South Africa Mining Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.52 Billion |

| Market Size (2026) | USD 7.83 Billion |

| Market Size (2031) | USD 9.26 Billion |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

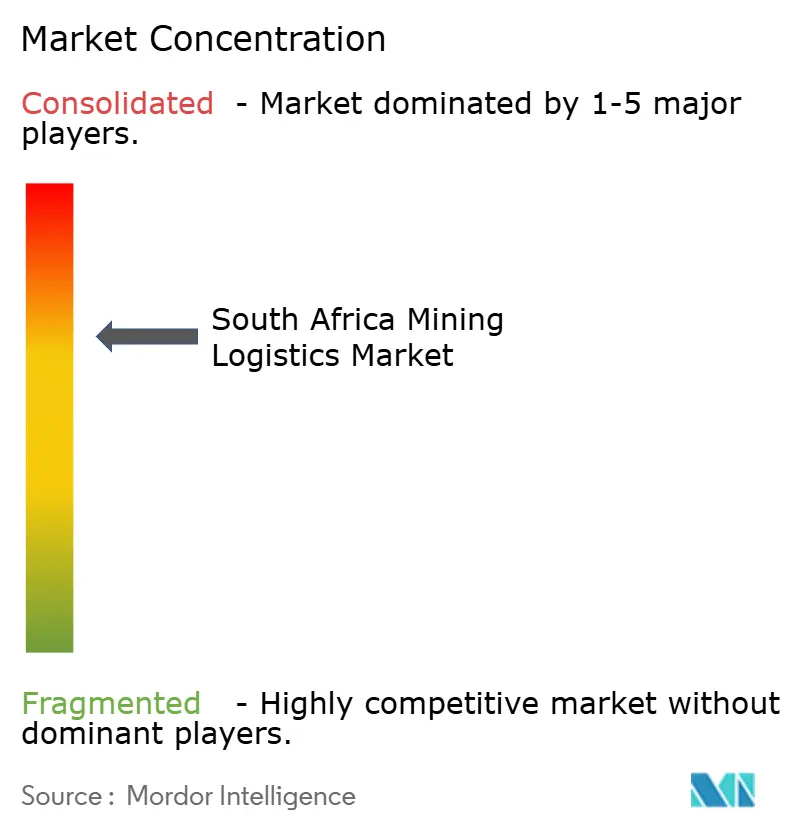

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Mining Logistics Market Analysis by Mordor Intelligence

The South Africa mining logistics market size was valued at USD 7.52 billion in 2025 and estimated to grow from USD 7.83 billion in 2026 to reach USD 9.26 billion by 2031, at a CAGR of 3.42% during the forecast period (2026-2031).

The South Africa mining logistics market is moving forward because the long-running rail monopoly that shaped freight economics is now being opened to private operators, which gives mineral exporters a more credible route back to rail-linked export infrastructure after extended underperformance. As of May 2026, all 11 private train operating companies have signed Rail Access Agreements with the Transnet Rail Infrastructure Manager, and the first wave of new capacity targets 24 million tons with scope to reach 52 million tons over 5 years. Private capital is also shifting from discussion to execution, with formal public-private processes underway for Richards Bay, Ngqura, and other mineral corridors that matter most for flows of coal, iron ore, manganese, and chrome. Operational recovery at the Richards Bay Coal Terminal, where exports rose to 57.7 million tons in 2025, shows that even limited rail and port improvements can lift mining throughput when train frequency improves. Growth remains constrained by theft, rolling stock shortages, weak slot reliability, port congestion, and stronger competition from Maputo, which continue to limit how much of the South African mining logistics market can convert resource potential into export volumes.

Key Report Takeaways

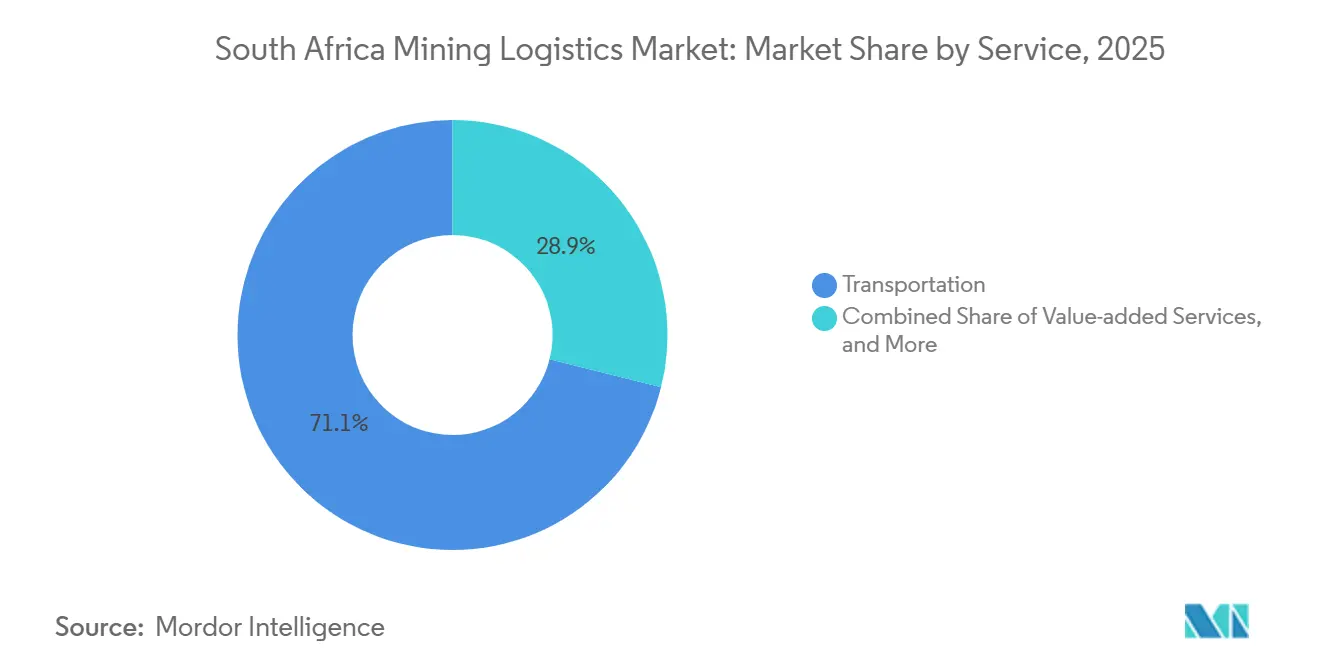

- By service, transportation held 71.09% of the South Africa mining logistics market share in 2025, while value-added services are forecast to expand at a 5.12% CAGR through 2031.

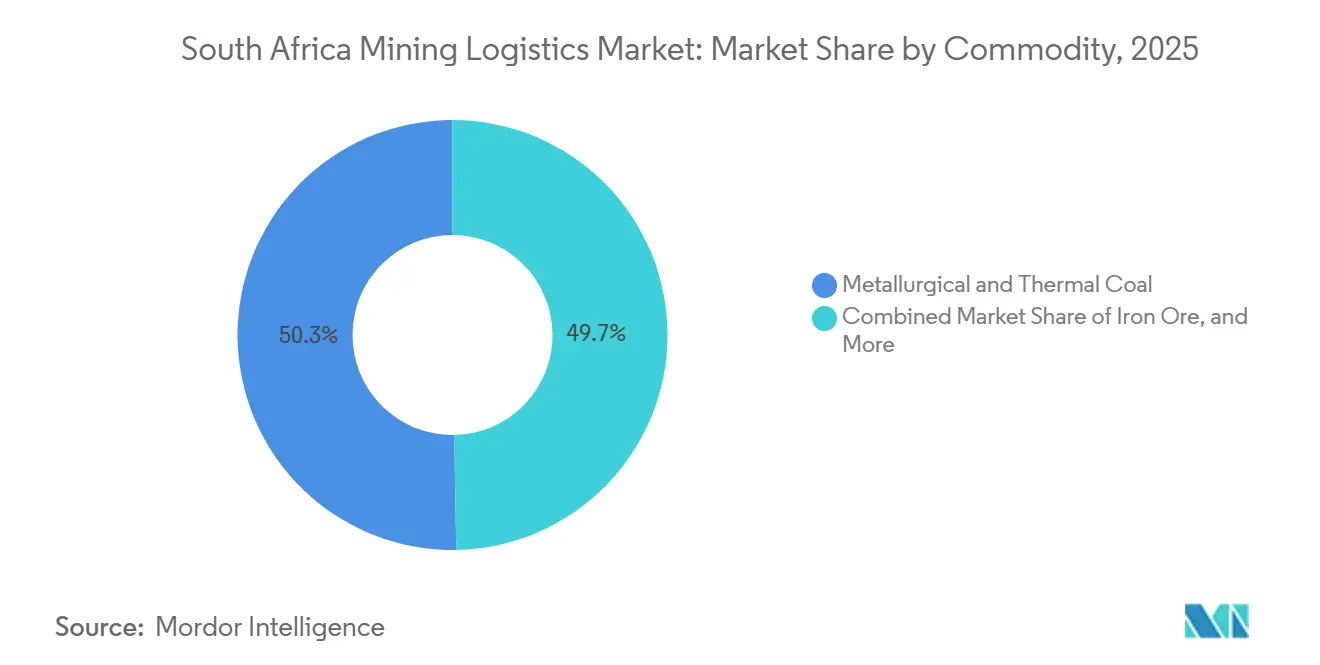

- By commodity, metallurgical and thermal coal held 50.28% of the South Africa mining logistics market share in 2025, while base metals (Cu, Zn, Ni) are forecast to expand at a 4.30% CAGR through 2031.

- By geography, Mpumalanga and Limpopo captured 42.03% share of the South Africa mining logistics market size in 2025, while Gauteng and Inland are expected to grow fastest at a 3.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Mining Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Open-Access Rail Reform And 11-Operator Market Entry | +0.8% | National, with early gains in Mpumalanga, Northern Cape, and Limpopo corridors | Short term (≤ 2 years) |

| PSP Capital For Mineral Corridors And Terminals | +0.6% | National, concentrated in Richards Bay, Saldanha Bay, and Ngqura | Medium term (2-4 years) |

| Mining Freight As South Africa's Densest Cargo Base | +0.5% | National, with strongest pull from Mpumalanga, Limpopo, and Gauteng and Inland | Long term (≥ 4 years) |

| Recovery In Bulk Export Railings And Coal Throughput | +0.7% | North Corridor and Iron Ore Corridor | Short term (≤ 2 years) |

| Rolling-Stock LeaseCo Lowers Private-Entry Capex | +0.4% | National, across multiple rail corridors | Medium term (2-4 years) |

| Dry-Port And Back-of-Port Routing Flexibility | +0.3% | Gauteng, Komatipoort, and KwaZulu-Natal | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Open-Access Rail Reform and 11-Operator Market Entry

Open-access rail reform is the most important structural change shaping the South Africa mining logistics market in 2026 because it breaks the state-only model that had limited corridor choice for mineral exporters[1]“Critical Minerals and Metals Strategy South Africa 2025,” South African Government, gov.za. All 11 private TOCs, including Grindrod, Menar Ports & Rail, Traxtion, ARC South Africa, and Barberry, completed Rail Access Agreements with TRIM in May 2026, following their selection from 25 applicants in August 2025. TRIM expects the first wave of entrants to add 24 million tons of freight capacity, with the platform designed to scale that figure to 52 million tons over 5 years against Transnet Freight Rail's 160 million tons in the 2024/25 financial year. The route mix matters because 15 of the 41 allocated routes sit on the North Corridor, which means coal and chrome traffic remains at the center of early private rail economics. That concentration makes the early reform case far more about bulk minerals than general freight and places Mpumalanga, Limpopo, and the Northern Cape at the front of the operating test period. Some operators want to start before the end of 2026, but TRIM expects most services to become operational during 2027, so the South Africa mining logistics market is pricing in reform before full delivery is visible on the ground.

PSP Capital For Mineral Corridors and Terminals

Private sector participation is moving from policy language to deal structures, which makes it one of the clearest growth channels in the South Africa mining logistics market. The Department of Transport's March 2025 request for information focused on coal and chrome to Richards Bay, iron ore and manganese to Saldanha Bay, and container flows to Durban, which signaled that corridor reform would be tied to bankable freight demand. Transnet's capital plan reached ZAR 127 billion (USD 6.9 billion) over 5 years in late 2025, making outside funding essential rather than optional. The Richards Bay Dry Bulk Terminal process moved further in 2026 after Transnet set a minimum investment threshold of ZAR 5.2 billion (USD 281 million) for a 49% partner stake in a terminal that handles 16.7 million tons and can expand to 26.9 million tons. The proposed Ngqura manganese terminal adds another layer, as manganese producers, led by African Rainbow Minerals, are now seeking a direct role in export infrastructure rather than relying solely on state-run logistics. That shift reduces the historic separation between mining production and transport control, and it should favor providers that can align capital, tonnage commitments, and corridor access within one operating model[2]“Transport on Potential Private Sector Participation in Rail and Port Projects,” South African Government, gov.za.

Recovery in Bulk Export Railings and Coal Throughput

Recovery in bulk railings and coal throughput is giving the South Africa mining logistics market near-term support because it shows that freight volumes can respond quickly when operating discipline improves. RBCT exported 57.7 million tons of coal in 2025, up 11% from the prior year, and daily offloads rose from 17 trains in 2024 to 20 trains in 2025. RBCT management is targeting 60 million tons in 2026, and January 2026 running rates were already consistent with an annualized pace of 62 million tons. These gains came mostly from better signal maintenance, locomotive reactivation, and tighter cargo coordination rather than from new network capacity, which means the improvement is operational rather than structural. That also leaves the corridor exposed, because Transnet told Parliament in April 2026 that 377 locomotives had been out of service at the peak of the disruption while spare parts disputes were still being resolved. South Africa's target of 250 million tons of rail freight by 2030 still depends on both private TOC volumes and continued Transnet recovery, so a single recovery channel will not be enough to sustain the current momentum.

Mining Freight as South Africa's Densest Cargo Base

Mining freight remains the densest cargo base in the South Africa mining logistics market, and that density is what makes long-haul corridor investment more financeable than many other freight categories. Private operators and infrastructure investors keep returning to mining corridors because bulk minerals provide repeatable volumes, longer haul distances, and clearer anchor contracts than mixed freight. Mpumalanga produced 76% of South Africa's coal output and held 50% of its coal reserves, which keeps the North Corridor commercially relevant even when utilization stays below design levels. South Africa's manganese exports reached 26.2 million tons in 2025 after a prior high of 22.3 million tons in 2024, which shows that manganese and chrome logistics remain volume-rich even when rail allocation is tight. South Africa's selection as one of the 11 train operators also shows that international investors are willing to enter once corridor rules and access frameworks become clearer. Logistics providers that secure anchor tonnage agreements with mining houses in 2026 should enter the next reform stage with stronger corridor leverage than late entrants because freight density compounds quickly once slot access and rolling stock are matched.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Theft, Vandalism, Rolling-Stock Shortages, and Aging Assets | -0.8% | National, with greatest pressure on the North Corridor and chrome routes | Short term (≤ 2 years) |

| Port-Side Bottlenecks Offset Rail Gains | -0.5% | KwaZulu-Natal, Eastern Cape, and Western Cape | Medium term (2-4 years) |

| Non-Bankable Slot Reliability and Access-Agreement Terms | -0.4% | National, concentrated on North and Iron Ore corridors | Short term (≤ 2 years) |

| Competing Regional Corridors Erode Gateway Leverage | -0.4% | Mpumalanga, Limpopo, and Northern Cape | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Theft, Vandalism, Rolling-Stock Shortages, and Aging Assets

Theft, vandalism, rolling-stock shortages, and aging assets remain the deepest operational restraints in the South Africa mining logistics market because they reduce reliability at the exact point where reform needs bankable service levels. Transnet said in October 2025 that it was spending ZAR 4 billion (USD 216 million) a year on private security, yet still lost 4.5 million tons to theft-related incidents and another 7 million tons to derailments, equal to ZAR 9 billion (USD 486 million) in annual economic losses. Security incidents fell 23% in the 2024/25 financial year to 6,345 from 8,234, but revenue losses still reached ZAR 1.59 billion (USD 86 million), indicating that improvements in case numbers have not yet restored commercial confidence. The locomotive shortage deepened the problem because Parliament heard in April 2026 that 377 locomotives had been out of service during peak disruption, much of it linked to the disputed ZAR 54.4 billion (USD 2.9 billion) CRRC procurement and to delayed spare-parts releases. Transnet still needs ZAR 14 billion (USD 757 million) a year to restore infrastructure, which is far above its current funding room and explains why LeaseCo and wider PSP mechanisms have become operational necessities. Until those asset, funding, and security gaps narrow together, new entrants will continue to face higher insurance, buffer stock, and fleet planning costs than the reform narrative alone would suggest.

Port-Side Bottlenecks Offset Rail Gains

Port-side bottlenecks continue to offset rail gains in the South Africa mining logistics market, especially as corridor recovery reaches Durban and then loses momentum within the port precinct. Durban ranked near the bottom of the World Bank's 2024 Container Port Performance Index, which confirmed that vessel delays, terminal congestion, and landside access problems remain severe. Even where rail performance improves, dwell times, crane outages, and road congestion on Bayhead Road can absorb much of the benefit before mineral cargo reaches the vessel window. The 25-year ICTSI concession for Durban Container Terminal Pier 2, backed by ZAR 11 billion (USD 594 million), was signed in January 2026 and is now moving through its operating transition stage. That investment matters, but infrastructure observers also note that the system problem is day-to-day volatility rather than a simple lack of rated crane capacity, so execution discipline matters as much as capex. Cape Town's sharp 2024 improvement proves that targeted interventions can change South African port performance, but Richards Bay and Saldanha still need sustained upstream rail reliability to translate port capability into mining throughput.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Dominance Masks A Modal-Shift Opportunity

Transportation accounted for 71.09% of South Africa mining logistics market share in 2025, which shows that corridor capacity still decides whether miners can move tonnage at an export scale. Road haulage remained the preferred option for chrome, manganese, and shorter-haul coal flows, and Reinhardt Transport Group said it moves more than 18 million tons of bulk mining commodities annually with a fleet of more than 1,000 specialized vehicles. Rail remained concentrated on the coal line to Richards Bay and the iron ore line to Saldanha Bay, so the modal mix stayed skewed even after reform began. Sea freight handled the export leg for bulk minerals, while air freight stayed limited to precious metal samples and specialized mining equipment components where speed and value outweighed tonnage.

Value-added services are the fastest-growing sub-segment, with a 5.12% CAGR through 2031, as mining houses demand coordinated pit-to-port planning, improved tracking visibility, and storage solutions that can absorb rail disruptions. Warehousing and inventory management is becoming a margin-protection tool because closed storage near export nodes lets producers hold cargo when train schedules shift without losing vessel commitments. Reinhardt's Richards Bay warehousing footprint and DP World's Komatipoort dry port both show how back-of-port capacity can protect exporters when the North Corridor is constrained. The NT55 Gauteng dry port project, which is planned to start construction in 2027, will add a rail-linked inland consolidation option that supports the South Africa mining logistics industry beyond simple origin-to-port trucking. Traxtion's ZAR 3.4 billion (USD 184 million), commitment to 46 locomotives and around 920 wagons is the clearest sign that private operators expect freight to shift from road to rail as open access becomes operational. That shift should favor providers that can combine transport, storage, compliance, and coordination inside one contract, while smaller single-service operators may find the South Africa mining logistics industry harder to serve profitably.

By Commodity: Coal's Structural Weight, Base Metals' Growth Momentum

Metallurgical and thermal coal accounted for 50.28% share of the South Africa mining logistics market size in 2025, which kept the North Corridor and the Richards Bay coal system at the center of freight economics. RBCT exported 57.7 million tons in 2025 against an installed capacity of 91 million tons, so the corridor still carries clear upside if rail consistency improves. Menar Ports & Rail's 2026 establishment turned a mining group into a logistics operator, showing how commodity producers are moving closer to direct control of transport. Orion Minerals' Prieska Copper-Zinc project advanced that case in May 2026 after securing ZAR 280 million (USD 10.9 million) in South African institutional funding for site infrastructure and development[3]"Richards Bay Coal Terminal Exports Rise Over 10% in 2025 in Latest Sign of Transnet Reboot." Daily Maverick, dailymaverick.co.

Base metals, including copper, zinc, and nickel, are the fastest-growing commodity segment at a 4.3% CAGR through 2031, supported by the national critical minerals strategy and active project development. Iron ore on the 861-kilometer Sishen-Saldanha corridor remained below nameplate throughput in 2025 even though Saldanha Bay was running at 96% berth utilization, which confirms that rail performance is the primary limiting factor. Industry users have therefore argued for an integrated rail concession structure on the iron ore line, with Transnet keeping asset ownership while private operators bring performance discipline and investment. Gold logistics still move smaller tonnages, but they sustain premium handling demand because bonded storage, secure transport, and controlled chains of custody remain essential. South Africa's 26.2 million tons of manganese exports in 2025 show how large the bulk opportunity remains, yet the continued use of road for a large share of those volumes underlines the cost of limited dedicated export infrastructure. Providers that align rolling stock, route access, and terminal strategy with each commodity's corridor timetable should capture more of the South Africa mining logistics market than firms that approach mineral freight as a generic cargo pool.

Geography Analysis

Mpumalanga and Limpopo held 42.03% of the South Africa mining logistics market share in 2025, and that lead reflects freight density that remains difficult for other regions to match. The region combines coal from Mpumalanga with chrome and ferromanganese flows from Limpopo, so it attracts road hauliers, private rail entrants, and terminal investors at the same time. The Maputo Corridor recorded 8% growth in both road and rail freight volumes between 2024 and 2025, which shows that exporters are already using cross-border optionality when South African corridors become constrained. The Port of Maputo handled a record 32 million tons in 2025 and is undergoing a USD 500 million expansion, targeted for completion in the first quarter of 2027, which intensifies competition for coal, chrome, and magnetite flows. CFM's second-phase upgrade of the Ressano Garcia line, set to begin in June 2026 and lift corridor capacity to 19 million tons a year, reinforces the commercial logic of dual-corridor strategies for inland miners.

KwaZulu-Natal and the Western Cape now show the strongest near-term port reform contrast inside the South Africa mining logistics market because one gateway is still struggling with volatility while the other has already started to recover its standing. The ICTSI concession at Durban Container Terminal Pier 2 is the biggest governance shift in South African ports, and Transnet also said vessel arrivals at national ports rose 9% in the 2025/26 financial year even though freight forwarders warned that the rebound starts from a low base. Cape Town's 240-point improvement in the 2024 CPPI benefits Northern Cape exporters and proves that disciplined intervention can change performance within a short time frame. On the ore side, Transnet's ZAR 3.4 billion (USD 184 million), infrastructure support for the Sishen-Saldanha corridor and Saldanha Bay's 96% berth utilization in 2025 show that the port is not the main bottleneck, because the rail system still limits delivered tonnage.

Gauteng and Inland is projected to grow at a 3.97% CAGR through 2031, which marks a structural reappraisal of the province inside the South Africa mining logistics market. The NT55 inland hub and DHL Supply Chain's ZAR 220 million (USD 12 million), multi-user distribution center investment in Johannesburg point to a model where Gauteng serves as a contract logistics and consolidation base rather than just a pass-through zone. Gauteng's concentration of mining head offices, engineering contractors, equipment importers, and warehousing demand gives it a resilience that pure extraction regions do not always have. The Lobito Corridor's planned 30% to 40% cost advantage by 2030 is therefore a direct long-term challenge, because inland South African logistics must offer better service and routing value if they want to retain Copperbelt-linked flows[4]"Lobito Corridor Further Weakens South Africa's Logistics Value." Engineering News, engineeringnews.co.za.

Competitive Landscape

The South Africa mining logistics market is moderately concentrated at the top, with Transnet Freight Rail still holding the largest structural position in rail, yet the broader field remains fragmented across road carriers, warehouse operators, forwarding groups, and terminal service providers. The 11-operator rail reform is the biggest competitive reset in a generation, and Grindrod, Traxtion, and Menar Ports & Rail are the clearest private challengers because they already have access agreements, capital programs, and corridor plans in motion. Traxtion's ZAR 3.4 billion (USD 184 million) investment in locomotives and wagons is the largest private freight rail commitment yet announced in South Africa, which gives it early scale before many rivals have secured operating depth. Grindrod's link between Mpumalanga mining flows, its wholly owned Matola terminal, which handled a record 9.9 million tons in 2025, and its planned Richards Bay container-handling facility for 2028 shows how vertical integration is becoming a defensible strategy. Global logistics groups are also tightening service standards on multimodal mining routes, which raises competitive pressure on domestic operators that still depend on corridor workarounds rather than stable execution.

White-space opportunities are strongest in back-of-port logistics, rolling stock leasing, and digital mine-to-port tracking because those are the points where volume losses from theft, derailments, and schedule breaks are most visible. The LeaseCo process, with shortlisted bidders in place during 2026, could commercialize 600 locomotives and 21,000 wagons through a joint venture structure that lowers entry costs for private rail operators. Bidvest's freight division is already active across South Africa's major ports and remains engaged in port PSP discussions, which keeps it relevant even as rail competition opens up. DP World's mix of Imperial Logistics capabilities, the Komatipoort dry port, and Maputo corridor operations gives it one of the broadest inland-to-export positions in the current field.

The Lobito Corridor is the most credible external disruptor because its completion by 2030 could lower transport costs for DRC and Zambian copper and cobalt by 30% to 40% compared with South African routes. That risk is most serious for operators whose models rely on moving regional minerals through South African gateways without enough service differentiation. Companies that build rail-linked volume positions before 2027 should be better placed to absorb that pricing pressure because they can spread fixed costs across denser corridors and stronger customer contracts. In that setting, the South Africa mining logistics market should reward corridor depth, terminal access, and asset readiness more than simple geographic coverage.

South Africa Mining Logistics Industry Leaders

-

DP World (Including Imperial Pty Ltd.)

-

DSV A/S (Including DB Schenker)

-

UNITRANS

-

Grindrod Limited

-

TransNet Rail

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Grindrod confirmed its signed Rail Access Agreement with TRIM for the Northeast Corridor, targeting initial volumes of 288,000 tonnes in year one using 2 allocated slots, with operations primarily carrying coal to its Matola terminal in Mozambique. Full-scale operations are expected to ramp significantly from 2029, per Engineering News.

- May 2026: Menar Ports and Rail confirmed readiness to progress its TRIM partnership following an 8.69-million-tonne rail allocation, with procurement processes underway for wagons and locomotives. The company plans to transport coal, anthracite, manganese, and ferromanganese, per Mining Weekly.

- April 2026: Transnet set a minimum investment threshold of ZAR 5.2 billion (USD 281 million) for a 49% private partner stake in the Richards Bay Dry Bulk Terminal, with the PSP process expected to culminate in a joint special-purpose vehicle. The terminal currently handles 16.7 million tons annually, with expansion capacity to 26.9 million tons, per Business Day.

- April 2026: DHL Supply Chain announced a ZAR 220 million (USD 12 million) investment in a new multi-user distribution center in Johannesburg, with construction starting in July 2026 and operations expected by July 2027, reinforcing its commitment to South Africa's cross-border logistics infrastructure.

South Africa Mining Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea and Inland Waterways | |

| Air | |

| Warehousing and Inventory Management | |

| Value-Added Services |

| Iron Ore |

| Metallurgical and Thermal Coal |

| Base Metals (Cu, Zn, Ni) |

| Gold |

| Other Minerals/Metals |

| Gauteng and Inland |

| Western Cape |

| KwaZulu-Natal |

| Eastern and Northern Minor Region |

| Mpumalanga and Limpopo |

| Rest of South Africa |

| By Service | Transportation | Road |

| Rail | ||

| Sea and Inland Waterways | ||

| Air | ||

| Warehousing and Inventory Management | ||

| Value-Added Services | ||

| By Commodity | Iron Ore | |

| Metallurgical and Thermal Coal | ||

| Base Metals (Cu, Zn, Ni) | ||

| Gold | ||

| Other Minerals/Metals | ||

| By Region | Gauteng and Inland | |

| Western Cape | ||

| KwaZulu-Natal | ||

| Eastern and Northern Minor Region | ||

| Mpumalanga and Limpopo | ||

| Rest of South Africa |

Key Questions Answered in the Report

What is the size outlook for South Africa mining logistics through 2031?

The South Africa mining logistics market was valued at USD 7.52 billion in 2025, stands at USD 7.83 billion in 2026, and is forecast to reach USD 9.26 billion by 2031 at a 3.42% CAGR.

What is driving growth in mining freight across South Africa?

Rail open access, private sector participation in corridors and terminals, coal throughput recovery at Richards Bay, and rising demand for integrated pit-to-port services are the main growth factors.

Which service segment leads mining logistics demand in South Africa?

Transportation is the leading service segment, with 71.09% share in 2025, because rail and road capacity still determine export competitiveness for mineral cargo.

Which commodity has the largest logistics requirement in South Africa?

Metallurgical and thermal coal leads with 50.28% share in 2025, while base metals are growing faster at a 4.30% CAGR through 2031.

Which region is growing fastest for mining logistics activity?

Gauteng and Inland is the fastest-growing regional segment with a 3.97% CAGR to 2031, supported by dry port plans, warehousing expansion, and rising contract logistics activity.

What is the biggest risk to execution in South Africa mining logistics?

Theft, vandalism, locomotive shortages, and port congestion remain the biggest risks because they weaken service reliability even when corridor reform and private entry are moving forward.

Page last updated on: