Custom Software Development Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

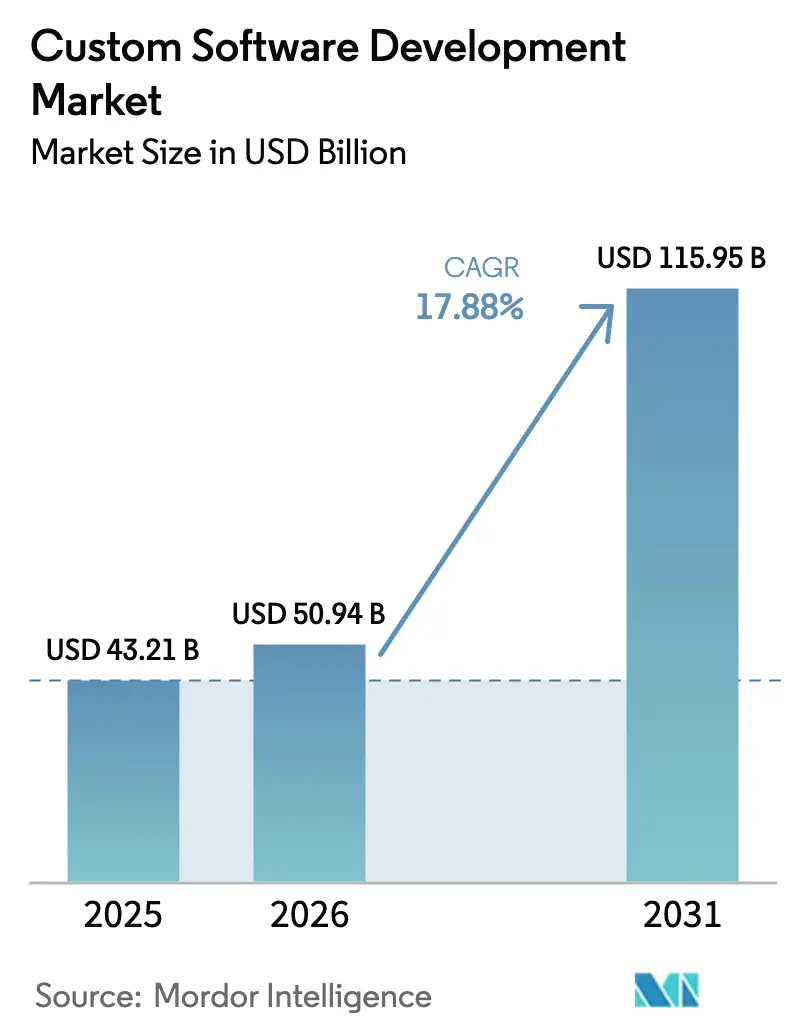

| Market Size (2026) | USD 50.94 Billion |

| Market Size (2031) | USD 115.95 Billion |

| Growth Rate (2026 - 2031) | 17.88% CAGR |

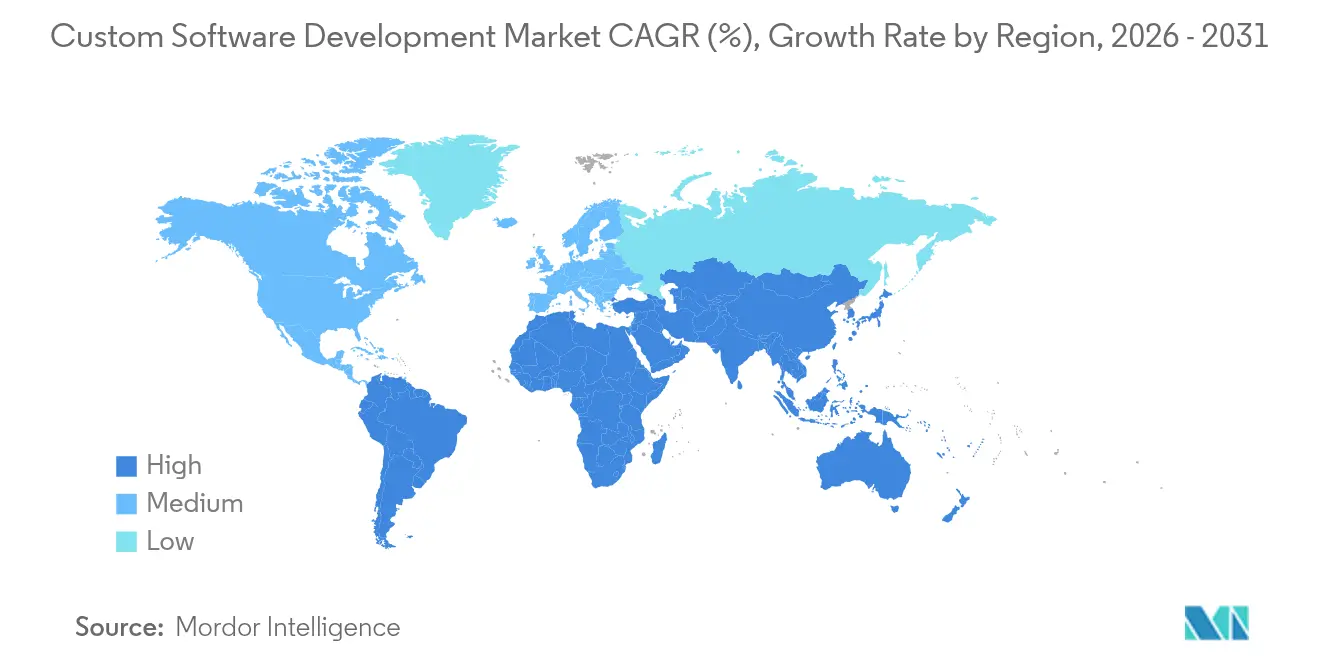

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Custom Software Development Market Analysis by Mordor Intelligence

Custom software development market size in 2026 is estimated at USD 50.94 billion, growing from 2025 value of USD 43.21 billion with 2031 projections showing USD 115.95 billion, growing at 17.88% CAGR over 2026-2031. Strong growth reflects enterprises’ migration from packaged applications toward highly tailored solutions that meet specific business process, compliance and differentiation goals. Mandatory software-supply-chain security requirements, rapid generative-AI adoption in coding workflows and a sharp increase in edge-computing projects are expanding the addressable opportunity. Heightened developer productivity through AI tools, combined with cloud-native architectures and micro-services, is shortening release cycles while raising demand for specialized skills. Regional investment incentives and vertical digital-transformation budgets are further supporting the custom software development market.

Key Report Takeaways

- By solution, enterprise software led with 36.60% revenue share in 2025; embedded and IoT software is set to advance at a 22.35% CAGR to 2031.

- By deployment model, cloud-hosted solutions captured 61.40% of the custom software development market share in 2025 while growing at a 21.10% CAGR through 2031.

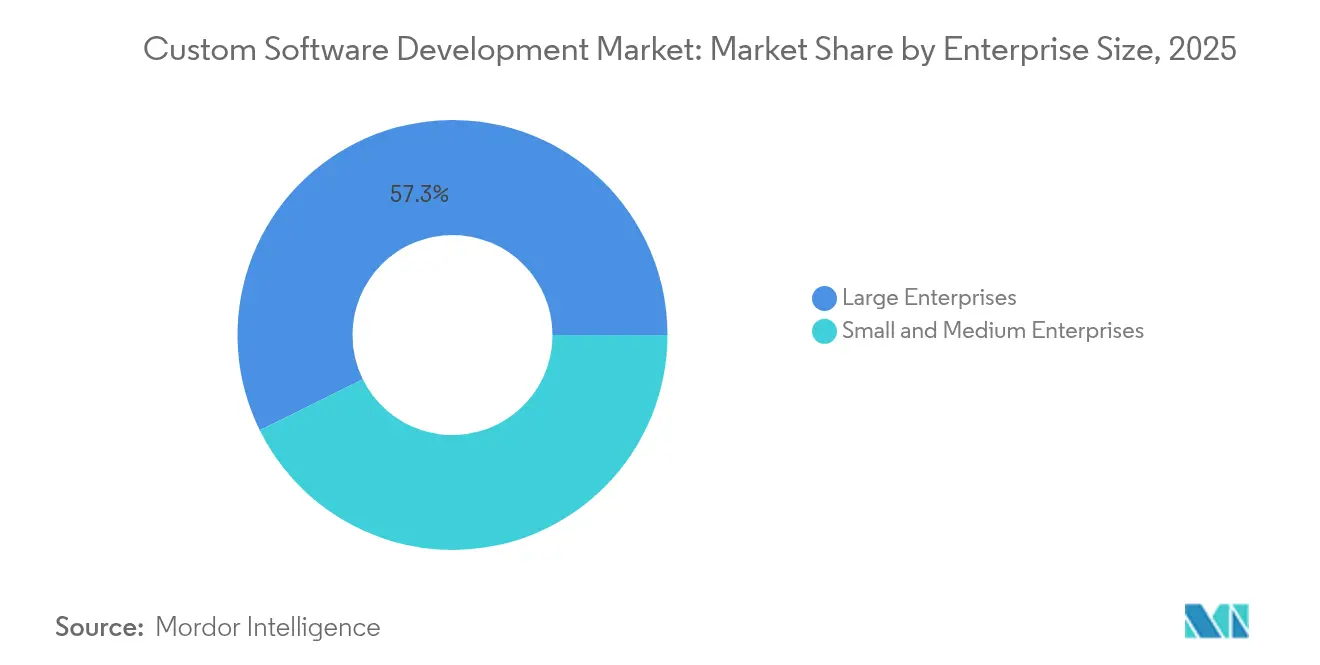

- By enterprise size, large enterprises held 57.30% share of the custom software development market size in 2025; SMEs are projected to expand at a 20.15% CAGR between 2026 and 2031.

- By end-user vertical, BFSI commanded 23.70% revenue share in 2025, but healthcare and life sciences is forecast to grow at 19.95% CAGR to 2031.

- By geography, North America accounted for 38.60% of 2025 revenue; Asia-Pacific is expected to post the fastest regional CAGR at 20.90% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Custom Software Development Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Digital transformation programs across verticals | +4.2% | Global, with early gains in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Cloud-native and micro-services architecture uptake | +3.8% | North America and EU, spill-over to APAC | Short term (≤ 2 years) |

| Integration of advanced analytics, ML and Gen-AI coding tools | +5.1% | Global, concentrated in tech-forward markets | Short term (≤ 2 years) |

| Proliferation of IoT edge deployments | +2.9% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Low-code / No-code platform proliferation | +1.8% | Global, particularly SME-heavy regions | Long term (≥ 4 years) |

| SBOM-centric software-supply-chain compliance mandates | +0.4% | North America, Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation Programs Across Verticals

Enterprise investment in modernizing core operations is steering software budgets toward bespoke solutions that embed sector-specific workflows. Global IT spending is projected at USD 4.5 trillion for 2025, with individual enterprises allocating an average USD 33 million to modernization projects.[1]Integrio Systems, “The Cost to Implement Digital Transformation in 2024,” integrio.net Case evidence from SBI Bank shows a 400% lift in lead conversion and a 90% reduction in loan-processing time after deploying a custom CRM platform. Similar momentum is visible in manufacturing, where PPG’s polymer plants are capturing an additional USD 400,000 in monthly revenue thanks to custom digital-twin applications. Such outcomes highlight why the custom software development market continues to secure priority funding across industries.

Cloud-Native and Micro-Services Architecture Uptake

Organizations pursuing agility and cost optimization are refactoring monolithic systems into containerized micro-services that release multiple times per day. Elite DevOps teams now push production changes in under 24 hours, a feat enabled by cloud-native patterns.[2]Google LLC, “Re Architecting to Cloud Native,” cloud.google.com This shift creates a sizeable customization workload around service mesh design, continuous-integration pipelines and API governance. Singapore’s Land Transport Authority achieved 60% cost savings through phased cloud migration, demonstrating real-world efficiency gains. Providers skilled in incremental modernization strategies are therefore well positioned to capture premium engagements within the custom software development market.

Integration of Advanced Analytics, ML and Gen-AI Coding Tools

Generative-AI copilots are writing up to 30% of new code, making development teams faster yet simultaneously introducing novel security risks. Accenture secured USD 3 billion in generative-AI bookings during 2024[3]Accenture plc, “Value from Every Angle and is upskilling talent to meet rising demand. Enterprises adopting AI-augmented workflows cite shorter sprints and lower defect rates, but also invest heavily in model validation and secure coding practices to offset hallucination-risk exposure. Vendors capable of pairing AI productivity with robust DevSecOps are gaining share in the custom software development market.

Proliferation of IoT Edge Deployments

Global IoT revenue is projected to reach USD 1.8 trillion by 2028, with 72% arising from enterprise use cases that require specialized edge software. Embedded-system complexity spurs demand for real-time analytics, RISC-V porting and 5G-enabled data orchestration. Bharat Forge’s adoption of an industrial IoT platform cut unplanned downtime to zero and lifted equipment effectiveness by 15%. These deployments are fueling the fastest-growing segment of the custom software development market.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising security and privacy breaches | -2.1% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Persistent shortage of senior developers | -3.4% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Tight IT-investment budgets at SMEs | -1.7% | Global, concentrated in emerging markets | Medium term (2-4 years) |

| Open-source "good-enough" alternatives cannibalising demand | -0.8% | Global, particularly cost-sensitive segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Security and Privacy Breaches

High-profile supply-chain attacks and executive orders mandating strict SBOM compliance are elongating testing cycles and raising project costs. Executive Order 14144 now obliges federal contractors to align with NIST secure-software standards, directly influencing vendor-selection criteria. Enterprises are adopting zero-trust architectures and code-signing protocols, but SMEs often lack budget for dedicated security teams, tempering adoption velocities in segments of the custom software development market.

Persistent Shortage of Senior Developers

An estimated 1.2 million developer roles will remain unfilled in the United States alone by 2026, with demand for AI and cybersecurity skills outpacing supply increases. Top providers counter the gap by expanding near-shore delivery centers and automating repeatable tasks through AI copilots. Nonetheless, rising wage inflation and longer recruitment cycles push up total-cost-of-ownership for buyers and could constrain some custom projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Enterprise Software Drives Market Leadership

Enterprise software retained the largest share at 36.60% in 2025, confirming the preference for sophisticated ERP, CRM and industry-specific suites that embed proprietary workflows. Web-based solutions hold the second-largest position, thanks to cross-platform progress in progressive-web-app frameworks. The embedded and IoT category is, however, scaling fastest at 22.35% CAGR as Industry 4.0 initiatives demand sensor-rich edge applications. Embedded deployments are drawing heightened interest in automotive and medical-device manufacturing, a trend expected to raise this segment’s contribution to the custom software development market size through 2031.

Momentum in embedded systems is tied closely to digital twin and predictive-maintenance rollouts. Emerson Electric’s deployment of plant-level twins illustrates how real-time production analytics can lift throughput while lowering waste. Development vendors that master secure firmware updates and AI inferencing at the edge will exert outsized influence over future custom software development market share.

By Deployment Model: Cloud-Hosted Solutions Accelerate

Cloud-hosted installations represented 61.40% of revenue in 2025 and are expanding at a 21.10% CAGR to 2031. This dominance is underpinned by scalable infrastructure, usage-based pricing and integrated DevOps tooling that reduce time-to-value. On-premise workloads persist in heavily regulated settings, yet hybrid-cloud blueprints now satisfy most sovereignty requirements, which further propels cloud adoption within the custom software development market.

Financial-services examples such as BPER Banca reveal operational and experiential gains from multi-channel, cloud-native platforms. Healthcare organizations including Florida Blue have recorded 40% faster transaction processing after modernization. These proofs of concept position cloud-first strategies as default choices for new custom builds.

By Enterprise Size: SMEs Emerge as Growth Engine

Large enterprises still account for 57.30% of worldwide spend; nonetheless, SMEs show the highest growth trajectory at 20.15% CAGR. Low-code and no-code environments are democratizing software creation, enabling smaller firms to launch tailored applications without full-stack teams. Gartner projects that 70% of new business apps will rely on these platforms by 2025, a dynamic that expands the user base for the custom software development market.

Australian SMEs highlight the pattern, prioritizing cost-reduction while coping with mounting IT complexity. Vendors bundling advisory and managed services with modular code accelerators are securing footholds in this underserved yet rapidly scaling market layer.

By End-User Vertical: Healthcare Accelerates Past BFSI Leadership

BFSI led with 23.70% of 2025 revenue, propelled by risk-management mandates and omnichannel banking. Heightened regulatory oversight, including the EU’s Digital Operational Resilience Act, sustains ongoing investment in bespoke applications. Healthcare and life sciences, rising at 19.95% CAGR, are expected to overtake BFSI by 2031 owing to interoperability mandates and AI-enabled diagnostics. Telehealth platforms, EHR integration and clinical-decision tools rank high on hospital CIO agendas, driving incremental demand in the custom software development market.

Manufacturing maintains steady growth, energised by Industry 4.0 and quality-analytics imperatives. Retail and e-commerce actors seek personalization engines, while public-sector spending is rising on citizen-service digitization projects. Together, these trends underpin diverse, resilient demand patterns across verticals.

Geography Analysis

North America contributed 38.60% of global revenue in 2025 and remains the largest regional buyer, supported by deep enterprise tech budgets and an advanced venture-capital ecosystem. Accenture alone generated USD 30.7 billion in North American revenue during fiscal 2024, illustrating the region’s capacity for large-scale engagements. Mandatory SBOM documentation and executive orders on secure-software development are fuelling additional service demand.

Asia-Pacific is expanding fastest at 20.90% CAGR as massive digitization programs and manufacturing investments converge. India’s TCS logged USD 7.51 billion in Q1 FY2025 revenue, with domestic growth of 61.8%, demonstrating robust in-region momentum. China’s focus on open-source AI frameworks and Singapore’s successful cloud migrations are further raising regional spend on custom development.

Europe shows steady progression anchored in data-sovereignty legislation and sustainability mandates. Hybrid-cloud adoption and privacy-by-design requirements create lucrative niches for specialized providers. Latin America’s near-shore sector benefits from time-zone alignment with North America, while Middle East and Africa initiatives around smart-city infrastructure and e-government services cultivate early-stage opportunities, though macroeconomic volatility tempers pace.

Competitive Landscape

The custom software development industry remains moderately fragmented. Accenture, TCS, Cognizant, Capgemini and IBM headline the global tier, leveraging broad service portfolios, global delivery centers and ecosystem partnerships. Mid-market and regional specialists differentiate through domain expertise in AI, quantum-safe cryptography and sustainability analytics. Acquisition strategies are accelerating: Cognizant added more than 6,500 engineers by closing the USD 1.3 billion Belcan deal, bolstering its aerospace and defense presence. Capgemini purchased Syniti to enhance data-management scope, while IBM’s planned buyout of Applications Software Technology LLC strengthens public-sector Oracle capabilities.

AI-centric services are emerging as the new battleground. Accenture has allocated USD 1 billion to its LearnVantage platform and further expanded Nordic reach through the Halfspace acquisition. Providers that pair AI-enabled productivity with proven security assurances are capturing premium contracts, thereby increasing their influence on the custom software development market.

Custom Software Development Industry Leaders

Accenture

Capgemini

TCS

HCL Tech

Infosys

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Accenture acquired TalentSprint to bolster its LearnVantage talent-development platform (210 professionals added).

- March 2025: Accenture acquired Halfspace, bringing 80 AI specialists and 100+ Nordic AI projects under its Center for Advanced AI.

- January 2025: KKCG agreed to acquire Avenga, consolidating European custom-software capabilities.

- January 2025: CGI signed to acquire BJSS, adding 2,400 professionals across key verticals.

Global Custom Software Development Market Report Scope

Custom software development encompasses the thorough planning, designing, developing, and deploying of digital solutions that are specifically customized to address the specific needs of particular functions, users, and organizations.

The custom software development market is segmented by service development type (web-based solutions, mobile apps, enterprise software), deployment mode(on-premise and cloud), end-user vertical(BFSI, healthcare, retail, government, IT & telecom, manufacturing, and others), and geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for the above segment.

| Web-based Solutions |

| Mobile Applications |

| Enterprise Software |

| Embedded and IoT Software |

| On-premise |

| Cloud-hosted |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| Healthcare and Life-sciences |

| Retail and E-commerce |

| Government and Public Sector |

| IT and Telecom |

| Manufacturing and Industrial |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East and Africa |

| By Solution | Web-based Solutions | |

| Mobile Applications | ||

| Enterprise Software | ||

| Embedded and IoT Software | ||

| By Deployment Model | On-premise | |

| Cloud-hosted | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-user Vertical | BFSI | |

| Healthcare and Life-sciences | ||

| Retail and E-commerce | ||

| Government and Public Sector | ||

| IT and Telecom | ||

| Manufacturing and Industrial | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the custom software development market?

The custom software development market is valued at USD 50.94 billion in 2026.

How fast is the custom software development market growing?

The market is forecast to expand at an 17.88% CAGR and reach USD 115.95 billion by 2031.

Which solution segment holds the largest share of spending?

Enterprise software leads with 36.60% revenue share in 2025.

Why are cloud-hosted deployments preferred over on-premise models?

Cloud-hosted deployments deliver scalability, lower infrastructure costs and integrated DevOps tooling, giving them 61.40% market share in 2025.

Which region shows the highest growth potential?

Asia-Pacific records the fastest regional CAGR at 20.90% through 2031, driven by government digitization programs and manufacturing investments.

What is the main challenge limiting market growth?

A persistent shortage of senior developers, estimated to remove 1.2 million professionals from the talent pool by 2026, is slowing project delivery and raising costs.

Page last updated on: