Lung Exercise Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 4.40% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lung Exercise Machine Market Analysis by Mordor Intelligence

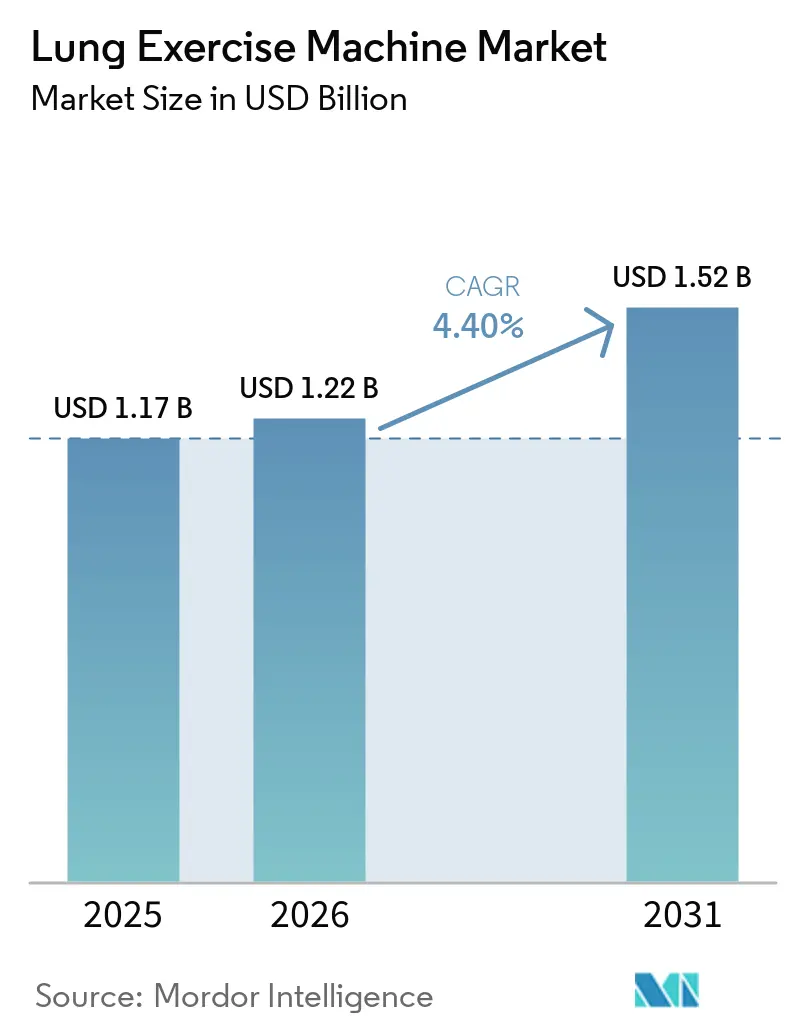

The Lung Exercise Machine Market size is projected to expand from USD 1.17 billion in 2025 and USD 1.22 billion in 2026 to USD 1.52 billion by 2031, registering a CAGR of 4.40% between 2026 to 2031.

The demand for pulmonary rehabilitation has remained strong in the post-pandemic period. Expanded coverage for at-home ventilation and the normalization of remote monitoring have shifted respiratory therapy from hospital settings into everyday routines. Developers are incorporating artificial intelligence engines to automate biofeedback, manage training progression, and track adherence, reflecting the growing importance of connected care as a core component of evidence-based practice. Clinicians are transitioning from passive volume-expansion tools to mechanical resistance devices that effectively strengthen inspiratory and expiratory muscles. Simultaneously, payers are aligning their strategies with these developments by recognizing virtual supervision and implementing outcome-based reimbursement models that incentivize reduced readmissions.

Key Report Takeaways

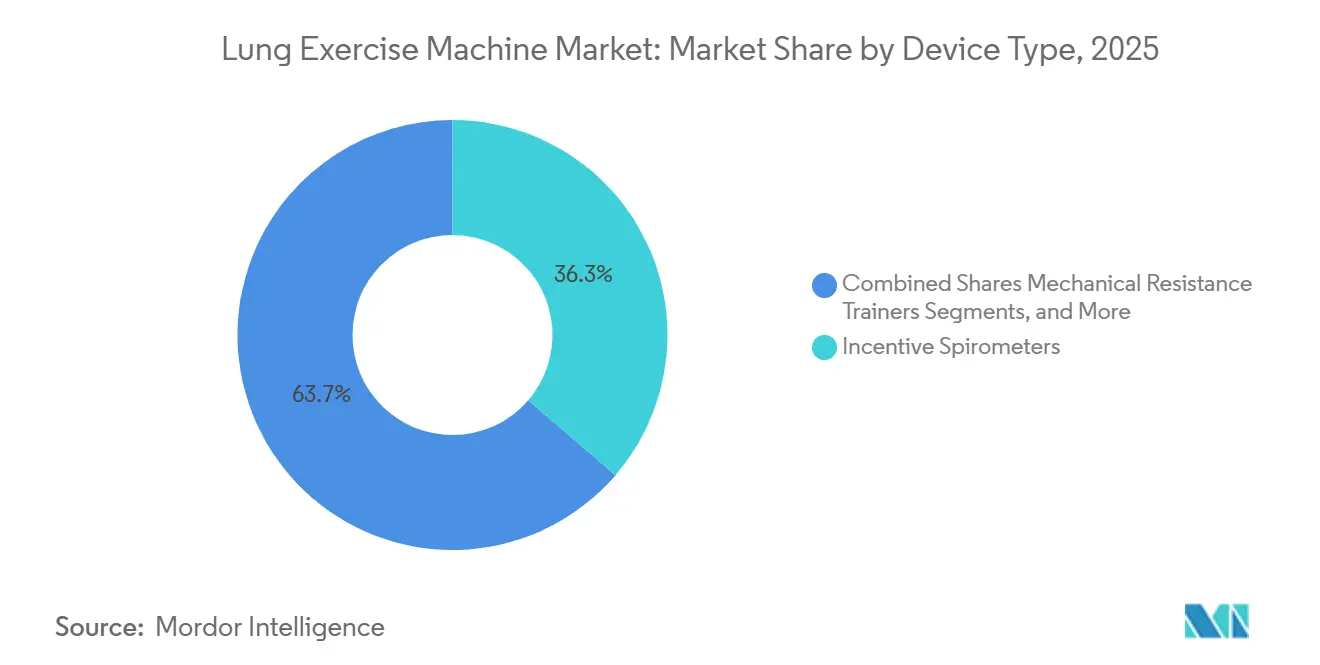

- By device type, incentive spirometers led with 36.3% of the lung exercise machine market share in 2025, and mechanical resistance trainers are projected to advance at a 4.67% CAGR through 2031.

- By application, post-operative pulmonary therapy accounted for 35.2% share of the lung exercise machine market size in 2025 and is rising at a 4.82% CAGR to 2031.

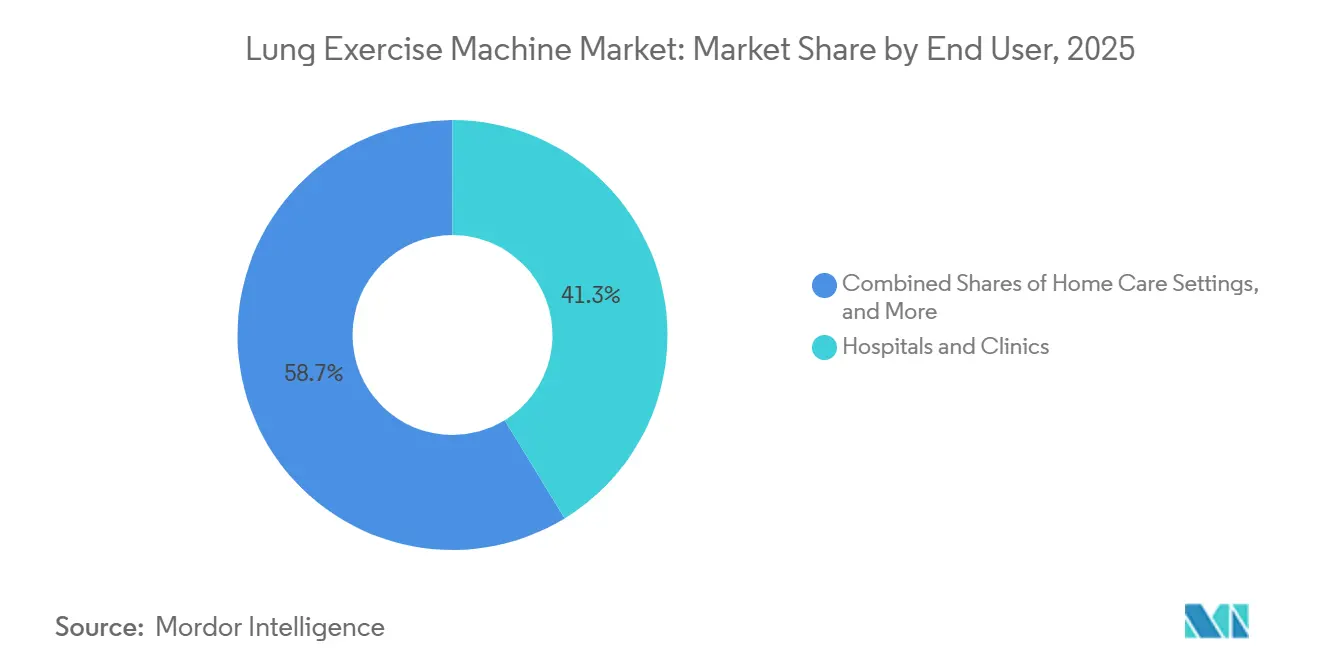

- By end user, hospitals and clinics held 41.26% of 2025 revenue, while ambulatory surgical and endoscopy centers show the fastest growth at 4.72% CAGR over 2026-2031.

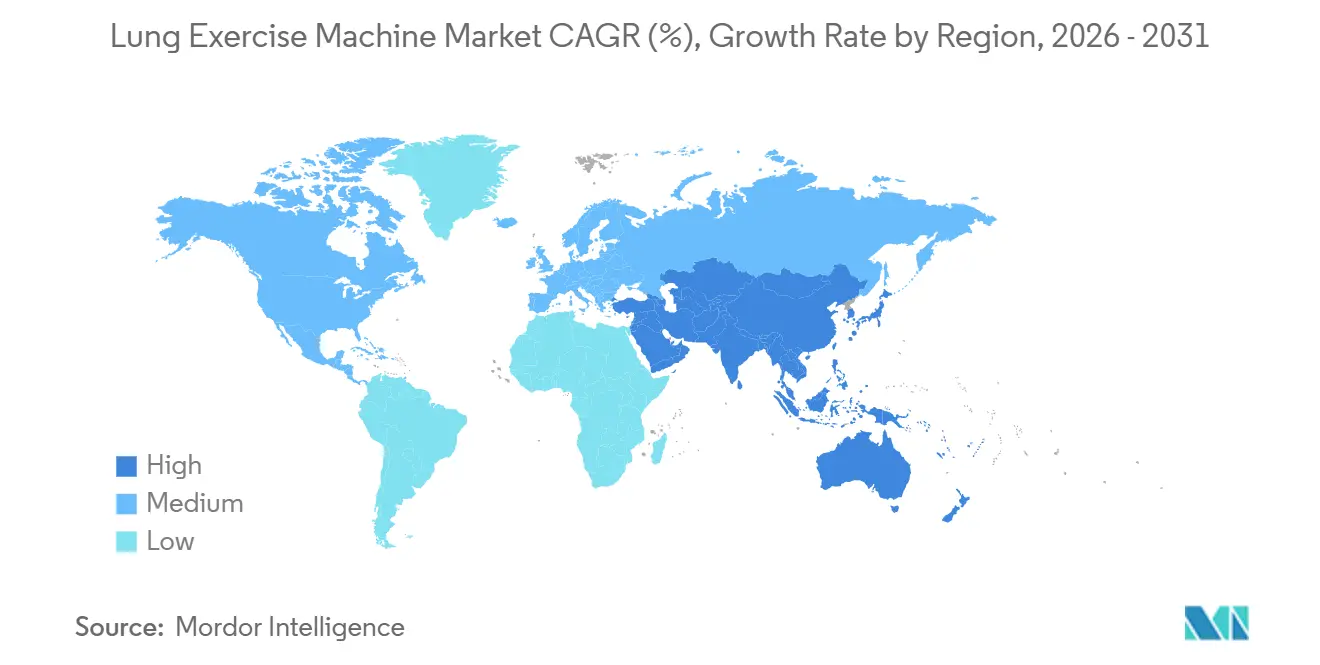

- By geography, North America captured 39.61% revenue in 2025, whereas Asia-Pacific is forecast to expand at a 4.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lung Exercise Machine Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising COPD prevalence & post-COVID pulmonary-rehab demand | +1.2% | Global, with highest absolute burden in China (50.6M cases), India, and aging OECD markets | Medium term (2–4 years) |

| Shift toward home-based respiratory therapy | +0.9% | North America & EU (reimbursement-driven), APAC urban centers (telehealth infrastructure) | Short term (≤2 years) |

| Adoption of connected / AI-enabled trainers | +0.7% | North America, Western Europe, urban APAC (high smartphone penetration, digital-health ecosystems) | Medium term (2–4 years) |

| Gamified biofeedback improving adherence | +0.5% | Global, with early traction in North America, Northern Europe, South Korea, Japan | Long term (≥4 years) |

| Employer-sponsored lung-health programs | +0.3% | North America, EU (corporate wellness mandates), select APAC markets (Singapore, Japan) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Global COPD Cases Surge, Prompting Increased Demand for Post-COVID Pulmonary Rehabilitation

In 2024, global cases of COPD reached 213.4 million, resulting in 3.7 million deaths.[1]Global Initiative for Chronic Obstructive Lung Disease, “Artificial Intelligence and Emerging Technologies,” goldcopd.org Ambient particulate matter has emerged as the leading risk factor, surpassing smoking. India faces a growing burden due to deteriorating urban air quality. Randomized trials conducted in 2024 demonstrated that two-week respiratory muscle programs effectively restored forced vital capacity and reduced systemic inflammation in long-COVID patients. In response, CMS expanded pulmonary rehabilitation coverage in 2026 to include post-COVID patients and established virtual supervision guidelines. These policy changes have reduced cost barriers and integrated devices into chronic care pathways, driving growth in the lung exercise machine market.

Home-Based Respiratory Therapy Gains Traction

In June 2025, CMS approved reimbursements for at-home non-invasive ventilation, removing the requirement for facility supervision and legitimizing remote pulmonary rehabilitation sessions.[2]Centers for Medicare & Medicaid Services, “CMS Finalizes Coverage for At-Home Non-Invasive Ventilation,” cms.gov A 2024 study revealed that internet-of-things respiratory programs significantly improved the six-minute walk distance by 63.74 meters and reduced 90-day rehospitalizations compared to center-based care. Data from the United Kingdom indicate that home-based therapy users are younger and more socioeconomically disadvantaged, highlighting the role of tele-pulmonary rehabilitation in expanding access for underserved populations. CMS has extended telehealth flexibilities through 2027, allowing hospitals to bill for remote therapy sessions conducted at patients' homes. Device manufacturers have responded by acquiring digital diagnostics firms to integrate hardware, data, and services into seamless home-care ecosystems.

Connected and AI-Driven Trainers on the Rise

A 2024 meta-analysis showed that AI-enhanced pulmonary rehabilitation delivered superior improvements in the six-minute walk distance compared to standard protocols. In September 2024, a Bluetooth Smart Adaptor was introduced, enabling traditional mechanical trainers to function as connected platforms that monitor real-time pressures and synchronize with coaching applications. Updated guidelines in 2026 emphasized artificial intelligence, positioning remote monitoring as a standard practice rather than an experimental tool. Cloud networks now manage millions of patients, leveraging predictive algorithms to adjust therapies proactively and prevent clinical deterioration. Although semiconductor shortages continue to extend lead times, strong patient demand for data-driven feedback sustains the backlog for smart trainers.

Gamified Biofeedback Boosts Patient Adherence

Studies conducted between 2024 and 2025 highlighted that gamified breathing programs achieved adherence rates of nearly 70%, doubling those of standard care. Gamification strategies, such as point scoring, escalating difficulty levels, and visual progress dashboards, leverage behavioral economics to encourage consistent daily use. Platforms now incorporate coaching narratives into data streams, transforming muscle pressure metrics into engaging video-game-style challenges that appeal to younger, tech-savvy users. Rehabilitation guides have endorsed these devices for addressing long-COVID-related dyspnea, providing clinicians with a credible basis for prescriptions. Continued integration with smartphones and wearables is expected to enhance adherence further and generate recurring app subscription revenue, creating additional growth opportunities for the lung exercise machine market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent certification & reimbursement hurdles | -0.8% | Global, with highest friction in EU (MDR/IVDR), U.S. (FDA 510(k) backlog), emerging markets (local registration) | Medium term (2–4 years) |

| Low awareness in emerging markets | -0.5% | APAC (ex-Japan), Middle East & Africa, Latin America (limited pulmonary-rehab infrastructure) | Long term (≥4 years) |

| Sensor-chip shortages inflating BOM costs | -0.4% | Global, with acute impact on electronic/smart trainers in North America, EU, APAC | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent Certification And Reimbursement Hurdles

In December 2025, the European Commission proposed revisions to the Medical Device Regulation, extending certificate validity while increasing post-market-surveillance requirements for software-driven trainers.[3]European Commission, “Proposal to Amend the Medical Device Regulation,” ec.europa.eu These changes are expected to raise both the documentation workload and associated costs. In November 2024, Becton Dickinson received an FDA warning for quality-system deficiencies, resulting in a significant USD 83 million remediation accrual, which underscores the financial impact of non-compliance. The 2026 Physician Fee Schedule introduced a -2.5% efficiency adjustment, reducing reimbursements for pulmonary rehabilitation and prompting providers to consider lower-cost devices or fewer supervised sessions. Coverage under CPT codes 94625 and 94626 remains restricted to GOLD Stage II-plus COPD patients or those with post-COVID indications, excluding asthma-only users, which limits potential growth for certain device categories.

Low Awareness In Emerging Markets

In India, the rural COPD burden is exacerbated by biomass-fuel exposure, yet structured pulmonary rehabilitation programs are largely unavailable outside major metropolitan areas. A 2024 global review revealed that low- and middle-income countries bear a disproportionate share of COPD-related disabilities but lack sufficient outpatient therapy infrastructure. Although WHO guidance supports the use of inspiratory muscle trainers, their distribution to primary-care clinics has been inconsistent, leaving many physicians unaware of evidence-based treatment protocols. These gaps hinder the adoption of lung exercise machines in densely populated regions with rising disease prevalence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Mechanical Trainers Outpace Legacy Spirometers

In 2025, incentive spirometers accounted for 36.3% of revenue, reflecting their established role in surgical pathways. However, mechanical resistance trainers are projected to grow at a 4.67% CAGR, surpassing the overall lung exercise machine market growth rate by a quarter-point. This trend is supported by data showing that preoperative inspiratory-muscle conditioning significantly reduces pulmonary complications. Electronic smart trainers, featuring Bluetooth chips, pressure sensors, and coaching algorithms, are driving market growth through premium pricing and recurring software subscriptions.

Multi-ball exercisers cater to pediatric and geriatric users with their engaging visual cues but lack the reimbursement support of higher-evidence categories, limiting their market share. Semiconductor shortages have extended lead times for electronic trainers, prompting some providers to maintain mechanical trainers as a risk mitigation strategy. However, as chip supplies stabilize between 2027 and 2028, the revenue mix is expected to shift further toward digitally enabled devices.

By Application: Post-Operative Therapy Leads And Accelerates

In 2025, post-operative pulmonary therapy accounted for 35.2% of revenue and is projected to grow at the fastest rate, with a 4.82% CAGR through 2031. Enhanced recovery protocols now mandate prehabilitation sessions, including inspiratory-muscle conditioning, driving increased procurement at surgical centers. COPD rehabilitation continues to see high demand due to a global patient base of 213.4 million cases, though its growth is constrained by diagnostic infrastructure limitations in emerging markets, which restrict patient volumes.

Asthma management remains in an exploratory phase. While breathing protocols such as Buteyko improve quality of life and reduce reliance on rescue inhalers, they lack dedicated reimbursement outside of research settings. Sports-performance and vocal-cord therapy represent untapped opportunities, but the absence of coverage limits near-term commercialization. As surgical case volumes recover and hospitals aim to meet length-of-stay benchmarks, procurement committees increasingly prioritize devices with proven postoperative risk reduction, reinforcing the dominance of post-operative therapy in the lung exercise machine market.

By End User: Ambulatory Centers Capture Momentum

In 2025, hospitals and clinics accounted for 41.26% of end-user revenue, supported by traditional inpatient and outpatient rehabilitation programs. However, ambulatory surgical and endoscopy centers are expected to grow at a 4.72% CAGR, driven by reimbursement policies that favor shorter admissions and same-day discharges. Extended telehealth provisions through 2027 allow hospital systems to bill for remote therapy delivered at home, reducing the competitive advantage of brick-and-mortar facilities and strengthening ambulatory networks.

Home-care adoption is increasing, following a 2024 trial that demonstrated tele-rehabilitation improves functional distance and reduces readmissions. Data from the United Kingdom indicate that home-care participants are often from socioeconomically disadvantaged groups, highlighting the channel’s role in promoting healthcare equity. Device manufacturers are incorporating cloud dashboards to enable clinicians to monitor adherence remotely, ensuring accountability in home settings. As insurers link reimbursements to outcomes, evidence supporting the effectiveness of home-based programs positions this channel for sustained growth within the lung exercise machine market.

Geography Analysis

In 2025, North America accounted for 39.61% of the revenue, driven by favorable coverage decisions and strong telehealth penetration. The Centers for Medicare & Medicaid Services extended virtual supervision through 2027, ensuring reimbursement for connected trainers used in patient homes. Although a -2.5% efficiency cut has reduced session margins, providers have mitigated the impact by shifting to lower-overhead home programs and selecting devices that digitally document outcomes. ResMed, headquartered in San Diego, has leveraged its expertise in hardware and diagnostics integration, supported by its acquisition of VirtuOx, which combines sleep-testing and pulmonary-rehabilitation data into a unified cloud platform.

Europe's regulatory environment presents a mix of opportunities and challenges. Planned adjustments to MDR/IVDR in 2027 aim to expand pathways for breakthrough devices and regulatory sandboxes, while also imposing stricter post-market evidence requirements for software-as-a-medical-device, increasing cost pressures. Despite these challenges, strong public-health reimbursements, an aging population, and growing environmental health awareness ensure a stable baseline demand.

Asia-Pacific is projected to be the fastest-growing region, with a compound annual growth rate of 4.96%. China, with its 50.6 million COPD patients, represents a significant market opportunity. However, limited spirometry adoption delays diagnosis and subsequent device uptake. While urban hospitals in Beijing, Shanghai, and Guangzhou are piloting AI trainers, nationwide implementation depends on clearer reimbursement policies. In India, rising COPD cases due to particulate-matter exposure and biomass fuel usage contrast with the limited availability of structured pulmonary-rehabilitation units in tertiary hospitals.

Competitive Landscape

The lung exercise machine market is moderately fragmented. Key players include Becton Dickinson, Philips, ResMed, and Medtronic, alongside specialized respiratory-training companies such as POWERbreathe International and AirPhysio. Additionally, Teleflex’s divested respiratory portfolio, now under Medline, contributes to the competitive landscape. In June 2024, Becton Dickinson enhanced its portfolio with the acquisition of Edwards Lifesciences’ Critical Care unit for USD 4.2 billion, integrating Swan-Ganz hemodynamic sensors and AI decision tools. This acquisition enables the company to bundle monitoring solutions with inspiratory-muscle devices for perioperative contracts. ResMed's acquisition of VirtuOx in 2024 reflects its focus on home diagnostics, aiming to enhance algorithmic coaching and drive sales of connected trainers. Philips is integrating lung-function training modules into its HealthSuite cloud platform, leveraging its existing sleep-apnea base to offer post-COVID rehabilitation kits.

Emerging players are exploring applications in pediatric, vocal-cord, and high-altitude segments, though these niches require formal reimbursement to achieve scalability. As payers transition from device-based fees to outcome-based contracts, strategic partnerships between hardware manufacturers and telehealth providers are expected to intensify competition in the digital platform segment of the lung exercise machine industry.

Lung Exercise Machine Industry Leaders

Koninklijke Philips N.V.

Medtronic plc

ResMed Inc.

Becton, Dickinson and Company

Cardinal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Boston Scientific began the RESPI study to validate mask-based end-tidal CO₂ and spirometry sensors, a project that could expand the company’s digital-health respiratory footprint.

- March 2026: India’s Health Minister inaugurated a heart-and-lung machine at King George Hospital, underscoring national interest in respiratory infrastructure.

- January 2026: Climatic Y launched the L Max breathable daily lung-health system, positioning respiratory care as a proactive consumer habit.

Global Lung Exercise Machine Market Report Scope

As per the scope of the report, a lung exercise machine, commonly known as an incentive spirometer or respirometer, is a handheld, plastic device used to strengthen lungs, increase capacity, and clear mucus through deep breathing exercises. Often used post-surgery or during recovery from illnesses like COVID-19 and pneumonia, it provides visual feedback (a rising piston or balls) to guide slow, deep inhalations, ensuring lungs stay fully expanded and functional.

The lung exercise machine market is segmented by device type, application, end user, and geography. By device type, the market is segmented into mechanical resistance trainers, electronic/smart trainers, incentive spirometers, positive expiratory pressure (PEP) devices, and multi-ball respiratory exercisers. By application, the market is segmented into COPD rehabilitation, post-operative pulmonary therapy, asthma management, sports & fitness performance, and geriatric lung health. By end user, the market is segmented into hospitals & clinics, home care settings, rehabilitation centers, and sports institutions. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| Mechanical Resistance Trainers |

| Electronic / Smart Trainers |

| Incentive Spirometers |

| Positive Expiratory Pressure (PEP) Devices |

| Multi-Ball Respiratory Exercisers |

| COPD Rehabilitation |

| Post-operative Pulmonary Therapy |

| Asthma Management |

| Sports & Fitness Performance |

| Geriatric Lung Health |

| Hospitals & Clinics |

| Home Care Settings |

| Rehabilitation Centers |

| Sports Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Mechanical Resistance Trainers | |

| Electronic / Smart Trainers | ||

| Incentive Spirometers | ||

| Positive Expiratory Pressure (PEP) Devices | ||

| Multi-Ball Respiratory Exercisers | ||

| By Application | COPD Rehabilitation | |

| Post-operative Pulmonary Therapy | ||

| Asthma Management | ||

| Sports & Fitness Performance | ||

| Geriatric Lung Health | ||

| By End User | Hospitals & Clinics | |

| Home Care Settings | ||

| Rehabilitation Centers | ||

| Sports Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big will the lung exercise machine market be by 2031?

Mordor Intelligence projects the lung exercise machine market size to reach USD 1.50 billion by 2031, expanding at a 4.4% CAGR over 2026-2031.

Which device type is growing the fastest?

Mechanical resistance trainers are forecast to grow at a 4.67% CAGR to 2031, outpacing overall market growth while shifting clinical focus toward inspiratory-muscle strengthening.

What application currently drives the largest revenue?

Post-operative pulmonary therapy commanded 35.2% of 2025 revenue and remains the leading use-case category.

Which region will post the strongest growth?

Asia-Pacific is expected to record the highest CAGR at 4.96% during 2026-2031 due to Chinas large COPD burden and improving telehealth infrastructure.

How are reimbursement policies shaping home-based therapy adoption?

CMS coverage for at-home ventilation, extended telehealth flexibilities, and virtual supervision rules have lowered financial barriers, accelerating U.S. home-care uptake.

What is the competitive outlook for digital respiratory trainers?

Leading firms are integrating cloud analytics and AI coaching; acquisitions like ResMed VirtuOx illustrate a race to create end-to-end home-care ecosystems.

Page last updated on: