India Frozen Traditional Meals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

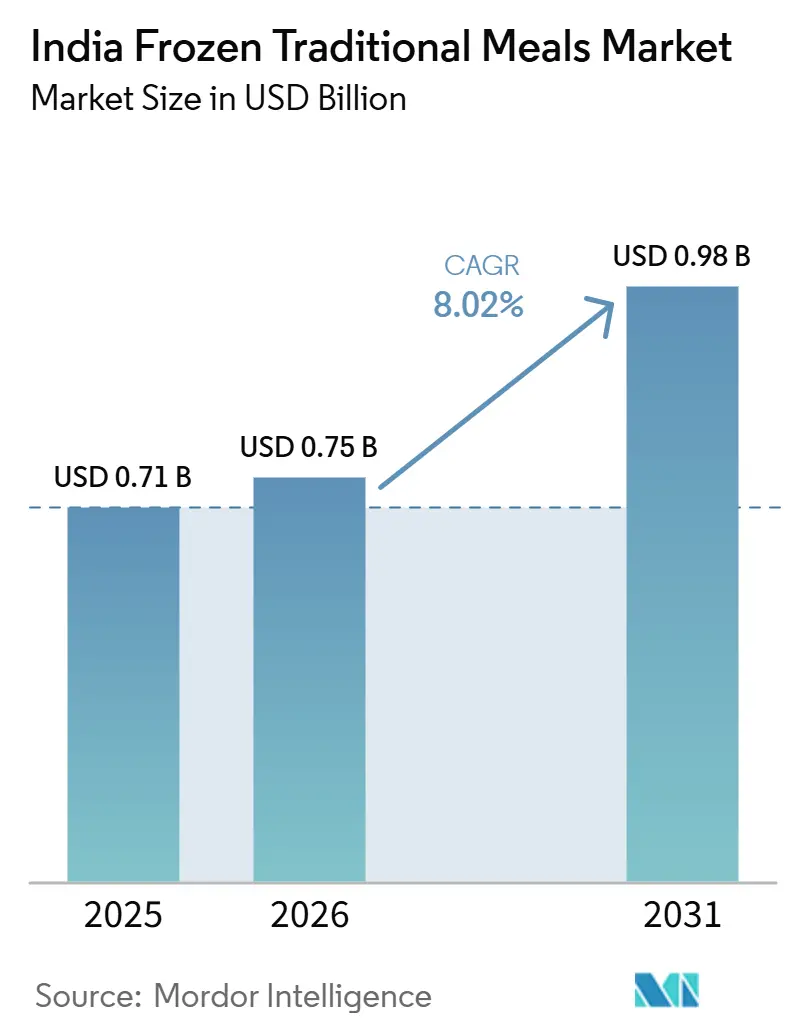

| Base Year Market Size (2025) | USD 0.71 Billion |

| Market Size (2026) | USD 0.75 Billion |

| Market Size (2031) | USD 0.98 Billion |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

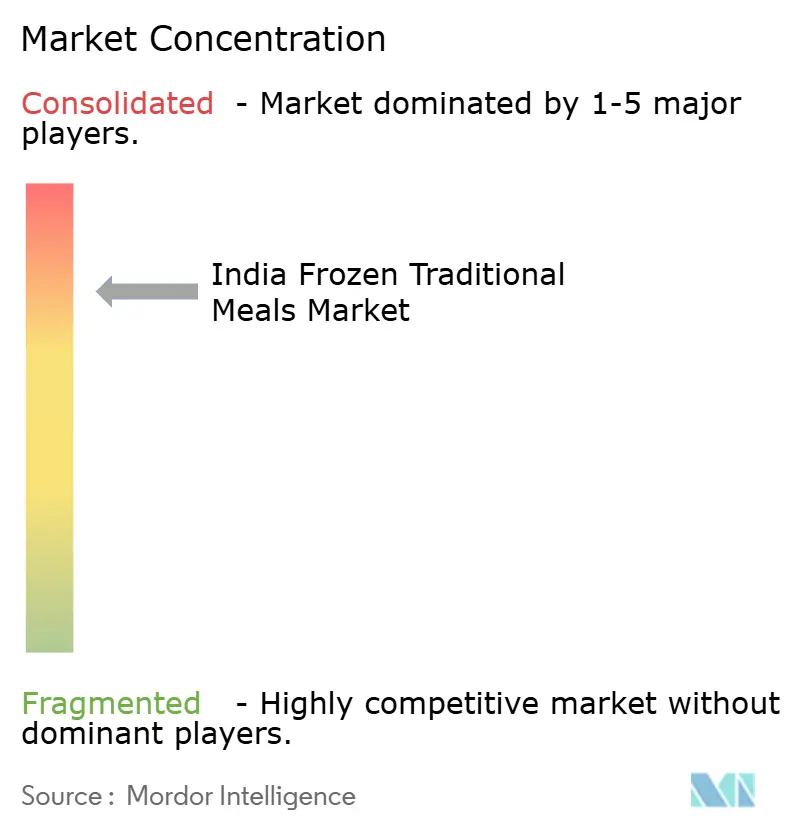

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Frozen Traditional Meals Market Analysis by Mordor Intelligence

The India frozen traditional meals market size is expected to increase from USD 0.71 billion in 2025 to USD 0.75 billion in 2026 and reach USD 0.98 billion by 2031, growing at a CAGR of 8.02% over 2026-2031. The India frozen traditional meals market is moving from occasional convenience use toward more routine household consumption in urban centers, supported by rising female workforce participation, the spread of nuclear households, and stronger quick-commerce access. Demand in the India frozen traditional meals market is shaped by a clear preference for familiar regional dishes instead of generic frozen food, which keeps authenticity central to product design and brand positioning. The India frozen traditional meals market is also seeing a wider product push beyond core gravies and parathas, which is opening room for rice meals, thali formats, and regional cuisine lines. Organized players in the India frozen traditional meals market are strengthening their position through cold-chain investment, modern trade presence, and packaging choices that improve visibility and ease of use. At the same time, the India frozen traditional meals market still faces uneven cold storage access outside major metros and a lasting consumer bias toward freshly prepared food, which keeps growth concentrated in better-served cities.

Key Report Takeaways

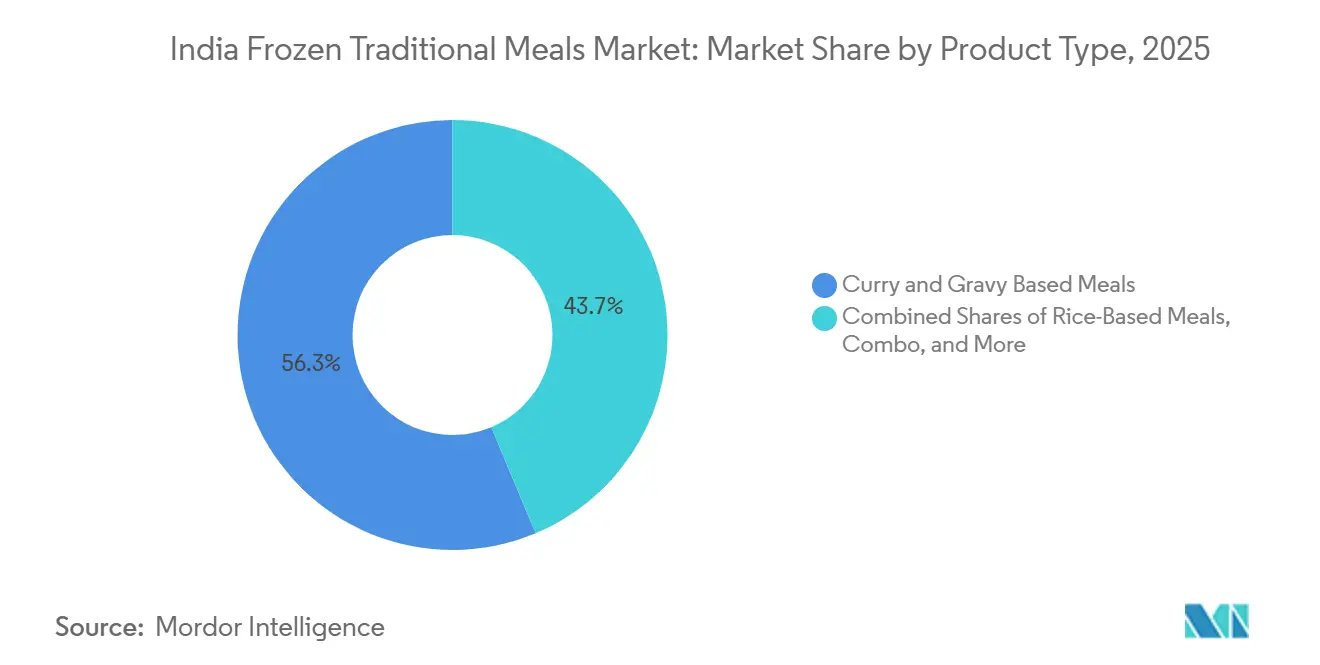

- By product type, Curry and Gravy Based Meals held 56.32% of the India frozen traditional meals market share in 2025, while Rice-Based Meals are projected to grow at a 9.78% CAGR through 2031.

- By cuisine type, North Indian Meals accounted for 42.38% of the India frozen traditional meals market size in 2025, while Western Indian Meals are forecast to expand at a 10.11% CAGR through 2031.

- By packaging type, Retort and Microwaveable Trays held a 45.32% share in 2025, while Boxes and Cartons are projected to grow at a 9.96% CAGR through 2031.

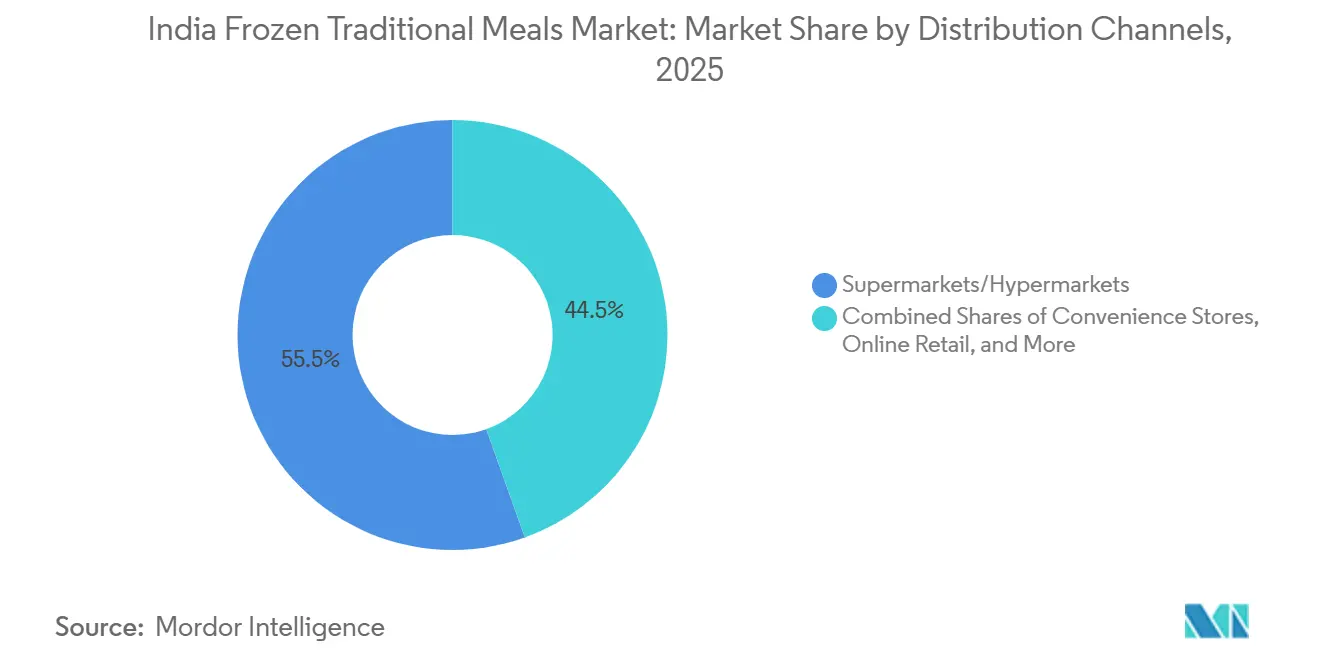

- By distribution channel, Supermarkets/Hypermarkets held 55.47% share in 2025, while Online Retail Channels is projected to expand at a 10.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Frozen Traditional Meals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Regional Indian Meals in Convenient Formats | +1.5% | National; intensity concentrated in Tier 1 cities (Mumbai, Delhi, Bengaluru, Hyderabad) | Medium term (2-4 years) |

| Expansion of Organized Retail and Quick-Commerce Platforms | +1.8% | National; early gains in metro and Tier 1 cities | Short term (≤ 2 years) |

| Increasing Innovation in Frozen Indian Cuisine | +1.2% | National; premium uptake concentrated in Bengaluru, Mumbai, Delhi | Medium term (2-4 years) |

| Growing Demand from Students and Young Professionals | +1.0% | National; skewed toward university cities and IT employment hubs | Short term (≤ 2 years) |

| Expansion of Foodservice and Institutional Demand | +0.8% | National; accelerating in cloud kitchen hubs (Bengaluru, Pune, Hyderabad) | Medium term (2-4 years) |

| Increasing Disposable Income and Premium Food Consumption | +0.9% | National; concentrated in Tier 1 and emerging Tier 2 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Regional Indian Meals in Convenient Formats

The India frozen traditional meals market is benefiting from stronger demand for regional dishes that save time without losing familiarity. Consumers are increasingly choosing products that match everyday Indian meal habits, which is keeping local flavor profiles at the center of category growth. Demand is no longer limited to North Indian meals, and brands are widening portfolios toward South Indian and Western Indian formats. This demand is increasing, owing to the rising working population. According to the World Bank data from 2025, the total labor force in India was 617.62 million[1]Source: World Bank, " Total Labor Force in India", data.worldbank.org. This broadening demand is pushing companies to map local taste preferences more carefully across cities and consumer groups. As a result, innovation in the Indian frozen traditional meals market is becoming more cuisine-specific and less dependent on standard frozen food formats.

Expansion of Organized Retail and Quick-Commerce Platforms

The India frozen traditional meals market is gaining from better access through organized retail and quick-commerce channels in dense urban areas. Dedicated freezer sections in modern trade improve product discovery, while rapid delivery makes frozen purchases easier for households that do not plan large weekly stock-ups. This channel shift reduces one of the main barriers to trial, because consumers can buy frozen meals as needed instead of building large freezer inventories at home. It also supports repeat buying, especially for single-serve and small family packs that fit urban routines. In practice, the India frozen traditional meals market is becoming easier to access at the point of need, which supports both trial and regular use.

Increasing Innovation in Frozen Indian Cuisine

Product innovation is improving the fit between traditional Indian dishes and frozen meal formats in the India frozen traditional meals market. IQF processing and retort packaging have made it easier to preserve texture, taste, and shelf stability in ways that were harder to achieve earlier. This is especially relevant for rice dishes, gravies, and multi-component meals that require better heat performance after storage. Companies are also investing in more region-specific products, which expands the category beyond a narrow set of staple frozen items. The India frozen traditional meals market is therefore moving toward broader menu depth rather than just broader brand presence.

Growing Demand from Students and Young Professionals

Students and young professionals remain an important demand base for the India frozen traditional meals market because they often face time pressure, limited cooking space, and digital-first buying habits. According to the Press Information Bureau data from 2026, India had only 17 universities and 636 colleges serving about 2.38 lakh students[2]Source: Press Information Bureau (PIB), "India’s Higher Education from Tradition to Transformation", pib.gov.in. Consumption is stronger in major education and employment centers where single-person and shared living formats are more common. Dual-income households add to this demand, because convenient traditional meal options fit better into compressed weekday routines. Urban demand is also more concentrated in cities that combine IT employment, student populations, and stronger modern retail networks. This makes employment density and lifestyle patterns more useful demand indicators for the India frozen traditional meals market than population size alone.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate Cold Chain Infrastructure in Smaller Cities | -1.2% | Tier 2, Tier 3, and rural India | Medium term (2-4 years) |

| Consumer Preference for Freshly Prepared Home-Cooked Meals | -0.8% | National; more pronounced in Tier 2, Tier 3, and older consumer segments | Long term (≥ 4 years) |

| Perception of Lower Nutritional Value | -0.5% | National; concentrated in health-aware urban segments | Medium term (2-4 years) |

| Strict Food Safety and Regulatory Compliance Requirements | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inadequate Cold Chain Infrastructure in Smaller Cities

The India frozen traditional meals market remains heavily concentrated in metro areas because cold-chain coverage outside major cities is still uneven. The Ministry of Food Processing Industries has continued to expand PMKSY support, and the scheme outlay was raised to INR 6,520 crore, which is USD 782 million, through March 2026. IBEF reported that more than 1,100 projects under PMKSY components had been completed as of 2025, which shows clear policy support for post-harvest and cold-chain expansion[3]Source: IBEF Staff, “Over 1,100 Projects Completed Under Pradhan Mantri Kisan SAMPADA Yojana (PMKSY), Benefiting 34 Lakh Farmers Across India,” ibef.org. Even so, the gap between approval and operational last-mile rollout still limits frozen distribution economics in smaller cities. Until project execution improves at the local level, the India frozen traditional meals market will continue to expand faster in the top urban centers than in the broader national footprint.

Consumer Preference for Freshly Prepared Home-Cooked Meals

Consumer preference for freshly prepared meals remains a major demand restraint for the India frozen traditional meals market. Many households still judge food quality through freshness cues such as aroma, texture, and just-cooked flavor, which frozen products cannot fully reproduce. This preference is stronger outside metro areas and among older consumers, which slows conversion from first-time trial to habitual use. Younger urban consumers are more open to frozen formats, but that openness is not yet strong enough to remove the wider cultural bias toward home-cooked food. Because of this, companies in the India frozen traditional meals market need steady brand building and product education rather than relying only on discounts or short-term promotions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Curry Anchors Volume, Rice-Based Formats Set the Growth Pace

Curry and Gravy-Based Meals held 56.32% of the product type mix in 2025, making them the volume anchor of the India frozen traditional meals market. Their position reflects the strong role of gravy-led dishes in everyday Indian eating patterns across cities, households, and income groups. These meals also adapt well to retort and microwave reheating because sauces retain structure more effectively than many dry preparations. That technical fit supports both taste consistency and ease of use after storage. In practical terms, this segment remains the category base for the India frozen traditional meals industry.

Rice-Based Meals are projected to grow at a 9.78% CAGR from 2026 to 2031, making them the fastest-expanding product type. Urban demand is widening for biryani, pulao, and region-specific rice dishes that can work as full meal solutions with limited preparation. Better freezing and reheating methods are helping brands address the long-standing concern that frozen rice loses grain integrity after heating. This improvement matters because texture has often been the main barrier to repeat purchase in rice meals. The India frozen traditional meals market is therefore seeing product mix growth move from core gravies toward more complete heat-and-eat formats.

By Cuisine Type: North Indian Anchors Share, Western Indian Gains Momentum

North Indian Meals held 42.38% share by cuisine type in 2025, giving them the lead position in the India frozen traditional meals market size across cuisine formats. Their scale reflects broad national familiarity with dishes such as dal makhani, paneer butter masala, rajma, and chole. These dishes also travel well across regions because they are already part of mainstream restaurant and household consumption in many cities. Their sauce-based structure further supports consistency after frozen storage and reheating. This combination of familiarity and format fit keeps North Indian meals at the center of category demand.

Western Indian Meals are projected to grow at a 10.11% CAGR from 2026 to 2031, making them the fastest-growing cuisine segment. This growth reflects stronger organized packaging and brand attention around Maharashtrian, Gujarati, and Rajasthani preparations. Demand also benefits from migrant populations in large cities that look for food linked to their home-region tastes. That pattern is commercially meaningful because it creates stable urban demand pockets that broad national data may not fully show. The India frozen traditional meals market is therefore widening its cuisine mix through both regional loyalty and better organized distribution.

By Packaging Type: Retort Trays Lead on Convenience, Boxes Signal Premiumization

Retort and Microwaveable Trays held 45.32% share in 2025, making them the leading packaging format in the India frozen traditional meals market. Their strength comes from simple use, since the same pack can often serve for storage, heating, and serving. This reduces handling steps and fits well with single-serve meals, office consumption, and compact urban kitchens. For brands, trays also support clearer portion control and more reliable product presentation after heating. That practical benefit keeps them central to category growth.

Boxes and Cartons are projected to grow at a 9.96% CAGR from 2026 to 2031, making them the fastest-growing packaging segment. Premium brands are using these formats to improve shelf presence and give more space for ingredient, cuisine, and usage communication. Stronger outer-pack design also helps products stand out in modern trade freezers, where visual competition matters. This format is therefore tied not only to containment but also to brand positioning. The India frozen traditional meals market is using packaging more actively as a tool for premium appeal and regional storytelling.

By Distribution Channels: Supermarkets Command Share, Online Retail Sets the Pace

Supermarkets/Hypermarkets held an 85.47% share of India's frozen traditional meals distribution in 2025, an outsized dominance that reflects organized modern trade's role as the primary environment where consumers first discover, evaluate, and trial frozen meal products. Retail formats operated by chains such as Reliance Retail and DMart provide dedicated freezer sections that improve product visibility, enable price benchmarking, and support in-store impulse purchases. Convenience and Specialty Stores serve a complementary access-point function, particularly in Tier 2 cities and dense urban neighborhoods where hypermarket access is limited; they are the primary frozen traditional meal touchpoint for consumers outside the organized modern-trade footprint.

Online Retail is the fastest-growing distribution channel, projected at a 10.02% CAGR from 2026 to 2031, driven primarily by quick-commerce platforms, Blinkit, Zepto, and Swiggy Instamart that deliver frozen traditional meals within 10-30 minutes of ordering across dense urban markets. India's quick-commerce sector generated a gross order value of USD 7.4 billion (INR 652.8 billion) in FY 2024-25 and is projected to reach USD 18-20 billion (INR 1,587.4-1,763.8 billion) by 2027. The more durable implication of online retail growth is behavioral: quick-commerce eliminates the requirement for consumers to maintain large home-freezer inventories.

Geography Analysis

The India frozen traditional meals market is a single-country market, but demand remains concentrated in a limited set of large urban centers. Mumbai, Delhi NCR, Bengaluru, Hyderabad, Chennai, and Pune account for the dominant share of organized consumption because they combine stronger cold-chain density, deeper modern trade presence, and higher disposable income. Bengaluru and Chennai support strong South Indian meal demand, while Delhi NCR remains a major center for North Indian volumes. The India frozen traditional meals market share is therefore closely linked to where freezer infrastructure and organized retail are already well established. This geographic concentration also aligns with the city clusters where frozen food brands have drawn meaningful investment and rapid delivery coverage.

Quick-commerce density in these cities has changed frozen meals from a planned stock-up purchase into a more flexible top-up purchase. That shift matters because households no longer need to maintain large freezer inventories to participate in the category. It also supports trial for newer formats, including regional meals and premium packs. Reorder cycles become shorter when products can be delivered quickly and stored in smaller home freezer space. For the India frozen traditional meals market, city-level convenience is now shaping consumption as much as product familiarity.

Rier 2 cities such as Jaipur, Indore, Lucknow, Coimbatore, and Nagpur are the next meaningful expansion zone for the India frozen traditional meals market. Their demand base is improving, but cold-chain rollout remains the main constraint on faster penetration. PMKSY support is relevant here, and Uttar Pradesh alone had 27 approved cold chain projects as of 2025. The Ministry of Food Processing Industries also issued a May 2025 expression of interest under the PMKSY cold chain scheme for underserved geographies. As these projects move from approval to operation, Tier 2 demand should become a more material part of the India frozen traditional meals market size.

Competitive Landscape

The India frozen traditional meals market remains highly consolidated, with competition shaped mainly by cold-chain capacity, trusted branding, and broad modern trade access. ITC Limited, through ITC Master Chef and Aashirvaad frozen lines, and MTR Foods, part of Orkla India, hold leading positions through strong retail relationships and product credibility. Scale matters in this category because reliable cold distribution and freezer placement are difficult for smaller players to replicate quickly. Larger companies also have more room to support product trials, broader assortments, and national launches. This keeps leadership concentrated among players that can combine supply chain strength with recognizable food brands.

ITC strengthened its position in February 2025 by acquiring Prasuma, which expanded its frozen portfolio and reinforced cold-chain capability. Orkla India signaled another scale strategy in 2025 by setting aside INR 700 crore, or USD 83.90 million, for further acquisitions as it prepared for an IPO process. Bikaji Foods International approved investment of up to INR 88 crore, or USD 10.50 million, in January 2026 to enter frozen food and bakery manufacturing through Bikaji Bakes Private Limited. These moves show that both established FMCG players and ethnic snack companies view frozen traditional meals as a strategically adjacent category. The India frozen traditional meals market is therefore seeing consolidation through acquisition, adjacency expansion, and capacity building rather than only through price competition.

White-space opportunities remain strongest in sub-regional cuisines where organized national coverage is still thin. Western Indian, eastern Indian, and more localized South Indian formats offer room for specialized players that can build credibility faster than broad portfolio brands. Founder-led companies such as Gits Food Products and Innovative Foods Limited are using regional authenticity and cleaner positioning to carve out smaller but defensible pockets. At the same time, higher regulatory standards can favor better-capitalized companies that already operate with stronger compliance systems. The 2025 FSSAI amendment, effective February 2026, is likely to raise formulation and process demands across the category. This means the India frozen traditional meals market may stay consolidated even as new cuisine niches open up.

India Frozen Traditional Meals Industry Leaders

-

ITC Limited

-

MTR Foods Private Limited

-

Haldiram Snacks Private Limited

-

Bikaji Foods International Limited

-

Godrej Tyson Foods Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Vishnu Bhavan Frozen Foods, backed by the Vishnu Namboothiri Group, launched a premium range of ready-to-eat frozen Kerala snacks, vegetarian curries, meals, and sweets in India. The launch includes products manufactured using preservative-free blast-freezing technology

- April 2026: MTR Foods (Orkla India) launched the MTR Minute Fresh Batter range in Hyderabad, introducing Dosa Batter and Rice Rava Idli Batter in multiple pack sizes. The launch marks MTR's strategic push into chilled, fresh-format convenience foods, leveraging the brand's established South Indian cuisine authority to address the quick-prep consumer segment

- January 2026: Bikaji Foods International's board approved investment of up to INR 88 crore (approximately USD 10.5 million) to enter frozen food and bakery manufacturing through Bikaji Bakes Private Limited, a joint venture with Bakemart's founder. Bikaji will hold a 70% stake in the JV. The move marks Bikaji's first formal expansion into frozen food manufacturing beyond ethnic snacks

India Frozen Traditional Meals Market Report Scope

| Rice-Based Meals |

| Curry and Gravy Based Meals |

| Indian Bread-Based Meals (Parathas) |

| Combo/Thali Meals |

| Others |

| North Indian Meals |

| South Indian Meals |

| Western Indian Meals |

| Other Cuisine Types |

| Retort and Microwaveable Trays |

| Pouches |

| Boxes and Cartons |

| Other Packaging Formats |

| Supermarkets/Hypermarkets |

| Convenience/Specialty Stores |

| Online Retail |

| Other Distribution Channels |

| By Product Type | Rice-Based Meals |

| Curry and Gravy Based Meals | |

| Indian Bread-Based Meals (Parathas) | |

| Combo/Thali Meals | |

| Others | |

| By Cuisine Type | North Indian Meals |

| South Indian Meals | |

| Western Indian Meals | |

| Other Cuisine Types | |

| By Packaging | Retort and Microwaveable Trays |

| Pouches | |

| Boxes and Cartons | |

| Other Packaging Formats | |

| By Distribution Channels | Supermarkets/Hypermarkets |

| Convenience/Specialty Stores | |

| Online Retail | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the current size of frozen traditional meals in India?

The India frozen traditional meals market size stands at USD 0.75 billion in 2026 and is projected to reach USD 0.98 billion by 2031, growing at an 8.02% CAGR over 2026-2031.

Which product category leads sales in frozen traditional meals?

Curry and Gravy Based Meals led the category with 56.32% share in 2025 because these dishes fit Indian eating habits and perform well after reheating.

Which cuisine type is expanding most quickly?

Western Indian Meals are projected to grow at a 10.11% CAGR through 2031 as organized brands expand beyond the core North Indian range.

Why are metro cities still the main demand centers?

Large metros combine better cold-chain coverage, modern trade presence, stronger quick-commerce density, and consumer groups that are more open to convenient meal formats.

Page last updated on: