Survey Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.12 Billion |

| Market Size (2031) | USD 9.6 Billion |

| Growth Rate (2026 - 2031) | 13.38% CAGR |

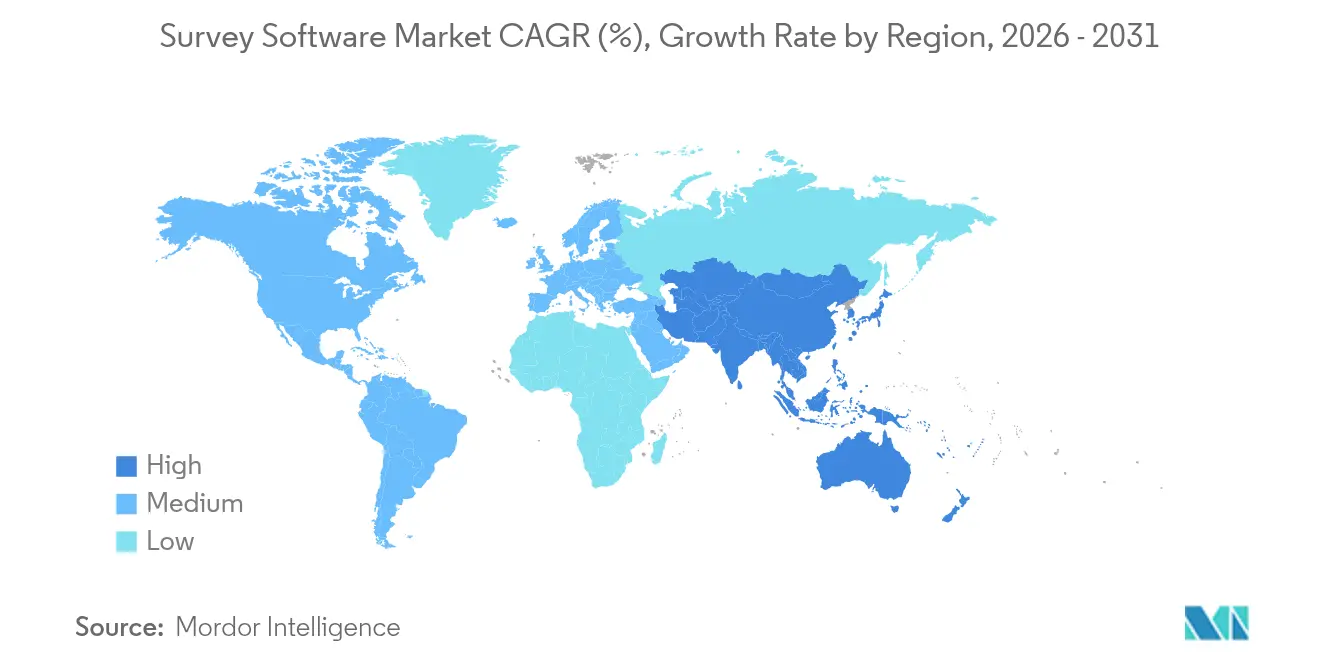

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

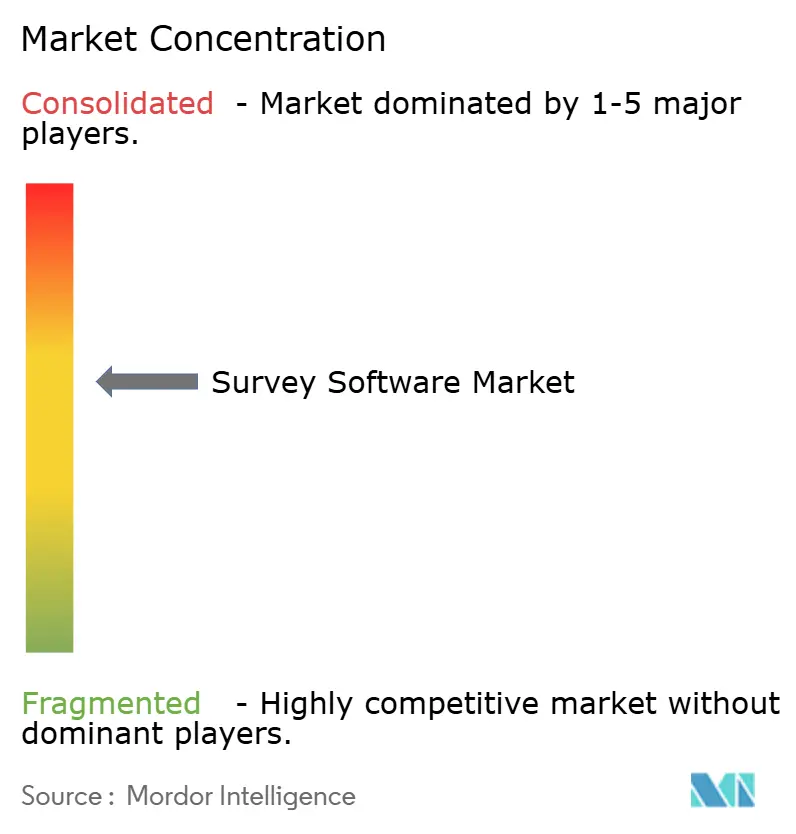

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Survey Software Market Analysis by Mordor Intelligence

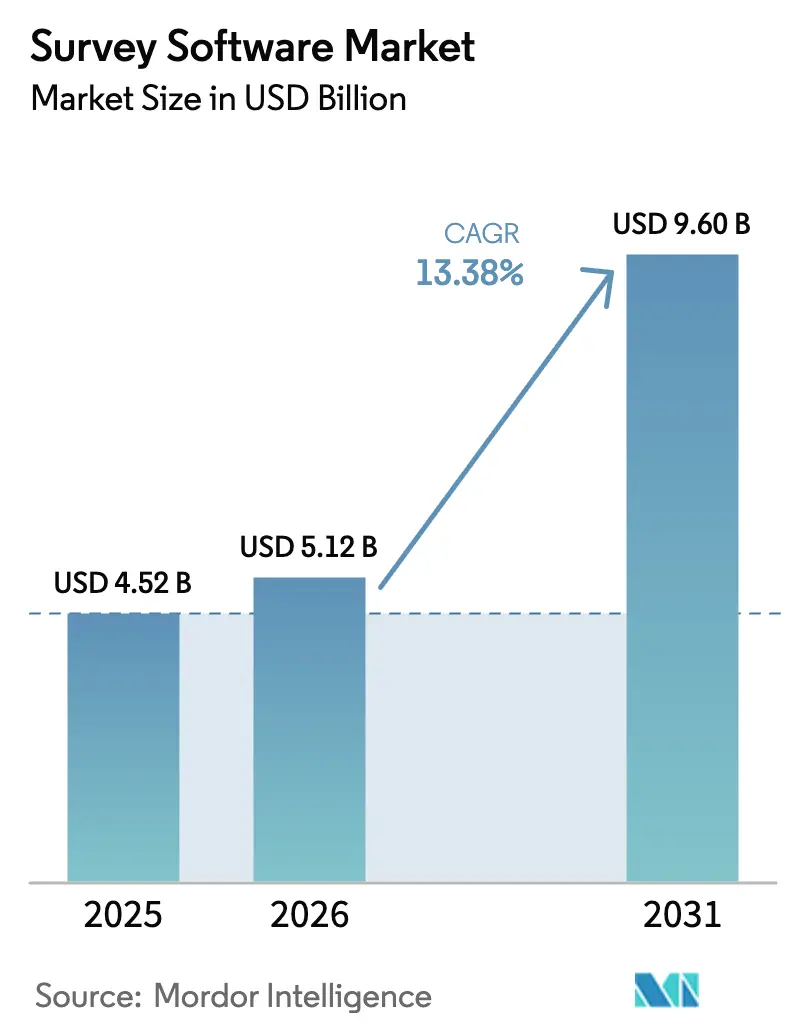

The Survey Software Market size was valued at USD 4.52 billion in 2025 and estimated to grow from USD 5.12 billion in 2026 to reach USD 9.6 billion by 2031, at a CAGR of 13.38% during the forecast period (2026-2031). Growth is underpinned by the shift from periodic research toward always-on feedback loops that plug directly into customer-experience, employee-engagement, and product-development workflows. Enterprise buyers drive near-term spending on artificial-intelligence-ready analytics and deep application-program-interface (API) stacks, while price-sensitive small businesses unlock similar capabilities through tiered SaaS subscriptions. Cloud deployment sustains momentum thanks to low upfront cost and automatic model updates, and retailers, banks, and healthcare providers remain the heaviest users because feedback metrics now connect directly to revenue, regulatory compliance, and reimbursement formulas. Regionally, North America provides scale and reference use cases, but Asia-Pacific supplies the fastest incremental revenue as local SaaS ecosystems mature.

Key Report Takeaways

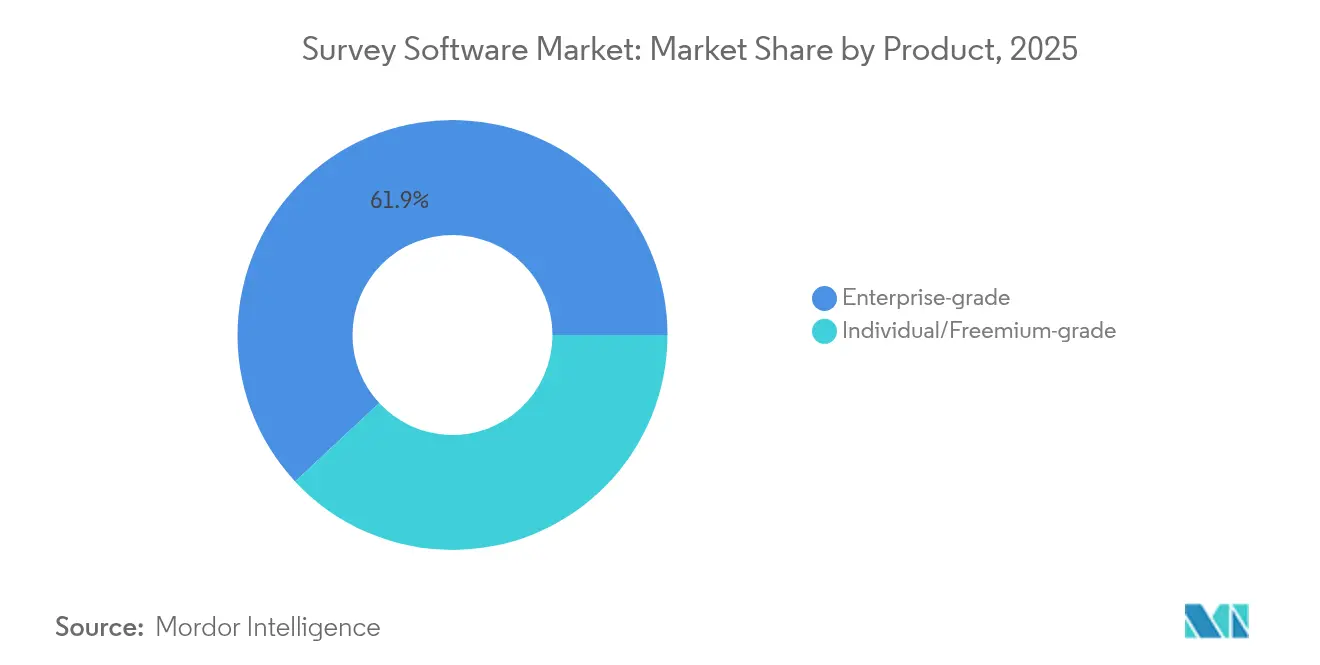

- By product, enterprise-grade solutions captured 61.92% of the survey software market share in 2025, while the individual/freemium segment is forecast to expand at 16.32% CAGR to 2031.

- By method, online deployment held 85.88% revenue share in 2025; offline/kiosk is projected to grow 15.52% CAGR through 2031.

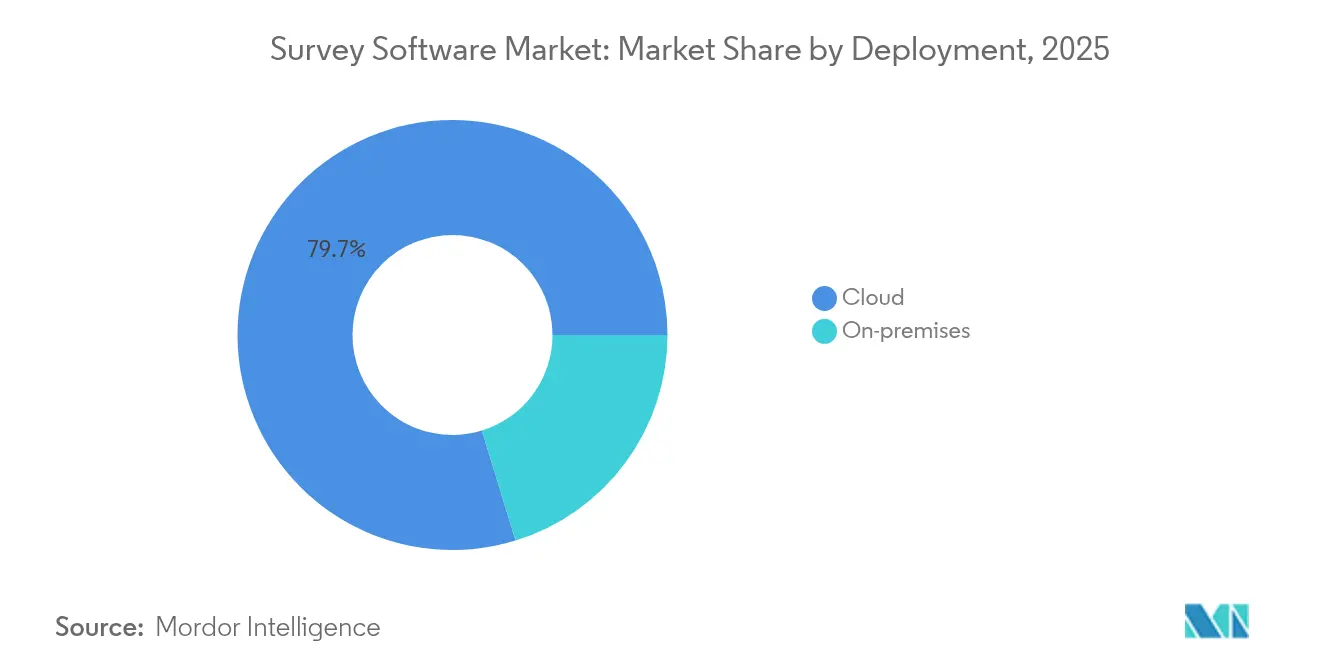

- By deployment, cloud commanded 79.74% of the survey software market size in 2025 and is advancing at 15.18% CAGR to 2031.

- By organization size, large enterprises held 63.58% share in 2025, while SMEs are rising at 16.08% CAGR on the back of SaaS adoption.

- By end-user industry, retail and e-commerce led with 29.02% revenue in 2025; healthcare and life sciences are advancing at 15.34% CAGR through 2031.

- By geography, North America contributed 38.15% of 2025 revenue, whereas Asia-Pacific is set to grow 15.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Survey Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digital-first CX programs | +3.4% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Expansion of remote and hybrid workforces | +2.7% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Rising SaaS adoption among SMEs | +2.0% | APAC core, spill-over to Latin America and MEA | Medium term (2-4 years) |

| AI-driven adaptive questionnaires | +1.6% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Growing demand for voice and video survey inputs | +1.4% | Global, with early gains in tech-forward markets | Long term (≥ 4 years) |

| ESG-linked stakeholder feedback mandates | +1.2% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Digital-First CX Programs Drive Platform Sophistication

Enterprises now route purchase-journey, churn-risk, and service-quality triggers through real-time feedback APIs, upgrading survey software from episodic research tools to mission-critical systems. Buyers emphasize sentiment analysis, auto-alerting, and workflow connectors that cut response-to-action cycles from days to minutes. [1]SurveyMonkey, “State of surveys: What our platform says about 2025,” surveymonkey.com Retailers link store-level satisfaction scores to on-shelf availability and staffing schedules, turning the survey software market into a direct lever on operating margin. This demand for instantaneous insight keeps average deal values high and accelerates multi-year contracts. Vendors capable of bundling predictive analytics and native integrations strengthen pricing power. Together, these factors add measurable uplift to overall survey software market growth.

AI-Driven Adaptive Questionnaires Reshape Response Quality

Natural-language-processing engines personalize question flow in surveys, raising completion rates and depth of insight. [2]Fillout, “AI Survey Maker,” fillout.com Platforms that generate follow-up probes on the fly mitigate respondent fatigue without sacrificing data richness, a pivotal advantage in high-frequency pulse programs. Japanese innovators such as atarayo deliver 30-second voice-of-customer snapshots, illustrating how agile AI can compress research timelines. The improvement in respondent experience feeds back into user acquisition, reinforcing the virtuous cycle driving survey software market expansion over the long term.

Rising SaaS Adoption Among SMEs Democratizes Advanced Analytics

Tiered subscription models and no-code onboarding now bring predictive modelling and dashboarding to cash-constrained firms that previously ran manual polls. Low-touch sales cycles shorten time-to-value, letting micro-brands act on customer sentiment within hours of launch. This bottom-up diffusion enlarges the global survey software market addressable base while curbing revenue cyclicality linked to enterprise budget freezes. Vendors that can package compliance templates and vertical taxonomies for SMEs stand to outpace category averages through 2030.

ESG-Linked Stakeholder Feedback Mandates Create Compliance-Driven Demand

European and North American regulators increasingly require auditable stakeholder engagement metrics in sustainability disclosures. Boards and investors now expect standardized survey outputs aligned with global frameworks, elevating demand for platforms offering automated audit trails and consent management. These compliance add-ons lift average selling prices without proportionate cost escalation, supporting margin expansion across the survey software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-quality and survey fatigue concerns | -1.4% | Global, particularly in over-surveyed markets | Short term (≤ 2 years) |

| Stringent data-privacy regulations (GDPR, CCPA) | -1.1% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Browser cookie deprecation limiting respondent tracking | -0.9% | Global, with immediate impact on digital marketing | Short term (≤ 2 years) |

| Rising cost of respondent incentives | -0.7% | Developed markets with high labor costs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Quality and Survey Fatigue Concerns Threaten Response Reliability

Rampant feedback requests in retail and banking have pushed average open rates down, undermining data validity just as executives lean harder on real-time metrics. Shortening questionnaires can trim dropout, but often erodes analytic depth. Advanced platforms deploy send-frequency caps and predictive timing, yet these require coordination across marketing, service and HR silos. Until such governance matures, response-rate risk will temper near-term survey software market growth.

Stringent Data-Privacy Regulations Complicate Global Deployment

GDPR and CCPA drive up implementation costs by demanding explicit consent, geo-fenced data residency, and rigorous deletion processes. Multinationals must configure parallel workflows to run one questionnaire across multiple legal regimes, elongating sales cycles and raising the bar for vendor compliance certifications. Smaller firms sometimes stall adoption for fear of fines, trimming achievable survey software market penetration in heavily regulated sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Enterprise Solutions Lead Despite Freemium Surge

Enterprise-grade platforms generated 61.92% of 2025 revenue, cementing their hold on complex deployments that require granular permissioning, custom dashboards, and HIPAA-calibre security. The segment’s continued dominance bolsters average selling prices in the survey software market even as competition intensifies. Enterprise buyers value consultative onboarding and native connectors into customer-relationship-management and data-warehouse stacks, reinforcing high switching costs.

Momentum, however, clearly sits with individual and freemium tools growing at 16.32% CAGR through 2031, a pace that eclipses overall survey software market growth. Freemium vendors monetise through AI-powered premium tiers that auto-generate questionnaires and insights, sparking word-of-mouth adoption among resource-constrained users. As conversions accelerate, platform owners capture incremental revenue without proportional marketing spend, adding leverage to the survey software market economics.

By Method: Online Dominance Faces Offline Innovation

Online methods accounted for 85.88% of 2025 revenue, reflecting unmatched scalability and integration with email, SMS, and in-app channels. Dominance persists as mobile-optimised interfaces and real-time analytics stay core to enterprise feedback strategies. Offline and kiosk collection nonetheless advances at 15.52% CAGR, outpacing the broader survey software market. In-store tablets, airport terminals, and hospital waiting-room kiosks capture voice and video feedback on the spot, generating rich media datasets that augment text-based responses.

The hybridisation of online alerts triggered by offline inputs merges the best of both worlds. Vendors that enable seamless data sync while maintaining offline resilience position themselves for above-average share gains as the survey software market matures.

By Deployment: Cloud Infrastructure Accelerates Market Transformation

Cloud deployment represented 79.74% share of the survey software market size in 2025 and is tracking 15.18% CAGR to 2031. Automatic upgrades, zero-footprint scaling, and bundled AI services make the cloud the default for new rollouts. On-premises persists where data sovereignty is non-negotiable, yet even conservative industries increasingly pilot hybrid models that keep raw data local while running analytics in the cloud.

With security certifications such as ISO 27001 and SOC 2 now table stakes, risk perceptions favour hyperscale infrastructure over legacy server rooms. As cloud unit economics improve, total cost of ownership declines, opening the survey software market to firms that once balked at enterprise-grade pricing.

By Organization Size: SME Growth Challenges Enterprise Dominance

Large enterprises retained 63.58% of 2025 spending thanks to global rollouts and multi-department licences. Yet SMEs are scaling revenue faster at 16.08% CAGR, eroding the gap in absolute contribution. Drag-and-drop builders, AI-generated sentiment clustering, and out-of-the-box regulatory templates lower adoption friction, inserting survey workflows into the daily operations of retailers, clinics, and SaaS start-ups alike.

Price-sensitive buyers reward vendors offering monthly contracts and usage-based tiers, which compress sales cycles and widen the survey software market funnel. As SMEs mature, upsell paths into advanced integrations and role-based analytics promise sustained revenue lift with limited churn.

By End-user Industry: Retail Leadership Meets Healthcare Innovation

Retail and e-commerce contributed 29.02% of 2025 global revenue by linking Net Promoter Scores to merchandising and staffing targets in real time. Beyond transactional feedback, retailers deploy longitudinal community panels that inform product innovation, cementing the vertical’s primacy within the survey software market.

Healthcare and life sciences post the fastest expansion at 15.34% CAGR through 2031. Mandatory patient-experience metrics tied to reimbursement motivate hospital groups to invest in HIPAA-compliant, closed-loop survey workflows. Integrated dashboards cascade insights from ward to boardroom, illustrating how regulated environments can still drive cutting-edge adoption when value aligns with compliance.

Geography Analysis

North America generated 38.15% of 2025 revenue on the back of mature SaaS procurement processes, sophisticated buyer expectations, and a dense ecosystem of experience-management specialists. Continued innovation in predictive analytics and voice analysis maintains spend, yet market saturation tempers headline growth. Data-privacy expansion, including state-level rules modelled on CCPA, raises compliance costs but also differentiates vendors that embed consent orchestration.

Asia-Pacific delivers the steepest trajectory at 15.76% CAGR to 2031, quadrupling its slice of the survey software market by the end of the period. India’s SaaS boom and Japan’s AI-powered survey breakthroughs highlight how emerging and advanced economies alike converge on cloud-first feedback stacks. Localization, regional data centres, and multibyte-character support become must-have features for global vendors pursuing share.

Europe advances steadily as GDPR-aligned consent and data-residency mandates push buyers toward platforms with built-in compliance modules. Latin America and the Middle East and Africa remain nascent but attractive thanks to rising smartphone adoption and government digitization agendas, making them next-wave contributors to survey software market expansion once macro volatility eases.

Competitive Landscape

The survey software market displays moderate fragmentation. Qualtrics tops revenue tables at USD 1.4 billion and leverages Silver Lake backing to double down on AI product launches. [4]Financier Worldwide, “Qualtrics acquired by Silver Lake for USD 12.5bn,” financierworldwide.com SurveyMonkey, with USD 313.3 million turnover, courts mid-market clients by broadening language support and regional hosting. Typeform’s conversational interface resonated with SMEs, lifting 2024 revenue to USD 141.1 million, a 41% jump year on year.

Product differentiation now centres on native natural-language processing, multichannel delivery, and embedded workflow actions. Smaller challengers like SurveySparrow channel USD 1.42 million in fresh capital toward offline support and role-based reporting to prise open retail and hospitality accounts. Partnerships with CRM, marketing-automation, and data-visualisation incumbents deepen moats for vendors that achieve ecosystem fit.

Price competition remains measured because switching costs are high once surveys, dashboards, and historical benchmarks live on a platform. Consequently, top-five suppliers collectively control around 45% of global revenue, leaving meaningful room for niche entrants focused on vertical templates, language coverage, or on-device artificial intelligence.

Survey Software Industry Leaders

Qualtrics International Inc.

SurveyMonkey (Momentive Inc.)

Alchemer LLC

Zoho Corporation Pvt. Ltd. (Zoho Survey)

Typeform S.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: atarayo launched a 30-second AI consumer-insight engine in Japan.

- May 2025: The Product Force and Marketing Applications survey showed 42.6% of users will increase self-research service use.

- April 2025: Qualtrics released predictive churn modelling and automated insight generation, cutting analysis time by 60%.

- April 2025: Softcreate IT utilisation survey revealed 76% of companies are migrating to Windows 11.

- March 2025: SurveyMonkey opened a Costa Rica hub to bolster Spanish and Portuguese localisation.

- March 2025: Alchemer added the Reporter role for controlled data sharing.

- February 2025: Qualtrics retained leadership in voice-of-customer technology rankings.

- January 2025: Typeform reported USD 141.1 million in 2024 revenue, up 41% year on year.

- October 2024: SurveySparrow secured USD 1.42 million in seed funding for offline feedback modules.

Global Survey Software Market Report Scope

Survey software is a tool that allows businesses to create, conduct, and analyze surveys either online or offline. Software tools for surveys are varied, ranging from desktop applications to complex web systems for monitoring consumer behaviour.

The survey software market is segmented by product (enterprise grade, individual grade), by method (online, offline), by deployment (cloud, on-premises), by enterprises (SMEs, large enterprises), by end-user (BFSI, healthcare, retail, education, government, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Enterprise-grade |

| Individual/Freemium-grade |

| Online |

| Offline/Kiosk |

| Cloud |

| On-premises |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Education |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Product | Enterprise-grade | ||

| Individual/Freemium-grade | |||

| By Method | Online | ||

| Offline/Kiosk | |||

| By Deployment | Cloud | ||

| On-premises | |||

| By Organization Size | Small and Medium-sized Enterprises (SMEs) | ||

| Large Enterprises | |||

| By End-user Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Education | |||

| Government and Public Sector | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the survey software market?

The survey software market size stands at USD 5.12 billion in 2026 and is projected to reach USD 9.6 billion by 2031.

Which segment is expanding fastest within the survey software market?

The individual/freemium-grade product segment is forecast to grow at 16.32% CAGR through 2031, outpacing all other categories.

Why is cloud deployment preferred for survey platforms?

Cloud delivers automatic updates, elastic scaling and built-in AI services, giving it 79.74% share of 2025 revenue and a 15.18% growth path.

Which region offers the highest growth opportunity?

Asia-Pacific is projected to expand at 15.76% CAGR to 2031, buoyed by rapid digitalisation and rising SaaS penetration.

How are data-privacy laws affecting adoption?

GDPR and CCPA increase compliance complexity and cost, but they also push buyers toward platforms with native consent and data-residency controls.

Who are the leading vendors in the survey software market?

Qualtrics, SurveyMonkey and Typeform head the field, together holding a significant share and driving innovation in AI-powered analytics.

Page last updated on: