Singapore Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.47 Billion |

| Market Size (2026) | USD 2.56 Billion |

| Market Size (2031) | USD 3.06 Billion |

| Growth Rate (2026 - 2031) | 3.64% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Containerboard Market Analysis by Mordor Intelligence

The Singapore containerboard market size was valued at USD 2.47 billion in 2025 and estimated to grow from USD 2.56 billion in 2026 to reach USD 3.06 billion by 2031, at a CAGR of 3.64% during the forecast period (2026-2031). The Singapore containerboard market is shaped more by trade intensity than by local fiber supply or population growth, as the country serves as a regional transit and export platform. Record port activity, steady re-export flows, and export-linked manufacturing keep packaging demand resilient across the forecast period. E-commerce fulfillment is adding another layer of demand, even as right-sized packaging guidelines reduce box use in selected lightweight categories. The Singapore containerboard market also benefits from demand for stronger and cleaner corrugated packaging from electronics, precision-engineering, and pharmaceutical exporters. Competition remains fragmented, leaving room for converters that can combine fast turnaround, structural design capability, and reliable delivery within industrial clusters.

Key Report Takeaways

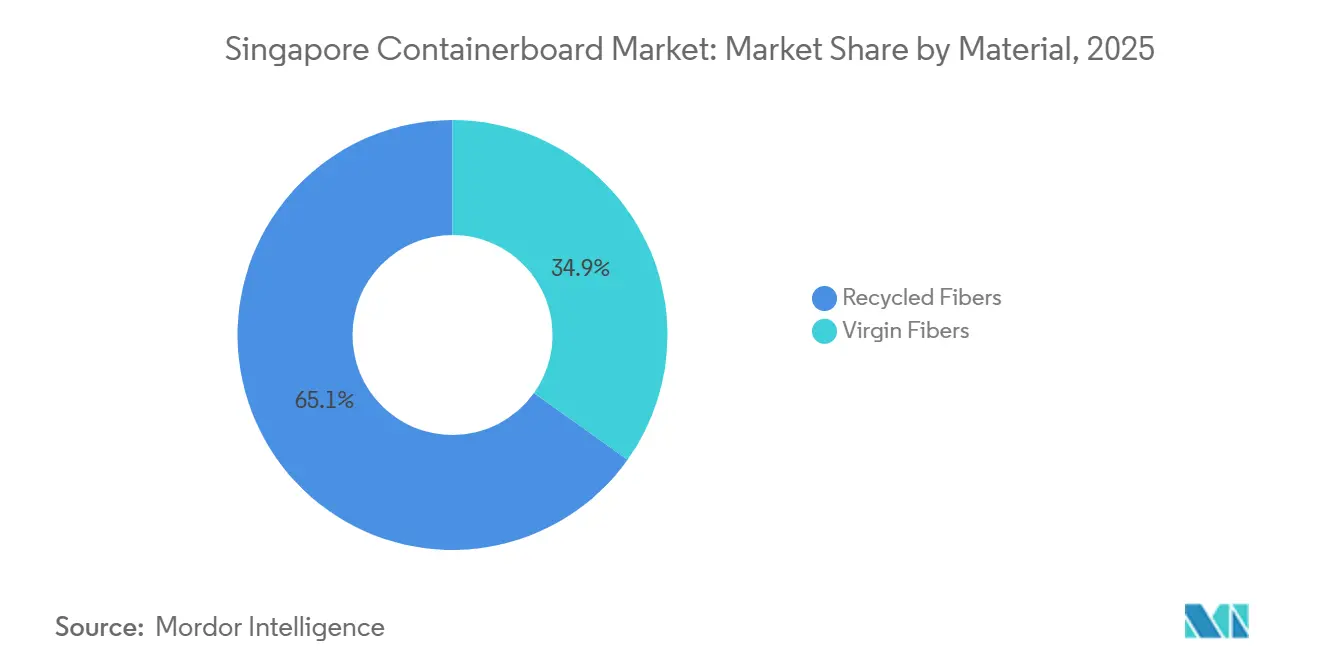

- By material, recycled fibers captured 65.14% of the Singapore containerboard market share in 2025.

- By product type, the Singapore containerboard market size for the kraftliners segment is forecast to advance at a 4.07% CAGR through 2031.

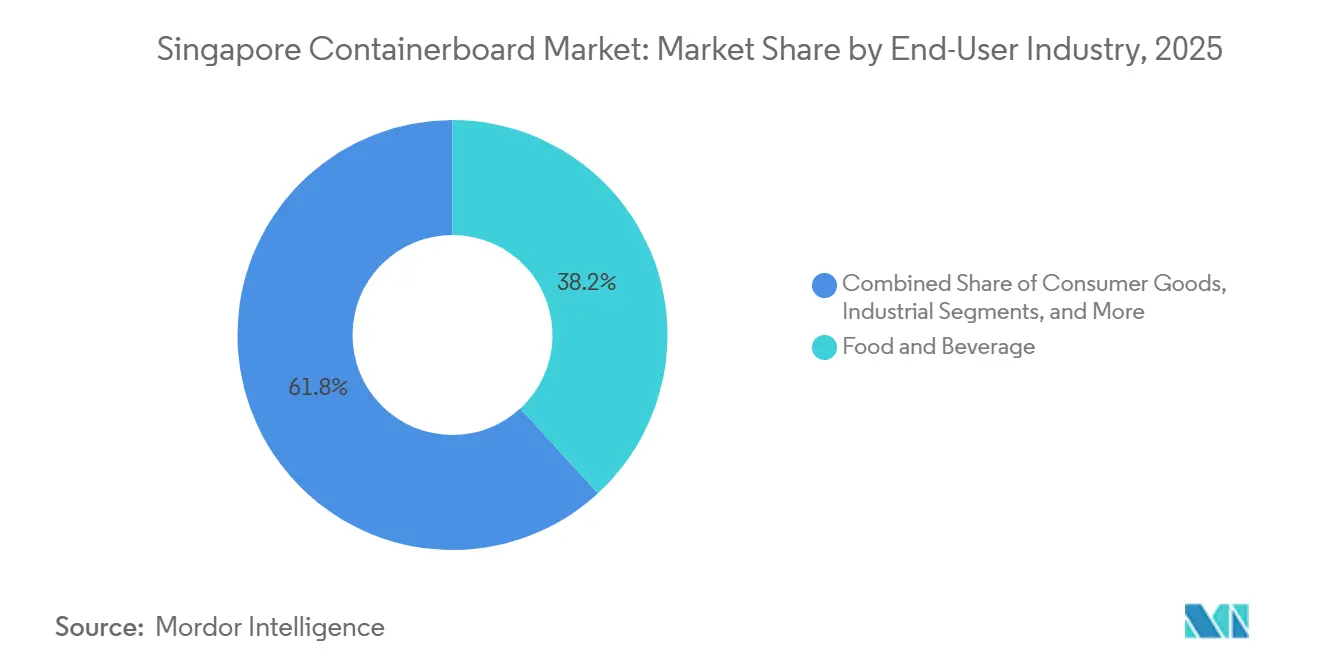

- By end-user industry, food and beverage captured 38.17% of the Singapore containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Fulfillment And Last-Mile Parcel Growth | +1.0% | National, concentrated in urban e-commerce corridors and regional logistics hub zones | Short term (≤ 2 years) |

| Sustainability Regulations Favoring Recyclable Fiber Packaging | +0.8% | National, with compliance spill-over to Singapore-headquartered exporters targeting EU markets | Medium term (2-4 years) |

| Export-Oriented Advanced Manufacturing Demand | +0.6% | National, concentrated in Tuas, Jurong Island, and Changi aerospace and semiconductor clusters | Medium term (2-4 years) |

| Food Delivery And Processed Food Shipment Growth | +0.5% | National, with re-export spill-over to ASEAN and the Middle East | Short term (≤ 2 years) |

| Sustainable E-Commerce Packaging Guidelines Encouraging Right-Sized Corrugated Designs | +0.3% | National, extending to Singapore-headquartered regional brand operations | Medium term (2-4 years) |

| Record Port Throughput Supporting Re-Export Packaging Demand | +0.2% | National, with spill-over to re-export hubs serving Southeast Asia and Oceania | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Fulfillment And Last-Mile Parcel Growth

The Singapore containerboard market is supported by rising parcel density because packaging demand responds to shipment counts, handling frequency, and delivery speed as much as to headline online sales values. In March 2025, SingPost committed SGD 30 million (USD 22.2 million) to expand small-parcel processing capacity at its Regional eCommerce Logistics Hub from 100,000 to 300,000 parcels per day by mid-2026. That investment showed that logistics operators were planning for sustained parcel growth rather than only for short seasonal peaks. Cross-border B2C shipments in categories such as electronics, cosmetics, and health-related goods tend to rely on corrugated transport packaging because they move through more handling points than purely domestic deliveries. This pattern supports repeat ordering from converters that serve logistics providers, regional fulfillment programs, and short-run e-commerce packaging needs across the Singapore containerboard market. It also favors suppliers that can respond quickly to changing order profiles, because parcel-led demand is more dynamic than conventional retail replenishment.

Sustainability Regulations Favoring Recyclable Fiber Packaging

The Singapore containerboard market is also benefiting from a regulatory framework that steadily increases the value of recyclable and traceable packaging formats.[1]National Environment Agency, “Packaging Partnership Programme and Singapore Packaging Agreement,” National Environment Agency, nea.gov.sg NEA's Mandatory Packaging Reporting framework, in force under the Resource Sustainability Act 2019, requires companies with annual turnover above SGD 10 million (USD 7.4 million) that supply packaged goods to submit annual packaging data and 3R plans. That system rewards packaging choices that can show recycled-content pathways, recovery potential, and clearer documentation for compliance purposes. Singapore then launched the Beverage Container Return Scheme on April 1, 2026, with more than 1,070 reverse vending machines and a SGD 0.10 (USD 0.07) refundable deposit on eligible plastic and metal beverage containers. The scheme is focused on beverage containers, yet it still raises the overall compliance baseline for packaging design, labeling, and producer accountability. Over time, that policy direction supports fiber-based packaging formats that fit recycling systems more easily than mixed-material formats, which strengthens the operating backdrop for the Singapore containerboard market.

Export-Oriented Advanced Manufacturing Demand

The Singapore containerboard market is gaining support from the country's export manufacturing base, which expanded industrial production by 8.7% in 2025, the strongest increase since 2021. Electronics has been the main engine within that recovery, and AI-related semiconductor output rose 32.4% in December 2025. Electronics Non-Oil Domestic Exports increased 12.7% in 2025 and then rose 56.1% in January 2026, with integrated circuits up 80.5% and disk media products up 70.2% year over year. Export-oriented semiconductor, precision-engineering, and pharmaceutical producers need corrugated packaging that can withstand stacking loads, vibration, and clear-compliance printing during multimodal shipments. Micron began operations at a new USD 7 billion high-bandwidth memory advanced packaging facility in Singapore in 2026, adding a visible source of ongoing demand for higher-specification export cases. As higher-value chips and components move through Singapore, packaging's share of end-product value declines, supporting premium board adoption across the Singapore containerboard market.

Food Delivery And Processed Food Shipment Growth

The Singapore containerboard market also draws steady support from the food chain, where delivery growth, packaged food demand, and re-export activity all require corrugated transport packaging. Singapore's food delivery market reached USD 2.9 billion in gross merchandise value in 2025, up 13%, which kept secondary packaging demand firm across the supply chain. The retail packaged food market was estimated at nearly USD 3.5 billion in 2024 and is forecast to reach USD 4.4 billion by 2029, supported by a premium consumer base and heavy reliance on imports.[2]Food Export Association of the Midwest USA and Food Export USA-Northeast, “Singapore,” Food Export Association, foodexport.org Foodservice delivery generated USD 2,234.9 million in consumer sales in 2023 and expanded at a 33.3% CAGR from 2018 to 2023, with third-party delivery accounting for a large part of the increase.[3]Agriculture and Agri-Food Canada, “Foodservice Profile - Singapore,” Agriculture and Agri-Food Canada, agriculture.canada.ca Singapore also acts as a re-export platform for processed food moving into ASEAN and the Middle East, which raises demand for corrugated formats with documented food-contact compliance and stronger transit performance. That mix of domestic consumption and outward shipment keeps food-related demand broad and dependable within the Singapore containerboard market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Fiber And Board Cost Volatility | -0.8% | National, with acute exposure to US OCC price swings and Asian containerboard import pricing dynamics | Short term (≤ 2 years) |

| Competition From Flexible And Reusable Packaging Formats | -0.6% | National, concentrated in fresh food delivery, personal care, and fast-moving consumer goods segments | Medium term (2-4 years) |

| Weak Domestic Paper Recycling Economics | -0.4% | National, high logistics cost for collected OCC within a compact urban geography with no domestic mills | Medium term (2-4 years) |

| Packaging Reporting Rules Incentivizing Material Reduction | -0.3% | National, with ASEAN export market spill-over as Singapore brands deploy MPR-driven lightweighting | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imported Fiber And Board Cost Volatility

The Singapore containerboard market remains exposed to input volatility because local converters depend entirely on imported recovered fiber and finished containerboard. US OCC 11 imported into Southeast Asia stood at USD 175-180 per tonne in January 2025, down 20.2% year over year. European OCC 95/5 was assessed at USD 145-150 per tonne during the same period, indicating that lower recovered paper prices were widespread rather than isolated. Lower fiber prices do not always protect converter margins because finished board prices and freight costs can move sharply over the same period. Fastmarkets reported that intra-Asia container shipping rates tripled on some route pairs in mid-2024, and routes from the United States to Southeast Asia also saw steep increases. Converters that lack long-term contracts or multi-origin sourcing, therefore, face sharper landed-cost swings, which limit pricing stability across the Singapore containerboard market.

Competition From Flexible And Reusable Packaging Formats

The Singapore containerboard market also faces substitution pressure from flexible and reusable packaging formats in applications where moisture protection, lower weight, or compact form factors matter more than box strength. Retail-to-door food delivery, which grew at a 39.9% CAGR for third-party delivery services in Singapore from 2018 to 2023, relies mainly on rider-mounted insulated bags rather than corrugated boxes for prepared food. In March 2025, the Alliance for Action on packaging waste reduction published sustainable e-commerce packaging guidelines that recommended paper mailers and reusable formats to reduce packaging needs by up to 90% in suitable B2C categories. The Straits Times reported that Watsons Singapore achieved 5-10% in procurement cost savings by repurposing shredded cardboard and reducing bubble wrap use. This means sustainability-led packaging changes do not always lift box volumes, because some light parcels shift from corrugated boxes toward flatter paper-based formats. The greatest pressure is in lightweight consumer shipments such as apparel, accessories, and cosmetics, where packaging reduction matters more than transit strength in parts of the Singapore containerboard market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Anchor Volumes, Virgin Grades Grow In Export Packaging

Recycled fibers held 65.14% of the Singapore containerboard market share in 2025, which kept them firmly at the center of the material mix for standard corrugated applications. Local converters have built long-running procurement relationships with mills in Malaysia, South Korea, and China, and those links continue to support recycled testliner and fluting supply for cost-sensitive box programs. The everyday demand base comes from food distribution, industrial packaging, and domestic consumer-goods movement, where converters prioritize consistent supply and workable price points over premium finish. NEA's packaging reporting rules also reinforce the value of materials that can be documented clearly in packaging submissions and reduction plans.[4]National Environment Agency, “Packaging Partnership Programme and Singapore Packaging Agreement,” National Environment Agency, nea.gov.sg That combination keeps recycled grades structurally important to the Singapore containerboard market rather than treating them as a temporary response to pricing cycles.

Virgin fibers are projected to grow at a 3.98% CAGR from 2026 to 2031, making them the fastest-growing material segment within the Singapore containerboard market. Demand is tied to exporters in semiconductors, aerospace maintenance, and pharmaceuticals that need kraftliner-faced board for burst strength, cleaner printing, and better consistency in regulated shipping environments. Singapore's export manufacturing profile supports that shift because high-value goods often require packaging performance that standard recycled board does not always provide. Micron's new USD 7 billion advanced packaging facility in Singapore gives a clear example of the type of customer base that can sustain premium board demand over time. The result is a split structure in the Singapore containerboard industry, with recycled grades carrying volume demand and virgin grades expanding selectively in export-focused applications.

By Product Type: Testliners Lead Core Demand, Kraftliners Advance Faster

Testliners held 43.72% of the Singapore containerboard market in 2025, reflecting their strong cost-performance fit in mainstream corrugated conversion. They remain well-suited to food and beverage retail, consumer-goods distribution, and industrial components packaging, where recycled furnish provides adequate ring crush and flat crush performance for routine shipment. Testliners also align with the purchasing logic of converters serving short lead times and repeat domestic orders, as they balance affordability with acceptable box strength for many everyday uses. Flutings remain an essential supporting input in this structure, and procurement decisions for medium layers often move with broader liner choice and price trends across the converting base.

Kraftliners are projected to expand at a 4.07% CAGR from 2026 to 2031, making them the fastest-growing product segment in the Singapore containerboard market. Their growth is tied more to export manufacturing than to mass local consumption, because outbound electronics and precision shipments place greater weight on surface quality, cleanliness, and stacking performance. Singapore's semiconductor and electronics momentum has reinforced that shift, with AI-related chip demand adding pressure for stronger export packaging in 2025 and 2026. As those goods carry higher unit values, buyers are less likely to compromise on board specification for relatively small packaging savings. This keeps testliners central to volume demand even as kraftliners grow faster inside the Singapore containerboard industry.

By End-User Industry: Food And Beverage Holds The Base, Consumer Goods Moves Ahead Faster

Food and beverage accounted for 38.17% of the Singapore containerboard market share in 2025, which made it the largest end-user segment in the demand mix. Singapore's broad foodservice economy, premium retail food profile, and dependence on imported and re-exported food products all help sustain corrugated usage across primary transit, secondary handling, and shelf-ready formats. The packaged food market is forecast to keep expanding through 2029, and that supports recurring demand for regular-slotted cartons, display-ready units, and stronger cases for processed food movement. Tat Seng Packaging Group's FY2025 revenue mix, with 42% from food and beverage customers and another 15% from medical and pharmaceutical accounts, shows how food-led demand continues to anchor converter order books even during pricing pressure. That base-load demand gives the Singapore containerboard market a stable volume center even as other end uses move with export cycles.

Consumer goods are projected to grow at a 4.14% CAGR from 2026 to 2031, which makes it the fastest-growing end-user segment in the Singapore containerboard market. Singapore serves as a premium regional fulfillment hub for personal care, home products, and wellness goods moving through ASEAN channels, and these products often require packaging that is both presentable and transit-ready. Brand owners also want better print consistency and dimensional accuracy because outer cases may serve as both shipping packs and retail-ready displays. Industrial demand from precision engineering, chemicals, and aerospace maintenance adds a separate layer of need for double-wall and triple-wall formats, which broadens the customer base beyond consumer categories. Across the Singapore containerboard market, that end-user mix favors converters that can deliver structural design, print quality, and just-in-time service in the same program.

Geography Analysis

The Singapore containerboard market size was USD 2.47 billion in 2025, and its geographic profile is shaped by the city-state's role as a trade gateway rather than by local pulp or fiber production. Singapore does not produce domestic virgin fiber, so demand is closely tied to trade throughput, export packaging needs, and re-export flows across Asia and beyond. The Port of Singapore handled a record 44.66 million TEUs in 2025, up 8.6% year over year, which confirms the scale of cargo movement supporting packaging demand. International separately reported 44.5 million TEUs at its Singapore terminals in 2025, reinforcing the picture of exceptionally high container intensity. That throughput creates a steady demand for corrugated outer packaging for goods moving to South Asia, the Middle East, and Oceania, even when local consumer demand is not the main driver.

Singapore's position within Southeast Asia also differs from that of larger neighboring markets, as value intensity matters more than mass volume in many packaging programs. Semiconductor, pharmaceutical, and precision-engineering shipments use higher-specification corrugated formats than the recycled single-wall boxes common in many consumer-led regional markets. Malaysia and Thailand remain important nearby sources of finished boards and semi-finished rolls, making regional trade lanes central to converter procurement decisions. Enterprise Singapore's upgrade of the 2026 NODX growth forecast to 2-4% further strengthened the case for export-linked packaging demand in the Singapore containerboard market.

Regulation gives Singapore a second layer of geographic differentiation within Southeast Asia. The Resource Sustainability Act 2019 and NEA's Mandatory Packaging Reporting framework require larger producers and importers of packaged goods to submit packaging data and 3R plans each year. That system encourages recyclable, traceable fiber formats because those materials align better with reporting and reduction plans than mixed-material alternatives. The Beverage Container Return Scheme began on April 1, 2026, with more than 1,070 reverse vending machines deployed across the island, demonstrating how physical collection infrastructure is becoming part of packaging policy. Together, high trade intensity, export manufacturing, and structured compliance requirements make the Singapore containerboard market more value-dense and more specification-sensitive than many other Southeast Asian packaging markets.

Competitive Landscape

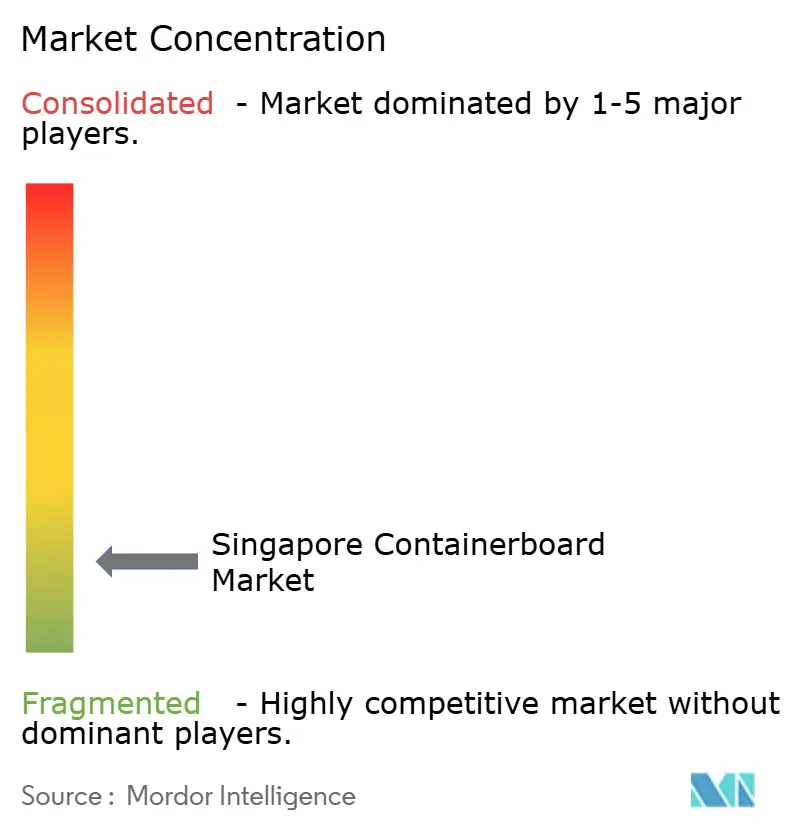

The Singapore containerboard market is fragmented at the converter level, and no single domestic player holds a dominant position. The competitive base includes Interpak Industries, Trio Packaging Industries, Cheng Heng Paper Products, Singapore Cartons, and Atlas Paper Products, as well as other small- and medium-sized corrugated box manufacturers that compete on lead time and customization. Customers often value fast turnaround, low minimum-order flexibility, and quick structural mock-up capability because many deliveries are tied to just-in-time industrial schedules. That operating pattern favors local responsiveness over raw scale in large parts of the Singapore containerboard market. Tat Seng Packaging Group remains the most visible listed Singapore-based corrugated packaging company, yet its Singapore segment generated SGD 42.3 million (USD 31.4 million) in FY2025 revenue within the group's SGD 231.4 million (USD 171.5 million) in revenue, underscoring the limited absolute scale of even the best-known incumbent.

Competitive strategy has split between larger operators investing in certification and operating depth, and smaller firms using service responsiveness as their main edge in the Singapore containerboard market. Tat Seng disclosed that a new corrugator line at its Suzhou plant commenced operations in October 2025, and the group also reported that its Tianjin facility achieved FSSC 22000 V6 certification for food packaging materials. Those moves matter for Singapore because multinational food, medical, and export customers increasingly screen suppliers for process discipline and compliance credentials. In August 2025, Dr. Goi Seng Hui launched a mandatory unconditional cash offer for all outstanding Tat Seng shares at SGD 0.899 (USD 0.687) per share after his acquisition of controlling shareholder PSC Corporation, signaling that consolidation pressure had begun to build around the sector. If that pressure continues, procurement scale and certification breadth will matter more, but local service speed is still likely to remain a strong defense in the Singapore containerboard market.

White space remains strongest in short-run, digitally printed corrugated cases for cross-border e-commerce and in certified-provenance packaging for semiconductor and pharmaceutical exports. Regional suppliers such as SCG Packaging and Oji Holdings already influence local competition through board supply and by serving accounts that need consistent certified volumes across multiple markets. That dynamic pushes local converters to differentiate through faster design cycles, lower minimum runs, and closer customer coordination inside the Singapore containerboard market. Overall, the competitive structure remains broad rather than concentrated, which keeps pricing, service, and compliance capability in close balance across the Singapore containerboard market.

Singapore Containerboard Industry Leaders

Tat Seng Packaging Group Ltd

Far East Packaging Industrial Pte Ltd

Trio Packaging Industrial Pte Ltd

Cheng Heng Paper Products Co (Pte) Ltd

Singapore Cartons Pte Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Singapore's Beverage Container Return Scheme (BCRS) launched on April 1, 2026, deploying over 1,070 reverse vending machines across the island and mandating a SGD 0.10 (USD 0.07) refundable deposit on eligible plastic and metal beverage containers. The scheme is Singapore's first large-scale EPR mechanism and establishes a regulatory precedent for future EPR expansion to corrugated and fiber packaging categories, directly affecting the food and beverage segment of the containerboard market.

- March 2026: Tat Seng Packaging Group completed the business transfer of United Packaging Industries Pte. Ltd. on March 31, 2026, acquiring UPI's business, assets, and liabilities for SGD 7,928,396 (USD 5.88 million) to consolidate Singapore operations into a single entity, reduce structural overhead, and improve just-in-time service delivery efficiency. The transaction rendered United Packaging Industries inactive.

- February 2026: Enterprise Singapore upgraded Singapore's full-year 2026 NODX growth forecast to 2-4% from 0-2%, citing improved global economic outlook and sustained AI-related electronics demand. The upgrade reinforces the demand signal for export-grade corrugated and containerboard packaging across Singapore's semiconductor and precision-engineering manufacturing clusters.

- January 2026: PSA International reported a record 44.5 million TEUs processed at its Singapore terminal in 2025, an increase of over 8% year on year, as part of a global record of 105 million TEUs across PSA's network. The record throughput directly supports re-export packaging demand throughout the containerboard value chain.

Singapore Containerboard Market Report Scope

The Singapore Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Singapore Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

How large is the Singapore containerboard market?

The Singapore containerboard market was valued at USD 2.47 billion in 2025, is expected to reach USD 2.56 billion in 2026, and is forecast to reach USD 3.06 billion by 2031 at a 3.64% CAGR.

What is driving growth in Singapore containerboard demand?

Trade intensity, record port throughput, export-oriented electronics and semiconductor production, and steady food and parcel shipment activity are the main demand drivers.

Which material segment leads demand in Singapore?

Recycled fibers led with 65.14% share in 2025 because they remain the main procurement base for standard corrugated applications across food, industrial, and consumer distribution.

Which product type is growing the fastest?

Kraftliners are projected to grow at a 4.07% CAGR through 2031, supported by stronger export packaging requirements in electronics, precision-engineering, and regulated manufacturing shipments.

Why does food and beverage remain the largest end-user segment?

Food and beverage held 38.17% share in 2025 because Singapore combines a large foodservice economy with strong packaged food imports and re-export activity that depend on corrugated transport packaging.

What are the main risks facing converters in Singapore?

Imported OCC and board price volatility, freight cost swings, and competition from flexible or reusable packaging formats can pressure margins and limit volume growth in selected applications.

Page last updated on: