post-market obligations such as eMDR electronic adverse-event reporting. In February 2026, the FDA Quality Management System Regulation (QMSR) took effect, aligning 21 CFR Part 820 with ISO 13485:2016 and raising audit readiness and documentation rigor for manufacturers of generators, handpieces, and accessories. FDA clearance activity in January 2026 (for example, K251692 under 21 CFR 876.4300) also points to ongoing review cadence for energy-enabled surgical tools.

In Europe, the Medical Device Regulation (EU MDR 2017/745), enforced since May 2021, governs conformity assessment and classification (Annex VIII). Reusable surgical instruments fall under Class I, with Notified Body involvement limited to reusability aspects (cleaning, disinfection, sterilization). For higher-risk Class IIb and III ultrasonic ablation platforms, the limited pool of notified bodies continues to affect launch sequencing, as manufacturers balance MDR technical documentation and vigilance expectations alongside US FDA design controls and complaint-handling requirements.

Value Chain Analysis

The value chain starts with specialized upstream materials and components, including piezoelectric ceramics and transducer assemblies that drive ultrasonic energy conversion, as well as electronics (semiconductors), precision machined metals, and polymer housings used in generators and single-use instruments. Concentration of advanced piezoceramic capabilities in established industrial hubs (notably Japan and Germany) increases allocation risk and can expose OEMs to input price swings. Suppliers such as CeramTec and specialist transducer houses (for example, Piezo Technologies producing Langevin-style surgical transducers) sit at the critical component tier, where resonance stability and yield can determine finished-device performance.

Midstream, OEMs integrate transducers, power electronics, and software into capital generators and proprietary consumables, then validate sterilization, biocompatibility, and reliability before distribution via direct hospital/IDN sales, GPO-linked channels, and specialized distributors for ASCs. Downstream, service, repairs, and accessories support recurring revenue, while reprocessing programs and third-party service channels increasingly shape consumable economics. Operationally, ongoing device-supply-chain pressure and the FDA medical device shortages list reinforce the need for dual sourcing, safety-stock strategies, and written supply continuity commitments, especially for high-volume handpieces and tips used in minimally invasive and outpatient workflows.

Competitive Landscape

Ethicon, Medtronic, Stryker, and Olympus together command between 55% and 65% of worldwide revenue, a range that confirms moderate concentration. Olympus differentiates via THUNDERBEAT II which bundles three energy modes and a heat shield that cuts residual probe temperatures by 26.9%. Ethicon leans on Harmonic 700 improvements that extend pad life twenty-four times compared with the prior ACE+7 model.

KARL STORZ’s September 2024 buyout of Asensus gives it a robot capable of hosting ultrasonic handpieces and positions the firm against Intuitive Surgical which has yet to adopt ultrasound energy. Stryker disrupts consumable pricing with reprocessed Harmonic clearances that slice ASC costs by half. InSightec pioneers non-invasive MR-guided focused ultrasound that bypasses traditional ORs entirely and already owns multiple FDA approvals.

Smaller challengers such as BOWA-electronic, Bioventus, and Söring win niche shares in ENT and orthopedic debridement, often thriving in regions where import tariffs block bigger brands. Competitive advantage now pivots on integration. Vendors that combine AI-guided energy modulation, robotic articulation, and cross-modality generators lock in multiyear accounts as hospitals pursue single-vendor standardization.

Ultrasonic Electrosurgery Devices Industry Leaders

Medtronic

Boston Scientific Corporation

Olympus Corporation

Johnson & Johnson

Bioventus LLC (Misonix, Inc)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Platform consolidation and workflow integration are creating near-term whitespace in multi-energy operating rooms where hospitals standardize on fewer consoles and seek device-management software and uptime services. Johnson & Johnson MedTech's March 2025 launch of the DUALTO Energy System highlights this move toward modular, multi-modality footprints. As reimbursement mechanics strengthen outpatient surgery scrutiny on per-case costs, opportunities widen for bundled pricing, reprocessed offerings, and durability improvements that reduce instrument swaps.

Safety, traceability, and robotic compatibility remain key development vectors for vendor roadmaps. Recall activity in 2026 tied to mechanical failure and insulation defects in certain forceps and THUNDERBEAT II shear models points to demand for stronger insulation integrity, materials validation, and post-market surveillance readiness under the FDA QMSR and EU MDR. In parallel, academic work published in March 2026 on a miniature flextensional ultrasonic surgical device prototype integrated with a KUKA robot indicates continued miniaturization and articulated-tool design efforts, supporting differentiation for robot-assisted procedures where ultrasonic end effectors and feedback-controlled power modulation remain less adopted than bipolar sealing.

Recent Industry Developments

- June 2026: Reach Surgical (Genesis MedTech Group) received CE Mark approval for the SOUND REACH Swift ultrasonic shear for open surgical procedures. The approval expands the companys commercialization footprint in Europe and increases competitive pressure in cost- and workflow-focused open surgery segments where simplified setup and reduced handpiece management are procurement priorities.

- March 2025: Johnson & Johnson MedTech launched the DUALTO Energy System, integrating multiple energy modalities, including ultrasonic capability, into a modular platform for open and minimally invasive surgery. The launch supports operating room consolidation strategies and ties capital sales to service and fleet-management software, reinforcing multi-year account stickiness for platform vendors.

- December 2024: CMR Surgical launched an ultrasonic dissector instrument for its Versius surgical robotic system. Adding ultrasonic energy to a robotic ecosystem broadens surgeon tool choice in minimally invasive workflows and raises the bar for competing energy-device suppliers to deliver robotic-compatible tips and articulation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers ultrasonic electrosurgery devices used in clinical procedures to cut and seal tissue by converting ultrasonic energy into mechanical vibration and heat, which supports hemostasis and controlled dissection. We size the market in value terms based on sales of the core equipment and the procedure-linked disposables.

Scope exclusions: We exclude capital equipment and consumables that are not specific to ultrasonic energy delivery (such as general electrosurgery generators, standard laparoscopic tools, and non-surgical therapeutic ultrasound systems when they are not used as electrosurgery devices).

Segmentation Overview

- By Product

- Generators

- Consumables

- Active Blades & Shears

- Handpieces & Tips

- Accessories & Cables

- By Type

- HIFU Ablators

- MR-Guided FUS Ablators

- Ultrasonic Surgical Ablation Systems

- Shock Wave Therapy Systems

- Ultrasonic Dissection & Coagulation Systems

- By Procedure

- Minimally-Invasive / Laparoscopic Surgery

- Robot-Assisted Surgery

- Open Surgery

- By Application

- Cardiology (Electrophysiology & Cardiothoracic)

- Gynecology

- General Surgery

- Urology

- Bariatric Surgery

- Orthopedic Surgery

- Oncology (Tumor Ablation)

- Others (Neurosurgery, ENT)

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Academic & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with understanding procedure volumes and where ultrasonic energy devices are most used, and then mapping demand back to device adoption. We referenced public healthcare statistics and clinical utilization signals from sources such as the World Health Organization, the US FDA device database, the US Centers for Medicare and Medicaid Services procedure and payment files, and the OECD health statistics series.

To keep assumptions realistic, we also reviewed peer reviewed clinical literature (for use patterns in general surgery, gynecology, and urology), trade association publications, and medical device company filings and investor decks for mix and pricing commentary. For cross checking, we used paid subscriptions for company financials and intelligence, patent databases, and an import or export shipment level database where trade flows were relevant for specific countries. These desk sources are illustrative, and many other public and paid references were used to collect data, validate inputs, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on confirming what drives real purchasing and use, so we spoke with surgeons, operating room managers, procurement teams, and distributor or service partners across major regions. We used these discussions to validate adoption rates by procedure type, typical replacement and upgrade cycles for generators, and disposable usage per case, and then we aligned assumptions to what was observed in hospitals and ambulatory surgical centers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | APAC: 44% |

| Mid tier: 52% | Functional/Unit leaders: 40% | EMEA: 32% |

| Smaller Players: 14% | Managers: 48% | Americas: 24% |

Market-Sizing & Forecasting

Sizing began with a top-down build that reconstructed the addressable demand pool from procedure volumes that commonly use ultrasonic energy, followed by penetration rates and device utilization per site. To reach value, average selling prices were applied for generators and for key consumables, and then totals were distributed by region using hospital infrastructure indicators and surgical access patterns.

To keep the number grounded, we also ran selective bottom-up checks such as supplier revenue roll ups for the energy category, distributor channel checks, and sampled price x volume sanity tests for disposable pull-through. Inputs that mattered most included minimally invasive surgery volumes, hospital and ambulatory surgical center case mix, installed base and replacement timing for generators, disposable units per procedure, and observed ASP differences by region and tender versus non-tender channels.

For forecasting, scenario analysis was used around procedure growth and penetration, and then trends were tightened using exponential smoothing on the near-term run rate that interviewees considered achievable. When bottom-up signals were incomplete in smaller countries, gaps were handled through proxying from similar healthcare systems and then rechecked with local feedback before finalizing.

Data Validation & Update Cycle

Triangulation was done through a few clear checks that our team can repeat, including reconciling value totals against procedure-based demand, installed base logic, and supplier revenue direction. Outliers were flagged when regional growth or ASP movement broke from known reimbursement changes, import trends, or hospital budget signals, and those areas were sent back for another review.

Before sign-off, the model and assumptions go through stepwise analyst reviews, and respondents are re-contacted when a key input shifts beyond an agreed tolerance band. Reports are refreshed annually, and interim updates are made when major policy, pricing, or technology events materially change the outlook. Right before delivery, a final pass is completed so the numbers reflect the latest available information.

Mordor Intelligence's Ultrasonic Electrosurgery Devices Market Size Compared Against Other Published Estimates

It is normal to see different market values for ultrasonic electrosurgery devices because publishers do not always count the same product boundary, clinical use cases, and timing of the price base. Some estimates lean heavily on broad energy device categories, and others depend on limited regional snapshots, which can move the total up or down.

Procedure volume signals and disposable pull-through checks are what keep Mordor Intelligence tied to the surgical use case driven demand pool, and they also help keep non-surgical ultrasound and adjacent electrosurgery equipment from being counted by mistake. Differences usually come from whether shock-wave and focused ultrasound systems are treated as part of the same market, how consumables are valued (per case versus shipment value), and whether currency conversion and inflation are updated close to the base year or left unchanged for longer.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.95 B (2025) | |

| Industry Data Publisher A | USD 3.60 B (2023) | This figure is presented as a modality segment inside a broader electrosurgical units study, so product boundaries can shift depending on how mixed energy systems and overlapping categories are allocated. |

| Regional Consultancy B | USD 3.90 B (2025) | The estimate provides limited detail on inclusion rules and how consumables are valued, so totals can vary based on whether pricing is modeled per procedure or based on higher level revenue assumptions. |

The spread is mainly explained by category mapping and how procedure-linked consumables are treated in the value build. By keeping the scope tied to surgical ultrasonic energy devices and cross checking with utilization signals, our estimate stays traceable to repeatable steps that can be revisited as procedure mix and pricing change.

Key Questions Answered in the Report

What is the current value of the ultrasonic electrosurgery devices market?

The market stood at USD 4.15 billion in 2026 and is on course to reach USD 5.33 billion by 2031.

Which product category leads revenue today?

Consumables such as active blades and handpieces generated 56.65% of 2025 sales.

Which geographic region shows the fastest future growth?

Asia-Pacific is forecast to expand at a 6.54% CAGR through 2031, the quickest rate among all regions.

How are ambulatory surgical centers influencing purchase decisions?

ASCs now collect 58.24% of end-user revenue and grow at an 8.32% CAGR, encouraging suppliers to launch cost-optimized generators and reprocessed handpieces.

What technological feature is most critical in next-generation platforms?

Thermal management, exemplified by Olympus THUNDERBEAT II's 26.9% lower residual probe temperature, ranks highest among surgeon safety priorities.

Which application area is expected to grow the fastest?

Gynecology is projected to climb at an 8.55% CAGR through 2031, driven by outpatient hysterectomy migration and demonstrated reductions in blood loss.

Page last updated on: