Software Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

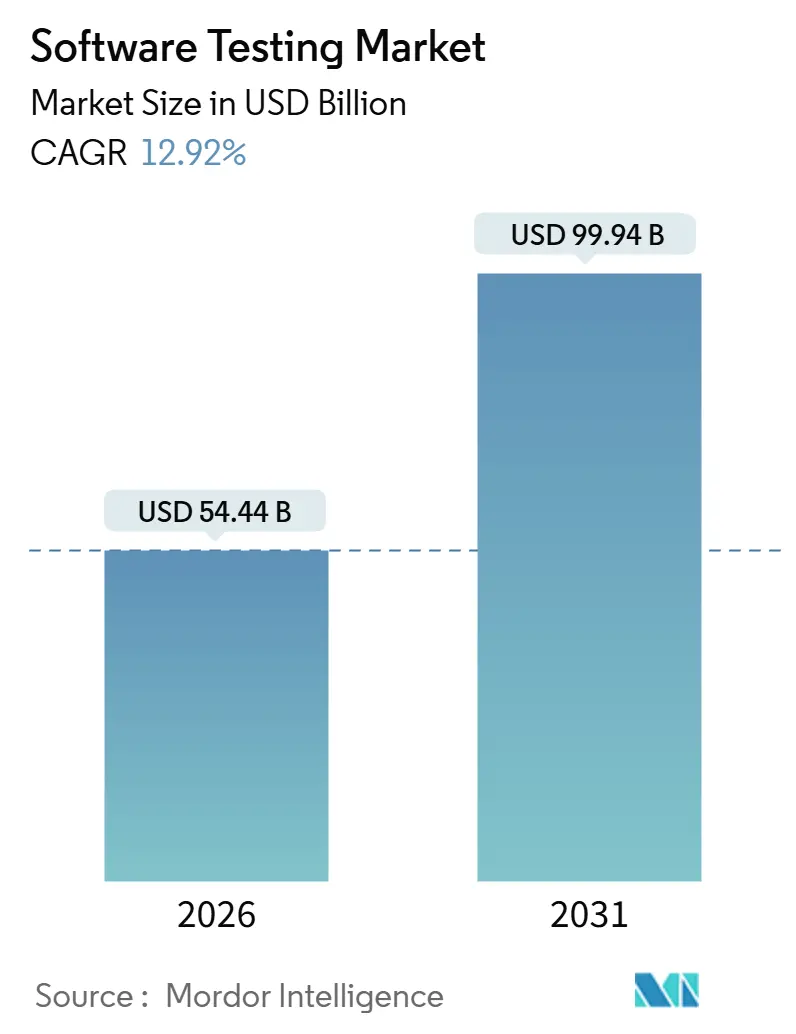

| Market Size (2026) | USD 54.44 Billion |

| Market Size (2031) | USD 99.94 Billion |

| Growth Rate (2026 - 2031) | 12.92% CAGR |

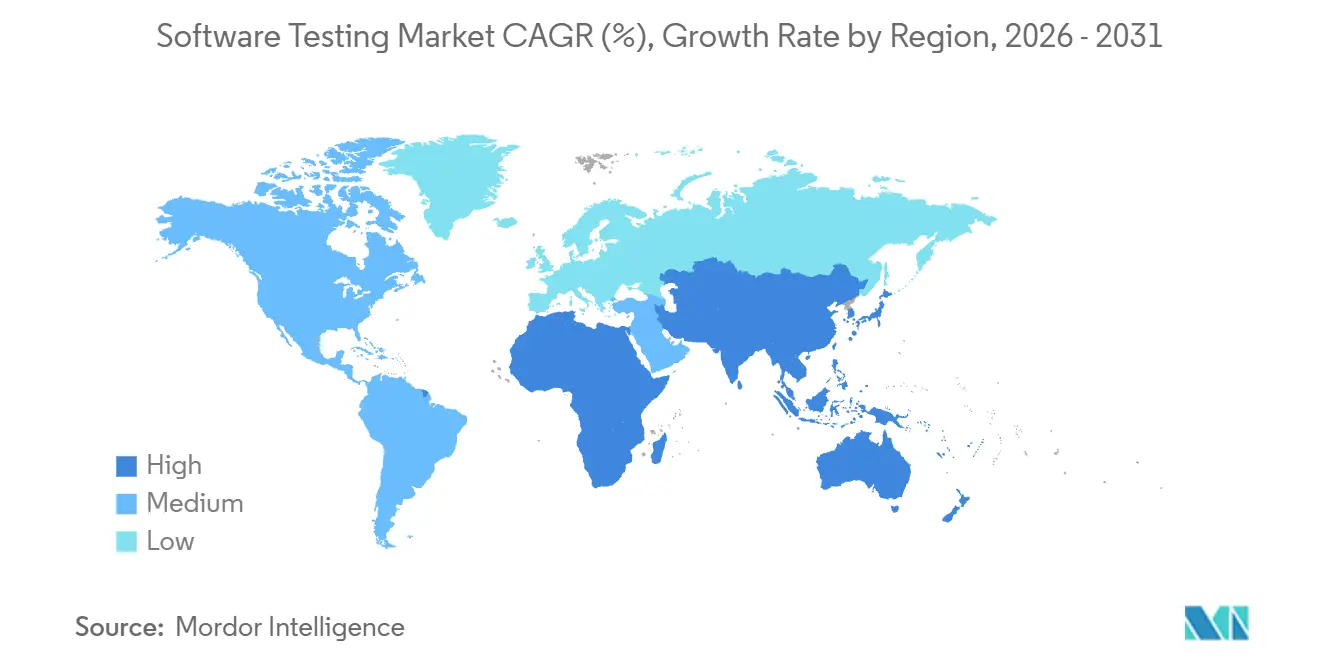

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

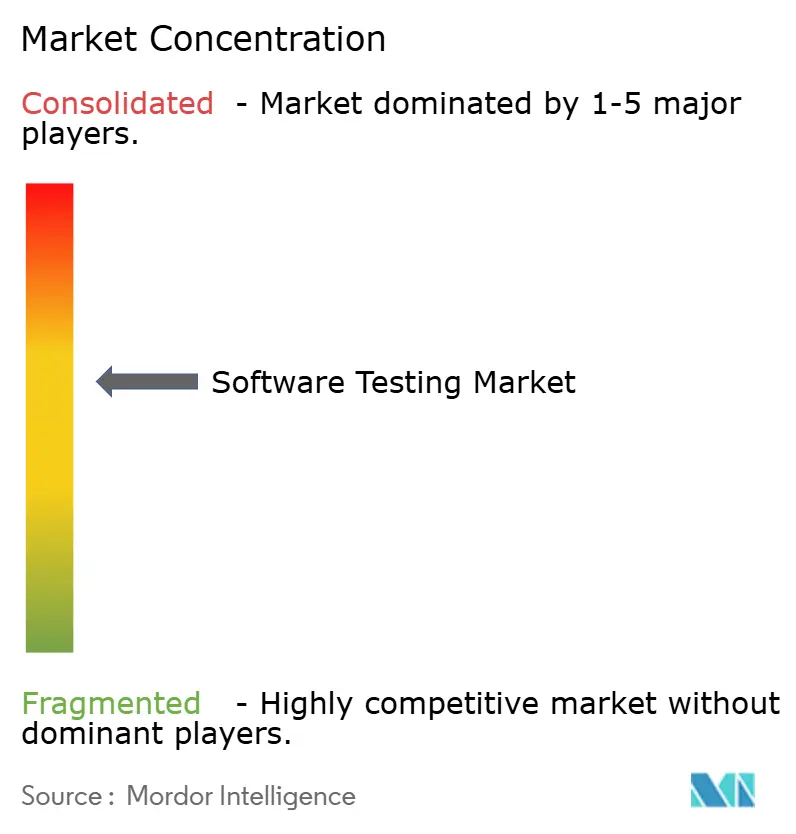

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software Testing Market Analysis by Mordor Intelligence

The software testing market size reached USD 54.44 billion in 2026 and is projected to climb to USD 99.94 billion by 2031, advancing at a 12.92% CAGR throughout the forecast period. Growth is tied to enterprises embedding quality gates directly into continuous integration and continuous deployment pipelines, shifting quality assurance from a post-release checkpoint to an always-on engineering practice. Widespread uptake of AI-augmented automation, rising cloud migration, and the expansion of Testing-as-a-Service models are lowering cycle times while broadening access to elastic test infrastructure. Demand is further energized by sector-specific compliance pressures, including IEC 62304 traceability in life sciences and open-banking API mandates in financial services, that require continuous validation of security and performance. At the same time, a persistent shortage of engineers versed in chaos engineering and AI model validation is inflating salary premiums in North America and Western Europe, raising execution risk for large transformation programs.

Key Report Takeaways

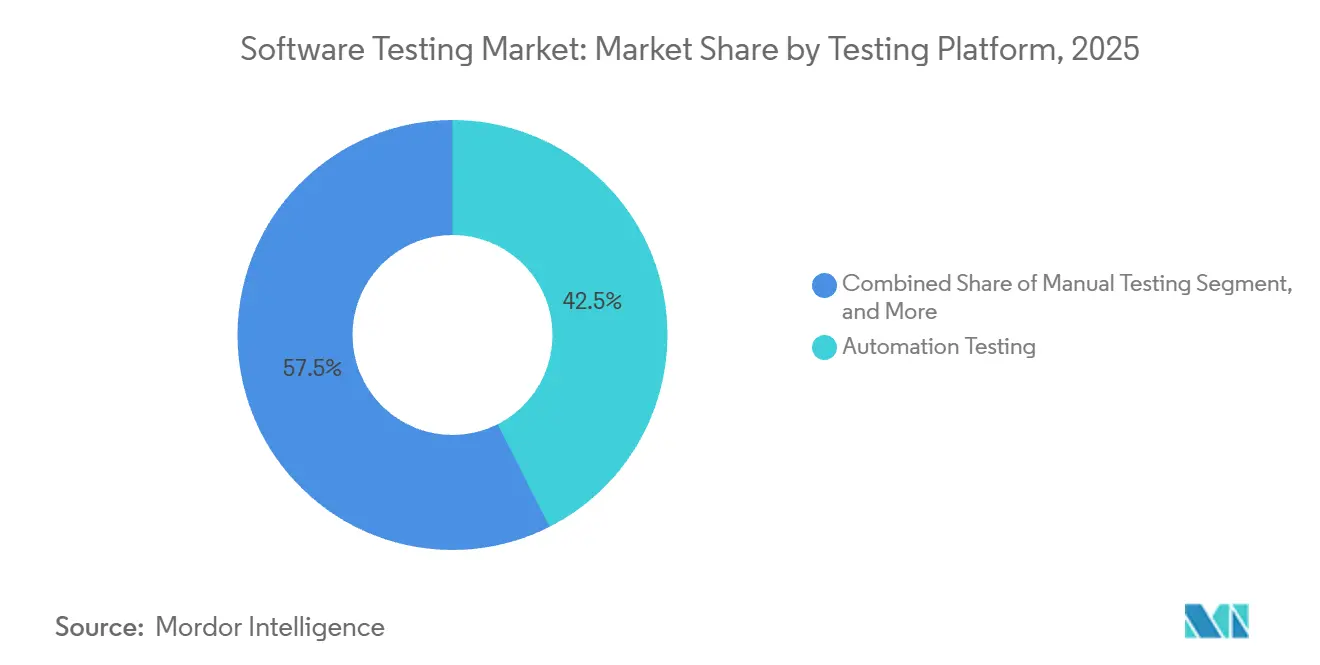

- By testing platform, automation testing held 42.53% of software testing market share in 2025, while AI-augmented and autonomous testing platforms are set to expand at a 13.16% CAGR to 2031.

- By testing type, functional and system testing accounted for a 50.13% slice of the software testing market size in 2025, whereas security and penetration testing is on track to grow at 14.83% through 2031.

- By deployment model, on-premises installations accounted for 54.63% of revenue in 2025, yet cloud-based testing is forecast to register a 14.13% CAGR over the same horizon.

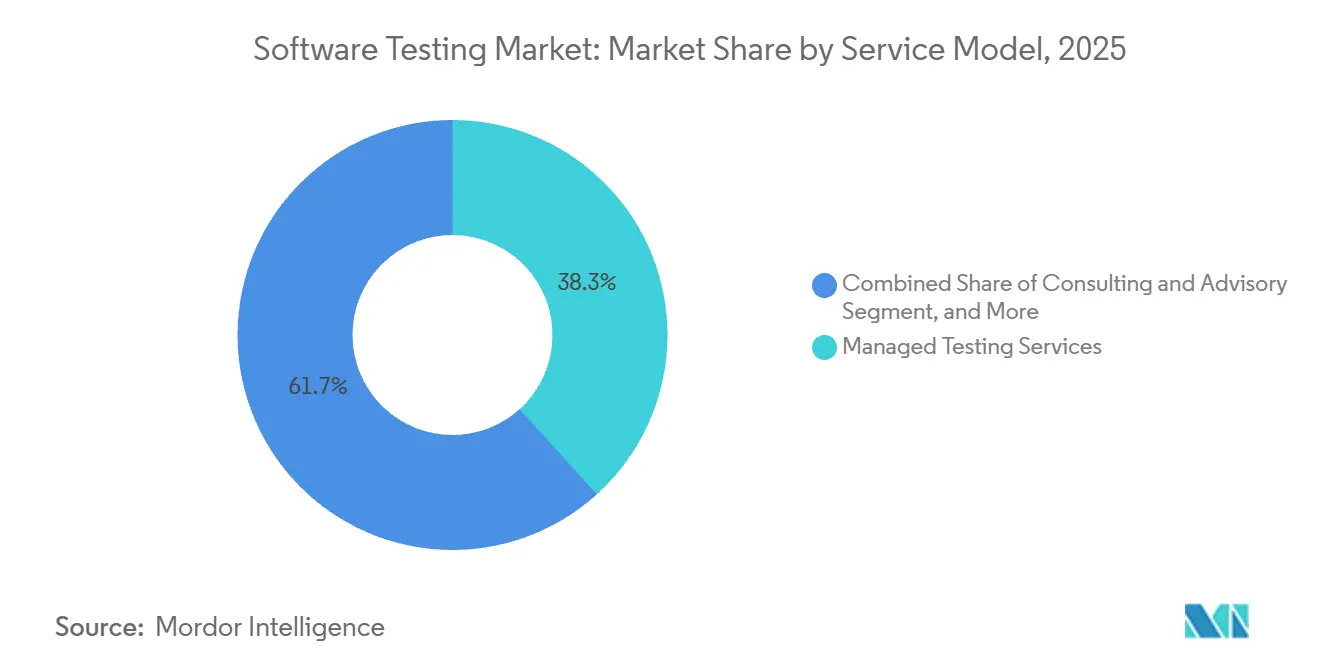

- By service model, managed testing services captured 38.29% of 2025 spending, but Testing-as-a-Service is projected to accelerate at 15.09% as pay-per-test-cycle pricing gains favor.

- By end-user industry, banking, financial services, and insurance represented 26.41% of demand in 2025, whereas healthcare and life sciences is expected to advance at 13.56% to 2031.

- By geography, North America accounted for 36.63% revenue in the software testing market in 2025; Asia-Pacific records the highest regional CAGR at 13.46% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Software Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise digital-first and DevOps adoption | +3.2% | Global with North America and Europe leading | Medium term (2-4 years) |

| Rising mobile and IoT application volumes | +2.8% | Asia-Pacific core with global spill-over | Long term (≥ 4 years) |

| Accelerated uptake of test-automation and AI | +4.1% | Global and concentrated in developed markets | Short term (≤ 2 years) |

| Cloud migration boosting TaaS | +2.5% | Global with regulatory variations in the EU | Medium term (2-4 years) |

| AI safety and ethics compliance mandates | +1.8% | North America and the EU | Long term (≥ 4 years) |

| Sustainability-linked green QA demand | +0.9% | Europe leading and expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Digital-First and DevOps Adoption

Organizations practicing DevOps recorded 208-fold higher deployment frequency and 106-fold faster lead times in 2024, compressing the window available for manual exploratory testing. Continuous quality gates inside GitLab, Jenkins, and Azure DevOps pipelines now validate every commit within minutes, forcing QA teams to modernize regression suites and integrate service-mesh observability. Financial institutions decomposing monoliths into hundreds of microservices are generating exponential growth in API contract tests, overwhelming legacy test-management tools. The resulting expansion of automated coverage elevates demand for engineers skilled in infrastructure-as-code, distributed tracing, and zero-downtime deployment validation. Over the medium term, this driver will sustain double-digit adoption of AI-assisted test orchestration across North America and Europe.

Rising Mobile and IoT Application Volumes

Global mobile-app downloads surpassed 255 billion in 2024, while connected IoT endpoints topped 16 billion units, multiplying device-OS-network permutations that must be validated. Automotive OEMs simulating intermittent 4G connectivity, healthcare wearables transmitting real-time biometrics under FCC guidelines, and industrial plants integrating edge sensors all require specialized test labs equipped with RF chambers and protocol analyzers. Asia Pacific drives much of the device volume, with India and China anchoring demand for large-scale test automation that covers regional network conditions. Given the long replacement cycle of embedded devices, the resulting test burden will continue into the next decade, contributing a long-term uplift to the software testing market.

Accelerated Uptake of Test-Automation and AI-Driven QA

AI-augmented platforms that analyze production logs and natural-language requirements now build regression suites in hours rather than weeks. Tricentis customers achieved 68% faster suite creation after adopting its AI-based module in 2025.[1]Tricentis, “Vision AI Module Launch for UI Testing,” tricentis.com Self-healing locators cut maintenance effort by 30-40%, freeing engineers for higher-value exploratory activities. North American enterprises are leading early deployments, while India’s global capability centers operationalize these tools at scale for multinational clients. Over the short term, rapid ROI from cycle-time reduction and script maintenance savings is expected to lift global adoption, with platform vendors racing to embed explainable-AI dashboards that mitigate false positives.

Cloud Migration Boosting Testing-as-a-Service

Clients shifting workloads to Amazon Web Services, Microsoft Azure, and Google Cloud Platform increasingly provision ephemeral test beds on demand, avoiding capital outlays for device farms. Capgemini reported 22% year-over-year growth in Testing-as-a-Service engagements in 2025. Cloud-native TaaS offerings integrate with infrastructure-as-code templates, enabling QA teams to spin up Kubernetes clusters, seeded data, and mock services in under 10 minutes. While cross-region data-transfer fees can inflate spend, most enterprises still realize net savings relative to idle on-premise infrastructure. Over the medium term, broad cloud migration and consumption-based budgeting will keep this driver firmly positive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global shortage of skilled QA engineers | -2.1% | Global and acute in North America and Europe | Short term (≤ 2 years) |

| Free/open-source frameworks squeeze margins | -1.8% | Global, impacting service providers | Medium term (2-4 years) |

| Low-code/no-code platforms limit manual QA | -1.3% | Global and focused in developed markets | Medium term (2-4 years) |

| Data-sovereignty rules hamper cloud QA | -0.9% | Europe primarily with growing adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Shortage of Skilled QA Engineers

Median time-to-fill senior automation roles exceeded 90 days in North America during 2025, as demand for Kubernetes-native testing and AI model validation outstripped supply. Salaries for professionals certified in Tricentis Tosca, ReadyAPI, and Sauce Labs commanded 18-25% premiums. High attrition in India and Eastern Europe, where hyperscalers and fintechs woo talent with remote-work flexibility, compounds the issue. The shortage forces service providers to fund lengthy upskilling programs and delays the ramp-up of complex engagements, trimming near-term market growth.

Free and Open-Source Frameworks Squeezing Service Margins

Seventy-three percent of enterprises used at least one open-source testing framework in production during 2024.[2]Linux Foundation, “Open Source Testing Framework Survey 2024,” linuxfoundation.org Selenium, Appium, and Playwright have commoditized browser and mobile automation, enabling in-house teams to sidestep commercial licensing fees. Service vendors now differentiate through consulting, CI/CD integration, and analytics rather than tool resale, eroding traditional revenue streams. Margin compression is most acute in Asia Pacific and Latin America, where cost sensitivities drive rapid adoption of free tooling, posing a medium-term drag on the software testing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Testing Platform: AI Reshapes Automation Economics

Automation testing held a 42.53% software testing market share in 2025 as enterprises relied on Selenium-based suites and proprietary tools, underlining its centrality to release management. The share will gradually cede ground to AI-augmented and autonomous platforms that are forecast to grow at a 13.16% CAGR, reflecting demand for self-healing locators and generative test-case design. Market leaders such as Tricentis report 68% faster suite creation after adopting AI-driven modules, a direct boost to productivity. Manual testing continues to play a critical role in usability, accessibility, and subjective user-experience checks, especially in consumer apps where human judgment remains indispensable.

Over the next five years, autonomous frameworks that combine AI-powered generation with low-code authoring will expand access to automation for business analysts. This democratization shifts hiring profiles away from pure coders toward domain experts skilled in prompt engineering. Vendors are layering explainability features to address false-positive risk, a key consideration for regulated sectors. As these capabilities mature, their contribution to overall software testing market expansion will intensify, particularly among digitally native enterprises that prioritize weekly or daily releases.

By Testing Type: Security Vaults Ahead

Functional and system testing commanded half of overall revenue in 2025, underscoring the need to validate core business logic across omnichannel workflows. However, security and penetration testing is projected to be the fastest moving category at 14.83%, lifted by zero-trust architectures that demand continuous vulnerability scanning of APIs, microservices, and container layers. Open-banking mandates require OAuth token validation and SQL injection checks for each new partner integration, while FDA cybersecurity guidance is triggering encryption and threat-modeling tests in medical-device submissions.

The convergence of functional, security, and performance checks within DevSecOps pipelines is accelerating test frequency. Static and dynamic security tools now run in parallel with unit and regression suites, surfacing defects earlier and reducing post-release incident costs. Performance testing, though mature, still anchors e-commerce and media workflows that face extreme seasonal peaks. Unit and integration coverage continues to rise through test-driven development, aided by AI models that analyze commit graphs to prioritize relevant regression cases.

By Deployment Model: Cloud Gains Despite Data-Sovereignty Friction

On-premise deployments accounted for 54.63% of 2025 revenue, reflecting historical investments in device farms and air-gapped environments for defense and regulated finance. Cloud-based testing is expected to grow at 14.13% annually as agile teams favor elastic capacity that scales with sprint velocity. Early adopters spin up Kubernetes clusters, seed data, and service mocks in minutes, improving throughput and lowering total cost of ownership.

Yet data-sovereignty rules under GDPR, China’s localization mandates, and India’s Digital Personal Data Protection Act impose in-region storage requirements, complicating global QA delivery. Many enterprises therefore settle on hybrid architectures that keep sensitive datasets on-premise while offloading compute-intensive load tests to the cloud. Cost-conscious teams also juggle workloads across multiple hyperscalers to optimize pricing and reduce cross-region latency.

By Service Model: TaaS Disrupts Managed-Services Incumbents

Managed testing services retained a 38.29% stake in 2025 as long-term engagements bundled test strategy, automation framework development, and defect triage under fixed retainer contracts. Testing-as-a-Service, however, is forecast to post a 15.09% CAGR, propelled by consumption-based pricing that charges per test cycle or device hour. Platforms such as Sauce Labs and BrowserStack expose self-service portals enabling developers to trigger thousands of cross-browser runs without expanding headcount.

This shift forces incumbents to unbundle offerings, separating infrastructure from advisory work and fueling a marketplace of best-of-breed modules. Crowdsourced testing, which leverages global communities to validate localization and real-world network conditions, is gaining popularity for consumer apps. Training services that upskill manual testers into automation and DevOps specialists are also expanding, reflecting the broader talent shortfall discussed earlier.

By End-User Industry: Healthcare Accelerates on Regulatory Tailwinds

Banking, financial services, and insurance delivered 26.41% of 2025 demand, driven by real-time payment rails and open-banking ecosystems that require sub-second latency and PCI-DSS compliance. Healthcare and life sciences is projected to expand 13.56% annually, powered by FDA-mandated cybersecurity reviews and IEC 62304 traceability for software-as-a-medical-device filings.

Telecom operators validating 5G network slicing, manufacturers adopting industrial IoT sensors, and retailers preparing for Black Friday traffic all require specialized testing rigs, reinforcing the breadth of domain-specific needs. Government agencies migrating to cloud platforms must meet FedRAMP and NIST controls, adding a security overlay to functional validation. Collectively, these sector dynamics broaden the software testing market by introducing unique compliance-driven workloads that cannot be deferred.

Geography Analysis

North America generated 36.63% of 2025 revenue, supported by hyperscale cloud providers and financial institutions re-platforming to distributed ledgers, which require exhaustive API contract validation. U.S. startups such as Mabl and Testim.io are leading global innovation in self-healing test frameworks, while Canada’s banks are piloting quantum-safe encryption tests. Mexico’s nearshoring boom attracts Indian vendors, easing time-zone alignment for U.S. clients constrained by visa caps.

Asia Pacific is poised for the fastest expansion at 13.46% through 2031, led by India’s global capability centers that exported more than USD 8 billion in testing services during FY 2024-25.[3]National Association of Software and Service Companies, “India IT Services Exports FY 2024-25,” nasscom.in China’s semiconductor firms validate embedded code against ISO 26262 automotive safety standards, and Japan’s manufacturers fold QA into digital twin simulations to minimize factory downtime. Australia and New Zealand rely on cloud-based test grids to overcome geographic distance, underscoring the region’s appetite for TaaS.

Europe’s landscape is shaped by GDPR and the upcoming EU AI Act, which require audit trails of training data and model validation. Germany’s automotive industry tests autonomous-driving software against UN Regulation 155 cybersecurity rules, while the United Kingdom validates open-banking APIs mandated by the Competition and Markets Authority. Sovereign-cloud requirements in France, Italy, and Spain are fragmenting once-centralized offshore delivery, prompting vendors to build in-region facilities. Elsewhere, Brazil’s banking modernization and Saudi Arabia’s Vision 2030 digitization plans fuel localized performance testing, although Africa’s market remains nascent, driven mainly by mobile-money platform validation.

Competitive Landscape

The top 10 vendors collectively control roughly 35-40% of global revenue, indicating moderate fragmentation. Indian IT services majors Tata Consultancy Services, Infosys, Wipro, and Tech Mahindra blend labor arbitrage with proprietary accelerators to secure multi-year deals, whereas global integrators such as Accenture, Capgemini, and Cognizant wrap QA inside broader cloud and data programs. Specialized firms including Cigniti Technologies, Qualitest, and EPAM Systems differentiate via domain-specific libraries that accelerate compliance for healthcare, telecom, and retail clients.

AI-augmented platforms are leveling the playing field by reducing dependence on large offshore headcounts. Tricentis has patented techniques for AI-based test-case prioritization and self-healing locators, signaling that proprietary algorithms will be a key moat as commoditized open-source frameworks erode traditional tool revenue. Open-source adoption simultaneously pressures service margins, pushing vendors toward outcome-based contracts tied to defect-escape rates and mean time to resolution.

Talent scarcity remains a decisive factor. High-demand skills such as Kubernetes-native test orchestration, API contract validation, and AI model explainability command premium compensation, especially in North America and Western Europe. Vendors that invest aggressively in training and career pathways can shorten project ramp-up times, reduce attrition, and capture higher-value outcome-based engagements, reinforcing the market’s dynamic competitive equilibrium.

Software Testing Industry Leaders

Accenture plc

Tata Consultancy Services Ltd.

Cognizant Technology Solutions Corp.

Capgemini SE

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sauce Labs introduced a visual-testing add-on for its Continuous Testing Cloud that compares UI screenshots across browser versions, cutting visual defect detection time by 40%.

- October 2025: Capgemini completed its acquisition of WNS Global Services’ travel and leisure business-process unit, integrating QA for airline reservation and hospitality platforms into its portfolio.

- September 2025: Cognizant launched an AI-powered test analytics dashboard that surfaces defect clustering and root-cause patterns across CI pipelines, claiming 30% faster triage for pilot customers.

- August 2025: Tricentis secured a USD 1.33 billion valuation after a growth-equity investment led by GTCR, earmarked for scaling AI-augmented test-generation capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global software testing market as all fee-based validation, verification, and quality-assurance activities performed on software code or cloud services across the lifecycle, including manual, automated, and AI-assisted test execution delivered through on-premise, cloud, or hybrid models to end-user enterprises. Revenue from pure-play service providers, integrated IT service arms, and testing-as-a-service platforms is counted once at the point of contract billing by Mordor Intelligence.

Scope exclusion: Pure hardware burn-in, silicon wafer probing, and embedded board certification tasks lie outside this study.

Segmentation Overview

- By Testing Platform

- Manual Testing

- Automation Testing

- AI-Augmented / Autonomous Testing

- By Testing Type

- Unit Testing

- Functional / System Testing

- Integration Testing

- Performance / Load Testing

- Security / Pen-Testing

- Regression and Other Testing

- By Deployment Model

- On-Premise

- Cloud-Based

- Hybrid

- By Service Model

- Consulting and Advisory

- Managed Testing Services

- Testing-as-a-Service (TaaS)

- Crowdsourced Testing

- Training and Certification

- By End-User Industry

- BFSI

- IT and Telecom

- Healthcare and Life Sciences

- Manufacturing

- Retail and E-Commerce

- Government and Public Sector

- Media and Entertainment

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We validate secondary findings through structured discussions with QA directors, DevOps tool vendors, independent test consultants, and regional trade bodies across North America, Europe, and Asia-Pacific. Their real-time views on automation penetration, pricing spreads, and offshore capacity shifts let us refine assumptions and close information gaps before final triangulation.

Desk Research

Our analysts pull foundational evidence from respected public sources such as national ICT expenditure tables, U.S. Bureau of Labor Statistics software employment series, Eurostat digitization indicators, OECD ICT investment datasets, and trade studies like the annual World Quality Report. Company 10-Ks, investor decks, and regulatory submissions add pricing benchmarks and vertical adoption clues, while paid repositories (D&B Hoovers, Dow Jones Factiva) supply firm-level revenue splits. The references listed are illustrative only; many additional sources informed data collection, validation, and research clarification.

Market-Sizing & Forecasting

A top-down model begins with enterprise IT spending and global software output statistics, which are then multiplied by historic QA spend ratios and adjusted for automation share, open-source uptake, and cloud migration intensity. Supplier roll-ups and sampled average-selling-price times project counts provide a bottom-up reasonableness check. Key inputs include annual release velocity, automation percentage of test cases, DevOps adoption rate, regulated-industry share of software budgets, average QA wage, and macro IT capex growth. Five-year outlooks employ multivariate regression blended with scenario analysis to capture shifts in AI-augmented testing and economic cycles. Missing bottom-up datapoints are bridged using regional wage indices and typical staffing patterns.

Data Validation & Update Cycle

Mordor analysts run cross-series variance checks, senior-review audits, and a pre-publication refresh. We update each study annually, triggering interim revisions when material regulations, M&A, or currency swings alter underlying drivers.

Why Our Software Testing Baseline Commands Reliability

Published estimates often diverge because publishers mix adjacent QA activities, freeze exchange rates differently, or refresh models at uneven intervals. We acknowledge these structural choices so clients grasp why numbers vary.

Key gap drivers include inclusion of in-house testing payrolls by some firms, aggregation of hardware validation with software QA, optimistic automation curves, and forecasts built without systematic primary checks. Mordor ties every assumption to documented variables and refreshes each year.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 48.17 B | Mordor Intelligence | - |

| USD 57.70 B | Global Consultancy A | Includes internal QA labor and packaged test tools in scope |

| USD 54.68 B | Industry Association B | Uses constant 2023 exchange rates and bundles training revenue |

These comparisons show that our disciplined scope selection and dual-track modeling give decision-makers a transparent, balanced baseline they can retrace and stress-test with confidence.

Key Questions Answered in the Report

What is the current value of the software testing market?

The software testing market size reached USD 54.44 billion in 2026 and is projected to almost double by 2031.

Which segment is expanding the fastest within software quality assurance?

Testing-as-a-Service is the fastest growing service model, forecast to rise at 15.09% annually as enterprises favor consumption-based pricing.

Why is security testing gaining momentum?

Zero-trust architectures and open-banking APIs are widening the attack surface, driving security and penetration testing to a 14.83% CAGR through 2031.

Which region will contribute the most incremental revenue by 2031?

Asia Pacific is expected to post the highest regional CAGR at 13.46%, led by India’s global capability centers and China’s embedded-software validation demand.

How are AI tools changing traditional test automation?

AI-augmented platforms generate test cases from production logs and self-heal locators, cutting regression-suite build time by up to 68% and maintenance effort by 30-40%.

What is the talent outlook for QA engineers?

Median time-to-fill senior automation roles exceeds 90 days in North America, with salary premiums of 18-25% for skills in Kubernetes-native testing and AI model validation.

Page last updated on: