Russia Warehousing And Storage Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

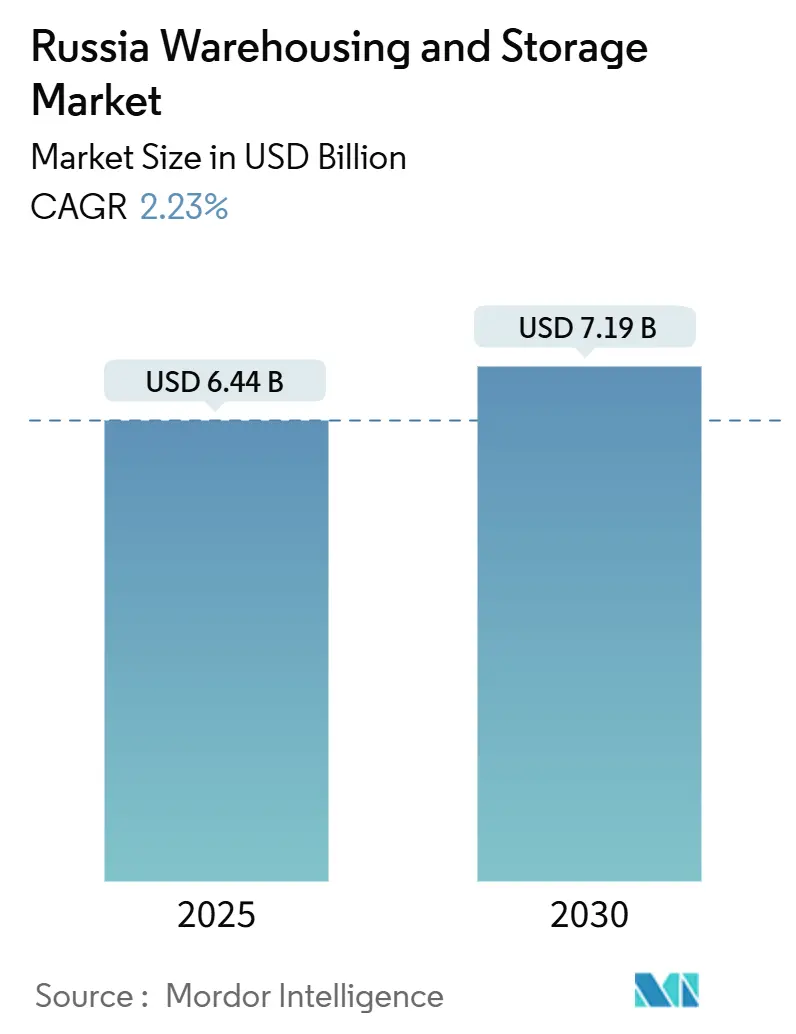

| Market Size (2025) | USD 6.44 Billion |

| Market Size (2030) | USD 7.19 Billion |

| Growth Rate (2025 - 2030) | 2.23% CAGR |

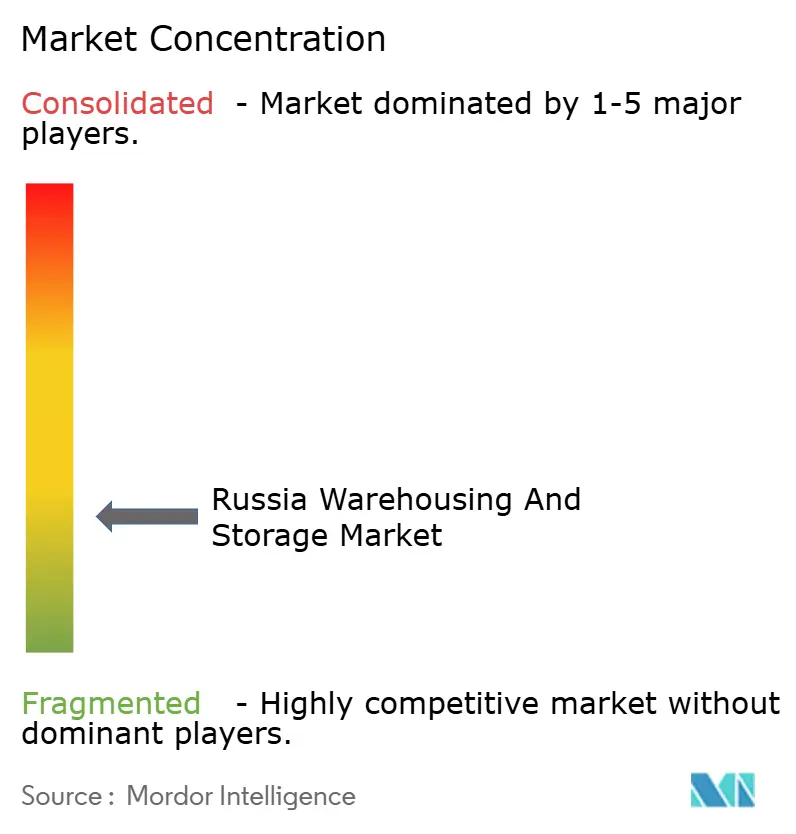

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Warehousing And Storage Market Analysis by Mordor Intelligence

The Russia Warehousing And Storage Market size is estimated at USD 6.44 billion in 2025, and is expected to reach USD 7.19 billion by 2030, at a CAGR of 2.23% during the forecast period (2025-2030).

This moderate expansion is underpinned by government‐led infrastructure spending, regional e-commerce penetration, and rising cold-chain investments that collectively offset geopolitical headwinds. Structural adaptation, notably the turn toward import-substitution and “friend-shoring” trade corridors, supports sustained demand for storage space across Russia’s vast geography. Operators are reallocating capital toward regional fulfillment hubs, cold storage complexes, and multimodal facilities that leverage new rail and Northern Sea Route capacity. Technology adoption receives a strong push from labor shortages, with domestic warehouse management systems and automation solutions progressively replacing restricted Western equipment.

Key Report Takeaways

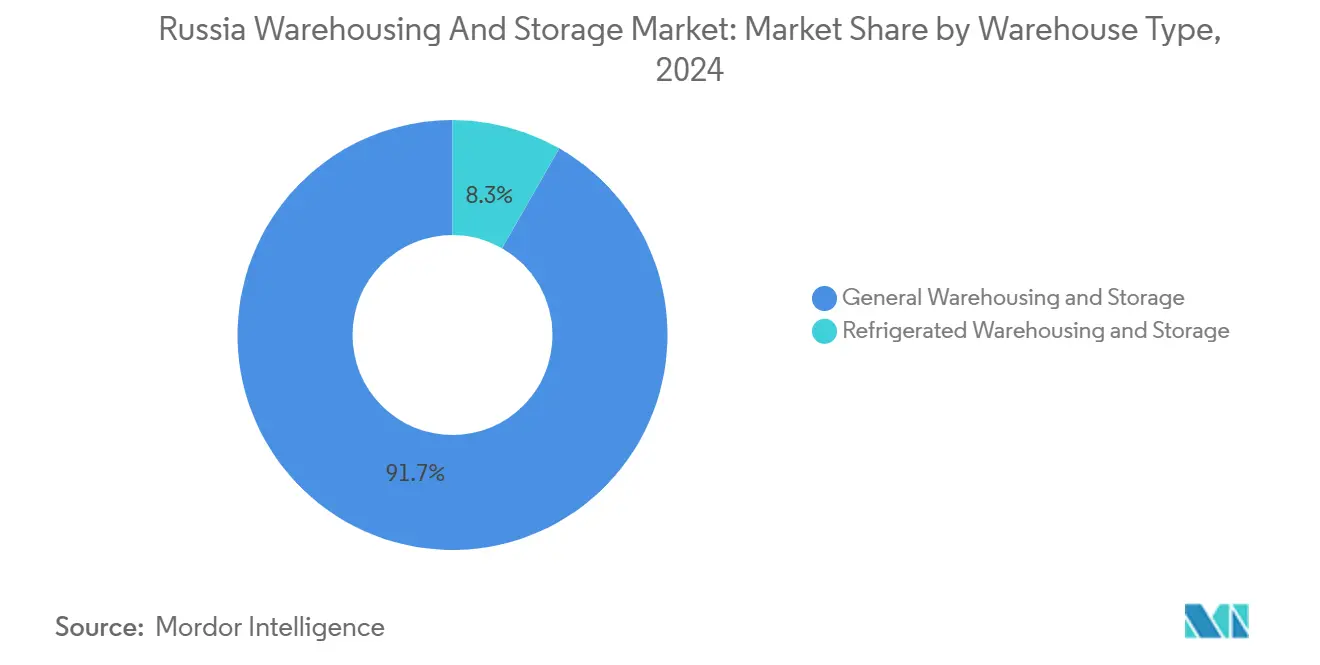

- By warehouse type, general warehousing and storage dominated with 91.74% of Russia warehousing and storage market share in 2024 while refrigerated warehousing and storage recorded the fastest 2.79% CAGR through 2030.

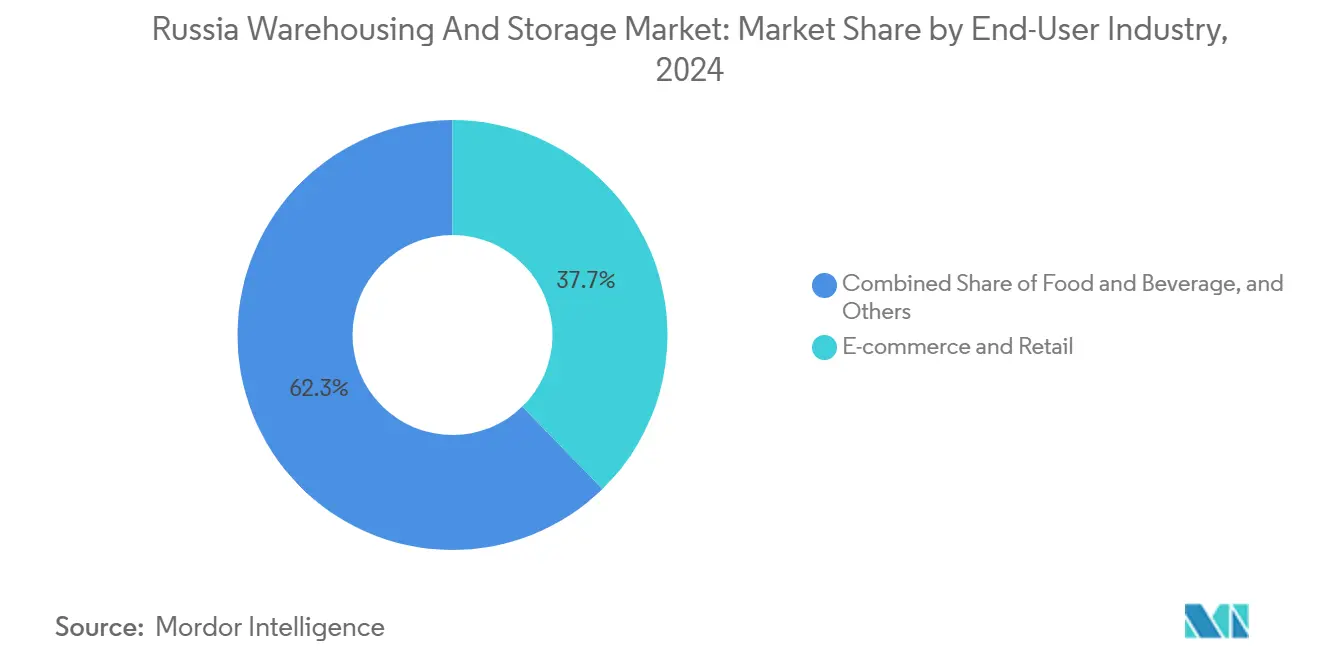

- By end-user industry, e-commerce and retail commanded 37.70% of the Russia warehousing and storage market size in 2024, and is projected to expand at a 2.85% CAGR to 2030.

Russia Warehousing And Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of e-commerce fulfillment demand beyond Moscow and St Petersburg | +0.8% | National, with early gains in Kazan, Yekaterinburg, Novosibirsk | Medium term (2-4 years) |

| Government incentives for domestic cold-chain infrastructure | +0.4% | National, concentrated in agricultural regions and Arctic zones | Long term (≥ 4 years) |

| Localization push amid import-substitution policies driving inventory buffering | +0.3% | National, with emphasis on manufacturing hubs | Short term (≤ 2 years) |

| Rising adoption of warehouse automation and WMS in Russian 3PLs | +0.2% | Moscow, St Petersburg, major industrial centers | Medium term (2-4 years) |

| Development of multimodal logistic corridors via NSR and Belt-and-Road | +0.3% | Arctic regions, Far East, border zones with China | Long term (≥ 4 years) |

| Growing demand for near-border "friend-shoring" hubs serving CIS and Central Asia | +0.2% | Western borders with Belarus, southern regions near Kazakhstan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of E-commerce Fulfillment Demand Beyond Moscow and St Petersburg

Regional online retail growth fuels the Russia warehousing and storage market as marketplaces establish fulfillment centers in secondary cities for faster last-mile delivery. Yandex.Market’s 70,000 m² hub in Kazan processes more than 100,000 orders daily and created 2,500 jobs, highlighting regional scale requirements. Fix Price’s USD 43 million (RUB 4 billion) facility near Kazan supports 3,000 stores across central Russia, signaling retailer commitment to decentralized networks. Consumer expectations have shifted to 24-48 hour delivery in most urban areas, driving higher safety-stock levels and multi-node distribution strategies. E-commerce penetration outside the two largest cities remains below 15% versus 25% in metropolitan areas, leaving ample runway for warehousing expansion. Municipal authorities offer land and utility incentives, accelerating project timelines for developers targeting these underserved catchments[1]“Transport Infrastructure Development Program 2024-2028,” Government of Russia, government.ru.

Government Incentives for Domestic Cold-Chain Infrastructure

The Ministry of Agriculture earmarked RUB 12 billion (USD 111.04 million) in 2024 for cold-storage construction, with preferential loans at 3% versus benchmark rates above 20%. RZD Logistics enlarged its refrigerated terminal network by 30%, adding Novosibirsk, Yekaterinburg, and Primorsky Krai to serve meat shuttle services to China. Arctic development policy allocates RUB 15 billion (USD 138.80 million) for temperature-controlled depots that sustain year-round food flows via the Northern Sea Route. Cold-chain utilization already exceeds 85% in major cities, encouraging private-sector participation despite elevated building costs. Compliance with international food-safety standards (-25 °C to +25 °C) attracts export-oriented producers, anchoring long-term demand for specialized space[2]“Cold Storage Infrastructure Subsidies,” Ministry of Agriculture of Russia, mcx.gov.ru.

Localization Push Amid Import-Substitution Policies Driving Inventory Buffering

Domestic sourcing incentives, including a 15% price preference for local suppliers in public tenders, compel manufacturers to increase on-hand stock. Average inventory holding periods have risen 40-60 days since 2022, boosting demand for general storage capacity near production clusters. Automotive producers now retain components for 90-120 days, triple prior levels, to mitigate supply-chain risk. Parallel-import channels, although useful, require additional inspection space to satisfy compliance controls. The Federal Antimonopoly Service reported capacity utilization of domestic plants lifting to 78% in 2024, up from 65% the previous year, reinforcing the need for expanded warehousing to accommodate raw materials and finished goods.

Rising Adoption of Warehouse Automation and WMS in Russian 3PLs

Labor shortages estimated at 1.5 million vacancies across logistics have accelerated automation uptake. Sixty percent of facilities have begun partial mechanization, though only 3% are fully robotized. Domestic WMS vendors captured the bulk of the RUB 5-6 billion (USD 46-55 billion) software market in 2024, as Western solutions became restricted. LemanA PRO installations delivered 4× faster order processing and trimmed workforce needs by 35% while reaching 99.8% accuracy. X5 Group’s in-house WMS now orchestrates 1 million SKUs across 15 distribution centers, setting a template for retail automation. Local equipment suppliers report 12-18 month order backlogs, indicating sustained investment momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical sanctions restricting access to western material-handling tech | -0.4% | National, most severe in high-tech logistics hubs | Short term (≤ 2 years) |

| Volatile ruble and high interest rates inflating construction / operating costs | -0.3% | National, with regional variations in cost impact | Short term (≤ 2 years) |

| Regional labour shortages in Siberia and Far East limiting capacity ramp-up | -0.2% | Siberia, Far East, Arctic regions | Medium term (2-4 years) |

| Limited high-quality Class A space outside top two federal districts | -0.1% | Regional markets excluding Moscow and St Petersburg | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Geopolitical Sanctions Restricting Access to Western Material-Handling Technology

Export controls have eliminated direct supply of advanced automated storage systems and software from Europe and North America. Russian operators rely on parallel-import channels, which double acquisition costs and provide no OEM maintenance support. Domestic substitutes generally meet only 60-70% of desired performance, forcing facilities to mix legacy manual processes with local automation. High-throughput e-commerce centers feel the pinch most acutely, postponing rollout of high-speed sorters until local engineering capabilities mature. Certification under ISO 9001 and ISO 14001 remains possible but now entails longer validation cycles due to equipment origin checks[3]“Domestic Supplier Preferences,” Government Procurement Portal, zakupki.gov.ru.

Volatile Ruble and High Interest Rates Inflating Construction / Operating Costs

Warehouse construction costs surged to RUB 35,000-40,000 per m² in 2024, a 25% jump year-on-year, as imported materials and equipment became more expensive amid currency swings. The Central Bank maintained a 21% key rate, lifting financing costs and forcing developers to seek state-backed loans or joint ventures with anchor tenants. Rental rates in the Moscow region softened 8% through September 2025, while vacancy edged up to 3.8%, reflecting the inability of tenants to absorb full cost pass-through. Some projects require returns above 25% to remain feasible, delaying ground-breakings outside priority corridors[4]“Infrastructure Investment Program,” Ministry of Transport of Russia, mintrans.gov.ru.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Cold Storage Drives Specialized Growth

General warehousing and storage represented 91.74% of Russia warehousing and storage market share in 2024, underscoring the segment’s role as the backbone for diversified inventory requirements across manufacturing, retail, and distribution networks. Import-substitution has extended average stock coverage by 40-60 days, boosting demand for flexible racking and bulk space close to production clusters. New federal rail links reduce line-haul costs, prompting shippers to relocate overflow stock from the Greater Moscow area to emerging nodes such as Samara and Krasnoyarsk, thereby broadening the regional revenue base of the Russia warehousing and storage market.

Refrigerated warehousing, though much smaller, is forecast to post a 2.79% CAGR—the highest among all warehouse types—through 2030. Strong Asian appetite for Russian meat and fish, combined with rising domestic consumption of convenience foods, underpins sustained cold-chain expansion. Subsidized 3% financing and tax credits tilt the investment calculus in favor of temperature-controlled projects, making them more attractive than generic sheds in many regions. The Russia warehousing and storage market size attached to cold storage is further amplified by advanced terminal builds along the Northern Sea Route, where capacity utilization levels above 80% justify accelerated commissioning schedules. Developers face hurdles meeting HACCP and GDP standards but gain pricing power given the scarcity of compliant space.

By End-User Industry: E-Commerce Dominance Accelerates

E-commerce and retail secured 37.70% of the Russia warehousing and storage market size in 2024 and is forecast to expand at a 2.85% CAGR to 2030, maintaining its dual status as market leader and fastest-growing vertical. Major marketplaces pursue hub-and-spoke models, opening mid-sized fulfillment centers within 500 km of second-tier cities to guarantee two-day delivery. This decentralization catalyzes demand for modern cross-dock space and mezzanine-equipped sortation zones, lifting the Russia warehousing and storage market overall.

Food and beverage ranks second, propelled by record agricultural exports and the government’s RUB 12 billion (USD 111.04 million) cold-chain stimulus. Meat “shuttle trains” to China require multi-temperature depots adjacent to railheads, creating opportunities for specialized 3PLs. Manufacturing and automotive clients lengthened component stockpiles to 90-120 days, necessitating buffer warehouses with enhanced security and just-in-time sequencing capabilities. Healthcare and life sciences seek GDP-certified space with temperature mapping and redundant power, a niche still undersupplied outside Moscow. Chemicals and specialty materials rely on hazardous-goods compliant facilities with spill containment, while emerging sectors such as defense equipment and electronics create new revenue streams for operators offering bonded and high-security storage.

Geography Analysis

Moscow and St Petersburg together captured around 60% of Russia warehousing and storage market value in 2024 due to superior infrastructure, dense population, and legacy supply chains. Nevertheless, growth momentum is shifting. The Volga Federal District posted double-digit uptake of modern space, anchored by Kazan’s new e-commerce hubs and automotive suppliers. Developers benefit from lower land prices and municipal incentives that compress payback periods to five years.

Siberian hubs like Novosibirsk and Krasnoyarsk are experiencing surging throughput as the Eastern Polygon rail project unlocks capacity. Cold-chain and bulk grain depots blossom along the corridor, positioning the region as a consolidating point for eastbound exports. The Russia warehousing and storage market share in the Far Eastern Federal District is climbing fastest, aided by port upgrades in Vladivostok and strategic proximity to Chinese and Korean consumers. Cargo volumes there grew 25% year-on-year in 2024, spurring speculative construction of class A facilities.

Arctic territories, though small in absolute terms, enjoy outsized government funding. NSR nodes such as Murmansk and Sabetta host refrigerated transshipment centers that handle seafood and meat exports year-round. Border oblasts with Kazakhstan and Belarus gain from simplified customs and “friend-shoring” flows, prompting conversion of idle industrial plots into bonded warehouses. Yet quality gaps persist; outside the top two federal districts only 22% of inventory meets class A standards, highlighting a structural supply-demand mismatch that will continue to shape rental differentials.

Competitive Landscape

The Russia warehousing and storage market features moderate fragmentation, with local champions FM Logistic Russia, RZD Logistics, and STS Logistics leveraging established rail links and government relationships to widen capacity. International firms that remain active, chiefly GEFCO and Volga-Dnepr Group, localize procurement and switch to domestic software stacks to ensure compliance. Sanctions have tilted market power toward Russian-owned providers that can access state financing at below-market rates.

Retail chains such as PJSC Magnit and Fix Price accelerate vertical integration, building proprietary logistics complexes to lock in service quality and cut third-party costs. Technology partnerships flourish: X5 Group rolled out an in-house WMS, while NOYTECH supplies AI-driven slotting algorithms to third-party warehouses, improving pick rates by 18%. Automation specialists LemanA PRO and Locotek secure multi-site orders, signaling a shift toward home-grown solutions.

White-space opportunities cluster in pharmaceutical cold-chain logistics, hazardous-goods storage, and bonded fulfillment serving cross-border e-commerce into Central Asia. Operators that combine specialized real estate with compliance certifications enjoy pricing premiums and lower churn. Conversely, oversupply risks emerge in generic class B facilities around Moscow, where vacancy edged higher in 2025. Competitive intensity remains highest in tier-1 cities, yet provincial markets offer superior margins due to limited modern stock.

Russia Warehousing And Storage Industry Leaders

FM Logistic

RZD Logistics

PJSC Magnit

STS Logistics

Major Logistics Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: TransContainer unveiled a RUB 10.7 billion (USD 99.01 million) plan to modernize and expand terminals in Novosibirsk, Yekaterinburg, and Primorsky Krai, reinforcing East-West rail corridors.

- December 2024: RZD Logistics completed a 30% expansion of its refrigerated terminal network, adding multi-temperature facilities across key regions.

- November 2024: Yandex.Market opened a 70,000 m² fulfillment center in Kazan, creating 2,500 jobs and processing 100,000 orders daily.

- October 2024: Fix Price invested RUB 4 billion (USD 37.01 million) in a logistics complex near Kazan to serve 3,000 stores.

Russia Warehousing And Storage Market Report Scope

| General Warehousing and Storage |

| Refrigerated Warehousing and Storage |

| E-commerce and Retail |

| Food and Beverage |

| Manufacturing and Automotive |

| Healthcare, Pharmaceuticals, and Life Sciences |

| Chemicals and Specialty Materials |

| Others |

| By Warehouse Type | General Warehousing and Storage |

| Refrigerated Warehousing and Storage | |

| By End User Industry | E-commerce and Retail |

| Food and Beverage | |

| Manufacturing and Automotive | |

| Healthcare, Pharmaceuticals, and Life Sciences | |

| Chemicals and Specialty Materials | |

| Others |

Key Questions Answered in the Report

What is the 2025 value of the Russia warehousing and storage market?

The market is valued at USD 6.44 billion in 2025.

How fast is the market expected to grow through 2030?

It is forecast to register a 2.23% CAGR, reaching USD 7.19 billion by 2030.

Which segment holds the largest share of warehouse type?

General warehousing and storage led with 91.74% share in 2024.

Why is cold storage attracting investment?

Government subsidies, export demand to Asia, and domestic food safety standards are driving a 2.79% CAGR for cold storage facilities.

Which end-user industry is expanding fastest?

E-commerce and retail commands the largest share at 37.70% and is growing at a 2.85% CAGR as regional fulfillment networks scale up.

How are sanctions affecting warehouse technology?

Export controls limit access to Western automation, raising equipment costs and encouraging adoption of domestic solutions.

Page last updated on: