Communication Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.17 Billion |

| Market Size (2031) | USD 26.58 Billion |

| Growth Rate (2026 - 2031) | 15.08% CAGR |

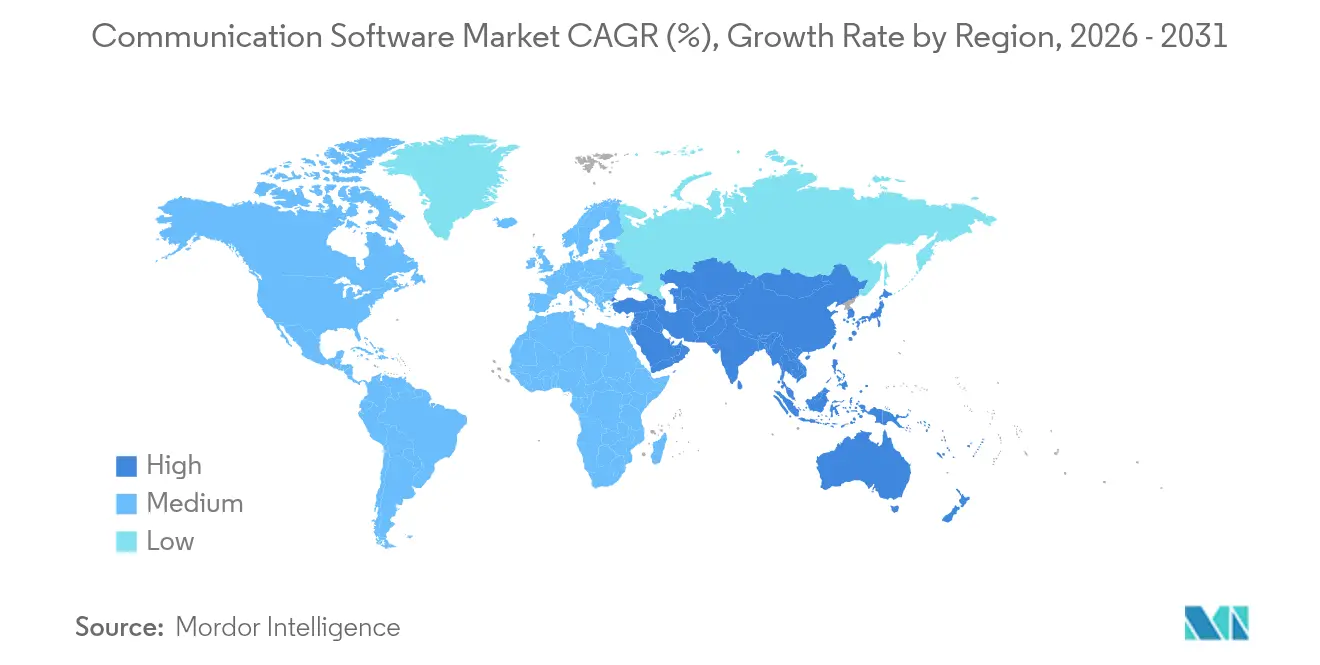

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

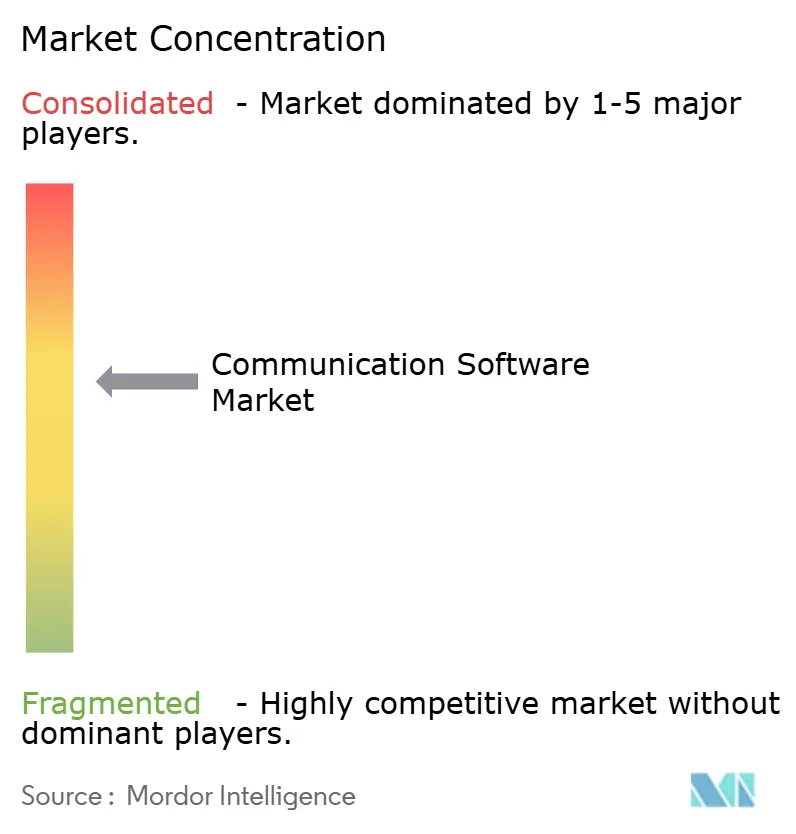

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Communication Software Market Analysis by Mordor Intelligence

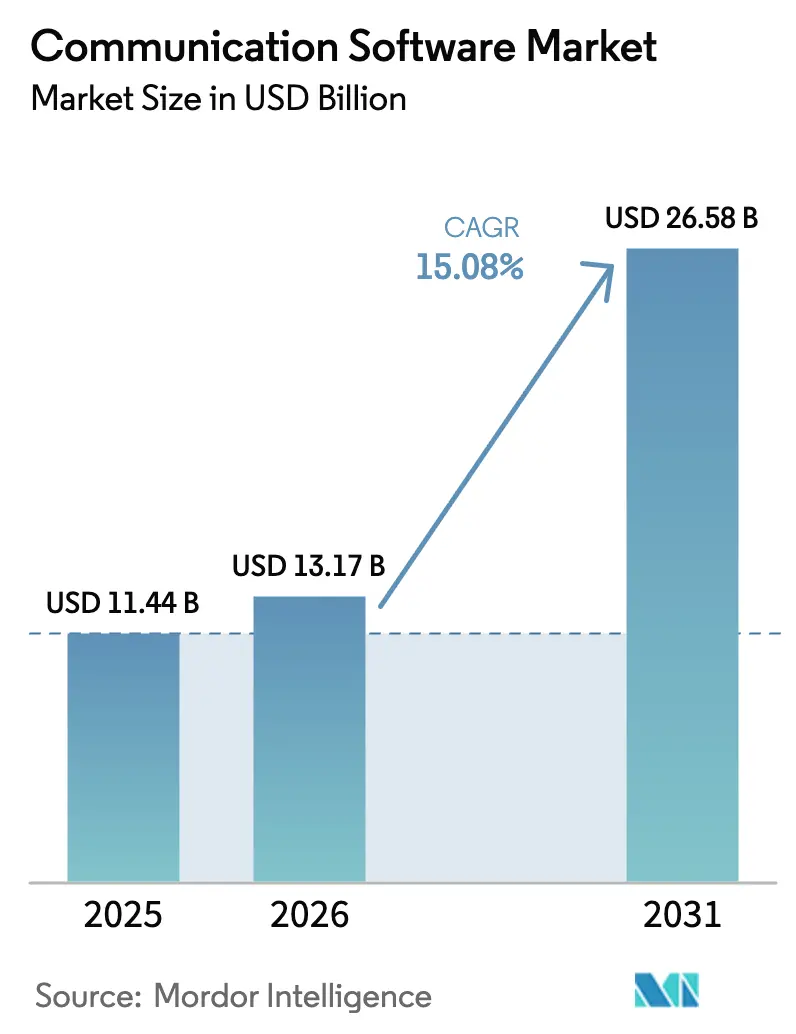

The communication software market size is expected to grow from USD 11.44 billion in 2025 to USD 13.17 billion in 2026 and is forecast to reach USD 26.58 billion by 2031 at 15.08% CAGR over 2026-2031. Intensifying hybrid work requirements, 5G network roll-outs, and fast-maturing AI capabilities are driving sustained investment, while subscription pricing and cloud delivery models lower entry barriers for small and mid-sized firms. Vendors are layering predictive analytics, compliance tooling, and low-code integrations onto core voice, video, and messaging stacks, broadening the addressable user base across regulated verticals. Competitive intensity has heightened through consolidation and AI-focused M&A, prompting faster feature cycles and regional data-sovereignty offerings. Heightened cybersecurity costs and collaboration fatigue temper growth, yet they also spur innovation around zero-trust architectures and digital-wellbeing functions.

Key Report Takeaways

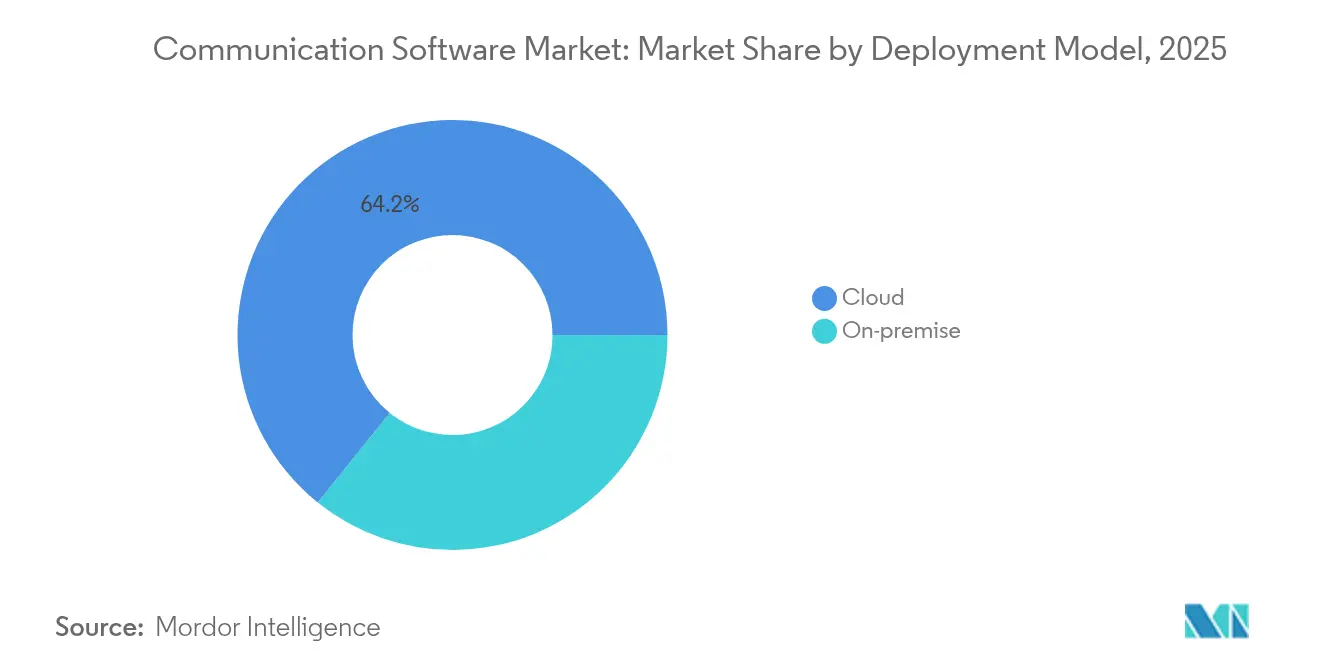

- By deployment model, cloud solutions captured 64.22% of communication software market share in 2025; hybrid cloud is forecast to expand at a 18.6% CAGR through 2031.

- By enterprise size, large enterprises controlled 52.10% of the communication software market in 2025, yet small and medium enterprises lead growth at 17.6% CAGR.

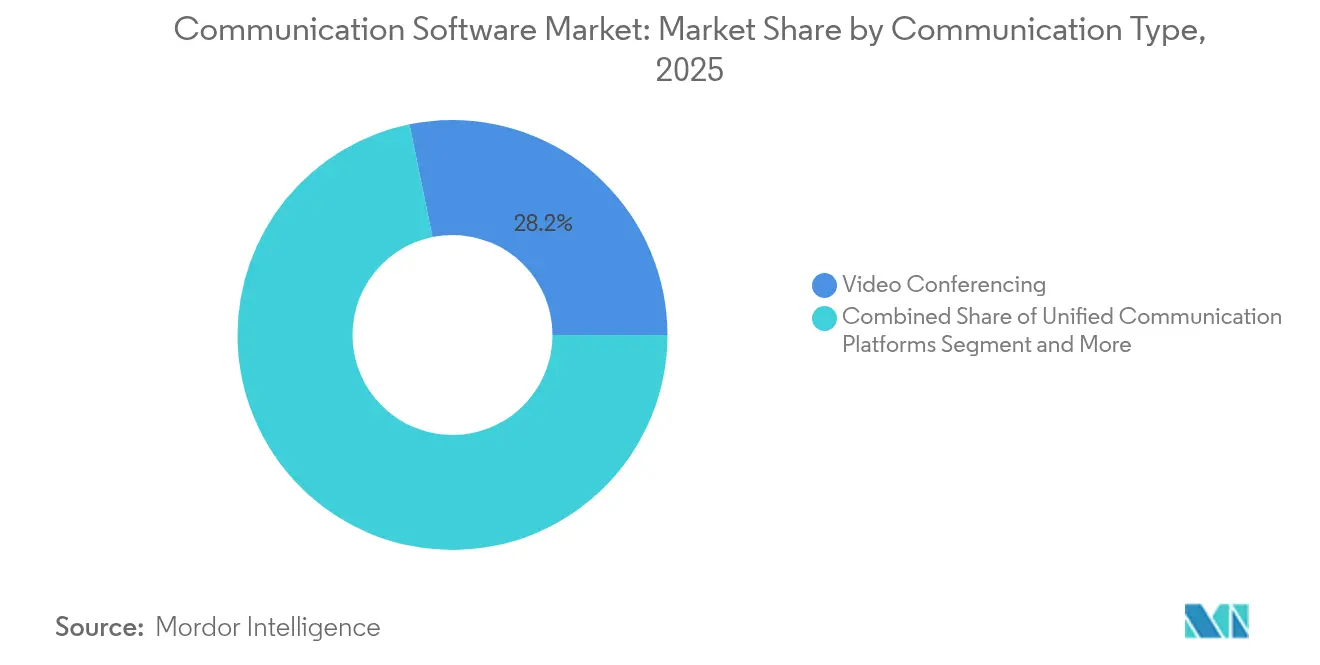

- By communication type, video conferencing held 28.21% of communication software market share in 2025, while unified platforms post the fastest CAGR at 18.1% to 2031.

- By vertical, IT and telecom commanded 28.22% share of the communication software market size in 2025, whereas healthcare is projected to grow at a 16.0% CAGR.

- By geography, North America led with 38.02% revenue share in 2025; Asia-Pacific is advancing at a 21.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Communication Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid work culture boosts UCaaS demand | +4.2% | Global, strongest in North America and EU | Medium term (2–4 yrs) |

| 5G and fiber proliferation improves quality | +3.8% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 yrs) |

| API-driven CPaaS embeds comms in apps | +2.9% | Global, early gains in North America and EU | Short term (≤ 2 yrs) |

| AI-powered analytics enhance ROI | +2.7% | North America and EU, expanding to Asia-Pacific | Medium term (2–4 yrs) |

| Compliance-ready stacks for regulated industries | +1.8% | Global, strongest in North America and EU | Long term (≥ 4 yrs) |

| Cloud adoption accelerates scalability and efficiency | +3.5% | Global, highest in Asia-Pacific and North America | Short–medium (1–3 yrs) |

| Hybrid work culture boosts UCaaS demand | +4.2% | Global, strongest in North America and EU | Medium term (2–4 yrs) |

| Source: Mordor Intelligence | |||

Hybrid Work Culture Boosts UCaaS Demand

Seventy percent of Fortune 500 companies now deploy Microsoft 365 Copilot, underscoring a structural shift toward unified platforms that keep distributed workforces connected.[1]Frank X. Shaw, “Microsoft earnings release FY25 Q1,” Microsoft, microsoft.comZoom’s enterprise revenue rose 5.8% year-over-year to USD 698.9 million in Q3 2025, validating enterprise appetite for integrated collaboration suites. Persistent digital workspaces, threaded chat, and contextual file sharing help organizations re-establish cohesion after prolonged remote-only periods. Vendors now emphasize workflow-level integration over standalone meetings, with AI assistants summarizing threads and highlighting action items. Demand for always-on, low-latency video, messaging, and whiteboarding therefore remains elevated, anchoring growth across the communication software market.

5G and Fiber Proliferation Improves Quality

Ericsson’s 2024 launch of seven 5G-Advanced network software packages illustrates how intelligent RAN and core upgrades lower jitter and latency thresholds once considered prohibitive for mission-critical communications.[2]Fredrik Jejdling, “Ericsson introduces 5G-Advanced,” Ericsson, ericsson.comETSI’s F5G Quality-of-Service specification further provides standardized performance targets that developers can reference when embedding live video or AR collaboration features. CNBC projects edge-computing spending will reach USD 232 billion in 2024, moving compute closer to endpoints and slashing round-trip times for voice and interactive video.[3]Annie Palmer, “Edge computing spend to hit USD 232 billion,” CNBC, cnbc.com Asia-Pacific’s aggressive 5G roll-out accelerates AI-driven use cases, such as real-time translation and sentiment analytics, propelling the communication software market throughout the decade.

API-Driven CPaaS Embeds Communications in Apps

Low-code APIs let developers weave voice, messaging, and video into line-of-business applications without provisioning network infrastructure, effectively turning communications into “invisible plumbing”. Usage-based billing aligns costs with interaction volumes, attracting product teams that favor agile experimentation over capital outlays. Early adopters in finance and retail report faster on-boarding journeys and higher customer-service NPS scores after embedding CPaaS modules, confirming that seamless experience gains outweigh integration overhead. The model broadens the communication software market by tapping developer communities rather than central IT.

AI-Powered Analytics Enhance ROI

Microsoft’s AI business reached a USD 13 billion annual run rate in 2025, showcasing commercial conviction around AI-enabled communication insights. Healthcare providers using AI chatbots report 57% fewer missed appointments and 78% better patient feedback handling, quantifying tangible operational returns. Zoom’s AI Companion 2.0 spurred a 59% jump in active users, reflecting user willingness to adopt productivity-enhancing features embedded in familiar interfaces. Predictive models that surface customer churn risk or identify collaboration bottlenecks create clear upgrade pathways, reinforcing recurring revenue streams across the communication software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and privacy compliance costs | -2.8% | Global, strongest in North America and EU | Medium term (2–4 years) |

| Collaboration fatigue and digital wellbeing issues | -1.9% | Global, particularly in developed markets | Short term (≤2 years) |

| Large-enterprise market saturation | -1.2% | North America and EU | Medium term (2–4 years) |

| Economic constraints in emerging markets | -0.9% | South America and MEA | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Cyber-security and Privacy Compliance Costs

First-year data-loss-prevention deployments average USD 385,000 for 10,000 seats, putting smaller buyers at a disadvantage. Compliance spans multiple frameworks: HIPAA for healthcare, GDPR for European operations, and SOC 2 or ISO 27001 for regulated finance. Vendors divert engineering resources toward zero-trust, encryption, and audit tooling, delaying feature roadmaps. Mid-market customers lacking in-house security teams therefore face higher total cost of ownership, slowing purchase cycles across the communication software market.

Collaboration Fatigue and Digital Wellbeing Issues

Harvard Business Review shows collaborative activities rose 50% in 12 years, yet knowledge workers now check email 77 times daily and receive 121 new messages, eroding productivity. Asana finds 71% of workers reported burnout in 2024, with 26% of deadlines missed because of fragmented workflows. Organizations increasingly deploy usage analytics, notification throttling, and focus-mode features, but skepticism remains around adding another channel to already crowded stacks. These concerns can elongate sales cycles or limit feature adoption, muting upside in otherwise buoyant segments of the communication software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Dominance Drives Hybrid Innovation

Cloud solutions captured 64.22% of communication software market share in 2025, underscoring enterprise confidence in elastic, vendor-managed environments. The communication software market size allocated to hybrid deployments, however, is projected to expand at a 18.6% CAGR, reflecting growing demand for sovereign data control alongside cloud flexibility. Heavily regulated sectors continue to maintain on-premise nodes for sensitive workloads, yet integration bridges now allow call routing, archiving, and analytics to reside in the public cloud with minimal latency.

Multi-tenant architectures compress per-user costs and speed feature delivery, but CIOs increasingly pilot sovereign-cloud regions and customer-managed encryption keys to meet data-residency statutes. Microsoft’s sovereign-cloud program and Zoom’s on-premise media nodes exemplify vendor adaptations that keep sensitive voice traffic local while cloud services handle meeting intelligence. As these hybrid patterns mature, the communication software market will see convergence between private and public deployment models rather than outright substitution.

By End-user Enterprise Size: SME Growth Challenges Enterprise Saturation

Large enterprises commanded 52.10% of the communication software market in 2025 after years of enterprise-wide Teams, Webex, and Zoom deployments. Growth momentum now shifts to SMEs, which post an 17.6% CAGR as user-based subscriptions, template-driven APIs, and managed-service bundles simplify adoption. The communication software market size associated with micro-enterprises is still modest but rising quickly due to remote-first hiring and gig-economy expansion.

RingCentral, 8x8, and Intermedia market AI-assisted onboarding and pre-configured compliance packs that strip away integration friction. Consumption-based pricing aligns with seasonal demand, while app-store plug-ins automate CRM or EHR integrations previously considered enterprise-only. Heightened SME adoption thereby diversifies revenue pools and dilutes vendor reliance on Fortune 500 renewals across the communication software market.

By Communication Type: Unified Platforms Converge Stand-alone Tools

Video conferencing retained 28.21% communication software market share in 2025, but unified communication (UC) suites are growing fastest at an 18.1% CAGR as enterprises consolidate point tools. Developers embed email, chat, voice, and webinars inside broader workflow surfaces, enabling single sign-on, cross-channel presence, and AI-driven topic extraction. The communication software market size linked to unified suites is forecast to exceed USD 13.2 billion by 2031, outpacing point solution growth.

Microsoft’s integration of Teams with Dynamics, and Cisco’s Webex extension into contact-center and event-management domains demonstrate the gravitational pull toward one-stop platforms. At the same time, CPaaS players let product teams add context-specific messaging without forcing full suite adoption, ensuring coexistence of embedded and suite models. Social-network-style feeds are also gaining traction, bringing informal culture channels into formal communication workflows.

By Industry Vertical: Healthcare Acceleration Outpaces IT Leadership

IT and telecom led the communication software market in 2025 with 28.22% share, reflecting digital-native operations and early adoption maturity. Yet healthcare is projected to grow at 16.0% CAGR as telehealth, remote monitoring, and patient engagement initiatives place real-time communication at the heart of care delivery. Communication software market share gains in healthcare are bolstered by HIPAA-ready video and AI transcription, which help address clinician-burnout and patient-satisfaction metrics.

CHIME’s 2024 trends survey reports 95% of providers link communication quality to patient outcomes, but 36% remain dissatisfied with existing tools, signaling runway for growth. BFSI, manufacturing, and retail follow healthcare’s lead by aligning omnichannel customer experience M&Ates with compliance automation. Government and education sectors modernize legacy PBX and email stacks, attracted by grant-funded cloud migration programs that promise lower total cost of ownership.

Geography Analysis

North America dominated the communication software market with 38.02% revenue share in 2025 as enterprises embraced AI-enabled collaboration and robust regulatory frameworks ensured predictable security baselines. Vendor headquarters concentration fosters tight customer feedback loops, yet growth moderates as Fortune 500 saturation peaks. Providers now focus on differentiated analytics, vertical editions, and domestic data residency to defend renewal cycles.

Asia-Pacific is expanding at a 21.2% CAGR, catalyzed by sustained 5G roll-outs and proactive government AI roadmaps. The GSMA projects regional mobile subscribers will reach 2.1 billion by 2030, extending the communication software market’s addressable base dramatically. High linguistic diversity fuels demand for real-time translation and local compliance gateways. China’s national AI Plan and Singapore’s USD 1 billion AI spending accelerate enterprise interest in multilingual, sovereign-cloud-capable platforms. Emerging megacities further boost SMB adoption as digital marketplaces proliferate.

Europe represents a compelling but complex landscape where GDPR and data-sovereignty M&Ates shape vendor roadmaps. Providers offering in-region data centers and advanced encryption win disproportionate share, while slower macroeconomic growth tempers seat expansion. South America and the Middle East and Africa remain nascent yet promising: telecom-led digitization and startup ecosystems unlock new customer segments, but currency volatility and bandwidth gaps restrain full-scale UC adoption. Despite these hurdles, pilot projects around CPaaS and contact-center AI indicate that the communication software market will broaden geographically as infrastructure catches up.

Competitive Landscape

The communication software market is moderately concentrated, anchored by Microsoft, Zoom, Cisco, and Google yet punctuated by agile specialists targeting niches such as vertical compliance, AI analytics, and CPaaS. Microsoft leverages its productivity-suite halo effect, embedding Teams chat, voice, and meeting intelligence throughout Office workloads. Zoom defends user-experience leadership through continual latency reductions and AI note-taking, while Cisco intertwines Webex with network-security and observability assets, as highlighted by its USD 28 billion Splunk acquisition in 2025.

M&A shapes competitive boundaries. RingCentral acquired Mitel’s UC-aaS assets for USD 650 million to deepen voice expertise, and Twilio absorbs niche AI startups to reinforce CPaaS breadth. Startups focus on secure sovereign clouds, low-code integration, and AI-driven sentiment analytics to win departmental deals overlooked by incumbents. Vertical specialization intensifies: Smarsh targets financial-services compliance, Weave concentrates on healthcare front-office automation, and Lusha optimizes B2B sales intelligence.

Product roadmaps converge on AI copilots, predictive analytics, and workflow automation, raising the innovation bar while reducing feature differentiation gaps. As capabilities commoditize, vendors increasingly compete on ecosystem breadth, partner marketplaces, and regional compliance certifications. Price competition remains muted due to high switching costs, but feature velocity and bundled analytics reshape value perceptions across the communication software market.

Communication Software Industry Leaders

Microsoft Corporation

Zoom

Cisco Systems, Inc.

Salesforce, Inc.

Google

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Lusha acquired Novacy, a Tel-Aviv conversation-intelligence provider, to enhance AI-driven sales coaching.

- February 2025: Smarsh purchased CallCabinet, adding cloud-native compliance recording and analytics.

- May 2025: Weave Communications announced a USD 35 million deal to acquire TrueLark, accelerating AI receptionist capabilities in healthcare.

- June 2025: CallMiner bought VOCALLS to expand omnichannel AI automation for customer-service teams.

Global Communication Software Market Report Scope

Communication software facilitates remote system access and enables the exchange of files and messages be it text, audio, or video across various computers or users. This encompasses terminal emulators, file transfer applications, chat and instant messaging tools, and similar functionalities embedded within MUDs.

The study tracks the revenue accrued through the sale of the communication software solutions by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

Communication software market is segmented by deployment model (on-Premise, cloud), by enterprise size (large enterprises, small and medium enterprises), by type (email software, instant messaging software, social networking software, video conferencing software, voice over internet protocol software), by industry vertical (BFSI, manufacturing, retail, healthcare, IT and telecom, others), by geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| On-premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Email Software |

| Instant Messaging |

| Social Networking |

| Video Conferencing |

| Voice over IP (VoIP) |

| Unified Communication Platforms |

| Project Collaboration Tools |

| BFSI |

| Manufacturing |

| Retail and E-commerce |

| Healthcare and Life Sciences |

| IT and Telecom |

| Education |

| Government |

| Media and Entertainment |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN-5 | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | On-premise | ||

| Cloud | |||

| By End-user Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Communication Type | Email Software | ||

| Instant Messaging | |||

| Social Networking | |||

| Video Conferencing | |||

| Voice over IP (VoIP) | |||

| Unified Communication Platforms | |||

| Project Collaboration Tools | |||

| By Industry Vertical | BFSI | ||

| Manufacturing | |||

| Retail and E-commerce | |||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Education | |||

| Government | |||

| Media and Entertainment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| ASEAN-5 | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected size of the communication software market by 2031?

The communication software market is forecast to reach USD 26.58 billion by 2031, growing at a 15.08% CAGR.

Which deployment model shows the fastest growth?

Hybrid cloud solutions are expanding at a 18.6% CAGR as enterprises blend sovereign control with cloud scalability.

Why is Asia-Pacific considered the growth epicenter?

Aggressive 5G roll-outs, government AI investments, and a rising base of mobile subscribers are driving a 21.2% CAGR in the region.

Which industry vertical is expected to accelerate the most?

Healthcare leads with a 16.0% CAGR due to telehealth expansion and HIPAA-compliant video and messaging adoption.

How are cybersecurity requirements influencing vendor strategies?

Providers invest heavily in zero-trust architectures, encryption, and compliance automation to address first-year security costs of USD 385,000 for 10,000 seats.

Page last updated on: