Singapore Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

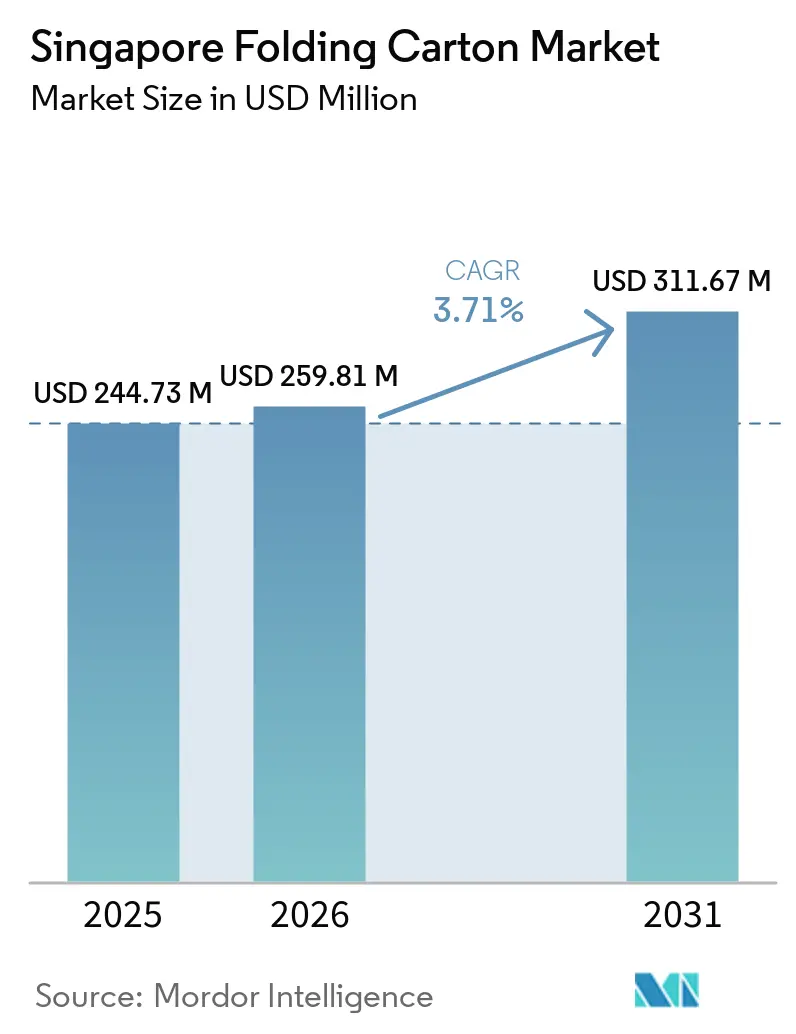

| Base Year Market Size (2025) | USD 244.73 Million |

| Market Size (2026) | USD 259.81 Million |

| Market Size (2031) | USD 311.67 Million |

| Growth Rate (2026 - 2031) | 3.71% CAGR |

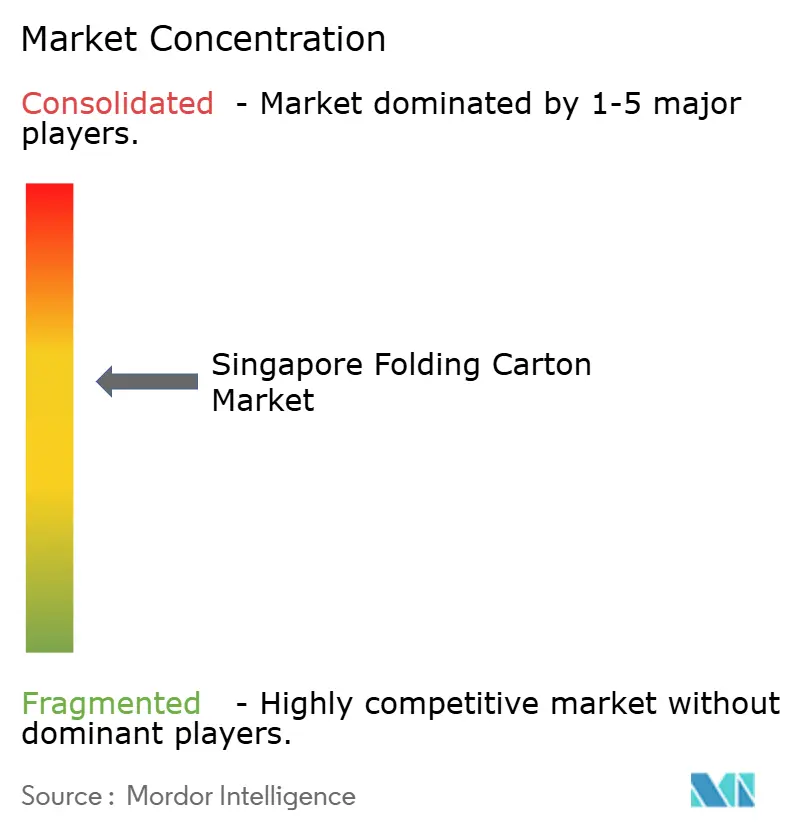

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Folding Carton Market Analysis by Mordor Intelligence

The Singapore Folding Carton Market size is projected to be USD 244.73 million in 2025, USD 259.81 million in 2026, and reach USD 311.67 million by 2031, growing at a CAGR of 3.71% from 2026 to 2031. The measured pace reflects a mature packaging ecosystem in which brand-owner preferences, strict sustainability rules, and a robust e-commerce logistics backbone interact. Ongoing shifts from rigid plastics to recyclable paperboard, the city-state’s continuing importance as a distribution gateway for Southeast Asia, and a rising appetite for premium ready-to-eat meals collectively reinforce demand for folding cartons. At the same time, elevated land and labor costs compel many converters to automate core processes or outsource high-volume production to lower-cost neighbors, even as they keep design, prepress, and short-run work in Singapore to protect intellectual property and meet rapid-response orders. Multinational fast-moving consumer goods (FMCG) players, pharmaceutical firms, and luxury cosmetic brands all specify folding cartons that support brand storytelling, digital traceability, and greener material footprints, further anchoring growth in the Singapore folding carton market.

Key Report Takeaways

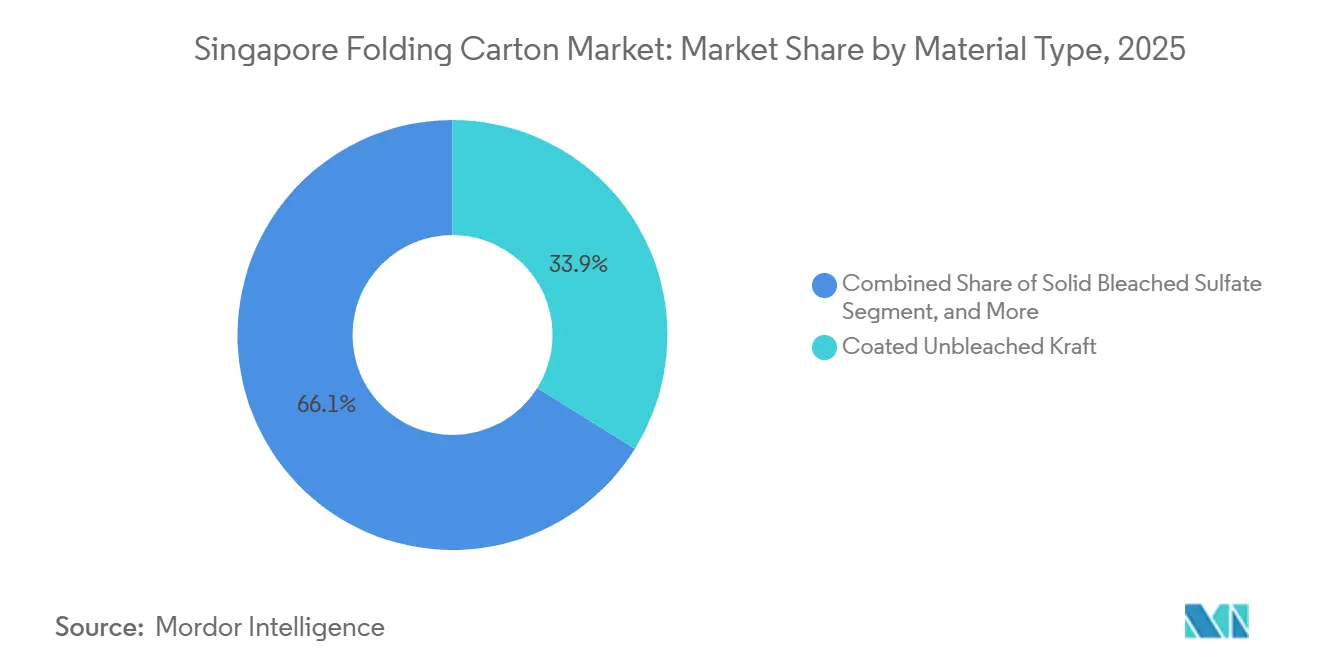

- By material type, coated unbleached kraft captured with 33.87% of the Singapore folding carton market share in 2025.

- By printing technology, the Singapore folding carton market size for digital printing is projected to grow at a 5.96% CAGR to 2031.

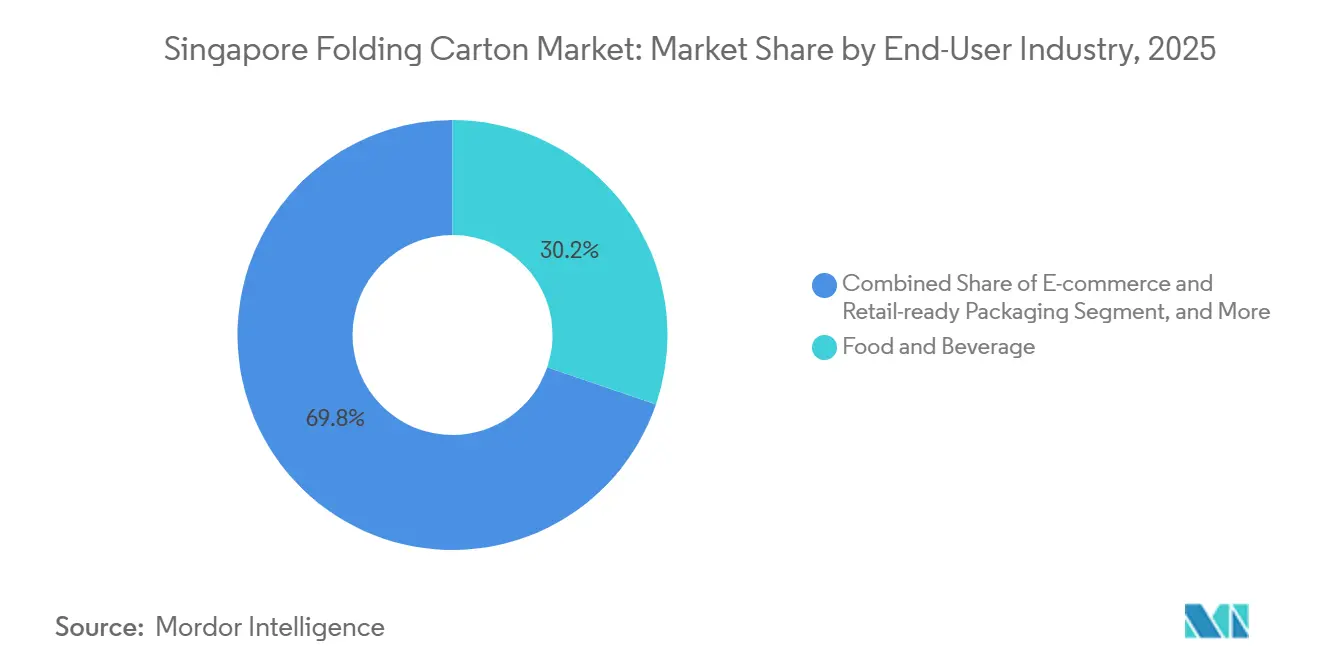

- By end-user industry, the food and beverage industry captured 30.23% of the Singapore folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in E-Commerce Packaging Demand | +1.2% | National, logistics nodes Changi and Tuas | Short term (≤ 2 years) |

| Government Push for Sustainable Packaging and Green Plan 2030 | +0.9% | National, NEA and MSE oversight | Medium term (2-4 years) |

| Growth of Ready-to-Eat Meal Deliveries Boosting Folding Carton Usage | +0.6% | National, urban residential clusters | Short term (≤ 2 years) |

| Technological Advancements in Digital Printing for Short Runs | +0.5% | National, mid-tier converters | Medium term (2-4 years) |

| Rising Demand for Premium Healthcare Packaging Amid Aging Population | +0.3% | National, pharmaceutical hubs | Long term (≥ 4 years) |

| Brand-Owner Shift Toward Plastic-to-Paper Substitution | +0.3% | National, multinational FMCG firms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in E-Commerce Packaging Demand

Singapore’s position as a regional fulfillment nexus allows digital retailers to consolidate inventory in bonded warehouses, re-label products, and ship within 48 hours to ASEAN shoppers. Each cross-border parcel typically uses at least one secondary folding carton, so transaction growth directly translates into additional tonnage for the Singapore folding carton market. E-tailers insist on tamper-evident designs, embedded QR codes, and robust corner protection to minimize return costs. Converters with automated CAD libraries and digital presses win these orders because they can quote, proof, and deliver runs of 3,000-15,000 cartons within a few days.

Government Push for Sustainable Packaging and Green Plan 2030

Mandatory Packaging Reporting and the interim 20% landfill-reduction target for 2026 accelerate corporate moves toward recyclable substrates.[1]Singapore Government, “Our Targets,” GREENPLAN.GOV.SG Folding-carton producers able to document Forest Stewardship Council (FSC) chain-of-custody status and minimum recycled-fiber thresholds now enjoy preferred-supplier status with global FMCG buyers operating in Singapore. Many beverage brands also use folding cartons to replace polyethylene terephthalate (PET) multipack rings, taking advantage of a regulatory gap because cartons currently fall outside the beverage-container deposit scheme.

Growth of Ready-to-Eat Meal Deliveries Boosting Folding Carton Usage

Takeaway meals ordered through platform apps grew sharply during and after the pandemic, and ghost kitchens continue to proliferate in mixed-use urban districts. Regulators have signaled the possibility of fees on single-use plastic food containers, prompting operators to switch to grease-resistant Coated Unbleached Kraft clamshells and Folding Boxboard sleeves. Grants under the Productivity Solutions Grant offset pilot tooling costs, lowering financial barriers for small caterers. Every shift away from plastic clamshells adds to the Singapore folding carton market.

Technological Advancements in Digital Printing for Short Runs

A workflow that couples pre-press automation with a seven-color inkjet press can turn around 2,500-sheet orders without costly make-ready. Such agility serves promotional campaigns, localized flavor launches, and ecommerce subscription boxes. The set-up translates into less waste and sharply lower labor hours critical in a jurisdiction where the Local Qualifying Salary rises to SGD 1,800 in 2026, and foreign-worker levies increase again in 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Land and Labor Costs Limiting Local Production Capacity | -0.8% | National, Jurong and Woodlands | Short term (≤ 2 years) |

| Competition From Lower-Cost Imports From Malaysia and China | -0.6% | National, commodity grades | Short term (≤ 2 years) |

| Limited Domestic Recovered Fiber Constraining Recycled Board Adoption | -0.3% | National | Medium term (2-4 years) |

| Volatility in Virgin Paperboard Prices Linked to Global Pulp Markets | -0.2% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Land and Labor Costs Limiting Local Production Capacity

Industrial rents keep trending higher while labor reforms raise minimum salaries and levies, inflating fixed costs for converters. The larger Singapore folding carton market must therefore be served through a two-track supply chain: regionally produced commodity cartons flow in from Malaysia and Indonesia, while local plants concentrate on short-run, premium, or IP-sensitive jobs. Automation investments in robotic die-cutting and AI vision systems aim to close the cost gap but require significant upfront capital.[2]Ministry of Trade and Industry, “Business Cost Conditions in Singapore’s Manufacturing and Services Sectors,” MTI.GOV.SG

Competition From Lower-Cost Imports From Malaysia and China

Integrated Malaysian producers ship corrugated and folding cartons overland within 24 hours, often at a landed cost 25%-30% lower than a Singapore converter can match. Chinese exporters exploit scale economies in pulp procurement and vertically integrated board production, quoting aggressive prices on high-volume sizes. Local converters safeguard niches that require complex structural design or regulatory traceability, yet margin erosion persists for commodity SKUs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Coated Unbleached Kraft Remains Dominant but Folding Boxboard Gains Ground

Coated Unbleached Kraft captured 33.87% of the Singapore folding carton market share in 2025 as beverage carriers, frozen-food sleeves, and greasy snack packs favor its wet strength and barrier coatings. The grade fits within municipal recycling streams and carries FSC tags, aligning with brand-owner pledges under the Green Plan 2030. Folding Boxboard, however, is pegged to outpace overall market growth at a 5.53% CAGR to 2031. Its smooth, clay-coated surface, superior brightness, and high stiffness support embossing, foil stamping, and crisp offset graphics demanded by premium cosmetics and nutraceutical brands. Converters that stock both substrates can recommend optimal grammage, barrier lamination, and post-press embellishment, strengthening their consultative role and capturing a larger share of the Singapore folding carton market as ASPs rise.

Demand for Solid Bleached Sulfate remains sticky in pharmaceutical cartons where stringent purity and optical requirements limit substitution. White Line Chipboard serves low-budget household goods, leveraging recycled content to satisfy corporate sustainability metrics at a lower cost per ton. Specialty grades, including dispersion-coated and plant-based polymer-lined boards, address microwave-safe food trays and modified-atmosphere packs, though volumes are currently limited by qualification cycles. As importers of luxury confectionery lean on unboxing theatrics to justify premium price tags, Folding Boxboard’s tactile finish and structural rigidity become decisive.

By Printing Technology: Lithography Anchors Scale, While Digital Unlocks Agility

Lithographic presses accounted for 40.52% of output value in 2025, with their cost-per-thousand advantage kicking in once run lengths exceed 15,000 sheets for unified campaigns across Singapore and neighboring ASEAN territories. Inline cold-foil stations and high-gloss overprint varnishes cater to beverage giants that need Pantone-matched shades across 20+ markets. The digital printing cohort is growing at 5.96% CAGR, driven by SKU proliferation, personalization, and omnichannel retail cycles. A converter that runs a seven-color, 650 mm-wide digital press can handle roll-to-roll jobs, then sheet-convert for gluing within hours, shrinking order-to-ship intervals. The technique also allows serialized codes for regulation-mandated track and trace, a capability increasingly mandatory for pharmaceuticals and high-value cosmetics, thereby deepening penetration of the Singapore folding carton market.

Flexographic units cover functional yet lower-graphic corrugated inserts and shipper cartons for e-commerce, while gravure remains confined to ultra-high-volume beverage and tobacco bundles where cylinder investments amortize. Hybrid lines that integrate offset, inkjet, and digital embellishment modules may emerge as the sweet spot, marrying litho-grade visuals with SKU agility. As brand owners press for late-stage customization, litho incumbents risk share loss if plate-dependent workflows cannot accelerate. Digital leaders, by contrast, can upsell variable text, seasonal artwork, and QR-linked loyalty programs, capturing higher margins in the Singapore folding carton market size spectrum.

By End-User Industry: Food and Beverage Leads, E-Commerce Races Ahead

The food and beverage vertical, with 30.23% revenue contribution in 2025, reflects Singapore’s outsized role as a value-adding node for regional dairy, plant-based drinks, ready-to-drink coffee, and premium confectionery. Multinationals frequently print multi-language panels on folding cartons to comply with destination-country labeling, boosting print-order complexity and unit value. Yet the e-commerce and retail-ready channel is projected to grow at 6.14% CAGR through 2031, as subscription boxes and direct-to-consumer drops adopt compact crash-lock cartons with tamper-evident sidewalls. Packaging design now doubles as a brand’s first physical point of contact with shoppers, so eye-catching cartons gain marketing clout.

Healthcare and pharmaceuticals are long-term demand anchors, propelled by an aging population and heightened serialization requirements. Personal care and cosmetics players commission limited-edition boxes with soft-touch lamination, magnetic lids, and foil debossing, elevating average selling prices and boosting the Singapore folding carton market. Electrical and electronics segments rely on antistatic inserts and robust outer sleeves for small consumer gadgets. Tobacco’s gradual contraction, owing to plain-pack legislation and falling consumption, places a ceiling on gravure carton volumes. Emerging niches such as craft-beverage six-packs and pet-nutrition sachet boxes create additional, though smaller, avenues of value.

Geography Analysis

A large proportion of folding cartons consumed in the Singapore folding carton market arrives from neighboring Malaysia and Indonesia, reflecting cost arbitrage and complementary production footprints. Malaysian converters enjoy streamlined customs processes at the Johor-Singapore Causeway, enabling just-in-time deliveries for FMCG lines located in western Singapore. Cartons perfected and die-cut in Johor can cross the border and proceed directly into automated filling lines within a single shift, highlighting the integrated regional logistics web.

Indonesia and Vietnam have attracted multimillion-dollar investments from global carton majors seeking to balance proximity and cost efficiency. When lead times tolerate slightly longer transit windows, converters tap Batam or Binh Duong factories for high-volume litho runs, shipping flat blanks into Singapore for final gluing, window patching, or specialty coating. Such a hub-and-spoke configuration lets brand owners hedge supply-chain risk without tying up working capital in Singapore’s costlier industrial real estate.

High-value, short-run, and IP-sensitive work continues inside the city-state. Pharmaceutical, luxury cosmetics, and regulatory prototype jobs rely on domestic prepress and converting capacity protected by stringent clean-room protocols and data security measures. Proximity to Changi Airport also permits emergency airfreight of time-critical cartons to distant ASEAN plants, preserving Singapore’s role as a control tower over regional folding-carton flows. These location dynamics collectively shape the revenue pie of the Singapore folding carton market.

Competitive Landscape

Global board producers and carton converters such as Tetra Pak, Mondi, and Stora Enso orchestrate regional supply chains that feed Singapore with competitively priced blanks and finished cartons. Tetra Pak’s EUR 97 million (USD 115 million) investment to more than double aseptic carton output in Vietnam exemplifies a network strategy that lowers cost-to-serve for Singaporean dairy and beverage fillers.[3]Vietstock, “Tetra Pak’s Bình Dương Plant to Power Beverage Carton Packaging Supply,” VIETSTOCK.VN Mondi’s April 2026 joint-venture commitment to manufacture 200 million paper bags annually in Indonesia signals broader regional scaling to secure volume and resource gravity.[4]MarketScreener, “Mondi Expands Paper Bags Business in Southeast Asia,” MARKETSCREENER.COM

Local converters, including Paper Products Singapore and LSY Packaging, answer by investing in digital presses, robot-assisted die-cutting, and ERP-to-CAD integration. Their proximity advantage enables artwork turnaround in under 24 hours, on-site microbiological audits, and small-batch production for marketing pilots. To lock in compliance-conscious customers, many carry ISO 9001 and FSC certificates, run lean Six Sigma workflows, and now deploy AI camera vision systems that stop lines if die-cut windows shift by more than 0.2 mm. Rising import competition squeezes margins, yet knowledge of local regulations, multilingual artwork, and sustainability reporting keep entrenched firms relevant in the Singapore folding carton market.

Several niche disruptors champion compostable coatings formed from plant-based polymers or sugarcane bagasse, promising moisture resistance without polyethylene. Others bundle serialization, cloud dashboards, and blockchain-anchored traceability, addressing pharmaceutical anti-counterfeit mandates and luxury brand authentication. As green-finance funds grow, converters able to evidence decarbonization paths access cheaper capital for digital and robotic upgrades. Competitive dynamism, therefore, hinges on technology adoption, compliance rigor, and regional orchestration rather than sheer press capacity.

Singapore Folding Carton Industry Leaders

Mayr-Melnhof Karton AG

Rengo Co. Ltd

Stora Enso Oyj

Mondi plc

Tetra Pak International S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Mondi formed a joint venture with PT Indocement Tunggal Prakarsa to install a paper-bag line capable of 200 million units per year at the Citeureup Cement Factory Complex, West Java, with operations slated for late 2026.

- April 2026: In response to the National Environment Agency’s (NEA) 2025 guidelines to reduce e-commerce packaging, major logistics providers in Singapore integrated optimized 3R (Reduce, Reuse, Recycle) folding carton solutions to replace plastic mailers, targeting a significant reduction in domestic packaging waste.

- February 2026: Singapore’s Ministry of Trade and Industry reported a 0.1% rise in the 2025 manufacturing unit business cost index, flagging short-term cost stability for converters ahead of levy hikes effective 2028.

- July 2025: Tetra Pak commissioned a second aseptic-carton line at its Binh Duong, Vietnam plant, lifting annual capacity beyond 30 billion packs and earmarking Singapore as a key beneficiary.

Singapore Folding Carton Market Report Scope

The report provides a comprehensive analysis of the folding carton market in Singapore. It examines the current trends, growth drivers, challenges, and opportunities in the market. The scope of the study includes an evaluation of market dynamics, competitive landscape, and key developments. Additionally, the report covers supply chain analysis, market segmentation, and forecasts for the study period.

The Singapore Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the Market size of the Singapore folding carton market?

The Singapore Folding Carton Market size is projected to be USD 244.73 million in 2025, USD 259.81 million in 2026, and reach USD 311.67 million by 2031, growing at a CAGR of 3.71% from 2026 to 2031.

Which material dominates demand in Singapore folding cartons?

Coated Unbleached Kraft leads with 33.87% market share as of 2025, favored for beverage multipacks and frozen-food sleeves.

How fast is digital printing for folding cartons growing in Singapore?

Digital printing is forecast to rise at a 5.96% CAGR between 2026 and 2031 as brands pursue mass customization and shorter promotional cycles.

Why are folding cartons gaining ground over plastic packaging?

The Green Plan 2030 pushes landfill-waste cuts and deposit schemes that exclude paperboard, motivating brand owners to substitute recyclable cartons for rigid plastics.

What effect do high land and labor costs have on local converters?

Elevated operating expenses incentivize automation or regional outsourcing, causing many commodity cartons to be imported while domestic plants focus on premium short runs.

Which end-user sector shows the fastest growth?

E-commerce and retail-ready packaging is expanding at a 6.14% CAGR, powered by direct-to-consumer shipments and shelf-ready designs.

Page last updated on: