Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 326.83 Billion |

| Market Size (2031) | USD 414.55 Billion |

| Growth Rate (2026 - 2031) | 4.87% CAGR |

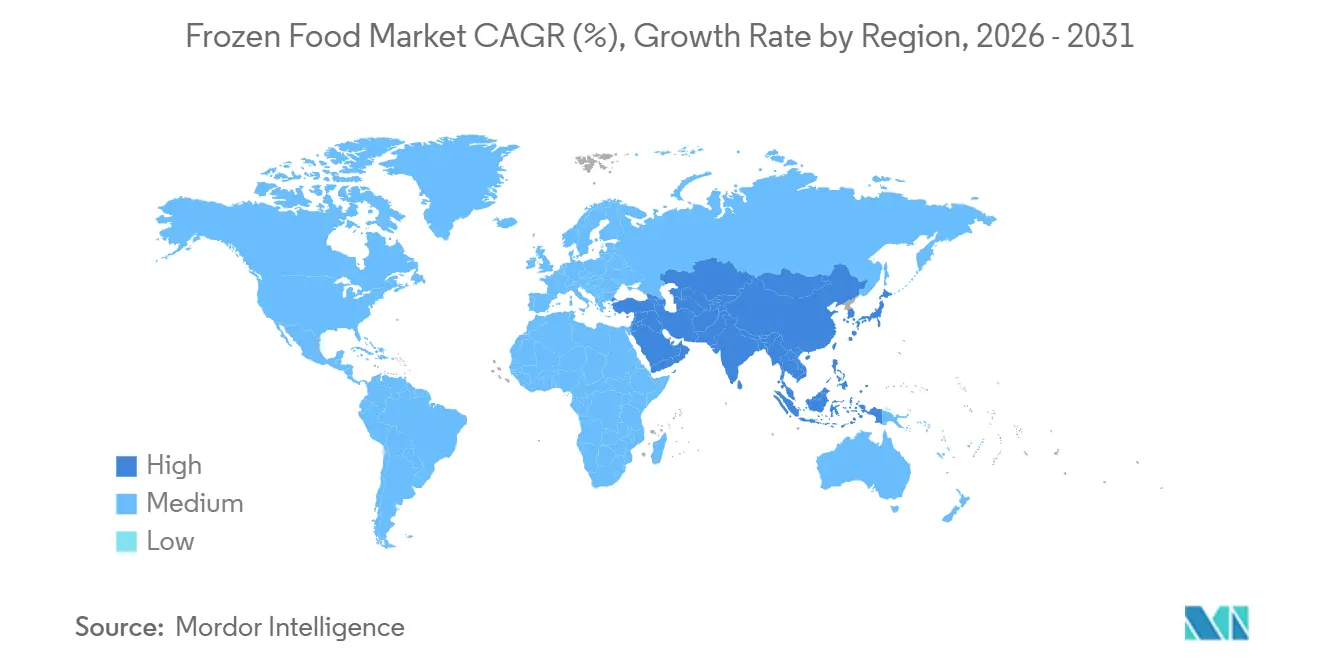

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

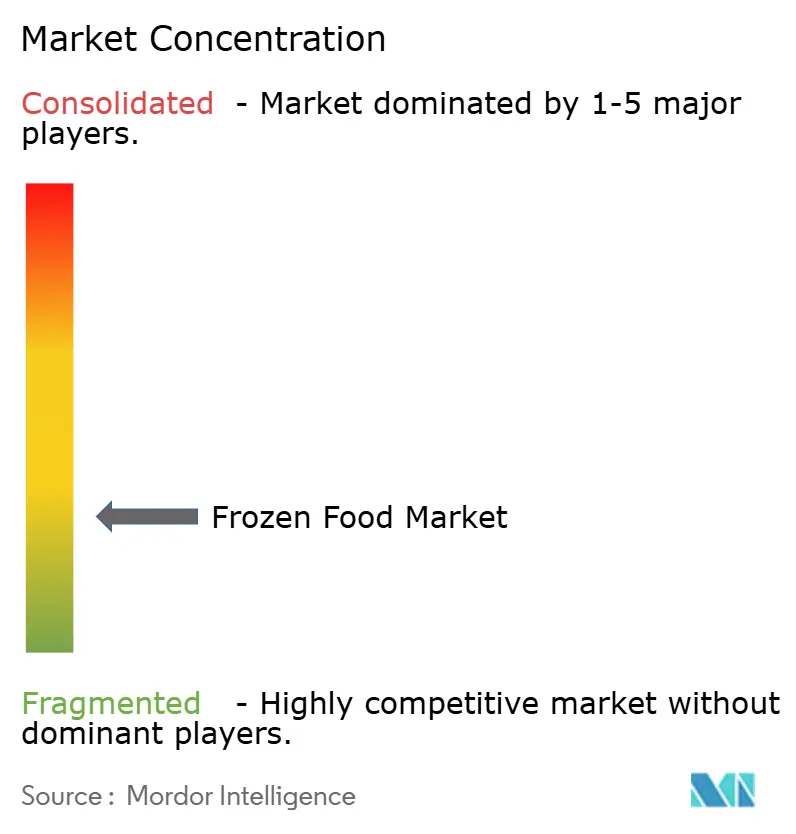

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Frozen Food Market Analysis by Mordor Intelligence

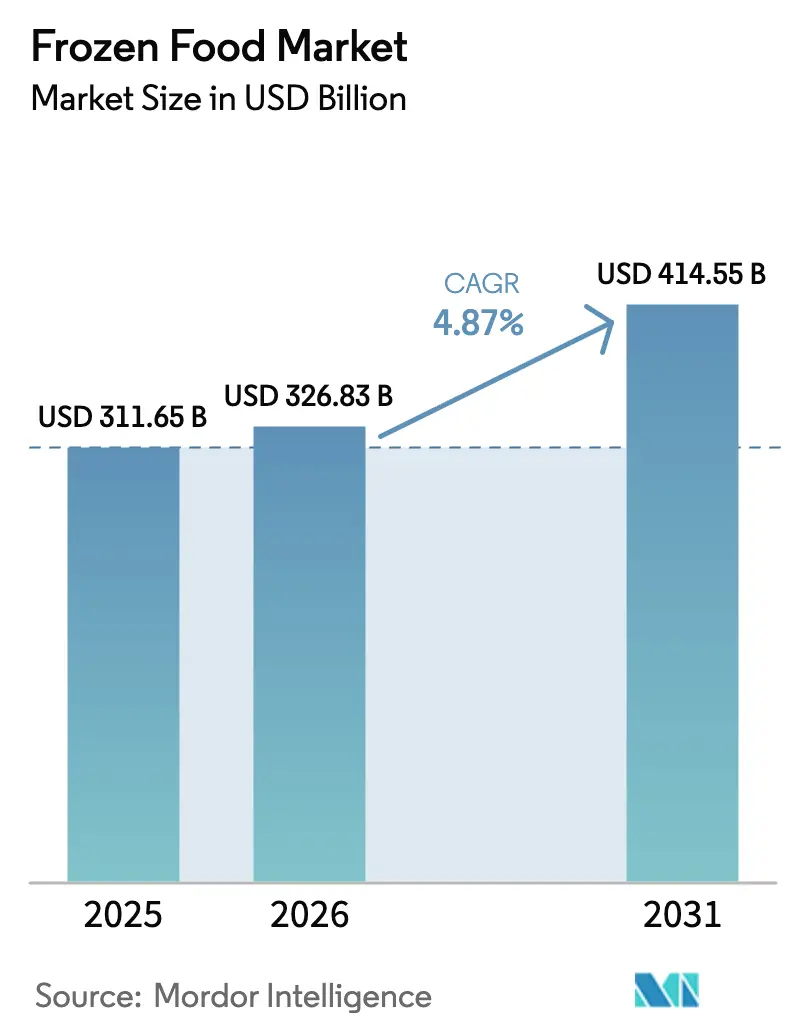

By 2031, the global frozen food market, valued at USD 326.83 billion in 2026, is projected to grow to USD 414.55 billion, marking a CAGR of 4.87%. Market growth is driven by rising consumer demand for convenient, long-shelf-life food products that reduce preparation time while maintaining quality and nutrition. Technological advancements such as Individual Quick Freezing (IQF) are improving product texture, flavor, and nutrient retention, strengthening consumer acceptance of frozen foods. Additionally, the expansion of modern retail and e-commerce platforms, along with temperature-controlled logistics, is improving product accessibility. In addition, rising investments in cold chain infrastructure across emerging economies are enhancing refrigerated storage, transportation, and distribution networks, enabling the efficient supply of frozen foods and supporting the market’s steady global growth [2]Source: United States Department of Agriculture "USDA Explanatory Notes - Food and Nutrition Service," usda.gov.

Key Report Takeaways

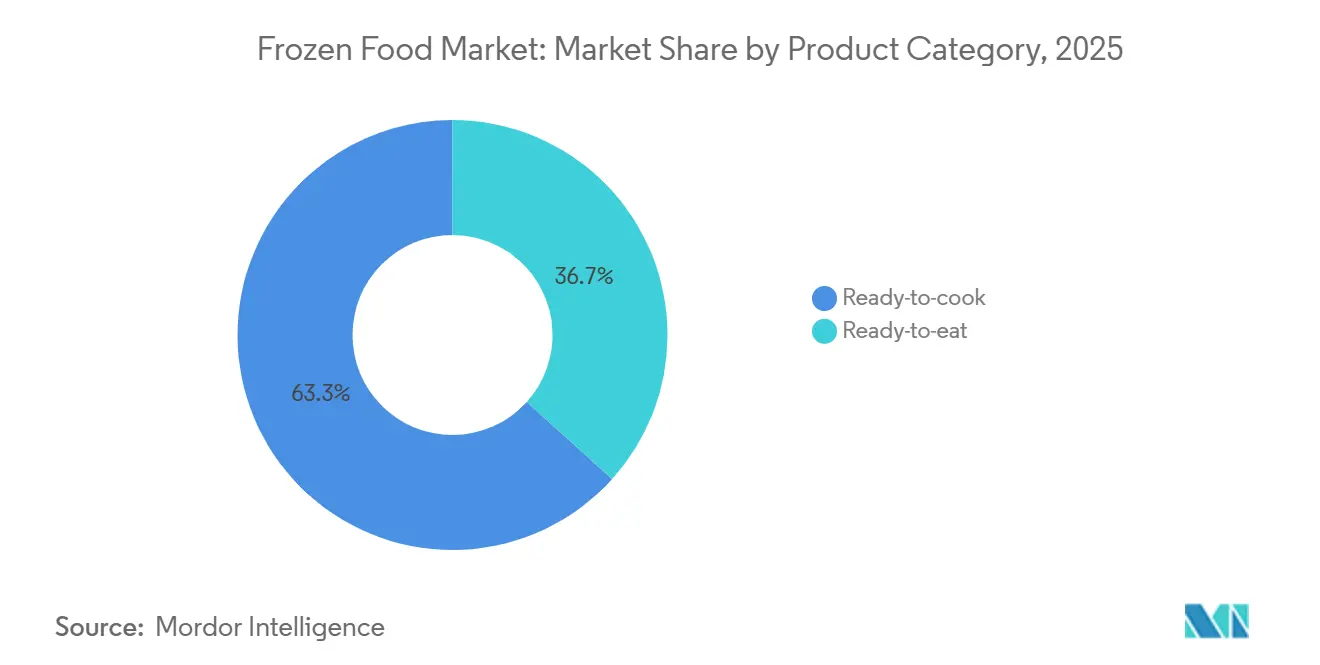

- By product category, ready-to-cook items led with 63.32% of frozen food market share in 2025, whereas ready-to-eat lines are forecast to register a 5.27% CAGR through 2031.

- By product type, frozen ready meals accounted for a 30.81% slice of the frozen food market size in 2025 while meat and seafood are pacing ahead at a 6.56% CAGR over the same horizon.

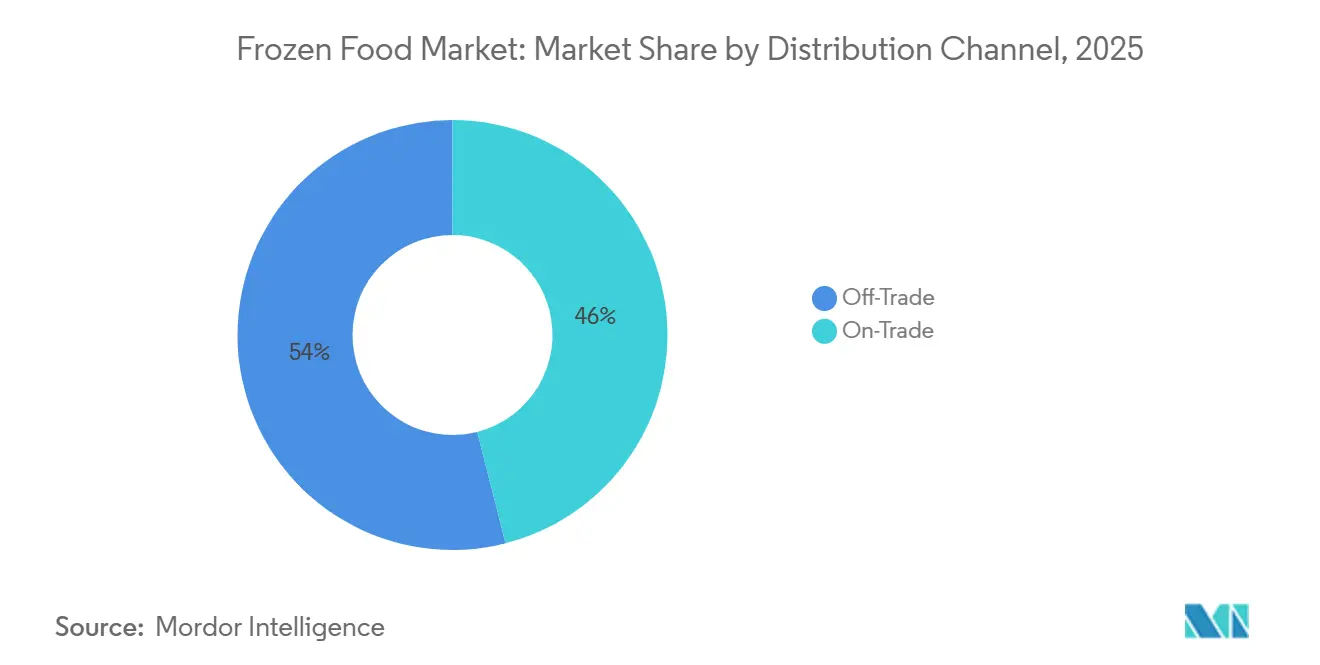

- By distribution channel, brick-and-mortar retail commanded 53.97% of global revenue in 2025, yet online platforms are scaling at a 7.12% CAGR to 2031.

- By geography, Europe represented 31.32% of 2025 revenue, but Asia-Pacific is set to outpace all other regions with a 6.80% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Frozen Food Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Frozen Snacking for Home-Based Socialising | +0.8% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Rapid Uptake of IQF Technology Enabling Texture-Safe Vegetables | +1.2% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Growth of Direct-to-Consumer Frozen Meal Kits | +0.6% | North America and Europe, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Clean-Label Frozen Entrées | +0.9% | North America and Europe, spillover to urban Latin America | Long term (≥ 4 years) |

| Increasing Frozen Aisles in Retail Channels | +0.7% | Global, strongest in emerging markets with expanding supermarket footprints | Medium term (2-4 years) |

| Increasing Demand for Plant-Based Frozen Foods | +1.0% | North America and Europe, nascent adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Frozen Snacking for Home-Based Socialising

As home entertainment trends continue to shape consumer habits, the demand for frozen snacks experiences significant growth during small gatherings and social events, thereby strengthening the frozen food market. Millennials and Generation Z consumers are increasingly drawn to bite-sized frozen appetizers compared to older generations. The market offers a wide range of frozen food options, including pizzas, sliders, and various snack foods, all designed to provide both convenience and variety. These products are easy to prepare and cater to diverse taste preferences, making them particularly suitable for social occasions. The frozen snack market is expanding as consumers increasingly seek solutions that combine efficiency with flavorful options for entertaining. This growth is primarily driven by Millennials and Generation Z, who prefer snacking options that are both convenient and varied. The growing adoption of air fryers in households further accelerates this market expansion, as frozen food manufacturers focus on developing products specifically tailored for air fryer preparation. In a strategic move, in April 2025, McCain Foods India collaborated with Philips to introduce a range of frozen snacks optimized for air fryers, including crispy fries that replicate the taste and texture of restaurant-quality offerings, providing consumers with quick and convenient dining solutions at home.

Rapid Uptake of IQF Technology Enabling Texture-Safe Vegetables

Individual Quick Freezing (IQF) technology has revolutionized the frozen vegetable market, ensuring that the structural integrity and nutritional value of produce are preserved. This advancement allows for the freezing of a wide array of vegetables, including those previously deemed challenging, such as avocados and leafy greens. As a result of this enhanced preservation quality, there has been a significant increase in frozen vegetable consumption, especially among health-conscious consumers. Furthermore, IQF technology plays a pivotal role in reducing food waste. By extending the seasonal availability of produce and minimizing spoilage throughout the supply chain, it addresses a critical concern in the industry. For example, the FLoFREEZE Individual Quick-Freezing freezer from JBT Frigoscandia employs advanced individual freezing technology, catering to vegetables, fruits, fish, and other premium IQF products. With its true fluidization capabilities, the system ensures both versatility and high-quality results. Additionally, JBT's Sequential Defrost technology offers substantial processing capacity in the Frigoscandia FLoFREEZE series-M range. Its adjustable airflow settings further enhance its utility, allowing it to accommodate products of diverse sizes and types.

Growth of Direct-to-Consumer Frozen Meal Kits

After encountering difficulties with the economics of chilled-box meal kits, HelloFresh and Blue Apron transitioned their focus to frozen formats in the direct-to-consumer meal kit market. They recognized that freezing not only enhances shelf life but also significantly reduces costs associated with spoilage during the final stage of delivery. Nestlé offers fully cooked meal options, enabling customers to conveniently reheat them in a short amount of time. This strategy appeals to consumers who value the convenience of meal kits but prefer not to feel pressured to cook immediately after receiving their delivery. By doing so, the model effectively separates the decision to purchase from the need for immediate consumption. Additionally, the subscription model benefits from this shift, as frozen meal kits are more adaptable to delivery delays and result in fewer customer-service complaints related to spoilage. At the same time, smaller companies are successfully carving out niches by offering meal subscriptions tailored to specific dietary preferences, such as ketogenic and paleolithic diets. These companies are leveraging the influence of social-media personalities to foster communities around these dietary protocols. However, a key challenge persists: the high cost of acquiring new customers in an increasingly competitive digital marketplace. Nevertheless, brands that achieve scalability can distribute their marketing expenses over a longer customer lifetime, made possible by the extended storage capabilities of frozen meal kits.

Rising Demand for Clean-Label Frozen Entrées

Clean-label positioning has shifted from fresh perimeters to the frozen aisle, as consumers increasingly scrutinize ingredient lists for artificial preservatives, flavor enhancers, and hard-to-pronounce additives. Parents of young children and health-conscious millennials, who see frozen meals as a convenient option rather than a compromise, are particularly willing to pay a premium for transparency. Regulatory changes are also coming into play; the United States Food and Drug Administration introduced front-of-pack labeling rules mandating calorie and sodium disclosures on frozen food[1]Source: Food and Drug Administration "FDA Proposes Requiring At-a-Glance Nutrition Information on the Front of Packaged Foods," fda.gov. This move is pushing manufacturers to reformulate their products to avoid negative labeling. Meanwhile, European Union member states are rallying around the Nutri-Score system, which penalizes high salt and saturated fat content. This has led brands to consider alternatives, like replacing palm oil with sunflower oil and significantly reducing sodium levels. The overarching message is clear: clean-label credentials are now essential for premium products, while value brands risk margin pressures if they cannot reformulate without increasing prices.

Restraints Impact Analysis of Frozen Food Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Gaps in Sustainable Seafood for Frozen SKUs | -0.5% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Consumer Perception of Freshness Gap vs. Chilled Meals | -0.6% | Global, strongest in Southern Europe and Latin America | Long term (≥ 4 years) |

| Rising Raw Material Cost | -0.7% | Global, most severe in import-dependent markets | Short term (≤ 2 years) |

| High Tariffs on Imported Frozen Goods | -0.4% | Asia-Pacific, Middle East, and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Gaps in Sustainable Seafood for Frozen SKUs

Frozen seafood manufacturers are facing significant supply chain challenges as consumer demand for sustainably sourced seafood continues to rise. The current market demand exceeds the availability of seafood certified by the Marine Stewardship Council (MSC) and responsibly harvested species. This imbalance is particularly evident in popular seafood varieties such as salmon, shrimp, and cod. Supplies of these wild-caught species are under increasing pressure due to overfishing and the adverse effects of climate change. The frozen food industry is experiencing notable shortages of seafood products that meet established sustainability standards. For example, the North Sea saithe fishery is expected to lose its certification from the Marine Stewardship Council by the end of June 2025. This suspension, announced by the Marine Stewardship Council earlier in the same month, follows a period of reduced stock productivity. A recent assessment conducted by the International Council for the Exploration of the Seas confirmed that the stock levels have fallen below sustainable thresholds. The North Sea saithe fisheries, which are a key source of cold-water species in the region, are the latest to face this certification setback.

Consumer Perception of “Freshness Gap” vs. Chilled Meals

Although freezing technology and product quality have significantly advanced, consumer perceptions continue to favor chilled meals over frozen alternatives. Many individuals associate chilled ready meals with a sense of freshness and higher quality, even though freezing can often preserve nutritional content more effectively over comparable periods. This perception is particularly strong among consumers with higher disposable incomes and in urban regions where well-established fresh food delivery systems are readily available. The appeal of chilled meals is further enhanced by their visual presentation, as transparent packaging allows consumers to clearly see the ingredients, reinforcing the perception of quality. To address these challenges, manufacturers are focusing on innovative packaging solutions that highlight product quality, initiating educational campaigns to inform consumers about the benefits of freezing, and developing hybrid products that integrate frozen components with fresh ingredients to meet evolving consumer preferences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Frozen Food Market Segment Analysis

By Product Category:

Ready-to-Cook Dominance and Ready-to-Eat MomentumIn 2025, ready-to-cook products commanded a dominant 63.32% of the market share, appealing to consumers who value control over seasoning and cooking methods, yet wish to save time on tasks like chopping vegetables or marinating proteins. Meanwhile, ready-to-eat formats are witnessing a robust annual growth of 5.27%, a trend projected to continue through 2031. This surge is largely fueled by single-person households and busy professionals who prioritize speed over customization. Such a divergence indicates a bifurcation in the category: ready-to-cook caters to families planning dinners together, while ready-to-eat focuses on quick lunches and last-minute meals.

In response, manufacturers are increasingly blurring category lines. They're rolling out hybrid products, such as pre-seasoned raw proteins that cook in just 8 minutes and fully cooked bowls that merely need a quick sear for texture enhancement. This wave of innovation is most pronounced in the Asia-Pacific region. Here, convenience-store chains, exemplified by 7-Eleven Japan, are offering frozen rice bowls and noodle kits, allowing customers to microwave them in-store, effectively transforming retail spaces into quasi-foodservice venues. Regulatory considerations also play a pivotal role. For instance, the European Union's Nutri-Score system, which penalizes high sodium content on front-of-pack labels, is nudging ready-to-eat manufacturers towards reformulation. This is crucial to avoid lower scores that could alienate health-conscious consumers. On the other hand, ready-to-cook items navigate these regulatory waters more smoothly, as the addition of salt during cooking grants brands greater formulation flexibility.

By Product Type:

Ready Meals Leadership and Protein SurgeIn 2025, frozen ready meals accounted for 30.81% of product-type revenue, solidifying their position as the leading category. At the same time, the meat and seafood segments are experiencing strong annual growth of 6.56%. This growth is fueled by the increasing popularity of protein-rich diets and the benefits of Individual Quick Freezing (IQF) technology, which preserves taste and texture immediately after harvest. Consumers are shifting toward ingredient-based cooking, preferring to purchase frozen chicken breasts or shrimp to prepare meals at home instead of relying on pre-made entrées. Additionally, the introduction of ethnic frozen meals, including Asian, Mediterranean, and Latin American cuisines, is meeting the growing demand for restaurant-quality meals at home. In March 2024, Bigbasket, a TATA Enterprise, launched 'Precia,' a new frozen foods brand. This brand is the result of Bigbasket's collaboration with Padma Shree Awardee Chef Sanjeev Kapoor. Every recipe under the Precia brand is carefully curated and tested by Chef Kapoor, utilizing IQF technology to maintain authentic flavors.

Frozen fruits and vegetables maintain a steady presence in the market, offering year-round availability and nutrient retention comparable to fresh produce. However, their growth is somewhat limited due to the perception that they are basic commodity items with minimal differentiation. On the other hand, frozen snacks and bakery products are gaining traction, particularly in the impulse purchase category. Single-serve options such as mini pizzas and stuffed pretzels are becoming popular choices for after-school snacks and late-night cravings. Frozen desserts, while a mature category, are seeing innovation in premium ice creams and novelty bars, which are attracting consumers with higher price points. Other product types, such as frozen soups and side dishes, serve as complementary items that enhance shopping baskets but rarely drive consumers to make store visits.

By Distribution Channel:

Off-trade Scale Meets Online AgilityIn 2025, retail channels, including hypermarkets, supermarkets, and convenience stores, led frozen-food sales, contributing 53.97% of the distribution. These retailers have capitalized on their ability to offer wide product assortments and encourage impulse purchases. However, online retail stores are rapidly gaining traction, growing at a (CAGR) of 7.12%. Platforms such as Instacart, Amazon Fresh, and Walmart Plus are driving this growth by implementing temperature-controlled last-mile logistics, ensuring frozen products maintain their integrity from warehouse to doorstep. The rise of online grocery platforms has expanded frozen food accessibility[3]Source: India Brand Equity Foundation "E-commerce Industry in India," ibef.org. This trend is particularly evident in urban markets, where consumers prioritize saving time over the traditional experience of browsing aisles. Additionally, the high delivery density in these areas makes the business model economically viable for these platforms.

Hypermarkets and supermarkets are responding by expanding their frozen-aisle offerings, introducing digital shelf labels to highlight promotions, and providing curbside pickup services that combine the convenience of online shopping with the variety of in-store selection. On the other hand, convenience and grocery stores are focusing on serving quick fill-in trips and emergency purchases but face challenges in competing on product assortment and pricing. The on-trade channel, which includes restaurants and institutional foodservice, benefits from frozen foods' ability to reduce waste and labor costs. However, its growth is limited by the perception that fresh ingredients signify higher quality. Retailers that successfully integrate online and offline channels are better positioned to thrive, using physical stores as micro-fulfillment centers to speed up delivery times and lower shipping costs.

Geography Analysis

Europe Frozen Food Market

Europe holds a 31.32% market share in 2025, supported by established frozen food consumption patterns and developed cold-chain infrastructure. The market encompasses major economies, including Germany, the United Kingdom, France, Spain, Italy, and Russia, each contributing significantly to the regional market dynamics. The European market focuses on product innovation, sustainable packaging solutions, and premium frozen food products.

APAC Frozen Food Market

Asia-Pacific demonstrates the fastest growth with a CAGR of 6.80% during 2026-2031. The frozen food industry shows significant growth potential, driven by rapid urbanization, changing consumer lifestyles, and increasing disposable incomes. The region encompasses major markets including China, Japan, India, and Australia, each showing distinct market characteristics and growth patterns. The region is experiencing substantial developments in cold chain infrastructure and retail network expansion, supporting growth in the frozen food market. Consumers in the Asia-Pacific show increasing acceptance of frozen food products, particularly in tier-1 and tier-2 cities.

North America Frozen Food Market

The North American frozen food market demonstrates robust growth driven by changing consumer lifestyles and increasing demand for convenient food options. The United States leads the regional market, followed by Canada and Mexico, with each country showing distinct consumption patterns and market dynamics. The frozen food industry in the United States has expanded its premium offerings, with manufacturers introducing new product variants to meet consumer preferences. For instance, in February 2024, Conagra announced the expansion of its Bertolli brand in the frozen food segment with the launch of Bertolli oven meals and appetizers. The oven meals include three varieties: chicken alfredo, chicken parmigiana and penne, and meatball rigatoni. The appetizers feature three cheese toasted ravioli and arancini Parmesan, which are compatible with air fryers.

Competitive Landscape

Global leaders such as Nestlé, Conagra Brands, and Nomad Foods continue to dominate the frozen food sector by leveraging their extensive product portfolios, strong research and development capabilities, and widespread distribution networks. For example, in January 2025, HyFun Foods, an Indian exporter specializing in frozen potato products, partnered with Woolworths, Australia's largest retail chain, to distribute its frozen snacks across more than 1,000 Woolworths stores. The market remains dynamic, with strategic transactions shaping its evolution. In May 2025, Conagra Brands, Inc. announced the sale of its Chef Boyardee brand to Hometown Food Company, a portfolio company of Brynwood Partners, for USD 600 million in cash.

The fastest-growing segment in the frozen food industry is driven by technological advancements. Companies are differentiating themselves through innovations such as Individual Quick Freezing (IQF) systems, vacuum skin-pack technology, and advanced packaging materials. Additionally, digital initiatives like product traceability and online recipe platforms are strengthening customer relationships and providing valuable consumer insights. Growth opportunities are particularly evident in premium ethnic foods and specialized frozen products catering to specific dietary needs, attracting new entrants who often become acquisition targets for established players.

Regional companies maintain their market presence by emphasizing local ingredient sourcing, traditional recipes, and environmentally sustainable practices. New entrants are experimenting with direct-to-consumer distribution models as alternatives to conventional retail channels. Competition in the market is focused on innovation, speed, and the ability to meet consumer demands for flavor, nutrition, sustainability, and convenience.

Frozen Food Industry Leaders

-

General Mills Inc

-

Unilever Plc

-

Tyson Foods Inc.

-

The Kraft Heinz Company

-

Nomad Foods Ltd.

- *Disclaimer: Major Players sorted in no particular order

Frozen Food Market Companies Covered in this Report

- Nestlé S.A.

- Conagra Brands Inc.

- General Mills Inc.

- Nomad Foods Ltd.

- Tyson Foods Inc.

- McCain Foods Ltd.

- The Kraft Heinz Company

- Ajinomoto Co. Inc.

- Unilever PLC

- Hormel Foods Corp.

- Bellisio Foods Inc.

- Iceland Foods Ltd.

- Grupo Bimbo SAB de CV

- Charoen Pokphand Foods

- BRF S.A.

- Oetker Group

- Frosta AG

- NH Foods Ltd.

- Maple Leaf Foods Inc.

- CJ CheilJedang Corp.

Recent Industry Developments in Frozen Food Market

- May 2025: HyFun Foods expanded its ready-to-cook frozen snack portfolio by introducing Indian street-style flavors. The company launched Mumbai Aloo Vada and plans to introduce Spicy Paneer Patty to meet the growing demand for diverse frozen food options among urban Indian consumers.

- January 2025: Westbridge Foods, a UK importer and developer of Asian foods, launched Kitchen Joy, a Thai-specialist ready meal brand, at Tesco. The brand introduced six rice and noodle-based frozen meals in over 580 Tesco stores, including Thai classics such as Chicken Panang, Tom Yum, and Green Curry, along with fusion dishes like Spicy Sesame Chicken Noodles.

- January 2025: Siniora Foods, a meat processing company, is establishing a new manufacturing facility in Saudi Arabia with a USD 40 million investment. The new facility in Jeddah will increase Siniora's production capacity for cold cuts and frozen foods.

Frozen Food Market Report Scope and Research Methodology

Market Definition and Coverage

According to Mordor Intelligence, the frozen food market comprises all packaged edible products that are mechanically frozen and stored at or below 0 C to extend shelf life, spanning ready meals, fruits and vegetables, meat and seafood, bakery items, desserts, and snack foods sold through retail and food-service channels worldwide.

Scope exclusion: Chilled-only goods and freeze-dried products lie outside this study's purview.

Segments Covered in This Report

-

By Product Category

- Ready-to-Eat

- Ready-to-Cook

-

By Product Type

- Frozen Fruits and Vegetables

- Frozen Meat and Seafood

- Frozen Ready Meals

- Frozen Snacks and Bakery

- Frozen Desserts

- Other Product Types

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Stores

- Other Retail Formats

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Primary Research

To refine assumptions, Mordor analysts held structured interviews with frozen food manufacturers, cold-chain logistics managers, grocery buyers, and e-commerce category heads across North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. These conversations clarified average selling prices, emerging diet trends, private-label shares, and regional regulatory shifts, which we then triangulated with desk findings.

Desk Research

We first mapped the industry using publicly available macro and trade datasets such as FAOSTAT, UN Comtrade, the USDA's Cold Storage Reports, and Eurostat retail sales, which outline volume flows and consumption patterns. Company filings, investor decks, and leading trade journals complemented these basics, while select proprietary datasets from D&B Hoovers and Dow Jones Factiva helped gauge corporate revenue splits and news momentum. Additional inputs came from regional food-processing associations and patent searches via Questel to track IQF technology uptake. This list is illustrative; many more secondary sources fed the core model.

Market-Sizing and Forecasting

The baseline value derives from a blended top-down and bottom-up framework. Top-down, we reconstructed demand from production and cross-border trade volumes, adjusted for retail and food-service penetration. Bottom-up checks rolled up sampled supplier revenues and channel ASP times unit estimates to validate totals. Key variables include household frozen food penetration, cold-storage capacity, IQF adoption rate, online grocery share, and average retail price movements; these feed a multivariate regression that projects consumption over the forecast period. Where company-level data were incomplete, interpolation used regional consumption ratios before being re-benchmarked to national accounts.

Data Validation and Update Cycle

Every draft model passes three reviews: an automated variance scan, peer analyst audit, and senior analyst sign-off. We refresh figures annually, with interim updates triggered by material events such as tariff shifts or major M&A, ensuring clients receive the latest vetted view.

How Mordor Intelligence's Frozen Food Market Size Compares to Other Published Estimates

Published estimates often diverge because firms select different product mixes, sales channels, currencies, and refresh cadences.

Key gap drivers include narrower category coverage, reliance on single-source assumptions, currency conversion lags, or longer update cycles. By contrast, Mordor's scope spans all major product groups and both retail and food-service demand, and our annual refresh captures rapid gains in online grocery and plant-based offerings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 311.74 B (2025) | Mordor Intelligence | - |

| USD 297 B (2024) | Global Consultancy A | Excludes food-service sales; biennial update |

| USD 310.77 B (2024) | Industry Journal B | Top-down only, limited ASP validation |

| USD 314.55 B (2025) | Research Provider C | Omits frozen fruits and vegetables segment |

In sum, our disciplined variable selection, dual-angle modeling, and tight validation steps give decision-makers a transparent, reproducible baseline they can trust, while highlighting precisely why alternative figures may skew higher or lower.

Key Questions Answered in the Report

How large is the frozen food market in 2026?

The frozen food market size is valued at USD 326.83 billion in 2026, with a forecast to reach USD 414.55 billion by 2031.

Which product category leads global sales?

Ready-to-cook items hold the top position, accounting for 63.32% of 2025 revenue.

What region shows the fastest growth?

Asia-Pacific is projected to advance at a 6.80% CAGR through 2031, outpacing all other regions.

How fast is online grocery expanding for frozen foods?

Online platforms are registering a 7.12% CAGR, nearly doubling urban frozen volumes through 2031.

Which product type is gaining share over ready meals?

Meat and seafood are growing at a 6.56% CAGR as consumers favor ingredient-based cooking alongside protein-rich diets.

Page last updated on: