Bread Crumbs Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.30 Billion |

| Market Size (2031) | USD 1.73 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bread Crumbs Market Analysis by Mordor Intelligence

The bread crumbs market size is expected to grow from USD 1.23 billion in 2025 to USD 1.30 billion in 2026 and is forecast to reach USD 1.73 billion by 2031 at a 5.88% CAGR over 2026-2031. Demand is tracking the surge in at-home meal preparation, where consumers want coatings that deliver restaurant-level crunch without deep-frying. Momentum is strongest for panko because its light, slivered structure tolerates convection heat, a necessity as ownership of air fryers accelerates. Quick-service restaurants are locking in multi-year contracts for bulk panko to standardize texture across global menus, which lifts volumes for vertically integrated suppliers. Ingredient innovation is shifting toward gluten-free and multi-grain blends that appeal to clean-label shoppers while reducing allergen risk for food processors. Against this backdrop, efficient hedging against wheat price swings and rapid SKU launches will determine which manufacturers capture the next wave of growth.

Key Report Takeaways

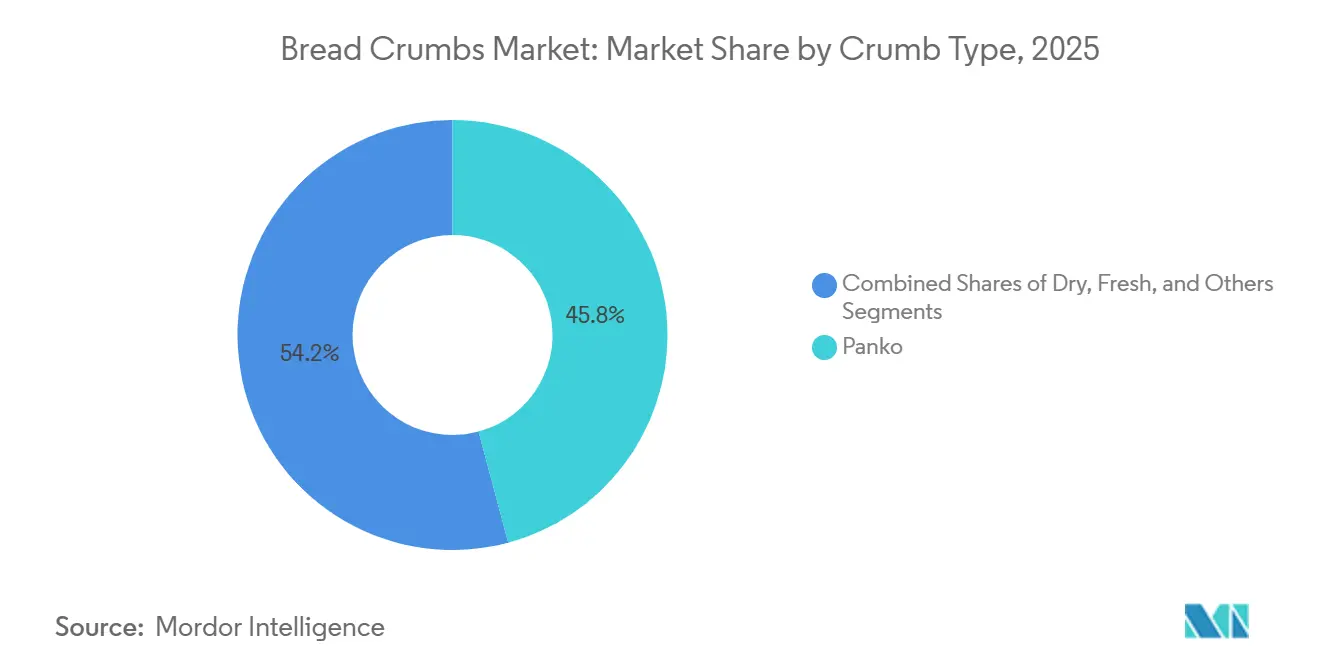

- By crumb type, panko led with 45.83% of bread crumbs market share in 2025 and is projected to post a 6.85% CAGR through 2031.

- By ingredient, wheat accounted for 61.81% share of the bread crumbs market size in 2025, while multi-grain is advancing at a 6.91% CAGR over the same period.

- By flavor, unflavored products dominated with a 66.87% revenue share in 2025; flavored coatings are the fastest riser, with a 7.15% CAGR to 2031.

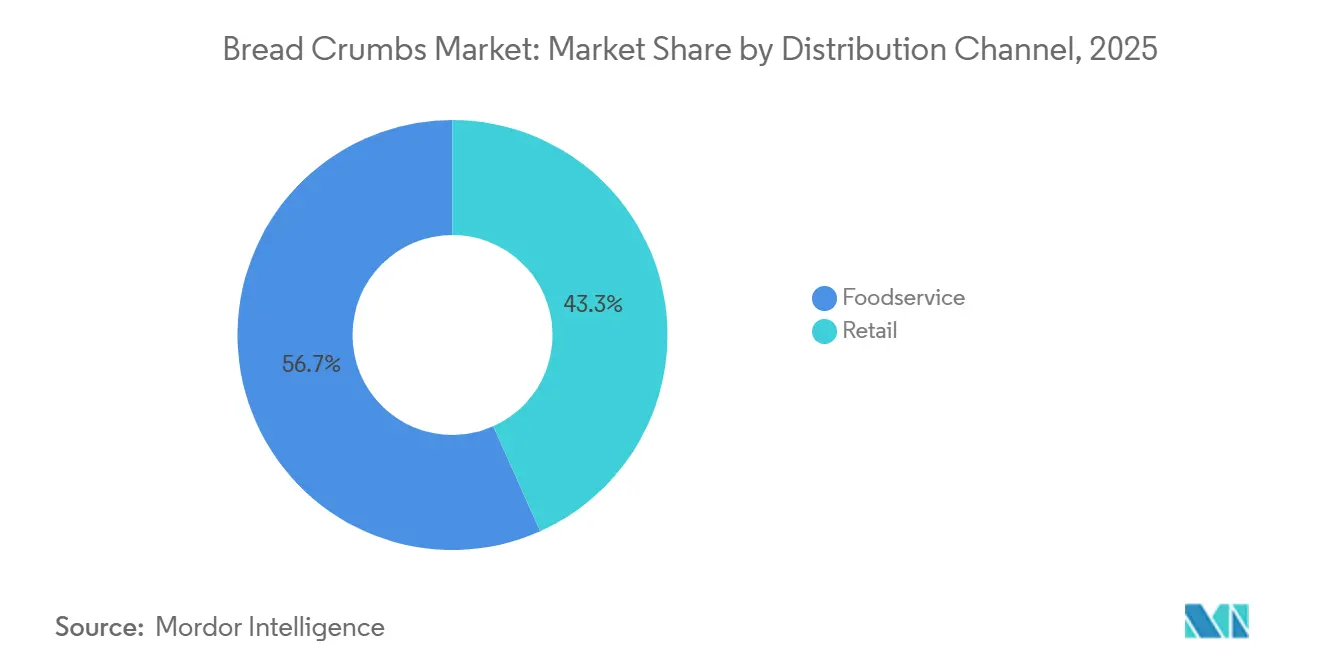

- By distribution channel, foodservice accounted for 56.69% of 2025 sales, while retail is expanding at a 6.76% CAGR on the strength of private-label launches.

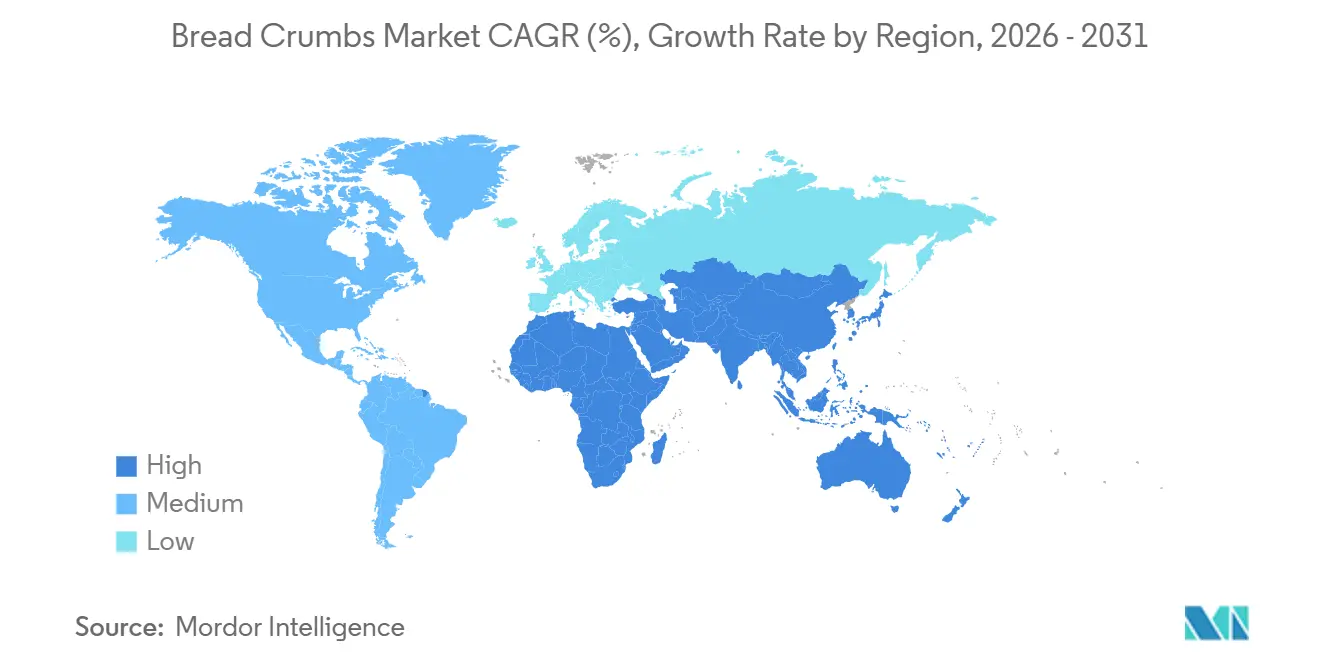

- By geography, Asia-Pacific captured 51.05% of the 2025 value and is forecast to grow at 6.74% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bread Crumbs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for convenience and ready-to-cook foods | +1.2% | Global, with strongest uptake in North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Expansion of processed meat and plant-based product applications | +0.9% | North America and Europe, spillover to Asia-Pacific QSR chains | Long term (≥ 4 years) |

| Rising popularity of air-frying and home-based cooking trends | +1.1% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Innovation in gluten-free and specialty bread crumb formulations | +0.7% | Europe and North America, emerging in Asia-Pacific premium segments | Medium term (2-4 years) |

| Technological advancements improving texture and functionality | +0.6% | Global, with early adoption in Japan and South Korea | Long term (≥ 4 years) |

| Increased consumption of fried and coated snack products | +0.8% | Asia-Pacific core, expanding to Middle East and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Convenience and Ready-to-Cook Foods

The shift toward home-prepared meals that mimic restaurant quality is compressing preparation time expectations, with 93% of US consumers reporting increased at-home cooking frequency in 2024, according to a HelloFresh survey[1]Source: HelloFresh, “Consumer Cooking Trends Survey 2024,” hellofresh.com. Breadcrumbs serve as the critical textural component in air-fried chicken tenders, fish fillets, and vegetable patties, categories where frozen-food manufacturers are reformulating to achieve crispness without deep-frying. This demand is quantifiable: Conagra Brands reported that air-fryer-compatible frozen foods generated USD 6.1 billion in US retail sales in 2024, a segment where breadcrumb coatings differentiate premium SKUs from commodity offerings[2]Source: Conagra Brands, “Frozen Foods and Air Fryer Compatibility Report,” conagrabrands.com. The trend extends beyond North America, as urbanization in Southeast Asia drives demand for pre-breaded proteins that reduce cooking complexity for dual-income households. Ingredient suppliers are responding by developing adhesion systems that maintain coating integrity during freezer-to-air-fryer transitions, a technical challenge that separates market leaders from regional players.

Expansion of Processed Meat and Plant-Based Product Applications

Breadcrumbs serve as both binder and texturizer in plant-based meat analogs, absorbing moisture released during cooking and helping prevent the rubbery mouthfeel that plagued early formulations. The Plant-Based Meat Association documented that breadcrumbs and starches together account for 8-12% of formulation weight in successful plant-based nuggets and patties, providing structural integrity that isolated soy protein alone cannot deliver[3]Source: Plant Based Meat Association, “Formulation Guidelines 2025,” plantbasedmeats.org. Beyond Meat's 2025 reformulation of its chicken tenders increased breadcrumb content by 3 percentage points to improve bite-through resistance, a change that lifted repeat-purchase rates by 18% in test markets. Traditional processed-meat applications remain the volume driver, with QSR chains standardizing on panko coatings for chicken sandwiches to achieve the audible crunch that drives social-media virality. This dual-track growth, conventional and plant-based, insulates breadcrumb demand from protein-source disruptions.

Rising Popularity of Air-Frying and Home-Based Cooking Trends

Air fryer ownership is rising in consideration among US households, with most owners using the appliance weekly. This adoption curve is reshaping breadcrumb formulation priorities, as traditional coatings designed for deep-frying often burn or fail to crisp in convection-heat environments. Panko's coarser particle size and lower moisture content make it inherently better suited to air-frying, explaining its 6.85% CAGR advantage over fine dry crumbs. Retailers are capitalizing on this shift by expanding shelf space for specialty breadcrumbs marketed explicitly for air-fryer use, a merchandising strategy that commands 20-30% price premiums over generic SKUs. The trend is self-reinforcing: as more consumers acquire air fryers, food manufacturers reformulate frozen entrees to optimize for that cooking method, which in turn drives breadcrumb suppliers to invest in research and development for heat-stable coatings. This cycle is most advanced in North America and Western Europe, but is accelerating in Asia-Pacific markets, where compact air fryers align with smaller kitchen footprints.

Innovation in Gluten-Free and Specialty Bread Crumb Formulations

Celiac disease affects approximately 1% of the global population, but gluten avoidance extends to an estimated 6-8% of consumers in North America and Europe who self-report gluten sensitivity, creating an addressable market that justifies dedicated production lines, according to the FDA Gluten-Free Labeling. Gluten-free breadcrumbs rely on rice flour, corn starch, and hydrocolloids to replicate the binding properties of wheat gluten, a technical challenge that Kansas State University research in 2024 addressed through modified tapioca starch blends that improved coating adhesion by 35%[4]Source: Kansas State University, “Wheat and Grain Science 2024,” k-state.edu . The Gluten-Free Certification Organization (GFCO) requires products to test below 10 parts per million of gluten, a standard that necessitates segregated milling and packaging, capital investments that favor large-scale producers but create entry barriers, and premium pricing. Multi-grain formulations are emerging as a parallel innovation track, blending quinoa, amaranth, and millet to appeal to health-conscious consumers willing to pay 40-50% premiums for perceived nutritional superiority. These specialty segments are growing faster than the overall market but remain subscale, suggesting consolidation opportunities for ingredient companies with clean-room manufacturing capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing shift toward low-carb and reduced-bread diets | -0.8% | North America and Western Europe, emerging in urban Asia-Pacific | Long term (≥ 4 years) |

| Allergen and gluten sensitivity concerns | -0.5% | Europe and North America, with regulatory spillover to Asia-Pacific | Medium term (2-4 years) |

| Volatility in wheat and raw material prices | -0.6% | Global, with acute impact in import-dependent Middle East and Africa | Short term (≤ 2 years) |

| Stringent food safety and labeling compliance requirements | -0.4% | Europe and North America, cascading to export-oriented manufacturers in Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Shift Toward Low-Carb and Reduced-Bread Diets

Ketogenic and low-carb diets attracted 12.9 million US adults in 2024, a cohort that actively avoids bread-based products, including breadcrumbs, according to consumer surveys tracked by the International Food Information Council[5]Source: International Food Information Council, “Food and Health Survey 2024,” foodinsight.org . This dietary shift contributed to an 8% decline in US bread consumption between 2020 and 2024, a headwind that breadcrumb suppliers cannot fully offset through product innovation, according to the USDA Economic Research Service. The restraint is most acute in retail channels, where health-conscious consumers scrutinize carbohydrate content on nutrition labels and substitute almond flour or crushed pork rinds for traditional breadcrumbs in home cooking. Foodservice operators face less pressure, as restaurant diners prioritize taste and texture over macronutrient composition, but the long-term risk is that younger consumers who adopt low-carb eating in their 20s and 30s will carry those preferences into higher-spending decades. Breadcrumb manufacturers are responding with cauliflower-based and protein-fortified variants, but these alternatives remain niche and have not achieved repeat-purchase rates sufficient to replace lost volume from conventional SKUs.

Volatility in Wheat and Raw Material Prices

Soft red winter wheat, the primary input for breadcrumb production, traded between USD 5.50 and USD 6.00 per bushel in 2024-2025, reflecting weather disruptions in the US Great Plains and Black Sea export restrictions, according to USDA price reporting. This 9% price swing over a 12-month period compresses margins for breadcrumb producers who lack forward hedging programs or long-term supply contracts with millers. Smaller manufacturers are disproportionately affected, as they cannot absorb input-cost spikes through operational efficiencies or pass them through to large foodservice buyers who negotiate annual contracts. The volatility also disrupts new-product development, as research and development teams struggle to forecast ingredient costs for formulations that require 18-24 months from concept to commercialization. Diversification into non-wheat substrates, rice, corn, and legume flours, offers partial mitigation, but these alternatives introduce their own price risks and require reformulation to match the textural benchmarks that wheat-based breadcrumbs have established over decades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crumb Type: Panko Dominance Driven by Texture Premiumization

Panko breadcrumbs captured 45.83% of the market in 2025 and are expanding at 6.85% through 2031, outpacing dry and fresh variants due to their coarser particle size and superior crispness retention in both deep-fried and air-fried applications. The segment's growth is anchored in QSR adoption, where chains like Chick-fil-A and Shake Shack specify panko for chicken sandwiches to achieve the audible crunch that drives social-media engagement and repeat visits. Panko's manufacturing process, using electric current to create a crustless bread loaf that is then shredded, produces slivers rather than granules, a structural difference that creates more surface area for oil absorption and browning, according to the Kikkoman Corporation. This technical advantage is difficult to replicate with conventional milling, giving Japanese producers like Kikkoman a defensible position in premium foodservice channels.

Dry breadcrumbs remain the workhorse of the category, used in meatloaf, meatballs, and casseroles where binding rather than texture is the priority, but their slower growth reflects limited innovation and the pressures of commoditization. Fresh breadcrumbs, made from day-old bread and sold refrigerated, serve a niche in European bakeries and high-end restaurants but face shelf-life constraints that limit scalability. The "Others" segment includes specialty formats like gluten-free, organic, and flavored variants, which collectively are growing at 7.2% as manufacturers target health-conscious and premium-tier consumers. Regulatory compliance under ISO 22000 food safety standards is becoming a baseline expectation for panko suppliers serving multinational foodservice chains, a requirement that favors large-scale producers with certified quality-management systems.

By Ingredient: Multi-Grain Formulations Challenge Wheat Hegemony

Wheat-based breadcrumbs held 61.81% of ingredient share in 2025, reflecting decades of supply-chain optimization and consumer familiarity, but multi-grain variants are expanding at 6.91% as manufacturers seek differentiation in crowded retail aisles. Multi-grain formulations blend wheat with oats, barley, quinoa, or millet to deliver higher fiber content and a nuttier flavor profile that appeals to consumers willing to pay 30-40% premiums for perceived health benefits. The challenge lies in maintaining coating adhesion, as non-wheat grains lack gluten's elastic properties; suppliers are addressing this through hydrocolloid binders like xanthan gum and guar gum, which add 0.5-1.0% to formulation costs but enable clean-label claims that resonate in natural-foods channels, according to the Food Hydrocolloids Journal.

Corn-based breadcrumbs serve the gluten-free segment and Latin American markets where corn is a dietary staple, offering a slightly sweeter flavor that pairs well with seafood and vegetable applications. Rice-based variants are growing in Asia-Pacific, particularly in Japan and South Korea, where rice flour is abundant and consumer acceptance of non-wheat coatings is higher than in Western markets. The "Others" category includes legume-based breadcrumbs made from chickpea or lentil flour, which deliver higher protein content (18-22% vs. 10-12% for wheat) but face texture challenges that limit their use to plant-based meat applications. Ingredient diversification is also a risk-mitigation strategy against wheat price volatility, as manufacturers with multi-substrate capabilities can shift production in response to commodity-market swings without reformulating end products.

By Flavor: Unflavored Breadcrumbs Retain Versatility Advantage

Unflavored breadcrumbs accounted for 66.87% of the market in 2025, a dominance rooted in their versatility across sweet and savory applications, but flavored variants are growing at 7.15% as foodservice operators seek labor-saving ingredients that reduce on-site seasoning steps. Flavored breadcrumbs incorporate herbs (Italian seasoning, garlic, onion), spices (Cajun, lemon pepper), and cheese powders directly into the coating, allowing restaurant kitchens to streamline prep workflows and ensure flavor consistency across shifts. This trend is most pronounced in casual-dining chains, where menu complexity has increased, but labor availability has declined, creating demand for "pre-seasoned" ingredients that maintain quality with less-skilled cooks. McCormick & Company reported in its 2025 investor presentation that flavored breadcrumb sales to foodservice customers grew 14% year-over-year, driven by new SKUs targeting ethnic cuisines like Korean fried chicken and Nashville hot chicken.

Unflavored breadcrumbs retain their lead in retail channels, where home cooks prefer to control seasoning levels and avoid the sodium content that flavored variants often carry (400-600 mg per serving vs. 150-200 mg for unflavored). The segment also dominates in industrial applications like meatball and sausage production, where manufacturers blend breadcrumbs with proprietary spice mixes and do not want flavor interference from the coating ingredient. Regulatory influence is minimal in this segmentation, as both flavored and unflavored variants must comply with the same allergen-labeling and nutritional-disclosure rules under FDA and EFSA frameworks. The growth gap between the two segments suggests that convenience and labor efficiency are becoming more valuable than ingredient flexibility in commercial kitchens, a shift that could accelerate if wage pressures persist in the foodservice sector.

By Distribution Channel: Retail Gains Ground Through Private Label and E-Commerce

Foodservice channels held 56.69% of distribution share in 2025, reflecting the high-volume purchasing patterns of QSR chains, casual-dining restaurants, and institutional caterers, but retail is expanding at 6.76% as private-label breadcrumbs proliferate and e-commerce reduces the friction of specialty-product discovery. Walmart, Costco, and Kroger have all launched or expanded store-brand breadcrumb lines in the past 18 months, leveraging their scale to negotiate lower input costs and undercut branded SKUs by 20-30% on shelf price. This private-label push is eroding the market share of mid-tier brands that lack the marketing budgets to sustain consumer loyalty, creating a barbell market structure where premium brands (organic, gluten-free) and value brands (private label) gain at the expense of the middle.

E-commerce penetration in the breadcrumb is rising, as Amazon and specialty grocers like Thrive Market offer subscription models that reduce per-unit costs for consumers who buy in bulk. Online channels are particularly important for gluten-free and specialty breadcrumbs, which often lack distribution in smaller grocery stores but can reach national audiences through digital fulfillment. Foodservice remains the larger channel due to the sheer volume consumed by restaurant chains, a single QSR location can use 50-100 pounds of breadcrumbs per week, but its slower growth reflects market saturation in developed regions and the shift toward ghost kitchens and delivery-only concepts that use simpler menus with fewer breaded items. The distribution dynamics suggest that breadcrumb suppliers must develop dual go-to-market strategies: high-touch relationship management for foodservice accounts and digital-first marketing for retail consumers.

Geography Analysis

Asia-Pacific commanded 51.05% of the market in 2025 and is forecast to grow at 6.74% through 2031, propelled by Japan's panko export engine and China's accelerating QSR penetration. Japan exported approximately 45,000 metric tons of panko in 2024, with the United States and Europe as primary destinations, a trade flow that positions Japanese producers like Kikkoman and Ajinomoto as global standard-setters for premium breadcrumb quality according to the Japan External Trade Organization. China's breadcrumb consumption is rising in tandem with Western fast-food expansion; KFC and McDonald's collectively operate over 10,000 locations in China, each standardizing on breaded chicken products that require consistent coating ingredients. India represents an emerging opportunity, where vegetarian breaded snacks like paneer pakoras and aloo tikkis are gaining traction in QSR formats, but the market remains fragmented with limited penetration of international breadcrumb brands. Southeast Asian nations, Thailand, Indonesia, and Vietnam, are experiencing similar dynamics, as rising incomes and urbanization drive demand for convenient protein options that rely on breadcrumb coatings. Regulatory frameworks in Asia-Pacific are less harmonized than in Europe, with each country maintaining distinct food-safety standards, a complexity that favors regional suppliers with local compliance expertise over multinational entrants.

North America continues to exhibit steady growth, although expansion is moderated by the maturity of foodservice penetration and the previously noted shift toward low-carbohydrate diets. The region’s competitive advantage is rooted in a strong pace of innovation. Ingredient suppliers in the United States have introduced a broad range of new breadcrumb SKUs, including vegetable-based alternatives, protein-enriched formulations, and globally inspired flavor profiles. Canada’s breadcrumb demand remains closely aligned with its robust frozen food industry, where manufacturers utilize breadcrumb coatings across a variety of products intended for retail and foodservice channels. Mexico is increasingly positioning itself as a strategic production hub, supported by major bakery and ingredient companies operating breadcrumb lines that cater to both domestic quick-service restaurants and export markets. The USMCA trade framework continues to support seamless cross-border movement, encouraging supply chain efficiencies and regional integration.

Europe presents a distinct market landscape shaped by rigorous regulatory standards and a strong consumer preference for clean-label products. Compliance with EU food labeling and disclosure regulations increases operational complexity, particularly for smaller producers, while simultaneously strengthening the position of established manufacturers with certified quality systems. Germany and the United Kingdom represent key markets, supported by consistent demand for breaded and coated food products. In contrast, France demonstrates a greater inclination toward fresh breadcrumbs used in traditional culinary applications, although this segment faces gradual pressure from shifting consumer lifestyles and rising demand for convenience foods. Southern European countries, including Italy and Spain, are witnessing increased interest in gluten-free breadcrumb alternatives, reflecting heightened awareness of dietary sensitivities and a cultural focus on ingredient quality. Regional growth prospects in Europe remain somewhat constrained by broader macroeconomic challenges and demographic shifts, including an aging population and evolving dietary habits that favor lighter or less fried food options. Nevertheless, premium and specialty breadcrumb segments continue to demonstrate resilience, supported by demand for higher-quality, health-oriented, and differentiated product offerings.

South America and the Middle East & Africa collectively represent a smaller share in the market in 2025, with growth driven by urbanization and QSR expansion in key cities. Brazil's breadcrumb market is tied to its large poultry industry, where breaded chicken products are staples in both retail and foodservice channels. Argentina and Chile show similar patterns, with breadcrumb consumption concentrated in urban centers like Buenos Aires and Santiago. The Middle East is witnessing growth in halal-certified breadcrumbs, a segment where compliance with Islamic dietary laws requires dedicated production lines and third-party certification from bodies like the Islamic Food and Nutrition Council of America (IFANCA). South Africa and Nigeria are emerging markets where rising incomes are driving demand for Western-style fast food, but infrastructure gaps and import tariffs limit breadcrumb availability outside major metropolitan areas. These regions offer long-term growth potential but require patient capital and local partnerships to navigate regulatory and logistical complexities.

Competitive Landscape

The breadcrumbs market exhibits moderate fragmentation, with no single player commanding more than 15% global share. Yet the top 5 players include Kerry Group, Newly Weds Foods, McCormick, Kikkoman, and Grupo Bimbo with vertical integration and long-term foodservice contracts. These leaders leverage backward integration into milling and forward integration into seasoning to capture margin at multiple value-chain stages, a strategy that smaller toll manufacturers cannot replicate without significant capital investment. Kerry Group's 2025 annual report highlighted that its Taste & Nutrition division, which includes breadcrumb coatings, achieved 6.2% organic growth driven by new product wins with North American QSR chains.

The competitive dynamic is shifting toward technical service capabilities, where suppliers embed food scientists in customer R&D facilities to co-develop coatings that meet specific frying-time, texture, and cost targets, a consultative approach that creates switching costs and deepens customer relationships. White-space opportunities exist in organic and halal-certified segments, where compliance costs deter incumbents but enable 20-30% price premiums. Emerging disruptors include plant-based ingredient specialists like Ingredion, which is adapting its pea-protein and tapioca-starch portfolios to serve the breadcrumb category, and regional players in Asia-Pacific that are scaling panko production to challenge Japanese exporters on price.

Technology is becoming a competitive differentiator, with leaders investing in extrusion and spray-drying equipment that produces breadcrumbs with controlled particle-size distributions and moisture levels, attributes that improve coating uniformity and reduce waste in automated breading lines. Patent filings in breadcrumb formulation have increased 18% since 2023, with innovations focused on adhesion promoters, anti-caking agents, and shelf-life extension, according to USPTO records, according to the United States Patent and Trademark Office. The landscape suggests that breadcrumb suppliers with R&D depth, regulatory agility, and multi-region manufacturing footprints will consolidate share, while undifferentiated commodity producers face margin compression and potential exit.

Bread Crumbs Industry Leaders

Kerry Group plc

Newly Weds Foods Inc.

McCormick & Company Inc.

Kikkoman Corporation

Grupo Bimbo SAB de CV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Newly Weds Foods has inaugurated a new production line. The facility spans 5,200 square meters with an 8,000-square-meter production area and reaches a height of 22 meters. The facility has storage capacity for 2,400 pallets. The upper level contains a production line for Japanese-style breadcrumbs, featuring an autobake oven for crisp bread production.

- October 2024: Aleia's Gluten Free Foods, LLC relocated to a new facility that has received certification from two gluten-free organizations: GFCO and The GFMP (Gluten Free Manufacturing Program). The facility operates under SQF and HACCP standards, with established GMP and operating procedures for cleanup and sanitation.

- September 2024: AB Kauno Grūdai, a subsidiary of AB Akola Group, has invested EUR 6.7 million in a new breadcrumb factory. The investment covers the construction and equipment of the facility.

Global Bread Crumbs Market Report Scope

Bread crumbs are small particles of dry bread that are used as an ingredient or coating in cooking. They are typically made by grinding or processing leftover or fresh bread into fine, medium, or coarse pieces. The market is segmented into crumb type, ingredient type, by flavor, distribution channel, and geography. By crumb type, the market is segmented into dry bread crumbs, fresh bread crumbs, panko, and others. Based on ingredients, the market is categorized into wheat-based, corn-based, rice-based, multi-grain, and other ingredient types. By flavor, the market is divided into unflavored and flavored bread crumbs. By distribution channel, the market is segmented into foodservice and retail, with the retail segment further classified into supermarkets and hypermarkets, convenience stores, online retail, and others. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. This report provides a comprehensive analysis of the global bread crumbs market, with market size estimations and forecasts presented in both value (USD Million) and volume (Tons).

| Dry |

| Fresh |

| Panko |

| Others |

| Wheat-Based |

| Corn-Based |

| Rice-Based |

| Multi-Grain |

| Others |

| Unflavored |

| Flavored |

| Foodservice | |

| Retail | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Crumb Type | Dry | |

| Fresh | ||

| Panko | ||

| Others | ||

| By Ingredient | Wheat-Based | |

| Corn-Based | ||

| Rice-Based | ||

| Multi-Grain | ||

| Others | ||

| By Flavor | Unflavored | |

| Flavored | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the bread crumbs market be by 2031?

It is projected to reach USD 1.73 billion by 2031, growing at a 5.88% CAGR from 2026.

Which crumb type is growing fastest?

Panko is expanding at a 6.85% CAGR through 2031 due to superior performance in air-fryers.

What drives demand for gluten-free breadcrumbs?

Rising allergen awareness and GFCO certification standards encourage consumers and QSRs to switch to certified gluten-free coatings.

Why is Asia-Pacific the leading region?

Japan’s panko exports and China’s rapid QSR expansion help Asia-Pacific command over 50% of global sales.

How are commodity price swings managed by suppliers?

Market leaders hedge wheat, diversify into multi-grain substrates, and adjust formulations to protect margins.

Page last updated on: