Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.86 Billion |

| Market Size (2031) | USD 11.25 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

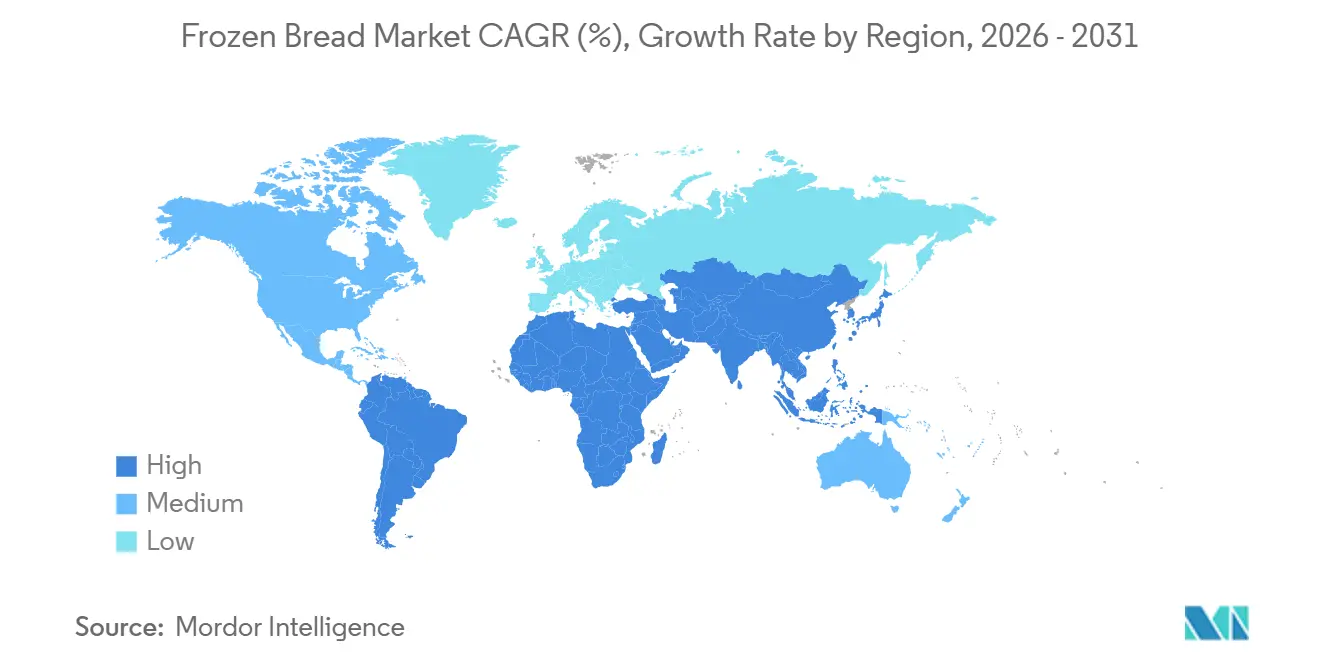

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

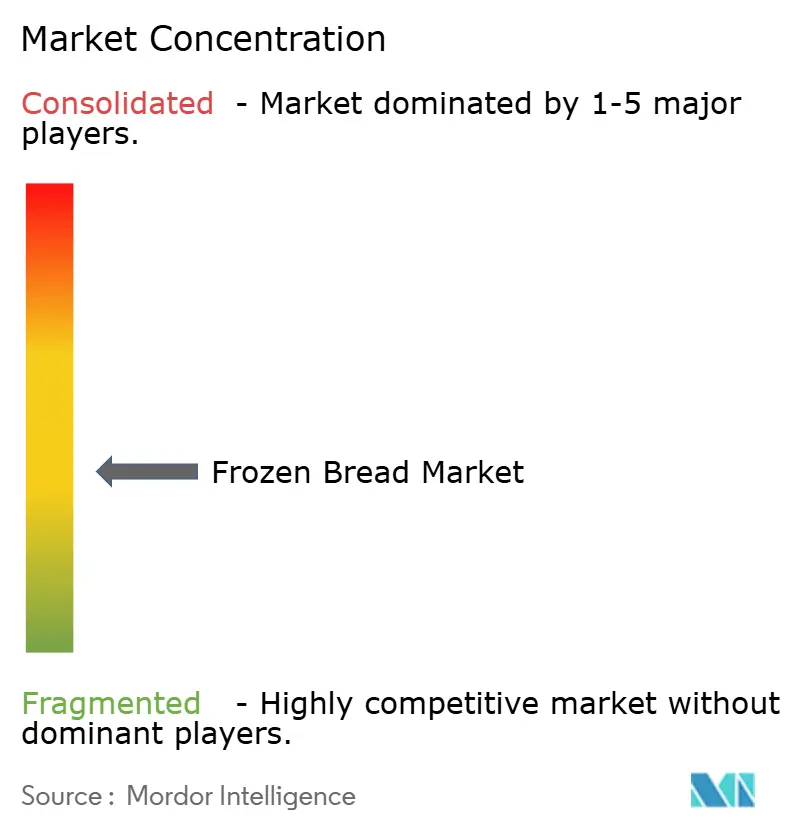

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Frozen Bread Market Analysis by Mordor Intelligence

The frozen bread market size is expected to grow from USD 8.72 billion in 2025 to USD 8.86 billion in 2026 and is forecast to reach USD 11.25 billion by 2031, expanding at a 4.92% CAGR over 2026-2031. Labor shortages across commercial kitchens and the universal push for uniform product quality are making frozen formats a non-negotiable component of large-scale food operations, a structural change that secures long-term volume growth. Retail cold-chain upgrades, rising acceptance of par-baked products that mimic fresh bread, and urban consumers’ demand for low-waste convenience underpin a steady trade-down from fresh to frozen across supermarkets and e-commerce channels. Asia-Pacific’s outsized cold-chain buildout, combined with accelerating Western menu adoption in China, India, and Southeast Asia, signals a geographic rebalancing away from North America’s legacy dominance. Premiumization through multigrain, free-from, and artisanal positioning is widening the price ladder, enabling manufacturers to protect margins even as wheat-price swings pressure input costs.

Key Report Takeaways

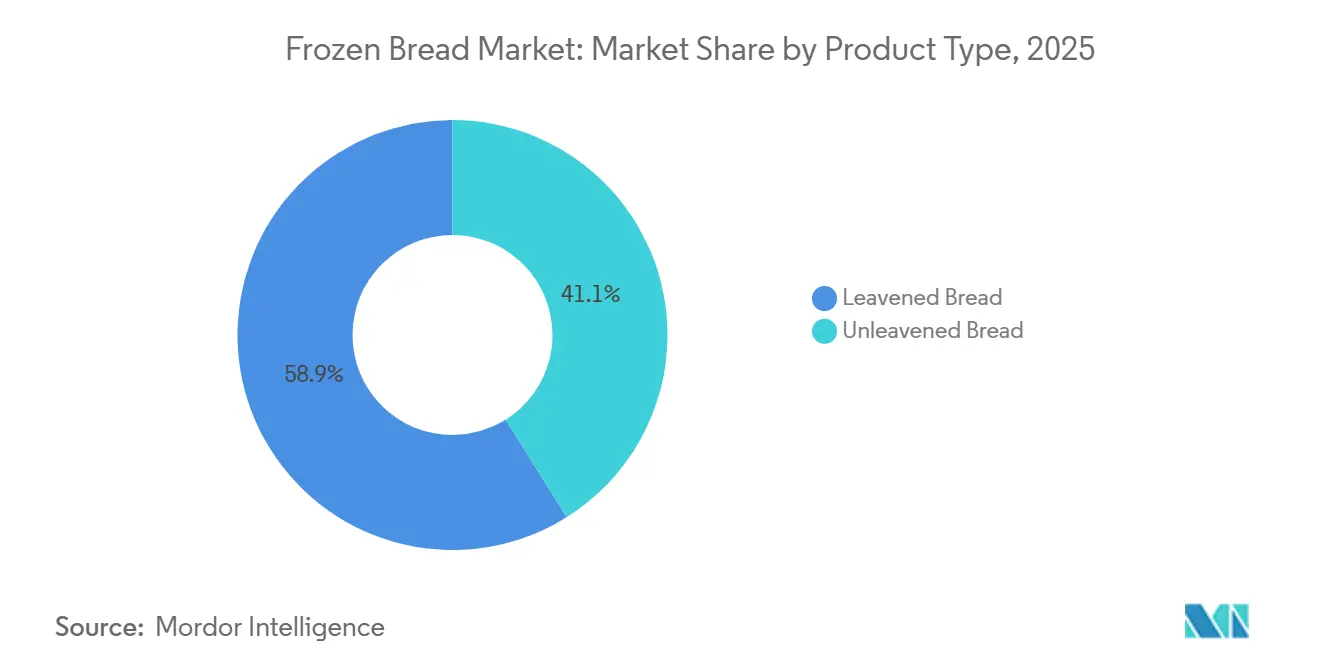

- By product type, leavened bread held 58.92% of the frozen bread market share in 2025. Unleavened bread is poised to expand at 5.28% CAGR to 2031.

- By ingredient type, white bread commanded 62.15% share of the frozen bread market size in 2025. Multigrain bread is projected to accelerate at 6.21% CAGR through 2031.

- By nature, conventional variants captured 86.28% revenue in 2025. Free-from alternatives are set to grow at 6.18% CAGR to 2031.

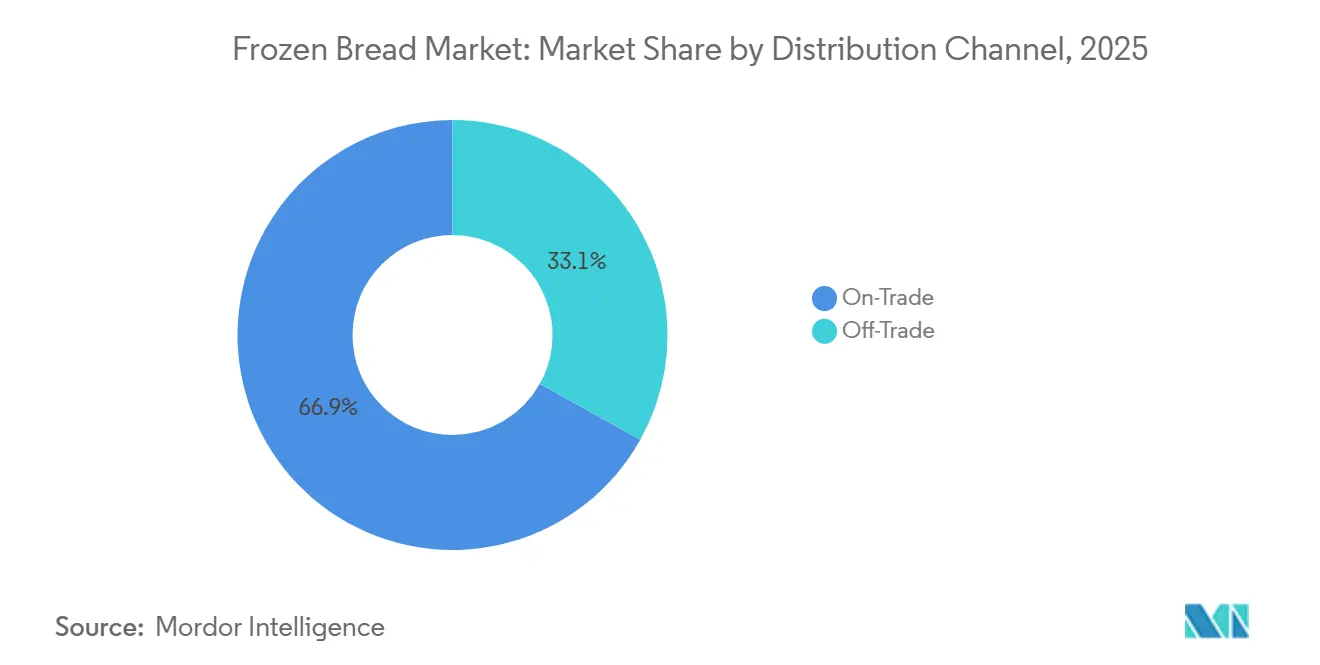

- By distribution channel, on-trade controlled 61.54% of the frozen bread market size in 2025. Off-trade outlets are forecast to rise at 6.21% CAGR through 2031.

- By geography, North America led with 50.25% revenue share in 2025, and Asia-Pacific is on track for a 6.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Frozen Bread Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Convenience Foods | +1.2% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Rising Health Consciousness and Demand for Fortified or Multigrain Bread | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Long term (≥ 4 years) |

| Uniform Quality Requirements across Large-Scale Food Operations | +0.6% | North America and Europe, emerging in urban Asia-Pacific | Short term (≤ 2 years) |

| Growing Demand for Gourmet and Premium Frozen Bread Loaves | +0.8% | Global, led by North America and urban Asia-Pacific markets | Medium term (2-4 years) |

| Shifting Consumer Preferences towards Ethnic, Artisanal, and Specialty Frozen Bread Loaves | +0.5% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Product Innovation and Expansion of Variety in Frozen Bread Loaves | +0.7% | Global, with premium positioning in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Convenience Foods

Frozen bread plays a pivotal role in addressing the structural labor shortages faced by foodservice operators. By removing the need for in-house baking, it significantly reduces labor requirements, minimizes waste, and ensures consistent quality across multi-unit chains. Quick-service restaurant chains have widely adopted standardized frozen burger buns and sandwich rolls, enabling them to maintain uniform product specifications across thousands of locations. This approach not only strengthens supplier relationships but also creates substantial switching costs, making it challenging to shift to alternative suppliers. Retail channels are increasingly adopting this model, reflecting its growing appeal. The convenience offered by frozen bread extends beyond foodservice operators to end-consumers. Consumers value the ability to store bread for longer periods without spoilage and to bake single servings as needed. This usage pattern aligns with the evolving dynamics of smaller household sizes and the rising focus on reducing food waste. As a result, frozen bread is becoming an essential solution for both operational efficiency and consumer convenience in the foodservice and retail markets.

Rising Health Consciousness and Demand for Fortified or Multigrain Bread

Multigrain and fortified bread variants command 15-25% price premiums in retail channels, yet their growth signals that consumers are willing to absorb higher costs in exchange for fiber, whole grains, and micronutrient fortification. Peer-reviewed research published in the Journal of Food Science documents successful fortification of wheat bread with vitamin D3 at levels that deliver 25% of the daily recommended intake per serving without compromising sensory attributes, a formulation strategy that food manufacturers are now commercializing. Wildgrain launched a gluten-free subscription box in September 2024, while Lancaster Colony introduced a patent-pending gluten-free frozen garlic bread in August 2024, both moves indicating that allergen-free platforms have transitioned from niche to mainstream. Clean-label formulations, those free from artificial preservatives, emulsifiers, and dough conditioners, are gaining traction in European markets where regulatory scrutiny under EFSA guidelines and consumer activism around E-numbers drive reformulation efforts.

Uniform Quality Requirements across Large-Scale Food Operations

Chain restaurants and institutional foodservice operators prioritize product consistency over artisanal variation, a preference that frozen bread satisfies through controlled manufacturing environments and blast-freezing protocols that lock in moisture and crumb structure. Quick-service restaurant specifications for burger buns often mandate tolerances of ±2 grams in weight and ±3 millimeters in diameter, standards that in-house baking cannot reliably meet across shifts and locations. Frozen formats also enable centralized procurement and just-in-time inventory management, reducing the working capital tied up in perishable stock. Hospital and school cafeteria operators face additional compliance burdens under FDA Current Good Manufacturing Practice regulations (CFR Title 21 Part 110) and HACCP protocols, making frozen bread an attractive option because suppliers bear the food-safety certification costs and audit risks[1]Source: Food and Drug Administration, "CFR Title 21 Part 110", accessdata.fda.gov/. The shift toward ghost kitchens and delivery-only restaurant formats further amplifies demand for frozen bread, as these operations lack the square footage and ventilation infrastructure for on-site ovens and rely entirely on supplier-managed baking processes.

Growing Demand for Gourmet and Premium Frozen Bread Loaves

Premium frozen bread, characterized by artisanal shaping, heritage grain varieties, and par-baked formats that require final oven finishing, targets affluent consumers willing to pay EUR 2.50 to EUR 3.50 (USD 2.72 to USD 3.81) per loaf for a fresh-baked experience without the time commitment of scratch baking. UK retailer SlooOW positions its part-baked sourdough at GBP 2.50 (USD 3.18), a 150% premium over budget frozen bread priced at GBP 0.99 (USD 1.26). Yet, the brand has expanded distribution through independent grocers and farm shops, indicating that a segment of consumers values provenance and slow-fermentation claims. Par-baked technology—whereby dough is baked to 70-80% completion, then frozen—allows retailers to offer warm, crusty bread in-store without installing full bakery operations, a capital-efficient model that Europastry has scaled across 29 plants. The gourmet segment also benefits from limited-edition and seasonal varieties—pumpkin seed, fig and walnut, rosemary focaccia—that drive trial and repeat purchase among food enthusiasts who treat bread as a culinary statement rather than a commodity staple.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shifting Consumer Preference for Fresh Products | -0.6% | Europe, Middle East, South America | Long term (≥ 4 years) |

| Higher Price Points compared to Fresh Alternatives | -0.4% | Price-sensitive markets in Asia-Pacific, South America | Medium term (2-4 years) |

| Competition from Local or Regional Bakers Supply | -0.3% | Europe, Middle East, localized markets | Medium term (2-4 years) |

| Raw Material Pricing Fluctuations | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shifting Consumer Preference for Fresh Products

Consumer research identifies freshness, visual appearance, habit, and price as the dominant factors in bread-purchasing decisions, with sensory attributes such as porosity, crust color, and floury or malty odors serving as proxies for freshness. This perception creates a structural headwind for frozen bread, particularly in European and Middle Eastern markets where daily bakery visits remain culturally embedded, and consumers associate frozen formats with inferior taste and texture. A household bread-freezing study found that 27% of consumers freeze bread immediately after purchase to extend shelf life and reduce waste, suggesting that a segment of the market has overcome freshness bias, yet the majority still prefer fresh-baked options when accessible. Retail strategies that position frozen bread as a backup or convenience option rather than a primary choice inadvertently reinforce this hierarchy, limiting category growth. The challenge is compounded by the fact that frozen bread requires thawing or reheating, adding a preparation step that contradicts the convenience proposition for time-pressed consumers who can purchase fresh bread with zero additional handling.

Higher Price Points compared to Fresh Alternatives

From 2021 to 2024, frozen food prices increased by approximately 17%, primarily due to energy-intensive freezing processes, complex cold-chain logistics, and the need for specialized packaging. Despite these higher costs, frozen bread remains a direct competitor to fresh alternatives, which avoid these additional expenses, as noted by the U.S. Bureau of Labor Statistics[2]Source: U.S. Bureau of Labor Statistics. "Consumer Price Index for Frozen Foods." bls.gov. UK retail pricing highlights this competition: premium part-baked frozen bread, priced at GBP 2.50 (USD 3.18), competes with fresh bakery loaves priced between GBP 1.50 and GBP 2.00 (USD 1.91 to USD 2.55). On the other hand, budget frozen options, priced at GBP 0.99 (USD 1.26), trade off quality perception to match the pricing of low-end fresh bread. The price premium for frozen bread is justified by its longer shelf life and reduced waste, but these benefits require consumer education and are realized over time. However, the upfront price difference is immediately noticeable at checkout. In price-sensitive regions such as Asia-Pacific and South America, where households allocate a larger share of their budget to food, the frozen premium can discourage adoption, limiting market penetration to affluent urban areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Leavened Formats Anchor Foodservice Demand

Leavened bread held 58.92% of the 2025 market share, driven by sandwich loaves, burger buns, and hot dog rolls that form the backbone of quick-service restaurant and institutional foodservice menus. These formats benefit from established supply chains, standardized specifications, and consumer familiarity, creating high switching costs for operators who have built recipes and portion sizes around specific bun dimensions and weights. Unleavened bread, flatbreads, pita, tortillas, naan will grow at 5.28% CAGR through 2031, propelled by ethnic cuisine adoption and the versatility of these formats across multiple dayparts (breakfast wraps, lunch sandwiches, dinner accompaniments).

Flowers Foods' September 2024 acquisition of Papa Pita signals that established players recognize the margin potential in ethnic bread platforms, which command premiums over commodity sandwich loaves and appeal to younger, more diverse consumer cohorts. Leavened bread faces maturity in North American and European markets, where per-capita consumption has plateaued, yet innovation in stuffed breads (cheese-filled, garlic butter-injected) and hybrid formats (pretzel buns, brioche rolls) is creating incremental growth pockets. Unleavened formats benefit from their alignment with low-carb and portion-control trends, as consumers perceive flatbreads and wraps as lighter alternatives to traditional sandwich bread, even when caloric content is comparable.

By Ingredient Type: Multigrain Variants Capture Health Premiums

Wheat bread commanded 62.15% of 2025 sales, reflecting its role as the default grain platform for sandwich loaves, burger buns, and most leavened formats due to gluten's structural properties and consumer familiarity. Multigrain bread will expand at 6.21% CAGR through 2031, the fastest growth among ingredient types, as consumers migrate toward fiber-fortified and whole-grain options that deliver functional health benefits and command 15-25% retail price premiums. Peer-reviewed research demonstrates successful fortification of wheat bread with vitamin D3 at levels providing 25% of the daily recommended intake per serving without compromising taste or texture, a formulation strategy that manufacturers are commercializing to differentiate products in crowded frozen aisles.

Rye bread serves niche European markets, Germany, Scandinavia, and Eastern Europe, where dense, dark loaves with extended shelf life are culturally preferred, yet limited global production and higher ingredient costs constrain volume growth. Other ingredient types, including ancient grains (spelt, einkorn, kamut), seed-enriched breads (flax, chia, sunflower), and alternative flours (chickpea, almond, coconut), target premium segments willing to pay USD 6 to USD 8 per loaf for perceived health benefits and novelty, yet these remain sub-1% of total market volume. The ingredient segmentation increasingly overlaps with clean-label and free-from positioning, as consumers who seek multigrain bread also prioritize organic certification, non-GMO verification, and minimal processing.

By Nature: Free-From Platforms Unlock Margin Expansion

Conventional frozen bread held 86.28% of the 2025 market share, encompassing standard formulations with commercial yeast, wheat flour, and conventional dough conditioners that optimize production efficiency and cost. The free-from segment is expected to grow at 6.18% CAGR through 2031, a rate that understates its strategic importance because these products command 40-60% price premiums and require dedicated production lines that create competitive moats. Lancaster Colony's August 2024 launch of a patent-pending gluten-free frozen garlic bread formulation illustrates how incumbents are investing in allergen-free platforms as margin-expansion levers rather than niche line extensions. Gluten-free bread production demands specialized ingredient systems, such as rice flour, tapioca starch, xanthan gum, psyllium husk, and rigorous cross-contamination protocols to achieve third-party certification, barriers that protect early movers from private-label competition.

Organic frozen bread serves a parallel niche, appealing to consumers who prioritize pesticide-free grains and non-GMO ingredients, yet organic wheat flour costs 50-80% more than conventional, limiting volume penetration to affluent segments. Clean-label formulations, those free from artificial preservatives, emulsifiers, and dough conditioners, are gaining traction in European markets where regulatory scrutiny under EFSA guidelines and consumer activism around E-numbers drive reformulation efforts. The conventional segment retains dominance because it delivers the cost-performance balance that foodservice operators and price-sensitive retail consumers require, yet the free-from segment's faster growth signals a bifurcation where premium and value tiers increasingly serve distinct customer bases with minimal overlap.

By Distribution Channels: Off-Trade Gains as Retail Cold Chains Mature

The on-trade channel captured 61.54% of 2025 revenue, reflecting frozen bread's entrenched role in commercial kitchens where labor efficiency, portion control, and consistency outweigh the fresh-baked premium. Quick-service restaurant chains standardize frozen burger buns and sandwich rolls to maintain uniform product specifications across thousands of locations, creating locked-in supplier relationships and high switching costs. Marks & Spencer's expansion of its frozen garlic bread program to 378 stores, with 2.1 million units sold since 2020, demonstrates that foodservice operators view frozen bread as a margin-accretive category that reduces waste and simplifies inventory management Marks & Spencer Corporate.

The off-trade channels are expected to grow at 6.21% CAGR through 2031, driven by retail cold-chain upgrades, consumer acceptance of par-baked formats, and the proliferation of single-serve and portion-controlled packaging that aligns with smaller household sizes. Supermarkets and hypermarkets dominate off-trade volume, leveraging promotional pricing and prominent freezer placement to drive trial, while convenience stores focus on grab-and-go formats (frozen sandwiches, breakfast breads) that cater to impulse purchases. Online retail remains nascent but is expanding rapidly in urban markets where last-mile cold-chain logistics have matured; frozen bread's extended shelf life (12+ months) reduces the delivery-timing sensitivity that constrains fresh bakery e-commerce.

Geography Analysis

In 2025, North America held a 50.25% market share, driven by the U.S.'s advanced foodservice infrastructure and Canada's cold-climate storage, which reduces freezing costs. The region benefits from high frozen food penetration, with U.S. retail sales reaching USD 91 billion in 2024, supported by a strong distribution network connecting manufacturers, wholesalers, and end-users. Grupo Bimbo's North American segment reported MXN 60.6 billion (USD 3.5 billion) in Q3 2024, a 5.2% year-over-year increase, fueled by bakery-cafe channel growth and innovations in premium frozen bread. Mexico's frozen bread market is expanding due to urbanization and dual-income households driving demand for convenience foods, though rural penetration remains limited due to concentrated cold-chain infrastructure. While the region continues to grow, market saturation in quick-service restaurants and retail channels is expected to slow growth compared to Asia-Pacific, prompting manufacturers to focus on premiumization and margin enhancement over unit-volume growth.

Europe's growth is shaped by fragmented markets with distinct national preferences, such as French baguettes, German rye, and Italian ciabatta, which complicate pan-regional product standardization. Compliance with EFSA Regulation (EC) No 852/2004, requiring cold-chain maintenance at -18°C and adherence to HACCP protocols, imposes costs that favor larger players with dedicated quality-assurance teams. The region's high density of artisanal bakeries, including over 30,000 independent bakeries in France alone, creates intense competition, limiting frozen bread to foodservice and emergency retail use in many markets. However, the UK's growing acceptance of part-baked formats, as seen with brands like SlooOW and Lidl, highlights a shift where convenience-oriented segments are overcoming traditional freshness biases.

Asia-Pacific is projected to grow at a 6.81% CAGR through 2031, the fastest among regions, driven by urbanization, expanding cold-chain infrastructure, and increasing Western food adoption in China, India, Japan, and Southeast Asia. Japan's convenience store chains, including Lawson, FamilyMart, and 7-Eleven, are expanding frozen bread offerings, leveraging the country's USD 3.2 billion frozen food import market. India's cold-chain capacity stood at 35.4 million metric tons in 2023, with the government's National Cold Chain Mission targeting infrastructure gaps that currently limit frozen food penetration outside major metros, according to the Indian Ministry of Food Processing Industries[3]Source: Indian Ministry of Food Processing Industries, “National Cold Chain Mission,” mofpi.gov.in. Meanwhile, South America and the Middle East & Africa market is driven by urbanization, expatriate populations, and food-security initiatives. The UAE's frozen food imports reached USD 1.8 billion in 2023, fueled by expatriate demand and local adoption of convenient alternatives to fresh-baked pita. Saudi Arabia's Vision 2030 prioritizes cold-chain infrastructure and domestic food production, creating opportunities for frozen bread manufacturers to establish local production or partnerships. South America's cold-chain networks remain concentrated in coastal cities, but rising middle-class incomes and supermarket expansion are gradually improving frozen food access.

Competitive Landscape

The frozen bread market demonstrates a moderate concentration, defined by a competitive landscape where established multinational bakery giants compete alongside emerging regional specialists. With a concentration score of 4, the market balances scale-driven incumbents with agile niche competitors, encouraging innovation and a wide range of product offerings. Leading players such as ARYZTA AG, Lantmännen Unibake, Europastry, and Vandemoortele hold significant market shares. Their leadership is supported by extensive product portfolios, strong brand recognition, and broad distribution networks catering to both retail and foodservice sectors. These industry leaders utilize their scale to maintain consistent quality, invest in research and development, and explore premium and health-oriented frozen bread categories.

Strategic consolidation is a key characteristic of the industry. Companies strengthen their market positions and diversify their product lines through acquisitions and partnerships. For example, Europastry has expanded its reach by investing in specialty frozen bakery producers, while Vandemoortele has enhanced its presence in Western Europe through acquisitions. These strategies not only improve operational capabilities and geographic reach but also accelerate innovation. The strategic initiatives of these industry leaders emphasize geographic expansion and portfolio diversification. ARYZTA AG is expanding its presence in North America and Europe with its branded frozen bread. Similarly, Lantmännen Unibake is leveraging its Scandinavian roots to introduce premium and sustainable bakery solutions globally.

Europastry is focusing on innovation centers to develop healthier and functional bread varieties, while Vandemoortele is prioritizing sustainability and clean-label formulations to align with evolving consumer preferences. In conclusion, the frozen bread market's competitive landscape is shaped by a combination of scale, specialization, and strategic consolidation. While established leaders drive global expansion and innovation, agile niche players bring flexibility and artisanal expertise, collectively creating a market that caters to diverse consumer preferences, ranging from health and convenience to premium offerings.

Frozen Bread Industry Leaders

-

Aryzta AG

-

Europastry S.A.

-

Grupo Bimbo S.A.B. de C.V.

-

Lantmännen Unibake

-

Vandemoortele

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Flowers Foods has strategically acquired Simple Mills for USD 795 million, aiming to significantly enhance its position in the health-conscious baked goods market. This acquisition allows Flowers Foods to expand its portfolio with a brand widely recognized for its dedication to clean ingredients and a strong nutritional focus.

- December 2024: Furlani Foods announced the acquisition of Cole's Quality Foods, a notable player in the frozen garlic bread market with two production facilities in Michigan, strengthening Furlani's position in the frozen bread segment.

- October 2024: General Mills Foodservice has introduced a new line of frozen bread doughs tailored for in-store bakeries, including Pillsbury Long French Bread Dough, Pillsbury Pre-Score Italian Bread Dough, Pillsbury French/Italian Bread Dough, and Pillsbury Sourdough Bread Dough.

- August 2024: T. Marzetti Co., a wholly-owned subsidiary of Lancaster Colony Corp., has launched its first gluten-free line of New York Bakery frozen bread. The line includes gluten-free versions of the brand’s Garlic Texas Toast and Five Cheese Texas Toast.

Global Frozen Bread Market Report Scope

Bread is often frozen to preserve freshness or extend shelf life.

The scope of the frozen bread market includes segmentation into product type, distribution channel, and geography. By product type, the market is segmented into conventional bread and gluten-free bread. The market is divided based on distribution channel, which includes retail channels and food service. The study also involves the global level analysis of the main regions such as North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

For each segment, market sizing and forecast have been done based on value (USD million).

By Product Type

| Leavened Bread |

| Unleavened Bread |

By Ingredient Type

| Wheat Bread |

| Rye Bread |

| Multigrain Bread |

| Other Ingredients |

By Nature

| Conventional |

| Free-From |

By Distribution Channels

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Leavened Bread | |

| Unleavened Bread | ||

| By Ingredient Type | Wheat Bread | |

| Rye Bread | ||

| Multigrain Bread | ||

| Other Ingredients | ||

| By Nature | Conventional | |

| Free-From | ||

| By Distribution Channels | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the frozen bread market be by 2031?

The frozen bread market size is projected to reach USD 11.25 billion by 2031.

Which region will post the fastest growth?

Asia-Pacific is forecast to expand at 6.81% CAGR on the back of rapid cold-chain investment.

Why are free-from frozen breads strategically important?

Though only 13.72% of sales, free-from SKUs grow at 6.18% CAGR and carry 40-60% price premiums.

What technological advance is reshaping premium frozen bread?

Cryogenic freezing cuts roll freeze time to 4 minutes, preserving texture and enabling delicate artisanal SKUs.

Page last updated on: