Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

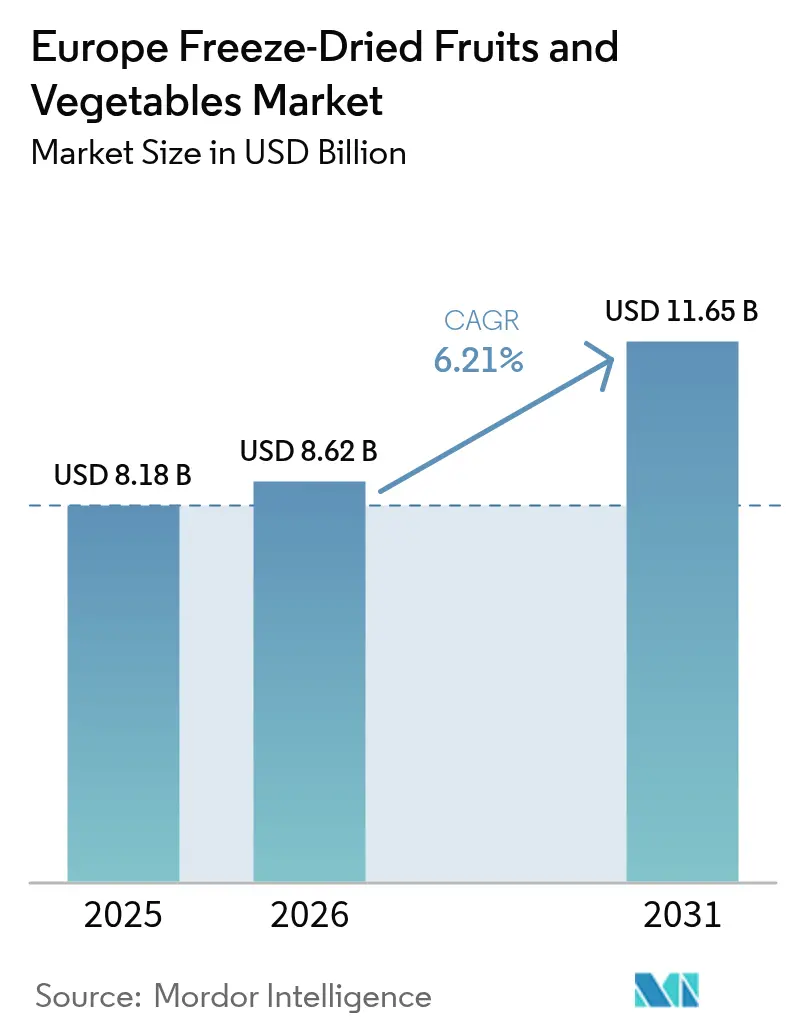

| Base Year Market Size (2025) | USD 8.18 Billion |

| Market Size (2026) | USD 8.62 Billion |

| Market Size (2031) | USD 11.65 Billion |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Freeze-Dried Fruits And Vegetables Market Analysis by Mordor Intelligence

The Europe freeze-dried fruits and vegetables market size was USD 8.18 billion in 2025, and is projected to reach USD 8.62 billion in 2026, and USD 11.65 billion by 2031, growing at a CAGR of 6.21% from 2026 to 2031. This expansion is underpinned by structural shifts toward plant-based diets, clean-label reformulation, and shelf-stable convenience formats that mitigate food waste and supply-chain volatility. Investments in freeze-drying capacity are accelerating as processors respond to EU Farm-to-Fork waste-reduction mandates, retailer shelf-life demands, and consumers’ willingness to pay premiums for sustainable foods. Ingredient suppliers are integrating freeze-dried powders to replace synthetic colorants in breakfast cereals and snacks, while drought-related crop variability in Southern Europe is pivoting processors toward shelf-stable vegetable inputs. Energy-efficient freeze-drying technology, e-commerce channel migration, and the rise of flexitarian consumers are further reinforcing demand momentum across the European freeze-dried fruits and vegetables market.

Key Report Takeaways

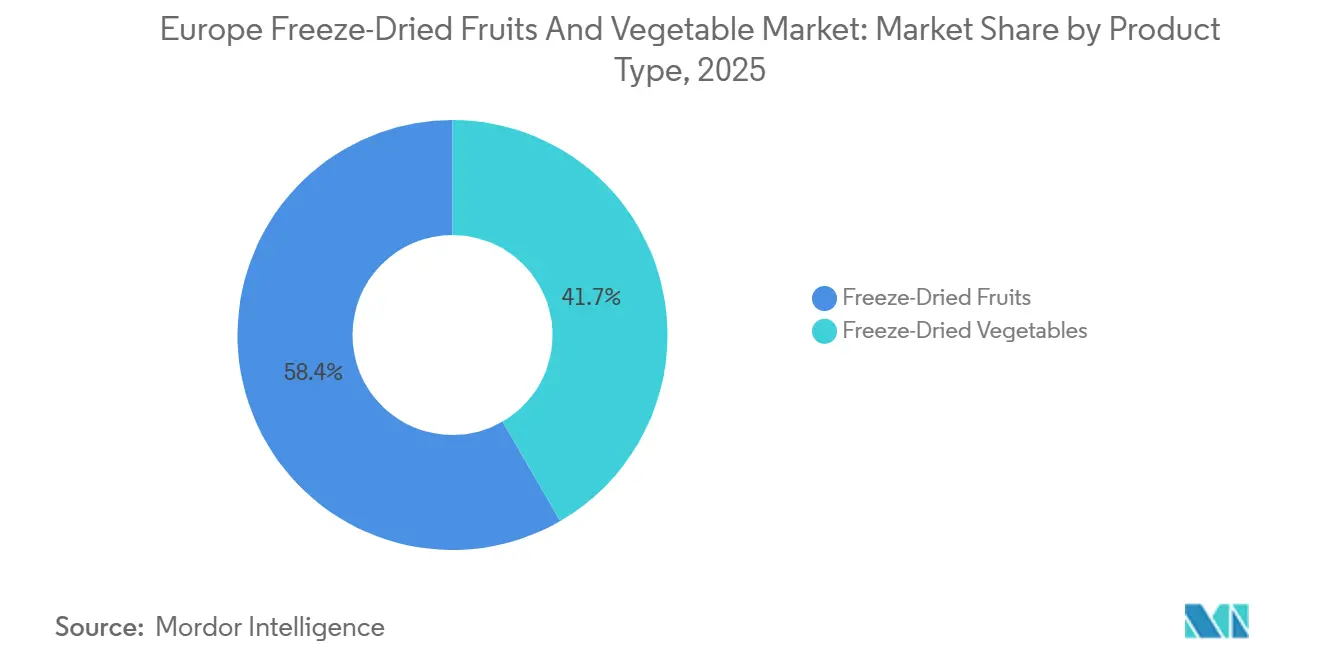

- By product type, fruits led with 58.35% of the Europe freeze-dried fruits and vegetables market share in 2025, and vegetables are projected to expand at a 7.81% CAGR through 2031.

- By form, powders and granules commanded 48.52% share of the Europe freeze-dried fruits and vegetables market size in 2025, and chunks and pieces are advancing at a 7.54% CAGR through 2031.

- By nature, conventional contributed 75.64% revenue share in 2025; organic is forecast to grow at a 6.86% CAGR to 2031.

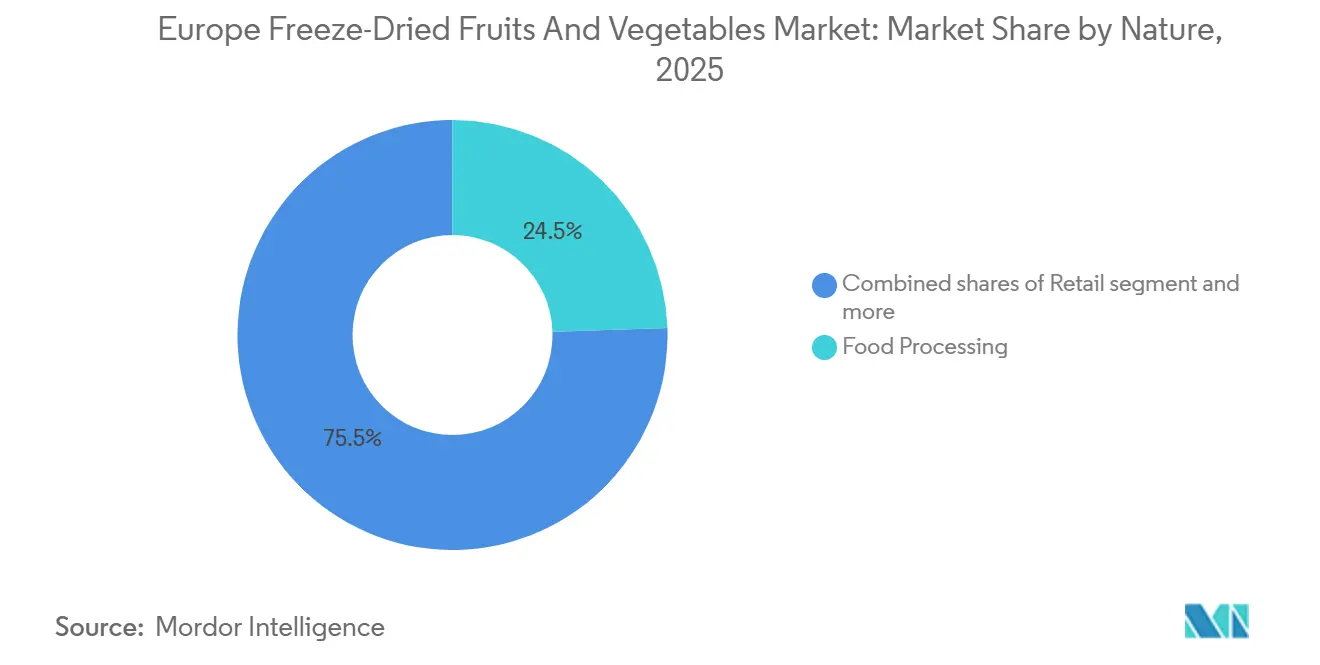

- By end-user, food processing contributed 24.48% revenue share in 2025; retail is forecast to grow at a 8.03% CAGR to 2031.

- By country, Germany contributed 26.71% revenue share in 2025; Spain is forecast to grow at a 7.17% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Freeze-Dried Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for convenient, ready-to-eat snack options | +1.8% | Germany, France, UK with spillover to Netherlands, Belgium | Medium term (2-4 years) |

| Advancements in freeze-drying technology and energy efficiency | +1.2% | Germany, Netherlands, Belgium with expansion to Spain, Italy | Long term (≥ 4 years) |

| Rising health and wellness awareness among European consumers | +1.0% | Global across all European markets | Short term (≤ 2 years) |

| Expansion of plant-based and vegan diets across Europe | +0.9% | Germany, France, UK, Netherlands with growth in Spain | Medium term (2-4 years) |

| Use of freeze-dried fruit inclusions and powders in breakfast cereals | +0.8% | Germany, France, UK, Netherlands, Belgium | Medium term (2-4 years) |

| Rising health and wellness awareness among European consumers | +0.6% | Germany, France, Italy with expansion to Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for convenient, ready-to-eat snack options

Urban lifestyles and dual-income households are compressing meal-prep time, propelling an 8.03% CAGR in retail sales of freeze-dried snacks through 2031. Freeze-dried raspberries, mango chunks, and vegetable crisps offer ambient stability and portion-controlled servings that fit on-the-go consumption in Berlin, London, and Paris. Digital-native brands leverage Ireland’s and the Netherlands’ online-shopping penetration to bypass supermarket gatekeepers, monetize direct-to-consumer subscriptions, and scale quickly. Shelf lives exceeding 24 months let marketers build pan-Europe coverage without refrigerated logistics. This immediacy underpins the short-term boost to the Europe freeze-dried fruits and vegetables market.

Advancements in freeze-drying technology and energy efficiency

Heat-pump-assisted freeze-dryers and hybrid systems combining microwave and vacuum technologies reduce cycle times from 24 hours to 16 hours while cutting energy consumption by 25-30%, improving unit economics for mid-tier processors competing on price with spray-dried and air-dried alternatives. Germany, the Netherlands, and Sweden, home to advanced manufacturing clusters and high electricity costs, are early adopters, with equipment suppliers like GEA and Buchi offering retrofit packages that amortize over 3 to 5 years through energy savings. The long-term impact timeline accounts for capital-replacement cycles: industrial freeze-dryers carry 15 to 20-year service lives, and processors defer upgrades until existing assets reach end-of-life or until energy-cost differentials justify accelerated depreciation.

Rising health and wellness awareness among European consumers

Freeze-dried fruits and vegetables deliver concentrated micronutrients, and vitamin C retention exceeds 90% versus 50-60% in thermally dried alternatives, without added sugars or preservatives, positioning them as ingredient solutions for fortified snacks and meal replacements targeting aging demographics and fitness-conscious millennials. Denmark and Sweden lead adoption, where per-capita organic food spending in 2024 reflects established consumer acceptance of premium-priced functional foods. European consumers are recalibrating food choices around functional nutrition as people are willing to pay premiums for sustainable and health-promoting products. The medium-term impact reflects the lag between consumer awareness and reformulation cycles in packaged goods, as brands require 18 to 24 months to validate freeze-dried ingredients in existing SKUs and secure retailer shelf space.

Expansion of plant-based and vegan diets across Europe

Freeze-dried formats solve a critical formulation challenge: fresh vegetables add moisture that destabilizes shelf life in ambient-stable plant-based products, while freeze-dried alternatives contribute texture and nutrition without compromising microbial safety. The Europe market for natural food additives is growing, driven by health-conscious consumers and regulatory preferences for natural over synthetic additives, with a focus on transparency and sustainability, as reported by the CBI [1]Source: CBI, "Which trends offer opportunities or pose a threat on the European natural food additives market?", cbi.eu. Freeze-dried vegetables, particularly peas, corn, and mushrooms, serve as protein and umami sources in plant-based ready meals, soups, and meat analogues, where their concentrated flavor profiles reduce the need for sodium and yeast extracts that carry negative clean-label connotations. Germany, the Netherlands, and the UK lead plant-based retail sales, with Germany's plant-based food market expanding annually and the Netherlands achieving a significant organic share of total food sales in 2024.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment requirements for freeze-drying equipment | -1.1% | Spain, Italy, France with spillover effects across Europe | Short term (≤ 2 years) |

| Premium pricing compared to conventional dried or fresh alternatives | -0.8% | EU-wide with particular impact in Germany, France | Medium term (2-4 years) |

| Stringent European Union food safety and labeling regulations | -0.7% | Global across all European markets | Long term (≥ 4 years) |

| Long production cycles in freeze-drying reduce throughput | -0.9% | Germany, Netherlands, Belgium with expansion barriers in Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capital investment requirements for freeze-drying equipment

Industrial freeze-dryers require upfront investments exceeding USD 1 million per production line, a capital barrier that limits market entry and constrains capacity expansion among mid-tier processors in Southern and Eastern Europe, where access to low-cost financing is restricted. This restraint is compounding as equipment suppliers consolidate and prioritize large-volume customers, leaving smaller operators with limited negotiating leverage on payment terms or technical support. The long-term impact reflects the durability of freeze-drying assets: once installed, equipment operates for years, creating a "first-mover advantage" for established players like Germany's Freeze-Dry Foods and the UK's Chaucer Foods that amortized capital costs during prior investment cycles and now compete on variable-cost efficiency.

Premium pricing compared to conventional dried or fresh alternatives

Freeze-dried fruits and vegetables command retail prices 3 to 5 times higher than air-dried or fresh equivalents, a premium that narrows addressable markets during periods of consumer income pressure. The medium-term impact reflects the lag between inflation stabilization and consumer willingness to resume uptrading: real wages began recovering in 2024, but purchasing-pattern shifts, such as increased private-label buying and channel migration to discounters, persist 2 to 4 years beyond macroeconomic recovery as households rebuild savings and adjust reference prices. This dynamic is bifurcating the market: premium freeze-dried snack brands targeting health-conscious consumers in high-income markets (Nordics, Germany, Netherlands) sustain volume growth, while mass-market food processors in price-sensitive regions substitute freeze-dried ingredients with lower-cost alternatives like drum-dried powders or IQF (individually quick frozen) products that offer partial shelf-life extension at a lower ingredient cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vegetables Gain as Supply-Chain Volatility Rises

Fruits held 58.35% of 2025 revenue, anchored by strawberries, raspberries, and mangoes that dominate breakfast cereal inclusions and snack mixes. Yet, vegetables are forecast to expand at 7.81% CAGR through 2031, outpacing fruits by 1.6 percentage points, as food-service operators and soup manufacturers hedge against fresh-vegetable price swings and labor shortages in commercial kitchens. Strawberries and raspberries retain premium positioning in organic muesli and ice-cream inclusions, where their visual appeal and concentrated flavor justify ingredient costs above those of conventional dried fruits, but pineapple and mango are gaining market share in tropical smoothie bowls and plant-based yogurt toppings as retailers expand exotic-fruit SKUs to differentiate private-label ranges.

Carrots and beetroot powders function as natural colorants in extruded snacks and pasta, replacing synthetic dyes under pressure from France's Nutri-Score and Germany's clean-label retailer mandates. Apple and mango chunks remain staples in trail mixes and granola bars, but their growth is capped by consumer familiarity and limited differentiation opportunities, whereas freeze-dried vegetables are penetrating new applications, such as instant ramen seasoning packets and camping meals, that were previously dominated by air-dried or spray-dried alternatives. The 7.81% vegetable CAGR also captures geographic expansion in Eastern Europe, where Poland's GreenField and emerging processors are targeting local food-service chains with bulk freeze-dried vegetable blends priced below Western Europe suppliers by leveraging lower labor costs and proximity to agricultural sourcing regions.

By Form: Chunks and Pieces Gain in Premium Visual Applications

Powder and granule forms commanded 48.52% of 2025 revenue, driven by bulk demand from breakfast-cereal lines, soup manufacturers, and bakery operations requiring consistent particle-size distribution and rapid rehydration rates, yet chunks and pieces are projected to grow at 7.54% CAGR through 2031 as premium muesli brands and ice-cream manufacturers prioritize visual differentiation and texture contrast. Chunks also deliver superior mouthfeel in yogurt parfaits and overnight oats, rehydrating to near-fresh texture within 5 to 10 minutes versus powders that dissolve instantly but lack the sensory cues consumers associate with whole-fruit ingredients. Flakes, the smallest segment, serve niche applications in instant beverage mixes and nutritional supplements, where rapid dissolution and homogeneous color distribution are critical, but their growth is constrained by limited differentiation versus spray-dried alternatives that offer comparable functionality at a lower cost.

Freeze-dried fruit chunks enable brands to command price premiums by delivering Instagram-worthy visual appeal, a marketing lever particularly effective in online retail, where most of the EU internet users now shop digitally, and product photography drives purchase intent. Powder and granule forms retain dominance in food-processing applications because they integrate seamlessly into dough systems, dry-mix formulations, and extruded snacks without requiring specialized dosing equipment, and their lower per-kilogram pricing (typically below chunks) aligns with cost-conscious procurement strategies in mass-market bakery and confectionery. However, the visual and textural advantages of chunks are driving reformulation in premium segments, as brands seek to differentiate in crowded categories where ingredient transparency and sensory experience increasingly determine consumer choice and retailer allocation of limited shelf space.

By Nature: Organic Certification Drives Niche Premiumization

Conventional freeze-dried products held 75.64% of 2025 revenue, reflecting their cost competitiveness and broad availability across food-processing and retail channels, but organic variants are expanding at 6.86% CAGR through 2031 as the EU organic retail market and new Regulation 2022/2092 streamlined certification for processors by harmonizing standards across member states and reducing administrative burdens. Organic certification adds to raw-material costs due to lower agricultural yields and stricter traceability requirements, but brands targeting health-conscious consumers in high-income markets, particularly Nordics, Germany, and the Netherlands, sustain volume growth by positioning organic freeze-dried products as functional snacks that deliver concentrated micronutrients without pesticide residues or synthetic additives.

Conventional products dominate food-processing applications because multinational cereal and soup manufacturers prioritize ingredient-cost optimization and supply-chain reliability over organic claims, and because organic-certified freeze-dried vegetables face availability constraints during off-seasons when processors must source from Southern Hemisphere suppliers at premium freight costs. Online retail growth enables organic freeze-dried brands to bypass traditional distribution gatekeepers and sell direct-to-consumer via subscription models, capturing margin that previously accrued to retail intermediaries and funding marketing investments that build brand equity in niche segments. A wild collection of organic berries, particularly in Finland's million hectares of certified wild areas, provides a differentiated sourcing narrative that resonates with consumers seeking "beyond-organic" provenance stories, though volumes remain limited relative to cultivated organic production.

By End-User: Retail Channels Disrupt Traditional Food-Processing Dominance

Food processing captured 24.48% of 2025 revenue, driven by bulk demand from breakfast-cereal lines, soup manufacturers, and bakery operations requiring consistent quality and multi-year supply contracts, yet retail channels are forecast to grow at 8.03% CAGR through 2031, the fastest rate across all end-user segments, as direct-to-consumer brands leverage e-commerce platforms to bypass traditional distribution and capture margin. Specialty stores serve affluent urban consumers seeking organic and exotic freeze-dried products, but their growth is capped by limited geographic footprints and higher operating costs relative to online-pure-play competitors that amortize customer-acquisition costs across pan-Europe markets.

HoReCa (foodservice) applications are recovering post-pandemic as restaurant and catering operators resume operations, but labor shortages and cost pressures are driving substitution of fresh vegetables with freeze-dried alternatives that require no prep labor and eliminate spoilage losses, a shift particularly pronounced in contract catering for schools, hospitals, and corporate cafeterias, where standardized menus and centralized kitchens favor shelf-stable ingredients. Bakery and confectionery applications, such as freeze-dried fruit powders in cake mixes and fruit-filled cookies, grow steadily but face competition from lower-cost spray-dried and drum-dried alternatives that offer comparable functionality at a lower ingredient cost, limiting freeze-dried penetration to premium SKUs where clean-label claims and natural-color positioning justify the price premium.

Geography Analysis

Germany held 26.71% of 2025 revenue, underpinned by a EUR 200 billion food industry employing over 650,000 workers and exporting 2 of every 3 products manufactured, but Spain is forecast to grow at 7.17% CAGR through 2031, the fastest rate among major geographies, as drought conditions and climate volatility compel processors to secure shelf-stable vegetable inputs and reduce dependence on fresh-crop supply chains [2]Source: Federal Statistical Office, "German Food Industry", destatis.de. Spain's agri-food exports reached EUR 72.5 billion in 2024, expanding 8.3% year-on-year despite fresh tomato and pepper yields declining 15-20% due to water scarcity, a supply-demand imbalance that is driving food processors toward freeze-dried alternatives that eliminate cold-chain logistics and extend shelf life from weeks to years [3]Source: Spanish Ministry of Agriculture, Fisheries, and Food (MAPA), "Spain's agri-food potential and its export" mapa.gob.es .

The UK and France market are expanding, propelled by clean-label reformulation mandates and retailer private-label programs that prioritize natural ingredients, though Brexit-related trade frictions have increased import costs for UK processors sourcing freeze-dried ingredients from EU suppliers, creating opportunities for domestic capacity expansion. Italy's billion-dollar food-processing sector and Poland's emerging freeze-dried industry are growing, driven by geographic proximity to agricultural sourcing regions and lower labor costs that enable competitive pricing versus Western European suppliers. The Netherlands and Belgium, small markets by revenue, punch above their weight as re-export hubs; positioning Dutch processors as intermediaries capturing margin on logistics and quality assurance.

Poland's GreenField and emerging processors are targeting local food-service chains and Eastern European export markets with bulk freeze-dried vegetable blends priced below Western European suppliers, leveraging lower energy costs and proximity to Ukrainian and Polish agricultural output. The Rest of Europe category, encompassing smaller markets like Romania, Bulgaria, and the Baltics, is expanding as rising incomes and supermarket modernization drive demand for packaged convenience foods, though price sensitivity limits freeze-dried penetration to urban centers and affluent consumer segments.

Competitive Landscape

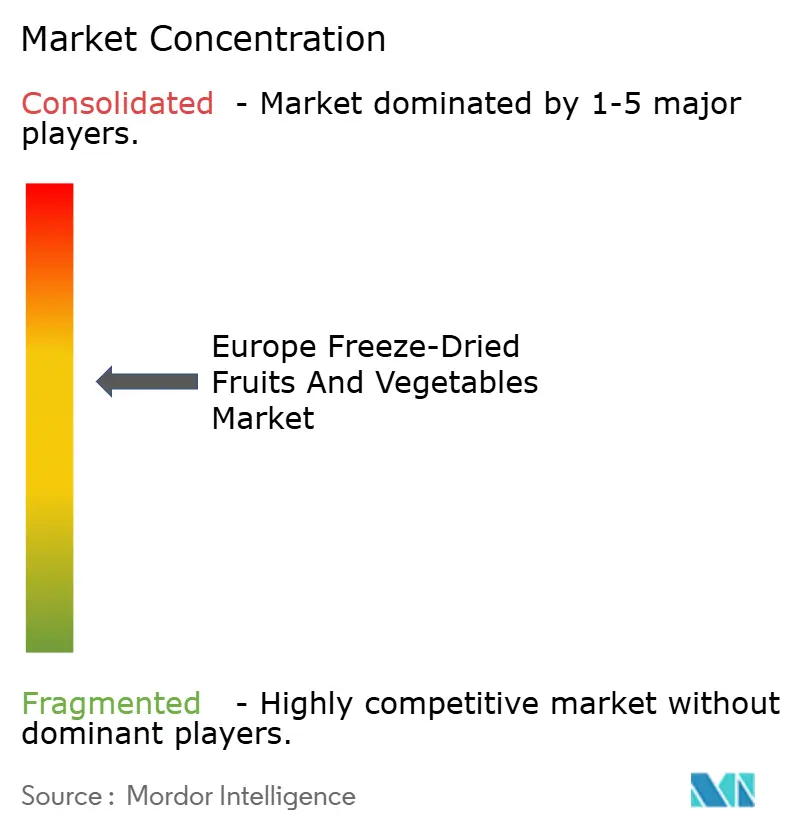

The Europe freeze-dried fruits and vegetables market exhibits moderate-to-high concentration, indicating that mid-tier specialists and regional processors retain meaningful share despite consolidation moves such as Thrive Freeze Dry's acquisition of Germany's Paradiesfrucht in July 2024, a transaction that combined North American freeze-drying capacity with European sourcing and distribution networks. Competitive intensity is rising as ingredient suppliers like Döhler and Givaudan vertically integrate into freeze-dried natural colors and flavors to serve multinational food companies demanding single-source solutions for clean-label reformulations; Döhler's December 2024 launch of its Tastecraft platform for freeze-dried fruit ingredients in North America and Europe exemplifies this strategy.

Scale players like Van Drunen Farms and Chaucer Foods leverage multi-site production footprints. Van Drunen operates facilities in Serbia and the US to amortize fixed costs across high-volume contracts and offer supply-chain redundancy that smaller processors cannot match. White-space opportunities exist in organic certification and direct-to-consumer channels: Poland's Lioforte and emerging brands are targeting online retail in high-penetration markets where digital-native consumers accept premium pricing for provenance transparency and subscription-based delivery models. Emerging disruptors include contract manufacturers offering toll-processing services that enable food brands to launch freeze-dried SKUs without capital investment, and Eastern European processors leveraging lower labor costs and proximity to agricultural sourcing regions to undercut Western European pricing.

Technology adoption is bifurcating the market: heat-pump-assisted freeze-dryers and hybrid microwave-vacuum systems reduce cycle times from 24 hours to 16 hours while cutting energy consumption by 25-30%, improving unit economics for mid-tier processors competing on price with spray-dried and air-dried alternatives, Technology adoption is bifurcating the market: heat-pump-assisted freeze-dryers and hybrid microwave-vacuum systems reduce cycle times from 24 hours to 16 hours while cutting energy consumption by 25-30%, improving unit economics for mid-tier processors competing on price with spray-dried and air-dried alternatives, but capital requirements exceeding million-dollar per line limit adoption to established players in Germany, the Netherlands, and Sweden. The EU's Corporate Sustainability Reporting Directive (CSRD) is creating compliance advantages for large processors with in-house ESG teams and energy-efficient equipment.

Europe Freeze-Dried Fruits And Vegetables Industry Leaders

-

Chaucer Foods Ltd

-

European Freeze Dry

-

Van Drunen Farms

-

GreenField Sp. z o.o. Sp. k.

-

Paradise Fruits Solutions GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Freeze‑dried fruits and vegetables from global suppliers, including several serving European markets, were showcased at Food Ingredients Europe (FIE) 2024 in Frankfurt, featuring products like pineapples, mangoes, strawberries, broccoli, and peas.

- August 2024: Thrive Freeze Dry, a leading manufacturer of freeze-dried products, has entered into a definitive agreement to acquire Paradiesfrucht GmbH, a global freeze dryer based in Germany. This acquisition will enhance Thrive's manufacturing capabilities and presence in Europe, expand its freeze-dried pet product offerings in the European market, and strengthen its position as a leader in the fast-growing freeze-dried food industry.

- February 2024: Paradise Fruits Solutions expanded its product portfolio by launching instant Smoothee with tropical flavors and Savory drops with CBD. According to the company claim, Smoothee Drops are made from freeze-dried pure fruit, or combined with yogurt or vegetables, with or without added sugar.

Europe Freeze-Dried Fruits And Vegetables Market Report Scope

Freeze-drying fruit and vegetables is a technique of preserving fresh produce so that it can be shelf-stable and last longer without adding additives. The Europe Freeze-Dried Fruits and Vegetables Market is Segmented by Product Type (Fruits and Vegetables), Form (Powder/Granules, Flakes, and More), Nature (Organic and Conventional), End-User (Foodservice/HoReCa, Food Processing, and Retail), and Geography (United Kingdom, Germany, France, Spain, Italy, Netherlands, Belgium, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

By Product Type

| Fruits | Strawberry |

| Raspberry | |

| Pineapple | |

| Apple | |

| Mango | |

| Others | |

| Vegetables | Pea |

| Corn | |

| Carrot | |

| Potato | |

| Mushroom | |

| Others |

By Form

| Powder/Granules |

| Chunks/Pieces |

| Flakes |

By Nature

| Organic |

| Conventional |

By End-User

| Foodservice/HoReCa | |

| Food Processing | Breakfast Cereals |

| Soups and Snacks | |

| Ice Creams and Desserts | |

| Bakery and Confectionery | |

| Others | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Others |

By Country

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Belgium |

| Sweden |

| Poland |

| Rest of Europe |

| By Product Type | Fruits | Strawberry |

| Raspberry | ||

| Pineapple | ||

| Apple | ||

| Mango | ||

| Others | ||

| Vegetables | Pea | |

| Corn | ||

| Carrot | ||

| Potato | ||

| Mushroom | ||

| Others | ||

| By Form | Powder/Granules | |

| Chunks/Pieces | ||

| Flakes | ||

| By Nature | Organic | |

| Conventional | ||

| By End-User | Foodservice/HoReCa | |

| Food Processing | Breakfast Cereals | |

| Soups and Snacks | ||

| Ice Creams and Desserts | ||

| Bakery and Confectionery | ||

| Others | ||

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Country | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Poland | ||

| Rest of Europe | ||

Key Questions Answered in the Report

Which product type is expanding fastest?

Vegetables are forecast to grow 7.81% annually as processors hedge against fresh-supply volatility and leverage their higher protein content in plant-based meals.

Why are chunks and pieces gaining traction in premium products?

Visible fruit and vegetable inclusions enhance texture and shelf appeal, letting brands command price premiums in cereals, yogurts, and ice creams.

How does online retail influence market dynamics?

With most of the EU internet users shopping online, digital channels allow brands to bypass supermarket gatekeepers, expand margins, and reach niche consumer segments rapidly.

Which European country will register the fastest market growth?

Spain is expected to post a 7.17% CAGR through 2031 as drought-related crop challenges shift processors toward shelf-stable freeze-dried vegetables.

Page last updated on: