Europe Breadcrumbs Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

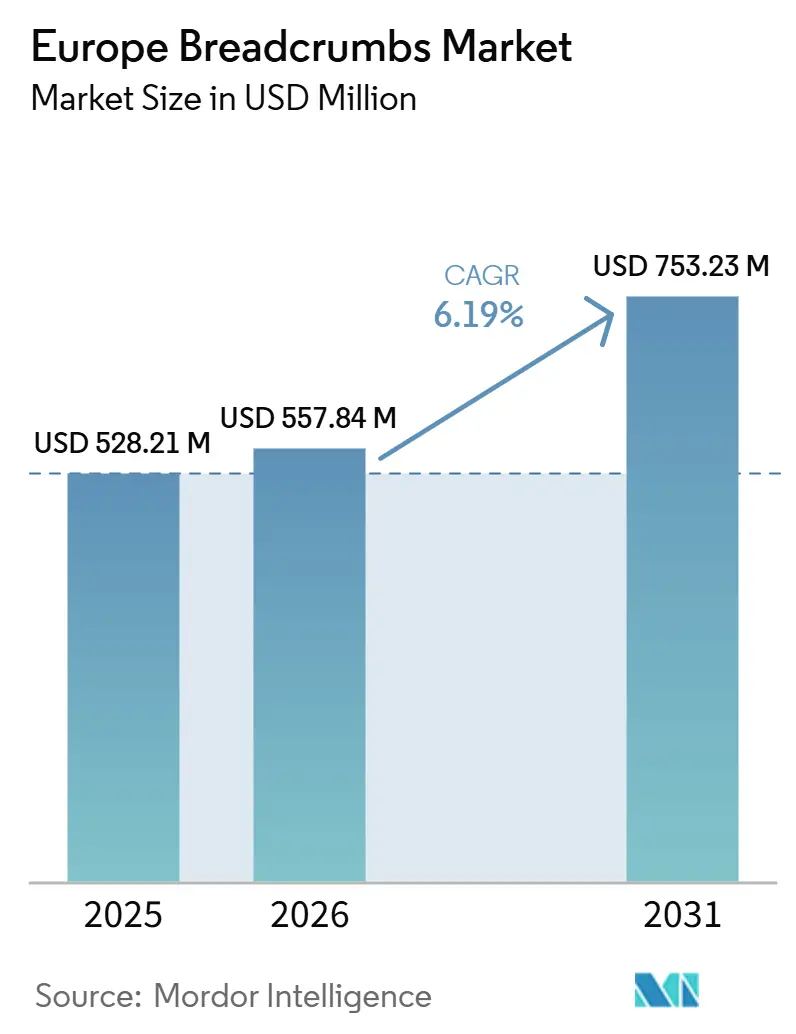

| Base Year Market Size (2025) | USD 528.21 Million |

| Market Size (2026) | USD 557.84 Million |

| Market Size (2031) | USD 753.23 Million |

| Growth Rate (2026 - 2031) | 6.19% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Breadcrumbs Market Analysis by Mordor Intelligence

The Europe breadcrumbs market size is expected to grow from USD 528.21 million in 2025 to USD 557.84 million in 2026 and is forecast to reach USD 753.23 million by 2031 at 6.19% CAGR over 2026-2031. The market is advancing on steady demand from frozen food processors, quick-service chains, and retail buyers seeking coatings that perform well in ovens and air fryers. Large-volume conventional products continue to anchor the category, but growth is clearly shifting toward panko, gluten-free options, and seasoned formats that offer improved texture and higher unit value. Procurement standards are also tightening, as food manufacturers require consistent crumb size, stable adhesion, and documentation supporting allergen and labeling compliance across several countries. This trend is pushing the Europe breadcrumbs market toward suppliers that can combine scale, product development support, and dependable sourcing rather than compete on price alone. The opportunity in the Europe breadcrumbs market remains strongest for suppliers that can serve both the legacy high-volume business and the faster-moving specialty range without weakening service levels.

Key Report Takeaways

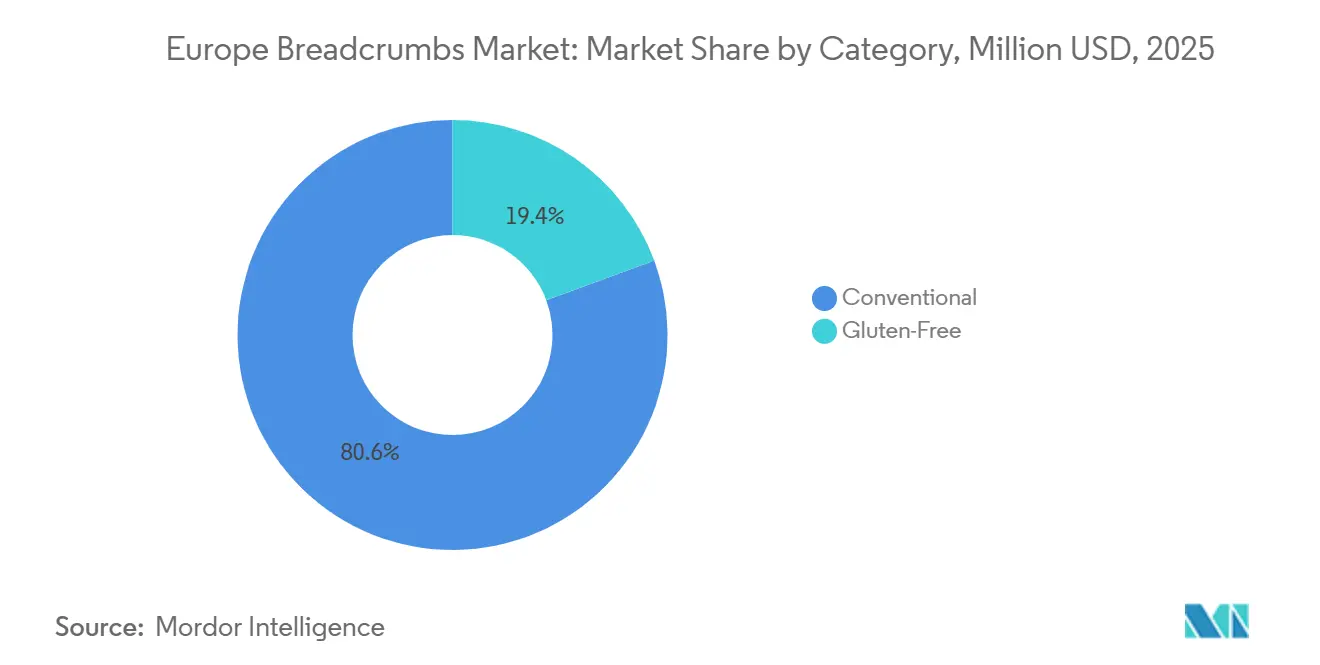

- By category, conventional breadcrumbs held 80.63% of the Europe breadcrumbs market share in 2025, while gluten-free breadcrumbs are forecast to expand at 7.28% CAGR through 2031.

- By crumb type, dry breadcrumbs accounted for 84.26% of the Europe breadcrumbs market size in 2025, while panko is projected to grow at 6.99% CAGR through 2031.

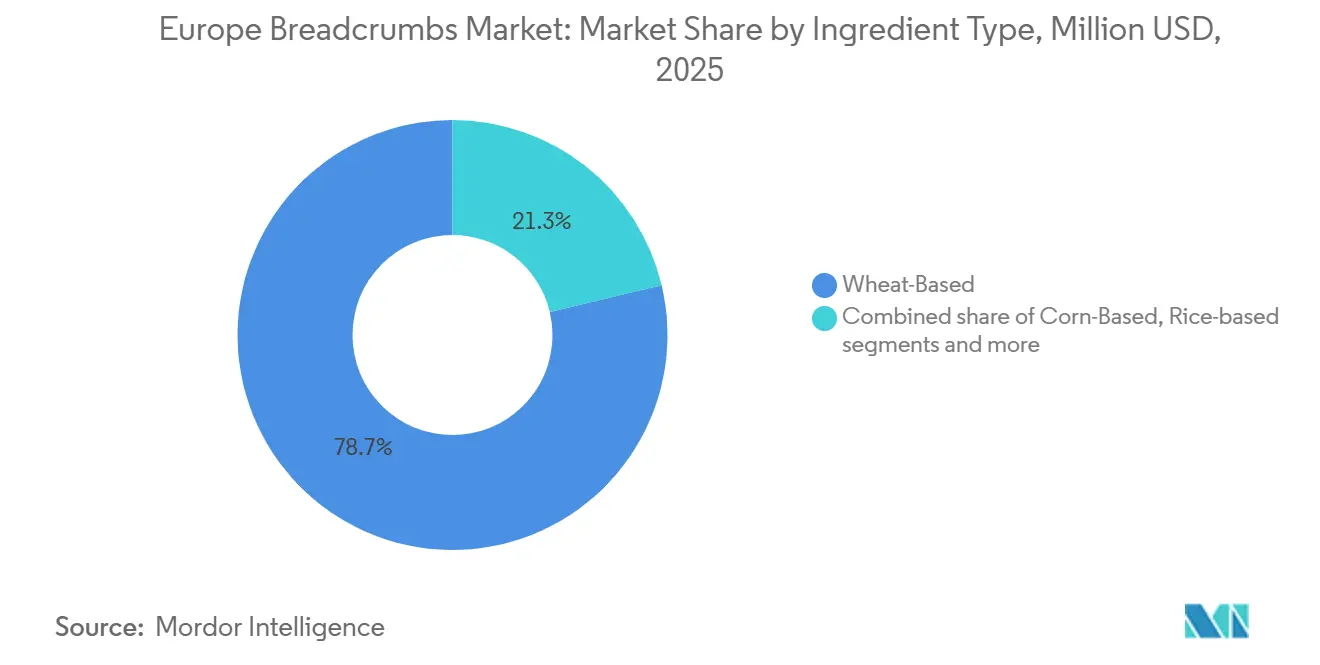

- By ingredient type, wheat-based breadcrumbs captured 78.71% share of the Europe breadcrumbs market size in 2025, while corn-based breadcrumbs are set to rise at 7.19% CAGR through 2031.

- By flavor, unflavored breadcrumbs held 66.21% share in 2025, while flavored breadcrumbs are expected to advance at 7.16% CAGR through 2031.

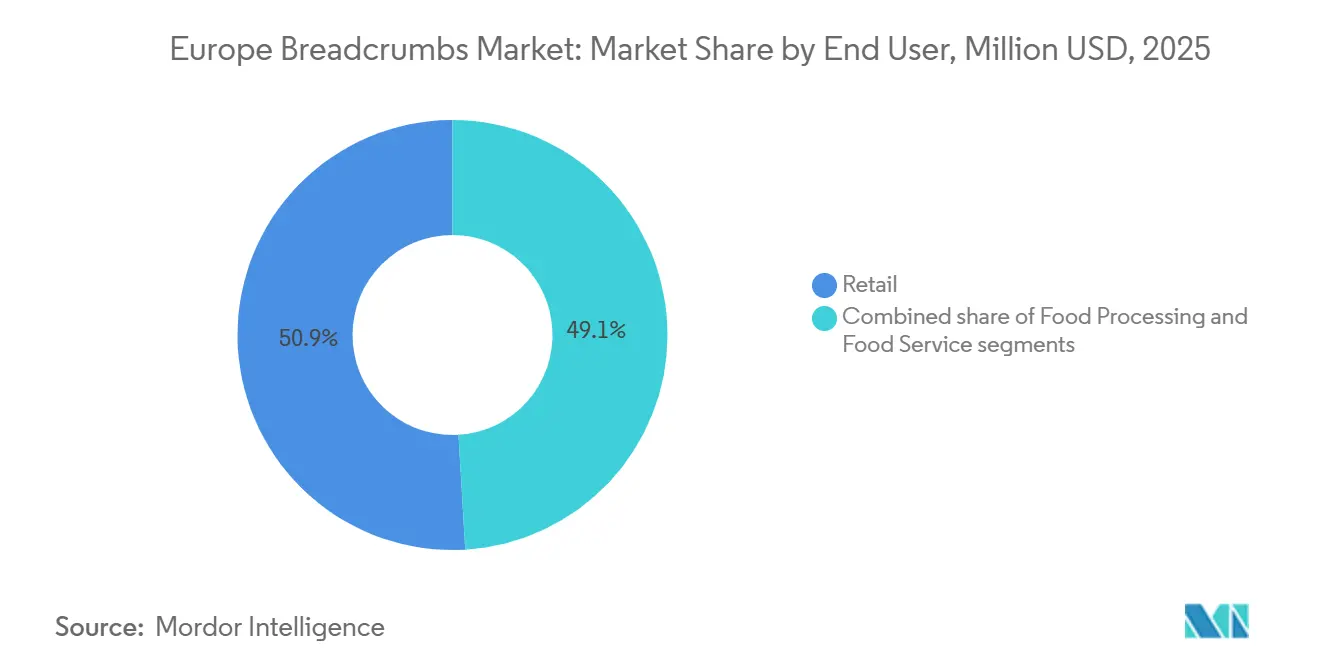

- By end user, retail accounted for 50.94% share in 2025 and is also the fastest-growing end-user segment with a 6.94% CAGR through 2031.

- By geography, Germany led with 21.82% share in 2025, while Poland is forecast to record the fastest country-level growth at 7.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Breadcrumbs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for convenience and ready-to-cook foods | +1.5% | Europe wide, with strong pull in the United Kingdom, Germany, and France | Short term (≤ 2 years) |

| Expansion of the frozen food industry | +1.2% | Western Europe, especially Germany, France, and the Netherlands | Medium term (2-4 years) |

| Rising consumption of coated meat, seafood, and poultry products | +1.0% | Europe wide, with high intensity in Germany, the United Kingdom, and Poland | Medium term (2-4 years) |

| Growth of foodservice sector | +0.8% | Western and Southern Europe, especially the United Kingdom, Germany, Spain, and Italy | Short term (≤ 2 years) |

| Increasing bakery and processed food production | +0.7% | Western Europe, with Poland emerging as a supply hub | Medium term (2-4 years) |

| Surging demand for premium and specialty breadcrumbs | +0.6% | Germany, Italy, the United Kingdom, and Scandinavia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for convenience and ready-to-cook foods

Consumer lifestyles across Europe are increasingly centered around convenience, encouraging higher consumption of ready-to-cook and easy-to-prepare food products that require minimal preparation time. This shift has significantly increased the use of breadcrumbs as a coating, binding, and texture-enhancing ingredient in frozen meals, breaded meat, seafood, poultry, and vegetable products. According to Eurostat, final household consumption expenditure on food and non-alcoholic beverages in the European Union reached approximately EUR 1.18 trillion in 2024, reflecting sustained spending on packaged and convenience foods, including ready-to-cook meal solutions[1]Source: Eurostat, "PRODCOM – Statistics by Product", ec.europa.eu. Food manufacturers are expanding their portfolios of frozen and chilled prepared foods to cater to busy urban consumers seeking quick meal options without compromising on taste or quality. These factors continue to strengthen demand for breadcrumbs across the region's processed and convenience food manufacturing industry.

Expansion of the frozen food industry

The continued expansion of the frozen food industry across Europe is creating significant demand for breadcrumbs, which are widely used as coating and binding ingredients in frozen meat, seafood, poultry, vegetable, and snack products. The increasing preference for frozen foods is driven by their extended shelf life, convenience, and consistent quality, making them popular among both households and foodservice operators. The European Union remains one of the world's largest producers of frozen potato products, frozen vegetables, frozen bakery products, and frozen prepared meals, supported by strong manufacturing capabilities across countries such as Belgium, the Netherlands, Germany, France, and Poland. Food manufacturers continue to expand production capacities and introduce innovative frozen product offerings to meet evolving consumer preferences. The rapid growth of modern retail channels and cold-chain logistics has further improved the availability and distribution of frozen foods throughout the region.

Rising consumption of coated meat, seafood, and poultry products

The increasing consumption of coated meat, seafood, and poultry products across Europe is contributing to higher demand for breadcrumbs as an essential coating ingredient. Consumers continue to favor breaded products such as chicken nuggets, schnitzels, fish fingers, breaded shrimp, and cutlets due to their convenience, crispy texture, and ease of preparation. According to the European Commission's Meat Market Observatory, EU poultry meat production exceeded 13 million tonnes in 2024, supporting strong demand for breaded and coated poultry products across both retail and foodservice channels[2]Source: European Commission, "Meat Market Observatory", agriculture.ec.europa.eu. Food manufacturers are expanding their portfolios of value-added coated protein products to meet changing consumer preferences and rising demand for ready-to-cook meals. Quick-service restaurants and casual dining establishments are also increasing their offerings of breaded chicken, seafood, and appetizer products, further boosting breadcrumb consumption.

Increasing bakery and processed food production

The steady expansion of bakery and processed food production across Europe is supporting greater demand for breadcrumbs as a functional ingredient in a wide range of food applications. Breadcrumbs are extensively used as coatings, binders, fillers, and toppings in processed meat products, ready meals, snacks, and bakery formulations, making them an integral part of food manufacturing. For instance, according to Unione Italiana Food, Italy's bakery production reached 1,463,994 tons in 2024, highlighting the strong production scale that continues to support robust demand for bakery ingredients and related food inputs[3]Source: Unione Italiana Food, “Bakery Products”, unioneitalianafood.it. Growing consumer preference for packaged baked goods, frozen bakery products, and convenience foods is encouraging manufacturers to expand production capacities across the region. Food processors are also introducing innovative value-added products that require consistent texture and coating performance, further increasing breadcrumb utilization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in wheat and grain prices | -0.8% | Europe wide, with France and Germany most exposed | Short term (≤ 2 years) |

| Stringent EU food safety, labeling, and allergen regulations | -0.5% | All EU member states, especially multi-country operators | Long term (≥ 4 years) |

| Supply chain disruptions affecting raw materials | -0.4% | Eastern Europe and Mediterranean import corridors | Medium term (2-4 years) |

| High energy and labor costs increasing production expenses | -0.6% | Germany, Sweden, and Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in wheat and grain prices

Fluctuations in wheat and other grain prices continue to create cost pressures for breadcrumb manufacturers across Europe, as these raw materials account for a significant share of production expenses. Variability in grain prices is influenced by factors such as adverse weather conditions, geopolitical tensions, changing trade policies, and disruptions in global agricultural supply chains. Rising input costs often reduce manufacturers' profit margins or necessitate price increases, which can affect competitiveness in both retail and foodservice markets. Smaller and regional producers are particularly vulnerable because they have limited bargaining power and fewer opportunities to hedge against raw material price volatility. In addition, unpredictable grain costs make production planning, inventory management, and long-term supply contracts more challenging for manufacturers.

Stringent EU food safety, labeling, and allergen regulations

Stringent food safety, labeling, and allergen regulations across the European Union present significant compliance challenges for breadcrumb manufacturers. Producers must adhere to rigorous requirements related to ingredient traceability, allergen declaration, food hygiene, labeling accuracy, and product quality to ensure compliance with EU regulations. Meeting these standards often requires continuous investments in quality assurance systems, certification processes, laboratory testing, and production upgrades, increasing overall operational costs. Manufacturers producing gluten-free or allergen-free breadcrumbs face additional requirements to prevent cross-contamination and maintain certified production environments. Frequent regulatory updates also require companies to revise product formulations, packaging, and labeling, adding further complexity to operations. Small and medium-sized manufacturers may face greater financial and administrative burdens due to limited technical and regulatory resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Conventional Dominance Masking Specialty-Led Margin Capture

Conventional breadcrumbs accounted for 80.63% of the Europe breadcrumbs market in 2025, making them the dominant category due to their widespread use across retail, foodservice, and industrial food processing applications. Their leadership is supported by strong demand from bakeries, restaurants, and ready-meal manufacturers that rely on conventional breadcrumbs for coating, binding, stuffing, and texture enhancement. These products remain highly preferred because they are cost-effective, readily available, and compatible with a broad range of meat, seafood, vegetable, and snack preparations. Large-scale food manufacturers continue to favor conventional breadcrumbs owing to their consistent quality, long shelf life, and ease of integration into automated production lines.

The gluten-free breadcrumbs segment is projected to register the fastest CAGR of 7.28% between 2026 and 2031, driven by the rising adoption of gluten-free diets across Europe. Increasing consumer awareness of celiac disease, gluten intolerance, and digestive health is encouraging households and foodservice operators to choose gluten-free coating and binding alternatives. Food manufacturers are expanding their portfolios with gluten-free breadcrumbs made from ingredients such as rice, corn, chickpea, quinoa, and other gluten-free grains to meet evolving dietary preferences.

By Crumb Type: Dry Breadth, Panko Momentum, and Fresh’s Niche Role

Dry breadcrumbs acccounted for an 84.26% share in 2025, giving them the broadest installed base across the Europe breadcrumbs market. Their leadership stems from their long shelf life, ease of transport, lower handling risk, and compatibility with automated breading lines that cannot tolerate significant variation in moisture or density. These attributes make dry crumbs especially important in frozen proteins, ready meals, and high-throughput processing environments where operators closely monitor line efficiency. The dominance of dry products also reflects the strength of legacy recipes in retail and foodservice, where buyers understand their performance and cost profile.

Panko is forecast to grow at a CAGR of 6.99% through 2031, making it the fastest-growing crumb type and a clear premium growth segment. Foodservice operators are adopting panko because it creates a lighter, more visible crust that performs well across deep frying, convection cooking, and home air-fryer applications. Retail demand is also expanding, as shoppers seek restaurant-style texture in easy-to-use formats. Fresh breadcrumbs serve a different purpose, as they are better suited for binding, stuffing, and high-moisture recipes. However, their short shelf life and more complex logistics continue to limit their adoption. As a result, the crumb-type structure remains divided into three distinct roles: dry crumbs lead in scale, panko drives growth, and fresh crumbs serve a smaller but defensible niche.

By Ingredient Type: Wheat Anchors the Base, Corn Leads the Reformulation Curve

Wheat-based breadcrumbs held a 78.71% share in 2025, confirming wheat’s position as the primary functional and commercial base for the Europe breadcrumbs market. Established milling networks in Germany, France, and Poland continue to support this position, while processors remain familiar with the performance of wheat crumbs in standard breading systems. Existing equipment and recipes further strengthen the segment, as reformulating away from wheat may require additional validation in large-scale production settings. As a result, wheat is expected to account for most volumes sold across industrial and retail applications. This established base helps maintain broad supply availability, but it also exposes a significant share of the Europe breadcrumbs market to wheat price and quality volatility.

Corn-based breadcrumbs are projected to expand at a CAGR of 7.19% from 2026 to 2031, driven by allergen management requirements and the broader shift toward gluten-free products. Corn also appeals to processors seeking different oil absorption characteristics or a distinct texture while staying close to familiar coating practices. Rice-based crumbs remain relevant in specialty applications, particularly where a lighter grain profile or regional food traditions support their use. The smaller “others” category, which includes pulse- and vegetable-derived crumbs, remains limited in size but holds strategic importance because it aligns with plant-based coated products and cleaner ingredient positioning. Poland’s export platform further supports supply, as agri-food exports are expected to reach EUR 58.4 billion (USD 63.1 billion) in 2025, strengthening the broader manufacturing base for grain-derived food ingredients.

By Flavor: Unflavored Scale, Flavored Premiumization

Unflavored breadcrumbs accounted for a 66.21% share in 2025, reflecting the preferences of processors and foodservice operators that need a neutral base they can season later according to brand or menu requirements. This segment aligns well with large-scale production systems, as it gives customers greater control over final recipe design and reduces the number of stock keeping units they need to manage. Neutral crumbs also simplify allergen and traceability management in many cases, especially compared with heavily seasoned blends. These factors explain why unflavored products remain central to the Europe breadcrumbs market across industrial and institutional channels. Their strong market position remains steady, supported by buyers’ practical requirements rather than habit alone.

Flavored breadcrumbs are forecast to grow at a CAGR of 7.16% through 2031, with most of the momentum coming from retail and premium foodservice applications. Shoppers want ready-to-use formats that reduce meal preparation time and deliver distinct taste profiles without additional mixing at home. At the same time, seasoned crumbs increase complexity for producers, as spice blends can require additional allergen declarations, stricter segregation, and more detailed documentation. These added requirements increase the effective cost of each flavored stock keeping unit, which can make it difficult for smaller suppliers to scale them profitably. The premium segment of the market is expected to shift further toward flavored formats, especially as the use of air-fryer and oven-ready meals continues to expand.

By End User: Retail’s Dual Dominance and the Foodservice Competitive Frontier

Retail accounted for 50.94% of end-user demand in 2025 and is projected to expand at a CAGR of 6.94% through 2031, making it both the largest and fastest-growing outlet in the Europe breadcrumbs market. This trend reflects more than routine home cooking, as retail shelves and online stores now offer a broader range of panko, gluten-free, and flavored products than in previous years. Specialty demand, which once depended on a limited health-food retail footprint, is now reaching mainstream shoppers through supermarkets, hypermarkets, and digital channels. This shift has expanded access for smaller brands and specialists while encouraging larger suppliers to refresh their retail product ranges. In terms of the Europe breadcrumbs market size, retail remains the most visible channel, as it combines broad household penetration with a rising premium product mix.

Food processing remains the industrial core of the category, as processors purchase larger volumes and often commit to recurring programs linked to ready meals, coated meats, and frozen seafood. Foodservice sits between retail and processing, as it supports both recurring institutional demand and a premium segment shaped by chef-led texture and presentation choices. Online retail is gaining importance within the broader retail mix because it allows specialty products to scale without relying solely on physical shelf space. This is important for gluten-free and premium formats, which often build repeat demand through targeted digital discovery and direct-to-consumer availability.

Geography Analysis

Germany held 21.82% of the Europe breadcrumbs market share in 2025, maintaining its position as the largest country-level market in the region. Its leadership stems from a large food processing base, broad consumption of breaded protein products, and a manufacturing ecosystem that supports frozen foods, prepared meals, and retail grocery supply. Germany also has a strong domestic heritage in breadcrumbs, which helps sustain local expertise even as international suppliers expand. LEIMER remains part of this long-standing base, while larger coating system suppliers also use Germany as a key industrial supply point. As a result, the Europe breadcrumbs market continues to have a strong German center, supported by deep local demand and manufacturing capability.

France, the United Kingdom, and the Netherlands form the next important group in the Europe breadcrumbs market, with each country contributing in a distinct way. France benefits from a sizable industrial bakery and food production base. Its industrial bakery sector is expected to generate EUR 16.2 billion (USD 17.5 billion) in revenue in 2025, supporting the broader bread substrate and processing ecosystem around crumb production. The United Kingdom remains important due to multi-site coating operations that serve processors, foodservice customers, and private-label retail requirements. The Netherlands plays a strategic role as a distribution and logistics platform for premium crumb formats moving across Western Europe.

Southern and Northern Europe add different demand signals to the Europe breadcrumbs market. Italy and Spain support stronger gluten-free and specialty demand, driven by culinary traditions and the expansion of certified production capacity by specialist suppliers. Dr. Schär reported a EUR 17 million (USD 18.4 million) investment in its Alagón, Spain, site in 2024, with 85% of the output exported, highlighting how Iberian facilities support broader European supply rather than only local demand. Sweden’s health-focused consumer base supports specialty adoption, while Belgium’s concentrated retail structure continues to pressure private-label quality and cost. Poland is the fastest-growing country market with a 7.56% CAGR through 2031, supported by processing growth and export links into Western Europe.

Competitive Landscape

The Europe breadcrumbs market remains highly fragmented, characterized by the presence of numerous multinational ingredient suppliers, specialized coating solution providers, and regional breadcrumb manufacturers competing across diverse end-use industries. Market participants cater to retail consumers, foodservice operators, and industrial food processors with a broad portfolio of plain, seasoned, panko, whole wheat, and specialty breadcrumbs. While large international companies benefit from extensive manufacturing capabilities and established distribution networks, regional producers maintain a competitive advantage through localized product offerings, flexible production, and strong relationships with domestic food manufacturers.

Product innovation and application-specific development remain key competitive strategies among manufacturers. Companies are increasingly investing in the development of clean-label, gluten-free, organic, and allergen-free breadcrumbs to align with evolving consumer preferences and regulatory requirements. Manufacturers are also introducing value-added products such as seasoned coatings, crispy textured breadcrumbs, and customized crumb sizes designed for meat, seafood, plant-based foods, and ready-to-cook applications. Investments in advanced processing technologies and quality assurance further strengthen competitive positioning. These innovations enable suppliers to differentiate their offerings in an increasingly competitive marketplace.

Competitive intensity is further influenced by expanding demand from convenience foods, frozen products, and foodservice establishments across Europe. Manufacturers are strengthening their market presence through capacity expansions, strategic partnerships, acquisitions, and broader distribution networks to improve regional coverage and customer reach. Sustainability has also emerged as an important area of competition, with companies focusing on responsible sourcing, waste reduction, recyclable packaging, and energy-efficient manufacturing processes. These combined strategies are expected to shape the competitive landscape of the Europe breadcrumbs market throughout the forecast period.

Europe Breadcrumbs Industry Leaders

-

Dr. Schär AG

-

LEIMER KG

-

Kikkoman Corporation

-

Newly Weds Foods, Inc.

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Dr. Schär planned to invest EUR 28 million (~USD 30 million) in production facilities across Italy, Spain, and Germany. The investment includes expanding its Apolda facility in Thuringia, Germany, to support gluten-free bread and roll production and building foodservice supply capabilities for system caterers and QSR operators in Europe.

- January 2026: Newly Weds Foods acquired UK-based JDM Food Group, a manufacturer of fresh liquid food products in Bicker, Lincolnshire. The acquisition expands Newly Weds Foods’ liquid and sauce manufacturing capabilities across the United Kingdom and mainland Europe, directly strengthening its integrated coating-and-sauce offering for food processors, foodservice operators, and retailers.

- May 2025: Nactarome Group merged I.P.A.M. Industrie Prodotti Alimentari Manenti S.R.L. with Aromata Group S.R.L. to support growth and optimization. Following the merger, Aromata Group S.R.L. rebranded as Nactarome S.R.L.

Europe Breadcrumbs Market Report Scope

Breadcrumbs are dry, finely or coarsely ground bread particles produced from fresh or baked bread that are processed and dried for use as a food ingredient. The Europe breadcrumbs market is segmented by category, crumb type, ingredient type, flavor, end user and geography. Based on category, the market is segmented into conventional and gluten-free. Based on crumb type, the market is segmented into dry, panko and fresh. Based on ingredient type, the market is segmented into wheat-based, corn-based, rice-based and others. Based on flavor, the market is segmented into unflavored and flavored. Based on end user, the market is segmented into food processing, food service and retail. Based on geography, the market is segmented into Germany, France, United Kingdom, Spain, Netherlands, Italy, Sweden, Poland, Belgium, and Rest of Europe. For each segment, the market sizing and forecasting have been done in value terms (USD million) and volume (Tons).

| Conventional |

| Gluten-Free |

| Dry |

| Panko |

| Fresh |

| Wheat-Based |

| Corn-Based |

| Rice-Based |

| Others |

| Flavored |

| Unflavored |

| Food Processing | Processed Meat |

| Ready-to-Cook Foods | |

| Others | |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| Germany |

| France |

| United Kingdom |

| Spain |

| Netherlands |

| Italy |

| Sweden |

| Poland |

| Belgium |

| Rest of Europe |

| By Category | Conventional | |

| Gluten-Free | ||

| By Crumb Type | Dry | |

| Panko | ||

| Fresh | ||

| By Ingredient Type | Wheat-Based | |

| Corn-Based | ||

| Rice-Based | ||

| Others | ||

| By Flavor | Flavored | |

| Unflavored | ||

| By End User | Food Processing | Processed Meat |

| Ready-to-Cook Foods | ||

| Others | ||

| Foodservice | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the 2031 outlook for breadcrumbs in Europe?

The Europe breadcrumbs market is forecast to reach USD 753.23 million by 2031, rising from USD 557.84 million in 2026 at a 6.19% CAGR over 2026 to 2031.

Which product group holds the largest share today?

Conventional breadcrumbs lead by category with 80.63% share in 2025, while dry breadcrumbs lead by crumb type with 84.26% share.

Why is retail so important across Europe?

Retail accounted for 50.94% of demand in 2025 and is also the fastest-growing end-user channel, supported by broader shelf assortment and stronger online access for specialty products.

Which country leads demand and which one is growing fastest?

Germany held the largest share at 21.83% in 2025, while Poland is expected to record the fastest growth at 7.56% CAGR through 2031.

What is changing competition among suppliers?

Competition is shifting toward suppliers that can provide specialty formats, strong allergen control, technical support, and wider coating system capabilities rather than only commodity crumb volumes.

Page last updated on: