Russia Mining Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

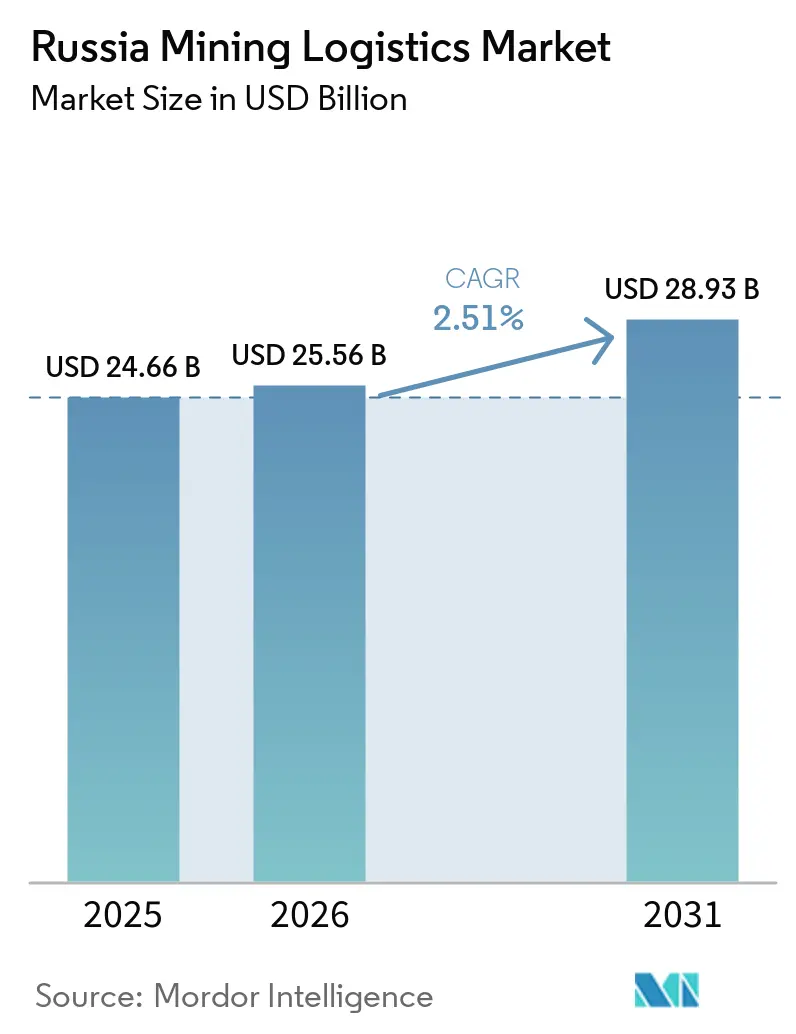

| Base Year Market Size (2025) | USD 24.66 Billion |

| Market Size (2026) | USD 25.56 Billion |

| Market Size (2031) | USD 28.93 Billion |

| Growth Rate (2026 - 2031) | 2.51% CAGR |

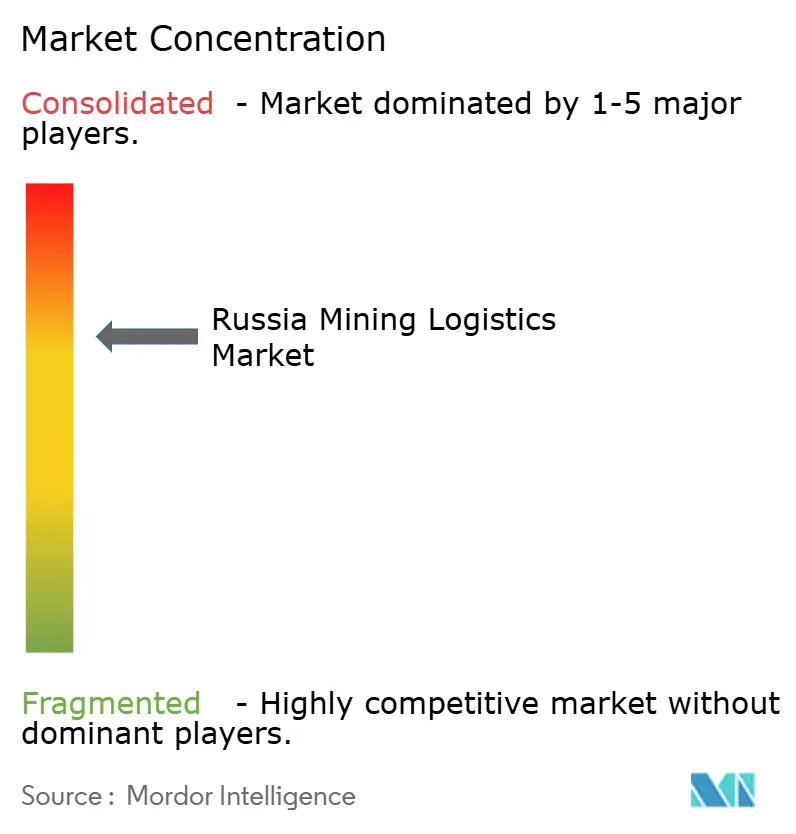

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Mining Logistics Market Analysis by Mordor Intelligence

The Russia mining logistics market size was valued at USD 24.66 billion in 2025 and estimated to grow from USD 25.56 billion in 2026 to USD 28.93 billion by 2031, registering a CAGR of 2.51% during the forecast period (2026-2031).

Russia’s broad output across coal, base metals, iron ore, and gold keeps freight demand active even as sanctions and rerouted trade lanes pressure margins on some export flows. The Eastern Polygon corridor surpassed 180 million tons of annual cargo capacity by late 2024, confirming that the main logistics pivot is now centered on Far Eastern ports and China-facing border crossings. Rail shipments to China through the Russian Railways network reached 62.7 million metric tons in January to April 2026, up 3% year over year, indicating that the Russia mining logistics market is still supported by corridor redirection even as the wider rail network is under pressure. Long-term infrastructure commitments on the BAM and Trans-Siberian systems, together with Lavna's rise in Murmansk, are widening route choice and reducing dependence on a single outlet. The shift to compulsory electronic freight documentation from 2026 is also pushing the Russia mining logistics market toward lower friction, better shipment visibility, and higher demand for bundled service models.

Key Report Takeaways

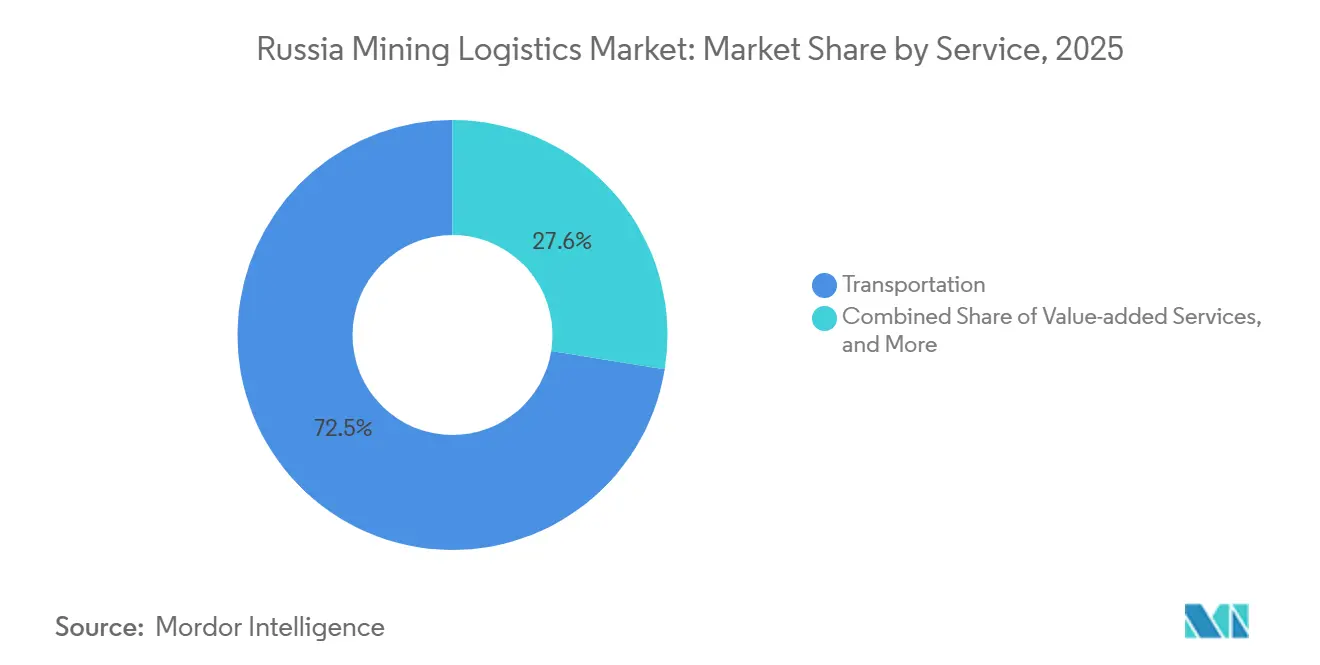

- By service, transportation held 72.45% of the Russia mining logistics market share in 2025, while value-added services are projected to grow at a 2.97% CAGR through 2031.

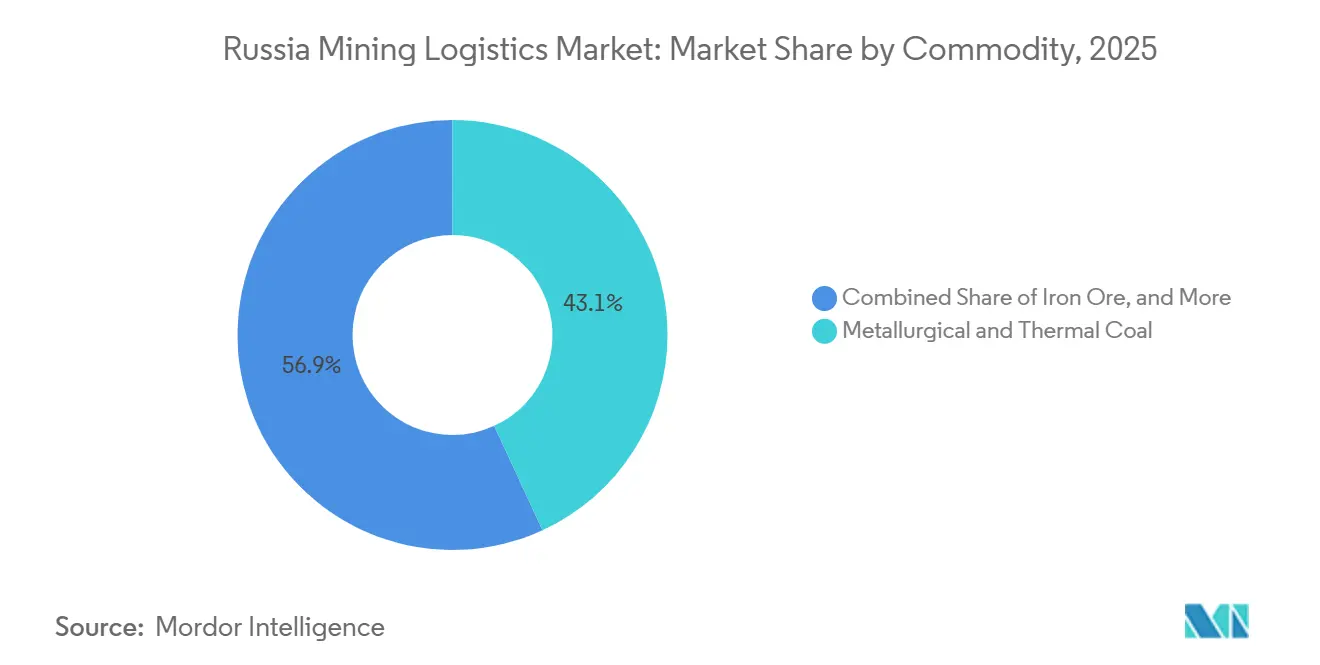

- By commodity, metallurgical and thermal coal accounted for 43.13% of the Russia mining logistics market size in 2025, while base metals are forecast to expand at a 3.03% CAGR through 2031.

- By geography, Siberia held 57.79% of the Russia mining logistics market share in 2025, while the Russian Far East is expected to record the fastest growth at a 3.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Mining Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Eastbound export corridor reorientation | +0.7% | Russian Far East, Siberia, Ural, with spillover to Central Russia | Short term (≤ 2 years) |

| BAM and Trans-Siberian capacity upgrades | +0.6% | Siberia, Russian Far East | Long term (≥ 4 years) |

| Far East terminal capacity expansion | +0.4% | Russian Far East | Medium term (2-4 years) |

| Digital freight orchestration and visibility | +0.2% | National, with early gains in Siberia, Northwest Russia, and the Russian Far East | Medium term (2-4 years) |

| Private mine-to-port logistics chains | +0.3% | Russian Far East, Eastern Siberia | Medium term (2-4 years) |

| Lavna and arctic outlet optionality | +0.2% | Northwest Russia, with export flows to Asia-Pacific and India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Eastbound Export Corridor Reorientation Accelerates Rail Demand

The structural shift away from European export routes and toward Asia-facing gateways remains the clearest volume driver in the Russia mining logistics market. Rail shipments to China through the Russian Railways network rose 3% year over year to 62.7 million metric tons in January to April 2026, while container throughput at the Zabaikalsk border crossing climbed 32% to 197,400 TEU over the same period. Russia and China also agreed in May 2026 to build a second main track at the Zabaikalsk to Manchuria crossing, and that project is expected to add 11 million tons of annual capacity by 2030 and support up to 50 train pairs per day. This corridor shift matters for revenue as well as volume because longer Asia-bound hauls raise logistics spend per ton even when unit transport pricing does not change. That combination is keeping the Russia mining logistics market supported by route length, border capacity, and continued redirection of export demand toward eastern channels[1]“Rail Shipments to China via Russian Railways Network Rise by 3% in January-April,” TASS Business & Economy, tass.com.

BAM and Trans-Siberian Capacity Upgrades Redefine the Infrastructure Ceiling

The Russian government’s RUB 3.74 trillion (USD 38 billion) investment program in the supplied draft gives the Russia mining logistics market its clearest long-term capacity signal. The third stage of the Eastern Polygon aims to increase throughput from 180 million tons to 210 million tons by 2030, and then to 270 million tons by 2032. The work covers major BAM bottlenecks, including additional tunnel capacity, bridge construction, and expansion of key sections that carry mining cargo toward the Pacific. This matters because mining shippers still need capacity that is commercially available and physically usable, not only capacity that has been announced. The program therefore sets the long-run ceiling for the Russia mining logistics market, even though near-term delivery will still depend on execution speed and slot allocation discipline[2]Capacity to Be Increased on Siberian Main Lines,” Railway Gazette International, railwaygazette.com.

Far East Terminal Capacity Expansion Deepens Export Optionality

Port investments along the Pacific coast are creating a broader outlet base for the Russian mining logistics market. Coal exports through Vanino ports increased 50.3% in 2025 to 36.3 million tons, underscoring how heavily shippers relied on Far Eastern terminals. The launch of the Blagoveshchensk Dry Port in May 2026 added a new rail-handling point with an initial capacity of 520,000 tons per year, rising to 1 million tons by 2030. The federal target to add 136 million tons of Far East port capacity by 2036 gives operators and mining groups a long planning horizon for terminal and inland investment. These additions are widening destination choice inside the Russia mining logistics market, even though rail access still determines how much of that terminal capacity can be used in practice[3]“Eastern Polygon Freight Turnover Rose 2.7% in January-April 2025,” PortNews, portnews.ru.

Digital Freight Orchestration Transforms Mine-To-Port Visibility

Transport document digitalization is changing how the Russia mining logistics market handles dispatch, handover, and compliance. Electronic transport waybills become compulsory for virtually all freight movements from September 1, 2026 under Federal Law No. 140-FZ, which means mining cargo chains must connect to the state electronic document environment. The operational effect is likely to be lower paperwork friction, faster exception handling, and better shipment traceability across rail, terminal, and brokerage activity. This shift also favors providers that can combine physical freight with document management, rather than those that offer only wagons, trucks, or port slots. As a result, the Russia mining logistics market is moving toward bundled contracts where digital execution becomes part of the service value, not a separate add-on.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rail bottlenecks and last-mile congestion | -0.5% | Russian Far East, Siberia | Short term (≤ 2 years) |

| Tariff inflation and equipment-spares shortages | -0.4% | National, with concentrated impact in Siberia and the Russian Far East | Short term (≤ 2 years) |

| Elga-Pacific corridor climate fragility | -0.2% | Russian Far East, especially Yakutia and Khabarovsk | Medium term (2-4 years) |

| Rail-port capacity mismatch | -0.3% | Russian Far East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rail Bottlenecks and Last-Mile Congestion Constrain Throughput Efficiency

Congestion across the Eastern Polygon remains the most direct operating constraint on the Russia mining logistics market. The issue is not only mainline rail capacity, because the network also has to balance bulk mining cargo against faster-growing container and fertilizer traffic that competes for the same eastbound slots. Eastern Polygon freight turnover reached record levels in early 2025 as containers, fertilizers, and non-ferrous metals all advanced, which increased the pressure on path allocation for coal and other bulk flows. Policy decisions also shape the outcome, as shown by support for a 60 million ton Kuzbass coal export quota to the east in 2026. This means the Russia mining logistics market still faces a bottleneck at the point where infrastructure, commodity priority, and final branch-line connectivity meet.

Tariff Inflation and Equipment-Spares Shortages Erode Operator Margins

Cost pressure is another clear cap on the Russia mining logistics market. Rail freight tariffs were indexed upward by 10% from December 1, 2025, and that step followed a year when logistics costs were already rising faster than miners wanted to absorb. The effect is most visible in coal, where transport is a large share of delivered cost and margin erosion quickly changes shipment economics. At the same time, sanctions have made maintenance and equipment support more difficult, which is why domestic industrial responses such as the BelAZ and Nornickel haul-truck factory project have gained strategic weight. The combined result is that the Russia mining logistics market can still grow, but part of that growth is being offset by higher cost per move and more pressure on fleet serviceability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Value-Added Services Gain Share as Integrated Solutions Command a Premium

Transportation held 72.45% of the Russia mining logistics market share in 2025, which kept the service mix anchored to long-haul mineral freight. Rail remained the core mode because cargo often moves 3,000 to 4,000 km from Siberian and Yakutian deposits to Pacific ports. That rail movement depended on RZD infrastructure and a set of large private wagon operators, including Freight One, Globaltrans, and NefteTransService, that supply equipment and route coverage across the main export corridors. Road transport supported the first mile and last mile around mines and transfer points, especially where dispatch flexibility mattered more than line-haul efficiency. Sea and inland waterways added seasonal support for Arctic and Siberian operations, while air freight remained limited to urgent spare parts and high-value equipment.

Value-added services are projected to grow at a 2.97% CAGR through 2031, making them the fastest-growing service category in the Russia mining logistics market. Demand is rising for customs clearance, bonded warehousing, cargo inspection, and electronic waybill compliance as the transport document regime becomes more formalized from September 2026. Providers that can combine rail booking, terminal handling, brokerage, and documentation should widen revenue per customer even if pure haulage margins stay tight. Warehousing and inventory management also keep a strategic role in Kuzbass and the Ural regions because stockpile capacity helps miners manage uneven rail access and release cargo when slots reopen. This is pushing the Russia mining logistics industry toward broader, end-to-end contracts rather than isolated transport tasks[4]“Eastern Coal Exports via RZD Hit Record 118.2 Million Tons,” PortNews, portnews.ru.

By Commodity: Coal Anchors Volume, Base Metals Drive Value Growth

Metallurgical and thermal coal accounted for 43.13% of the Russia mining logistics market size in 2025, which left coal as the largest single commodity revenue base. Eastbound coal exports through the RZD network reached a record 118.2 million tons in 2025, while total coal exports held at 177 million tons. Iron ore flows stayed concentrated around the Ural and Northwest Russia systems, where inland supply connects with domestic steel capacity and selected export routes. Gold volumes remained modest in tonnage terms, but these shipments generated stronger revenue per ton because of security handling, insurance, and selective air freight needs. Other minerals also became more demanding from a logistics standpoint as non-ferrous ore shipments on the Eastern Polygon rose 36.2% in January to April 2025.

Base metals are forecast to grow at a 3.03% CAGR through 2031, the fastest pace among commodity groups in the Russia mining logistics market. Nornickel stated in April 2026 that it had rerouted seaborne metals exports around Africa due to the Iran-United States conflict, extending transit times by 3 weeks while maintaining its output and delivery commitments. That shift matters because longer routes keep freight demand active even when shipment volumes do not jump sharply. It also pulls more attention toward schedule control, secure handling, and reliable export sequencing for copper, nickel, and zinc cargo. In that sense, the Russia mining logistics industry is gradually drawing more value from complex metal flows than from bulk coal alone.

Geography Analysis

Siberia held 57.79% of the Russia mining logistics market share in 2025, making it the country’s largest logistics base for mining cargo. Kuzbass and Yakutia keep the region central to coal exports, while Krasnoyarsk and Irkutsk add large flows of metals and ore. Elga produced 35.1 million tons in 2025 and began construction of the second track of its Pacific Railway in April 2025, which shows how output growth and private infrastructure are moving together. This scale means Siberia will remain the core freight origin zone for the Russia mining logistics market through the forecast period.

The Russian Far East is projected to expand at a 3.15% CAGR through 2031, the fastest regional pace in the Russia mining logistics market. Vanino ports handled 36.3 million tons of coal exports in 2025, up 50.3%, which underlines the region’s role as the main release valve for eastbound shipments. The Blagoveshchensk Dry Port started operations in May 2026 with capacity of 520,000 tons per year and is planned to reach 1 million tons by 2030. Federal plans to add 136 million tons of Far East port capacity through 2036 support further deployment of terminals and inland links across the region. Even so, actual throughput will continue to depend on rail access and slot discipline more than on port nameplate capacity alone.

Northwest Russia gained stronger relevance after Lavna reached 12 million tons of annual capacity in January 2026, giving Kuzbass coal a new outlet outside the main Pacific route set in the Russia mining logistics market. Central Russia and the Ural Region still matter as processing and transit zones that connect inland ore and coal flows with steelmaking and export chains. Southern Russia and the Caucasus handle smaller mining volumes, but the corridor is becoming more relevant for cargo moving toward Turkish, Iranian, and Arabian Peninsula buyers. This regional spread is making the country less dependent on any single port system, even though eastern corridors still set the pace of expansion.

Competitive Landscape

The Russia mining logistics market shows moderate to high concentration because RZD controls the national rail network and therefore the base terms of access for the largest freight flows. A group of large private wagon operators, led by Freight One, Globaltrans, and NefteTransService, still competes for fleet positioning and route access on the most constrained corridors. FESCO stands out as the main integrated intermodal player because it combines Far Eastern port handling, shipping services, and rail operations in one platform. In March 2026, FESCO signed cooperation agreements with China’s NOVA Supply Chain Management and Neptune Logistics to expand cross-border rail container services. Those moves show that the advantage in the Russia mining logistics market is shifting toward corridor coordination and service bundling rather than simple asset ownership.

A separate model is emerging through dedicated mine-to-port systems inside the Russia mining logistics market. Elga’s Pacific Railway has become the country’s first privately owned freight main line in this space, which gives the project a route structure that is less exposed to RZD tariff and slot decisions. That matters for large mining groups because captive infrastructure can protect export timing and reduce dependence on public-network congestion. Ownership is also becoming more domestic and more concentrated after Globaltrans sold its Russian operating subsidiaries in 2025 for USD 766.8 million. The field is therefore narrowing toward locally controlled operators with stronger influence over wagons, terminals, and corridor strategy.

Digital capability is becoming the clearest competitive separator in the Russia mining logistics market as compulsory electronic freight documentation approaches. Operators that can combine GIS EPD compliance, booking visibility, customs services, and terminal execution are better placed to win full-chain mining contracts. TransContainer’s 2025 loss and debt burden show that asset scale alone does not guarantee resilience when tariffs rise and rate conditions weaken. Competition is therefore moving toward dependable corridor access, higher asset productivity, and better execution across documentation and physical freight.

Russia Mining Logistics Industry Leaders

Russian Railways (RZD)

Freight One (PGK)

Globaltrans

TransContainer

FESCO Transportation Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Freight One (PGK) Irkutsk branch dispatched its first long-formation gondola train of 63 wagons (6,000 tons) from the Eastern Siberian Railway, exceeding the previous standard of 54 wagons, improving asset utilization under Eastern Polygon slot constraints.

- April 2026: FESCO Transportation Group launched a new intermodal container service between Ankara, Turkey, and Novorossiysk, Russia, via the Port of Gebze, expanding multimodal mining-adjacent connectivity to Central Asian and Middle Eastern buyers.

- April 2026: FESCO completed its first export voyage from Novorossiysk to Jeddah, Saudi Arabia, as part of the Indian Line West network, opening a new logistics corridor for Russian mineral and metal exporters toward the Arabian Peninsula.

- April 2026: Freight One (PGK) launched a RUB 15 billion (USD 170 million) bond issuance program to support its rolling stock investment plan amid accelerating fleet retirement, with annual gondola car retirements projected at approximately 3,500 units per year through 2029.

Russia Mining Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea and Inland Waterways | |

| Air | |

| Warehousing and Inventory Management | |

| Value-Added Services |

| Iron Ore |

| Metallurgical and Thermal Coal |

| Base Metals (Cu, Zn, Ni) |

| Gold |

| Other Minerals/Metals |

| Central Russia |

| Northwest Russia |

| Ural Region |

| Siberia |

| Russian Far East |

| Southern Russia and Caucasus |

| By Service | Transportation | Road |

| Rail | ||

| Sea and Inland Waterways | ||

| Air | ||

| Warehousing and Inventory Management | ||

| Value-Added Services | ||

| By Commodity | Iron Ore | |

| Metallurgical and Thermal Coal | ||

| Base Metals (Cu, Zn, Ni) | ||

| Gold | ||

| Other Minerals/Metals | ||

| By Geography | Central Russia | |

| Northwest Russia | ||

| Ural Region | ||

| Siberia | ||

| Russian Far East | ||

| Southern Russia and Caucasus |

Key Questions Answered in the Report

What is the current size of Russia’s mining logistics space?

The Russia mining logistics market stands at USD 25.56 billion in 2026 and is forecast to reach USD 28.93 billion by 2031 at a 2.51% CAGR.

Which service category generates the most revenue in Russia’s mining freight chain?

Transportation is the largest service category, with 72.45% revenue share in 2025, because long-haul rail remains essential for bulk mineral flows.

Which commodity drives the most logistics revenue in Russia?

Metallurgical and thermal coal led with 43.13% of revenue in 2025, supported by record eastbound coal exports of 118.2 million tons through the RZD network.

Which region is expanding the fastest for mining cargo handling in Russia?

The Russian Far East is the fastest-growing region, with a projected 3.15% CAGR through 2031, helped by Vanino growth, dry port additions, and planned port expansion.

Why are value-added logistics services growing faster than transport alone in Russia?

They are growing at a 2.97% CAGR because miners increasingly need customs support, warehousing, inspection, and electronic freight document compliance alongside physical transport.

What is the biggest operating challenge for mining cargo in Russia?

The main challenge is corridor congestion on the Eastern Polygon, where mining cargo must compete with other traffic types for limited eastbound slots, while tariffs and equipment support issues add cost pressure.

Page last updated on: