Brazil Mining Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

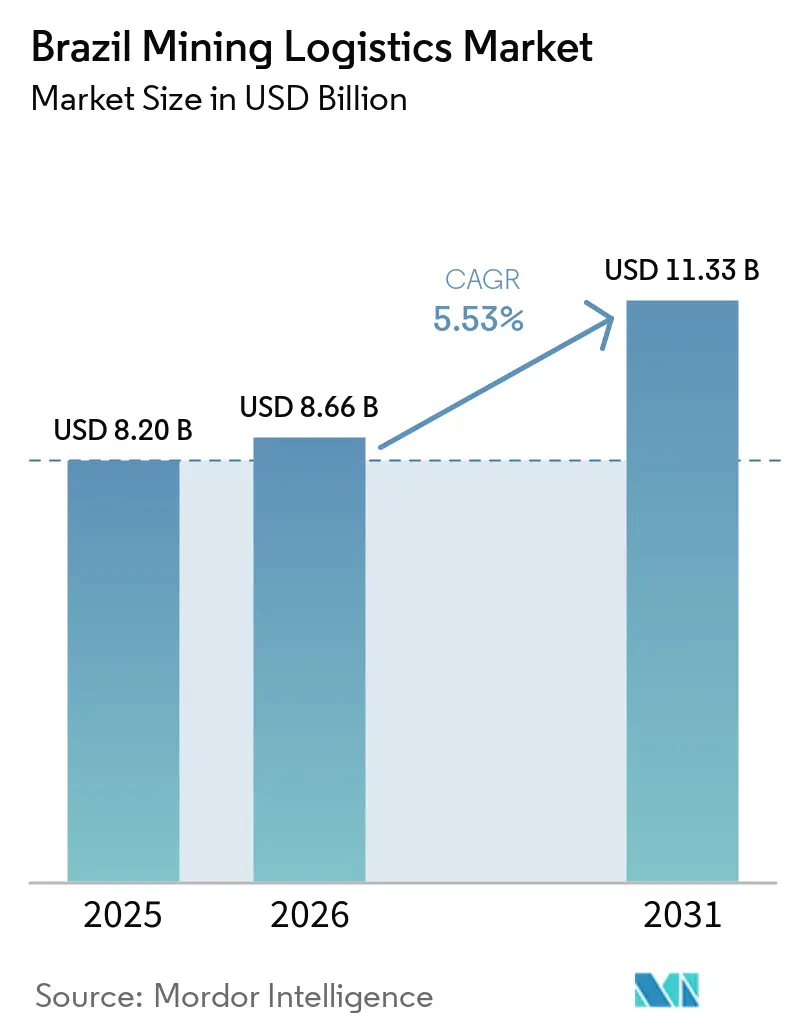

| Base Year Market Size (2025) | USD 8.20 Billion |

| Market Size (2026) | USD 8.66 Billion |

| Market Size (2031) | USD 11.33 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

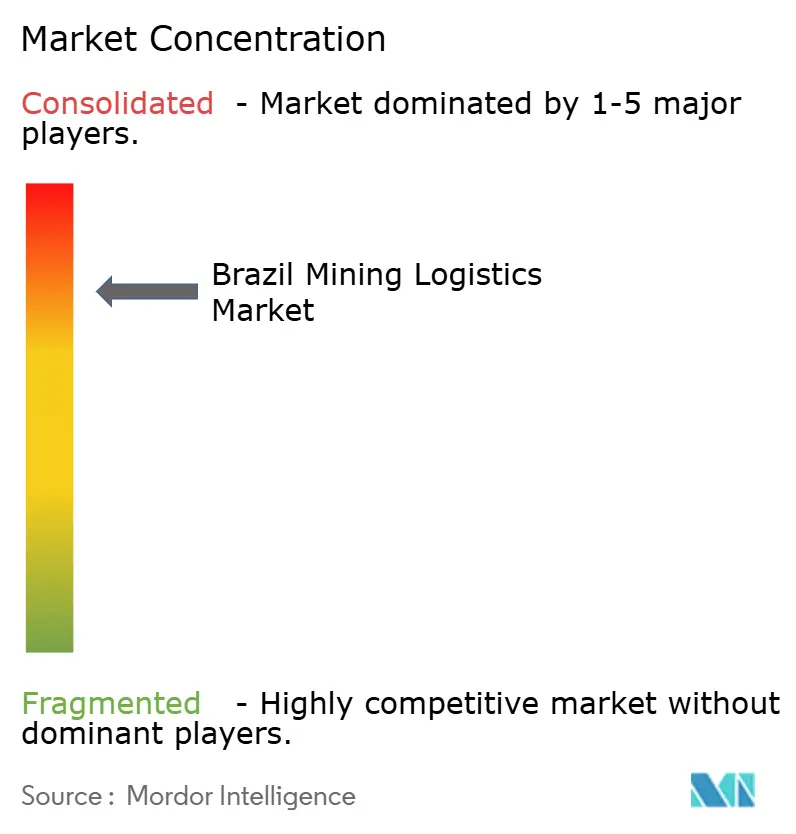

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Mining Logistics Market Analysis by Mordor Intelligence

The Brazil mining logistics market size is expected to grow from USD 8.2 billion in 2025 to USD 8.66 billion in 2026 and is forecast to reach USD 11.33 billion by 2031 at 5.53% CAGR over 2026-2031.

The Brazil mining logistics market is being supported by record iron ore export volumes, renewed rail concessions, and a higher mining investment base. Brazilian mining companies project USD 11.3 billion in logistics investments between 2026 and 2030, which is 3.4% above the 2025-2029 cycle and points to demand that is tied to mine development and corridor build-out rather than a short freight upswing. The Brazil mining logistics market is also broadening beyond iron ore, as copper, nickel, lithium, and niobium projects require different terminal handling, custody, storage, and inland transport configurations than legacy bulk systems. Renewed rail and port concessions are giving operators more certainty about capex timing, while multimodal projects are creating space to shift part of mineral flows away from roads in saturated corridors. At the same time, the Brazil mining logistics market still faces licensing delays, corridor dependence, and network fragmentation, which keep scale, asset control, and execution discipline at the center of competition.

Key Report Takeaways

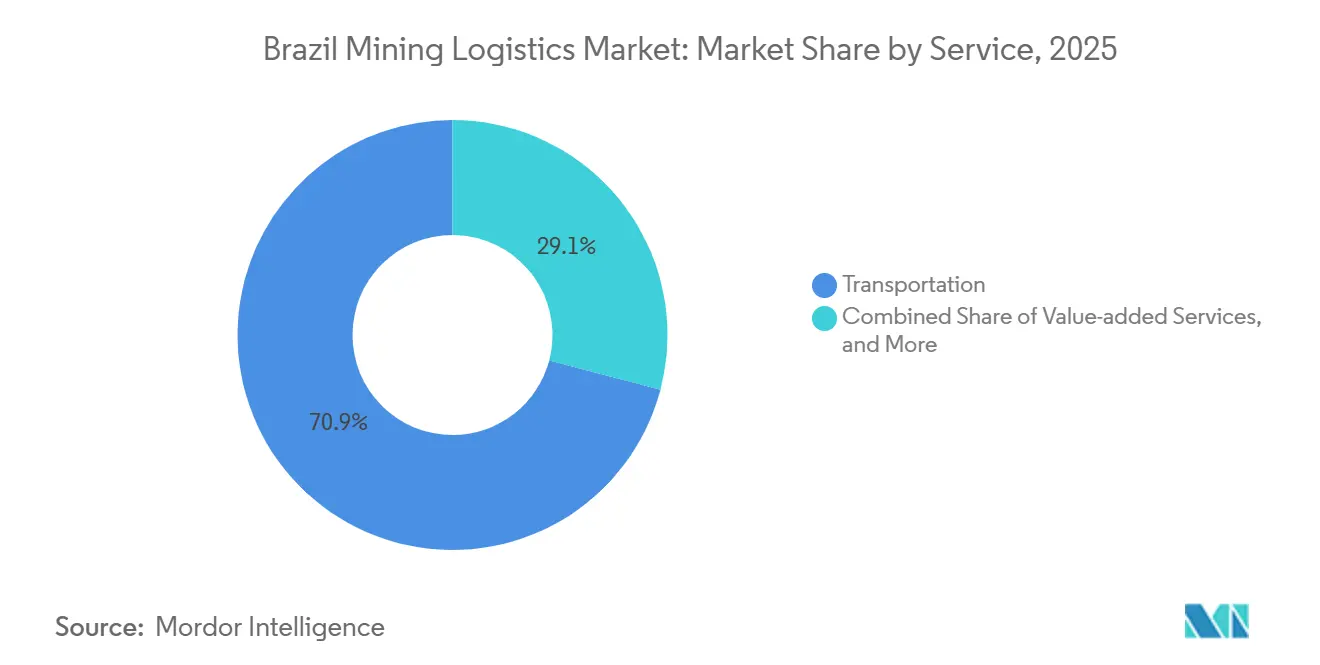

- By service, transportation held 70.91% of the Brazil mining logistics market share in 2025, while value-added services are forecast to expand at a 6.42% CAGR through 2031.

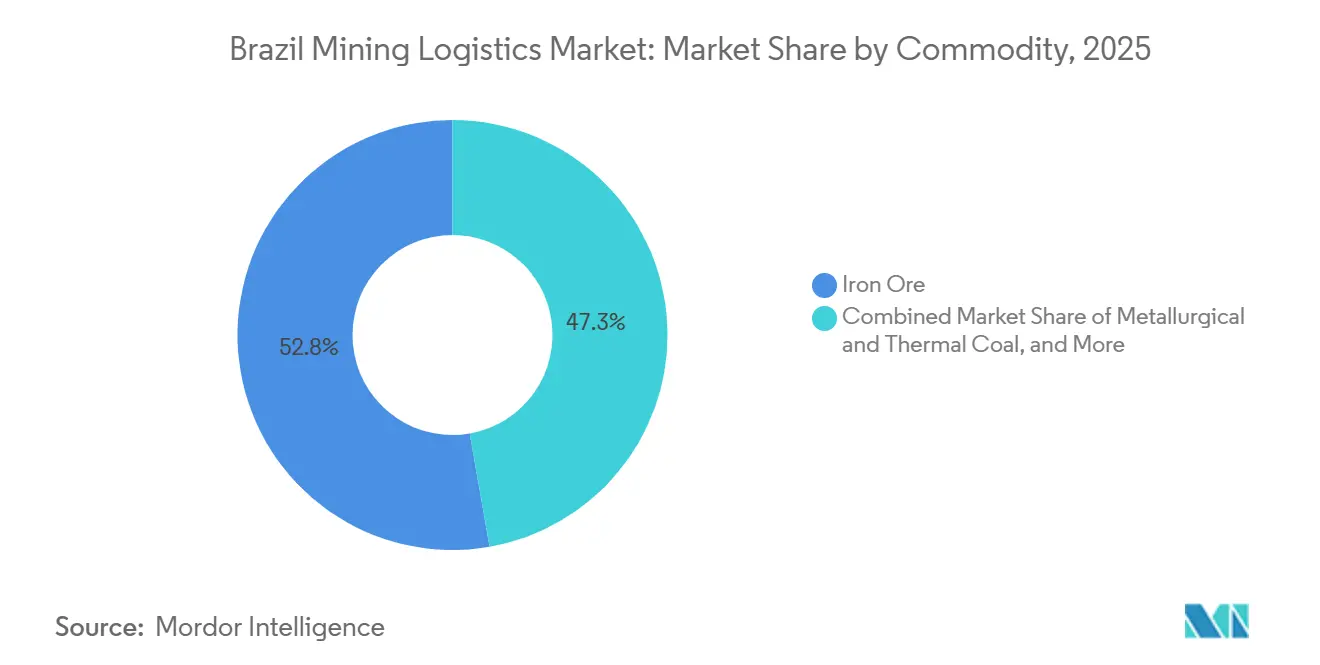

- By commodity, iron ore accounted for 52.75% of the Brazil mining logistics market share in 2025, while base metals are projected to grow at a 5.77% CAGR through 2031.

- By geography, the Southeast accounted for 41.96% of the Brazil mining logistics market size in 2025, while the North is projected to grow at a 6.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Mining Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-led iron ore corridor expansion | +1.3% | Southeast, Minas Gerais, Espírito Santo, Rio de Janeiro, North, Pará, Maranhão | Medium term (2-4 years) |

| Rail and port concession renewals unlocking capex | +1.0% | National, all regions with concession rail arteries | Short term (≤ 2 years) |

| Critical minerals project pipeline scaling | +0.9% | North, Pará, Central-West, Goiás, Mato Grosso, Southeast | Long term (≥ 4 years) |

| Multimodal optimization and modal shift for bulk flows | +0.7% | National, with early gains in São Paulo, Minas Gerais, Mato Grosso | Medium term (2-4 years) |

| Northern arc and bioceanic corridor diversification | +0.5% | North, Pará, Maranhão, Central-West, with spillover to the Northeast | Medium term (2-4 years) |

| Traceability and climate disclosure pressure are lifting auditable low-carbon logistics | +0.3% | Global mandate, concentrated in Southeast and North export nodes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Export-Led Iron Ore Corridor Expansion Sustains Capex Density

The Brazil mining logistics market continues to be shaped by the scale of the iron ore corridors that connect Carajas and Minas Gerais to Atlantic export terminals. Vale regained its position as the world’s largest iron ore producer in 2025 with output of 336 million tons, and it targets 335 million to 345 million tons in 2026 with a long-run ambition of 360 million tons by 2030, which keeps rail and terminal capacity needs on an upward path. The December 2024 framework agreement for the early renewal of the EFC and EFVM concessions removed much of the planning uncertainty that had held back rolling stock and terminal decisions. As export volumes approach the upper end of installed berth capacity, pre-shipment storage, blending yards, and staging operations gain value in the Brazil mining logistics market. This keeps corridor investment dense even when the main volume driver remains a single commodity.

Rail and Port Concession Renewals Unlock a Self-Financing Infrastructure Cycle

The Brazil mining logistics market is also benefiting from a concession cycle that is creating a funding path for new rail assets without depending on broad fiscal spending. Fees and commitments linked to Vale, MRS Logistica, and Rumo are being directed toward new projects such as the 575-kilometer EF-118 Southeast Railway Ring, projected at BRL 6.12 billion (USD 1.08 billion), with Vale contributing BRL 1.8 billion (USD 319 million) to support its viability[1]“Environmental, Social and Governance Laws and Regulations Report 2026, Brazil,” ICLG, iclg.com. CSN Mineracao’s completion of its BRL 3.35 billion (USD 578 million) acquisition of MRS Logistica shares in December 2025 deepened vertical integration in the Southeast corridor and points to a more asset-linked ownership structure in the Brazil mining logistics market. VLI’s proposal for a 30-year FCA concession renewal, tied to BRL 30 billion (USD 5.17 billion) in investments, would reshape capacity in the Northeast and Central-West if it is finalized. The rail transport agent model under Law 14.273/2021 also begins testing whether corridors that once operated under captive economics can move toward more open access and lower tariff premiums.

Critical Minerals Pipeline Creates Structurally New Logistics Sub-Markets

The Brazil mining logistics market is no longer defined only by iron ore, because the investment pipeline for critical and strategic minerals reaches USD 21.3 billion for 2026-2030 within a wider mining pipeline of USD 76.9 billion. Copper alone accounts for USD 8.6 billion in projected investments through 2030, and Vale Base Metals plans USD 1.6 billion of capex in 2026 before moving toward USD 2 billion per year from 2027, with a copper production target of 500,000 tons by 2030[2]“Study Proposes Ways to Enhance Interoperability and Intermodality in Brazil’s Railways,” Portal FGV, portal.fgv.br.. Vale’s 20-year renewal of its copper terminal at Itaqui, together with BRL 221.5 million (USD 42 million) in additional spending, shows that copper flows are being built as a separate logistics chain with distinct handling and yard requirements. Gold, niobium, and lithium projects also require stronger purity custody and more specialized handling than mainstream bulk systems usually provide. From 2026, sustainability disclosure requirements under CVM Resolution 193/2023 add another layer of traceability pressure, which lifts demand for auditable logistics services in the Brazil mining logistics market.

Multimodal Integration Unlocks Latent Rail Capacity at Logistics Hubs

The Brazil mining logistics market is also moving toward a broader mix of rail, road, waterways, and port integration. MRS Logística is investing BRL 1.5 billion (USD 259 million) to enter waterway logistics through two terminals on the Tiete-Parana Waterway, indicating that leading rail operators are seeking to capture value beyond the core line-haul leg. In the first quarter of 2026, MRS transported 46.3 million tons and invested BRL 753.6 million (USD 133 million), while its intermodal corridor with Ocean Network Express added a live example of rail-sea integration on the Santos axis. FGV Transportes found that rights-of-way and mutual traffic account for only 8% of rail freight, while 70% of the network remains idle, which means the Brazil mining logistics market still has large unrealized productivity inside existing assets. Rumo’s first 162-kilometer Mato Grosso Railway phase, inaugurated in June 2026 with 10 million tons per year of capacity, reinforces the economic case for shifting part of mineral flows away from all-road movement in inland districts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rail-port licensing and execution delays | -0.8% | National, most acute in Bahia, FIOL and Porto Sul, and the Northeast, including Transnordestina | Medium term (2-4 years) |

| Commodity price volatility delaying logistics commitments | -0.6% | Global, with concentrated impact in the Southeast for iron ore and the North for copper and bauxite | Short term (≤ 2 years) |

| Gauge fragmentation and captive-corridor dependence | -0.6% | National, most severe at Southeast-Northeast junction corridors | Long term (≥ 4 years) |

| Social-environmental constraints in amazon and coastal nodes | -0.4% | North, Amazon basin, Northeast coastal zones, Central-West Cerrado | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Licensing and Execution Delays Impose a Structural Tax on Logistics Investment

The Brazil mining logistics market continues to absorb delays that are not always visible in headline project values. BAMIN’s FIOL Section 1 concession remains incomplete in 2026, and the pending Mota-Engil acquisition process still needs to settle ownership and financing before the Pedra de Ferro mine, railway, and port plan can move ahead[3]“Brazilian Mining Drives Logistics Investments,” BNamericas, bnamericas.com.. The Transnordestina railway tells a similar story, because it has already absorbed BRL 8.2 billion (USD 1.48 billion) in cumulative investment and received BRL 3.6 billion (USD 650.35 million) in financing authorization, yet it still lacks completion certainty after many years of review. These delays weigh more heavily on smaller producers than on integrated majors, because a miner with one route cannot redirect cargo as easily as Vale or other large operators. That asymmetry keeps execution risk elevated across parts of the Brazil mining logistics market even when long-term mineral demand remains favorable.

Gauge Fragmentation Constrains Network Efficiency Across Mineral Corridors

The Brazil mining logistics market also remains constrained by a railway network that is physically extensive but operationally fragmented. Brazil has 30,653 kilometers of railways, yet a 2024 audit found that only 12.7% operated at high capacity and close to 19,000 kilometers were idle or underused, which points to governance and interoperability gaps rather than a simple shortage of track. Broad, standard, and meter gauges still prevent direct wagon movement across several mineral corridors, forcing transshipment and raising cost per tonne on multi-origin flows. FGV Transportes also found that inter-concession interoperability accounts for only 8% of national rail freight, indicating that contractual barriers persist even where parallel capacity exists. Because the current infrastructure agenda prioritizes added capacity more than gauge standardization, this friction is likely to stay in place across the forecast horizon of the Brazil mining logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Integration Value Lifting Transportation While Value-Added Services Outpace the Market

Transportation held 70.91% of Brazil mining logistics market share in 2025, which kept it as the core revenue engine of the Brazil mining logistics market. Rail remained the largest contributor inside Transportation, supported by Vale’s EFC and EFVM systems, MRS Logistica’s record 213 million tons in 2025, and Rumo’s expanding network footprint. MRS posted BRL 7.58 billion (USD 1.31 billion) in net revenue in 2025 and BRL 1.55 billion (USD 280.01 million) in profit, which shows how quickly earnings strengthen when iron ore volumes rise on fixed rail infrastructure. Sea and inland waterway services are gaining ground within Transportation, with Northern Arc ports handling 163.3 million tons in 2025 and mineral flows, such as bauxite, moving through that corridor on a larger scale. Road transport still matters for pre-rail collection in remote copper and nickel areas, while air freight remains limited to samples, urgent parts, and very small high-value shipments.

Value-Added Services is projected to post the fastest Brazil mining logistics market size expansion by service at a 6.42% CAGR through 2031. That growth reflects a shift in the Brazil mining logistics industry, where reporting, traceability, emissions accounting, and chain-of-custody support are moving from optional add-ons to operational requirements. International voluntary certification systems such as TSM, IRMA, and ASI are reinforcing that shift by raising expectations for auditable logistics records and verified handling procedures. Warehousing and Inventory Management also keeps a steady role, supported by Samarco’s BRL 13.8 billion (USD 2.65 billion) investment plan to restore full capacity by 2028, which requires more buffer storage and pellet yard support at Ubu.

By Commodity: Iron Ore Anchors Revenue While Base Metals Drive Structural Diversification

Iron ore accounted for 52.75% of the Brazil mining logistics market size in 2025, which confirms that the Brazil mining logistics market still rests on the country’s deepest mine-rail-port systems. That position reflects the long build cycle of integrated assets in the Southeast and North, where sunk capital, corridor permits, and export terminals are difficult to replicate under current licensing conditions. Samarco produced 15.1 million tons of iron ore pellets and fines in 2025, its highest level since operations resumed, and first quarter 2026 output reached 3.8 million tons, up 18% year on year, which supports added logistics demand through the Ubu complex. Coal, gold, and other minerals remain smaller logistics streams and often move on corridors that were built primarily for iron ore. That leaves non-iron-ore shippers exposed to tariff and scheduling conditions on shared networks.

Base Metals is projected to deliver one of the clearest new growth lanes in the Brazil mining logistics market, with a 5.77% CAGR through 2031. Vale Base Metals plans USD 1.6 billion in capex for 2026 and targets 500,000 tons of copper output by 2030, up from 382,400 tons in 2025, underscoring the need for separate concentrate logistics and terminal design. Vale’s 20-year renewal of the Itaqui copper terminal, tied to BRL 221.5 million (USD 42 million) of additional investment, and Ero Copper’s 2026 capex plan both show that dedicated copper handling is becoming a capital priority. In the Brazil mining logistics industry, this shift creates room for higher-margin services in segregated storage, moisture control, and custody-sensitive movement for concentrates and refined intermediate products.

Geography Analysis

The Southeast held 41.96% of Brazil mining logistics market share in 2025, which kept it as the anchor geography in the Brazil mining logistics market. This lead rests on the Quadrilatero Ferrifero ore base and on the corridor systems controlled by Vale, MRS Logistica, and CSN Mineracao. The region also benefits from the concentration of export terminals at Tubarao, Itaguai, and Acu, which limits diversion distance and supports high throughput density. CSN Mineracao’s TECAR modernization and the EF-118 project show that capacity additions in the Southeast are now moving beyond maintenance and into network expansion. The South adds smaller but relevant flows through the Rio Grande and Rumo’s southern network, mainly in steel-linked and coal-linked movements.

The North is the fastest-growing geography in the Brazil mining logistics market at a 6.09% CAGR through 2031. Northern Arc ports handled 163.3 million tons in 2025, well above the national growth pace, and bauxite throughput of 24.8 million tons confirms the region’s role in mineral bulk exports. The convergence of mineral and agricultural flows is making the North the decisive infrastructure axis for shared logistics scale. Planned studies on the bi-oceanic FIOL-FICO corridor and the longer-term path toward Ferrograo would deepen this role if permitting and execution move forward.

The Northeast sits near a structural turning point in the Brazil mining logistics market, but that turn still depends on FIOL and Porto Sul reaching operation. The Transnordestina case shows how financing approvals alone do not resolve multi-agency delay risk, even after BRL 8.2 billion (USD 1.48 billion) of cumulative investment and BRL 3.6 billion (USD 650.35 million) of financing authorization. The Central-West is still led by agricultural logistics, yet the Mato Grosso Railway and related corridor works start to create a mineral-capable network for shippers that currently depend on BR-163 road haulage. The speed at which these inland regions translate planned capacity into active mineral flows will shape the next phase of the Brazil mining logistics market.

Competitive Landscape

The Brazil mining logistics market remains concentrated around a small group of operators that control the main rail arteries and the linked export corridors. Vale, MRS Logistica, VLI Logística, and Rumo sit at the center of this structure because concession formats have historically favored corridor incumbency over broad intramodal competition. That pattern gives major operators stronger pricing power, deeper asset visibility, and a better ability to align mine output with terminal slots across the Brazil mining logistics market. CSN Mineracao’s BRL 3.35 billion (USD 578 million) acquisition of MRS shares in December 2025 is a clear example of this trend, because it tightens the link between ore production and the primary rail route to port in the Southeast. Vale’s interest in Porto Sudeste, if it progresses, would push concentration further at the terminal level in the Brazil mining logistics market.

Railway Law 14.273/2021 is starting to test whether this structure can become more open without dismantling concession economics[4]“Environmental, Social and Governance Laws and Regulations Report 2026, Brazil,” ICLG, iclg.com.. VLI’s entry onto Vale’s EFVM under the rail transport agent model is the first practical sign that third-party access could expand on corridors once treated as captive systems. The result matters for the Brazil mining logistics market because lower access barriers would affect tariffs, rolling stock planning, and customer choice across mine-to-port services. Even so, physical interoperability and commercial access remain limited, so the incumbent advantage is still strong.

Competitive white space is clearer in critical minerals than in legacy iron ore logistics. Copper concentrate handling, battery-grade lithium movement, and rare-earth custody services still lack purpose-built scale infrastructure, even though the critical minerals pipeline is large and growing. Mota-Engil’s due diligence on BAMIN could also change the Northeast corridor if Chinese-backed construction and financing capacity accelerates the FIOL and Porto Sul build-out. Technology is becoming a second layer of competition, with Wilson Sons using AI-led predictive maintenance and MRS adding monitoring and waterway capabilities to lift utilization without relying only on greenfield expansion. In the Brazil mining logistics market, that combination of asset scale, modal breadth, and operating technology continues to raise the bar for new entrants.

Brazil Mining Logistics Industry Leaders

Vale SA

MRS Logistica

VLI Logistica

CSN Mineracao

Rumo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Rumo inaugurates the first 162-kilometer phase of the Mato Grosso Railway on June 19, connecting Rondonopolis to the Dom Aquino and BR-070 terminal. The BRL 5 billion (USD 903.27 million) project, financed in part by a BRL 2 billion (USD 354 million) BNDES debenture, has a capacity for 10 million tons of grains and mining commodities per year, completing the largest active railway construction project in Brazil at the time of inauguration.

- April 2026: MRS Logistica and Ocean Network Express launch a 213-kilometer intermodal corridor from Paulinia to the Port of Santos, initiating live-cargo testing with a multinational chemicals client. The corridor represents the first rail-sea integration on Brazil’s most congested logistics artery.

- February 2026: CSN Mineracao announces a BRL 400 million (USD 70.8 million) investment to expand and modernize the TECAR pier at the Port of Itaguaí, with construction beginning in August 2026. Capacity will increase from 42 million to 60 million tons per year of iron ore by 2030, with berth expansion enabling two vessels to load simultaneously.

- February 2026: Tidewater announces a USD 500 million all-cash acquisition of Wilson Sons Ultratug Participacoes, expanding its Brazilian offshore fleet from 6 to 28 vessels. The transaction, approved by Tidewater’s board, is subject to CADE approval targeted for late second quarter 2026 and will more than quadruple Tidewater’s presence in Brazil’s offshore support logistics business.

Brazil Mining Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea and Inland Waterways | |

| Air | |

| Warehousing and Inventory Management | |

| Value-Added Services |

| Iron Ore |

| Metallurgical and Thermal Coal |

| Base Metals (Cu, Zn, Ni) |

| Gold |

| Other Minerals/Metals |

| North |

| Northeast |

| Central-West |

| Southeast |

| South |

| By Service | Transportation | Road |

| Rail | ||

| Sea and Inland Waterways | ||

| Air | ||

| Warehousing and Inventory Management | ||

| Value-Added Services | ||

| By Commodity | Iron Ore | |

| Metallurgical and Thermal Coal | ||

| Base Metals (Cu, Zn, Ni) | ||

| Gold | ||

| Other Minerals/Metals | ||

| By Geography | North | |

| Northeast | ||

| Central-West | ||

| Southeast | ||

| South |

Key Questions Answered in the Report

How large is the Brazil mining logistics market in 2026?

The Brazil mining logistics market stands at USD 8.66 billion in 2026 and is forecast to reach USD 11.33 billion by 2031 at a 5.53% CAGR.

What is driving growth in Brazil’s mining logistics space?

Growth is being supported by iron ore export volumes, concession renewals, mining-linked logistics investment, and rising needs in copper and other critical minerals.

Which service generates the most revenue in Brazil mining logistics?

Transportation led with 70.91% revenue share in 2025, supported mainly by rail-linked mine-to-port systems.

Which commodity creates the largest logistics demand in Brazil?

Iron ore remained the largest commodity segment with 52.75% share in 2025 because Brazil’s deepest logistics corridors were built around ore exports.

Which region is growing fastest for mining-related transport and handling?

The North is projected to grow the fastest at 6.09% CAGR through 2031, helped by Northern Arc ports and corridor diversification projects.

Why are value-added services gaining importance in Brazil?

They are expanding at 6.42% CAGR because miners increasingly need traceability, custody records, emissions data, and compliance support across logistics chains.

Page last updated on: