Software Development Tools Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

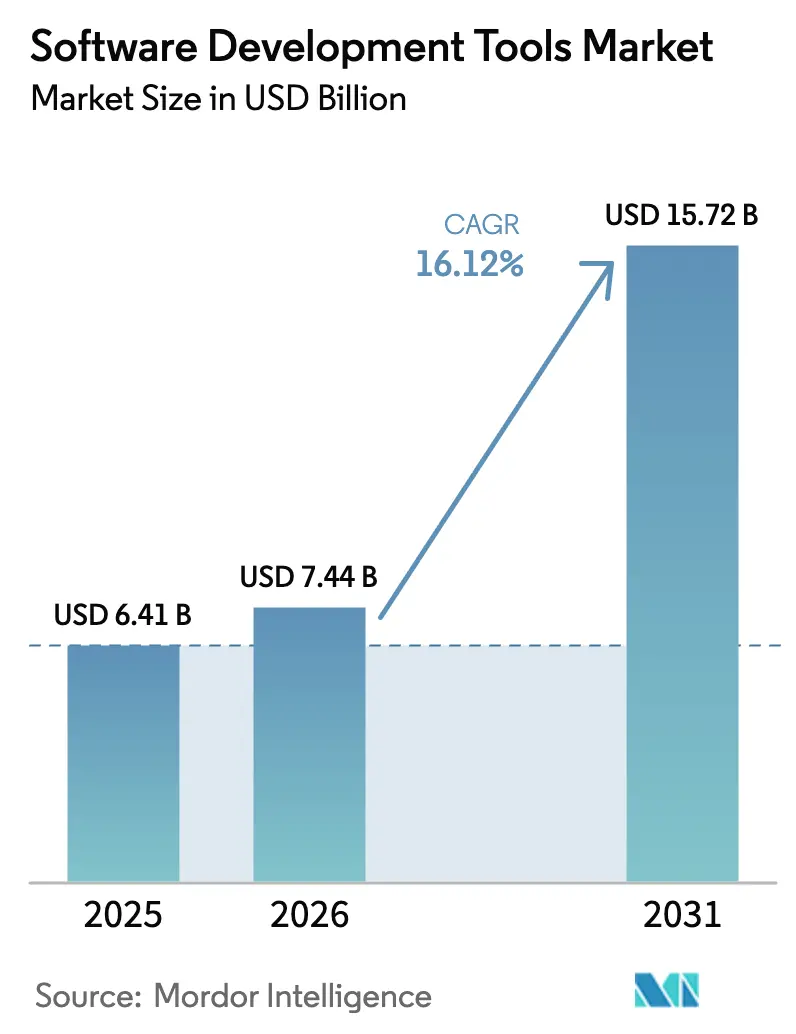

| Market Size (2026) | USD 7.44 Billion |

| Market Size (2031) | USD 15.72 Billion |

| Growth Rate (2026 - 2031) | 16.12% CAGR |

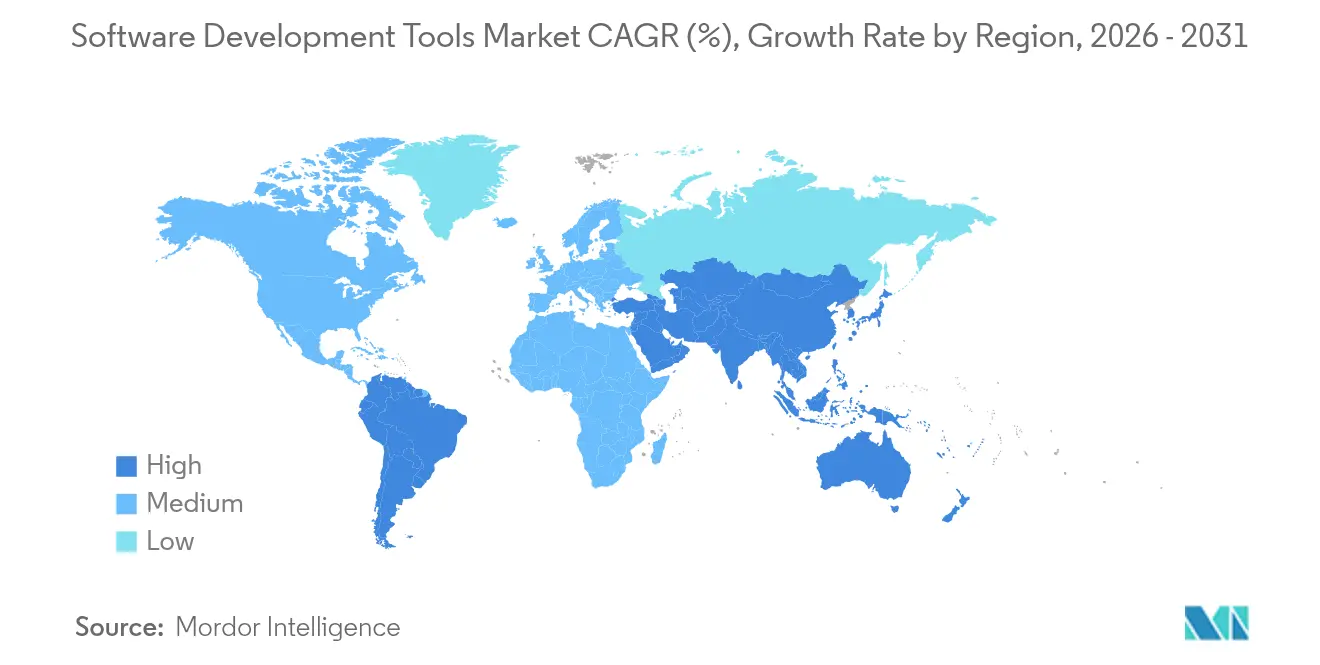

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software Development Tools Market Analysis by Mordor Intelligence

The software development tools market size is expected to grow from USD 6.41 billion in 2025 to USD 7.44 billion in 2026 and is forecast to reach USD 15.72 billion by 2031 at 16.12% CAGR over 2026-2031. Investment momentum stems from artificial intelligence–assisted coding, cloud-native development, and enterprise digital-transformation programs that prioritize faster, more reliable software releases. GitHub Copilot’s revenue jump to USD 400 million in 2025, a 248% year-on-year rise, illustrates how AI assistants have shifted from novelty to core productivity layer. Cloud deployment approaches now dominate both volume and growth curves, while integrated development environments (IDEs) retain the broadest installed base. End-user demand is highest in IT and telecom, yet retail and e-commerce are closing the gap as omnichannel commerce expands. Regional dynamics reveal North America’s scale advantage, but Asia-Pacific’s rapid digitization, new developer cohorts, and supportive public-sector policies make it the principal growth engine.

Key Report Takeaways

- By deployment mode, cloud-based tools held 59.10% software development tools market share in 2025 and are forecast to post a 31.2% CAGR through 2031.

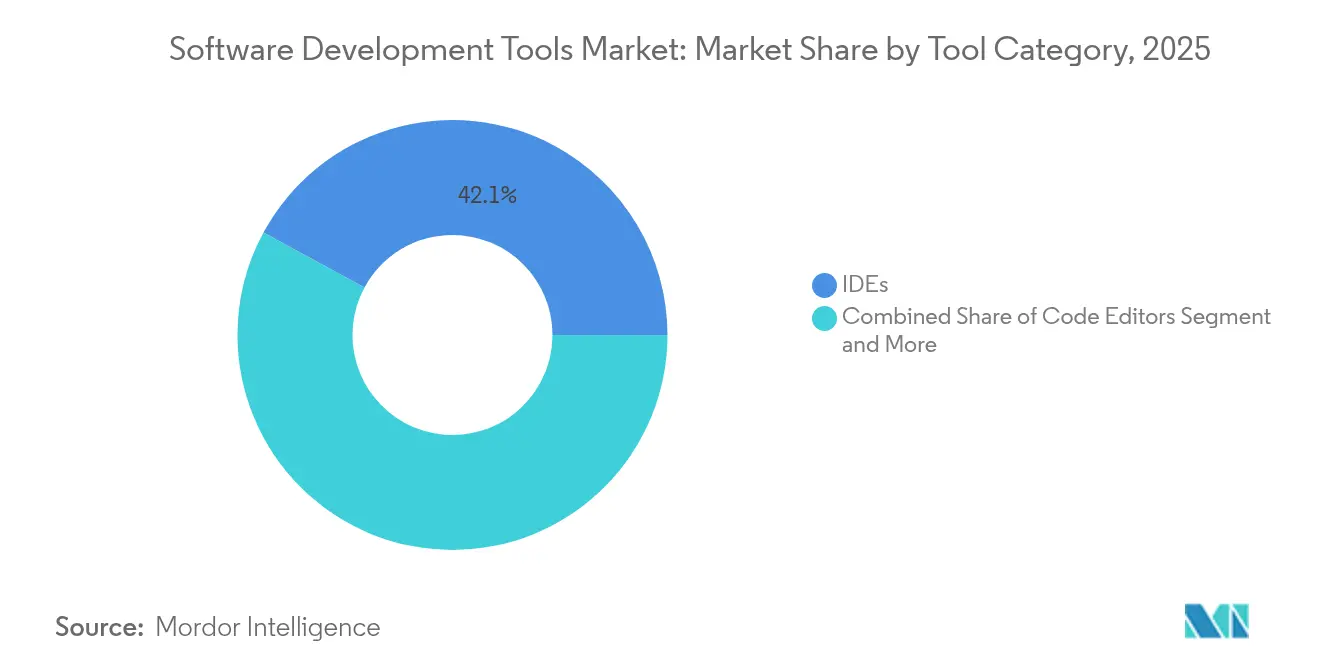

- By tool category, IDEs led with 42.10% revenue share in 2025, while code editors are projected to expand at 23.9% CAGR to 2031.

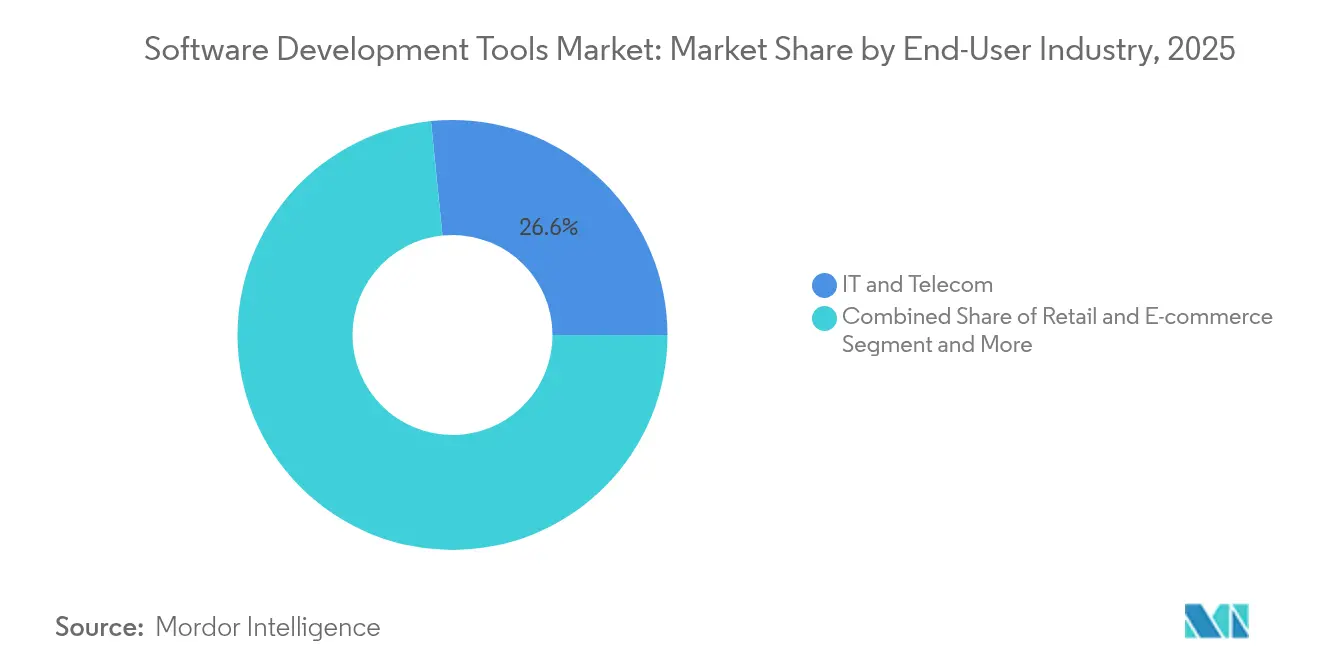

- By end-user industry, IT and telecom accounted for 26.60% of the software development tools market in 2025; retail and e-commerce is advancing at an 18.25% CAGR to 2031.

- By geography, North America captured 33.60% of revenue in 2025, whereas Asia-Pacific is set to grow at 20.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Software Development Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of cloud-native development | +4.2% | Global, with early gains in North America and EU | Medium term (2-4 years) |

| Proliferation of AI code assistants | +3.8% | North America and Asia-Pacific core, spill-over to EU | Short term (≤ 2 years) |

| DevOps and CI/CD culture mainstreaming | +2.9% | Global | Medium term (2-4 years) |

| Rise of low-code / no-code platforms | +2.1% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Developer-experience (DevEx) budgets surge | +1.7% | North America and EU | Short term (≤ 2 years) |

| Green software-engineering mandates | +1.3% | EU core, expanding to North America and Asia-Pacific | Long term (≥ 4 years) |

| Rapid adoption of cloud-native development | +4.2% | Global, with early gains in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of AI Code Assistants

More than 72% of engineers already rely on generative AI during daily workflows, and GitHub Copilot’s 2025 revenue underscores commercial acceptance. Enterprise pilots show 16% higher code throughput and improved developer satisfaction. Vendors are broadening model coverage—GitHub has added Anthropic Claude 3.5 Sonnet and Google Gemini 1.5 Pro—while JetBrains introduced its Junie AI agent. Productivity gains coexist with quality concerns because roughly one-third of AI output still contains exploitable flaws, driving demand for automated verification layers.[1]Black Duck, “Security Analysis of AI-Generated Code,” Black Duck, blackducksoftware.com Natural-language “vibe coding” marks a step toward democratized development, letting business users describe intent instead of writing syntax.

Rapid Adoption of Cloud-Native Development

Eighty-four percent of enterprises now run containers in production, and 78% use Kubernetes orchestration.[2]Docker, “2025 State of Containers Report,” Docker, docker.comOracle’s cloud-infrastructure revenue rose 27% to USD 6.7 billion in fiscal 2025, illustrating large-scale migration patterns. Serverless platforms remove infrastructure chores, while edge computing pushes code execution closer to data sources; analyst models expect 75% of enterprise data to reside at the edge by 2025. Together, these shifts elevate demand for observability, dependency management, and security solutions that can function across hybrid and distributed topologies.

DevOps and CI/CD Culture Mainstreaming

DevOps practices have transitioned from early-adopter status to enterprise norm. GitLab’s positioning as a leader in DevOps platforms signals a preference for unified pipelines that merge development, security, and operations. Yet developers juggle an average of 14 tools, prompting 62% of executives to prioritize consolidation. Platform engineering is emerging as the coping strategy; Gartner projects 80% adoption by 2026, and vendors are layering AI into pipelines to predict and remediate faults before code reaches production.

Rise of Low-Code / No-Code Platforms

Microsoft, Oracle, and Salesforce promote low-code suites that let citizen developers build internal apps quickly. AI integration further simplifies workflows through natural-language design and instant code scaffolding. Governance frameworks are becoming essential because uncontrolled low-code projects can introduce security and compliance gaps. Successful offerings blend tightly with professional-grade toolchains so that organizations avoid silos and maintain consistent architecture across custom and citizen-built software.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortage and rising developer salaries | -2.8% | Global, acute in North America and EU | Medium term (2-4 years) |

| Security vulnerabilities and IP-leakage risks | -2.1% | Global | Short term (≤ 2 years) |

| Toolchain sprawl and integration complexity | -1.9% | North America and EU core, expanding globally | Medium term (2-4 years) |

| Legal liability of AI-generated code | -1.4% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Talent Shortage and Rising Developer Salaries

The United States shows more than 918,000 unfilled IT roles, and a 1.2 million developer gap is expected by 2026. Worldwide, skilled-worker shortages could cost businesses USD 8.4 trillion in lost revenue by 2030. Wage inflation is especially sharp for AI and cybersecurity talent, squeezing startup budgets and slowing enterprise roadmaps. Only 13.2% of schools offer advanced computer-science coursework, perpetuating the skills deficit. Companies respond by expanding remote-first hiring, near-shore partnerships, and AI productivity tools to reduce reliance on scarce human capacity.

Security Vulnerabilities and IP-Leakage Risks

Roughly 40% of AI-generated code contains at least one vulnerability, and two-thirds of security leaders contemplate limiting or banning AI output.[3]TechRepublic, “Security leaders weigh risks of AI-generated code,” TechRepublic, techrepublic.com Flaw rates match human-written code, but velocity magnifies exposure. Legal uncertainties linger after class-action complaints against GitHub Copilot, raising fears around accidental copyright violations. Firms are adding AI-aware static analysis, multi-modal scanning, and policy-as-code frameworks to mitigate threats while preserving AI productivity benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tool Category: IDEs Dominate Despite Code-Editor Surge

IDEs captured 42.10% of 2025 revenue, reflecting enduring demand for single-window debugging, testing, and deployment environments. However, code editors are registering a 23.9% CAGR, bolstered by cloud synchronization and embedded AI pair-programmers. Market incumbents like JetBrains and Microsoft are weaving real-time code suggestions into flagship IDEs to hold users even as lighter editors reshape developer expectations. Version-control software and test-automation suites remain essential but grow more slowly, while AI-enabled code-review and security-scanning utilities drive incremental spending. A modular tool stack lets developers mix specialized components, and the resulting fragmentation opens niches for startups focused on workflow orchestration or metrics dashboards.

The trend toward plug-and-play tooling helps the software development tools market address diverse language ecosystems, microservices sprawl, and compliance mandates. Integration vendors now sell curated bundles that reduce context switching. Where IDE vendors once fought on feature breadth, they now compete on intelligence quality, extension ecosystems, and consumption flexibility (desktop, browser, or mobile). Consolidation is expected as platforms race to assemble end-to-end experiences, yet specialized point solutions with unique innovation cycles can still carve lucrative footholds.

By Deployment Mode: Cloud Acceleration Reshapes Infrastructure

Cloud deployment accounted for 59.10% revenue in 2025 and carries the fastest 31.2% CAGR, confirming that the software development tools market increasingly operates on elastic, usage-based pricing. Oracle’s multicloud services posted triple-digit growth rates, validating demand for database portability across hyperscale backbones. Hybrid and multi-cloud adoption let regulated industries retain sensitive workloads on-premises while exploiting cloud bursts for testing and analytics.

Edge and serverless paradigms blur definitions because workloads now spin up dynamically across clusters running from data centers to retail outlets or factory floors. Kubernetes gives teams a uniform control plane, yet its complexity elevates the value of managed services and turnkey DevOps stacks. Security and compliance certifications become competitive differentiators for platform vendors courting government and healthcare customers. As organizations rationalize tool portfolios, integrated cloud pipelines that embed CI/CD, security scanning, and observability gain share over isolated on-premises scripting engines.

By End-User Industry: IT Leads While Retail Accelerates

IT and telecom represented 26.60% of 2025 spending due to continual network-software upgrades and heavy automation investments. Banking, financial services, and insurance follow closely, where AI-assisted development drives 30–55% productivity gains during modernization cycles. Retail and e-commerce is the fastest riser at 18.25% CAGR because customer-facing applications must iterate weekly to align with real-time buying signals.

Healthcare and life-sciences teams are scaling digital-front-door applications and data-sharing platforms under strict privacy rules. Manufacturing relies on low-latency edge deployments to coordinate robotic cells and IoT sensors. Public-sector bodies modernize legacy mainframes to improve service delivery, yet procurement cycles remain lengthy. Collectively, diversified vertical momentum supports the long-run expansion of the software development tools market, while vertical-specific regulations shape vendor roadmaps and integration priorities.

Geography Analysis

North America held 33.60% revenue in 2025, home to the largest software vendor ecosystems and deepest venture funding pools. The region also faces the steepest skills shortage, prompting aggressive adoption of AI coding aids and offshore partnerships to maintain release velocity. Canada benefits from immigration pathways that funnel high-skilled talent into regional innovation hubs.

Asia-Pacific’s 20.85% CAGR rides expanding cloud footprints, government-funded upskilling programs, and a growing pool of venture-backed startups. India and Vietnam deliver cost-effective offshore capacity, while Japan and South Korea integrate software rigor into advanced manufacturing. The region diversifies language tooling and prefers SaaS delivery because many teams lack large on-premises budgets.

Europe advances at a steady clip, driven by GDPR, the proposed AI Act, and new carbon-footprint reporting that forces teams to measure software efficiency. Nordic countries are early adopters of green-software dashboards. Eastern Europe supplies competitive talent to near-shore projects despite geopolitical uncertainties. Middle East and Africa are nascent but accelerating as telecom operators and sovereign funds bankroll smart-city and fintech programs.

Together, these patterns reinforce the dispersed demand base that underpins long-term resilience for the software development tools market.

Competitive Landscape

Competition balances scale and specialization. Microsoft monetizes an integrated stack—Visual Studio Code, GitHub, Azure DevOps, and Copilot—generating more than USD 2 billion annually from GitHub alone. Oracle leverages a broad database customer base to upsell DevOps services, pushing fiscal 2025 revenue to USD 57.4 billion with 27% cloud-infrastructure growth. JetBrains retains a premium IDE niche with USD 593 million revenue in 2025 and is infusing AI into JetBrains Fleet and IntelliJ to defend share.

AI-native newcomers attract outsized valuations: Cursor AI closed a USD 900 million round at a USD 9.9 billion valuation in June 2025. HashiCorp’s USD 6.4 billion acquisition by IBM signals rising consolidation in infrastructure automation. Harness, CircleCI, and Atlassian compete on developer-experience metrics—setup time, incident recovery, and cognitive load—rather than raw feature counts.

Buyers increasingly prioritize platform breadth and frictionless integration because developers juggle double-digit tool counts. Vendors therefore bundle security scanning, observability, and project management into single subscriptions or pay-as-you-go tiers. AI governance and secure-coding add-ons differentiate offerings as enterprises weigh the risk of intellectual-property leakage. The resulting environment is moderately fragmented yet tilted toward ecosystems with large install footprints and rapid feature-release cadences.

Software Development Tools Industry Leaders

Microsoft Corporation

Amazon Web Services

JetBrains

Atlassian

GitHub

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cursor AI reached a USD 9.9 billion valuation after raising USD 900 million.

- May 2025: Microsoft launched a GitHub AI agent powered by Anthropic’s Claude 3.7 Sonnet, available to Copilot Pro+ and Enterprise customers.

- May 2025: OpenAI agreed to acquire Windsurf (formerly Codeium) for more than USD 3 billion, its largest deal to date.

- March 2025: AWS and GitLab introduced a joint AI bundle that merges GitLab Duo and Amazon Q to streamline code quality and release workflows.

Global Software Development Tools Market Report Scope

Software development tools encompass a range of programs and applications that assist developers in creating, testing, debugging, and maintaining software applications and systems. These tools facilitate a streamlined approach to the software development lifecycle, covering stages from planning and coding to deployment and maintenance.

The study tracks the revenue accrued through the sale of software development tools by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The software development tools market is segmented by type (integrated development environment (IDE), debugging tools, version control system (VCS), testing tools, project management tools), deployment mode (on-premises and cloud-based), end-user industry (it & telecom, banking, financial services & insurance (BFSI), healthcare, retail, manufacturing, and others), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| IDEs |

| Code Editors |

| Version Control Systems |

| Testing / QA Tools |

| Other Type |

| On-Premises |

| Cloud-based |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Manufacturing and Industrial |

| Media and Entertainment |

| Government and Public Sector |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN-5 | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Tool Category | IDEs | ||

| Code Editors | |||

| Version Control Systems | |||

| Testing / QA Tools | |||

| Other Type | |||

| By Deployment Mode | On-Premises | ||

| Cloud-based | |||

| By End-User Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Manufacturing and Industrial | |||

| Media and Entertainment | |||

| Government and Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| ASEAN-5 | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the software development tools market?

The software development tools market stands at USD 7.44 billion in 2026.

How fast is the software development tools market expected to grow?

The market is forecast to expand at a 16.12% CAGR, reaching USD 15.72 billion by 2031.

Which deployment mode is growing the fastest?

Cloud-based deployment leads with a 31.2% CAGR and already represents 59.10% of 2025 revenue.

Which geographic region shows the highest growth potential?

Asia-Pacific is projected to post the fastest regional growth at 20.85% CAGR through 2031.

What is the biggest restraint on market expansion?

A global developer talent shortage, projected to leave 1.2 million U.S. roles unfilled by 2026, is the most significant headwind.

Page last updated on: