Professional Development Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

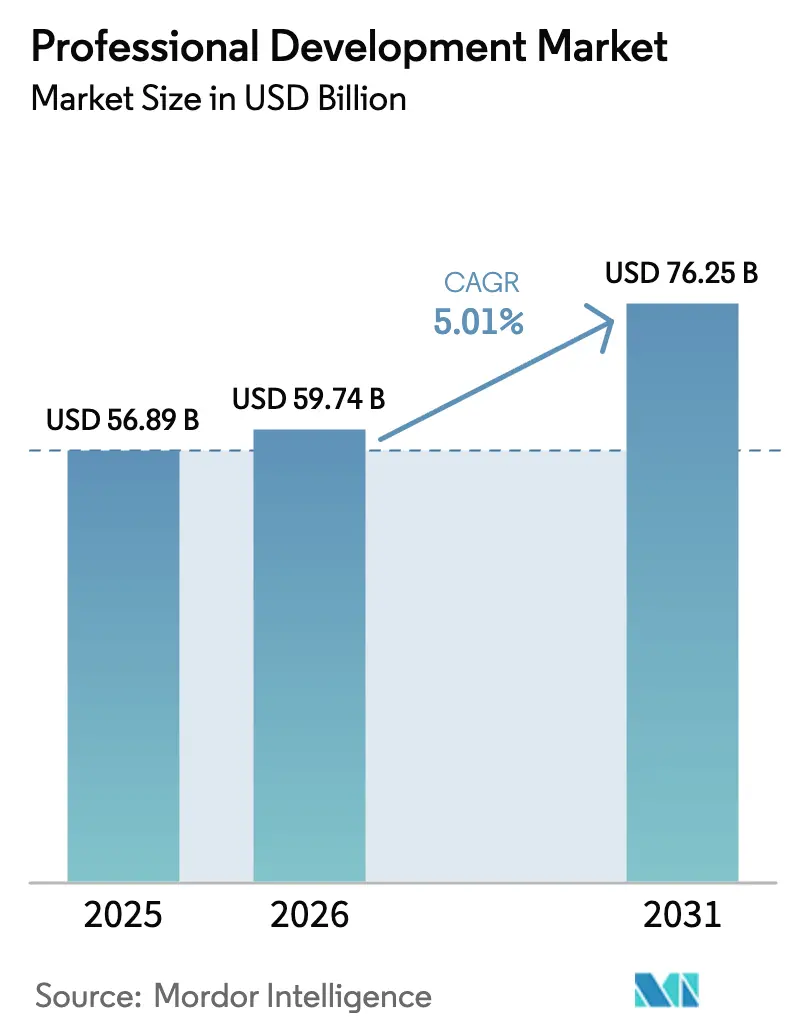

| Market Size (2026) | USD 59.74 Billion |

| Market Size (2031) | USD 76.25 Billion |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Professional Development Market Analysis by Mordor Intelligence

The professional development market size was valued at USD 56.89 billion in 2025 and estimated to grow from USD 59.74 billion in 2026 to reach USD 76.25 billion by 2031, at a CAGR of 5.01% during the forecast period (2026-2031). The rise stems from enterprises shifting away from one-size-fits-all classroom delivery toward AI-powered, outcome-based learning ecosystems that link training spend directly to productivity gains. North America presently underpins demand through digital-transformation mandates and stringent compliance frameworks, while Asia-Pacific scales rapidly on the back of government reskilling funds and employer moves from credential-centric to skills-centric hiring. Vendors differentiate through data-driven personalization, embedded analytics, and seamless integration with daily productivity suites. Meanwhile, public-sector outlays—from Massachusetts’ USD 200 million FutureSkills program to the Biden Administration’s USD 250 million Semiconductor Workforce Center—signal durable public-private collaboration. Cost scrutiny, however, forces providers to balance premium features against flexible pricing as organizations measure every training hour against tangible ROI.

Key Report Takeaways

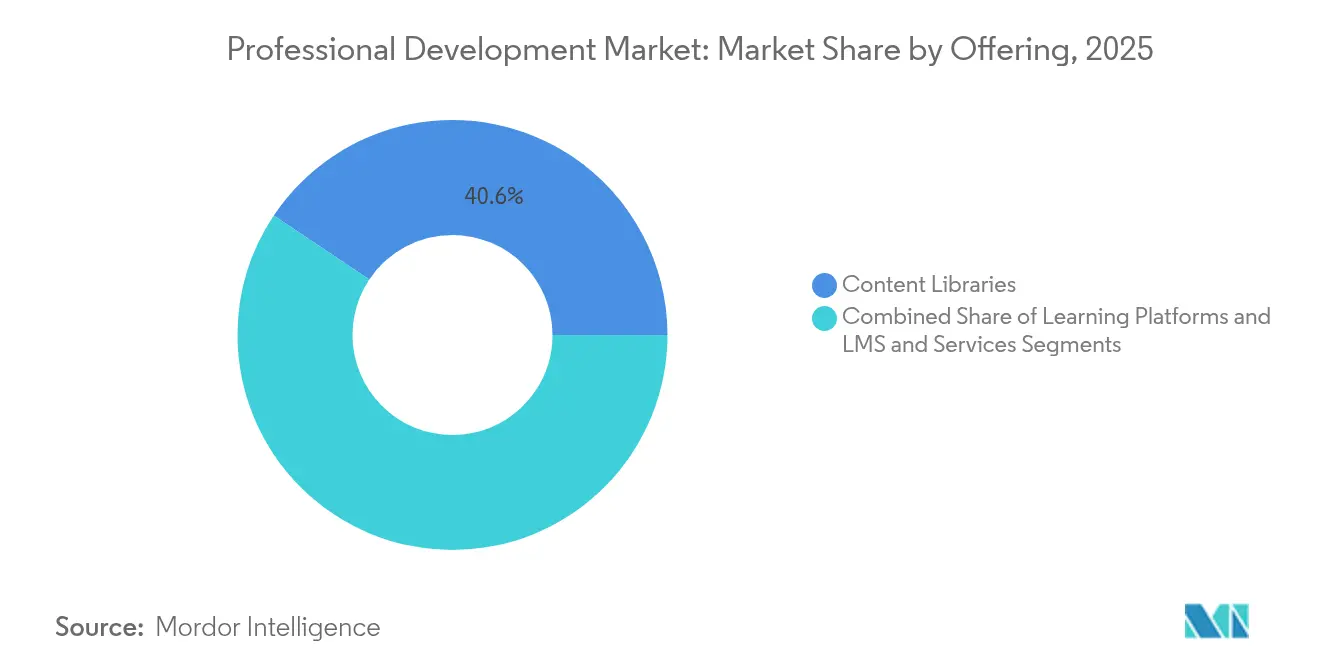

- By offering content libraries led with 40.62% revenue share of the professional development market in 2025, AI-based coaching platforms are forecast to advance at a 13.86% CAGR through 2031.

- By focus area, skillset enhancement accounted for 39.12% of the professional development market share in 2025, while mental health programs post the highest projected CAGR at 13.12% to 2031.

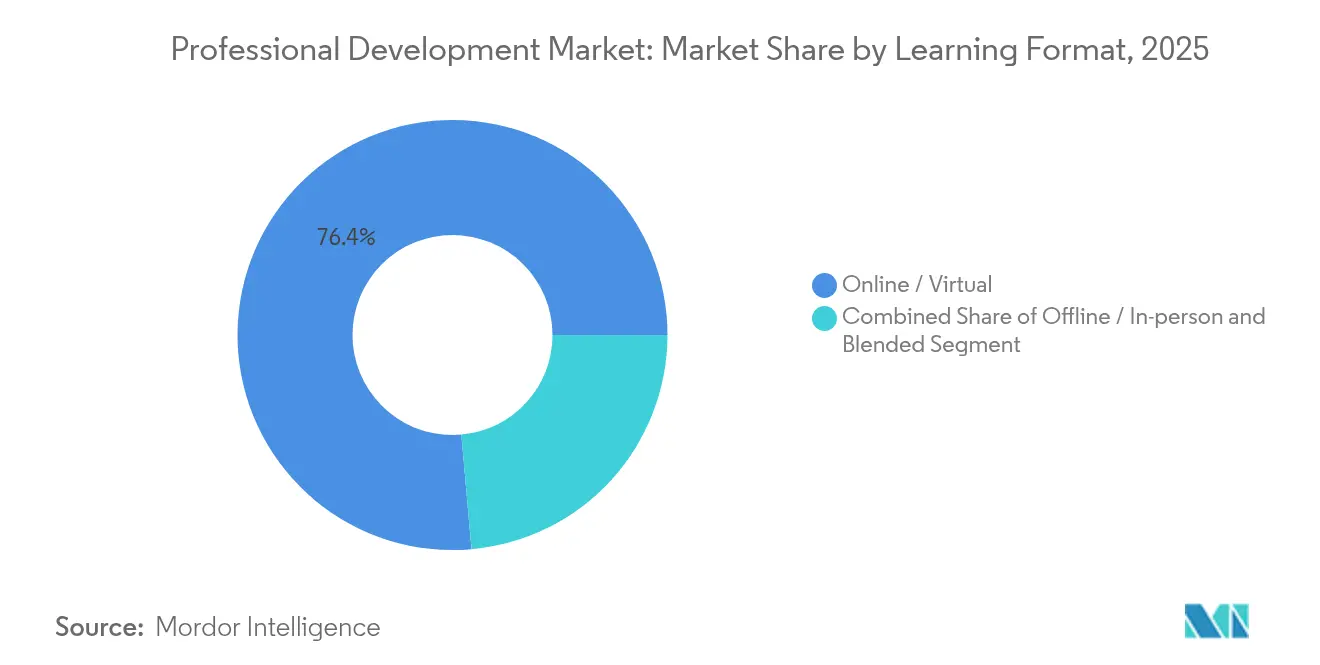

- By learning format, online/virtual delivery captured 76.41% of the professional development market size in 2025; blended learning is projected to grow at a 12.46% CAGR to 2031.

- By end-user industry, IT and telecom held 28.62% share of the professional development market size in 2025; government agencies recorded the fastest CAGR at 10.78% through 2031.

- By geography, North America commanded 37.65% of the professional development market in 2025, while Asia-Pacific is forecast to expand at a 10.45% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Professional Development Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of e-learning platforms | +1.2% | Global, with a stronger impact in North America and Europe | Medium term (2-4 years) |

| Accelerating digital transformation across enterprises | +1.5% | Global, with early adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Expansion of remote and hybrid work models | +0.9% | Global, with a stronger impact in developed economies | Short term (≤ 2 years) |

| Growing need for compliance and ESG / DEI up-skilling | +0.6% | North America and Europe, with emerging impact in Asia-Pacific | Medium term (2-4 years) |

| AI-driven personalised coaching boosting measurable ROI | +0.7% | North America, Europe, and advanced Asia-Pacific economies | Medium term (2-4 years) |

| Micro-credential ecosystems aligning with talent marketplaces | +0.4% | Global, with stronger impact in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of E-learning Platforms

Enterprises accelerate platform roll-outs because cloud-hosted learning delivers scale, version control, and predictable subscription economics. Coursera reported USD 179.3 million revenue in Q1 2025 alongside 7 million new learners, underscoring sustained digital uptake[1]Coursera Inc., “Q1 2025 Shareholder Letter,” coursera.org. Udemy’s subscription mix reached 68%, evidencing a pivot toward recurring models that fund continuous content refresh. Cost curves also favor digital: once virtual environments are deployed, marginal learner cost falls sharply, enabling global roll-outs without travel or venue spend. Providers now embed AI-assisted search to surface precise content, which shortens time-to-competency and improves learner satisfaction scores. The convergence of cloud economics and data-driven curation thus cements e-learning as an enterprise default rather than a pandemic stop-gap.

Accelerating Digital Transformation Across Enterprises

Technology roadmaps in manufacturing, healthcare, and finance hinge on upskilling workforces at speed. Purdue University and Accenture’s Smart Manufacturing Academy exemplifies how tailored curricula target machine operators, technicians, and managers with Industry 4.0 skills. In parallel, Microsoft’s AI agents within Office 365 Copilot embed learning nudges directly into daily workflows, shrinking the gap between knowledge acquisition and application. Organisations now view workforce capability as a critical success factor for technology adoption, prompting multi-year training budgets insulated from discretionary cuts. Public grants—such as the USD 49.2 million Workforce Opportunity for Rural Communities fund—extend transformation benefits to underserved regions.

AI-driven personalised coaching boosting measurable ROI

Generative AI now matches each learner’s pace, style, and role, converting generic playlists into adaptive pathways. Skillsoft’s Codecademy integration adds real-time coding assistants, enabling instant practice and remediation[2]Skillsoft Corp., “Next-Gen Learner Experience Announcement,” skillsoft.com. Firms deploying AI-guided programs report productivity lifts of up to 50% in technical roles and 75% reductions in classroom time. Cost barriers are falling because pre-trained language models and no-code orchestration slash development cycles. Digital credentials such as Credly’s Open Badge 3.0 allow HR teams to verify completion and tie skills to performance dashboards, closing the feedback loop between training spend and business outcomes.

Growing Need for Compliance and ESG / DEI Upskilling

Regulators demand demonstrable proficiency in areas spanning climate reporting, diversity, and safe-work cultures. California’s 2025 statutes mandate mental-health awareness and expanded harassment prevention for employers with as few as 20 staff, forcing thousands of firms to upgrade curricula[3] LMS Portals, “California 2025 Training Mandates Overview,” lmsportals.com. Corporates respond at scale: EY launched a sustainability master’s program for its 300,000-plus employees, integrating academic partners to confer transferable credentials. Financial institutions adopt ESG coursework to align board oversight with investor expectations, while manufacturing groups deploy climate-literacy modules to satisfy supplier audits. The compliance clock keeps ticking, anchoring a resilient demand stream across industries and geographies.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of premium programs | -0.7% | Global, with stronger impact in emerging markets | Short term (≤ 2 years) |

| Employee time-constraint and attention fatigue | -0.5% | Global | Medium term (2-4 years) |

| Data-privacy and IP-security concerns in online delivery | -0.6% | Global, with a stronger impact in highly regulated industries and regions | Medium term (2-4 years) |

| Credential-stack fatigue lowers willingness to pay | -0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Premium Programs

Comprehensive professional development rollouts require investment in licensing, high-quality production, integrations, and ongoing content refresh cycles. The need for specialized crews, animation, scripting, and post-production raises initial outlays, especially for organizations new to multimedia content creation. Budget holders weigh these costs against budget pressures, headcount, and competing digital priorities, which can delay large-scale initiatives. AI-assisted video-editing and voice-cloning technologies promise to ease some cost burdens, yet early adopters report that human oversight remains essential for brand compliance, accessibility, and narrative quality. This balance between efficiency gains and quality assurance will shape procurement decisions over the next two years.

Data-Privacy and IP-Security Concerns in Online Delivery

Video frequently embeds proprietary product roadmaps, strategy briefings, and intellectual property, making data governance a board-level concern. Compliance frameworks such as GDPR and CCPA amplify scrutiny over where and how content is stored, processed, and shared. Enterprises, therefore, demand granular permission controls, encrypted streaming, multi-factor authentication, and immutable audit trails. Solution vendors respond by offering region-specific hosting, zero-trust architectures, and on-premises deployment options. In healthcare and financial services, any perceived security gap can stall procurement cycles until third-party penetration tests are passed, prolonging sales lead times and flattening near-term adoption curves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: AI Reshapes Content Delivery

Content Libraries dominated 40.62% of the professional development market in 2025 due to their breadth and immediate accessibility. Yet AI-based Coaching Platforms are charting a 13.86% CAGR, reflecting stronger engagement metrics that translate into lower churn for vendors and higher skill-retention for employers. Services such as consulting and facilitation remain resilient because organisations still lean on external experts to guide change management, especially in manufacturing upskilling alliances led by firms like Bosch Rexroth. Learning Management Systems continue to serve as the integration hub, with D2L’s user base exceeding 20 million learners across 1,430 clients, showcasing scale benefits.

AI’s rise underscores dissatisfaction with static catalog digestion. EY’s Tech MBA illustrates how adaptive curricula position advanced analytics, leadership, and blockchain modules in sequences driven by learner data. Skillsoft’s Smart Content Discovery uses natural-language input so employees locate resources inside vast libraries without browsing fatigue. Adobe’s Digital Academy pledges USD 100 million toward scholarships that funnel learners into its creative and marketing ecosystem, further entwining content with software usage.

By Focus Area: Mental Health Gains Strategic Priority

Mental Health initiatives controlled 37.88% of 2025 revenue and are expanding at 13.12% CAGR as organisations recognise the link between well-being and productivity. California’s mandate that firms with 20 or more staff deliver mental-health awareness courses adds regulatory tailwind. In healthcare, New Mexico’s community-health-worker program shifts certification online, tackling rural access barriers.

Traditional Skillset Enhancement—technical, leadership, functional—still accounts for the largest absolute spend because its ROI is easiest to quantify. Yet employers increasingly weave mindfulness, resilience, and stress-management modules into leadership tracks, creating hybrid paths that boost retention. Partnerships between Yale School of Public Health and regional academies demonstrate how academic rigour lifts credibility while avoiding redundant course design.

By Learning Format: Blended Approaches Gain Momentum

Online/Virtual formats represented 76.41% of 2025 enrolments, reflecting pandemic-era infrastructure that has since become permanent. The professional development market size for blended learning is projected to grow strongly, with a 12.46% CAGR anticipated as firms combine synchronous video sessions, virtual labs, and periodic in-person workshops. Immersive training providers show that initial headset outlays amortise quickly at scale, making mixed modalities competitive against legacy bootcamps.

Blended frameworks deliver peer interaction and hands-on practice without incurring continuous travel costs. MIT’s technologist program combines VR simulations with facility visits, shortening pathways from theory to equipment mastery. Asia-Pacific pioneers mobile micro-lessons inside blended programs; Bring-Your-Own-Device policies adopted by 72% of regional employers underpin always-on access.

By End-user Industry: Government Sector Accelerates Adoption

The IT and telecom industry contributed 28.62% of 2025 revenue as continuous technology evolution demands perpetual up-skilling. Cloud-migration roadmaps, DevSecOps methodologies, and platform engineering paradigms generate unceasing content pipelines. Government entities, growing at an 10.78% CAGR, are upgrading legacy training programs to enhance citizen services and ensure policy compliance across widely dispersed workforces.

Defense and public-safety agencies stream secure briefings and mission rehearsals to personnel stationed globally, shrinking preparation timelines. Healthcare providers deploy professional development for surgical-procedure refreshers, patient-advisory clips, and compliance updates, while integrated imaging solutions from firms such as Optum streamline content access within clinical workflows. Educational institutions blend synchronous lectures with asynchronous study aids, extending reach to non-traditional learners. BFSI players harness video micro-modules to clarify complex product features and embed regulatory updates directly into frontline workflows. Manufacturing and energy operators use video to preserve institutional knowledge as experienced employees near retirement, pairing annotated footage with sensor data and 3D models to create rich digital twins.

Geography Analysis

Market structure remains moderately fragmented. Network-effect leaders—LinkedIn, Coursera, Udemy—monetise large learner pools via subscription models that grew 50% for LinkedIn in two years. Adobe and Microsoft bundle learning agents into core productivity suites, blurring lines between work and training. Skillsoft integrates generative AI across its catalog, and D2L upgrades mobile UX to defend education contracts. Niche insurgents focus on vertical depth or emerging tech: Degreed’s purchase of Learn In expands cohort-based academies, while Accenture funnels TalentSprint into its USD 1 billion LearnVantage platform to serve enterprise bootcamps. Patent filings in VR haptics and adaptive-assessment algorithms suggest escalating IP races. Buyers now demand outcome proof—documented productivity lifts or certification pass rates—shifting competitive vectors from content volume to efficacy.

Strategic moves in 2024-2025 highlight consolidation and capability stacking. Adobe’s Firefly unifies AI media generation and positions the firm as both tool and educator. Microsoft’s Copilot integration makes learning invisible and continuous. Vendors lacking data science capacity risk relegation to commodity content suppliers unless they partner or merge.

Competitive Landscape

The Professional Development Market is fragmented and has various global and regional players. Some of the major players in the market are Adobe Inc., Cambridge University Press, CAST, Inc., and Catapult Learning LLC, among opthers. Through strategic partnerships and acquisitions, these market players bolster their product portfolios and establish lasting competitive advantages.

Professional Development Industry Leaders

LinkedIn Learning

Coursera Inc.

Udemy Business

Skillsoft Corp.

Pluralsight LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Adobe launched Firefly, an all-in-one AI content platform in partnership with Google Cloud and OpenAI, supporting image, video, and audio generation.

- April 2025: Accenture acquired TalentSprint to deepen LearnVantage university certifications amid a USD 1 billion three-year investment plan.

- March 2025: Adobe and Microsoft announced AI agents inside Microsoft 365 Copilot, enabling real-time content creation within productivity apps.

- September 2024: The U.S. Commerce Department opened the National Semiconductor Technology Center Workforce Center of Excellence with USD 250 million funding.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the professional development market as all paid learning, coaching, and certification services purchased by working adults or their employers to improve role-related knowledge, leadership ability, or compliance readiness.

Delivery modes span instructor-led workshops, blended programs, and fully digital platforms; revenues from K-12 teacher training or hobbyist self-help books are excluded.

Segmentation Overview

- By Offering

- Content Libraries

- Learning Platforms and LMS

- Services (Consulting, Facilitation)

- By Focus Area

- Mental Health

- Motivation and Inspiration

- Physical Well-being

- Self-Awareness

- Skillset Enhancement

- By Learning Format

- Online / Virtual

- Offline / In-person

- Blended

- By End-user Industry

- Healthcare

- Education

- IT and Telecom

- BFSI

- Government and Public Sector

- Manufacturing and Energy

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple touch points with chief learning officers, HR tech vendors, professional services buyers, and regional accreditation bodies in North America, Europe, and Asia-Pacific clarified adoption triggers, price dispersion, and attrition rates. This feedback let us adjust default assumptions on digital penetration and refresh intervals before locking the model.

Desk Research

We began with publicly available data sets, such as UNESCO Institute for Statistics, the OECD Continuing Vocational Training Survey, U.S. Bureau of Labor Statistics employer training spend, and Training Magazine's annual industry census, to size learner pools and average spend. Company 10-Ks, investor decks, and association white papers (e.g., ATD, SHRM) supplied price points, completion volumes, and curriculum mix trends. Subscription repositories that Mordor analysts access, including D&B Hoovers for company L&D budgets and Dow Jones Factiva for deal flow, helped validate revenue splits. The sources above are illustrative; many additional references informed fact-checking and model calibration.

Market-Sizing & Forecasting

A top-down build starts with global corporate training outlays and adult education tuition flows, which are then filtered by the share attributable to professional upskilling. Selected bottom-up checks, supplier roll-ups of platform subscribers and sampled ASP x completion volumes, anchor the totals. Key variables tracked include employer L&D spend as a share of payroll, average paid learning hours per employee, digital course ASP trends, certification mandate counts, and regional GDP per worker. Forecasts rely on multivariate regression that links spending to GDP growth, digital adoption, and regulatory intensity; scenario analysis flags upside from AI-driven personalization. Data gaps in smaller geographies are bridged with proxy indicators (e.g., broadband penetration) validated by local experts.

Data Validation & Update Cycle

Outputs pass two analyst reviews, variance checks against independent spend trackers, and anomaly screening. We refresh every twelve months and trigger mid-cycle updates after material events such as large-scale policy shifts. Before dispatch, an analyst reruns the model to ensure clients receive the latest view.

Credibility Anchor-Why Our Professional Development Baseline Commands Reliability

Published estimates vary because firms apply different scopes, currency conversions, or refresh cadences.

Key gap drivers include whether consumer self-help spend is counted, how free MOOCs are treated, and if vendor revenues are gross or net of reseller margins. Mordor's disciplined scope, paid career-oriented learning for employees, plus annual bottom-up cross-checks keeps our 2025 baseline dependable for planners.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 56.89 B (2025) | Mordor Intelligence | - |

| USD 53.20 B (2025) | Regional Consultancy A | Excludes micro-learning subscriptions and small-firm spend |

| USD 55.59 B (2024) | Global Consultancy B | Uses historical average spend per learner without adjusting for post-pandemic hybrid uptake |

| USD 573.24 B (2024) | Trade Journal C | Blends personal self-improvement, K-12, and vocational programs, inflating totals |

In sum, while other publishers swing conservative or expansive, Mordor's model stays centered on verifiable corporate and professional expenditures, giving decision makers a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the projected value of the professional development market by 2031?

The professional development market is expected to reach USD 76.25 billion by 2031, growing at a 5.01% CAGR.

Which segment is growing fastest within the professional development market?

AI-based Coaching Platforms are the quickest-growing offering, advancing at 13.86% CAGR to 2031.

Why is mental-health training expanding so quickly?

Regulatory mandates such as California’s 2025 legislation and broader employer focus on wellness give Mental Health training a 13.12% CAGR, the highest among focus areas.

How large is North America’s share of the professional development market?

North America held 37.65% of global revenue in 2025, anchored by digital-transformation spending and compliance requirements.

What factors restrain market growth despite strong demand?

High program costs and employee time constraints reduce uptake, with premium plans often exceeding USD 100,000 annually and frontline staff struggling to allocate learning hours.

Page last updated on: