Southeast Asia Green IT Software and Cloud Sustainability Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

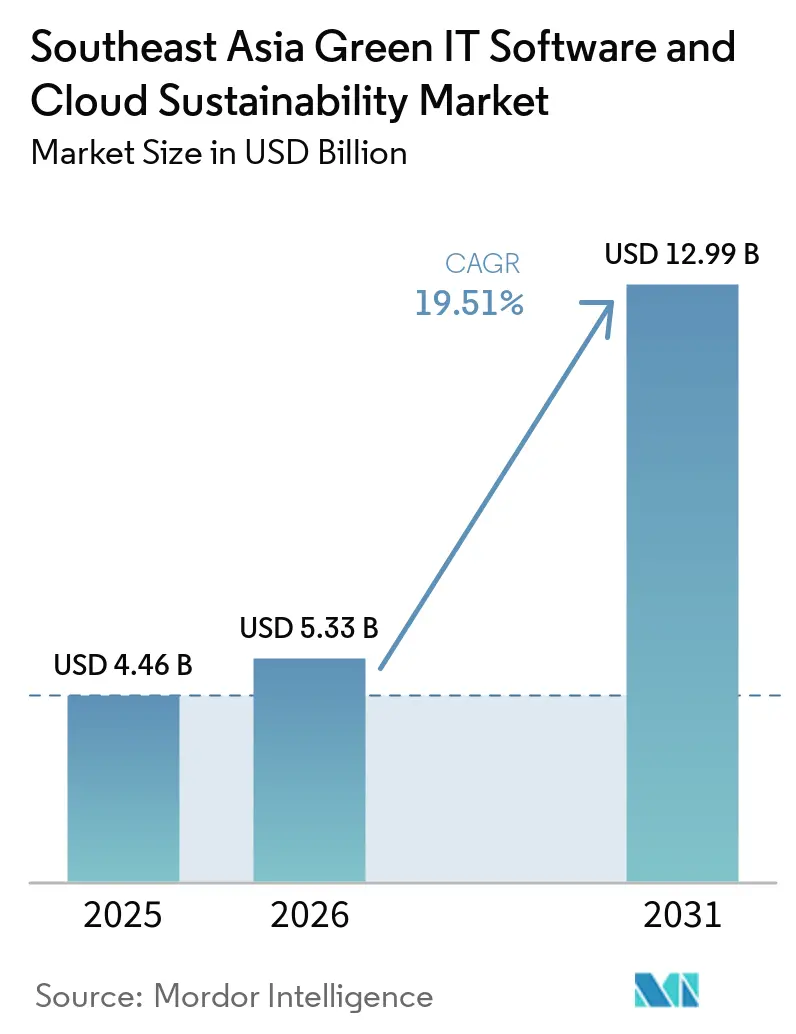

| Base Year Market Size (2025) | USD 4.46 Billion |

| Market Size (2026) | USD 5.33 Billion |

| Market Size (2031) | USD 12.99 Billion |

| Growth Rate (2026 - 2031) | 19.51% CAGR |

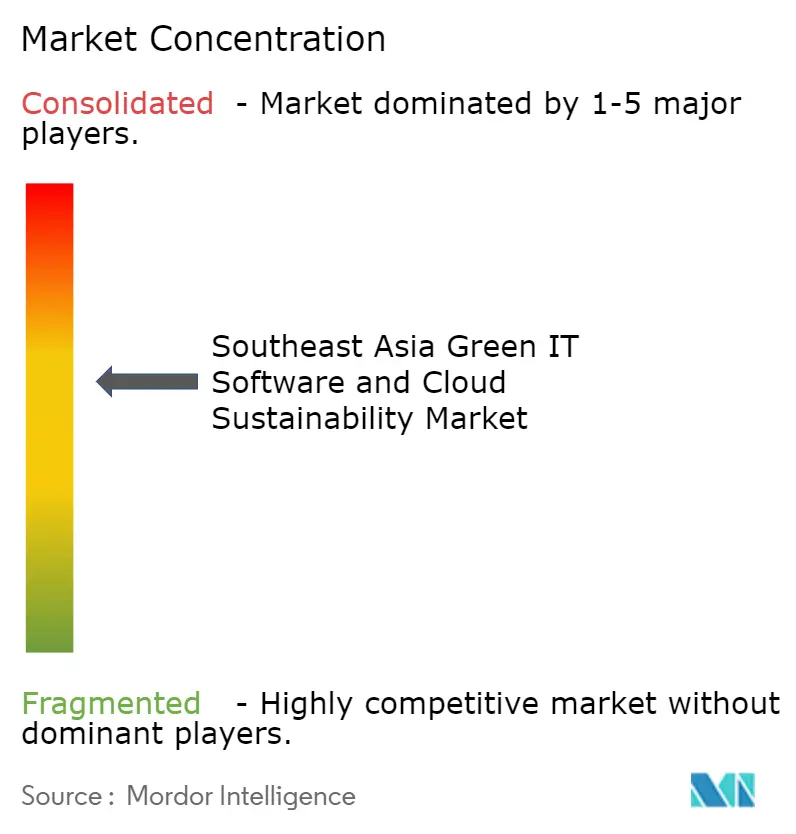

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Green IT Software and Cloud Sustainability Market Analysis by Mordor Intelligence

The Southeast Asia Green IT Software and Cloud Sustainability Market size was valued at USD 4.46 billion in 2025 and estimated to grow from USD 5.33 billion in 2026 to reach USD 12.99 billion by 2031, at a CAGR of 19.51% during the forecast period (2026-2031). The Southeast Asia Green IT Software and Cloud Sustainability Market is expanding as enterprises replace legacy infrastructure with cloud environments that enable tracking of energy use, carbon output, and resource efficiency in a single workflow. Regional policy is also raising the adoption baseline because green digital infrastructure is moving closer to a compliance requirement in cross-border digital trade. Multinational supply chain pressure is pushing companies in manufacturing, telecom, healthcare, and services to show more reliable carbon data across their operations. Public funding and state-backed digital programs in Singapore, Malaysia, Thailand, Vietnam, and Indonesia are strengthening the commercial case for buyers who had delayed these investments. Competition is strongest in enterprise accounts led by global cloud and software vendors, while regional specialists are finding room in local compliance, supplier reporting, and mid-sized customer deployments.

Key Report Takeaways

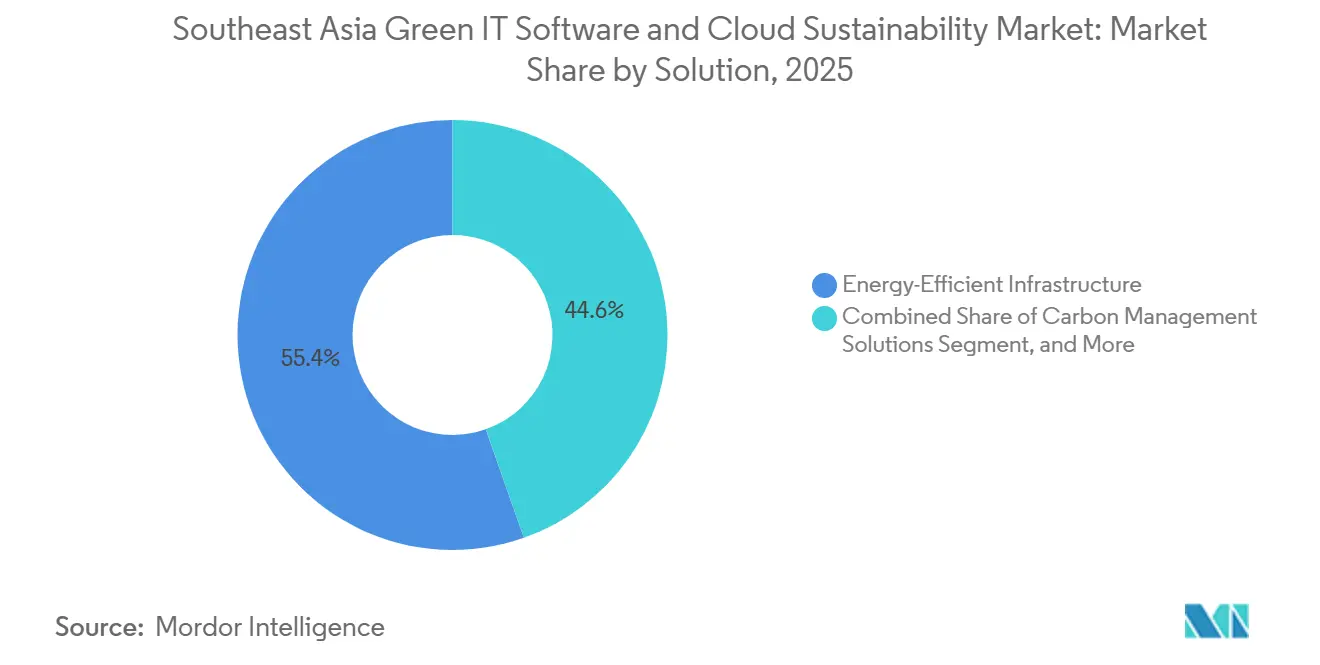

- By solution, Energy-Efficient Infrastructure held 55.39% share in 2025 in the Southeast Asia Green IT Software and Cloud Sustainability Market, while Carbon Management Solutions is projected to expand at a 20.56% CAGR through 2031.

- By deployment model, Cloud-Based held a 68.47% share in 2025 in the Southeast Asia Cloud Sustainability Market, while On-Premises remained relevant for regulated deployments.

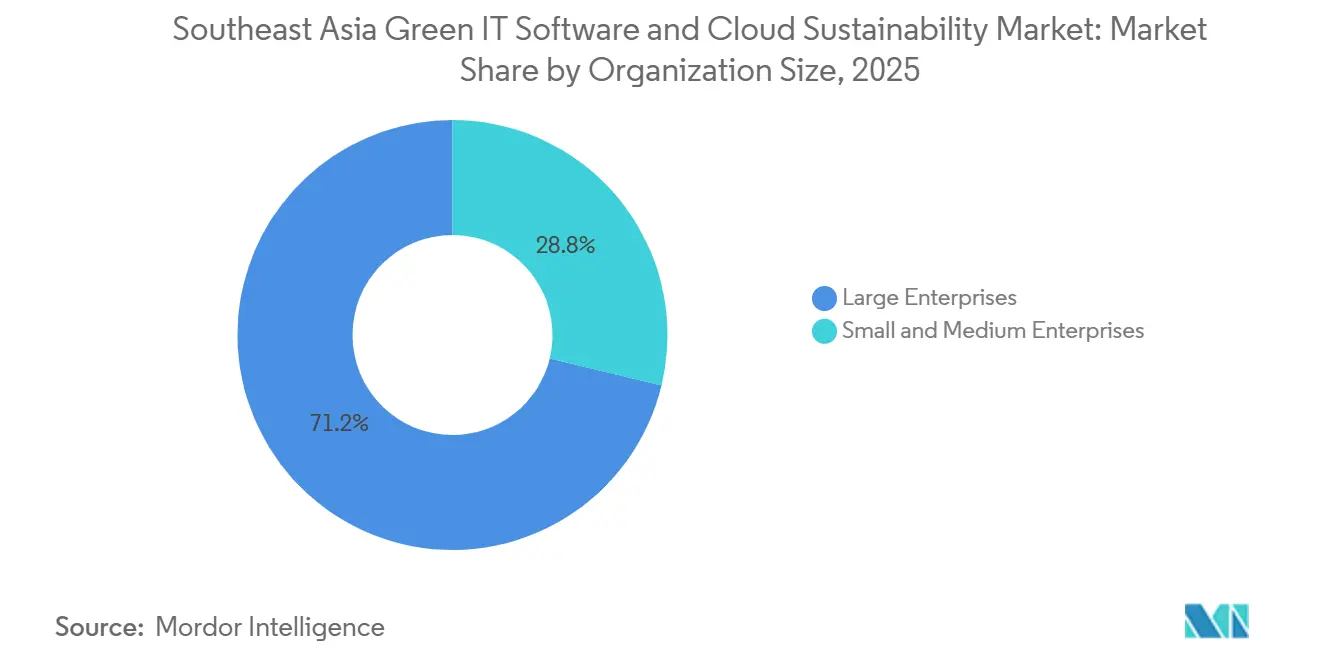

- By organization size, Large Enterprises held 71.22% share in 2025 in the Southeast Asia Green IT Software Market, while Small and Medium Enterprises are projected to expand at a 20.93% CAGR through 2031.

- By end user, Information Technology and Telecom accounted for 23.51% share in 2025, while Healthcare and Life Sciences a projected to expand at a 19.89% CAGR through 2031.

- By geography, Singapore held 26.42% share in 2025, while Vietnam is projected to expand at a 20.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Green IT Software and Cloud Sustainability Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Enterprise Cloud Modernization | +4.2% | Singapore, Malaysia, Indonesia, Thailand, Vietnam | Short term (≤ 2 years) |

| Carbon Reporting Pressure From Multinational Customers | +3.8% | Singapore, Malaysia, Thailand, Vietnam | Medium term (2-4 years) |

| Renewable-Powered Data Center Procurement | +3.1% | Malaysia, Singapore, Vietnam, Philippines | Medium term (2-4 years) |

| Green Software Engineering Adoption | +2.7% | Singapore, Indonesia, broader Southeast Asia | Medium term (2-4 years) |

| AI-Based Energy Optimization In IT Operations | +2.4% | Singapore, Malaysia, Thailand | Short term (≤ 2 years) |

| Government-Funded Digital Sustainability Programs | +2.1% | Vietnam, Indonesia, Thailand, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Enterprise Cloud Modernization

The Southeast Asia Green IT Software and Cloud Sustainability Market is receiving direct support from enterprise cloud modernization, as buyers replace legacy systems with platforms that manage performance and sustainability in a single environment. This replacement cycle matters because green software and cloud sustainability tools are easier to adopt when companies rebuild workloads rather than extending legacy infrastructure. Malaysia's Digital Ecosystem Acceleration incentive framework links data center investment support to the adoption of at least 1 green technology, which keeps sustainable deployment criteria close to new digital capacity decisions. A 2025 study on Malaysian SMEs found that structured IT competencies and a better understanding of cloud architecture improved firm performance, indicating that cloud readiness is not only a technical issue but also an organizational one. The same pattern supports vendors that can package training, architecture support, and reporting tools together rather than selling software in isolation. As more firms leave sunk investments behind, the Southeast Asia Cloud Sustainability Market should continue to see faster early-stage buying in cloud-first deployments.

Carbon Reporting Pressure From Multinational Customers

The Southeast Asia Green IT Software and Cloud Sustainability Market is also being shaped by customer-led reporting pressure because large buyers now expect suppliers to provide carbon data that can be reviewed and reused in formal disclosures. Zevero's July 2025 partnership with Tai Sin Electric in Singapore showed how exchange-linked climate disclosure requirements were already influencing software selection at the listed company level.[1]Zevero, “Zevero Partners With Tai Sin Electric to Prepare for SGX Climate Disclosure Mandate,” Zevero, zevero.earth This type of demand is harder to postpone because it sits within procurement, financing, and market access decisions rather than standing apart as a separate sustainability exercise. Vietnam's export manufacturers face this pressure more directly because carbon transparency is increasingly tied to external customer requirements and overseas trade conditions. Singapore's Gprnt platform launched in May 2025 with USD 4.62 million in seed funding from Ant International and MUFG Bank, and it used government utility data to automate the generation of sustainability metrics for businesses, reducing reporting friction for smaller firms. That structure creates a broader buyer base for the Southeast Asia Green Information Technology Software and Cloud Sustainability Market, as large enterprises often pass down reporting expectations to tier-1 and tier-2 suppliers.

Renewable-Powered Data Center Procurement

The Southeast Asia Green IT Software and Cloud Sustainability Market is benefiting from renewable-powered data center procurement because clean power contracts require stronger monitoring, attribution, and reporting across cloud operations. TotalEnergies and Google signed a 21-year power purchase agreement in Malaysia in December 2025 for 1TWh of renewable electricity tied to Google's data center operations, which connected long-term clean energy sourcing with digital infrastructure expansion. The ASEAN Guide for Sustainable Data Center Development, published in early 2026, called for more harmonized standards for sustainable data center development, including renewable energy verification and balanced infrastructure planning. Once operators commit to green power contracts, they also need software that can match procurement records with usage, emissions, and audit trails across facilities. This is especially relevant for smaller regional operators that lack the scale of hyperscalers but still need to demonstrate comparable sustainability performance to enterprise customers. That makes renewable-linked compliance and reporting software a practical growth path for the Southeast Asia Green IT Software and Cloud Sustainability Market.

Green Software Engineering Adoption

The Southeast Asia Green IT Software and Cloud Sustainability Market is starting to gain from green software engineering as enterprises look beyond hardware efficiency and focus on how software design affects energy use. Binus University research published in 2025 showed growing attention in Indonesia to dynamic power management, green cloud infrastructure selection, and modular software design, thereby giving this area greater institutional weight. Singapore's SS 715:2025 standard on the energy efficiency of data center IT equipment targets at least a 30% reduction in IT equipment energy consumption through operational optimization, helping connect hardware policy with software-led workload decisions. Global IT service providers are also incorporating software carbon-intensity methods into regional delivery models, changing how some enterprise buyers evaluate platform efficiency. The Univers AI lab, launched in Singapore in October 2024 with support from Microsoft, AMD, the National University of Singapore, and IMDA, added a local testing ground for digital energy optimization solutions. Over time, this should favor vendors in the Southeast Asia Green IT Software and Cloud Sustainability Market that demonstrate lower computational overhead and higher workload efficiency in real operating conditions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Transition Cost From Legacy IT Environments | -2.8% | Indonesia, Thailand, Philippines, Vietnam | Medium term (2-4 years) |

| Limited Green Software Standards and Measurement Consistency | -2.1% | Region wide, most acute in Indonesia, Vietnam, Philippines | Long term (≥ 4 years) |

| Split Incentives Between IT, Finance, and Sustainability Teams | -1.6% | Regional, most acute in large conglomerates | Medium term (2-4 years) |

| Shortage of Specialized Green Cloud and Sustainability Skills | -1.4% | Region wide, most acute in Vietnam, Philippines, Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Transition Cost From Legacy IT Environments

The Southeast Asia Green IT Software and Cloud Sustainability Market still faces a real slowdown due to the high cost of migrating from legacy environments, as many firms must modernize core systems before they can use advanced sustainability tools effectively. That spending is hard to approve when migration programs span several quarters and savings accrue later than the initial capital outlay. A 2025 study in Cogent Business and Management found that cloud migration in developing-market institutions is often slowed by technical, organizational, and cultural barriers, which aligns with the pattern seen across regulated and asset-heavy sectors in the region. This problem is strongest in firms that still rely on custom on-premises systems, fragmented data estates, and separate ownership between technology, finance, and operations. Even when buyers accept the compliance value of new tools, the prerequisite infrastructure work can delay procurement decisions by a full budget cycle. As a result, the Southeast Asia Green IT Software and Cloud Sustainability Market grows faster where cloud migration is already underway and more slowly where legacy replacement still dominates the agenda.

Limited Green Software Standards and Measurement Consistency

Inconsistent standards also constrain the Southeast Asia Green IT Software and Cloud Sustainability Market, as enterprises still lack a fully consistent regional framework for measuring software-related carbon intensity. A 2025 Tech for Good Institute survey found that 40% of regional capital providers cited unclear return on investment as a major barrier, while 39% pointed to regulatory uncertainty, which shows how unclear measurement weakens buyer confidence. Singapore has moved further ahead through standards and certification work, but similar operating frameworks are less established across Indonesia, Vietnam, Thailand, and the Philippines. The ASEAN Guide for Sustainable Data Center Development also identified fragmented governance across energy, water, ICT, and land use as a major structural challenge for credible sustainability measurement. This makes procurement comparisons harder because vendors may present carbon efficiency claims in different formats and with different assumptions. Until standards align more closely, the Southeast Asia Green IT Software Market will continue to incur higher verification costs and slower cross-border adoption in larger multi-country accounts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Energy Efficiency Leads While Carbon Platforms Gain Ground

Energy-Efficient Infrastructure accounted for 55.39% of the Southeast Asia Green IT Software and Cloud Sustainability Market in 2025, making it the largest solution category in the region. This lead reflected its role as the first layer of spending because server optimization, cooling software, and workload management are usually easier to approve than broader carbon platforms. The segment also benefited from regional data center expansion, especially in markets where new capacity is being linked to stricter operating efficiency requirements. Singapore's Green Data Center Roadmap targeted at least 300MW of additional data center capacity and reserved another 200MW for operators that can deploy green energy, which kept demand firm for software that improves energy performance.[2]Infocomm Media Development Authority, “Green DC Roadmap,” IMDA, imda.gov.sg In practice, many buyers entered the Southeast Asia Green IT Software and Cloud Sustainability Market through this solution category before moving into deeper reporting and carbon management layers.

Carbon Management Solutions is projected to expand at a 20.56% CAGR through 2031, which makes it the fastest-growing solution area in the Southeast Asia Green IT Software and Cloud Sustainability Market. Demand is widening because buyers now want real-time visibility, automated disclosures, and auditable emissions records, not just efficiency gains. This shift is tied to reporting pressure from listed companies, export manufacturers, and supply chains that need better scope tracking across operations and partners. Financing conditions are also improving because the ASEAN Catalytic Green Finance Facility has mobilized more than USD 1 billion in co-financed green infrastructure loans, which supports a broader environment for sustainability-linked digital spending. Sustainable cloud platforms, green software tools, and asset lifecycle applications are also gaining relevance, but vendors that can connect carbon management with enterprise workflows still hold a stronger position as the Southeast Asia Green Information Technology Software and Cloud Sustainability Market matures.

By Deployment Model: Cloud-Based Platforms Hold the Advantage

Cloud-Based held 68.47% of the Southeast Asia Green IT Software and Cloud Sustainability Market share in 2025, demonstrating a clear lead in hosted delivery across the region. This format fits the software category because sustainability monitoring often needs centralized data collection, scalable analytics, and easier updates across many sites. It also aligns with how many buyers procure software, since subscription models reduce the need for extensive local infrastructure and shorten deployment timelines. The Southeast Asia Green IT Software and Cloud Sustainability Market has therefore leaned toward cloud-first rollouts in sectors that want faster implementation and more flexible reporting across several countries. As more buyers combine operational dashboards with audit needs, cloud delivery remains the simpler starting point for most new deployments.

On-Premises continued to matter in banking, government, and other sensitive environments where data sovereignty and internal control still shape technology choices. These deployments often act as a bridge for firms that want energy and carbon monitoring without moving all workloads to the public cloud at once. Vietnam's Decision 1121/QD-TTg, signed in June 2025, approved a national action program for cloud computing development and called for green, safe, and high-performance data center infrastructure, ensuring sustainability requirements remain relevant even when migration paths differ. That means vendors able to report across hybrid estates have a better chance of winning complex regional accounts. Over time, the Southeast Asia Cloud Sustainability Market is likely to favor providers that can handle both cloud and on-premises workloads under a single reporting structure, rather than forcing customers to manage separate tools.

By Organization Size: Large Enterprises Dominate While SME Demand Builds Fast

Large Enterprises held a 71.22% share in 2025, reflecting their larger budgets, broader reporting obligations, and greater exposure to buyer scrutiny across global supply chains. These firms also face more formal board oversight on sustainability and are more likely to run multi-country operations that need common reporting standards. That makes enterprise-grade carbon accounting, workload efficiency, and audit support easier to justify at the approval stage. In the Southeast Asia Green IT Software and Cloud Sustainability Market, large accounts therefore remained the first point of scale for global cloud vendors and enterprise software providers. The category also stayed ahead because large firms could more easily absorb the costs of modernization, integration, and change management than smaller buyers.

Small and Medium Enterprises are projected to expand at a 20.93% CAGR through 2031, which makes them the fastest-growing organization size group. Singapore's GPRNT reporting utility helped drive this shift by automating sustainability metrics for smaller companies using government utility data, reducing manual reporting burdens and the need for costly external support. A 2025 E3S Web of Conferences study on Indonesian SMEs found that cloud-based accounting information systems were positively related to sustainability performance, which supports the value case for affordable digital tools at smaller scale. Supplier reporting is expanding the addressable base because smaller firms are increasingly required to respond to carbon data requests from larger customers. Vendors that can balance low-cost deployment with credible reporting controls should gain more share as the Southeast Asia Green IT Software Market moves further into the mid-market.

By End User: Telecom Holds the Lead While Healthcare Expands Quickly

Information Technology and Telecom held a 23.51% share in 2025, making it the largest end-user group in the Southeast Asia Green IT Software and Cloud Sustainability Market. The lead came from the sector's role as both a direct user of energy-intensive digital infrastructure and a provider of cloud and network services to other industries. Telecom operators also face rising pressure to manage energy demand as data traffic and AI-linked activity increase across networks and data centers. Nokia's work with Indosat Ooredoo Hutchison on AI-powered energy efficiency and ISO 50001-aligned energy management showed how telecom deployments are becoming a live reference point for the rest of the region. Banking, manufacturing, government, utilities, and retail also represent important demand pools, but telecom still carries the broadest mix of operational need and implementation readiness.

Healthcare and Life Sciences is projected to expand at a 19.89% CAGR through 2031, which makes it the fastest-growing end-user segment. Malaysia's Persada National Digital Health Ecosystem, launched in June 2026 at MYR 650 million (USD 147.4 million), is set to deploy a cloud-based clinical management system across 150 government hospitals and 2,488 public healthcare facilities through 2028. Thailand also deployed the Thai Hospital Emission Management System as part of its smart energy and climate action framework, integrating digital emissions tracking into healthcare operations. A 2025 Tech for Good Institute assessment noted strong digital potential across healthcare investment opportunities in Southeast Asia, supporting continued software adoption as hospitals digitize more clinical and operational functions. The Southeast Asia Green IT Software and Cloud Sustainability Market is therefore experiencing durable growth in healthcare because digital care delivery and emissions accountability are advancing together.

Geography Analysis

Singapore captured 26.42% of the Southeast Asia Green IT Software and Cloud Sustainability Market share in 2025, maintaining its position as the largest country market in the region. The country's lead came from mature ESG reporting structures, a high concentration of multinational headquarters, and a clear policy focus on data center efficiency. IMDA's Green Data Center Roadmap sets requirements around efficiency and green energy expansion, including the use of SS 715:2025 and a 1.25 PUE target at full IT load for new entrants under DC-CFA2. Singapore also strengthened market access for smaller firms through GPRNT, which lowered sustainability reporting friction for businesses that would otherwise face a higher cost of entry.

Malaysia and Indonesia are the next important demand bases in the Southeast Asia Green IT Software and Cloud Sustainability Market, as each market is scaling digital infrastructure from a different starting point. Malaysia is pushing ahead with green data center development, and TM Nxera secured 280MW of electricity in January 2026 for its AI-ready green data center campus in Johor, with Phase 1 commercial operations set to start in 2026. ZDATA Group also began development of Malaysia's first GreenRE Platinum-certified hyperscale data center in Johor in March 2026 at MYR 8 billion (USD 1.81 billion), with linked solar assets designed to generate 630,000 MWh annually. These projects matter because renewable-linked infrastructure creates a direct need for cloud sustainability software that can verify energy sourcing and operating efficiency. Indonesia is moving more through enterprise transformation, and Kyndryl's December 2024 migration of Barito Renewables to Microsoft Azure showed that large local deployments are beginning to combine cloud modernization with sustainability goals.

Vietnam is projected to expand at a 20.18% CAGR through 2031, which makes it the fastest-growing geography in the Southeast Asia Green Information Technology Software and Cloud Sustainability Market. The country is benefiting from greenfield digital infrastructure, pressure from the export sector to improve sustainability, and formal government backing for cloud development. Decision 1121/QD-TTg set a policy path for green, safe, and high-performance cloud infrastructure, while the Vietnam Internet Association forecast that the national cloud market would reach USD 1.5 billion by 2030.[3]Vietnam Internet Association, “AI Will Drive the Cloud Market in Vietnam to Reach USD 1.5 Billion by 2030,” Vietnam.vn, vietnam.vn Thailand is important because SET Carbon gave manufacturers and other businesses a low-cost, state-backed route into structured emissions management from January 2025 onward. The Philippines remains at an earlier stage of formal reporting maturity, but STT GDC Philippines signed a 10-year renewable energy agreement for 40.5MW of clean power for its data centers, which points to stronger sustainability accountability at the operator level. Across these markets, demand is strongest when policy, power procurement, and export-linked reporting move in the same direction.

Competitive Landscape

The Southeast Asia Green IT Software and Cloud Sustainability Market remains moderately concentrated in enterprise accounts, where global cloud hyperscalers and large enterprise software vendors hold the strongest positions. Microsoft, Google, and Amazon Web Services lead cloud infrastructure relationships, while software vendors such as SAP and Salesforce benefit from embedding carbon tools inside broader enterprise workflows. This creates high switching costs in larger accounts because buyers often prefer sustainability functions that sit inside systems they already use for finance, operations, and reporting. The Southeast Asia Cloud Sustainability Market is still less consolidated in the mid-market, where local and regional providers compete on regulatory familiarity, implementation support, and pricing.

Strategic activity is shaping competitive positions more than headline consolidation. IBM's enterprise decarbonization work in Indonesia, through its TruMRV solution, demonstrated how AI-enabled monitoring is automating emissions tracking and improving data quality in complex operating environments. Zevero's partnership with Tai Sin Electric in Singapore showed that specialist platforms can still win where disclosure rules create a clear compliance need. Kyndryl's cloud migration work for Barito Renewables in Indonesia is another example of service-led positioning, where modernization and sustainability are sold together rather than as separate projects. These moves matter because buyers increasingly want measurable operating benefits, not only reporting features. The Southeast Asia Green IT Software Market is therefore rewarding vendors that can tie cloud architecture, energy control, and carbon visibility into a single operating case.

Regional standards are also influencing competition in the Southeast Asia Green IT Software and Cloud Sustainability Market by shaping what enterprise buyers expect from software functionality. The ASEAN Guide for Sustainable Data Center Development is drawing attention to renewable energy attribution, efficiency benchmarks, and broader interoperability across data center sustainability programs.[4]ASEAN Secretariat, “ASEAN Guide for Sustainable Data Centre Development,” ASEAN, asean.org That favors providers that can support hybrid workloads, renewable procurement traceability, and audit-ready reporting across several countries at once. Large vendors still have the advantage in enterprise bundling, but regional specialists have more room in supplier reporting, manufacturing compliance, and mid-sized customer onboarding. The Southeast Asia Green Information Technology Software and Cloud Sustainability Market should therefore remain mixed in structure, with concentrated enterprise spending at the top and a fragmented competitive landscape below.

Southeast Asia Green IT Software and Cloud Sustainability Industry Leaders

Microsoft Corporation

Oracle Corporation

Salesforce, Inc.

SAP SE

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Malaysia's Ministry of Health launched the Persada National Digital Health Ecosystem at a total investment of MYR 650 million (USD 147.4 million), deploying a cloud-based clinical management system across 150 government hospitals and 2,488 public healthcare facilities through 2028. The initiative mandates sustainable cloud infrastructure standards and embeds green IT requirements into 1 of Southeast Asia's largest public-sector digital transformation programs.

- March 2026: ZDATA Group commenced development of Malaysia's first GreenRE Platinum-certified hyperscale data center in Johor, involving an investment of MYR 8 billion (USD 1.81 billion). The facility is designed to achieve high energy efficiency standards and will be powered largely by renewable energy from linked solar assets generating 630,000 MWh annually.

- January 2026: TM Nxera, the joint venture between Telekom Malaysia and Nxera, Singtel's regional data center arm, signed a multi-year electricity supply agreement with Tenaga Nasional securing 280MW for its AI-ready green data center campus in Iskandar Puteri, Johor, with Phase 1 commercial operations beginning in 2026 and a mandate to anchor sustainable digital infrastructure for Malaysia's AI and cloud ambitions.

- December 2025: TotalEnergies and Google signed a 21-year power purchase agreement in Malaysia for 1TWh of renewable electricity from the Citra Energies solar plant in Kedah, locking in long-term clean energy supply for Google's data center operations and reinforcing Malaysia's position as a regional hub for sustainably powered hyperscale cloud infrastructure.

Southeast Asia Green IT Software and Cloud Sustainability Market Report Scope

The Southeast Asia Green IT software and cloud sustainability market encompasses energy-efficient infrastructure management, cloud sustainability platforms, carbon management tools, and green software applications. Such tools enable real-time monitoring and the reduction of emissions associated with IT activities. The market's momentum is fueled by swift cloud adoption, significant investments from hyperscalers, and heightened emphasis on ESG and net-zero targets from regulators and corporations. Ultimately, these solutions not only bolster energy efficiency and curtail carbon footprints but also ensure that enterprises' digital transformation efforts resonate with sustainability goals.

The Southeast Asia Green IT Software and Cloud Sustainability Market Report is Segmented by Solution (Energy-Efficient Infrastructure, Sustainable Cloud Platforms, Green Software Solutions, Carbon Management Solutions, and Other Solutions), Deployment Model (Cloud-Based, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), End User (Information Technology and Telecom, Banking, Financial Services, and Insurance, Healthcare and Life Sciences, Manufacturing, Government and Public Sector, Energy and Utilities, Retail and E-Commerce, and Other End Users), and Geography (Singapore, Indonesia, Malaysia, Thailand, Vietnam, Philippines, and Rest of Southeast Asia). The Market Forecasts are Provided in Terms of Value (USD).

| Energy-Efficient Infrastructure |

| Sustainable Cloud Platforms |

| Green Software Solutions |

| Carbon Management Solutions |

| Other Solutions |

| Cloud-Based |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Information Technology and Telecom |

| Banking, Financial Services, and Insurance |

| Healthcare and Life Sciences |

| Manufacturing |

| Government and Public Sector |

| Energy and Utilities |

| Retail and E-Commerce |

| Other End Users |

| Singapore |

| Indonesia |

| Malaysia |

| Thailand |

| Vietnam |

| Philippines |

| Rest of Southeast Asia |

| By Solution | Energy-Efficient Infrastructure |

| Sustainable Cloud Platforms | |

| Green Software Solutions | |

| Carbon Management Solutions | |

| Other Solutions | |

| By Deployment Model | Cloud-Based |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End User | Information Technology and Telecom |

| Banking, Financial Services, and Insurance | |

| Healthcare and Life Sciences | |

| Manufacturing | |

| Government and Public Sector | |

| Energy and Utilities | |

| Retail and E-Commerce | |

| Other End Users | |

| By Geography | Singapore |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

What is the 2026 size of Southeast Asia green IT software and cloud sustainability?

The Southeast Asia Green IT Software and Cloud Sustainability Market stands at USD 5.33 billion in 2026 and is projected to reach USD 12.99 billion by 2031 at a 19.51% CAGR.

Which solution category leads spending across the region?

Energy-Efficient Infrastructure led with 55.39% share in 2025, showing that buyers still begin with efficiency tools before moving into broader carbon platforms.

Which deployment model is used most often?

Cloud-Based led with 68.47% share in 2025 because buyers prefer scalable reporting, centralized analytics, and easier software updates across multiple sites.

Why are SMEs becoming more important in this space?

SMEs are projected to expand at a 20.93% CAGR through 2031 as lower-cost platforms and supplier reporting requirements make adoption more practical and more necessary.

Which end-user group is growing the fastest?

Healthcare and Life Sciences is projected to grow at a 19.89% CAGR through 2031, supported by public digital health programs and hospital emissions tracking initiatives.

Which country offers the strongest near-term growth outlook?

Vietnam is projected to grow at a 20.18% CAGR through 2031, supported by cloud policy, export-sector compliance needs, and new green digital infrastructure investment.

Page last updated on: