United States Mining Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

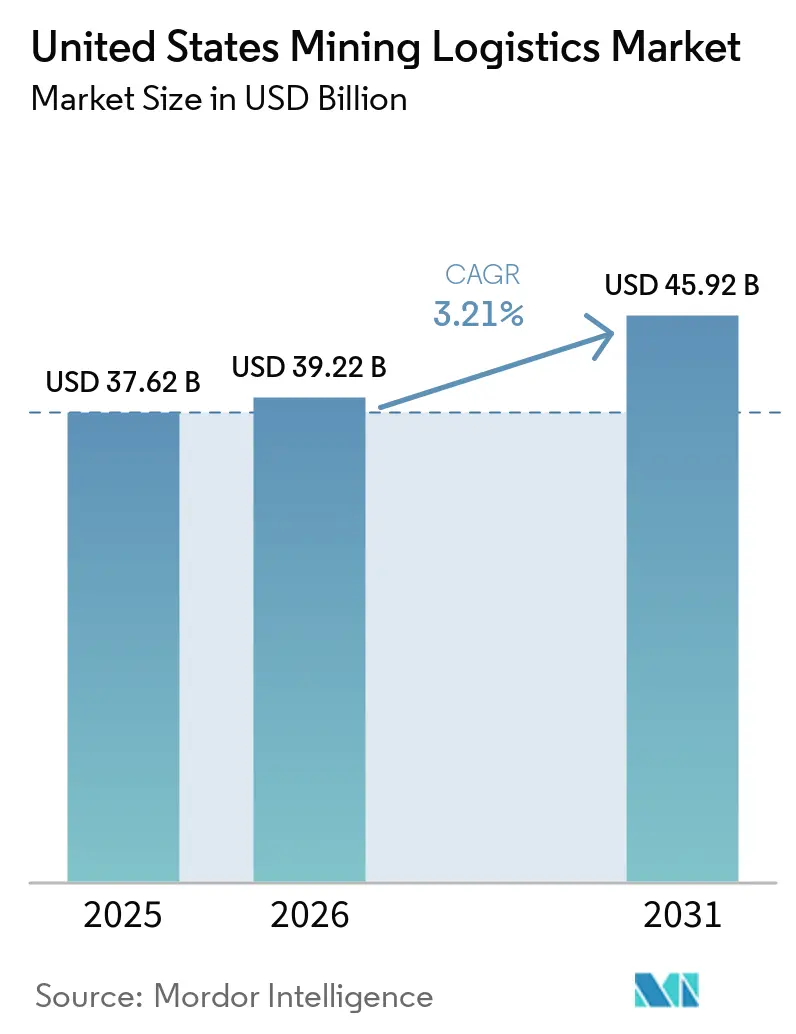

| Base Year Market Size (2025) | USD 37.62 Billion |

| Market Size (2026) | USD 39.22 Billion |

| Market Size (2031) | USD 45.92 Billion |

| Growth Rate (2026 - 2031) | 3.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Mining Logistics Market Analysis by Mordor Intelligence

The United States mining logistics market size was valued at USD 37.62 billion in 2025 and estimated to grow from USD 39.22 billion in 2026 to reach USD 45.92 billion by 2031, at a CAGR of 3.21% during the forecast period 2026-2031.

Federal action is pushing up logistics demand because Project Vault has introduced a USD 12 billion critical minerals reserve that requires corridor planning, storage capacity, and secure handling before full commercial output comes online. Domestic offtake requirements are also moving logistics providers closer to financing and procurement decisions, which favors operators that can provide traceability, secure storage, and a documented chain of custody across multiple handoff points. At the same time, long mine development and permitting cycles continue to keep project timing uncertain, so network expansion in the United States mining logistics market still depends on careful capital allocation rather than asset growth alone. Competitive pressure is also rising as merger activity among major railroads could reshape corridor control and pricing leverage across the national freight base. The United States mining logistics market, therefore, entered 2026 with a firmer demand floor than freight-cycle data alone would imply, while the clearest opportunities remain in corridor readiness, secure storage, and higher-value execution services.

Key Report Takeaways

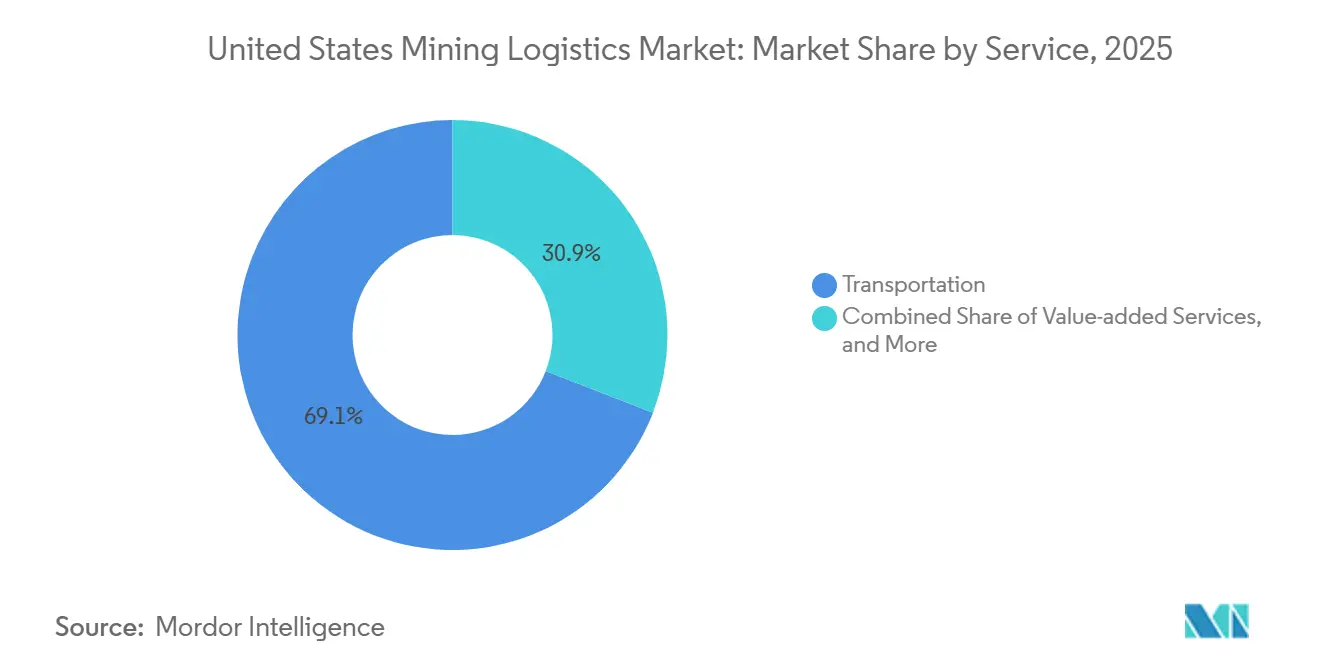

- By service, transportation held 69.12% of the United States mining logistics market share in 2025, while value-added services are forecast to expand at a 3.86% CAGR through 2031.

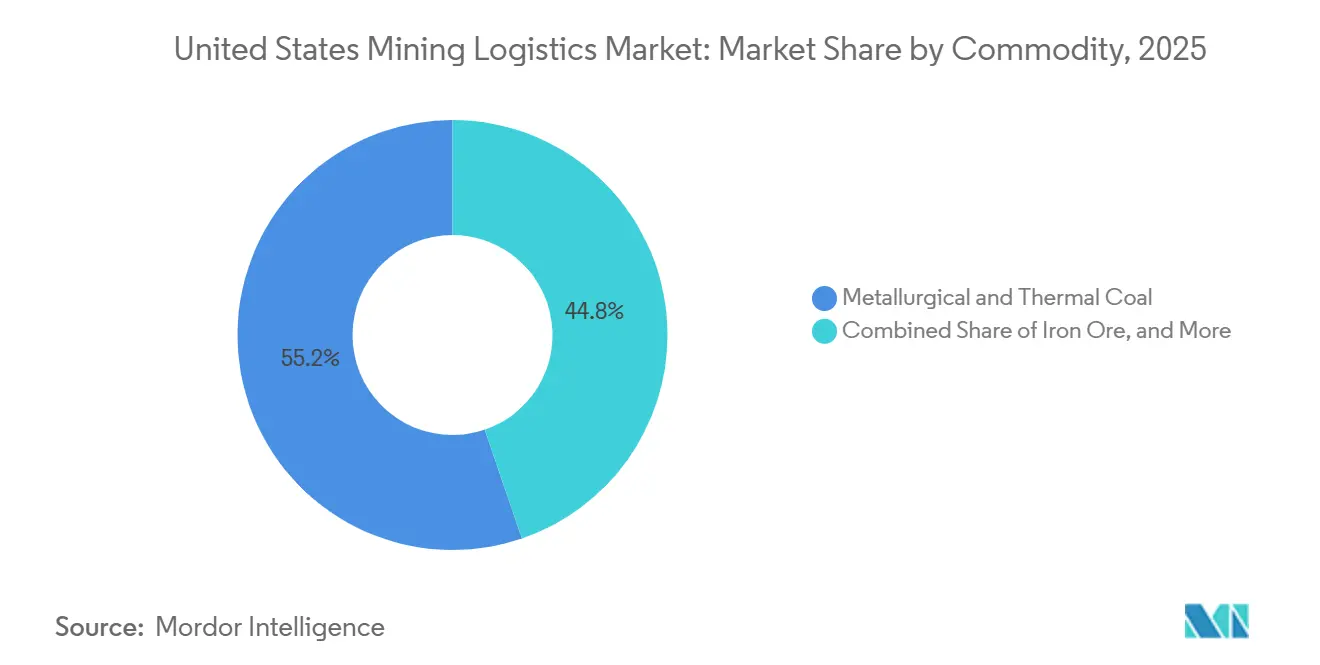

- By commodity, metallurgical and thermal coal accounted for 55.24% of the United States mining logistics market size in 2025, while base metals are projected to record the highest CAGR at 3.92% through 2031.

- By geography, the West held 40.08% of the United States mining logistics market share in 2025, while the Midwest is projected to grow at the fastest CAGR of 4.01% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Mining Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-mineral reshoring and domestic offtake | +0.8% | National, with early gains in West and Southeast | Medium term (2-4 years) |

| Rail and port corridor modernization | +0.6% | National, concentrated in West, Southeast, and Gulf Coast | Short term (≤ 2 years) |

| Domestic processing localization for battery materials | +0.5% | West, Southeast, and Midwest | Medium term (2-4 years) |

| Export resilience in coal and industrial minerals | +0.4% | East Coast and Gulf Coast | Short term (≤ 2 years) |

| Rail-interchange visibility and control-tower digitization | +0.3% | National, with early gains in Midwest and Southwest | Short term (≤ 2 years) |

| Strategic mineral stockpiling and secure storage nodes | +0.4% | National, anchored in West and Gulf Coast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Critical-Mineral Reshoring and Domestic Offtake

The federal shift from advisory support to direct procurement is giving the United States mining logistics market more durable project-linked demand. Project Vault's USD 12 billion reserve converts policy intent into a logistics requirement for secure movement, storage, and controlled inventory management at a national scale[1]“The Department of Commerce's CHIPS Program Announces a Letter of Intent with USA Rare Earth,” NIST News, nist.gov. In January 2026, the Department of Commerce issued a letter of intent with USA Rare Earth for a mine-to-magnet supply chain tied to the Round Top project in Texas, where the site is planned to extract 40,000 metric tons per day of rare earth and critical mineral feedstock. That changes the operating sequence because logistics providers are now being drawn into project design before normal freight volumes appear in shipment data. Operators that can combine switching, transloading, secure storage, and long-term corridor support are better positioned to win multi-year contracts rather than chasing spot moves after production ramps. Watco's June 2025 USD 600 million investment from Duration Capital Partners shows how private capital is already backing that approach in fragmented corridors.

Rail and Port Corridor Modernization

Corridor upgrades are improving the physical backbone that supports the United States mining logistics market across mine, rail, and export links. BNSF announced a USD 3.6 billion capital investment plan for 2026 that targets track renewal, terminal expansion, and network reliability improvements relevant to bulk mineral shippers. The Federal Railroad Administration's 2025-2026 CRISI cycle disbursed more than USD 2 billion across 122 rail improvement projects in 41 states, which materially supports freight congestion relief, bridge rehabilitation, and port rail access[2]“Infrastructure Investment and Jobs Act Information from FRA, CRISI Grant Program,” FRA, railroads.dot.gov. CSX completed the Howard Street Tunnel double-stack clearance expansion in 2025, which opened more flexible routing on the Baltimore corridor and reduced one long-standing network constraint. The Gainesville Inland Port in Georgia also began its soft opening in May 2026 with daily rail service to Savannah, showing how inland rail-port links are being built to redistribute traffic away from congested coastal nodes. As more public funding is tied to compliance and intermodal readiness, corridor modernization is increasingly shaping where the United States mining logistics market can add capacity fastest.

Domestic Processing Localization For Battery Materials

The United States mining logistics market is seeing new demand because mine growth now has to connect with a still-thin domestic battery materials midstream. Resources for the Future reported that the country accounts for 10% of global anode capacity, 6% of separator capacity, and 0% of cathode manufacturing capacity, which leaves a structural gap between extraction and downstream use. That means logistics providers often need to serve a two-leg chain that runs from mine to processor and then from processor to battery or industrial customer. Those flows need cleaner handling standards, tighter inventory control, and better contamination management than general bulk freight. In February 2025, the Center for Climate and Energy Solutions identified the Southeast as a strategic region for battery-material processing because of its rail connectivity, grid access, and labor base. Logistics companies that place specialized transloading and staging capacity near new processing nodes should be better positioned than operators that try to adapt general yards after projects are already committed.

Export Resilience In Coal And Industrial Minerals

Coal and industrial minerals continue to give the United States mining logistics market an export-oriented freight base even after a softer year for overall coal shipments. United States coal exports fell to 83 million short tons in 2025 from 108 million short tons in 2024, which reflected a 23% decline tied to lower benchmark prices and weather disruptions at East Coast terminals Even with that drop, export infrastructure stayed concentrated because East Coast corridors through Norfolk and Baltimore handled 62% of total United States coal exports over the five years through 2025, and Lambert Point Coal Terminal accounted for 58% of metallurgical coal export volumes. That concentration helps preserve corridor value because the operators serving those routes still control scarce heavy-haul rail and terminal assets. Canadian National also stated in its first-quarter 2026 results that rising thermal coal prices linked to Middle East supply disruption could improve export demand going forward. As a result, export resilience continues to support the United States mining logistics market, even as domestic utility coal demand remains under pressure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mine permitting delays and project slippage | -0.4% | National, most acute in West and Southwest | Long term (≥ 4 years) |

| Remote-haul driver scarcity and wage inflation | -0.3% | National, most severe in Mountain West and remote Southwest | Short term (≤ 2 years) to Medium term (2-4 years) |

| Processing bottlenecks after mine output growth | -0.2% | National midstream, concentrated in Southeast and Midwest | Medium term (2-4 years) |

| Short-line interchange friction at bulk handoff nodes | -0.2% | Midwest, Appalachia, and Mountain West short-line junctions | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mine Permitting Delays and Project Slippage

Permitting delays continue to slow the United States mining logistics market because new mine supply cannot move until project approvals are fully in place. The Department of the Interior noted that the permitting phase for new United States hard-rock mines has historically taken 7 to 10 years, and the full path from exploration to first production has historically been far longer[3]“Trump Administration Adds Key Mining Projects to FAST-41,” DOI Press Releases, doi.gov. That creates a mismatch between policy ambition and logistics planning, because corridor investment often needs to occur before a mine reaches commercial production. When approval schedules slip, early investments in branch lines, terminals, or mine-linked handling sites can sit underused for extended periods. The same uncertainty also makes private capital more selective when funding early-stage logistics assets tied to future mines. This timing risk keeps the United States mining logistics market from converting policy support into freight growth as quickly as headline demand signals might suggest.

Remote-Haul Driver Scarcity and Wage Inflation

Remote trucking remains one of the most exposed operating constraints in the United States mining logistics market. Mine-site pickup routes often run through isolated terrain and irregular schedules, which narrows the available labor pool beyond what is seen in standard over-the-road freight. That makes recruiting more difficult in the Mountain West and remote Southwest, where first-mile and last-mile service is essential even on rail-led corridors. Wage pressure also stays elevated because these routes are harder to staff and often require more specialized operating conditions. Larger mines are already testing automation responses, as Freeport-McMoRan's Bagdad operation runs 33 autonomous 235-metric-ton haul trucks and reports lower in-cab labor exposure in its mining system. Even so, the transition will take time because connectivity, equipment redesign, and workforce retraining still limit rapid adoption across the United States mining logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Rail Dominates Revenue, But Digital Services Reshape Margin Structure

Transportation held 69.12% of the United States mining logistics market share in 2025, making it the largest service category by a wide margin. Rail remains the structural backbone for long-haul bulk movements, especially on coal, copper, and iron ore corridors that favor high tonnage and lower unit costs. Trucking still handles first-mile and last-mile moves from remote mines to rail interchange points and serves operations outside rail-connected networks. Sea and inland waterways stay relevant for coal exports, Great Lakes iron ore flows, and Mississippi-linked industrial mineral traffic. LOGISTEC's March 2026 acquisition of Logistics Park Dubuque strengthened inland routing options between Midwest bulk producers and Gulf Coast export gateways.

Value-added services are projected to grow at a 3.86% CAGR, making it the fastest-expanding part of the United States mining logistics market size through 2031. The United States mining logistics industry is adding more demand for grade verification, inventory visibility, and digital chain-of-custody records as domestic offtake agreements become more formal. These services are no longer treated as optional extras in specialty mineral contracts because buyers increasingly want proof of origin and controlled handling across each transfer point. Warehousing and inventory management also gains relevance because strategic reserve programs and secure mineral storage need bonded, audit-ready sites instead of standard public warehouses. The margin structure of the United States mining logistics market is therefore shifting toward operators that can layer compliance and data services on top of physical transport.

By Commodity: Coal Anchors Revenue While Base-Metals Demand Sets the Growth Agenda

Metallurgical and thermal coal accounted for 55.24% share of the United States mining logistics market size in 2025, keeping coal as the largest commodity base. That position reflects the tonnage density of coal traffic on Class I networks and the concentration of export infrastructure on the East Coast and Gulf Coast. Norfolk and Baltimore handled 62% of total United States coal exports over the five years through 2025, and Lambert Point Coal Terminal in Norfolk accounted for 58% of metallurgical coal export volumes[4]“U.S. Coal Exports Decreased in 2025 After Four Years of Growth,” Today in Energy, eia.gov. Iron ore remains another large-volume category, supported by Midwestern steel-linked flows and Mesabi Metallics' planned DR-grade pellet facility, which secured USD 520 million in financing in April 2026 and is targeting a Q3 2026 production start. Gold has a smaller logistics footprint per ton, but large-scale, low-grade operations can still create corridor-specific transport demand when output is centralized for processing.

Base metals are forecast to expand at a 3.92% CAGR, and the United States mining logistics market size for this segment is set to outpace all other commodity categories through 2031. The United States mining logistics industry benefits from copper demand tied to grid reinforcement, renewable interconnection, and data-center buildouts, which gives this freight stream support beyond the EV cycle alone. These flows also tend to require more integrated links between mines, processors, and industrial users than legacy bulk coal corridors. Other minerals and metals such as aggregates, soda ash, potash, and specialty industrial minerals still provide the broadest geographic spread of loads and help stabilize demand across multiple end markets. Commodity growth in the United States mining logistics market therefore depends not only on mine output, but also on where processing, rail access, and compliant handling infrastructure are already in place.

Geography Analysis

The West held 40.08% of total revenue in 2025, giving it the largest footprint in the United States mining logistics market. The region combines Powder River Basin coal movements, Nevada and Utah mineral corridors, and expanding copper and lithium activity across Arizona, Nevada, and Utah. Its advantage comes from the density of active mines and from the long-haul economics that support bulk rail movement over wide distances. Western corridors also contain installed capacity that is now being evaluated for a broader mix of industrial minerals as older coal volumes remain below earlier peaks. That combination keeps the West central to the United States mining logistics market even as commodity demand shifts toward more diverse mineral flows.

The Midwest is projected to grow at a 4.01% CAGR, and this part of the United States mining logistics market size is expanding faster than any other region through 2031. Mesabi Range iron ore logistics are strengthening as Mesabi Metallics secured USD 520 million in financing in April 2026 and targeted a Q3 2026 production start for its new DR-grade pellet facility. Great Lakes shipping, inland terminals, and rail-served industrial sites deepen the region's network density, while LOGISTEC and Watco have both expanded their positions in Midwestern bulk corridors. The region is therefore moving from a legacy iron ore base toward a denser mix of ore, aggregates, industrial minerals, and connected processing demand.

The Southeast is building from coal export corridors through Mobile and New Orleans and from growing battery-material and lithium activity across the Carolinas and Gulf Coast. The Northeast still matters through terminal operations in Baltimore and Albany, while CSX's Howard Street Tunnel work adds more routing flexibility on the I-95 corridor. The Southwest remains tied to Arizona copper and New Mexico mining districts that depend heavily on Union Pacific and BNSF for long-haul moves. Together, these regions broaden the United States mining logistics market by adding export resilience, processing links, and more regionally balanced mineral demand.

Competitive Landscape

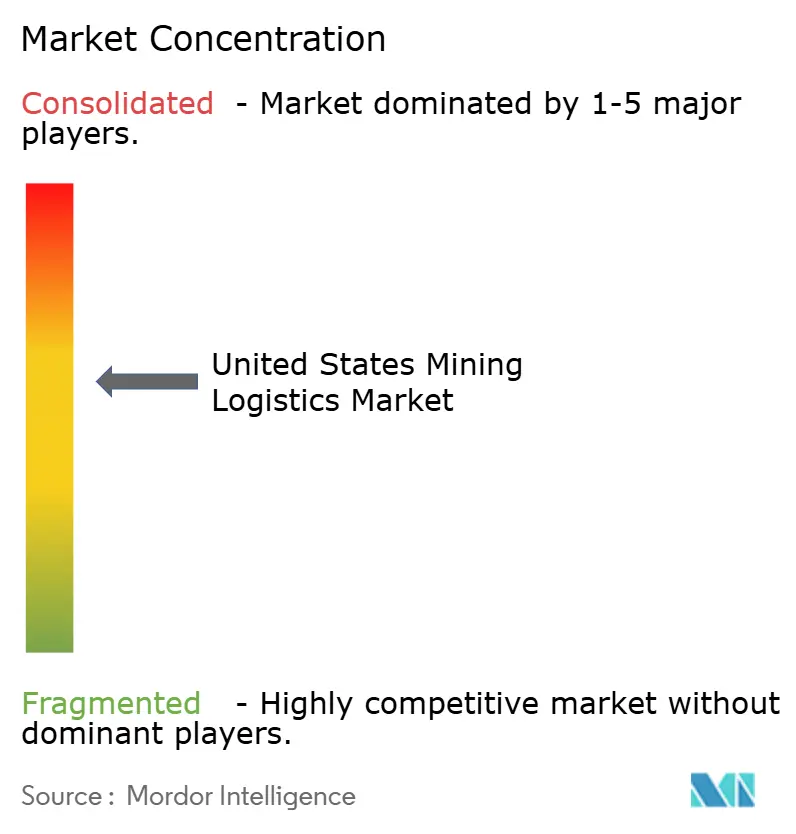

The United States mining logistics market is moderately concentrated at the Class I railroad level, where BNSF, Union Pacific, CSX, Norfolk Southern, and Canadian National control the main bulk-haul corridors. Overall concentration is a little lower across the full service chain because short lines, terminals, and third-party logistics providers remain fragmented and highly corridor-specific. The Surface Transportation Board accepted a revised application for the proposed Union Pacific and Norfolk Southern merger in May 2026, which keeps open the possibility of a single transcontinental network with much broader route control. If approved, that transaction would increase consolidation pressure and could shift bargaining power on long-haul mineral lanes across the United States mining logistics market. Competitive advantage is therefore being defined not only by track ownership, but also by who controls the most useful terminals, interchange points, and secure storage nodes.

Watco has been expanding in fragmented corridors through acquisition and capital backing, including Great Lakes Central Railroad, Colossal Transport Solutions, and a USD 600 million investment from Duration Capital Partners in 2025. Genesee & Wyoming outlined a USD 568 million 2026 capital investment program to support continued upgrades across its short-line network and reinforce its position in industrial corridors. OmniTRAX has pursued targeted corridor control rather than scale alone, extending its rail footprint through three Arkansas railroad acquisitions in April 2026. Cando Rail & Terminals also strengthened its first-mile and last-mile position by completing the acquisition of Savage Rail in May 2026.

Technology is becoming a clearer separator in the United States mining logistics market because traceability and cycle control are now closer to core service requirements. Norfolk Southern's digital twin program and Wabtec's remote train control tools show how larger operators are reducing bottlenecks, improving train handling, and raising service expectations on mineral corridors. White-space opportunities remain in bonded critical-mineral warehousing, secure storage nodes, and digital chain-of-custody services for battery-grade materials where physical infrastructure is still catching up with policy support. Regulatory oversight from the Surface Transportation Board and federal rail programs will continue to shape merger review, safety compliance, and capital deployment across the United States mining logistics market.

United States Mining Logistics Industry Leaders

BNSF Railway

CSX Transportation

Union Pacific Railroad

Canadian National Railway

Norfolk Southern Railway

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Cando Rail & Terminals completed its acquisition of Savage Rail from Savage Enterprises on May 1, 2026, establishing the combined entity as North America's market leader in first- and last-mile rail operating services and terminal infrastructure. Savage Enterprises will deploy proceeds to expand its energy and mineral services operations.

- April 2026: OmniTRAX acquired three Arkansas short-line railroads, Dardanelle and Russellville Railroad, Ouachita Railroad, and Camden & Southern Railroad extending its national rail network into a market whose cumulative economic growth over the past five years ran 40% above the national average, with operations beginning June 1, 2026.

- March 2026: LOGISTEC acquired Logistics Park Dubuque (LPD), a multi-purpose marine terminal on the Upper Mississippi River in East Dubuque, Illinois, expanding its US inland waterways network with strategic routing options connecting the Midwest and Gulf Coast for bulk mineral and industrial supply chains.

- January 2026: BNSF announced its USD 3.6 billion 2026 capital investment plan, the largest annual freight-railroad capex program in North America, with emphasis on Powder River Basin network reliability, Northern Transcon track renewal, and terminal expansion.

United States Mining Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea and Inland Waterways | |

| Air | |

| Warehousing and Inventory Management | |

| Value-Added Services |

| Iron Ore |

| Metallurgical and Thermal Coal |

| Base Metals (Cu, Zn, Ni) |

| Gold |

| Other Minerals/Metals |

| Northeast |

| Southwest |

| West |

| Southeast |

| Midwest |

| By Service | Transportation | Road |

| Rail | ||

| Sea and Inland Waterways | ||

| Air | ||

| Warehousing and Inventory Management | ||

| Value-Added Services | ||

| By Commodity | Iron Ore | |

| Metallurgical and Thermal Coal | ||

| Base Metals (Cu, Zn, Ni) | ||

| Gold | ||

| Other Minerals/Metals | ||

| By Geography | Northeast | |

| Southwest | ||

| West | ||

| Southeast | ||

| Midwest |

Key Questions Answered in the Report

What is the 2031 outlook for United States mining logistics?

The United States mining logistics market is forecast to reach USD 45.92 billion by 2031 from USD 39.22 billion in 2026, growing at a 3.21% CAGR over 2026-2031.

Which service category leads revenue in U.S. mining logistics?

Transportation led with 69.12% of revenue in 2025, supported by rail-heavy bulk movements and truck links from remote mine sites.

Which service area is growing fastest through 2031?

Value-Added Services is the fastest-growing service segment with a 3.86% CAGR, driven by traceability, inventory control, and certification needs.

Which commodity generates the largest freight base?

Metallurgical and thermal coal remained the largest commodity segment with 55.24% of market revenue in 2025 because of dense rail volumes and concentrated export infrastructure.

Which region is expanding fastest in the forecast period?

The Midwest is projected to grow at a 4.01% CAGR through 2031 as iron ore logistics, Great Lakes links, and short-line expansion deepen the regional network.

What is the biggest strategic risk for operators in this space?

Long mine permitting timelines remain a major risk because logistics assets often need to be positioned before production starts, which can delay utilization and pressure returns.

Page last updated on: