Processed and Frozen Vegetables Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 94.82 Billion |

| Market Size (2031) | USD 116.20 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Processed and Frozen Vegetables Market Analysis by Mordor Intelligence

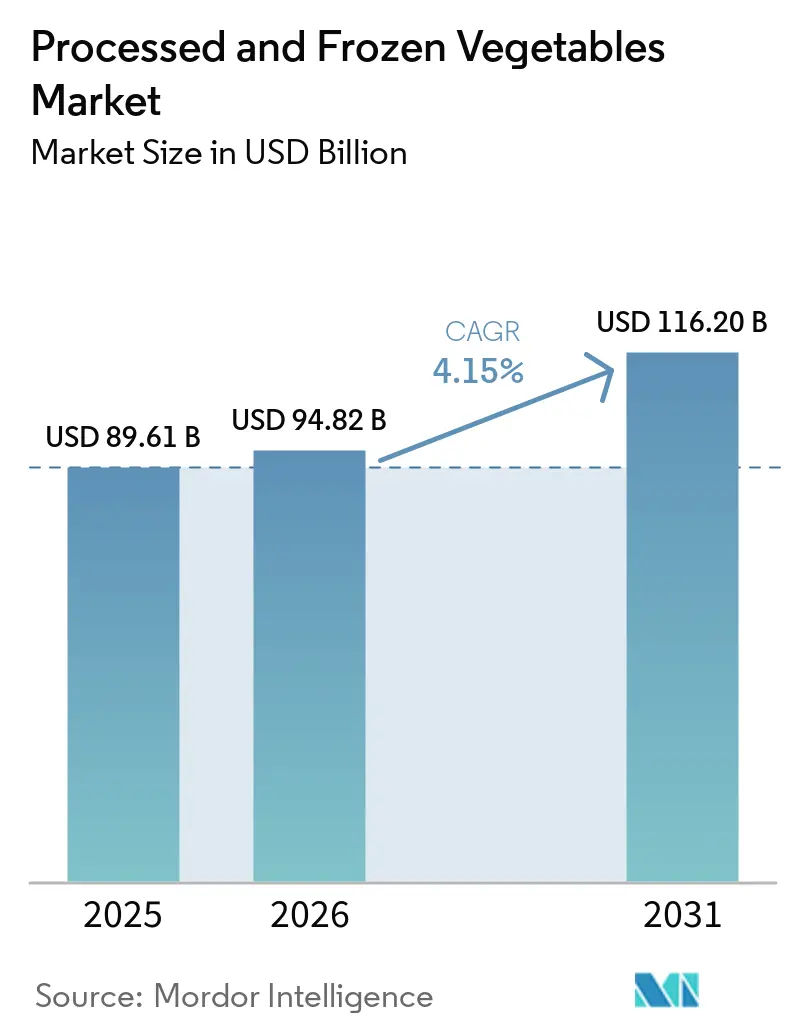

The processed and frozen vegetables market size reached USD 89.6 billion in 2025 and is forecast to reach USD 116.2 billion by 2031, growing at a CAGR of 4.1% from 2026 to 2031. The processed and frozen vegetables market is expanding because urban households are relying more on pre-portioned and freezer-ready formats that reduce shopping time and meal preparation effort. The processed and frozen vegetables market is also benefiting from advances in individually quick frozen processing, which have improved texture, nutrient retention, and product quality, allowing suppliers to compete on health, convenience, and value at the same time. Competitive conditions remain firm as large branded suppliers defend shelf space while private-label lines expand across major grocery chains, which is pushing investment toward premium, sauce-based, and globally inspired offerings. The processed and frozen vegetables market still faces pressure from rising refrigeration and energy costs, especially in Europe, where cold-chain expenses are rising faster than selling prices that many mid-tier producers can absorb. The same market is also being supported by foodservice demand, as restaurants, institutional kitchens, and caterers increasingly choose washed, cut, and portioned frozen vegetables to reduce labor needs, improve consistency, and manage total service costs more effectively.

Key Report Takeaways

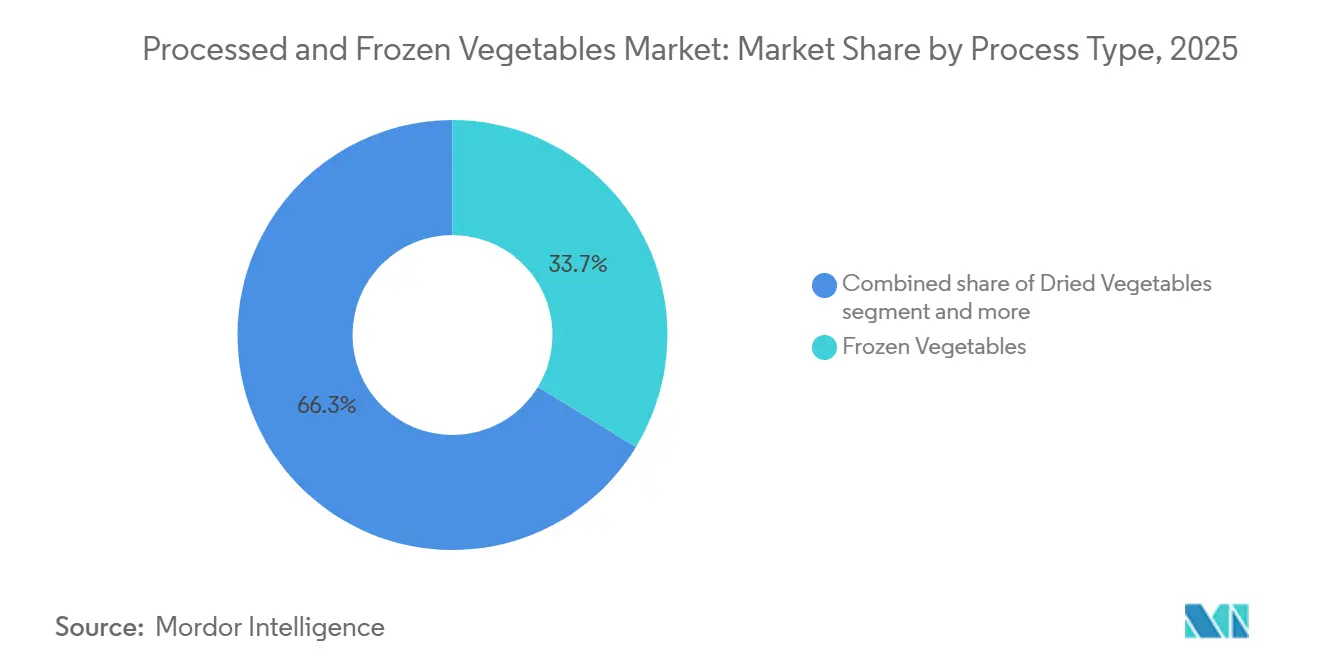

- By process type, frozen vegetables accounted for the largest share of the processed vegetables market, at 33.7% in 2025, while dried vegetables are projected to grow at the fastest CAGR of 6.06% during 2026-2031.

- By product type, peas accounted for the largest share of the processed vegetables market, at 33.6% in 2025, while broccoli is projected to grow at the fastest CAGR of 6.11% during 2026-2031.

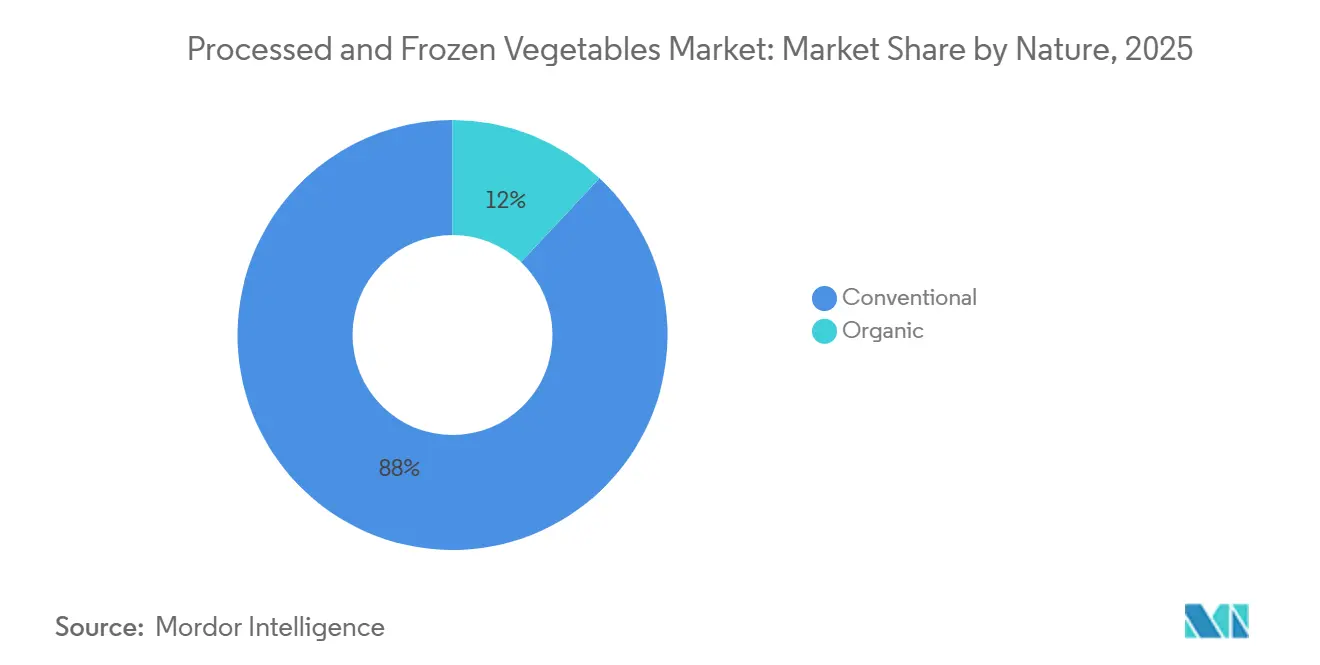

- By nature, conventional products retained 88.0% share of the processed vegetables market in 2025, whereas organic products are forecast to expand at a 7.03% CAGR through 2031.

- By distribution channel, retail accounted for the largest share of the processed vegetables market, at 55.1% in 2025, while foodservice is projected to grow at the fastest CAGR of 6.51% during 2026-2031.

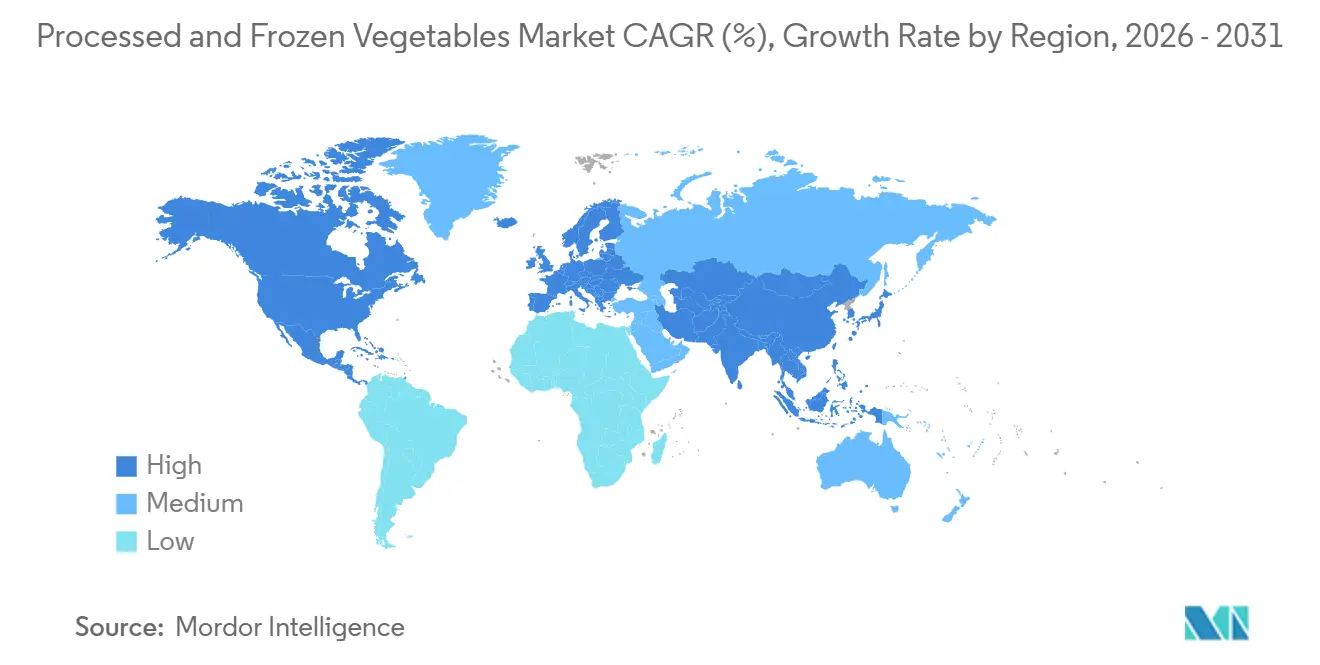

- By geography, Europe accounted for the largest share of the processed vegetables market, at 36.4% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 6.98% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Processed and Frozen Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Convenient and Ready-to-Cook Meals | +1.0% | Global, concentrated in North America and Europe | Medium term (2–4 years) |

| Expansion of Cold Chain and Frozen Retail Infrastructure | +0.9% | The Asia-Pacific core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Growth in Plant-Based and Flexitarian Eating Patterns | +0.7% | Global, with North America and Europe as early adopters | Medium term (2–4 years) |

| Year-Round Availability Versus Seasonal Supply Volatility | +0.6% | Global | Long term (≥ 4 years) |

| Retail Multipack Innovation and Meal-Solution Bundling | +0.5% | North America and Europe, spill-over to the Asia-Pacific | Short term (≤ 2 years) |

| Foodservice Menu Standardization and Prep-Labor Reduction | +0.5% | Global, concentrated in North America, Europe and the Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient and ready-to-cook meals

In developed markets, convenience has shifted from being a secondary consideration to the primary driver for the surge in frozen vegetable sales. According to Conagra Brands' 2025 Future of Frozen Foods report, premium frozen vegetable side dishes, like butter-sauced corn, cheesy broccoli florets, and globally-inspired medleys, saw an 11% volume increase[1]Source: Conagra Brands, “Future of Frozen Foods 2025,” Conagra Brands, conagrabrands.com. Overall, premium frozen sides experienced a 3% growth during the same timeframe. This trend indicates a market evolution, moving away from basic frozen peas and beans to meal components that rival restaurant-quality sides, leading to a noticeable price-tier expansion in the category. Foodservice operators are capitalizing on this trend: using pre-portioned frozen ingredients not only cuts down kitchen prep time but also standardizes plate costs. This becomes increasingly vital as minimum wage standards rise in the US and Western European foodservice sectors. Manufacturers at the forefront of sauce innovation and global flavor profiles, be it Mediterranean blends, Asian stir-fry medleys, or Latin-inspired mixes, stand to gain significantly from this premiumization trend. Supermarket chains are responding by allocating more shelf space to these higher-margin, sauce-bundled SKUs, ensuring they drive repeat customer visits.

Expansion of cold chain and frozen retail infrastructure

Emerging markets' cold-chain expansion is not just boosting frozen vegetable consumption; it's introducing entirely new consumer groups to the frozen category. In India's Union Budget for 2025-26, the Ministry of Food Processing Industries received an allocation of INR 4,364 crore (around USD 505.70 million)[2]Source: Ministry of Food Processing Industries, “Union Budget 2025-26,” Ministry of Food Processing Industries, mofpi.gov.in. This includes direct backing for the Integrated Cold Chain and Value Addition Infrastructure scheme, part of the Pradhan Mantri Kisan SAMPADA Yojana. Such financial moves are streamlining the journey from farm to freezer and minimizing quality discrepancies. This allows Indian processors to consistently meet export-grade standards for year-round contracts with global buyers. Meanwhile, on the supply front, Greenyard's EUR 50 million expansion of its IQF capacity in Belgium, coupled with a EUR 260 million alliance with Eureden in France, is reshaping the landscape. This alliance is consolidating a Brittany-origin frozen vegetable entity across four production sites, showcasing how European processors are ramping up IQF throughput and consolidating their supply base to cater to rising retail demand. Looking ahead, the supply landscape is set to evolve: the APAC region is shifting from being primarily export-focused to a market that both supplies and consumes, while European expansions are elevating IQF quality standards, positioning them in premium tiers that previously lacked a frozen counterpart.

Growth in plant-based and flexitarian eating patterns

Flexitarian eating, characterized by a regular yet non-exclusive reduction in animal protein intake, stands out as the most commercially significant dietary trend for frozen vegetable processors. In 2025, the Agriculture and Horticulture Development Board (AHDB) highlighted a notable price disparity: meals sans meat averaged GBP 1.57 per serving, while their meat-laden counterparts were priced at GBP 2.86. This 45% cost saving renders vegetable-centric meals not just an ideological choice but a financially savvy one for budget-conscious households. Such economic reasoning is broadening the appeal of flexitarianism, extending its reach from health-focused early adopters to mainstream households managing their budgets in the UK and Northern Europe. This shift is expanding the market for frozen vegetables. Broccoli, spinach, and mixed vegetable blends are reaping the rewards; their adaptability in stir-fries, pasta dishes, and curries resonates with the globally-inspired flexitarian meals. An AHDB study revealed that these meal choices are increasingly influenced by convenience over ideology. Thanks to innovations in IQF processing, retailers can now offer premium-quality frozen broccoli, boasting textures and nutrient profiles once thought exclusive to fresh produce. This advancement bolsters broccoli's status as the fastest-growing product in the frozen aisle.

Year-round availability versus seasonal supply volatility

Processors with geographically diversified sourcing networks gain a competitive edge due to seasonal supply volatility in key frozen vegetable crops like peas, broccoli, and green beans. An adverse weather event during harvest can drastically cut yields in primary growing regions. This leads to spikes in raw material costs, which vertically integrated processors can absorb more easily than those reliant on spot-market purchases. Frozen processing allows for a decoupling of consumer demand timing from agricultural seasonality. This advantage is becoming increasingly valuable as climate variability heightens harvest unpredictability in Northern Europe and North America. Processors with access to counter-seasonal growing regions in the Southern Hemisphere, such as Chile, Argentina, and South Africa, can stabilize raw material costs. They can also uphold 52-week supply contracts, a capability now deemed essential by major retailers in their frozen vegetable procurement tenders. A 2024 life cycle assessment study in MDPI Sustainability highlighted that frozen vegetables can be stored for up to 3.5 times longer than fresh produce without significant quality loss. This finding underscores the value of frozen vegetables as reliable supply tools for large retail and foodservice buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-Intensive Freezing and Refrigeration Cost Inflation | -1.5% | Global, most acute in Europe and North America | Short term (≤ 2 years) |

| Temperature Excursions and Quality Degradation Risk | -0.8% | The Asia-Pacific and MEA, where cold-chain infrastructure gaps persist | Medium term (2–4 years) |

| Consumer Bias Toward Fresh Produce in Premium Segments | -0.7% | Developed markets, Western Europe and North America | Medium term (2–4 years) |

| Packaging Sustainability Pressure on Cold-Chain Formats | -0.5% | Global, led by EU regulatory influence | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-intensive freezing and refrigeration cost inflation

The European energy price surge has disproportionately impacted production costs in processed vegetable supply chains, particularly in refrigeration and freezing. A 2024 study in MDPI Sustainability highlighted that storage costs for frozen vegetables are about 3.8 times higher than their fresh counterparts on a per-kilogram basis. This disparity is largely due to the stringent temperature maintenance and extended storage durations required for frozen goods. Mid-tier processors, often relying on older refrigeration systems, feel the brunt of these rising costs. Upgrading for energy efficiency demands significant capital, a challenge for smaller operators in today's high-interest climate. In response, industry-led initiatives like the Move to -15°C coalition, championed by Birds Eye (under Nomad Foods) and Sunswap's electric transport refrigeration, aim for a 20% energy cut in frozen food transport. Notably, Birds Eye's solar-powered trailer fleet boasts an impressive annual reduction of around 24 tonnes of CO₂ emissions. Additionally, the EU's Extended Producer Responsibility mandates on packaging further strain manufacturers. They are now tasked with creating mono-material cold-chain films that simultaneously meet recyclability and barrier-property standards.

Consumer bias toward fresh produce in premium segments

Higher-income consumers' preference for fresh vegetables in premium retail settings is limiting the growth of the frozen category. In premium grocery formats across Western Europe and North America, like organic specialty stores, upscale supermarkets, and farm-to-table concepts, fresh produce does more than just provide nutrition. It signals care in preparation and attentiveness to the seasons, a nuance that frozen options struggle to convey. According to the Organic Trade Association's 2026 Organic Market Report, while organic frozen fruits and vegetables saw a 3.0% growth in 2025, sales of organic frozen prepared foods dropped by 3.4%[3]Source: Organic Trade Association, “Organic Market Report 2026,” Organic Trade Association, ota.com. This shift indicates that even health-conscious shoppers are prioritizing cost over convenience. Furthermore, organic frozen foods made up only 5.2% of the total frozen market in 2025, highlighting that while the organic frozen segment is growing, it's lagging behind the expansion of conventional frozen options. This trend serves as a cautionary note for brands banking solely on organic premiumization for sustained growth. To maintain price premiums in the competitive landscape of conventional frozen and fresh organic alternatives, manufacturers aiming for a premium frozen positioning need to complement organic certification with clear differentiators. These could include provenance labeling, verified regenerative sourcing, or claims of unique crop varieties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Type: Dried Formats Gain Ground as Cold-Chain Costs Escalate

In 2025, frozen vegetables captured a 33.71% market share, driven by advancements in IQF technology and a robust retail cold-chain infrastructure in Europe and North America. IQF's ability to flash-freeze and preserve vitamins and cellular texture at harvest differentiates it from canning and drying, particularly in premium supermarkets where frozen broccoli and spinach are marketed as nutritional equivalents to fresh produce. Canned vegetables maintain steady demand in emerging markets and institutional purchases, especially in regions like sub-Saharan Africa, South Asia, and parts of Southeast Asia, where cold-chain access is limited. Their affordability, 20–30% cheaper than frozen options, sustains demand among price-sensitive consumers.

Dried vegetables are projected to grow at a 6.06% CAGR from 2026 to 2031, driven by demand from packaged-meal manufacturers and out-of-home catering services seeking shelf-stable ingredients. Manufacturers are investing in advanced dehydration methods like freeze-drying, vacuum drying, and spray drying, which improve nutrient retention compared to traditional hot-air drying. Freeze-drying, in particular, preserves cellular structure, color, and phytochemical content, commanding higher price premiums in premium ingredient markets. This shift in investment toward dried vegetables is reducing frozen capacity expansion at mid-tier European processors facing high refrigeration energy costs. If sustained, this trend could tighten IQF supply and support frozen vegetable prices in European retail. Additionally, the "Other Process Type" segment, including minimally processed and sous-vide methods, is gaining traction among premium foodservice operators and meal-kit providers targeting restaurant-quality offerings.

By Product Type: Peas Anchor Market Volumes as Broccoli Leads Premiumization

Distinct end-use occasions characterize the product mix, with spinach riding the wave of the plant-based protein trend. This versatile leafy green finds its way into smoothie packs, frozen curries, and pasta sauce blends. Broccoli, boasting a nutritional profile rich in vitamins C and K, dietary fiber, and phytochemicals, is the fastest-growing product type, projected to expand at a 6.11% CAGR from 2026 to 2031. Its growth is fueled by its alignment with flexitarian meal formats and its rising popularity in restaurant-style frozen preparations, such as roasted-style floret packs and multi-vegetable meal bases. Emerging product formats, like Conagra's Birds Eye Steamfresh Mediterranean and Tuscan-style blends, launched in early 2026, showcase broccoli paired with cauliflower, carrots, and leafy greens. These medleys aim to elevate frozen vegetables from mere side dishes to the centerpiece of dinner plates. Meanwhile, mushrooms and asparagus carve out a premium niche, gracing high-end supermarket shelves and restaurant menus, where their farmgate cost premiums find justification in retail price tiers absent in commodity markets.

In 2025, peas commanded a 33.62% share of the product type market. Their widespread appeal stems from commodity-scale production, deep retail penetration, and versatility across retail, foodservice, and industrial processing. As a testament to their significance, Mother Dairy's Safal brand in India, a pioneer of frozen peas since the 1990s, boasts a combined processing capacity of 17,000 MT per annum across its Delhi and Ranchi facilities, following a 2026 expansion. This underscores peas' role as the entry point for consumers venturing into the world of frozen vegetables, especially as cold-chain infrastructure expands into new regions. Meanwhile, premium retail is witnessing a surge in mixed vegetable blends. Curated "power blend" formulations are positioning frozen produce as functional food, appealing to health-conscious consumers who prioritize meal-planning simplicity without compromising on nutritional diversity.

By Nature: Organic Segment Outgrows Conventional Despite Sourcing Headwinds

Driven by retailer clean-label programs, health-conscious consumer demand, and growing institutional procurement of certified-organic frozen ingredients, the organic segment is set to outpace its counterparts, with a projected growth rate of 7.03% CAGR from 2026 to 2031. According to the Organic Trade Association's 2026 report, US organic food sales hit USD 70.1 billion in 2025, marking a 6.9% growth, notably double the 3.4% rise of the total food market. Within this, organic produce, encompassing vegetables, stood out as the leading category, raking in USD 22.7 billion. Stricter traceability mandates and an expanded scope under the EU Organic Regulation (EU 2018/848) have elevated supplier qualification hurdles. This shift predominantly benefits established certified processors, who have proactively invested in documentation and regenerative sourcing. Nomad Foods' 2025 Sustainability Report highlighted a 2.1% uptick from 2024, with 97% of its sourced vegetables, potatoes, and fresh herbs achieving silver or gold on the SAI Farm Sustainability Assessment, underscoring a growing alignment between sustainability credentials and major EU retail supplier standards.

In 2025, the conventional segment commanded a substantial 88.01% market share, underscoring its dominance in production scale and cost efficiency. Leveraging standardized procurement and high-volume processing, conventional frozen vegetables maintain price accessibility across retail tiers. While disruptions in supplies like peas or broccoli can be swiftly managed through a vast global sourcing network, the organic supply's geographical concentration poses challenges. This volume advantage not only facilitates ongoing investments in IQF equipment – a luxury for organic-only processors – but also highlights a processing-quality gap. Organic manufacturers now face the challenge of bridging this divide, necessitating strategic capital allocation in dedicated certified-organic processing lines.

By Distribution Channel: Retail Holds Volume Lead as Foodservice Accelerates

From 2026 to 2031, the foodservice channel is set to grow at a CAGR of 6.51%. Quick-service restaurant chains, contract caterers, and institutional buyers, spanning hospitals, schools, and corporate campuses, are leading the charge in bulk procurement of frozen vegetable inputs. In 2025, Conagra Brands rolled out over 50 new frozen food products across both retail and foodservice channels. These include globally-inspired Birds Eye Steamfresh medleys and sauce-bundled vegetable sides, tailored for foodservice. For institutional caterers, often constrained by tight staffing budgets, the appeal of pre-portioned frozen inputs is clear. By sidestepping the labor-intensive tasks of washing, peeling, and cutting, they can justify paying a premium for frozen over fresh. Meanwhile, both convenience stores and online retail are carving out a larger slice of the retail pie. E-commerce platforms, in particular, are offering customizable portion packs and subscription formats, filling a niche that physical shelves can't accommodate.

In 2025, retail held a dominant 55.13% share of distribution, primarily funneled through supermarkets and hypermarkets. These giants are heavily investing in expanding their frozen aisles, developing private-label programs, and optimizing their planograms. Online retail is emerging as the fastest-growing segment. Direct-to-consumer platforms are showcasing premium organic ranges, curated "power blend" formats, and specialty ethnic vegetable blends, items that mainstream supermarkets overlook. While convenience stores face challenges due to equipment and cold-storage limitations, urban formats in Japan, South Korea, and the UK are testing compact frozen sections. These sections cater to busy urban commuters, highlighting a distribution opportunity that hasn't yet seen significant investment from industry leaders.

Geography Analysis

In 2025, Europe held a 36.4% share of the processed and frozen vegetables market, making it the largest regional player. This dominance stems from Europe's mature cold chain infrastructure, high per-capita vegetable consumption, and strong processing hubs in France, Belgium, Germany, the Netherlands, Poland, and the United Kingdom. In February 2026, Greenyard finalized a strategic alliance with Eureden, approved by France’s competition authority. The merger created a frozen vegetable entity with pro forma revenue exceeding EUR 260 million across four Brittany sites and 900 employees. Birds Eye’s Steamfresh range in the UK achieved a 10% increase in category penetration over the 52 weeks to January 2026, highlighting that innovation outperforms pricing as a share driver in mature Western European markets. North America, the second-largest regional cluster, continues to see U.S. households adopt convenience-based vegetable formats, particularly premium options beyond staples like peas and corn.

Asia-Pacific is projected to grow at a 7.0% CAGR through 2031, making it the fastest-growing region in the processed and frozen vegetables market. Growth is driven by expanding cold-chain infrastructure, rising urban incomes, and stronger government support for food processing. India plays a key role, with the Union Budget 2025-26 allocating INR 4,364 crore (USD 505.7 million) to the Ministry of Food Processing Industries to enhance processing and cold-chain infrastructure. This investment improves supply consistency across agricultural zones and supports domestic sales and exports. China remains a leading exporter of frozen corn and carrots while expanding its domestic frozen retail market as urban consumers increasingly combine fresh and frozen purchases.

South America, the Middle East, and Africa are smaller segments of the processed and frozen vegetables market but hold strategic importance. Brazil and Argentina drive South American growth with expanding organized retail and improved cold-chain logistics, while also supporting counter-seasonal sourcing for Northern Hemisphere processors. Colombia, Peru, and Chile, though early-stage markets, benefit from urbanization and proximity to vegetable-growing zones that support regional processing. In the Middle East and Africa, the UAE, Saudi Arabia, and Morocco show strong import demand due to hospitality and foodservice needs for consistent quality and year-round volume. Nigeria and South Africa are building a more visible frozen retail presence, though canned and dried vegetables still dominate much of sub-Saharan Africa, with frozen penetration concentrated in urban areas with reliable refrigeration.

Competitive Landscape

The processed and frozen vegetables market shows moderate concentration in premium branded retail, but it remains far more fragmented when private-label suppliers and regional processors are included. Bonduelle, Greenyard, Nomad Foods, and Ardo hold strong shelf positions in Europe through owned brands and co-manufacturing arrangements. In North America, Conagra and General Mills continue to anchor branded volume across hypermarkets, club stores, and convenience channels. This structure keeps the processed and frozen vegetables market competitive because large multinational firms must still defend space and pricing against store brands and local processors.

A common response from major suppliers has been to move toward premium formats that are harder for private labels to copy quickly. Sauce-enhanced vegetables, globally inspired mixes, and organic lines are being used to protect margins and retain visibility in retailer planograms. Greenyard’s EUR 50 million IQF investment in Belgium and its alliance with Eureden in France are clear examples of a dual strategy built on scale, supply integration, and stronger origin positioning. Pictsweet Farms and J.R. Simplot continue to defend positions in North American retail and foodservice through regional sourcing strength and category focus. Hortex Holding and Frosta AG show that national provenance and localized brand trust can still support profitability against larger competitors in mid-market tiers.

Technology and sustainability are becoming more central to competition in the processed and frozen vegetables market. Advanced IQF lines, automated sorting, defect detection, and better energy management are increasingly concentrated among larger firms that can spread capital costs across more volume. Nomad Foods reported by May 2026 that all 14 legacy factories had shifted to 100% renewable energy, while absolute greenhouse gas emissions were down 41.1% from the 2019 baseline, and its 2050 net-zero target had been validated by the SBTi. Smaller regional operators are under greater pressure because they often cannot fund automation, green power transitions, and packaging upgrades on their own. That is why the processed and frozen vegetables market still offers room for consolidation, especially in regions where local product adaptation remains limited and larger players have not yet scaled affordable premium offerings.

Processed and Frozen Vegetables Industry Leaders

Bonduelle S.A.

Greenyard NV

Conagra Brands, Inc.

General Mills, Inc.

Nomad Foods Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mother Dairy Fruit and Vegetable Pvt. Ltd. completed a Rs 65 crore expansion of its Mangolpuri, Delhi facility, adding new Safal Frozen Peas processing lines to bring combined frozen processing capacity at Delhi and Ranchi to 17,000 MT per annum; the expansion supports a target to double its farmer network in Uttar Pradesh, Haryana, and Rajasthan through direct sourcing programs.

- February 2026: Greenyard finalized its strategic frozen vegetable alliance with Eureden, following approval by the French Autorité de la concurrence; the consolidated entity, combining Gelagri Bretagne, Eureden's frozen vegetable operations, and Greenyard Frozen France, operates from four Brittany sites, creating a leading player in French-origin frozen vegetables.

- September 2025: Greenyard announced a EUR 50 million investment in a new IQF production line at its Belgian facility, expanding annual frozen vegetable production capacity by 20% to meet accelerating European retail demand; this was followed in late 2025 by a EUR 4 million freezing tunnel investment at its Comines (Northern France) facility, increasing capacity from 40,000 to 60,000 tonnes annually.

Global Processed and Frozen Vegetables Market Report Scope

Processed vegetables include any edible plant or plant part altered from its natural state through washing, cutting, cooking, or preservation methods like canning and freezing. Frozen vegetables are fresh vegetables that undergo rapid temperature reduction below their freezing point to extend shelf life and preserve nutrients. The global processed and frozen vegetables market is segmented by process type, product type, nature, distribution channel, and geography. By process type, the market is segmented into frozen, canned, dried, and other process types. By product type, the market is segmented into peas, corn, broccoli, cauliflower, green beans, spinach, and other product types. By nature, the market is segmented into conventional and organic. By distribution channel, the market is segmented into foodservice and retail. The retail segment is further sub-segmented into supermarkets/hypermarkets, convenience stores, online retail, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Frozen Vegetables |

| Canned Vegetables |

| Dried Vegetables |

| Other Process Type |

| Peas |

| Corn |

| Broccoli |

| Cauliflower |

| Green Beans |

| Spinach |

| Mushrooms |

| Asparagus |

| Mixed Vegetables |

| Other Product Types |

| Conventional |

| Organic |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Process Type | Frozen Vegetables | |

| Canned Vegetables | ||

| Dried Vegetables | ||

| Other Process Type | ||

| Product Type | Peas | |

| Corn | ||

| Broccoli | ||

| Cauliflower | ||

| Green Beans | ||

| Spinach | ||

| Mushrooms | ||

| Asparagus | ||

| Mixed Vegetables | ||

| Other Product Types | ||

| Nature | Conventional | |

| Organic | ||

| Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of processed and frozen vegetables by 2031?

The category is forecast to reach USD 116.2 billion by 2031, rising from USD 89.6 billion in 2025 at a 4.1% CAGR from 2026 to 2031.

Which product type leads sales in frozen and processed vegetables?

Peas held the largest product type share at 33.6% in 2025 because they remain widely used across retail, foodservice, and industrial processing.

Which product is growing the fastest in this space?

Broccoli is the fastest-growing product type, with a projected 6.1% CAGR through 2031, supported by its health profile and wider use in premium meal formats.

Which distribution channel is strongest for processed and frozen vegetables?

Retail remained the largest channel with a 55.1% share in 2025, while foodservice is growing faster at a 6.5% CAGR through 2031.

Page last updated on: