Software As A Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

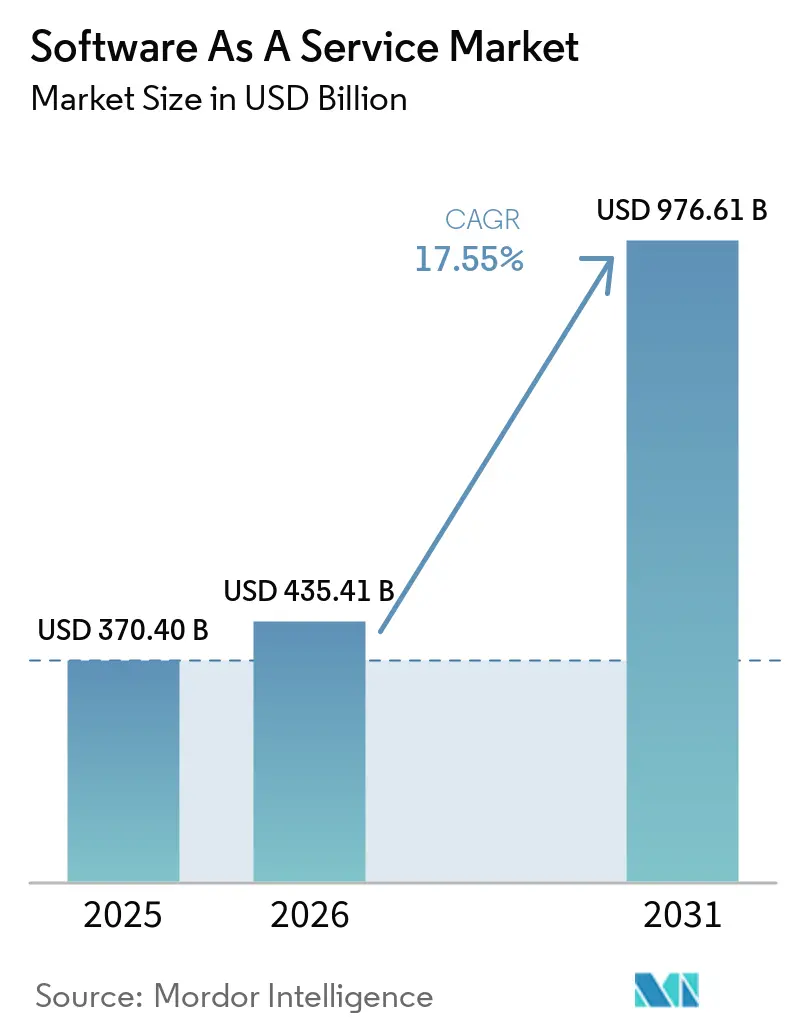

| Market Size (2026) | USD 435.41 Billion |

| Market Size (2031) | USD 976.61 Billion |

| Growth Rate (2026 - 2031) | 17.55% CAGR |

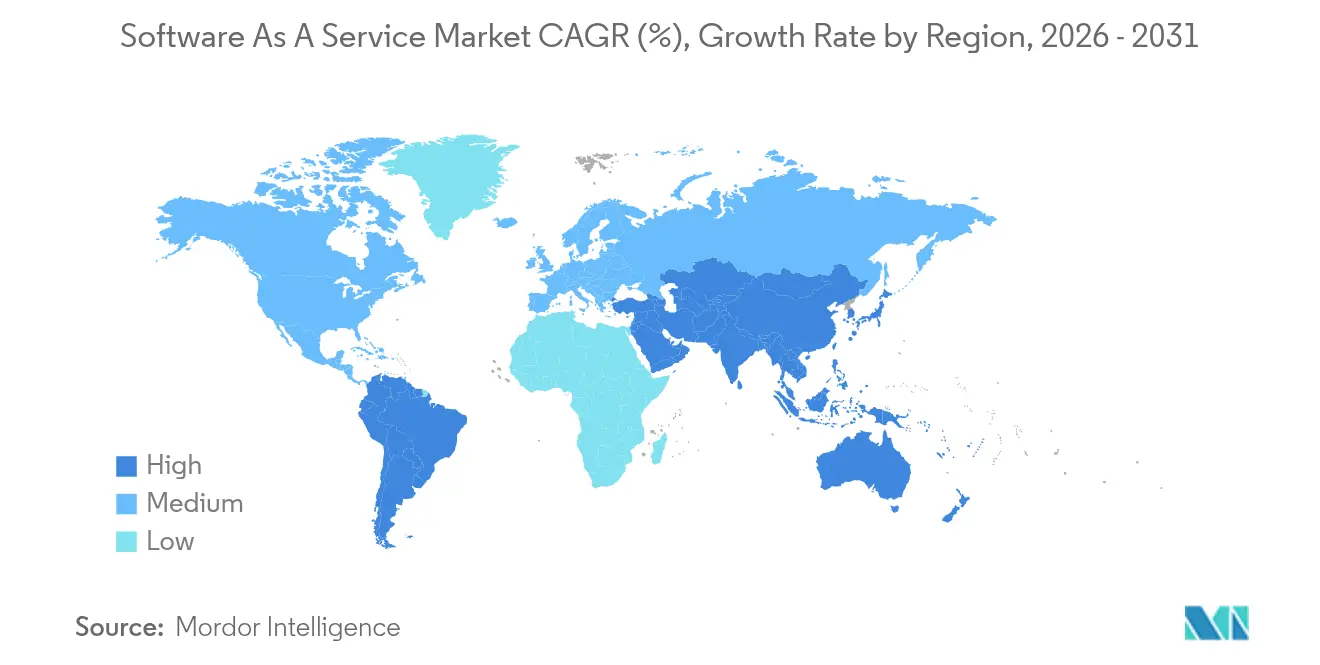

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software As A Service Market Analysis by Mordor Intelligence

The Software As A Service (SaaS) market size in 2026 is estimated at USD 435.41 billion, growing from the 2025 value of USD 370.4 billion, with 2031 projections showing USD 976.61 billion, growing at 17.55% CAGR over 2026-2031. This expansion is propelled by enterprise cloud migration, rapid AI integration, and the attractive economics of pay-as-you-go delivery. The dominance of public cloud models, the rise of usage-based pricing, and heightened security demands combine to enlarge the addressable SaaS market. Competitive intensity accelerates as platform vendors buy niche specialists to deepen functionality and lock in customers. Meanwhile, data-sovereignty mandates, vendor lock-in worries, and sustainability pressures temper growth but also open opportunities for hybrid and edge-ready offerings.

Key Report Takeaways

- By deployment model, public cloud held a 89.42% SaaS market share in 2025, while hybrid cloud is projected to expand at a 21.8% CAGR through 2031.

- By enterprise size, large enterprises accounted for 58.05% of the SaaS market size in 2025; small and medium enterprises (SMEs) represent the fastest-growing cohort at 19.2% CAGR.

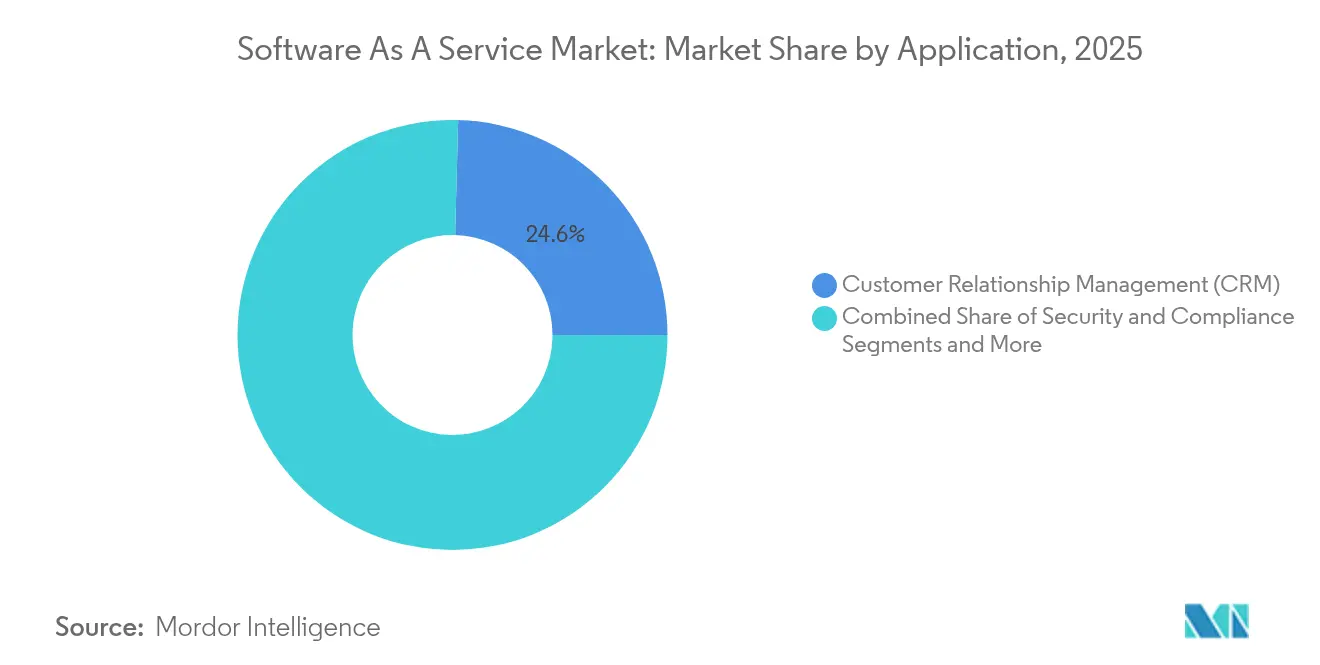

- By application, Customer Relationship Management captured 24.58% revenue share of the SaaS market in 2025; Security and Compliance applications are advancing at a 24.1% CAGR.

- By pricing model, subscription plans maintained 68.2% of the SaaS market in 2025, whereas usage-based models are rising at a 27.9% CAGR.

- By end-user vertical, IT and Telecom led with 22.45% share of the SaaS market size in 2025; Healthcare is the fastest-growing vertical at 22.9% CAGR.

- By geography, North America commanded 42.60% of the SaaS market in 2025; Asia-Pacific is projected to grow at a 18.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Software As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native architectures | +3.2% | Global North America and Europe lead | Medium term (2-4 years) |

| Rapid SME digitalization | +2.8% | APAC core Latin America follow-on | Short term (≤ 2 years) |

| Lower upfront costs vs. on-prem licensing | +2.1% | Global strongest in emerging markets | Long term (≥ 4 years) |

| Generative-AI-enabled revenue extensions | +4.5% | North America and Europe expanding to APAC | Medium term (2-4 years) |

| Edge-delivered ultra-low-latency SaaS | +1.8% | Global manufacturing and financial services focus | Long term (≥ 4 years) |

| Carbon-accounting compliance demand | +1.4% | Europe and North America spreading worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Cloud-Native Architectures

Cloud-native approaches replace monolithic software with containerized microservices orchestrated by Kubernetes, enabling continuous delivery and elastic scaling. Microsoft’s USD 42.4 billion Q3 FY2025 cloud revenue, up 20% year over year, underlines enterprise appetite for cloud-first rebuilding.[1]Microsoft Investor Relations, “FY2025 Q3 Earnings Release,” microsoft.com Freed from hardware constraints, companies spin up new environments in minutes, boosting developer velocity and service resilience. This architectural shift also fragments the SaaS market by lowering entry barriers for niche vendors that plug seamlessly into hyperscaler ecosystems. As multi-cloud tools mature, organizations diversify providers to avoid concentration risk while preserving best-of-breed innovation.

Rapid SME Digitalization

Post-pandemic, SMEs race to digitize front- and back-office functions to remain competitive. OECD research points to widening adoption gaps by size and sector, yet knowledge-intensive SMEs lead uptake.[2]OECD, “The Digital Transformation of SMEs,” oecd.org In China, SaaS spending hit CNY 58.1 billion in 2023, rising 23.1% despite macro softness. Budget-friendly SaaS subscriptions help SMEs bypass capital constraints, while AI-infused self-configuration trims onboarding effort. Vendors that bundle accounting, e-commerce, and marketing into unified dashboards gain traction as resource-strapped owners prioritize simplicity and ROI.

Lower Upfront Costs vs. On-Premises Licensing

Subscription models convert capex into opex and eliminate hardware refreshes. SAP delivered EUR 4.99 billion cloud revenue in Q1 2025, a 27% jump year on year, reflecting accelerated migrations from perpetual licenses.[3]SAP SE, “Q1 2025 Results,” sap.com Reduced maintenance overhead and automatic updates free IT teams to focus on higher-value tasks. Yet enterprises scrutinize lifetime spend, steering some mission-critical workloads to hybrid deployments where performance or sovereignty dictates local control.

Generative AI embeds predictive and creative functions directly inside SaaS workflows. Microsoft’s AI portfolio reached USD 13 billion annual run rate in Q2 FY2025, up 175% year on year. UnitedHealth runs 1,000 AI use cases spanning claims automation to care recommendations. High GPU costs spur usage-based pricing so customers pay only for compute consumed, realigning vendor economics and opening new monetization lanes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data sovereignty and compliance barriers | -2.3% | Europe regulates industries worldwide | Medium term (2-4 years) |

| Vendor lock-in and switching costs | -1.8% | Global acute for large enterprises | Long term (≥ 4 years) |

| FinOps scrutiny curbing SaaS sprawl | -1.5% | North America and Europe | Short term (≤ 2 years) |

| Green-cloud mandates are raising costs | -1.1% | Europe sustainability-centric firms elsewhere | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty and Compliance Barriers

GDPR and a wave of state-level privacy laws compel providers to localize data, appoint Data Protection Officers, and pass rigorous audits.[4]HeyData, “GDPR Compliance Steps for SaaS,” heydata.eu Compliance lifts costs and narrows hyperscaler location choices. Enterprises hedge by retaining sensitive workloads on-prem or in private clouds and selecting vendors with regional hosting frameworks.

Vendor Lock-in and Switching Costs

Extensive customizations, API integrations, and user retraining can trap organizations in long-term contracts. JPMorgan Chase’s USD 2 billion private-cloud build underscores efforts to keep exit options open. Hybrid strategies, open-source components, and container portability ease migration fears but seldom eliminate them.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Hybrid Models Drive Strategic Flexibility

Public cloud continues to dominate the SaaS market with 89.42% share in 2025. Hybrid configurations, though, are projected to grow at 21.8% CAGR as firms pursue regulatory compliance and latency-sensitive use cases. Discover Financial Services uses Red Hat OpenShift on AWS to manage seasonal demand spikes and move workloads freely, mitigating vendor lock-in risk. The SaaS market size for hybrid solutions is set to widen as edge nodes enable real-time analytics in manufacturing and finance.

Enterprises blend public, private, and edge resources to balance cost against control. IndiGo Airline migrated 80% of operations to a multicloud estate spanning Microsoft Azure and Google Cloud within 18 months. The SaaS market benefits from this diversity, encouraging vendors to ship container-ready versions that run consistently across environments.

By Enterprise Size: SME Growth Accelerates Digital Adoption

Large companies accounted for 58.05% of the SaaS market in 2025, attracted by unified suites that simplify global processes. Yet SMEs, forecast to expand at 19.2% CAGR, power the next growth wave. For this cohort the SaaS market size expands each year as subscription billing, guided onboarding, and AI-driven configuration remove technical barriers.

SMEs gravitate toward platforms offering accounting, sales, and HR in a single interface. OECD notes digital uptake remains uneven, prompting policy support for smaller firms. Vendors that invest in templates, partner ecosystems, and community learning lower the total cost of ownership and secure long-term loyalty.

By Application Type: Security Solutions Lead Growth Acceleration

CRM held the largest slice of the SaaS market size at 24.58% in 2025. Security and Compliance solutions are expanding 24.1% annually as ransomware incidents and evolving regulations keep CISOs on edge. Salesforce recorded USD 9.8 billion Q1 FY2026 revenue, underlining sustained CRM demand and the strategic USD 8 billion Informatica deal aimed at unifying data pipelines.

Security offerings span identity governance, SIEM, and automated incident response. As multi-cloud estates proliferate, integrated security stacks that cover endpoints to APIs become critical. Generative AI further raises the stakes by automating code and phishing attacks, making adaptive defense indispensable.

By Pricing Model: Usage-Based Models Gain AI-Driven Momentum

Subscription licenses retained 68.2% share in 2025. Nonetheless, usage-based plans are growing 27.9% per year, mirroring variable compute costs for AI workloads. The SaaS market adapts as tokens, API calls, and inference minutes replace seat counts.

Hybrid pricing blends predictable base fees with metered overages to accommodate spikes. Vendors refine telemetry to bill accurately while giving buyers visibility into unit economics, a prerequisite for FinOps teams focused on SaaS sprawl containment.

By End-User Vertical: Healthcare Drives Transformation Acceleration

IT and Telecom contributed 22.45% revenue in 2025, but Healthcare, at 22.9% CAGR, is the fastest climber. Moderna adopted ChatGPT Enterprise across its entire workforce and created 750 custom GPTs to expedite trials. HIPAA and FDA regulations drive demand for secure, auditable SaaS platforms.

Manufacturing, retail, and BFSI also deepen reliance on SaaS. Siemens automated 90% of delivery-note processing, saving EUR 5 million yearly. Vertical solutions that embed domain workflows outperform horizontal tools by shortening time-to-value.

Geography Analysis

North America held 42.60% of the SaaS market in 2025, benefitting from dense cloud infrastructure, robust cybersecurity standards, and capital access. Coca-Cola’s USD 1.1 billion expansion of its Microsoft partnership illustrates enterprise-scale adoption of multi-cloud SaaS strategies. Regulatory fragmentation among US states does raise compliance overhead, but vendors respond with configurable privacy modules and regionally replicated data stores.

Asia-Pacific is projected to grow 18.7% annually to 2031, becoming the epicenter of SaaS market expansion. Rising internet penetration, mobile-first consumption, and government digitization programs drive adoption. China recorded CNY 58.1 billion SaaS sales in 2023 with 23.1% growth, underscoring untapped demand across manufacturing and consumer services. Local hyperscalers battle global incumbents by offering language-localized UI and region-specific compliance features.

Europe posts steady yet compliance-centric growth. GDPR and country-level data-protection acts compel vendors to maintain regional datacenters and invest in encryption innovations. Sustainability goals also influence procurement, with enterprises evaluating provider carbon footprints and requiring green-cloud disclosures. Vendors that certify renewable-powered facilities and transparent reporting gain competitive advantage.

Mordor Intelligence provides coverage of the software as a service market across other key regional markets. Detailed country-level analysis extends to Denmark incorporating local coverage and market participation, as required.

Competitive Landscape

Consolidation defines the modern SaaS market as incumbents buy capabilities rather than build from scratch. Salesforce’s USD 8 billion Informatica and USD 1.9 billion Own deals extend its footprint into data management and backup. Vista Equity Partners acquired Acumatica for USD 2 billion, signaling private-equity confidence in vertical ERP niches.

AI capability is the new battleground. Microsoft leverages Azure to bundle compute, models, and developer tools, while SAP bought WalkMe for USD 1.5 billion to enhance user adoption. Emerging vendors differentiate through specialized LLMs, edge deployment, or compliance automation.

Partnership ecosystems expand as ISVs embed within hyperscaler marketplaces for co-sell opportunities. Vendors sharpen FinOps dashboards to expose per-feature usage and justify renewals. Competitive factors increasingly revolve around AI performance, integration breadth, security posture, and transparent pricing rather than core functionality, which has become table stakes.

Software As A Service Industry Leaders

Microsoft Corporation

Salesforce Inc.

Oracle Corporation

SAP SA

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Salesforce completed its USD 8 billion acquisition of Informatica to deepen data-cloud capabilities .

- May 2025: Vista Equity Partners finalized a USD 2 billion purchase of Acumatica, highlighting ERP growth potential.

- September 2024: Salesforce agreed to acquire Own for USD 1.9 billion, adding SaaS data protection.

- June 2024: SAP completed its USD 1.5 billion WalkMe acquisition.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the software-as-a-service market as all commercial application software that is delivered over the internet on a pay-as-you-go or subscription basis and that runs on public, private, or hybrid clouds. Revenues include license, support, and automatic update charges credited to vendors that market such cloud editions.

Scope Exclusions: Platform-as-a-service, infrastructure-as-a-service, on-premise perpetual licenses, and separate implementation consulting fees are not counted.

Segmentation Overview

- By Deployment

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Enterprise Size

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

- By Application Type

- Customer Relationship Management (CRM)

- Enterprise Resource Planning (ERP)

- Human Capital Management (HCM/HRM)

- Collaboration and Productivity

- Business Intelligence and Analytics

- Security and Compliance

- Other Applications

- By Pricing Model

- Subscription-Based

- Usage-Based / Pay-As-You-Go

- Freemium and Tiered

- By End-User Vertical

- IT and Telecom

- Banking, Financial Services and Insurance (BFSI)

- Retail and E-Commerce

- Healthcare and Life Sciences

- Manufacturing

- Other Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interview CIOs, finance heads, cloud resellers, and data-center operators across North America, Europe, and Asia-Pacific. Conversations and short surveys clarify live seat counts, renewal behavior, regional price dispersion, and emerging demand triggers, allowing us to balance the desk findings.

Desk Research

We gather baseline figures from respected public sources such as the United States Census ICT surveys, Eurostat Digital Economy datasets, OECD ICT indicators, and national telecom regulators, which reveal cloud adoption and software spend splits. These are blended with vendor subscription disclosures in SEC and equivalent filings, technology adoption reports from the Cloud Native Computing Foundation and similar associations, and news coverage archived in Dow Jones Factiva. D&B Hoovers supplies revenue brackets for privately held providers. The sources listed are illustrative; many additional governmental, trade, and academic records inform the desk phase.

Market-Sizing & Forecasting

A top-down build starts with total enterprise software and public-cloud outlays, then applies observed SaaS penetration ratios by company size and industry before multiplying by verified average subscription prices. Selective bottom-up vendor roll-ups and channel checks validate country totals. Key model inputs include broadband quality, remote-work intensity, SME cloud-first policy prevalence, price-per-user drift, and churn-to-expansion trends. Five-year forecasts employ multivariate regression enriched by scenario analysis agreed with industry experts to reflect regulatory or technological shocks.

Data Validation & Update Cycle

We run anomaly screens against quarterly vendor releases and macro time-series, escalate outliers for peer review, and refresh every twelve months, with interim updates triggered by material events such as mega acquisitions or sudden policy shifts.

Why Mordor's Software As A Service Baseline Commands Reliability

Published SaaS estimates vary because providers differ in scope picks, price weights, and refresh cadence. The table highlights the main divergence drivers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 370.4 B | Mordor Intelligence | |

| USD 315.7 B | Global Consultancy A | Omits freemium and usage-billed tiers; relies on 2023 survey weights |

| USD 464.8 B | Industry Association B | Adds managed services and cloud support revenue to SaaS totals |

| USD 241.8 B (2024) | Trade Journal C | Uses older base year and static price assumptions |

The comparison shows that, by adopting a clear scope, multi-variable model, and annual refresh, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can reproduce with confidence.

Key Questions Answered in the Report

What is the current size of the SaaS market?

The SaaS market was valued at USD 435.41 billion in 2026.

How fast will the SaaS market grow by 2031?

It is projected to reach USD 976.61 billion by 2031, reflecting a 17.55% CAGR during 2026-2031.

Which region leads the SaaS market?

North America leads with 42.60% share in 2025, while Asia-Pacific is the fastest-growing at a 18.7% CAGR.

What deployment model is growing fastest?

Hybrid cloud SaaS is expanding at a 21.8% CAGR as firms balance control and elasticity.

Why are usage-based pricing models gaining popularity?

AI workloads have variable compute demands, so metered pricing aligns customer cost with resource consumption.

Which vertical will grow fastest in SaaS adoption?

Healthcare is set to expand at a 22.9% CAGR as digital health and compliance needs accelerate software spending.

Page last updated on: