Australia Mining Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.02 Billion |

| Market Size (2026) | USD 10.43 Billion |

| Market Size (2031) | USD 12.53 Billion |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Mining Logistics Market Analysis by Mordor Intelligence

The Australia Mining Logistics Market size was valued at USD 10.02 billion in 2025 and is estimated to grow from USD 10.43 billion in 2026 to reach USD 12.53 billion by 2031, at a CAGR of 3.73% during the forecast period (2026-2031).

Rising bulk-haul volumes for iron ore, sustained federal and state capital spending on heavy-haul corridors, and rapid uptake of autonomous rail operations keep the Australia mining logistics market on a steady, efficiency-led growth path. Digital technologies, including AutoHaul locomotives and network-wide digital twins, are reducing fuel burn, minimizing unplanned downtime, and enhancing stockpile rotation, which helps stabilize per-ton costs even when diesel prices and labor scarcity exert upward pressure. Simultaneously, the emergence of lithium, rare earths, and copper exports is forcing operators to redesign networks around flexible, multi-commodity flows rather than single-product pipelines. Public commitments worth AUD 14 billion (USD 8.71 billion) to rail and port upgrades from 2024 to 2026 create capacity headroom that cushions against weather-related outages and commodity price swings.

Key Report Takeaways

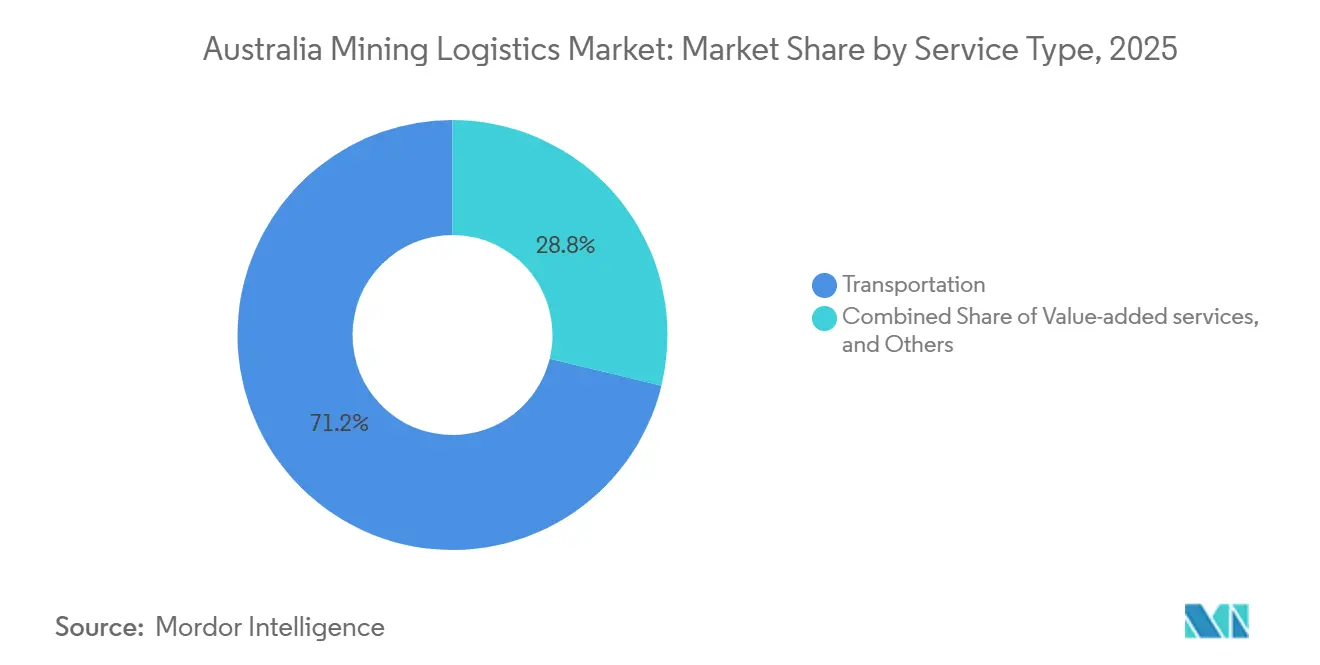

- By service type, transportation services led with 71.20% of the Australia mining logistics market share in 2025, while value-added services are projected to expand at a 4.65% CAGR between 2026-2031, the fastest rate among service categories.

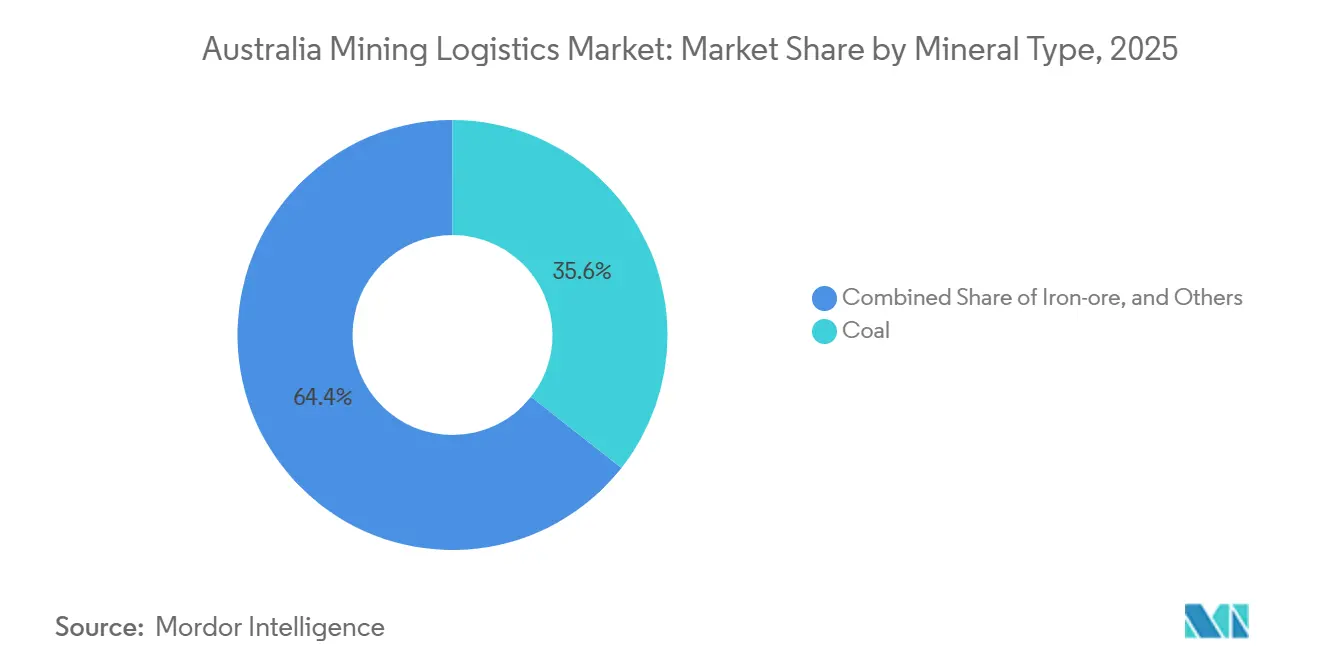

- By mineral type, coal captured 35.61% of the Australia mining logistics market size in 2025, the highest share among mineral segments. Gold logistics are advancing at a 5.13% CAGR between 2026-2031, the quickest pace among minerals.

- By geography, Western Australia held a 63.70% revenue share in 2025, the largest regional position. Queensland is set to post the strongest regional expansion, growing at a 4.50% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Mining Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging iron-ore export volumes sustain bulk-haul demand | +0.9% | Western Australia, with spillover to Northern Territory | Medium term (2-4 years) |

| Federal/state capex splurge on heavy-haul rail and port upgrades | +0.7% | National, with concentration in WA Pilbara and QLD coal corridors | Long term (≥ 4 years) |

| Rapid digitalisation (AutoHaul, telematics, digital twins) raises efficiency | +0.6% | Western Australia and Queensland core mining regions | Short term (≤ 2 years) |

| Global hunger for critical minerals (lithium, rare earths) diversifies flows | +0.5% | Western Australia lithium belt, Northern Territory rare earths | Medium term (2-4 years) |

| Green-iron pilot projects create new domestic pit-to-plant corridors | +0.3% | Western Australia Port Hedland and Pilbara region | Long term (≥ 4 years) |

| Early hydrogen-truck corridors cut fuel cost and open inland routes | +0.2% | South Australia, with early trials in copper belt to Port Adelaide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Iron-Ore Export Volumes Sustain Bulk-Haul Demand

Australia shipped 912 million tons of iron ore in 2025, 3.2% above 2024, and contracted volumes point to 945 million tons by 2027. The uplift concentrates on established Pilbara rail networks where Rio Tinto and BHP already operate more than 1,800 kilometers of heavy-haul track. Because mine life extensions rather than new pits generate the tonnage, incremental volumes flow over proven assets, preserving operator pricing power. Iron ore stays above 50% of total freight, anchoring the Australia mining logistics market even as critical minerals scale. The medium-term driver adds 0.9 percentage points to forecast CAGR by locking in long-term supply contracts that run to 2028[1]“Inland Rail Project,” Infrastructure Australia, infrastructureaustralia.gov.au.

Federal and State Capex on Heavy-Haul Rail and Ports

Canberra earmarked AUD 9.3 billion (USD 5.79 billion) for Inland Rail during 2024-2026, cutting Melbourne-to-Brisbane transit by 18 hours and per-ton-kilometer cost by 12% upon 2027 completion. Western Australia has allocated AUD 2.8 billion (USD 1.74 billion) for Pilbara port sidings, increasing Port Hedland's capacity from 570 million to 620 million tons by 2027. Queensland invested AUD 1.9 billion (USD 1.18 billion) to duplicate key coal lines, enabling 25 million extra tons when the works finish in late 2026. These assets lock in lower structural logistics costs for decades, giving Australian exports an edge over Brazilian and African rivals[2]“Global Hydrogen Review 2024,” International Energy Agency, iea.org.

Rapid Digitalisation Cuts Operating Cost

Fortescue’s AutoHaul fleet expanded to 54 autonomous locomotives and moved 1.2 billion tons in 2025 with zero crew incidents, trimming locomotive fuel use by 7%. Rio Tinto’s digital twin reduced unplanned maintenance by 18% soon after the 2024 rollout. BHP telematics lowered road-train fuel by 6% in 2024. Rapid payback places digital tools at the core of immediate gain, adding 0.6 percentage points to the Australia mining logistics market CAGR.

Global Hunger for Critical Minerals Diversifies Flows

Lithium output hit 86,000 tons LCE in 2025, up 22%, while rare-earth oxides reached 23,000 tons. Concentrates move in container loads that need contamination control, unlike bulk iron ore. Third-party logistics providers are installing inert-gas handling and blending sheds that carry 20%-plus margin premiums. Volumes will escalate through 2029, driving a 0.5 percentage-point bump to sector CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity-price volatility dampens 3PL contract visibility | -0.4% | National, with acute impact on coal and base-metals logistics | Short term (≤ 2 years) |

| Extreme cyclonic and flood events disrupt Pilbara / QLD supply chains | -0.3% | Western Australia Pilbara and Queensland coastal regions | Short term (≤ 2 years) |

| Escalating diesel-emission caps raise cost of road trains | -0.2% | National, with concentration in NSW and Queensland coal corridors | Medium term (2-4 years) |

| Acute remote-area driver and maintainer shortages strain capacity | -0.3% | Western Australia, Northern Territory, and Queensland remote mining regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Commodity-Price Volatility Shortens Contract Visibility

Iron ore prices yo-yoed between USD 95 and USD 135 per ton in 2025, while met-coal swung within a USD 100 band. Miners trimmed multi-year haulage deals and shifted toward spot slots, eroding revenue certainty for third-party carriers. Lower visibility lifts financing cost for specialized wagons and automated load-out, shaving 0.4 percentage points off forecast CAGR[3]“Mining Our Resources,” Queensland Department of Resources, resources.qld.gov.au.

Extreme Cyclonic and Flood Events Disrupt Supply Chains

Cyclone Ellie shut Pilbara rail for 12 days in February 2025, idling 4.5 million tons of ore and costing operators AUD 320 million (USD 199.29 million) in sales. Queensland floods in March 2025 swamped 40 kilometers of the Goonyella line, pausing exports for nine days. Recurrent events now push insurers to lift premiums 15%-25%, removing 0.3 percentage points from growth[4]“Australian Infrastructure Statistics Yearbook 2025,” Bureau of Infrastructure and Transport Research Economics, bitre.gov.au.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Automation Reweights Margin Pools Toward Value-Added Activities

Transportation services dominated the Australia mining logistics market with a 71.20% share in 2025. Rail moved 620 million tons, and road trains hauled 180 million tons, underscoring the scale of pit-to-port flows in Western Australia and Queensland. Yet digitalised locomotive fleets, predictive maintenance, and optimized loading are flattening the cost curve, tempering growth in the core haulage segment. Road remains indispensable for remote base-metal and gold sites beyond rail reach, while coastal shipping handles mineral sands and manganese where draft limits apply.

Value-added services such as blending, inventory management, quality assurance, and packaging are tracking a 4.65% CAGR (2026-2031), comfortably ahead of the Australia mining logistics market average. Miners cut stock-coverage days at Chinese steel mills to 18, stimulating demand for precise, just-in-time shipments. Fortescue reinvested AUD 216 million (USD 134.52 million) saved from AutoHaul into Pilbara blending hubs, confirming how automation reallocates capital toward higher-margin offerings. Qube and Toll added automated container handlers and expanded covered storage to capture lithium and copper flows that require contamination control, while drone-based stockyard measurement reduced blend variability by 15% at BHP facilities.

By Mineral/Metal: Diversification Boosts Higher-Value Streams

Coal retained 35.61% of Australia mining logistics market share in 2025, with metallurgical grades at 22% and thermal at 14%. Asian steelmakers’ gradual pivot to electric-arc furnaces eroded met-coal loadings 4% in 2025, and European climate policies trimmed thermal cargoes 6%.

Gold logistics, by contrast, are forecast to post a 5.13% CAGR between 2026-2031, outpacing coal and iron ore. Record USD 2,340 per-ounce prices accelerate Western Australia and Northern Territory output, triggering demand for secure, time-critical transport from mine gate to refinery. Emerging rare-earth and lithium corridors add specialized, container-based cargo that commands premiums over bulk freight. Copper concentrate from Mount Isa and Cloncurry rose to 1.8 million tons in 2025 and will benefit from the Australia mining logistics market size growth as new capacity at Townsville port comes onstream.

Geography Analysis

Western Australia contributed 63.70% of Australia mining logistics market value in 2025, anchored by 620 million tons of iron ore and 3.2 million tons of lithium concentrate. Captive rail spanning 1,800 kilometers and Port Hedland’s world-scale berths underpin the lowest delivered cost to Asian mills. Autonomous locomotives sliced rail operating expense 7% in 2025, reinforcing the region’s dominance. Still, three cyclones in two years triggered multi-day outages, highlighting resilience gaps in coastal assets. Green-iron pilots now create intra-state pit-to-plant corridors that may divert part of the export stream into domestic processing by 2028.

Queensland is projected to grow fastest at 4.50% CAGR (2026-2031), supported by met-coal demand recovery and copper expansion in the northwest. Rail duplications on the Goonyella and Blackwater systems deliver 25 million extra-ton capacity by late 2026, trimming queue times at Dalrymple Bay. However, the March 2025 flood that submerged 40 kilometers of track revealed the exposure of coastal corridors to climate events.

South Australia is emerging as a hydrogen logistics testbed. Six fuel-cell road trains on the Prominent Hill corridor target 30% fuel savings, and refueling capacity for 20 trucks will be operational by 2026. Northern Territory’s Nolans rare-earth project will move 14,000 tons annually by 2027 along a new 1,800 kilometer corridor to Darwin port that needs inert-gas ISO containers. New South Wales remains centered on Hunter Valley coal, while Victoria and Tasmania handle modest mineral sands and brown-coal loads, constrained by shallow ports. Collectively, these states account for 12% of Australia mining logistics market volume.

Competitive Landscape

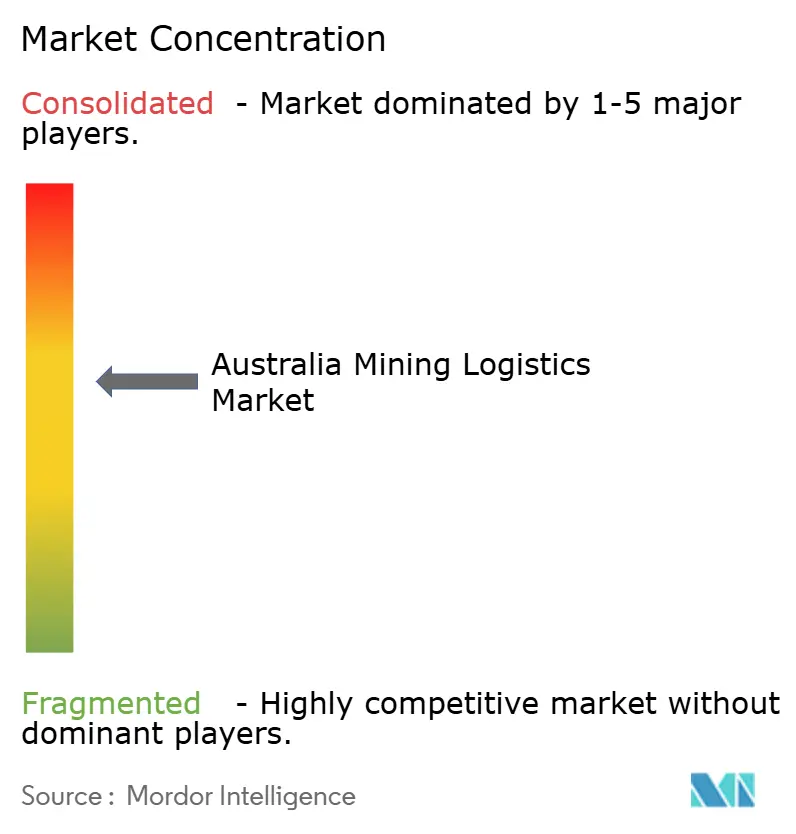

The Australia mining logistics market sits at a moderate concentration level. Integrated miners BHP, Rio Tinto, and Fortescue move two-thirds of iron-ore tonnage over captive networks, locking in scale efficiencies yet limiting third-party access. Aurizon’s Queensland rail hauled 210 million tons in 2025 but is channeling USD 78 million into new wagons for bulk diversification. Pacific National deploys predictive maintenance on coal corridors to defend contracts. Qube and Toll enlarge value-added footprints through automated warehouses that cater to lithium and copper flows, winning premium fees.

White-space growth lies in critical minerals that require contamination-free handling and inert atmospheres. Linfox partnered with Arafura on rare-earth containers tailored to oxidation control, capturing high-margin lanes. Smaller outfits like Centurion target gold-doré haulage where security and time sensitivity trump size. Hydrogen truck pilots threaten diesel incumbents on inland routes longer than 400 kilometers if fuel-cell costs decline as forecast.

Technology patents for autonomous rail climbed 35% during 2024-2025, with Hitachi and Wabtec refining obstacle detection and energy management. Compliance with ISO 55001 asset-management standards has turned into a contract prerequisite as miners push end-to-end transparency for ESG audits.

Australia Mining Logistics Industry Leaders

Aurizon

Linfox Pty, Ltd.

BIS Industries

Centurion

Toll Holdings, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Linfox extended its partnership with Fortescue Metals Group, adding specialized transport and warehousing services across the Pilbara.

- October 2024: Toll Group announced a AUD 200 million (USD 124.56 million) fleet renewal that includes 400 Euro 6 prime movers for long-haul mining routes.

- August 2024: Linfox teamed with Arafura Rare Earths to design inert-gas container systems for the Nolans project.

- June 2024: Rio Tinto completed the AutoHaul expansion, bringing autonomous control to additional Pilbara rail sections.

Australia Mining Logistics Market Report Scope

Mining logistics is associated with providing services and solutions to enable the smooth transportation of materials from mines, processing plants, and inventories to railways, ports, ships, and finally to the destination markets. Furthermore, the report offers a complete background analysis of the Australian mining logistics market, which includes an assessment of the economy, a market overview, market size estimation for critical segments, emerging trends in the market, market dynamics, and key company profiles.

The Australia Mining Logistics Market is segmented by service (Transportation, Warehousing and Inventory Management, and Value-added Service) and type of mineral/metal (Iron Ore, Base Metals, Coal, Gold, and others). The report offers the market size and forecast in value (USD billion) for all the above segments.

| Transportation | Road |

| Rail | |

| Coastal Shipping/Barge | |

| Air | |

| Warehousing and Inventory Management | |

| Value-added Services |

| Iron Ore |

| Metallurgical and Thermal Coal |

| Base Metals (Cu, Zn, Ni) |

| Gold |

| Other Minerals/Metals |

| Western Australia |

| Queensland |

| New South Wales |

| South Australia |

| Northern Territory |

| Victoria |

| Tasmania |

| By Service | Transportation | Road |

| Rail | ||

| Coastal Shipping/Barge | ||

| Air | ||

| Warehousing and Inventory Management | ||

| Value-added Services | ||

| By Mineral / Metal | Iron Ore | |

| Metallurgical and Thermal Coal | ||

| Base Metals (Cu, Zn, Ni) | ||

| Gold | ||

| Other Minerals/Metals | ||

| By Geography | Western Australia | |

| Queensland | ||

| New South Wales | ||

| South Australia | ||

| Northern Territory | ||

| Victoria | ||

| Tasmania |

Key Questions Answered in the Report

How large is the Australia mining logistics market in 2026?

How large is the Australia mining logistics market in 2026?

What is the forecast growth rate through 2031?

What is the forecast growth rate through 2031?

Which service area is expanding fastest?

Which service area is expanding fastest?

Which region records the highest value share in 2025?

Western Australia accounts for 63.70% of total market value in 2025, driven by Pilbara iron-ore output.

What technology trend is most transformative?

What technology trend is most transformative?

Which mineral segment shows the strongest growth outlook?

Which mineral segment shows the strongest growth outlook?

Page last updated on: