Processed And Frozen Fruits Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

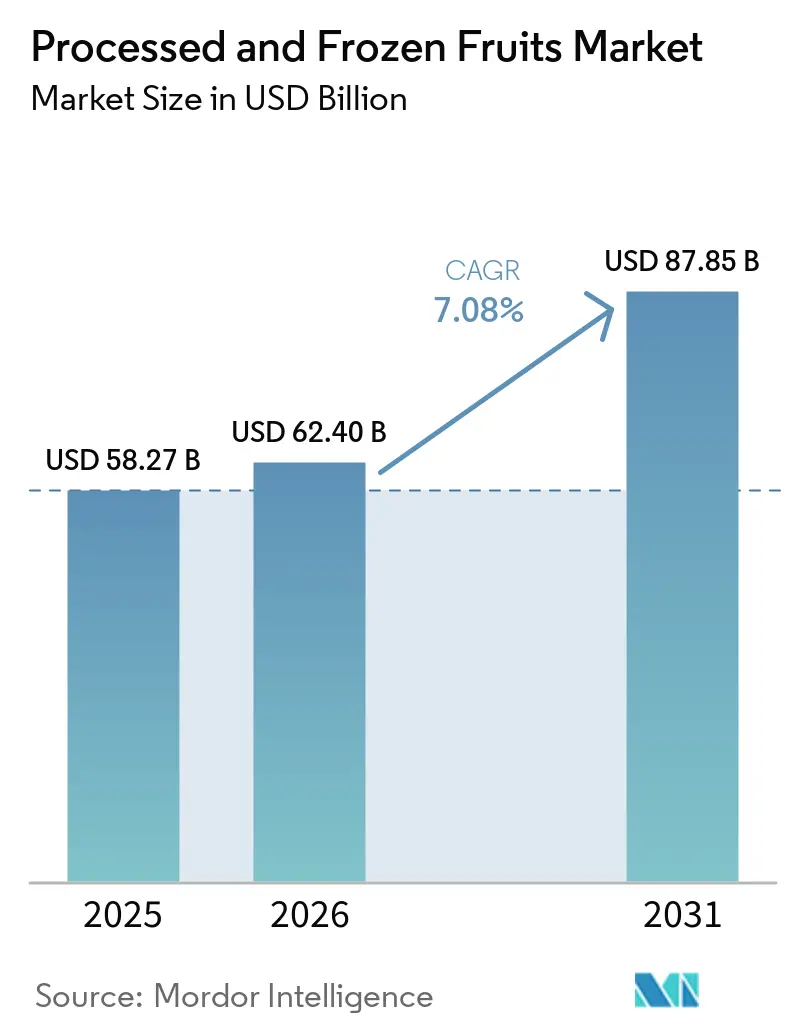

| Market Size (2026) | USD 62.40 Billion |

| Market Size (2031) | USD 87.85 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

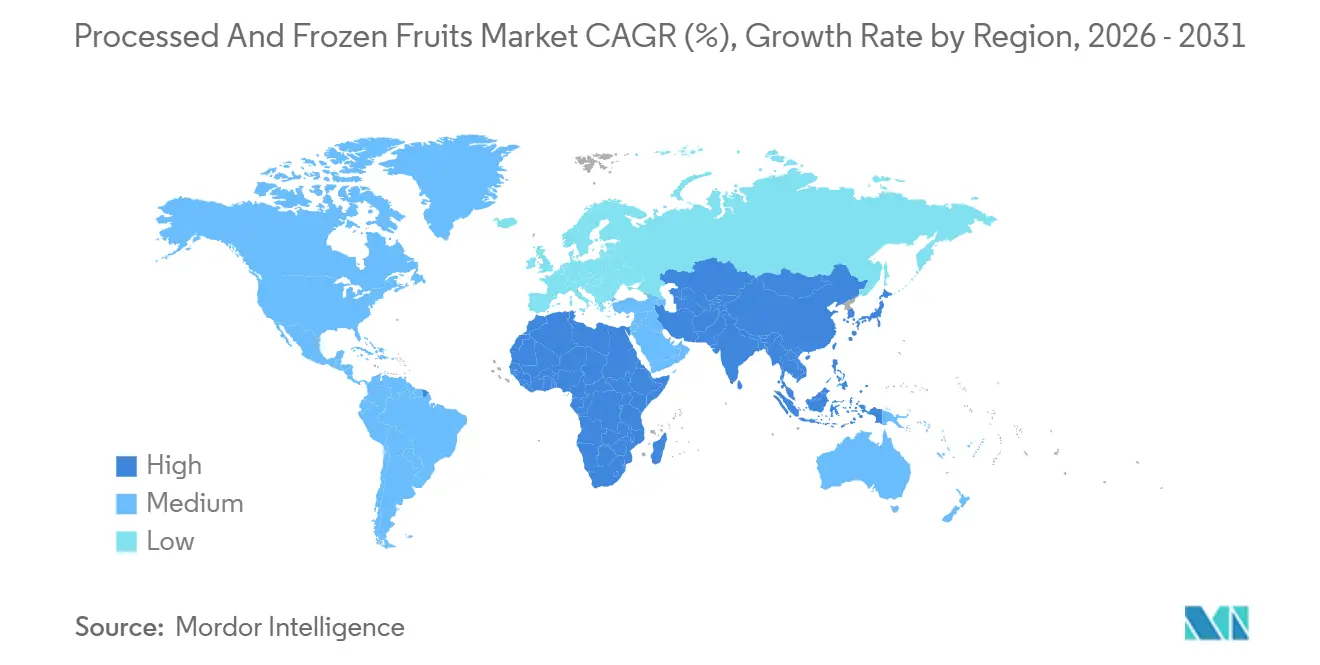

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Processed And Frozen Fruits Market Analysis by Mordor Intelligence

The Processed and Frozen Fruits Market is anticipated to grow from USD 58.27 billion in 2025 to USD 62.40 billion in 2026, reaching USD 87.85 billion by 2031, with a CAGR of 7.08% during the forecast period. This growth is driven by increasing consumer demand for convenient, nutritious fruit products with extended shelf life, aligning with modern lifestyles and changing dietary preferences. Rising health awareness and recognition of the nutritional benefits of fruits are prompting consumers to opt for preserved fruit products that ensure year-round availability while maintaining quality and nutritional value. Additionally, the growing preference for clean-label, minimally processed, and naturally preserved foods is boosting the adoption of processed and frozen fruit products, as consumers increasingly prioritize ingredient transparency and healthier food options.

Key Report Takeaways

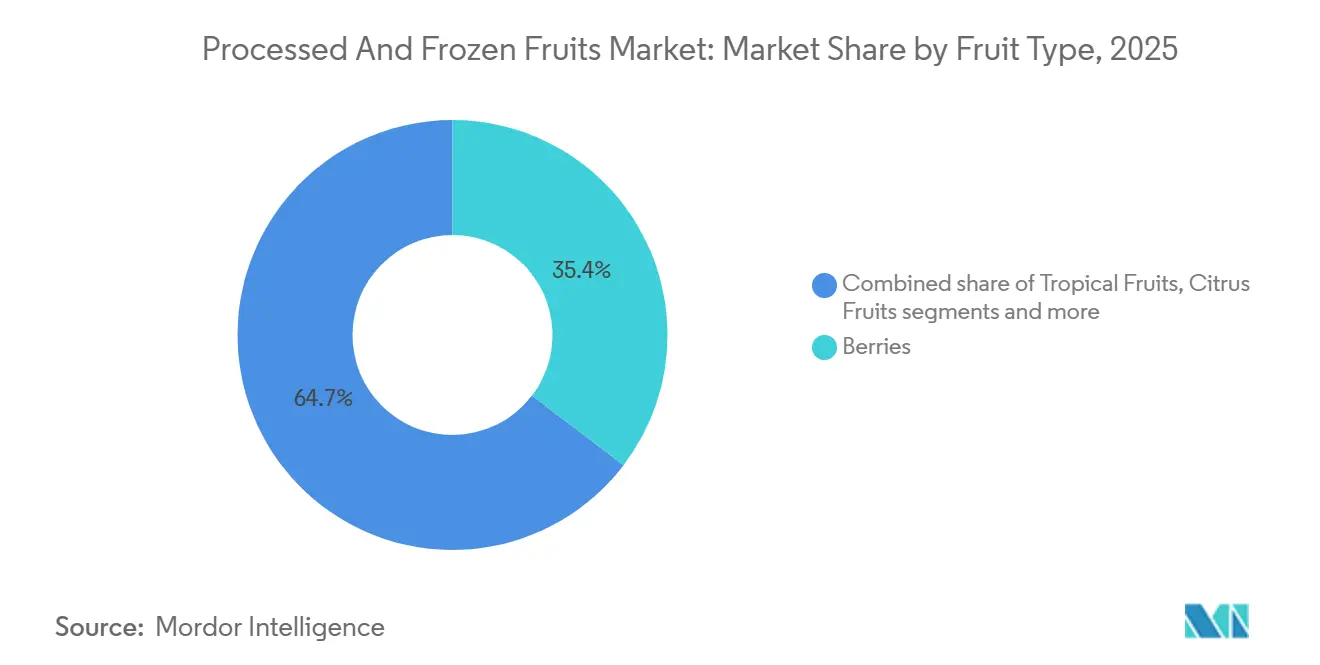

- By fruit type, berries led with 35.35% share in 2025, and tropical fruits are forecast to grow at a 7.69% CAGR through 2031.

- By processing type, canned fruits held 29.14% share in 2025, and freeze-dried fruits are projected to expand at an 8.03% CAGR through 2031.

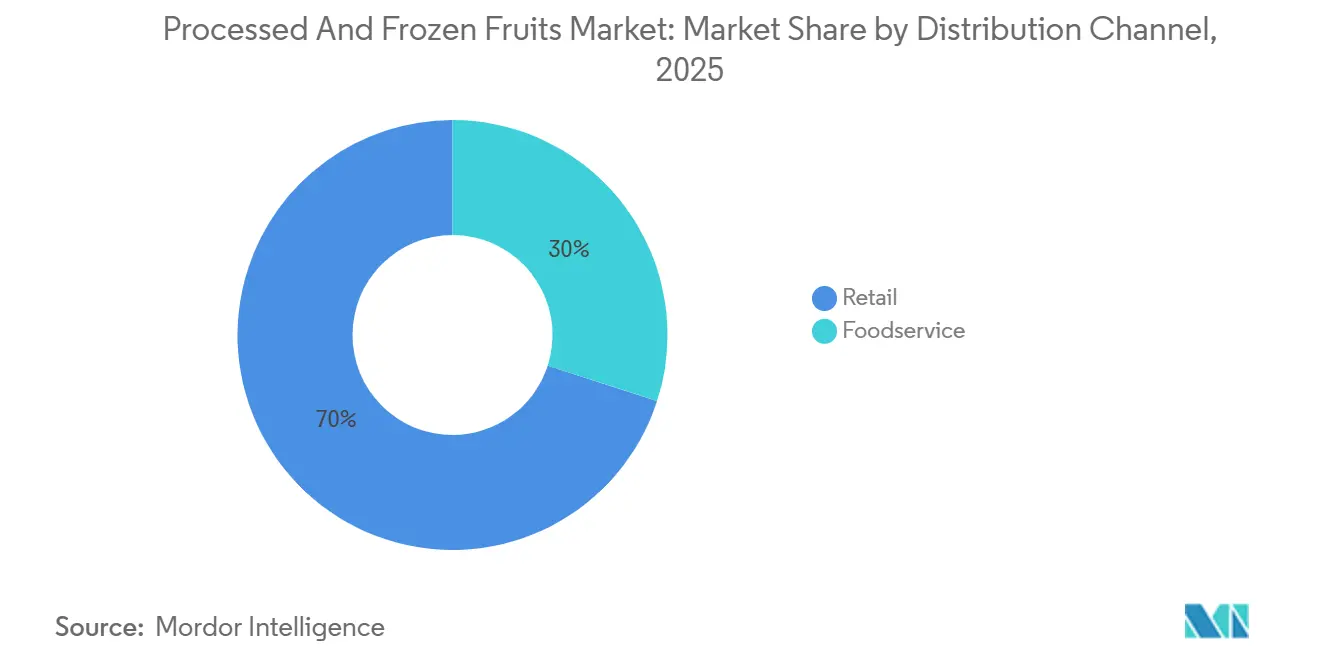

- By distribution channel, retail accounted for 70.03% share in 2025, and foodservice is projected to grow at a 7.93% CAGR through 2031.

- By geography, North America held 41.38% share in 2025, and Asia-Pacific is projected to grow at an 8.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Processed And Frozen Fruits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and wellness-oriented consumption | +1.8% | Global, with North America and Western Europe leading adoption | Short term (≤ 2 years) |

| Busy lifestyles and dual-income households | +1.5% | North America, Europe, urban Asia-Pacific core | Short term (≤ 2 years) |

| Increasing popularity of clean-label and minimally processed fruit | +1.2% | North America, Western Europe, spill-over to Asia-Pacific | Medium term (2–4 years) |

| Advancements in freezing and processing technologies | +1.0% | Global, led by Asia-Pacific and North America | Medium term (2–4 years) |

| Increasing consumer interest in exotic, tropical, and mixed fruit varieties | +0.6% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Growing demand for year-round availability of seasonal fruits | +0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness and wellness-oriented consumption

Rising health consciousness and wellness-oriented consumption trends are driving the growth of the market as consumers increasingly prioritize nutrient-rich, natural, and functional foods in their daily diets. Growing awareness of the health benefits associated with regular fruit consumption, including vitamins, minerals, dietary fiber, and antioxidants, is encouraging consumers to incorporate fruits into their eating habits year-round. Processed and frozen fruits are gaining popularity due to their convenience, as they provide easy access to nutritious fruit products while preserving much of their nutritional value and extending shelf life. This trend is evident across major fruit-consuming markets. For example, according to the Federal Office for Agriculture and Food (BLE), apples remained the most popular fruit among German consumers, with per capita consumption reaching approximately 21.2 kilograms in 2024/2025 [1]Source: Federal Office for Agriculture and Food (BLE), "Per capita consumption of fruit in Germany", ble.de. Bananas were the most consumed tropical fruit, with consumption of around 12 kilograms per person during the same period.

Busy lifestyles and dual-income households

Busy lifestyles and the increasing prevalence of dual-income households are influencing consumer behavior worldwide. As individuals face demanding work schedules and time constraints, there is a growing preference for convenient food options that minimize preparation time while maintaining nutritional value. Processed and frozen fruits provide a practical solution by offering ready-to-use, easy-to-store products with longer shelf lives compared to fresh fruits. These products enable consumers to incorporate healthy food choices into their daily routines with minimal effort. Additionally, the rising participation of women in the workforce and the growing number of households with multiple income earners are further reducing the time available for food preparation and grocery shopping, driving demand for processed and frozen fruit products. For example, according to the Ministry of Internal Affairs and Communications, approximately 13.3 million households in Japan were dual-income households in 2025 [2]Source: Ministry of Internal Affairs and Communications, "Number of dual income households Japan", soumu.go.jp .

Increasing popularity of clean-label and minimally processed fruit

The rising demand for clean-label and minimally processed fruit products is driven by consumers' growing focus on ingredient transparency, food quality, and nutritional value. Modern consumers are paying closer attention to product labels, preferring foods with recognizable ingredients, fewer additives, and minimal artificial preservatives. This change in purchasing behavior is prompting manufacturers to develop processed and frozen fruit products that maintain the natural qualities of fresh fruits while ensuring product safety and shelf life. Frozen fruits, in particular, are gaining from this trend as advanced preservation methods enable them to retain their natural flavor, texture, color, and nutrient content without extensive processing. Concerns about artificial ingredients and a stronger preference for natural, wholesome foods are further boosting the demand for clean-label fruit products.

Advancements in freezing and processing technologies

Advancements in freezing and processing technologies are driving the growth of the processed and frozen fruits market by enhancing product quality, extending shelf life, and improving operational efficiency across the value chain. Modern preservation methods allow fruits to better retain their natural flavor, texture, color, and nutritional content compared to traditional processing techniques, making these products more attractive to health-conscious consumers. Innovations such as freeze-drying and advanced dehydration techniques minimize nutrient loss while ensuring product stability during storage and transportation. These technological advancements also help reduce food waste by extending product usability and ensuring the year-round availability of seasonal fruits. Additionally, automation, artificial intelligence, sensor-based quality control systems, and advanced cold-chain monitoring technologies enable manufacturers to improve production consistency, reduce processing losses, and uphold high food safety standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for fresh, locally sourced produce | -0.8% | North America, Western Europe | Short term (≤ 2 years) |

| Fluctuations in raw fruit availability due to seasonal variations | -0.9% | Global, especially South America and Asia-Pacific sourcing regions | Short term (≤ 2 years) |

| Stringent food safety, labeling, and import/export regulations | -0.7% | Europe, North America, Asia-Pacific | Medium term (2–4 years) |

| Price volatility of fruits caused by weather uncertainties | -0.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer preference for fresh, locally sourced produce

Consumer preference for fresh and locally sourced produce continues to act as a significant restraint on the growth of the processed and frozen fruits market. Many consumers associate freshness with better taste, texture, nutritional value, and overall product quality, leading to a perception that fresh fruits are more natural and healthier than processed alternatives. This preference creates a structural limitation on the market penetration of processed and frozen fruit products, particularly among consumers who prioritize farm-to-table consumption and minimally processed foods. The growing interest in local food systems, seasonal produce, and direct sourcing from farmers further drives demand for fresh fruits, reducing the adoption of preserved fruit formats. Additionally, increasing awareness of food origin, sustainability, and product authenticity has led consumers to favor locally grown fruits, which are often viewed as fresher and less processed.

Fluctuations in raw fruit availability due to seasonal variations

Seasonal variations and climate dependency significantly impact the availability of raw fruits, posing a major challenge for the processed and frozen fruits market. The industry's reliance on a steady supply of high-quality fruits makes it susceptible to seasonal harvesting cycles, unpredictable weather conditions, droughts, floods, heatwaves, frost, and other climate-related disruptions. These factors can lead to supply shortages, inconsistent raw material quality, and procurement difficulties for processors. Additionally, crop diseases, pest infestations, and shifting environmental conditions further affect fruit yields and availability, creating uncertainties throughout the supply chain. Such fluctuations complicate the maintenance of stable production volumes, inventory levels, and long-term supply agreements. Seasonal constraints may also drive up sourcing costs as manufacturers turn to alternative suppliers or import fruits from other regions to sustain operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fruit Type: Berries Anchor Volume While Tropical Lead Growth

Berries accounted for a 35.35% share of the processed and frozen fruits market in 2025, driven by their high nutritional value, strong consumer preference, and increasing popularity among health-conscious consumers. This segment continues to lead due to growing awareness of antioxidant-rich and vitamin-rich fruits that promote healthy lifestyles and wellness-focused dietary habits. Berries are widely regarded as premium and naturally nutritious fruits, which has bolstered their demand in processed and frozen formats. Their compatibility with freezing technologies helps preserve their natural flavor, texture, color, and nutritional properties over extended periods, ensuring year-round availability and mitigating seasonal limitations. Additionally, the rising demand for convenient, ready-to-use fruit products with longer shelf lives has significantly supported the growth of the berries segment.

Tropical fruits are projected to grow at a CAGR of 7.69% between 2026 and 2031, representing the fastest growth within the fruit-type segment of the processed and frozen fruits market. This growth is attributed to increasing consumer preference for exotic, flavorful, and nutrient-rich fruits, coupled with the demand for year-round availability of tropical fruit products in processed and frozen formats. Tropical fruits such as bananas, mangoes, pineapples, papayas, and guavas are gaining popularity due to their natural sweetness, high vitamin and fiber content, and alignment with healthy and refreshing consumption trends. For example, according to the Food and Agriculture Organization (FAO), global tropical fruit production remained robust in 2024, with bananas leading at 139.41 million metric tons, underscoring the substantial raw material availability supporting processed and frozen tropical fruit production.

By Processing Type: Canned Stability Anchors Base While Freeze-Dried Sets the Pace

Canned fruits accounted for a 29.14% market share in 2025, driven by their extended shelf life, year-round availability, and strong consumer preference for convenient fruit preservation formats. This segment continues to dominate due to the rising demand for ready-to-consume and easily storable fruit products that retain quality and usability over long periods. Canning technology preserves the taste, texture, and nutritional value of fruits while minimizing spoilage and food waste, making canned fruits a dependable choice for both consumers and large-scale food supply chains. Additionally, the increasing demand for packaged and shelf-stable food products has significantly supported the segment's growth, particularly among consumers prioritizing convenience and reduced preparation time. The affordability and widespread availability of canned fruits, compared to certain fresh fruit varieties, have further strengthened their market penetration.

Freeze-dried fruits are projected to grow at a CAGR of 8.03% between 2026 and 2031, driven by increasing consumer demand for nutritious, lightweight, and long shelf-life fruit products. This segment is gaining momentum due to the growing preference for minimally processed foods that retain the natural flavor, texture, color, and nutritional content of fresh fruits. Freeze-drying technology effectively preserves vitamins, antioxidants, and other essential nutrients compared to many conventional preservation methods, making freeze-dried fruits particularly appealing to health-conscious consumers. Furthermore, the rising popularity of clean-label, natural, and plant-based food products is boosting demand for freeze-dried fruit options, as consumers increasingly seek products with fewer additives and preservatives.

By Distribution Channel: Retail Dominates, Foodservice Accelerates

The retail segment accounted for 70.03% of the market in 2025, driven by strong consumer demand for convenient, packaged, and easily accessible fruit products available through various retail formats. This segment continues to lead due to the increasing availability of processed and frozen fruits across supermarkets, hypermarkets, convenience stores, specialty food outlets, and online retail platforms, which enhance consumer reach and product visibility. Factors such as urbanization and evolving consumer lifestyles have significantly contributed to the preference for ready-to-use fruit products with longer shelf lives, conveniently purchased during routine shopping. Additionally, the growing demand for healthy snacking and nutritious food options has prompted retailers to expand their processed and frozen fruit product offerings, including premium, organic, and clean-label options.

The foodservice segment is projected to grow at a CAGR of 7.93% from 2026 to 2031, driven by the increasing use of processed and frozen fruits in restaurants, cafés, hotels, and quick-service restaurants. This growth is fueled by rising consumer demand for convenient, nutritious, and fruit-based menu options, encouraging foodservice operators to integrate processed and frozen fruits into their operations for consistency, efficiency, and year-round availability. These products enable foodservice establishments to reduce preparation time, minimize food waste, and maintain standardized quality, making them ideal for large-scale commercial food preparation. Furthermore, the growing popularity of healthy eating trends, fruit-based beverages, desserts, and plant-based dietary preferences is bolstering demand within the foodservice sector.

Geography Analysis

North America held a 41.38% share of the processed and frozen fruits market in 2025, driven by strong consumer demand for convenient, packaged, and long shelf-life fruit products. This growth is supported by the region’s highly developed retail and cold-chain infrastructure. The market benefits from increasing health-conscious consumption trends, a rising preference for ready-to-use frozen fruits, and widespread adoption of processed fruit products across households and commercial food operations. Additionally, the growing demand for nutritious and preservative-free fruit products is fostering continuous product innovation in the region. According to the Observatory of Economic Complexity (OEC), the United States was the world’s leading importer of frozen fruits in 2024, with imports valued at USD 1.31 billion, underscoring the region’s strong consumption and import demand for processed and frozen fruit products [3]Source: Observatory of Economic Complexity (OEC), " Frozen Fruits and Nuts", oec.world.

Asia-Pacific is projected to grow at a CAGR of 8.16% between 2026 and 2031, fueled by rapid urbanization, evolving dietary habits, and increasing demand for convenient and nutritious food products. The region is experiencing robust growth in the consumption of processed and frozen fruits due to the expanding middle-class population, heightened awareness of healthy eating, and a growing preference for packaged food products with extended shelf life. Improvements in cold-chain logistics, food processing capabilities, and retail infrastructure are significantly enhancing the accessibility and availability of processed fruit products. Furthermore, the rising demand for tropical and exotic fruit varieties, coupled with the increasing adoption of modern retail and e-commerce channels, is accelerating market expansion in Asia-Pacific.

Europe, the Middle East, and Africa are witnessing steady growth in the processed and frozen fruits market due to increasing consumer preference for healthy, convenient, and long shelf-life food products. In Europe, strong demand for clean-label, organic, and sustainably processed fruit products is driving market development, supported by advancements in freezing and preservation technologies. The Middle East market is benefiting from a growing reliance on imported processed food products and rising demand for premium packaged fruits due to climatic limitations in local fruit production. Meanwhile, Africa is gradually emerging as a promising market, supported by improving food processing infrastructure, expanding retail penetration, and increasing consumer awareness of convenient fruit preservation formats.

Competitive Landscape

The processed and frozen fruits market is fragmented, with competition driven by global food processing companies, regional fruit processors, frozen food manufacturers, and specialized preservation technology providers. Market participants are focusing on expanding their product portfolios, strengthening supply chain capabilities, and enhancing product quality to maintain competitive positioning. Key players in the market include Dole plc, Del Monte International GmbH, Ardo NV, Rhodes Food Group, and Nature’s Touch Frozen Foods Inc. These companies compete through product innovation, expansion of freezing and preservation capacities, and improvements in sourcing and distribution networks.

Manufacturers are increasingly prioritizing clean-label, organic, minimally processed, and preservative-free fruit products to meet evolving consumer preferences for healthier food options. Companies are also emphasizing sustainable sourcing practices, environmentally friendly packaging solutions, and reducing food wastage to strengthen brand positioning and build consumer trust. Additionally, the rising demand for year-round fruit availability and convenient ready-to-use products is driving efforts to enhance storage efficiency, cold-chain logistics, and processing technologies. Strategic collaborations with growers, distributors, and retail channels are further enabling market participants to improve supply stability and expand their geographic reach in both developed and emerging markets.

Technology is becoming a key competitive differentiator in the processed and frozen fruits market. Companies are increasingly investing in advanced processing and automation solutions to improve operational efficiency and product consistency. Investments in AI-driven quality sorting systems, sensor-based cold-chain monitoring technologies, and automated packing lines are helping manufacturers reduce wastage, optimize processing accuracy, and maintain consistent product quality across large-scale operations. Furthermore, advancements in freezing technologies and digital supply chain management systems are enabling companies to improve shelf life, traceability, and inventory management while reducing operational costs.

Processed And Frozen Fruits Industry Leaders

-

Dole plc

-

Del Monte International GmbH

-

Ardo NV

-

Rhodes Food Group

-

Nature’s Touch Frozen Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Natural Grocers has expanded its private-label product range by introducing five new Natural Grocers Brand Organic Frozen Fruits, including raspberries, strawberries, blueberries, and mixed berries.

- November 2025: Balance of Nature introduced its latest product line, Balance of Nature Freeze-Dried Fruit Snacks. These are made from 100% real fruit, freeze-dried to retain nutrients, color, and flavor, without any preservatives, dyes, or added sugars.

- August 2025: Countree Food has launched a new range of canned fruit balls aimed at both retail and foodservice customers. The product line emphasizes clean-label convenience and consistent quality, catering to diverse applications such as beverages, desserts, baking, and savory dishes.

Global Processed And Frozen Fruits Market Report Scope

Processed and frozen fruits are fruits that are washed, peeled, or chopped, and then flash-frozen at extremely low temperatures shortly after harvest. The processed and frozen fruits market is segmented by fruit type, processing type, distribution channel, and geography. Based on fruit type, the market is segmented into berries, tropical fruits, citrus fruits, pome fruits, stone fruits, and melons and grapes. Based on processing type, the market is segmented into canned fruits, dried fruits, pureed fruits, freeze-dried fruits, and frozen fruits. Based on distribution channel, the market is segmented into retail and foodservice. The retail segment is further segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. Geographically, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Berries |

| Tropical Fruits |

| Citrus Fruits |

| Pome Fruits |

| Stone Fruits |

| Melons and Grapes |

| Canned Fruits |

| Dried Fruits |

| Pureed Fruits |

| Freeze-Dried Fruits |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| Foodservice |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Fruit Type | Berries | |

| Tropical Fruits | ||

| Citrus Fruits | ||

| Pome Fruits | ||

| Stone Fruits | ||

| Melons and Grapes | ||

| By Processing Type | Canned Fruits | |

| Dried Fruits | ||

| Pureed Fruits | ||

| Freeze-Dried Fruits | ||

| By Distribution Channel | Retail | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Foodservice | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of processed fruits by 2031?

The processed fruits market is projected to reach USD 87.8 billion by 2031, up from USD 62.4 billion in 2026, at a 7.1% CAGR over 2026-2031.

Which fruit type leads sales in processed fruits today?

Berries led the category in 2025 with a 35.4% share, supported by strong use in smoothies, dairy, bakery, and frozen formats.

Which processing format is growing fastest through 2031?

Freeze-dried fruits are expected to post the fastest growth, with an 8% CAGR through 2031, supported by better texture, shelf life, and e-commerce fit.

Why is foodservice becoming more important for processed fruit suppliers?

Foodservice is projected to grow at a 7.9% CAGR because restaurants and institutions value consistent portions, lower prep time, and stable cold-chain supply.

Page last updated on: