Collaborative Whiteboard Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

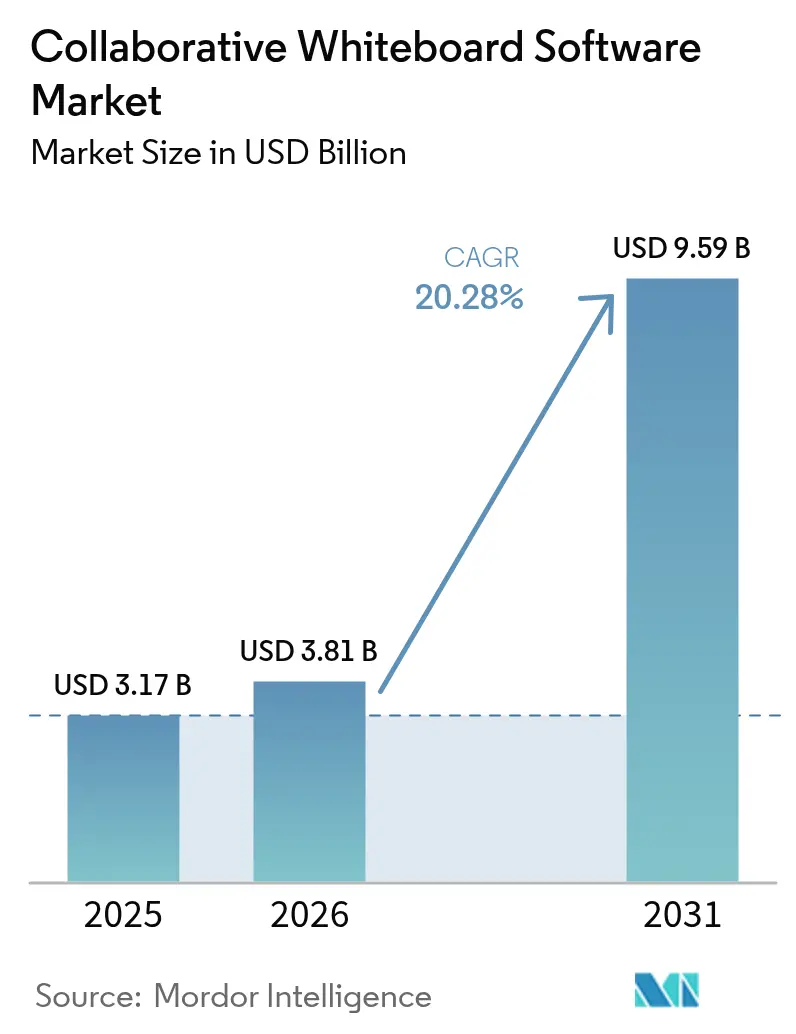

| Market Size (2026) | USD 3.81 Billion |

| Market Size (2031) | USD 9.59 Billion |

| Growth Rate (2026 - 2031) | 20.28% CAGR |

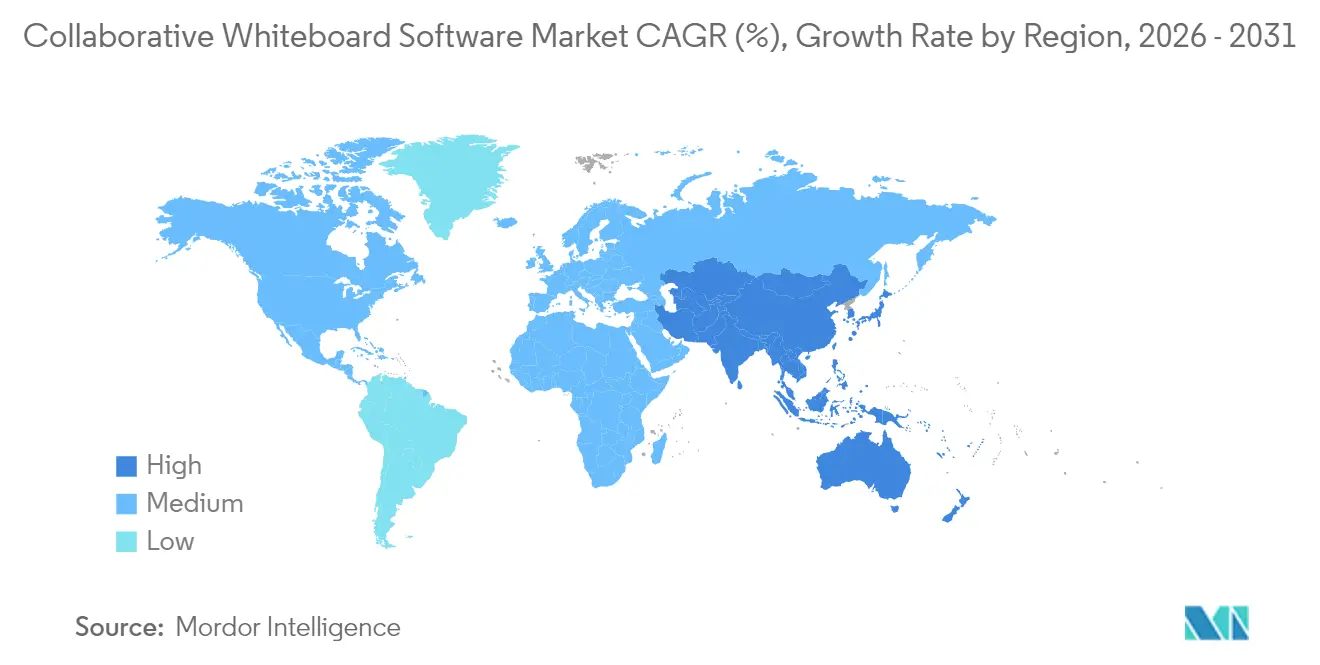

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Collaborative Whiteboard Software Market Analysis by Mordor Intelligence

The collaborative whiteboard software market size was valued at USD 3.17 billion in 2025 and estimated to grow from USD 3.81 billion in 2026 to reach USD 9.59 billion by 2031, at a CAGR of 20.28% during the forecast period (2026-2031). Heightened reliance on hybrid work structures, the rise of cloud-native SaaS ecosystems, and rapid infusions of artificial intelligence have turned visual collaboration from a discretionary spend into a core productivity requirement. Enterprises favor platforms that blend synchronous brainstorming with asynchronous iteration, reinforcing long-term contracts and deep integrations with project management, customer relationship management, and unified communications environments. Vendors able to certify zero-trust architectures and offer FedRAMP or GDPR assurances capture premium demand as security and compliance move to the forefront of purchasing criteria. Simultaneously, “canvas sprawl” governance and knowledge-management integrations are emerging as decisive evaluation factors, especially for multinational organizations that juggle thousands of simultaneous boards. The collaborative whiteboard software market, therefore, rewards providers that deliver secure, AI-enabled, and workflow-embedded experiences across desktop and mobile contexts.

Key Report Takeaways

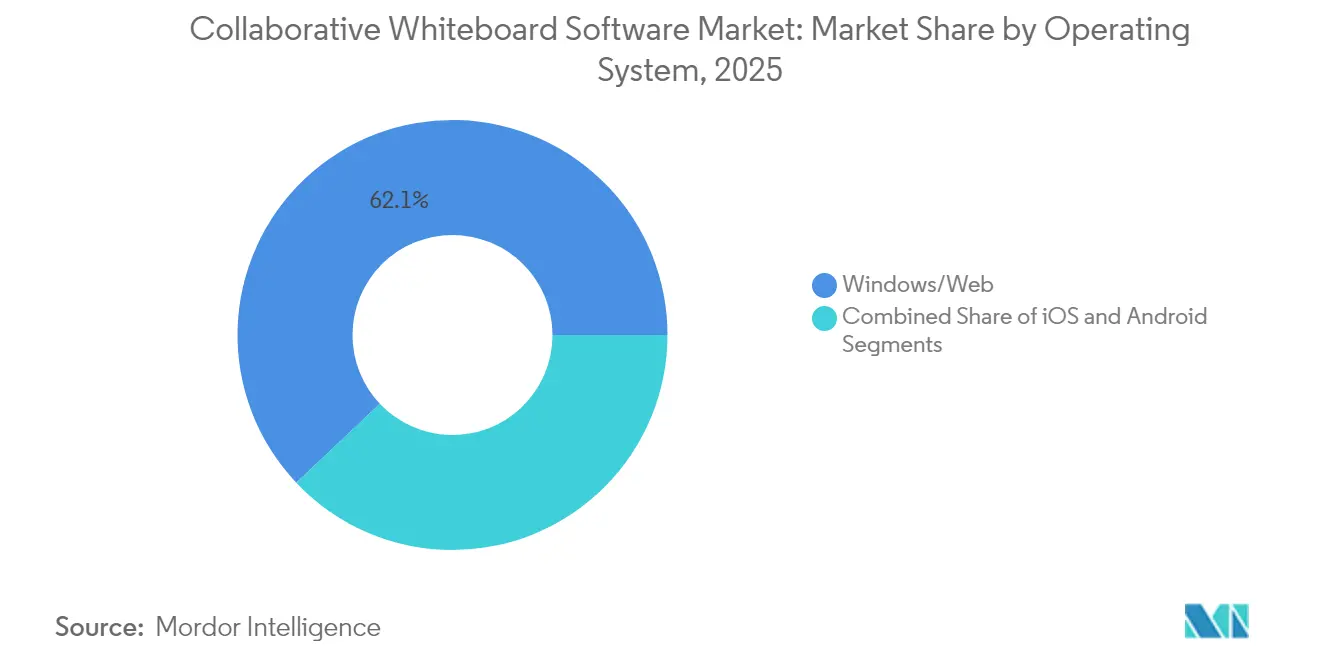

- By operating system, windows/web platforms commanded 62.05% share in 2025 in the collaborative whiteboard software market, whereas Android is projected to grow at a 21.55% CAGR through 2031.

- By deployment, cloud models accounted for 71.05% of the collaborative whiteboard software market size in 2025 and are forecast to accelerate at a 29.45% CAGR over the period.

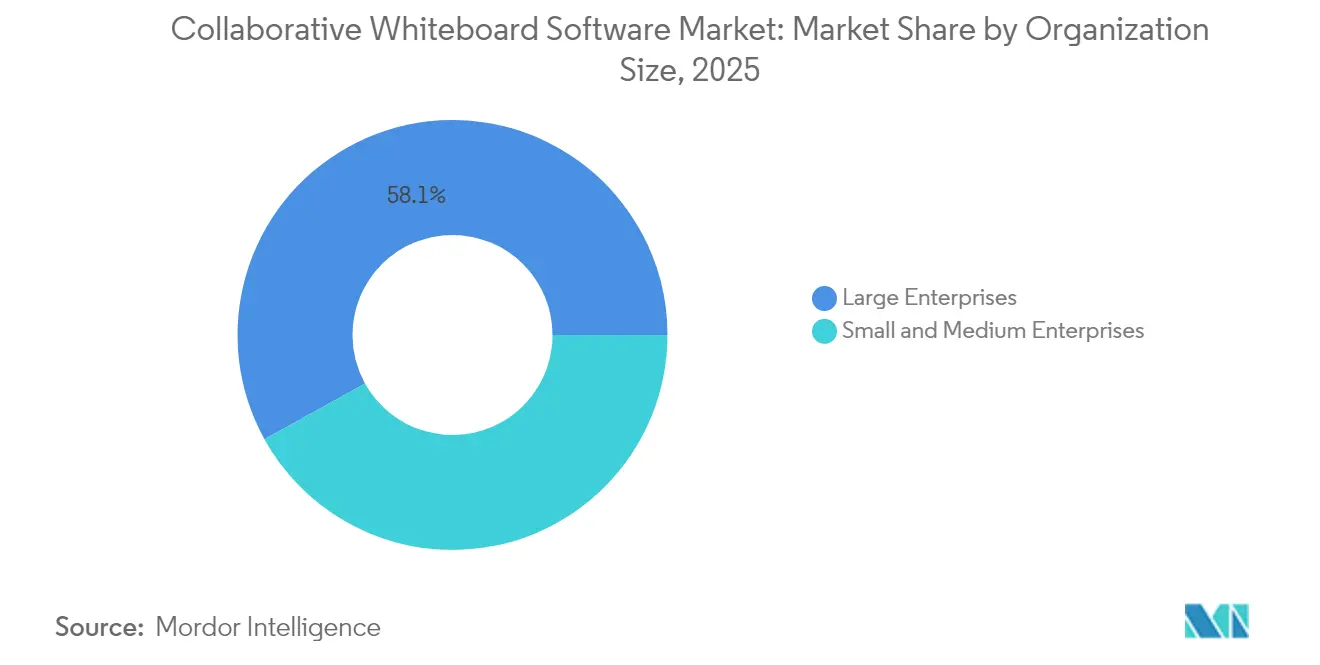

- By organization size, large enterprises held 58.05% revenue share of the collaborative whiteboard software market in 2025, while small and medium enterprises are advancing at a 21.32% CAGR to 2031.

- By end-user vertical, education captured a 30.10% share in 2025 in the collaborative whiteboard software market, yet healthcare is on track to climb at a 21.02% CAGR to 2031.

- By geography, North America led with 37.40% of collaborative whiteboard software market share in 2025, whereas Asia-Pacific is expanding at a 21.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Collaborative Whiteboard Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remote and hybrid work becoming permanent | +6.2% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Expansion of cloud-native SaaS ecosystems | +4.8% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Growing integration with UCaaS and project-management suites | +3.9% | North America and Europe primarily | Medium term (2-4 years) |

| AI-assisted facilitation and automated board summarization | +4.1% | Global, early adoption in North America | Short term (≤ 2 years) |

| Zero-trust whiteboarding demand in classified / defense sectors | +1.2% | North America and Europe, defense-focused | Medium term (2-4 years) |

| Vendor monetisation of template marketplaces and plug-in economies | +0.7% | Global, platform-dependent | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Remote and Hybrid Work Becoming Permanent

Enterprise surveys show that 80% of educators in 2025 believe technology simplifies their roles, up from 63% in 2023. Persistent hybrid arrangements therefore shift procurement from short-term fixes to strategic platforms that merge synchronous ideation with asynchronous follow-ups. Visual context maintained across time zones reduces project friction, prompting longer-term, organization-wide licensing. As a result, the collaborative whiteboard software market underpins core productivity stacks and supports zero-trust-aligned security postures demanded by government contractors and regulated industries.[1]Microsoft Corporation, “FY25 Q4 Productivity and Business Processes,” microsoft.com

Expansion of Cloud-Native SaaS Ecosystems

Microsoft’s cloud revenue climbed 27% year-over-year to USD 46.7 billion in Q4 FY25, underscoring the infrastructural capacity that powers embedded collaboration services.[2]Microsoft Corporation, “FY25 Q4 Productivity and Business Processes,” microsoft.com Vendors leverage open APIs and microservices to slot whiteboards directly into project, CRM, and ERP workflows, turning brainstorming sessions into actionable objects. Reduced implementation friction democratizes adoption among SMEs, while continuous delivery pipelines let providers roll out features such as AI templates and iterative analytics without client-side upgrades. Consequently, cloud alignment is both a competitive necessity and a primary accelerator of the collaborative whiteboard software market.

Growing Integration with UCaaS and Project-Management Suites

Unified communications suites now include native whiteboards, lowering switching costs and broadening exposure. Zoom offers AI-powered boards within existing subscriptions, highlighting how embedded functionality converts non-seekers into active users.[3]Zoom Video Communications, “Empower Visual Collaboration with Online Whiteboards,” zoom.com Standardization of features such as template libraries, infinite canvases, and task hand-offs pressures standalone vendors to specialize or vertically integrate. At the same time, convergence expands total addressable demand, lifting overall growth of the collaborative whiteboard software market.

AI-Assisted Facilitation and Automated Summarization

Miro’s in-product AI launched in 2023 shows how automation turns passive canvases into proactive copilots that generate diagrams, cluster ideas, and produce meeting summaries. Real-time automation boosts session throughput and addresses common fatigue associated with virtual workshops. Vendors investing in transparent data-handling policies and audit logs sidestep regulatory pushback, positioning AI as an accelerator rather than a compliance liability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and compliance concerns (GDPR, FedRAMP, HIPAA) | -2.8% | Europe and North America primarily | Short term (≤ 2 years) |

| Low digital infrastructure in parts of Africa and South Asia | -1.9% | Africa and South Asia regions | Long term (≥ 4 years) |

| "Good-enough" free whiteboards bundled with UC platforms | -2.1% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Canvas-sprawl creating governance and knowledge-management headaches | -1.4% | Global, enterprise-focused impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Compliance Concerns

GDPR, FedRAMP, and HIPAA stipulations extend sales cycles by 12–18 months in sectors handling protected data. Requirements for in-region storage, encryption, and penetration-test attestation raise vendor operating costs. Providers achieving full certifications, such as Bluescape’s FedRAMP Moderate authorization, enjoy an immediate differentiator among defense and public-sector clients, but the broader collaborative whiteboard software market temporarily slows while vendors retrofit security postures.

Low Digital Infrastructure in Africa and South Asia

Average fixed-line bandwidth below 10 Mbps in portions of Sub-Saharan Africa constrains real-time multi-user synchronization. Offline modes, compressed data streams, and simplified mobile interfaces are essential adaptations. As fiber backbone expansions continue, latent demand will unlock, but near-term growth remains tempered outside major metropolitan hubs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operating System: Mobile Platforms Drive Future Growth

The collaborative whiteboard software market size attributed to Windows/Web operating environments stood at USD 1.97 billion in 2025, translating to 62.05% dominance. Android platforms, however, are expected to post a 21.55% CAGR through 2031, reflecting the workforce shift toward device-agnostic collaboration. Android gains are reinforced by deep Google Workspace hooks and cost-effective hardware that suits field teams and emerging-market users. iOS adoption also rises in executive settings where tablets prove convenient for on-the-go ideation.

Traditional desktop integrations with legacy enterprise software safeguard the leadership of windows/web, yet touchscreen advancements and AI-generated diagramming are shrinking productivity gaps. Mobile security frameworks such as enterprise mobility management now match desktop controls, further propelling smartphone and tablet usage. Consequently, providers that deliver parity across screen sizes will seize disproportionate growth within the collaborative whiteboard software market.

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployments captured 71.05% of collaborative whiteboard software market share in 2025, equal to a USD 2.25 billion revenue pool. Fueled by 29.45% CAGR expectations, SaaS models appeal through automatic scaling, continuous feature rollout, and lower total cost of ownership. On-premises adoption persists in banking and defense, yet even these verticals gravitate toward hybrid architectures that partition sensitive data into private clouds while retaining public-cloud collaboration advantages.

Capital investments of USD 24.2 billion by hyperscale providers such as Microsoft in 2025 underscore the infrastructure race supporting cloud applications. Features like high-availability global points of presence and integrated observability tools enhance performance and governance. As a result, cloud-native orientation remains the bedrock for competitive resilience within the collaborative whiteboard software market.

By Organization Size: SME Adoption Accelerates

Large enterprises generated USD 1.84 billion of revenue in 2025, equal to 58.05% collaborative whiteboard software market share, owing to larger seat counts and deeper integrations. Yet SMEs represent the fastest expansion vector at a 21.32% CAGR through 2031, boosted by freemium entry points and credit-card-based self-service onboarding. Subscription elasticity lets smaller teams pilot advanced functionality without infrastructure expenditure.

SME enthusiasm is amplified by employee familiarity with collaboration apps from prior roles in bigger organizations. Conversely, large enterprises seek consolidation, bundling whiteboard capabilities into broader productivity suites to eliminate redundant tools. Vendors balancing ease of adoption with enterprise-grade governance will bridge both cohorts and capture outsized influence across the collaborative whiteboard software market.

By End-User Vertical: Healthcare Growth Outpaces Education Leadership

Education accounted for 30.10% of revenue in 2025 as classrooms embraced interactive digital content and remote learning. Healthcare, while smaller today, is projected to grow at 21.02% CAGR, fueled by telehealth, interdisciplinary case reviews, and medical-training simulations that benefit from visual collaboration.

Regulatory complexities traditionally slowed healthcare purchases, but vendors with HIPAA-ready or ISO 13485-aligned offerings now unlock budgets for collaboration in patient-centric and research workflows. Education demand remains stable, driven by curriculum innovation and government digital inclusion grants. Together these sectors anchor vertical diversification strategies inside the collaborative whiteboard software market.

Geography Analysis

North America generated the highest revenue at 37.40% collaborative whiteboard software market share in 2025, reflecting mature SaaS spending patterns and entrenched hybrid work cultures. Zero-trust mandates spur demand for platforms boasting FedRAMP or DoD Impact Level 4 credentials, particularly among aerospace and defense contractors. Saturation in traditional enterprise pockets propels vendors toward niche-vertical modules and advanced AI features to sustain renewal growth.

Asia-Pacific is on pace for a 21.05% CAGR through 2031, propelled by mobile-first workstyles, surging ed-tech investments, and government-backed digital programs across India, Indonesia, and Vietnam. Smartphone penetration and 5G rollouts lower access barriers, though providers must optimize for intermittent connectivity and multilanguage UI support. The collaborative whiteboard software market therefore rewards mobile-optimized architectures and region-specific pricing.

Europe’s steady adoption is moderated by GDPR data-sovereignty obligations that lengthen deployment cycles and limit AI functionality unless vendors can guarantee transparent data-handling. National cloud initiatives in France and Germany create opportunities for local hosting partnerships. Meanwhile, Middle East and Africa and South America represent long-term upside contingent on infrastructure upgrades and increased hybrid work prevalence.

Competitive Landscape

Market fragmentation persists, yet consolidation is ramping. Wrike announced plans in December 2024 to absorb Klaxoon, integrating infinite canvas capability directly into its work-management suite. In September 2025, Atlassian agreed to acquire The Browser Company, signaling intent to weave browser-native whiteboarding and AI insights into its developer collaboration stack.

Technology differentiation centers on embedded artificial intelligence. Miro’s beta assistants auto-generate templates, cluster sticky-notes, and draft follow-up tasks, raising the baseline for productivity features. Microsoft Whiteboard leverages Azure OpenAI services to summarize session outcomes and convert diagrams into Microsoft Planner tasks, tightening ecosystem lock-in.

Security and compliance remain decisive. Bluescape secured FedRAMP Moderate and DoD IL4 status, enabling classified collaboration scenarios. Vendors also monetize template marketplaces and custom integrations, diversifying revenue beyond per-seat SaaS subscriptions. Overall, intensified R&D around AI, security, and workflow convergence defines competitive trajectories across the collaborative whiteboard software market.

Collaborative Whiteboard Software Industry Leaders

InVisionApp Inc.

Microsoft Corporation

Google LLC

Cisco Systems, Inc.

Miro, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Atlassian announced a USD 610 million cash deal to purchase The Browser Company, aiming to embed Arc’s whiteboard and AI features into its portfolio.

- August 2025: Microsoft reported 15% growth in Microsoft 365 Commercial cloud revenue, with rising adoption of Microsoft Whiteboard and Loop components.

- December 2024: Wrike agreed to acquire Klaxoon to merge creative visual management with intelligent work management capabilities, targeting enterprise clients such as Total and LVMH.

- July 2024: Zoom expanded its AI Companion to include automated whiteboard content generation and summarization.

Global Collaborative Whiteboard Software Market Report Scope

Collaborative whiteboard software provides a shared, singular, and open design space where collaborators can simultaneously edit and share content from their respective devices. A collaborative whiteboard tool often resembles a physical whiteboard. These solutions include a spread of features that allow users to design, communicate, save, and share content in a customizable space.

The collaborative whiteboard software market is segmented by operating system (Windows and web, iOS, and Android), deployment mode (on-premise and cloud), organization size (large enterprises and small and medium enterprises), end-user vertical (BFSI, Healthcare, education, IT and telecommunications, and other end-user verticals), and Geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Windows and Web |

| iOS |

| Android |

| Cloud |

| On-premise |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare |

| Education |

| IT and Telecommunications |

| Other End-user Verticals |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Operating System | Windows and Web |

| iOS | |

| Android | |

| By Deployment Mode | Cloud |

| On-premise | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-user Vertical | BFSI |

| Healthcare | |

| Education | |

| IT and Telecommunications | |

| Other End-user Verticals | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the collaborative whiteboard software market?

The collaborative whiteboard software market size is USD 3.81 billion in 2026.

How fast is the market expected to grow by 2031?

It is projected to expand at a 20.28% CAGR, reaching USD 9.59 billion.

Which region is growing the quickest?

Asia-Pacific is forecast to register a 21.05% CAGR through 2031, the highest worldwide.

Why are cloud deployments so dominant?

Cloud models offer automatic updates, elastic scaling, and seamless integration, giving them 71.05% market share in 2025.

Which vertical shows the strongest growth potential?

Healthcare is poised to grow at a 21.02% CAGR as telehealth and clinical collaboration expand.

Page last updated on: