Russia Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

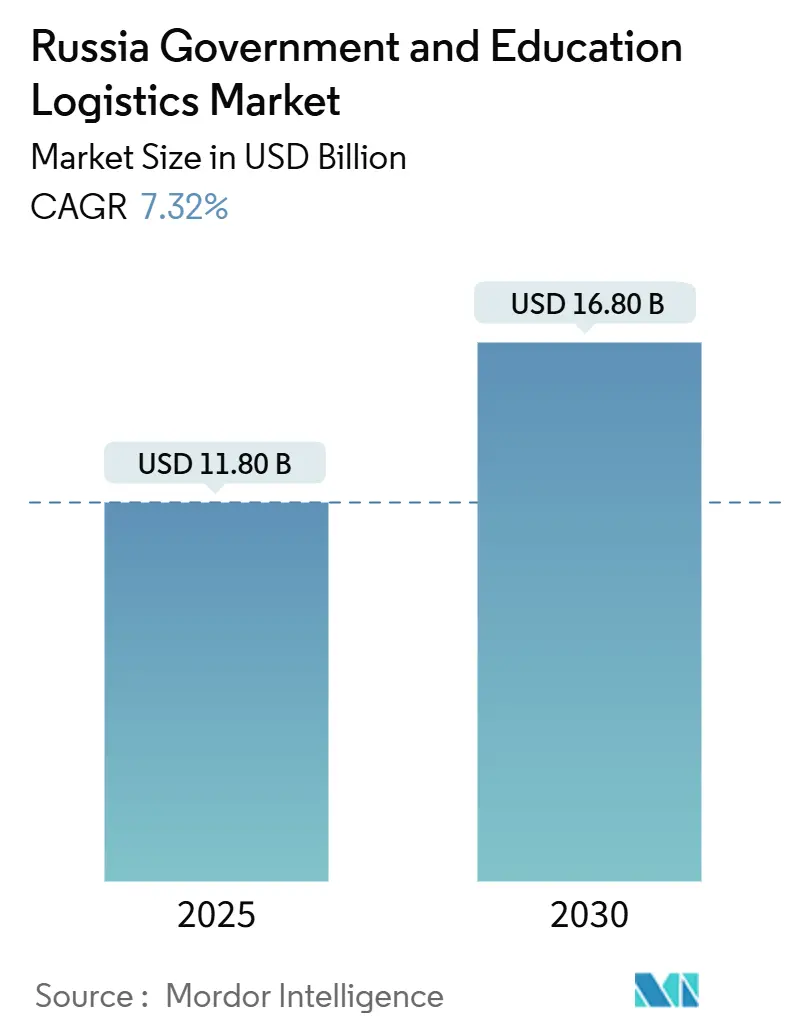

| Market Size (2025) | USD 11.80 Billion |

| Market Size (2030) | USD 16.80 Billion |

| Growth Rate (2025 - 2030) | 7.32% CAGR |

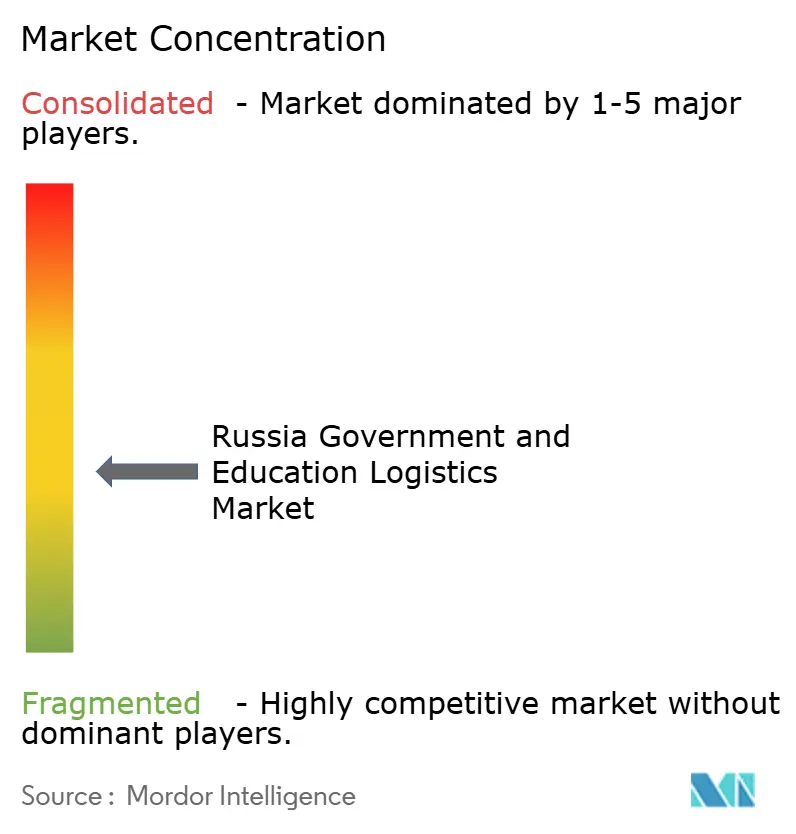

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Government And Education Logistics Market Analysis by Mordor Intelligence

The Russia Government And Education Logistics Market size is estimated at USD 11.80 billion in 2025, and is expected to reach USD 16.80 billion by 2030, at a CAGR of 7.32% during the forecast period (2025-2030).

The Russia government and education logistics market benefit from compulsory digitization mandates, sustained defense-sector spending, and a strategic realignment toward Asian trade corridors. Centralized automation funding is mitigating supply-chain bottlenecks that emerged after Western sanctions, while diversified multimodal options—rail, road, and northern sea lanes—are limiting route-specific risk. Demand for temperature-controlled distribution is rising as rural hospitals and laboratories require dependable vaccine and reagent flows. Meanwhile, domestic technology suppliers are expanding their footprint as import-substitution rules curb reliance on foreign hardware.

Key Report Takeaways

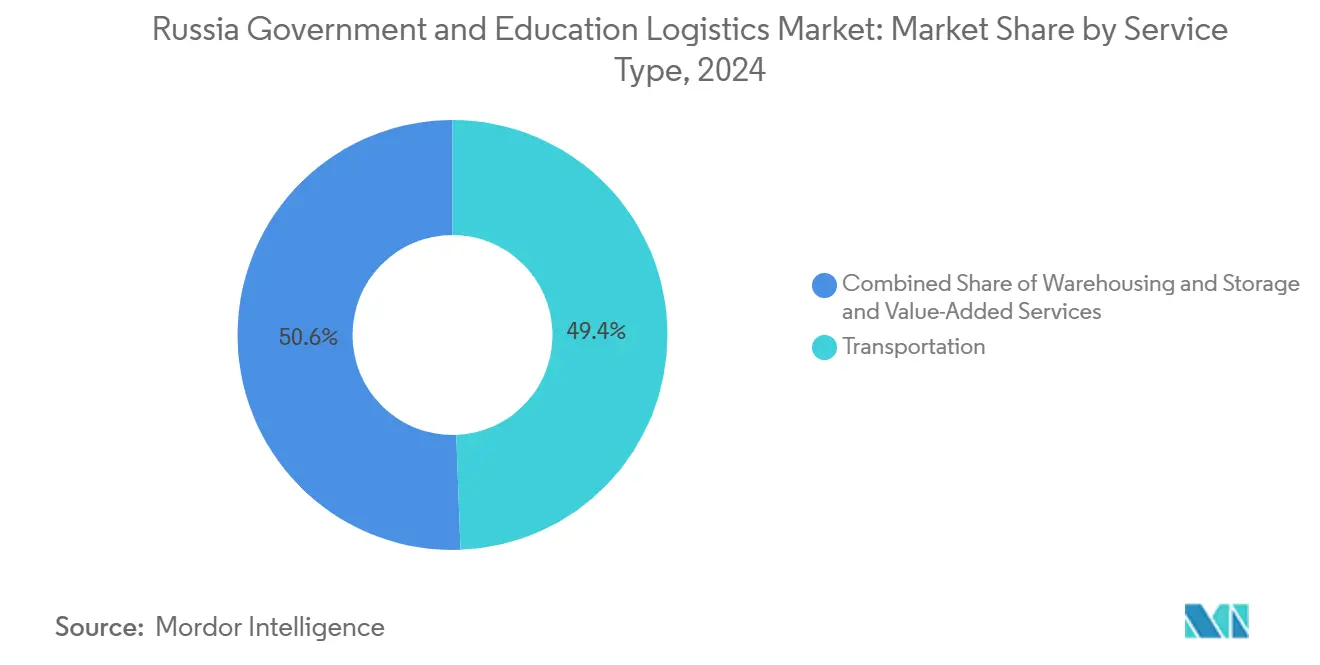

- By service type, transportation services led with a 49.40% of the Russia government and education logistics market share in 2024, while value-added services are forecast to expand at an 8.70% CAGR through 2030.

- By end-user, central/federal government agencies accounted for 33.00% of the Russia government and education logistics market size in 2024, whereas higher-education institutions are projected to grow at an 8.50% CAGR to 2030.

Relative standing becomes clear only when country-level and regional contributions are evaluated alongside one another at a global level. Mordor Intelligence's government and education logistics market share coverage captures this comparative structure.

Russia Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kremlin-mandated e-waybill rollout | +1.2% | National, early gains in Moscow, St. Petersburg, Novosibirsk | Medium term (2-4 years) |

| “Safe & High-Quality Roads” project | +0.8% | National, focus on rural and remote regions | Long term (≥ 4 years) |

| Pivot to China/EAEU freight corridors | +1.5% | Far East, Siberia, spillover to Central Russia | Short term (≤ 2 years) |

| Accelerated defense-sector procurement logistics | +1.1% | National, defense industrial regions | Short term (≤ 2 years) |

| Centralized warehouse-automation funding | +0.9% | National, major logistics hubs | Medium term (2-4 years) |

| Outcome-based 3PL/4PL contracting rules | +0.7% | National, pilot programs in federal districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Kremlin-Mandated E-Waybill Rollout Accelerates Digital Transformation

The 2027 electronic waybill deadline is reshaping every tier of the Russia government and education logistics market. Ministries integrating with the GosLog platform report double-digit cuts in document cycle time and closer oversight of public spending[1]Ministry of Digital Development, “GosLog Platform Expansion,” digital.gov.ru. Mandatory digital audit trails improve budget transparency, fostering trust among oversight bodies. Domestic software vendors are scaling quickly because import-substitution programs favor locally developed solutions. Early pilots inside defense and education ministries demonstrate that complex multimodal shipments can be tracked end-to-end without manual signatures. The resulting data lake is expected to inform national logistics planning well beyond 2030.

“Safe & High-Quality Roads” Project Transforms Rural Education Access

Government road-building outlays are unlocking last-mile delivery to remote campuses across Siberia and the Arctic[2]Ministry of Transport, “Safe and High-Quality Roads Program Update,” mintrans.gov.ru. New all-weather surfaces reduce seasonal closures that once halted textbook and equipment deliveries for months. Standardized loading zones at schools support heavier trucks, shortening unloading times. Integrated GPS tracking—now compulsory on public-sector vehicles—feeds real-time performance dashboards for provincial administrators. Better roads also lower fuel burn, freeing budget for technology upgrades in classrooms. The program aligns with the Russia government and education logistics market objective of universal service reliability.

China-EAEU Corridor Pivot Reshapes Freight Economics

Re-routing public-sector freight through China and Eurasian Economic Union corridors has cut typical transit times compared with disrupted west-bound lanes[3]Eurasian Economic Commission, “Freight Traffic Statistics,” eec.eaeu. Dedicated multimodal hubs in Vladivostok, Novosibirsk, and Yekaterinburg handle rising container volumes tied to university IT imports. Summer deployment of the Northern Sea Route adds capacity for bulk paper and lab glassware, though ice conditions still limit year-round use. Streamlined customs lanes for government cargo reduce clearance from days to hours at Zabaikalsk. Logistics firms with long-term Chinese partnerships gain pricing advantages in the Russia government and education logistics market.

Defense Procurement Logistics Drives Capacity Expansion

Heightened military procurement has triggered fresh investment in secure storage, armored trucking, and cleared workforce training[4]Ministry of Defense, “Logistics Modernization Initiative,” mil.ru. Specialized depots near defense industrial zones employ credentialed staff who later transition to civilian government logistics posts, raising overall competence in the Russia government and education logistics market. Shared transport corridors, including rail sidings and fortified road lanes, now benefit non-defense consignments during off-peak windows. Contracts specify Russian-made telematics devices to guard sensitive data, advancing the domestic hardware ecosystem. The rapid build-out of capacity reduces spot-market volatility across public-sector shipments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Border-crossing congestion with China | -0.8% | Far East, Zabaikalsk and Khorgos | Short term (≤ 2 years) |

| Federal budget austerity caps non-defense spend | -1.2% | National, larger effect on regional projects | Medium term (2-4 years) |

| Shortage of certified cold-chain capacity | -0.6% | Rural Siberia and Far East | Long term (≥ 4 years) |

| Import-substitution limits on automation hardware | -0.9% | National, major hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Border Congestion Constrains Asian Trade Efficiency

Truck queues stretching several kilometers at Zabaikalsk erode the time gains of the China pivot. Limited scanner lanes and manual declarations raise dwell time for sensitive educational electronics that require tamper-proof seals. Specialized vaccine shipments risk spoilage when refrigeration diesels idle too long at the checkpoint. Planned capacity upgrades face sanctions-driven import hurdles for advanced inspection equipment. Interim fixes include nighttime slotting and bonded rail shuttles, yet throughput remains below current demand in the Russia government and education logistics market.

Budget Austerity Threatens Non-Defense Logistics Investment

From 2026, tighter fiscal rules freeze civilian infrastructure allocations, delaying warehouse modernizations outside defense projects. Regional authorities reliant on federal transfers defer new cross-dock terminals, forcing reliance on outdated facilities. Universities expanding laboratory programs confront lead-time creep for imported reagents. Provincial governors lobby for public-private partnerships, but legal frameworks lag, adding complexity. The austerity headwind tempers the otherwise solid trajectory of the Russia government and education logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominance Amid Value-Added Expansion

Transportation services contributed 49.40% of 2024 revenue, underscoring their foundational role in the Russia government and education logistics market size. Road hauls dominate last-mile delivery, especially to settlements beyond the rail grid. Rail corridors, led by the Trans-Siberian mainline, provide cost-effective bulk moves for textbooks and construction inputs. Airfreight ensures continuity to Arctic and Far-East campuses during winter ice lock. Sea and inland waterways supplement capacity for bulky items during ice-free months, while the Northern Sea Route offers seasonal leverage.

Value-added services are on track for an 8.70% CAGR through 2030 as ministries seek integrated cold-chain, secure document handling, and real-time visibility. Automated distribution centers in Moscow and Novosibirsk process high-value lab instruments under 24-hour security. The adoption of robotics reflects warehouse-automation grants, with pick-to-light systems improving order accuracy. As the Russia government and education logistics market evolve, providers packaging transport, storage, and IT analytics into single contracts are winning multi-year tenders.

By End-User: Federal Agencies Lead While Higher Education Accelerates

The Central/Federal agencies represented 33.00% of the Russia government and education logistics market size in 2024, driven by standardized tendering that secures volume discounts and predictable service windows. Defense ministries negotiate long-haul rail slots with RZD at preferential tariffs, while civilian agencies leverage consolidated warehousing to trim inventory. State and local governments display uneven sophistication, with wealthier oblasts piloting 3PL partnerships.

Higher-education institutions are advancing at an 8.50% CAGR, reflecting campus expansions and research-grade equipment imports. University clusters such as Tomsk and Kazan now issue joint RFPs that bundle lab reagents and e-learning kits, driving economies of scale. IT-heavy degree programs escalate demand for just-in-time hardware replacement. As digital libraries proliferate, secure data center logistics also rise, adding nuance to the Russia government and education logistics market.

Geography Analysis

Metropolitan Moscow and St. Petersburg anchor hub-and-spoke distribution thanks to dense rail interchanges, multiple airports, and automated depots. From these nodes, trunk routes radiate to administrative capitals like Yekaterinburg, delivering government forms, school meals, and medical kits within predictable lead times. The Russia government and education logistics market benefit from coordinated night-trucking lanes that bypass urban congestion.

The Far-Eastern Federal District is emerging as the fastest-growing geography because of its proximity to China-centric corridors and targeted federal investment. Vladivostok’s free-port incentives lure 3PLs that bundle customs clearance with bonded warehousing. Cold-chain capacity is catching up as seafood and biotech supplies underpin route viability. Regional universities leverage cross-border partnerships, adding bilingual paperwork to logistics complexity.

Arctic and deep-Siberian territories remain cost-intensive due to sparse infrastructure and extreme temperatures. Winter aviation charters supply remote clinics and schools when roads close. Subsidized postal rates protect essential textbook deliveries, yet shipment variability persists. The Northern Sea Route offers relief during thaw months, but icebreaker scheduling limits total volumes. Government grants covering freight surcharges help level service standards, supporting equitable growth across the Russia government and education logistics market.

Analysis of the government and education logistics market by Mordor Intelligence spans multiple other regional evaluations across Europe, Africa, and Asia, supported by country-level insights for Spain, United Kingdom, South Korea, Mexico, France, and China, wherein local market conditions keep varying from one country to another.

Competitive Landscape

Market concentration is moderately fragmented. Russian Post combines the country’s largest last-mile network with growing warehouse automation, securing nationwide tenders. RZD Logistics leverages rail dominance and customs privileges, especially for defense consignments. FESCO and Baikal Service scale multimodal offerings that knit sea, rail, and trucking links into turnkey contracts. Sanctions have sidelined several international integrators, opening space for domestic players equipped with locally certified hardware and software.

Technology adoption is the defining rivalry axis. Leading firms deploy AI route planning and blockchain document vaults to meet e-waybill compliance. Cold-chain specialists retrofit fleets with Russian-made IoT thermographs, mitigating import restrictions. Regional challengers focus on niche verticals—such as hazardous-goods movement for emergency agencies—before extending into broader public contracts. Vertical integration from transport through IT platforms secures sticky, multi-year agreements in the Russia government and education logistics market.

Partnerships with Chinese rail carriers and port authorities have become critical differentiators. Providers that signed memoranda with CR Express gained priority slots on east-bound trains, protecting schedule integrity amid border delays. Meanwhile, state-backed financiers are co-investing in autonomous truck pilots, reinforcing domestic supply-side capacity. Competitive dynamics therefore reward capital access, regulatory insight, and geopolitical agility.

Russia Government And Education Logistics Industry Leaders

Russian Post

RZD Logistics

Oboronlogistics LLC

Delo Group

FESCO Transportation Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: FESCO Transportation Group and Softline launched a joint program to embed cloud-native analytics into public-sector freight operations.

- May 2025: Russian Post reinstated ground parcel services to China after a multimodal revamp, restoring a vital cross-border link for diplomatic mail and study-abroad documentation.

- April 2025: Two KAMAZ-54901 LNG trucks entered ITECO trial service, demonstrating ADR-compliant safety for hazardous materials crucial to emergency fuel deliveries.

- June 2024: ITECO and Sber signed a lease agreement covering 1,200 heavy trucks, channeling investments exceeding RUB 15 billion (USD 170 million) to refresh domestic long-haul capacity.

Russia Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing & Storage | |

| Value-Added Services |

| Central/Federal Government |

| State & Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing & Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State & Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others |

Key Questions Answered in the Report

What is the 2025 value of the Russia government and education logistics market?

It is valued at USD 11.8 billion in 2025.

How fast is demand for value-added logistics services growing?

Value-added services are projected to expand at an 8.70% CAGR through 2030.

Which end-user group is expanding the quickest?

Higher-education institutions lead growth with an 8.50% CAGR through 2030.

Why are e-waybills important for public-sector logistics?

The 2027 mandate streamlines documentation, cuts processing time, and supports budget transparency.

How do sanctions influence technology choices in logistics hubs?

Import-substitution rules favor domestically made hardware and software, shaping automation strategies.

Which geographic area shows the highest growth momentum?

The Far-Eastern Federal District, linked to China-EAEU corridors, is the fastest-growing region.

Page last updated on: