Market Overview

| Study Period | 2020 - 2031 |

|---|---|

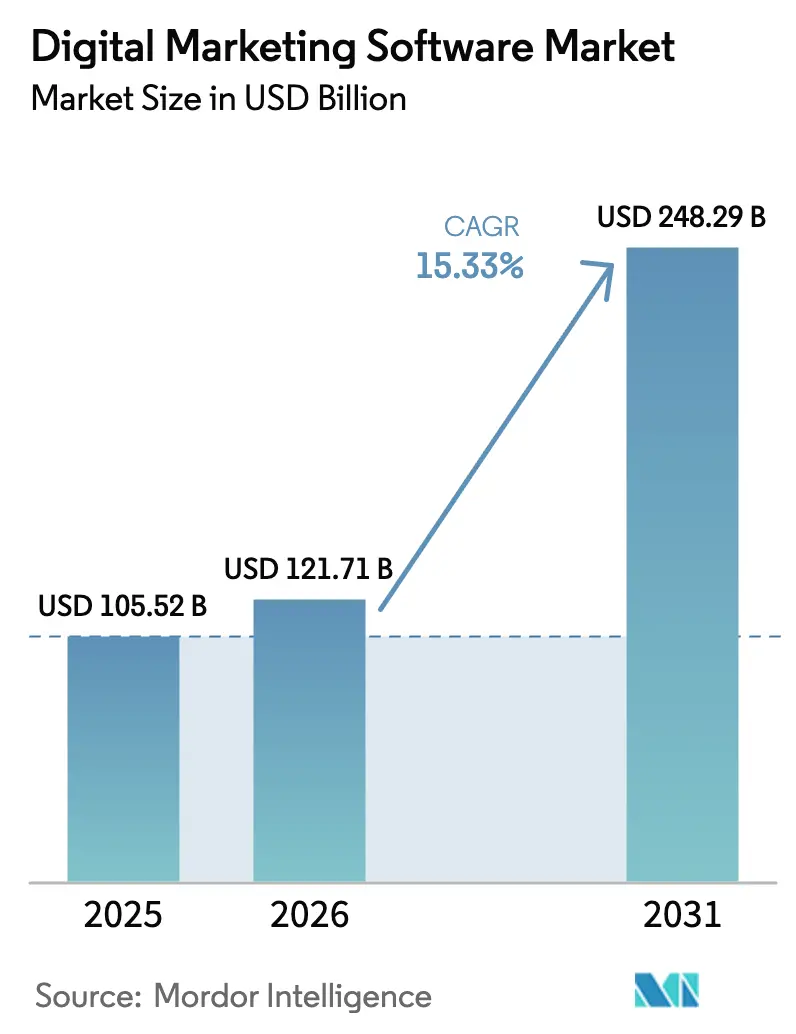

| Market Size (2026) | USD 121.71 Billion |

| Market Size (2031) | USD 248.29 Billion |

| Growth Rate (2026 - 2031) | 15.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Marketing Software Market Analysis by Mordor Intelligence

The Digital Marketing Software Market size is expected to increase from USD 105.52 billion in 2025 to USD 121.71 billion in 2026 and reach USD 248.29 billion by 2031, growing at a CAGR of 15.33% over 2026-2031. Heightened demand for generative-AI content engines, zero-party data strategies, and embedded modules inside vertical SaaS platforms has made the category one of the fastest-moving branches of enterprise applications. Cloud deployment, already the default delivery model, continues to widen its lead as budget owners shift capital expenditure to operating expenditure and as latency-sensitive edge architectures mature. Momentum is strongest among small and mid-sized enterprises because self-serve onboarding and usage-based pricing compress time-to-value, while services revenue is expanding faster than software as customers seek integration and change-management support. Vendors that couple marketing workflows with CRM, commerce, or payment capabilities are capturing early mindshare, whereas pure-play suites face lengthier sales cycles, steeper proof-of-concept requirements, and higher churn.

Key Report Takeaways

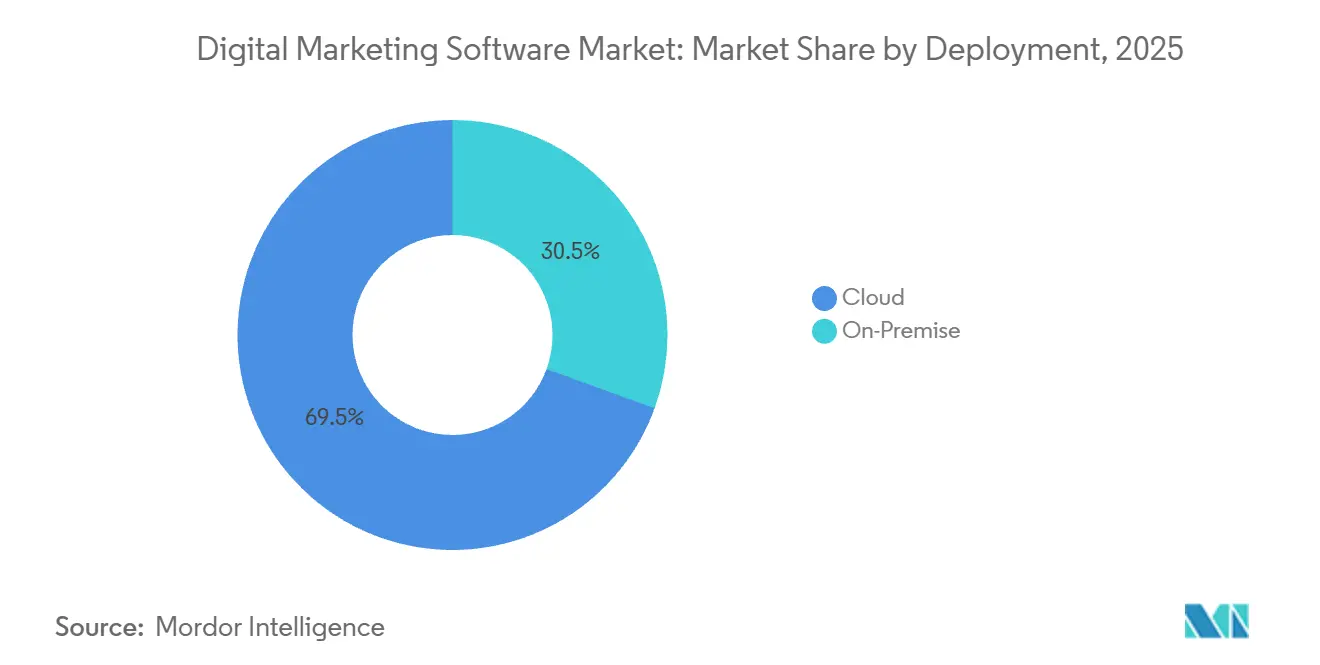

- By deployment, cloud solutions held 69.47% of digital marketing software market share in 2025, and the segment is forecast to expand at a 15.41% CAGR through 2031.

- By component, services revenue is advancing at a 16.13% CAGR, surpassing software licenses as enterprises budget for implementation and managed-service bundles. The software component held 60.13% of digital marketing software market share in 2025.

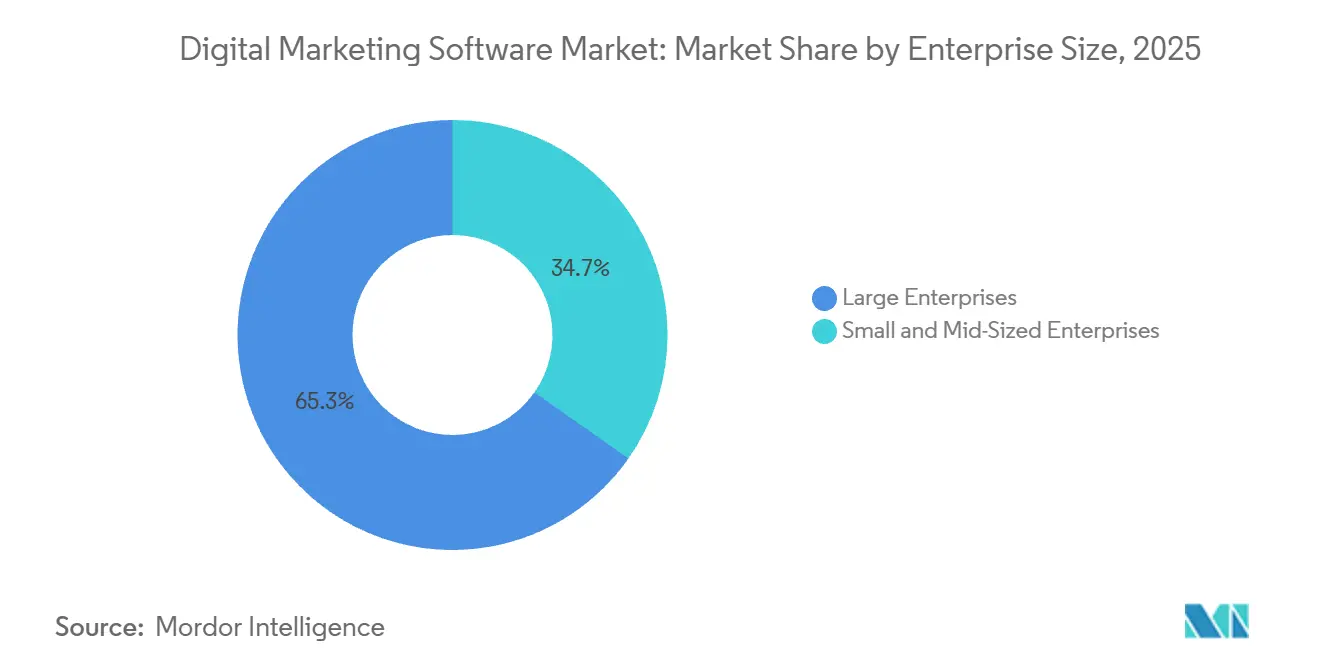

- By enterprise size, SMEs are projected to grow 15.64% annually through 2031, far outpacing large-enterprise outlays; large enterprises held 65.26% of digital marketing software market share in 2025.

- By end-user industry, healthcare and life sciences are expected to post the fastest 16.12% CAGR, while retail and e-commerce maintained a 28.29% revenue share in 2025.

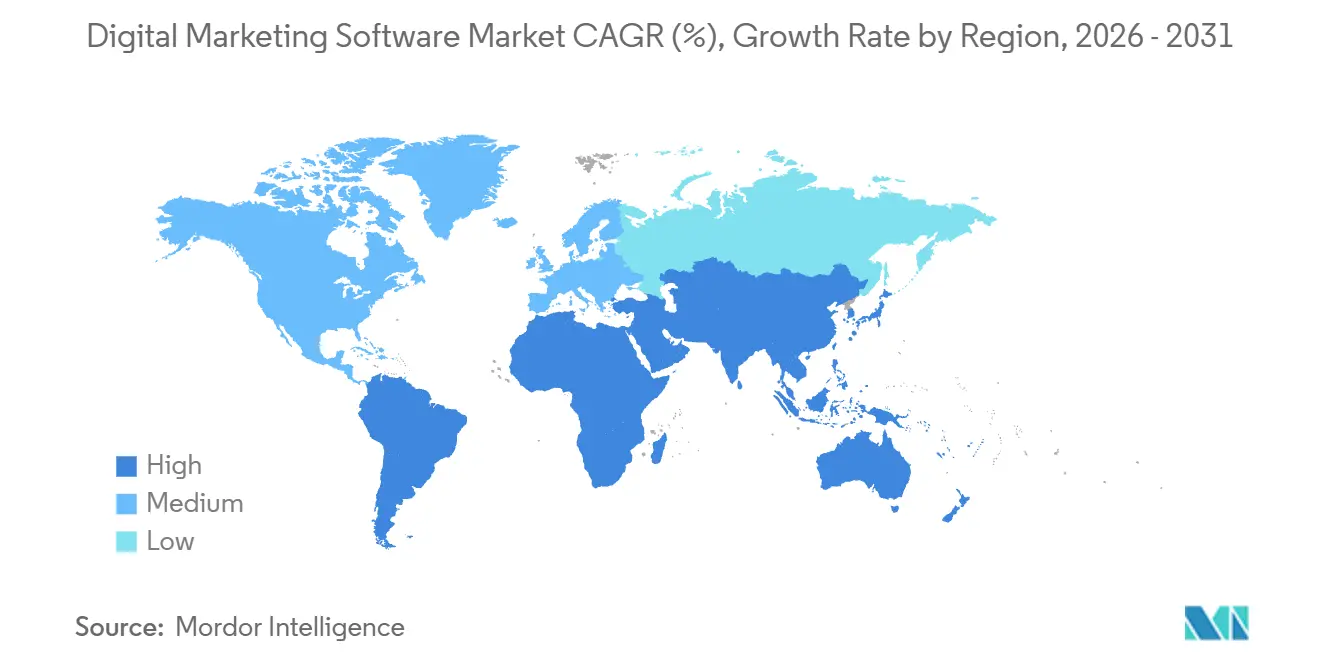

- By geography, North America contributed 35.54% of 2025 revenue, yet Asia Pacific is tracking a 16.27% CAGR on the strength of mobile-first commerce.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Digital Marketing Software Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Digital-First Customer Journeys | +3.2% | Global, with accelerated adoption in APAC and Middle East | Medium term (2-4 years) |

| Cloud-Native SaaS Cost Advantages | +2.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| AI-Powered Content and Campaign Optimization | +3.5% | Global, led by North America and APAC technology hubs | Medium term (2-4 years) |

| Omnichannel Engagement Demand from B2C and B2B | +2.6% | Global, with B2B concentration in North America and Europe | Medium term (2-4 years) |

| Zero-Party Data and Cookieless Personalization | +2.4% | Europe and North America core, expanding to APAC | Long term (≥ 4 years) |

| Embedded "One-Click" Marketing in Vertical SaaS and Payments Platforms | +2.1% | North America and APAC, spill-over to South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Powered Content and Campaign Optimization

Generative models are collapsing creative-production timelines from weeks to hours, letting marketers spin up localized ads, email sequences, and landing pages at scale without proportional headcount increases. Adobe embedded its Firefly engine into Experience Cloud in 2025 and reported 20-30% lower creative costs among early enterprise adopters.[1]Adobe Inc., “Firefly Integration Announcement,” adobe.com Salesforce exposed Einstein GPT across Marketing Cloud, boosting open rates 15-25% during pilots with retail and financial-services clients. Sectors with extensive product catalogs, including apparel, grocery, and consumer electronics, gain the most because manual asset creation breaks down past certain SKU counts. Yet data-science skills remain scarce, so vendors are monetizing managed services that package platform access with AI-strategy workshops. This services overlay explains why services revenue is rising faster than pure software subscriptions.

Zero-Party Data and Cookieless Personalization

Full Chrome cookie deprecation slated for late 2026 is forcing marketers to pivot toward volunteered data captured through preference centers, quizzes, and loyalty programs. Retailers such as Sephora and Nike deepened preference-center functionality in 2025, lifting email click-through rates 18-22% versus cookie-based cohorts. European enforcement of the Digital Markets Act standardized consent language, increasing compliance costs but also giving legal cover for uniform data-collection flows. Platforms that bundle consent orchestration with CDP capabilities (OneTrust, TrustArc, Adobe, Salesforce) see stronger renewals, while point solutions without native consent pipes risk latency that undercuts real-time personalization.

Surge in Digital-First Customer Journeys

Digital channels now drive more than 60% of customer interactions in banking, insurance, and B2B procurement, a ratio that has held steady since pandemic-era peaks. The permanence of online engagement is consolidating point solutions into unified clouds spanning email, SMS, push, and in-app messaging. HubSpot logged a 40% year-over-year jump in customers adopting its full-stack Marketing Hub during 2025. Industrial suppliers are following retail playbooks by layering account-based targeting and intent scoring atop standard lead-nurture tracks. Standalone email or social-publishing tools that lack workflow automation or CRM connectors face sliding renewal rates, while platforms that stitch marketing into broader customer-experience suites capture the bulk of expansion budgets.

Embedded One-Click Marketing in Vertical SaaS Platforms

Shopify, Square, GoDaddy, and other vertical SaaS players are baking marketing features directly into storefront, payment, and scheduling flows. Shopify merchants sent more than 10 billion messages through embedded Email and SMS modules in 2025, up 35% from 2024. Square added automated re-engagement campaigns tied to point-of-sale data, generating USD 200 million in incremental merchandise volume within six months. By collapsing the gap between transaction capture and campaign execution, these vendors win budgets before SMEs even evaluate standalone martech suites. Standalone platforms, therefore, race to deepen native connectors. Klaviyo’s real-time Shopify integration now syncs catalogs and order histories in seconds.

Restraints Impact Analysis of Digital Marketing Software Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity with Legacy Martech Stacks | -1.8% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Data-Privacy and Consent-Management Compliance Costs | -1.5% | Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Rising Unit Prices for First-Party Data Enrichment | -1.1% | Global, with higher impact in mature markets | Medium term (2-4 years) |

| CX Talent Shortage for AI-Led Campaign Design | -0.9% | Global, acute in North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy Martech Stacks

Enterprises commonly run 15-30 discrete marketing tools, and every additional API or schema mismatch compounds maintenance overhead. Monolithic suites built a decade ago often lack modular, API-first design, forcing IT teams to craft brittle connectors that break on vendor updates. Financial-services and healthcare organizations face added hurdles because audit trails and lineage tracking must span every system. Composable CDP architectures from providers such as Segment and mParticle offer a path to standard data pipes, yet uptake is slow where entrenched ERP or CRM deployments resist structural change. High integration cost therefore acts as a switching deterrent, bolstering incumbent renewal rates even when feature depth lags newer entrants.

Data-Privacy and Consent-Management Compliance Costs

Regulatory divergence across GDPR, CPRA, LGPD, and PIPL obliges multinationals to maintain region-specific pipelines for consent, storage, and deletion. Design teams must rebuild interfaces to avoid “dark patterns,” and engineering teams must enforce real-time consent checks before data activation. Penalties of up to 4% of global revenue under GDPR encourage conservative rollouts that delay campaign launches and shrink addressable segments. Vendors with certified consent modules bundled into their clouds reduce customer effort, whereas mid-market point solutions lacking legal resources either pivot to less-regulated verticals or absorb margin compression to fund compliance roadmaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Digital Marketing Software Market Segment Analysis

By Deployment:

Cloud Dominance Accelerates with Edge ComputingCloud-based offerings accounted for 69.47% of digital marketing software market share in 2025 and are on track for a 15.41% CAGR through 2031, reinforcing the asset-light preference of new buyers. Microsoft added more than 5,000 net-new Dynamics 365 Marketing accounts during 2025, many of which were migrating from on-premise systems.[2]Microsoft Corp., “Dynamics 365 Marketing Customer Growth,” microsoft.com On-premise stacks linger in regulated verticals that mandate data residency, but hybrid architectures now route analytics and campaign execution to the cloud while retaining sensitive identifiers on-site, blurring historical boundaries.

Edge deployments form a nascent third pillar, particularly for latency-sensitive personalization scenarios such as kiosk recommendations or in-app offers that cannot tolerate round-trip network delays. Salesforce and Adobe both pilot edge caches that store lightweight customer profiles locally, promising millisecond-level decisioning at point of interaction. If adoption broadens, the digital marketing software market size attributable to edge nodes could carve out a distinct revenue stream within five years.

By Component:

Services Surge as Integration Demands EscalateSoftware licenses still generated 60.13% of revenue in 2025, yet services lines such as implementation, integration, training, and managed campaigns are accelerating at a 16.13% CAGR. Accenture scaled its marketing-technology workforce by 2,000 specialists during 2025 to meet demand for Adobe, Salesforce, and Oracle rollouts. AI-heavy engagements command premiums because model tuning, feature engineering, and MLOps oversight exceed traditional configuration scope.

Vendors increasingly embed onboarding and success managers inside subscription tiers, converting one-time fees into recurring services annuities. This format stabilizes monthly recurring revenue and simplifies procurement for customers that prefer a single invoice. Over time, service-attached contracts could lift gross margin volatility, though they also raise capacity-management risk for vendors that lack global delivery footprints.

By Enterprise Size:

SMEs Drive Volume GrowthLarge enterprises retained 65.26% of 2025 spend, while SMEs are the fastest-growing cohort, with a 15.64% CAGR through 2031. Mailchimp, now inside Intuit, counted more than 13 million active users last year, 90% of whom are classified as SMEs. Zoho Marketing Plus, priced at USD 50 per month, added 8,000 accounts in 2025.

Drag-and-drop builders, freemium tiers, and template libraries lower the skills barrier, while usage-based pricing aligns cost with cash flow. As SME platforms mature, they begin layering governance, audit, and single-sign-on features that appeal to mid-market firms, potentially compressing the enterprise ASP premium that incumbents enjoy today.

By End-User Industry:

Healthcare Leads Growth as Retail MaturesRetail and e-commerce accounted for 28.29% of revenue in 2025, underpinned by large SKU catalogs and promotional cadences that require automated testing. However, persistent margin compression is shifting focus from broad-reach campaigns to loyalty-data-driven micro-segmentation. The healthcare and life-sciences segment is forecast to post a 16.12% CAGR, the fastest in the forecast window, aided by policy updates that allow direct-to-patient outreach under tighter consent frameworks and by pharmaceutical companies automating clinical-trial recruitment.

Pfizer and Novartis both deployed AI-enabled patient-engagement platforms in 2025, trimming trial enrollment timelines by nearly one-quarter. Banking, telecom, and media each represent between 12-18% of revenue, with financial institutions prioritizing audit-ready consent logs and broadcasters unifying subscription and ad-inventory data. Manufacturing, once a laggard, is adopting configurators and instant quoting, pulling CRM and marketing closer together.

Geography Analysis

North America Digital Marketing Software Market

North America contributed 35.54% of global revenue in 2025. Market maturity means most Fortune 500 companies have already rationalized sprawling stacks into two or three core platforms. Growth now pivots on optimization modules AI asset generation, real-time CDPs, and journey analytics and on mid-market rollouts in Canada and Mexico. California’s CPRA keeps privacy engineering top of mind, while the pending American Data Privacy and Protection Act may add federal oversight. Cross-border data flows remain relatively smooth inside the United States-Mexico-Canada corridor, accelerating regional vendor deployments.

APAC Digital Marketing Software Market

Asia Pacific is expanding at a 16.27% CAGR through 2031, faster than any other region, propelled by mobile-first commerce across India, Indonesia, Vietnam, and the Philippines. Smartphone penetration above 70% and rising disposable income are steering ad budgets from social-network auctions toward owned marketing clouds that minimize dependency risk. Domestic Chinese vendors dominate inside mainland borders due to PIPL localization mandates, yet Japanese and South Korean enterprises exhibit high adoption of global suites with localized compliance extensions. ASEAN startups gravitate to pay-as-you-grow pricing, making the region a laboratory for tiered usage models that could eventually filter into mature markets.

EMEA and South America Digital Marketing Software Market

Europe accounted for roughly 28% of 2025 spend. GDPR enforces strict consent regimes, prompting steady demand for platforms with built-in audit trails and geographic data fences. Germany, France, and the United Kingdom remain the largest contributors, while the Nordics display outsized AI module uptake relative to population. Southern European adoption trails because of legacy infrastructure and smaller IT budgets, although tourism and retail digitization programs are narrowing the gap. The Middle East and Turkey are investing under national diversification plans, and Brazil anchors South American demand despite currency volatility. Africa’s nascent markets rely on mobile-money rails to join digital commerce, offering greenfield upside for light-weight, cloud-native suites.

Regulatory Landscape

Digital marketing software vendors operate under an increasingly prescriptive privacy and online-safety framework that affects identity resolution, profiling, and cross-channel activation. In the European Union, GDPR remains the core rulebook for consent, purpose limitation, and data subject rights, increasing operating requirements for consent logs, deletion workflows, and audit trails used in campaign execution. In the United States, the Federal Trade Commission has continued to sharpen enforcement signals around children s data, including a February 2026 policy statement encouraging age-verification approaches under the COPPA Rule, which shapes ad targeting and personalization features where age gating is required.

The compliance perimeter is also expanding into AI governance as marketing suites embed generative and agentic capabilities. The EU Artificial Intelligence Act (Regulation (EU) 2024/1689) entered into force in 2024 and moves toward fuller application phases, with provisions relevant to general-purpose AI and transparency expectations. This is pushing vendors to add model documentation, risk controls, and monitoring into marketing workflows. Alongside this, EU institutions and regulators (for example, EDPB and EDPS through Joint Opinion 2/2026 on a Digital Omnibus proposal) have highlighted efforts to streamline overlaps between GDPR, AI-related rules, and adjacent digital legislation, reinforcing the need for harmonized controls across identity, consent, and AI-enabled content generation.

Value Chain Analysis

The digital marketing software value chain starts with data capture and identity inputs (first-party web and app events, CRM records, commerce and payment data, and consent and preference-center signals) and proceeds through data unification layers such as CDPs, integration middleware, and analytics. Upstream, cloud infrastructure and AI tooling provide the compute and model services used for segmentation, content generation, and experimentation. Midstream, core platforms deliver orchestration across channels (email, SMS, push, web, social, search) while connecting to ad-tech systems (ad servers, DSPs, SSPs) and to enterprise systems such as ERP and order management to support inventory-aware promotions.

Downstream, activation and measurement rely on connectors, APIs, and services partners that implement schema mapping, governance, and change management in complex stacks, particularly when enterprises run 15-30 tools. A recurring bottleneck is the gap between campaign optimization signals and operational capacity, when ad platforms optimize to conversions without real-time inventory and fulfillment visibility, which can lead to wasted spend and weaker customer experience. Recent ecosystem moves also point to consolidation and capability layering across the chain, including Adobe's completion of the Semrush acquisition in April 2026 to deepen SEO and brand visibility capabilities, and MoEngage's June 2026 acquisition of Aampe to embed autonomous decisioning into engagement platforms, reinforcing a shift toward integrated, AI-driven orchestration rather than isolated point tools.

Competitive Landscape

The five largest vendors, Adobe, Salesforce, Oracle, Microsoft, and Google, command a combined major share of 2025 revenue, indicating moderate concentration. Adobe couples the Experience Cloud with the Creative and Document Clouds, making switching an expensive, multi-workstream exercise. Salesforce leverages acquisitions such as Tableau, MuleSoft, and Slack to cross-sell analytics, integration, and collaboration, inflating customer lifetime value by up to one-third. Google’s ad-tech heritage gives it data-science heft, though enterprise buying centers sometimes balk at channel conflict between Google marketing additional services and in-house teams.

Challengers such as HubSpot, Klaviyo, and Braze compete on ease of use, transparent pricing, and rapid implementation. Their composable APIs slot into headless commerce and custom CRM back ends, resonating with product-led growth companies unwilling to adopt monolithic suites. Vertical SaaS entrants capture green-field budgets by embedding marketing features at the point of payment or booking, often before merchants realize they are adopting martech.

Emerging disruptors exploit edge computing and event-stream dataflows, letting clients toggle best-of-breed modules in or out as objectives evolve. Segment, now inside Twilio, routes more than 400 billion monthly API calls that feed analytics, personalization, and support tools without duplicate data pipes. Adobe lodged 47 AI-focused patents during 2025, covering image generation, tone adaptation, and predictive personalization.[3]United States Patent and Trademark Office, “Adobe AI Patent Filings,” uspto.gov Sustained R&D investment will likely intensify the gulf between full-suite leaders and mid-tier vendors that lack comparable engineering budgets.

Digital Marketing Software Industry Leaders

Adobe Inc.

Salesforce Inc.

Oracle Corporation

SAP SE

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Digital Marketing Software Market Companies Covered in this Report

- Adobe Inc.

- Salesforce Inc.

- Oracle Corporation

- SAP SE

- Microsoft Corporation

- Google LLC

- IBM Corporation

- HubSpot Inc.

- SAS Institute Inc.

- Teradata Corp.

- Criteo SA

- Infor Inc.

- ActiveCampaign LLC

- Klaviyo Inc.

- Intuit Inc.

- Brevo SAS

- Zoho Corporation

- Constant Contact

- Sitecore

- Acoustic, L.P.

- Insider Inc.

- Sprinklr

- Braze Inc.

- Shopify Inc.

- Hootsuite Inc.

- Block, Inc.

- GoDaddy Inc.

Market Opportunities and Future Outlook

Agentic marketing creates a whitespace for platforms that can orchestrate multi-step work across content, campaigns, data access, and measurement without forcing full data replication across systems. Vendor actions in 2026 provide clear signals of this direction. Shopify launched Campaign Autopilot in June 2026 to manage campaigns across Meta, Shop, and email from within the commerce workflow, while Google introduced Gemini-powered features for Indian businesses in July 2026, including a Business Agent for Leads that enables chat between users and advertisers directly within search results. Together, these moves point to demand for embedded marketing execution inside transaction and discovery surfaces, especially among SMEs that prefer native tools in commerce and productivity platforms.

Governance-first marketing operations are another near-term opportunity. Consent management, access control, and audit logging are becoming operational prerequisites for AI-assisted content creation and personalization under tighter privacy and child-safety scrutiny. As cookie deprecation approaches late 2026, zero-party data capture and consent orchestration are driving demand for packaged preference centers, compliant experimentation, and durable identity resolution across channels. On the enterprise side, unified content infrastructure and brand visibility tooling are gaining priority as discovery shifts toward AI search experiences, supported by Adobe's June 2026 introduction of Brand Visibility for the AI search era and by ongoing efforts to connect marketing data and content layers to broader customer experience stacks.

Recent Industry Developments in Digital Marketing Software Market

- July 2026: Salesforce released a major update to Agentforce Commerce, expanding AI-agent capabilities that automate commerce and marketing workflows. The release reinforces the shift from rule-based automation to agent-led execution across customer journeys, increasing pressure on competing suites to match cross-channel orchestration depth.

- June 2026: Adobe introduced Adobe Brand Visibility, positioning the offering for measurement and optimization in AI-mediated discovery across platforms such as ChatGPT, Microsoft Copilot, and Perplexity AI. The product extends marketing software beyond campaign execution into generative engine optimization, tying brand performance to emerging AI search and assistant surfaces.

- March 2024: Adobe and Microsoft announced a partnership to bring generative AI capabilities to marketers inside Microsoft 365 applications. The integration direction elevated productivity-suite entry points as a distribution channel for marketing creation and workflow execution, supporting embedded adoption among teams that already operate in Microsoft environments.

Digital Marketing Software Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market is defined as revenue earned from digital marketing software and related support services that help organizations plan, run, measure, and optimize marketing across web, mobile, email, social, and search channels, including cloud and on-premise deployments.

Scope exclusions: Advertising agency services, outsourced creative production, and stand-alone analytics tools that do not support campaign execution are not counted.

Segments Covered in This Report

- By Deployment

- Cloud

- On-Premise

- By Component

- Software

- Services

- By End-User Enterprise Size

- Large Enterprises

- Small and Mid-Sized Enterprises

- By End-User Industry

- IT and Telecom

- Media and Entertainment

- BFSI

- Retail and E-Commerce

- Manufacturing

- Healthcare and Life Sciences

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Australia and New Zealand

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the market boundaries, understand adoption patterns, and anchor the demand drivers that shape software spending. We refer to public sources such as the US Bureau of Economic Analysis, US Census Bureau, Eurostat, OECD digital economy releases, and the International Telecommunication Union for consistent macro and digital activity indicators.

To translate those indicators into software demand signals, we also review company annual reports and investor decks, product documentation, pricing pages, and reputable press coverage around platform changes and privacy rules. When needed, we use paid subscriptions for company financials and intelligence, news and financials, and patent databases to verify revenue exposure, product scope, and product launch timing. These desk research sources are illustrative only, and many other public and paid references were used during data collection and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what we see in desk findings, especially around packaging, discounting, and what buyers include inside a "digital marketing software" budget line. We spoke with a mix of platform providers, channel partners, and enterprise and SMB users across major regions, and then reconciled differences through follow-up questions on deployment mix, renewal behavior, and typical module attach rates.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 14% | APAC: 45% |

| Mid tier: 52% | Functional/Unit leaders: 39% | EMEA: 35% |

| Smaller Players: 21% | Managers: 47% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where regional software spend is reconstructed using digital ad activity, cloud adoption intensity, and marketing technology penetration by enterprise size, and then mapped back into the defined scope. Once this picture is formed, we corroborate it with selective bottom-up checks, such as sampled price-to-seat ranges, module bundle patterns, and channel partner feedback on deal sizes, which are then used to adjust outliers.

The model is guided by practical variables that change spending year to year, including digital advertising spend levels, active internet and smartphone user base trends, email and social channel usage, cloud versus on-premise mix, and renewal and churn behavior in subscription contracts. For forecasting, scenario analysis is applied so that different assumptions on privacy enforcement, AI-driven workflow adoption, and budget tightening can be tested, and then aligned to what interviewees view as realistic over the next few years. Where bottom-up signals are incomplete for smaller countries or niche modules, gaps are handled by using regional proxies tied to business counts and digital intensity, followed by a consistency check against total addressable marketing software spend.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals, such as regional software spending direction, disclosed revenue mix cues in filings, and observed pricing and packaging shifts, before the final totals are accepted. Variances are flagged when growth rates or regional splits move outside expected ranges, and then the assumptions are reworked and rechecked in a second analyst review.

The report is refreshed annually, and interim updates are made when material events affect pricing, currency movement, or major platform capability changes. Before delivery, a final pass is done to revalidate key inputs and to re-contact sources when the latest market signals do not line up with the prior model run.

Mordor Intelligence's Digital Marketing Software Market Estimate Compared With Other Published Estimates

Published market sizes for digital marketing software rarely match one another because the boundary of what is counted can shift, and because the same year can be measured with different currency timing and pricing assumptions. Differences also show up when some studies mix in adjacent spend lines that buyers treat separately, like agency services or non-execution analytics tools.

A common gap driver is refresh cadence, where late-year contract resets, discounting, and cloud price changes can materially move the current-year value if not rechecked close to publication. Another driver is ASP logic, since seat-based pricing, usage-based add-ons, and bundled modules can be treated differently, and then scaled across regions with uneven discount norms and FX conversion dates. By revalidating price progression and FX timing during the final update cycle, Mordor Intelligence keeps the 2025 estimate closer to what buyers actually paid in that year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 105.52 B (2025) | |

| Global Research Publisher A | USD 92.11 B (2025) | Often applies a more conservative pricing curve and may treat some modules and services as optional add-ons that are not consistently counted across countries, which can pull down the current-year total. |

| Industry Analytics Firm B | USD 86.27 B (2025) | Uses a different base build and forecast framing that can understate late-year renewals and bundle attach rates, and it may apply FX conversion at a different point in the year, which shifts reported USD value. |

Across the three figures, most of the spread can be traced to how quickly pricing and currency assumptions are refreshed and to where the line is drawn between execution platforms and adjacent spend. With clear inclusions, repeatable inputs, and checks tied to pricing and renewal behavior, the resulting number stays transparent and easier to reconcile to real buying patterns.

Key Questions Answered in the Report

How large is the global digital marketing software market in 2026?

The digital marketing software market size stood at USD 121.71 billion in 2026.

What CAGR is projected for digital marketing software between 2026 and 2031?

Revenue is forecast to grow at 15.33% annually through 2031.

Which segment of digital marketing software grows fastest, software or services?

Services are expanding at a 16.13% CAGR as buyers seek integration and managed support.

Why are SMEs adopting digital marketing platforms so rapidly?

Self-serve onboarding, freemium tiers, and usage-based pricing lower technical and financial barriers, yielding a 15.64% CAGR for SME spend.

Which end-user industry is expected to post the strongest growth?

Healthcare and life sciences lead with a projected 16.12% CAGR through 2031.

Which region offers the highest growth rate for vendors?

Asia Pacific is forecast to grow 16.27% per year, driven by mobile-first commerce and local SaaS adoption.

Page last updated on: