Russia Food Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

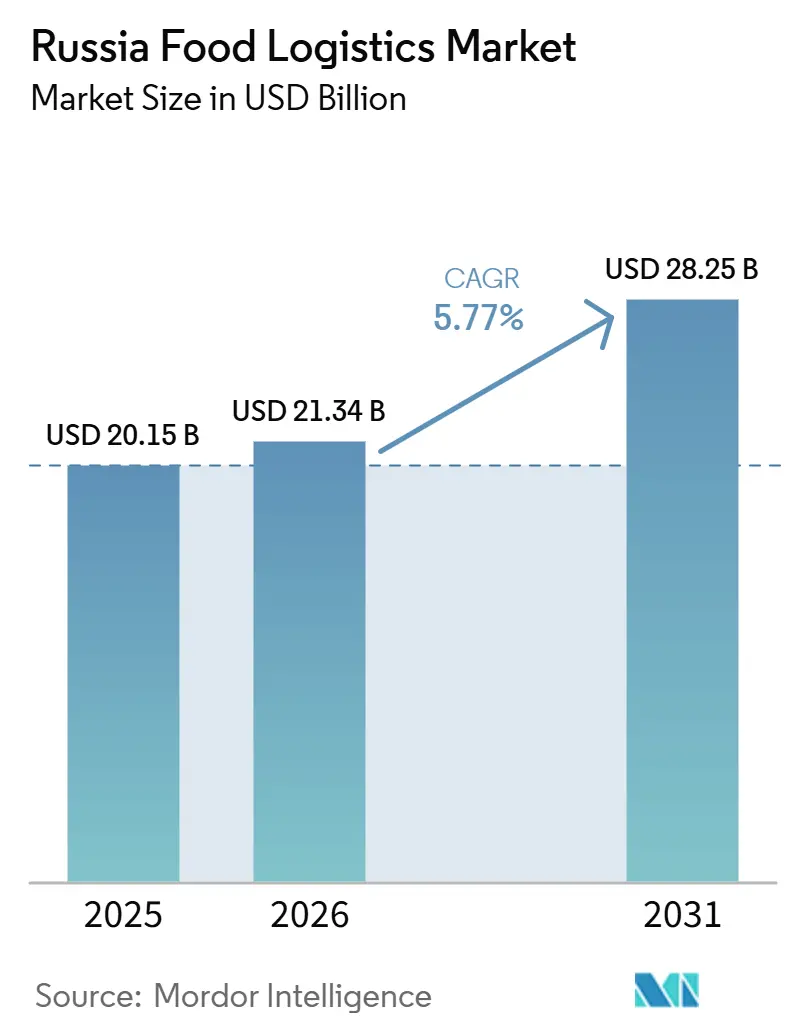

| Base Year Market Size (2025) | USD 20.15 Billion |

| Market Size (2026) | USD 21.34 Billion |

| Market Size (2031) | USD 28.25 Billion |

| Growth Rate (2026 - 2031) | 5.77% CAGR |

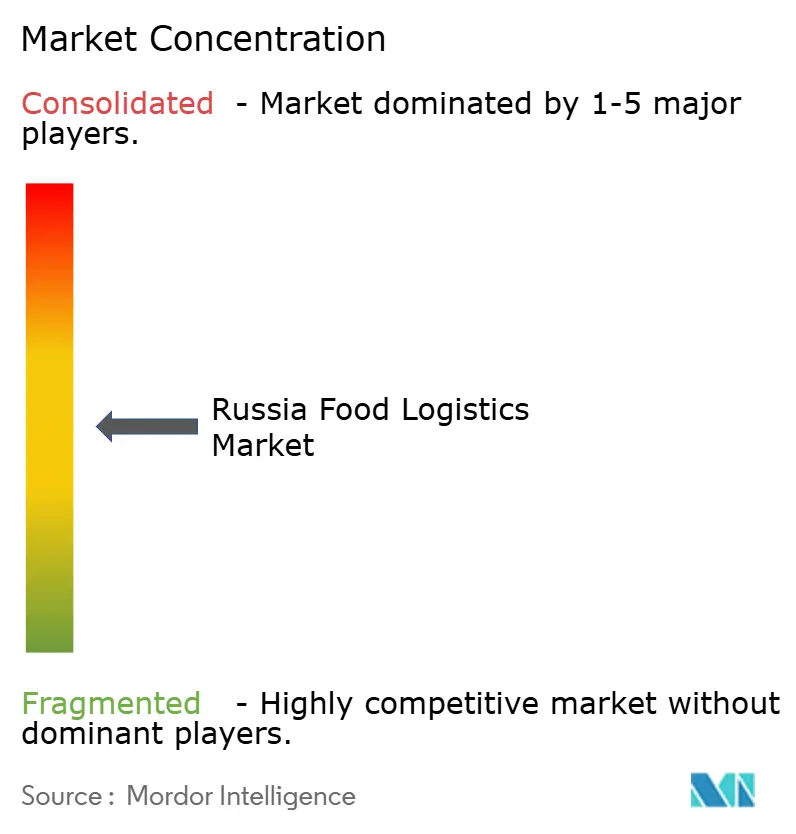

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Food Logistics Market Analysis by Mordor Intelligence

The Russia food logistics market size is projected to expand from USD 20.15 billion in 2025 and USD 21.34 billion in 2026 to USD 28.25 billion by 2031, registering a CAGR of 5.77% between 2026 to 2031.

Demand pivots toward premium cold-chain infrastructure as domestic organic and functional food consumption rises, while Far Eastern agricultural megaclusters re-route exports toward Asia, reshaping corridor economics and equipment deployment. Retailers roll out dark stores and micro-fulfillment hubs that compress delivery windows to 15-30 minutes, forcing operators to build high-frequency last-mile capacity that traditional regional warehouses cannot match. Import-substitution policies localize refrigerated-container production and accelerate blockchain-enabled trade-finance platforms that shorten payment cycles for perishable exports, offsetting friction from sanctions on cross-border settlements. Commercial fleet transition toward zero-emission assets is simultaneously supported by Minpromtorg’s preferential leasing program for domestically assembled electric commercial vehicles, running parallel to federal subsidies driving high-capacity charging infrastructure across designated pilot regions.[1]“Strategy for the Development of the Agro-Industrial Complex and Food Logistics,” Russian Ministry of Industry and Trade, minpromtorg.gov.ru

Key Report Takeaways

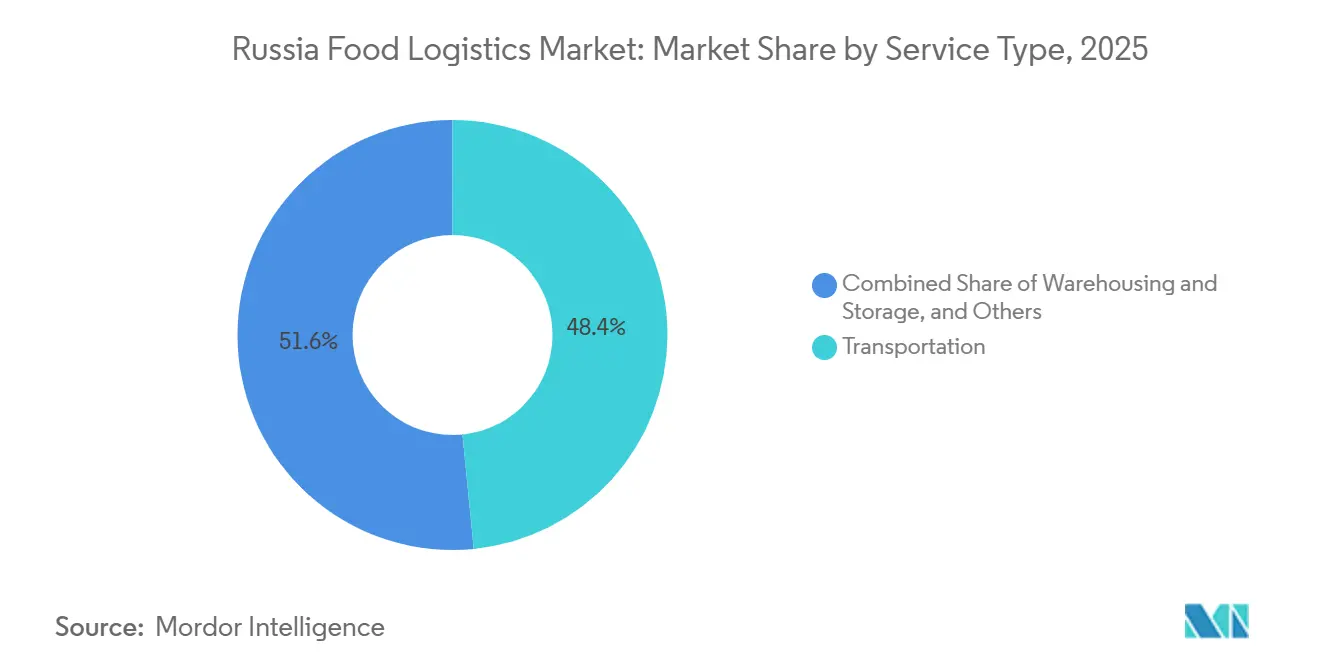

- By service type, transportation captured 48.42% of the Russia food logistics market share in 2025, while value-added services are advancing at an 8.33% CAGR through 2031.

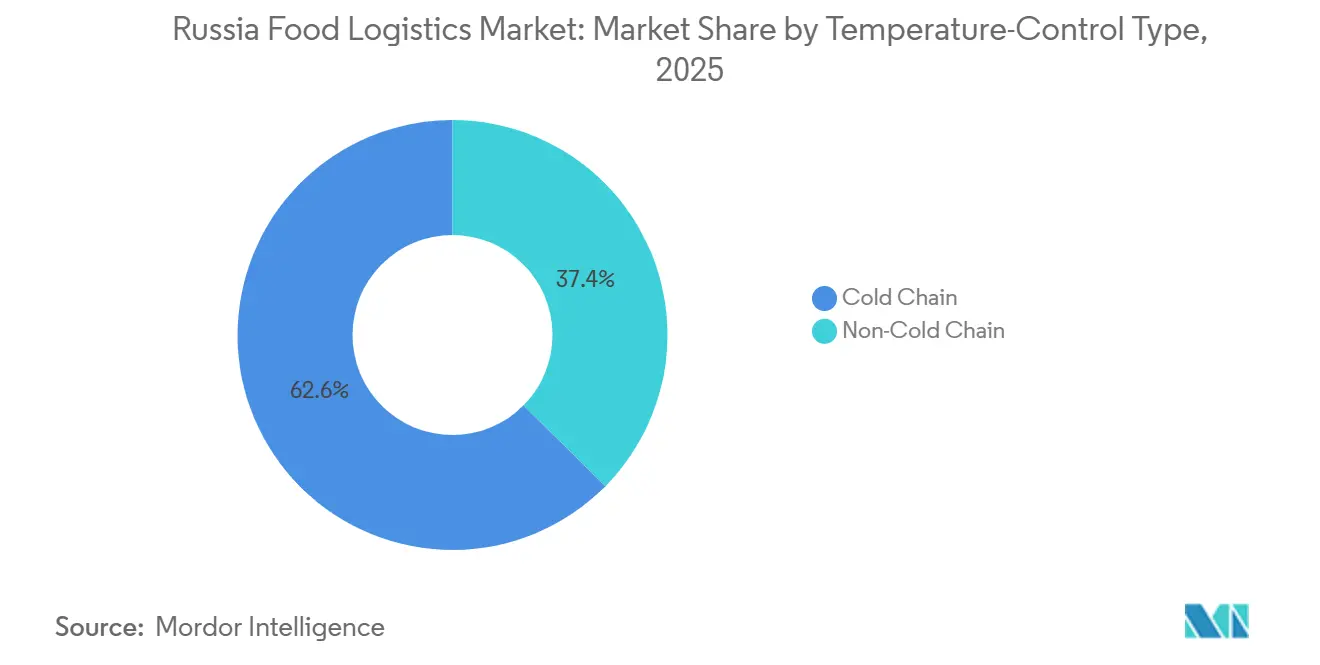

- By temperature control, cold-chain logistics commanded 62.59% of the Russia food logistics market size in 2025 and is progressing at a 7.20% CAGR between 2026 and 2031.

- By end-product, meat, seafood, and poultry held 27.23% Russia food logistics market share in 2025; pet food is forecast to expand at an 8.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Food Logistics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic Organic and Functional-Food Boom | +1.1% | Moscow, St. Petersburg, Kazan, Yekaterinburg | Short term (≤ 2 years) |

| Dark Store and Micro-Fulfillment Roll-Out | +0.9% | Major urban and tier-2 cities | Short term (≤ 2 years) |

| Far-East Agri-Mega cluster Investments | +1.0% | Primorsky Krai, Khabarovsk | Medium term (2-4 years) |

| Green-Tax Rebates for Battery-Electric Trucks | +0.7% | 12 pilot regions, including Moscow, Tatarstan | Medium term (2-4 years) |

| Localized Reefer-Container Production | +0.6% | National | Long term (≥ 4 years) |

| “Rusagrofin” Blockchain Export Finance | +0.5% | Cross-border trade corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Domestic Organic and Functional-Food Boom Needs Certified Cold-Chain

Russia’s expanding organic and functional food sector elevates certified cold-chain capacity from a compliance requirement to a strategic operational advantage. Regional agricultural subsidies and concessional financing programs actively incentivize organic production, while strict oversight by the Federal Service for Veterinary and Phytosanitary Surveillance (Rosselkhoznadzor), enforced via the FGIS Mercury electronic traceability system, mandates rigorous documentation of temperature integrity throughout transit. Furthermore, functional products such as probiotic dairy and fortified supplements are highly sensitive to nutrient degradation, compelling logistics providers to invest heavily in validation systems and specialized staff training. Operators possessing certified quality management systems successfully differentiate their service offerings, capturing higher-margin contracts over conventional carriers lacking verifiable cold-chain infrastructure.

Nation-Wide Roll-Out of Dark Stores and Regional Micro-Fulfillment Hubs

Rapid regional expansion by quick-commerce players such as Yandex Lavka and Samokat from 2024 onward is fundamentally rewriting urban food flows. Each dark store demands multiple daily replenishments, driving frequency-intensive chilled logistics flows that standard hub-and-spoke distribution models cannot efficiently absorb. While municipal zoning ordinances and strict nighttime noise regulations (SanPiN) complicate site selection, retailers continue deployment, calculating that consumer willingness to pay for sub-30-minute delivery offsets the elevated logistics costs. Operators are responding by deploying advanced route-optimization algorithms and utilizing light commercial vehicles (LCVs) tailored to navigate urban weight restrictions, while leveraging micromobility networks for the final mile. Regardless of future consolidation among individual operators, the sunk capital in this distributed infrastructure ensures the micro-fulfillment model will remain a structural fixture of the Russian food logistics market.

FDI-Backed Far-East Agri-Megaclusters Driving East-Bound Reefer Flows

Tax holidays and infrastructure co-investment under the Advanced Special Economic Zones (ASEZ) and Free Port of Vladivostok regimes have actively attracted Chinese and Korean capital into Primorsky Krai megaclusters producing soybeans, corn, and farmed seafood for Asian buyers. These reconfigured supply chains bypass traditional European distribution hubs like Saint Petersburg, elevating reefer and intermodal container demand at the primary Far Eastern ports of Vladivostok and Vostochny. Integrated processing-plus-logistics designs align capacity additions end-to-end, allowing lower per-unit transport costs than fragmented legacy networks. As Chinese import demand outstrips domestic supply, Far-East Russia offers a distinct proximity advantage over North and South American competitors. Operators capable of navigating complex cross-border customs protocols and alternative currency settlements are securing long-term contracts that anchor equipment utilization.

Green-Tax Rebates for Battery-Electric Refrigerated Trucks in 12 Pilot Regions

Commercial fleet transition toward zero-emission assets is supported by the Ministry of Industry and Trade’s (Minpromtorg) preferential leasing program, which offers upfront capital discounts for domestically assembled electric commercial vehicles. This vehicle procurement incentive operates alongside federal subsidies, driving high-capacity charging infrastructure deployment across designated pilot regions. While electric units effectively eliminate diesel excise exposure, payload sacrifices and sparse intercity charging corridors continue to hinder long-haul adoption. Domestic manufacturers, including KAMAZ and GAZ, are scaling production; however, a substantial initial capital expenditure premium over traditional diesel assets persists. Consequently, early adopters are concentrating deployment on high-frequency urban routes where regenerative braking and lower operational expenditures optimize asset productivity[2]“Report on the Execution of the Concept for the Development of Electric Motor Vehicle Production: Pilot Regions and Preferential Leasing Results,” Russian Ministry of Industry and Trade, minpromtorg.gov.ru.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing Provincial Cold-Storage Assets | -0.9% | Rural territories | Long term (≥ 4 years) |

| Escalating Insurance Premiums on Perishable Cargo | -0.7% | National | Short term (≤ 2 years) |

| Supply Crunch of Food-Grade CO₂ and Eco Refrigerants | -0.6% | National | Medium term (2-4 years) |

| Sub-Standard Rural Feeder Roads | -0.8% | Agricultural zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Provincial Cold-Storage Assets Causing 8–12% Product Loss

Soviet-era storage sites in rural Russia rely on obsolete compressors and poor insulation, causing temperature swings that ruin delicate produce and trim producer margins. Upgrade subsidies exist, yet complex paperwork and local corruption impede disbursement. High loss rates deter private capital, funneling investment toward metropolitan areas and widening the urban-rural infrastructure gap. Vertically integrated conglomerates with healthier balance sheets therefore gain share over fragmented farmer groups.

Escalating Insurance Premiums on Perishable Cargo Post-2024 Risk Recalibration

Insurance market recalibrations following elevated cold-chain loss events have compelled underwriters to tighten coverage terms for high-value perishables, such as seafood and premium horticulture. Contemporary cargo policies increasingly mandate the integration of continuous telematics, including GLONASS tracking and Internet of Things (IoT) thermal sensors, effectively transferring risk mitigation capital expenditures onto logistics operators. Consequently, undercapitalized regional carriers are frequently forced into self-insurance, exposing them to catastrophic loss scenarios that accelerate market exits. Conversely, Tier-1 fleets are able to amortize these technology investments across larger cargo volumes, enabling them to negotiate favorable underwriting terms and multi-year policy discounts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Capture Premium Positioning

Transportation held 48.42% of the Russia food logistics market share in 2025, reflecting the country’s vast geography and road-centric distribution network. However, value-added services such as blast freezing, labeling, and inventory management are growing at an 8.33% CAGR through 2031, as retailers and exporters demand integrated fulfillment packages that reduce hand-offs and ensure traceability. Large processors in Vladivostok rely heavily on blast-freezing to stabilize seafood quality before rail shipment to Moscow supermarkets, illustrating how specialized capabilities re-route volume to premium providers. Concurrently, inventory-management platforms built on predictive AI anticipate dark-store replenishment needs, minimizing out-of-stock events and shrinking working capital for grocers. Compliance-driven labeling is also expanding as Rosselkhoznadzor mandates traceability through its FGIS Mercury electronic veterinary certification system across all meat and seafood categories.

Despite slower growth, foundational transport services remain indispensable. Long-haul trucking dominates because rail lacks last-mile flexibility, and cabotage restrictions limit coastal maritime feeder options. Yet, margin pressure is intensifying as diesel excise taxes rise and an acute, nationwide driver shortage pushes wages higher. Carriers are therefore bundling temperature monitoring and prepaid insurance to defend yields, effectively transitioning clients toward quasi-value-added contracts. Hybrid models that integrate full-truckload (FTL) lanes with regional consolidation hubs near micro-fulfillment centers are emerging, strategically keeping fleets near urban consumption zones and minimizing empty repositioning hauls.

By Temperature-Control Type: Cold-Chain Dominance

Cold-chain logistics commanded 62.59% of the Russia food logistics market size in 2025, rising at a 7.20% CAGR, underscoring consumer migration toward fresh and frozen offerings. Frozen handling is witnessing growth on the back of pet-food exports, ready-meal demand, and ice-cream category expansion. To optimize operations, providers are heavily investing in multi-temperature cross-docks that toggle between chilled (2-8 °C) and frozen zones, lifting asset utilization across seasons. Concurrently, operators are piloting localized electric light commercial vehicles (LCVs) for high-frequency urban chilled runs to navigate municipal restrictions, though traditional assets remain the baseline for regional transport.

Ambient logistics (15-25 °C) still shifts significant tonnage of canned goods and grain-based staples, but pricing power firmly resides in temperature-controlled tiers where strict certification barriers discourage new entrants. Regulatory scrutiny continues to tighten around dairy and meat exports, adding compliance burdens such as mandatory FGIS Mercury integration that only technologically sophisticated operators can effectively navigate. As a result, integrated cold-chain fleets are securing multi-year volume contracts with major supermarket groups, while undercapitalized ambient carriers are increasingly relegated to the spot market. This widening capability gap directly reinforces the premium valuation of cold-chain assets in contemporary mergers and acquisitions.

By End-Product Category: Pet Food Surge Reshapes Capacity Allocation

Meat, seafood, and poultry led with a 27.23% share of the Russia food logistics market size in 2025, capitalizing on domestic protein abundance and expanding aquaculture operations in the Far East. Concurrently, the pet food segment is accelerating rapidly at an 8.62% CAGR through 2031, as Russia strategically repositions as a supplier of premium formulations to Middle Eastern and Asian markets. Dedicated freezer capacity for grain-free and fresh-frozen recipes forms a highly profitable new niche within multipurpose warehouses, enabling logistics operators to optimize infrastructure utilization during seasonal downtimes in human-nutrition traffic.[3]“Agro-Industrial Complex Development and Export Strategy: 2026 Annual Progress Report,” Ministry of Agriculture of the Russian Federation, mcx.gov.ru

Pet-food exporters are increasingly leveraging the same blockchain-enabled trade finance rails utilized by seafood shippers, accelerating receivables and freeing working capital for brand expansion. Domestically, consumption continues to rise as urban households embrace pet humanization, trading up to functional treats rich in specialized nutrients. This cross-category synergy improves overall warehouse utilization and disperses risk, further incentivizing operators to allocate incremental cold-chain capacity to premium pet food over lower-margin processed goods. Consequently, competitive intensity is actively migrating from traditional commodity protein lanes toward these high-value specialty clusters.

Geography Analysis

Moscow and Saint Petersburg dominate the national cold-chain warehouse footprint in 2025, benefiting from established network effects in labor, supplier clusters, and intermodal transport. However, challenges such as land scarcity, wage inflation, and urban congestion are squeezing margins. To mitigate these single-node risks, distributors are establishing satellite hubs in neighboring regions like Tver and Tula. Within metropolitan areas, retailers are investing in automated shuttle systems to boost throughput without expanding their footprint, while developers are pivoting toward multistory cold-storage projects to maximize vertical cubic utilization.

In the Far Eastern Federal District, the fastest-growing regional market megaclusters in Primorsky Krai are driving significant volume growth by funneling soy, corn, and frozen seafood to Asian markets via modernized rail lines and sea ports like Zarubino. Government initiatives, including port dredging and free-port customs zones, reduce transit times and allow Russian exporters to undercut South American competitors on freight costs. To balance round-trip economics, cold-chain operators routinely reposition empty refrigerated containers eastward to secure valuable seafood backhaul loads.

Meanwhile, the southern agricultural powerhouses of Krasnodar, Rostov-on-Don, and Stavropol maintain strong grain and horticulture volumes. However, these regions struggle with deteriorating feeder roads that significantly inflate first-mile transportation costs. While public-private partnerships have earmarked funds for necessary road infrastructure upgrades, project execution frequently lags behind the release of budgets.[4]“Regional Infrastructure & Cold-Chain Capacity Analysis: 2026 Progress Report on the West-East and North-South Corridors,” Federal Office for Logistics and Mobility, mintrans.gov.ru

Competitive Landscape

Russia food logistics market competition tilts toward mid-level concentration. Smaller carriers exited under pressure from higher fuel taxes and insurance deductibles, while scale players expanded fleets via distressed-asset purchases. X5 Group, operating more than 4,500 temperature-controlled trucks, is vertically integrating dark-store replenishment to lock out third-party carriers in strategic corridors. PEK Group rolled out an automated transport control center that slices empty mileage by double digits, freeing capacity for cross-border lanes into Kazakhstan and China.

Technology is now the chief differentiator. Operators deploy IoT sensor suites to broadcast real-time temperature to shippers, winning cargo-damage insurance discounts and premium contracts. Blockchain platforms like Rusagrofin cut receivable cycles, letting logistics firms extend favorable credit to exporters and lock in a share. Investment races center on battery-electric reefer fleets in pilot regions where green-tax rebates offset steep sticker prices; early adopters gain carbon-label advantages with grocery chains that publicize sustainability metrics.

Consolidation is expected to intensify as domestic banks channel subsidized credit toward operators with documented ESG roadmaps. Pure forwarders without own assets pivot into specialized customs and veterinary clearance niches, while asset-heavy carriers court joint-ventures with Asian partners seeking guaranteed Russia-Asia reefer slots. Private-equity funds eye multi-temperature cross-dock investments as an exit to larger strategic buyers within five years.

Russia Food Logistics Industry Leaders

Alfert

LIGNA Transport Company

GFC Logistics

Transgroup LLC

Bystraya Logistika

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: CEVA officially completed the 100% acquisition of the Fagioli Group. This massive acquisition integrates over 450 engineering employees and specialized heavy-lift assets, positioning CEVA as an end-to-end leader in global project logistics for industrial and EPC (engineering, procurement, and construction) customers.

- March 2026: KWE's subsidiary, Shanghai Kintetsu Logistics (SKL), opened a newly relocated, highly automated 34,242 sq. meter warehouse in the Shanghai Waigaoqiao Free Trade Zone. The facility focuses on advanced robotics, deploying automated guided forklifts and shuttle-based ASRS (Automated Storage and Retrieval Systems) to manage vendor-managed inventory (VMI) and buyer consolidation for multinational clients.

- December 2025: Jungheinrich officially completed the sale of its Russian subsidiary (Jungheinrich Lift Truck OOO) to a local financial investor. This move transferred its local rental fleet and roughly 600 staff, formally concluding the company's operations in the Russian market.

- December 2025: CEVA alongside KIKO Milano won the Logistics Operator of the Year award specifically in the "Technological Innovation" category.

Russia Food Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea and Inland Water | |

| Air | |

| Warehousing and Storage | |

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) |

| Cold Chain | Ambient (15-25 °C) |

| Chilled (2-8 °C) | |

| Frozen (Less than 0 °C) | |

| Non Cold Chain |

| Meat, Seafood, and Poultry |

| Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.) |

| Horticulture (Fresh Fruits and Vegetables) |

| Processed Food Products |

| Pet Food |

| Others (Spreads, Seasoning, dressing, Specialty and Functional Foods, etc.) |

| By Services | Transportation | Road |

| Rail | ||

| Sea and Inland Water | ||

| Air | ||

| Warehousing and Storage | ||

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) | ||

| By Temperature-Control Type | Cold Chain | Ambient (15-25 °C) |

| Chilled (2-8 °C) | ||

| Frozen (Less than 0 °C) | ||

| Non Cold Chain | ||

| By End-Product Category | Meat, Seafood, and Poultry | |

| Dairy Products and Frozen Deserts (Milk, Ice-cream, Butter, etc.) | ||

| Horticulture (Fresh Fruits and Vegetables) | ||

| Processed Food Products | ||

| Pet Food | ||

| Others (Spreads, Seasoning, dressing, Specialty and Functional Foods, etc.) | ||

Key Questions Answered in the Report

What is the current Russia food logistics market size?

The Russia food logistics market size stands at USD 21.34 billion in 2026 and is projected to reach USD 28.25 billion by 2031.

How fast will Russia’s food logistics sector grow?

The market is expected to expand at a 5.77% CAGR between 2026 and 2031.

Which service type leads in Russia’s food logistics?

Transportation services held 48.42% of market share in 2025, though value-added services are the fastest-growing segment.

Why is pet food important for Russian logistics providers?

Pet food volumes are advancing at an 8.62% CAGR through 2031, leveraging existing cold-chain assets and offering higher margins than commodity staples.

Which region shows the fastest food logistics growth?

The Far Eastern Federal District records the highest growth, fueled by export-oriented agri-megaclusters and upgraded port-rail links.

How are green-tax rebates influencing fleet decisions?

Rebates and lease discounts on battery-electric refrigerated trucks in 12 pilot regions are nudging carriers toward zero-emission assets and lowering urban delivery costs.

Page last updated on: