Market Overview

| Study Period | 2021 - 2031 |

|---|---|

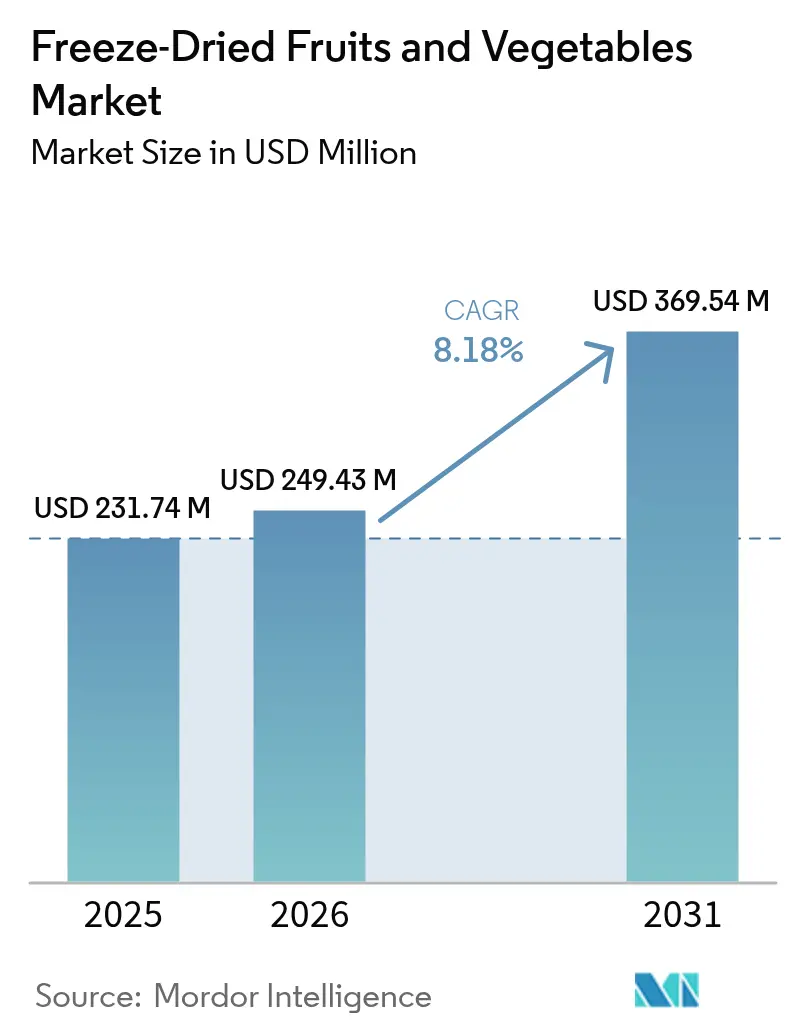

| Market Size (2026) | USD 249.43 Million |

| Market Size (2031) | USD 369.54 Million |

| Growth Rate (2026 - 2031) | 8.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Freeze-Dried Fruits And Vegetables Market Analysis by Mordor Intelligence

The freeze-dried fruits and vegetables market size in 2026 is estimated at USD 249.43 million, growing from the 2025 value of USD 231.74 million, with 2031 projections showing USD 369.54 million, growing at 8.18% CAGR over 2026-2031. Energy-efficient atmospheric systems now cut power consumption by 30% compared with legacy vacuum units, while hybrid ultrasound or infrared modules shorten primary drying time by as much as 70%, lowering per-kilogram costs and broadening commercial uptake. Regulatory pressure is equally pivotal: the United States Department of Agriculture-Environmental Protection Agency (USDA-EPA) National Food Loss and Waste Reduction Strategy, launched in 2024, brands freeze-drying as a priority technology for cutting household waste and salvaging cosmetically imperfect produce. Climate volatility reinforces adoption, as retailers hedge against fresh-produce shortages by carrying shelf-stable berries and tropical fruits that hold color and nutrients for multiple years. These structural and policy drivers together anchor a robust demand outlook for the freeze-dried fruits and vegetables market across meal kits, and emergency rations.

Key Report Takeaways

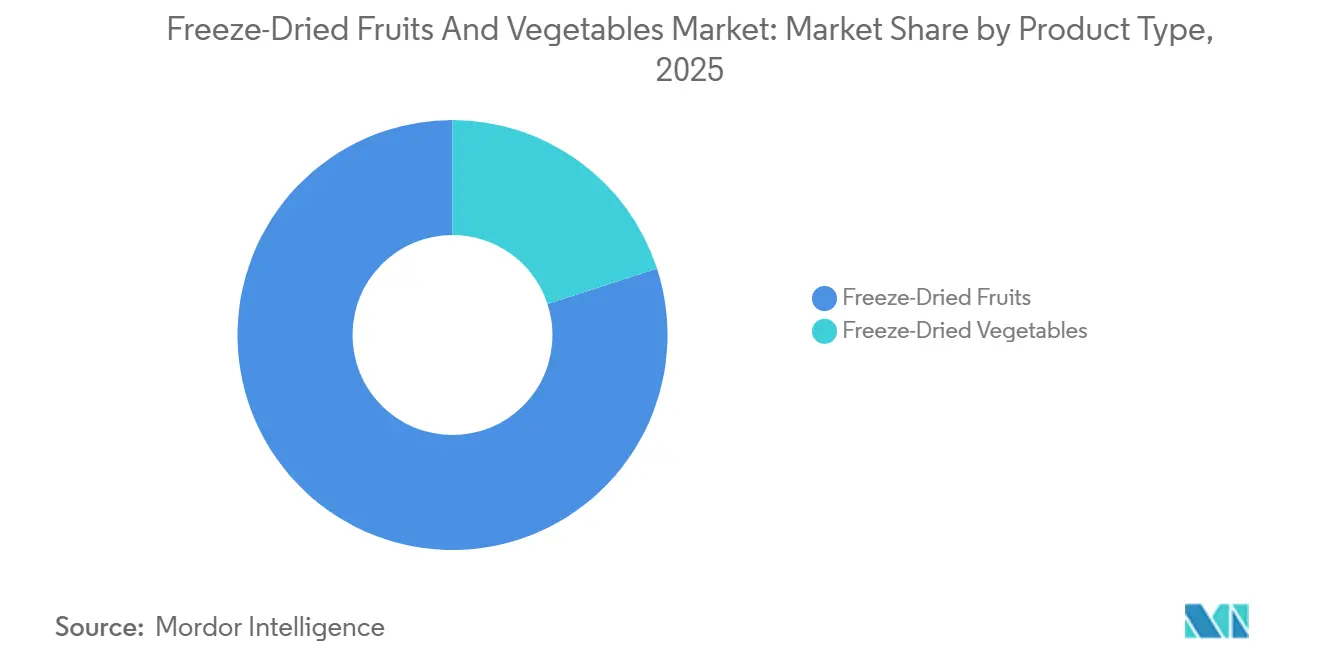

- By product type, freeze-dried fruits captured an 80.01% freeze-dried fruits and vegetables market share in 2025, while freeze-dried vegetables are projected to expand at an 8.71% CAGR through 2031.

- By form, whole or diced items accounted for 78.05% of the freeze-dried fruits and vegetables market size in 2025; powdered and granule formats are forecast to grow at an 8.86% CAGR over 2026-2031.

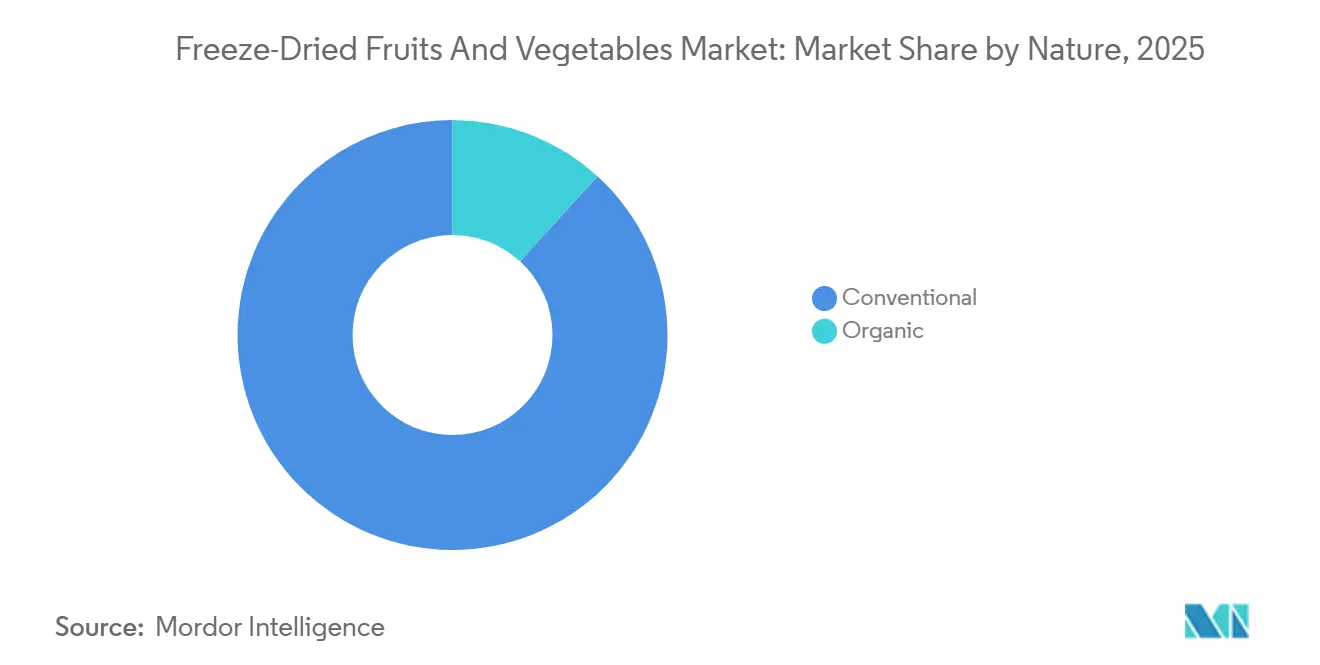

- By nature, conventional products represented 88.21% of 2025 volume, whereas organic lines are on course for a 9.52% CAGR during 2026-2031.

- By distribution channel, supermarkets and hypermarkets held 55.28% of global revenue in 2025, but online retail stores are poised for a 9.73% CAGR thanks to direct-to-consumer subscription models.

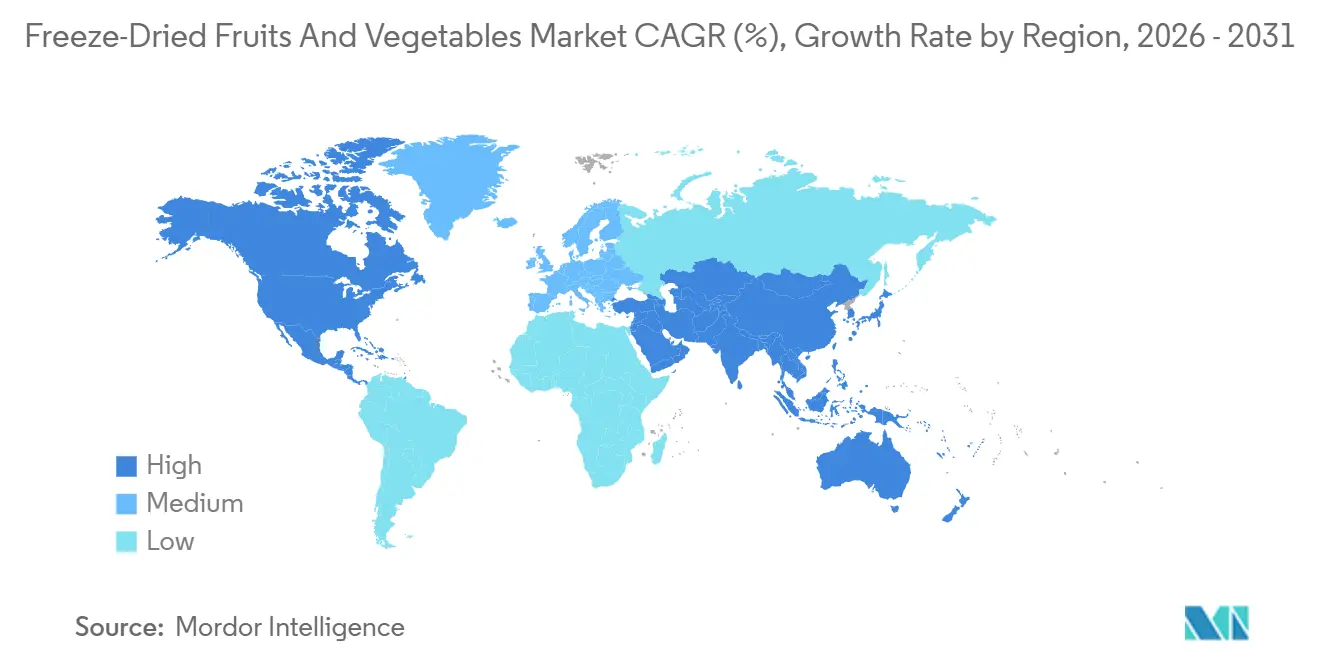

- By geography, North America commanded 35.43% of 2025 value; Asia-Pacific will be the fastest-growing region at 9.35% CAGR, led by China, India, and Japan.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Freeze-Dried Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for convenient, nutrient-rich snacks | +1.2% | Global, with peak penetration in North America and Europe | Medium term (2-4 years) |

| Growth of outdoor, adventure and emergency food channels | +0.9% | North America, Europe, Asia-Pacific (Australia, Japan) | Short term (≤ 2 years) |

| Expansion of e-commerce and D2C distribution | +1.1% | Global, led by North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Year-round availability and food-waste reduction benefits | +0.8% | Global, regulatory push strongest in North America and EU | Long term (≥ 4 years) |

| Hybrid energy-efficient freeze-drying technologies emerge | +0.7% | North America, Europe, Asia-Pacific (China, South Korea) | Long term (≥ 4 years) |

| Social media influence boosting market growth | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient, nutrient-rich snacks

Micronutrient retention remains the category’s signature benefit; vitamin C preservation above 90% surpasses the 50-60% typical of hot-air-dried fruit and underpins premium positioning in grocery aisles. Retail sales of freeze-dried strawberries and raspberries in United States supermarkets increased year-over-year in 2025 as millennials and Gen Z shoppers shifted away from sugar-laden confectionery. The shift is amplified by workplace and travel snacking occasions where shelf-stable, lightweight formats align with on-the-go consumption patterns. Freeze-dried mango and pineapple cubes have captured shelf space in airport convenience stores and corporate vending machines, displacing candy and chips in wellness-focused procurement policies. FDA traceability rules further boost appeal because the low water activity of freeze-dried produce minimizes microbial risk, extending shelf life and easing compliance surpasses the 50-60% typical of hot-air-dried.

Expansion of e-commerce and D2C distribution

Freeze-dried products are tailor-made for parcel networks because they avoid last-mile refrigeration costs. Subscription services such as Thrive Life report that quarterly berry and vegetable shipments yield four to five times the margins of single supermarket sales, while Amazon’s recommendation engine bundles freeze-dried snacks with protein powders, accelerating cross-category discovery. E-commerce also enables micro-segmentation: brands can offer single-origin organic strawberries or heirloom tomato powders that lack the volume to justify supermarket shelf space but command USD 40-60 per kilogram online, where niche audiences self-select through search and social channels. Amazon's algorithmic recommendation engine further amplifies discovery; freeze-dried snacks frequently appear in "Frequently Bought Together" bundles with protein powders and meal-replacement shakes, cross-pollinating customer bases

Year-round availability and food-waste reduction benefits

A 50% national waste-reduction target by 2030 forces United States processors to repurpose surplus or cosmetically imperfect produce, with freeze-drying the most scalable option[1]Source: International Telecommunication Union, "Facts and Figures 2024", itu.int . This regulatory push is mirrored in the EU, where member states must transpose waste-reduction directives into national law by 2027, creating procurement incentives for shelf-stable ingredients in public-sector catering. Year-round availability decouples consumption from harvest seasonality; freeze-dried raspberries and blueberries effectively maintain consistent pricing and quality across all quarters, enabling food manufacturers to lock in annual contracts and hedge against the 30-50% intra-year price swings typical of fresh berry markets. The strategic implication is profound: freeze-drying transforms perishable commodities into storable assets, allowing processors to arbitrage seasonal gluts and smoothing cash flows. For growers, this creates a new off-take channel that absorbs surplus tonnage without depressing fresh-market prices, effectively raising the floor price for premium varieties.

Social media influence boosting market growth

Social media is significantly influencing global demand for freeze-dried fruits and vegetables by shaping consumer perceptions and purchasing behaviors. Influencers and nutritionists, aligned with health trends, highlight these snacks as convenient and nutrient-dense options, resonating with the clean eating movement. The vibrant colors and visual appeal of freeze-dried fruits and vegetables make them popular for viral content, frequently featured in smoothie bowls, yogurt parfaits, and creative lunchbox ideas on platforms like Instagram and TikTok. Brands are increasingly leveraging influencer partnerships and user-generated content to enhance trust and visibility, moving beyond traditional marketing strategies. Additionally, a 2024 survey by the University of Portsmouth revealed that 60% of consumers trusted influencer recommendations, with nearly half of all purchasing decisions influenced by these endorsements[2]Source: University of Portsmouth, “New Research Unveils the ‘Dark Side’ of Social Media Influencers and Their Impact on Marketing and Consumer Behaviour", port.ac.uk.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High capital and energy intensity of freeze-drying plants | -1.3% | Global, acute in high-electricity-cost regions | Long term (≥ 4 years) |

| Consumer preference for fresh produce in price-sensitive areas | -0.9% | Asia-Pacific (excluding Japan, Singapore), South America, Middle East and Africa | Medium term (2-4 years) |

| Climate-driven volatility in premium fruit supply chains | -0.8% | Mediterranean, Central America, Southeast Asia | Short term (≤ 2 years) |

| Limited organic-certified freeze-drying capacity | -0.6% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production costs and capital investment

A baseline industrial freeze-dryer carries a high capital cost and cycle operating costs, with capital amortization accounting for 91-95% of total cost per cycle, creating a steep volume threshold before unit economics turn positive. For comparison, a commercial-scale Parker 6 freeze-dryer processing up to 1,500 pounds of wet product per cycle consumes approximately 998 kilowatt-hours, and matching that output with tabletop units would require 167 machines, underscoring the capital efficiency of scale but also the entry barrier for small and mid-sized processors[3]Source: Parker Freeze Dry, "Energy and time consumption in Freeze Drying", parkerfreezedry.com. Energy costs compound the challenge: freeze-drying ranks among the most energy-intensive food-preservation methods, with specific energy consumption (SEC) ranging from 7.2 to over 10 kilowatt-hours per kilogram of water removed, compared to 1-2 kilowatt-hours for hot-air drying. The long equipment lifespan (20-30 years) and high switching costs lock processors into technology choices, slowing the diffusion of newer, more efficient hybrid systems and perpetuating the cost disadvantage.

Consumer preference for fresh produce in price-sensitive areas

Freeze-dried fruits and vegetables command retail prices higher than fresh equivalents on a per-kilogram basis, and in markets where household food budgets are constrained much of Asia-Pacific (excluding Japan and Singapore), South America, and Middle East and Africa consumers prioritize fresh or minimally processed produce over shelf-stable convenience. Cultural factors reinforce this restraint: in many Asian and Latin American cuisines, texture and moisture content are integral to dish authenticity, and the crisp, lightweight character of freeze-dried vegetables is perceived as inferior or unsuitable for traditional preparations. Even in developed markets, fresh produce benefits from strong health halos and visual appeal in retail displays. The restraint is most binding in the vegetables segment, where lower intrinsic sweetness and fewer snacking occasions reduce the willingness to pay a premium; freeze-dried peas or carrots struggle to compete with frozen or canned alternatives priced.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fruits Dominate, Vegetables Accelerate on Plant-Based Demand

In 2025, freeze-dried fruits captured a commanding 80.01% market share, largely due to their popularity as retail snacks and as key ingredients in cereals, yogurt toppings, and baked goods. The convenience, long shelf life, and retention of nutritional value further contributed to their widespread adoption. Strawberries, raspberries, and pineapples, celebrated for their vibrant colors and high anthocyanin content, made up over half of the volume, especially favored by health-conscious millennials seeking natural and nutrient-rich options. While apples and mangoes were predominantly used as ingredient inputsapple pieces found their way into granola and oatmeal, and mango powder was added to smoothie mixes to cut down on added sugars and align with clean-label trends. Additionally, the growing demand for clean-label and minimally processed foods has bolstered the use of freeze-dried fruits across various applications.

Freeze-dried vegetables are projected to grow at 8.71% annually through 2031, outpacing the overall market. This growth is fueled by plant-based meal kits and emergency-food manufacturers focusing on protein-rich legumes and fiber-dense vegetables. Peas, corn, and carrots, once limited to camping meals and instant soups, are now used in plant-based protein bowls targeting Gen Z consumers who prefer whole-food proteins. Additionally, the vegetable segment's growth reflects geographic diversification, with Asia-Pacific markets driving demand due to higher vegetable consumption, independent of Western snacking trends.

By Form: Powdered Formats Gain as Functional Beverages Pull Ingredients

Whole and diced freeze-dried products captured 78.05% of the market in 2025, serving retail snacking, cereal inclusions, and trail-mix applications where visual appeal and texture drive purchase decisions. A single-serve sachet with freeze-dried mango, spinach, and spirulina illustrates why powders thrive in functional beverages: rapid rehydration, vibrant color, and nutrient retention. This visual equity is particularly valuable in children's snacks, where parents scrutinize ingredient lists and prefer recognizable whole foods over powders that may be perceived as overly processed or adulterated. The form segmentation also maps to distribution channels: whole/diced products dominate supermarket and convenience-store aisles, where impulse purchases and on-the-go consumption favor portion-controlled pouches.

Powdered and granule formats are projected to grow at 8.86% annually through 2031, pulled by functional-beverage manufacturers who prize the instant solubility and concentrated nutrient density of freeze-dried fruit and vegetable powders. A single-serve smoothie sachet with freeze-dried mango, spinach, and spirulina powders rehydrates in under 60 seconds with water or plant milk. It avoids the gritty texture and oxidation browning seen in spray-dried or drum-dried ingredients, while third-party lab data confirms over 90% vitamin C retention, supporting "superfood" claims. Protein-powder formulators are also shifting to freeze-dried inclusions: freeze-dried strawberry and blueberry granules deliver vibrant color and recognizable fruit pieces in shaker bottles, differentiating premium products from commodity whey blends and commanding price premiums over spray-dried fruit powders.

By Nature: Organic Premium Positioning Accelerates

In 2025, conventional freeze-dried products dominated the market, holding an 88.21% share. This dominance stems from a limited pool of certified organic freeze-drying facilities and the USDA's organic certification process, which spans 3 to 5 years. Conventional freeze-dried products maintain their market share through cost competitiveness and scalability. Processors can source from global commodity markets, blend origins for consistent quality, and operate continuously without the segregation required for organic certification. Asia-Pacific and South America will remain predominantly conventional through 2031 due to less-developed organic infrastructure and lower consumer willingness to pay premiums

Organic freeze-dried fruits and vegetables are projected to grow at an annual rate of 9.52% through 2031. Europe leads the organic movement, driven by stringent EU Regulation 2018/848 and strong consumer demand in Germany, France, and the Netherlands. North America follows closely, with retailers like Whole Foods and subscription services like Thrive Life reporting higher customer value for organic products. Europe and North America are expected to see organic products of the retail snacking and functional-beverage segments. The key insight is that organic capacity remains a bottleneck. Processors investing in certified facilities and long-term contracts with organic growers can secure higher margins and mitigate commodity price fluctuations.

By Distribution Channel: Online Retail Surges on Subscription Models and Ambient Stability

Supermarkets and hypermarkets captured 55.28% of freeze-dried fruits and vegetables sales in 2025, leveraging their broad footfall, impulse-purchase dynamics, and ability to cross-merchandise freeze-dried snacks alongside granola, yogurt, and breakfast cereals. These channels benefit from their ability to attract a wide range of consumers, offering convenience and accessibility. Supermarkets and hypermarkets cater to impulse and on-the-go occasions where single-serve pouches of freeze-dried mango or apple slices compete with candy bars and chips at checkout counters. However, this channel faces challenges as foot traffic declines and consumers shift routine purchases to online or warehouse clubs.

Online retail stores are projected to grow at 9.73% annually through 2031, driven by freeze-dried products' ambient stability, low breakage risk, and compatibility with subscription replenishment models. Direct-to-consumer brands like Thrive Life and Natierra have introduced quarterly subscription boxes offering freeze-dried berries, vegetables, and meal components at 15-20% discounts compared to one-time purchases. These models build lifetime customer value 4-5 times higher than transactional supermarket sales and lower customer-acquisition costs through predictable reorder cycles. Amazon's algorithmic recommendation engine further boosts discovery, with freeze-dried snacks frequently appearing in "Frequently Bought Together" bundles alongside protein powders and meal-replacement shakes, driving incremental sales.

Geography Analysis

In 2025, North America secured a 35.43% market share, driven by the United States outdoor recreation economy, emergency preparedness culture, and plant-based food trends favoring freeze-dried ingredients. The freeze-dried vegetable segment is growing rapidly, with meal-kit services and plant-based brands using freeze-dried peas, edamame, and corn for protein and fiber without cold-chain costs. Conagra's 2026 report highlighted protein as a key driver, with freeze-dried legumes achieving 10% volume growth. Canada and Mexico are emerging contributors, with Mexico becoming a hub for organic freeze-dried tropical fruits for the United States and European markets.

Asia-Pacific is forecast to grow at 9.35% annually through 2031, driven by urbanization, rising incomes, and demand for shelf-stable foods. China's market is seeing freeze-dried vegetables gaining popularity in instant noodles and ready-to-cook meals. India's market, though smaller, is expanding as e-commerce penetrates tier-2 and tier-3 cities, with freeze-dried mango and banana chips marketed as premium snacks. Japan's market is driven by disaster preparedness and an aging population seeking lightweight meals. Smaller markets like Singapore, South Korea, and Australia are growing rapidly, with Singapore emerging as a hub for premium freeze-dried snacks.

In 2025, Europe held a mid-20s share, propelled by Germany, the United Kingdom, and France. EU organic rules heighten compliance costs, but also let certified processors charge premiums that shield profit margins. South America and the Middle East and Africa held low-double-digit market shares, constrained by price sensitivity, limited cold-chain infrastructure, and low consumer awareness of freeze-dried products. Brazil and Argentina lead South American demand, with freeze-dried açaí and passion fruit powders gaining traction in exports, though domestic consumption remains low. In the Middle East and Africa, South Africa, Saudi Arabia, and the United Arab Emirates dominate, driven by expatriate populations, tourism, and food-security initiatives.

Competitive Landscape

The freeze-dried fruits and vegetables market is moderately fragmented and competitive, with numerous regional and international players. Companies such as Brothers International Food Holdings, LLC, Natierra, Expedition Foods Limited, American Outdoor Products, Inc., and Harmony House Foods Inc. hold a notable share of the global market. Key players are prioritizing product innovation to strengthen their market positions. Additionally, strategies such as mergers and acquisitions, along with the expansion of production and distribution networks, are being utilized to enhance market visibility and diversify product offerings.

In July 2024, Thrive Freeze Dry acquired Paradiesfrucht GmbH, representing a strategic move toward vertical integration. This acquisition enhances Thrive's market presence in Europe while optimizing its manufacturing capabilities. The acquisition also enables Thrive to expand its product range and cater to a broader customer base by leveraging Paradiesfrucht's expertise in freeze-dried products. Simultaneously, companies are investing in technologies to improve energy efficiency and automate processes, reducing labor costs while ensuring consistent product quality. These technological advancements are expected to drive operational efficiency and support sustainable production practices in the long term.

White-space opportunities cluster around organic certification, powdered formats, and direct-to-consumer channels: processors who invest in USDA or EU organic-certified freeze-drying lines can capture 50-80% price premiums and insulate themselves from commodity cycles, yet certified capacity remains scarce because the 3-to-5-year certification process and stringent segregation protocols deter incremental investment. Smaller contenders like Lyofood (Poland) and Buah (Germany) are unsettling incumbents by building direct-to-consumer subscription models that bypass supermarket slotting fees and promotional allowances, generating 30-50% higher gross margins and 4-5 times the lifetime customer value of transactional retail sales.

Freeze-Dried Fruits And Vegetables Industry Leaders

-

Brothers International Food Holdings, LLC

-

Natierra

-

Expedition Foods Limited

-

American Outdoor Products, Inc.

-

Harmony House Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Balance of Nature proudly unveiled the Balance of Nature Freeze-Dried Fruit Snacks across the United States. The products are claimed to be crafted entirely from whole, natural ingredients without any preservatives, dyes, or added sugars

- April 2025: Wambugu Apples, a Kenya-based company, has diversified its portfolio by entering the healthy snack market with the launch of a new freeze-dried fruit product line, exclusively claiming to utilize 100% locally sourced produce.

- February 2025: Brothers All Natural introduced its Chili Lime Mango freeze-dried fruit crisps at Expo West 2025. As per the company, these crisps are crafted from freeze-dried mango slices, combining the natural sweetness of mango with a tangy chili-lime flavor.

Global Freeze-Dried Fruits And Vegetables Market Report Scope

Freeze-dried fruits and vegetables are food items that have been frozen to attain a longer shelf life at a particular temperature. The process, called Lyophilisation, is used to extend the shelf life by preserving the nutrients and aroma compounds. The freeze-dried fruits and vegetable market is segmented by product type, form, nature, distributional channel, and geography. By product type, the market is segmented into freeze-dried fruits and freeze-dried vegetables. Freeze-dried fruits are further sub-segmented into strawberry, blueberry, raspberry, blackberry, pineapple, mango, apple, and other fruit types. Freeze-dried vegetables are further sub-segmented as corn, peas, carrots, potatoes, mushrooms, and other vegetable types. By form, the market is segmented into whole/diced and powder and granules. By nature, the market is segmented into conventional and organic. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and others. Further, the report provides an analysis of emerging and established economies across the world, comprising North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD) and Volume (Tons).

By Product Type

| Freeze-dried Fruits | Strawberry |

| Raspberry | |

| Pineapple | |

| Apple | |

| Mango | |

| Other Fruits | |

| Freeze-dried Vegetables | Pea |

| Corn | |

| Carrot | |

| Potato | |

| Mushroom | |

| Other Vegetables |

By Form

| Whole/Diced |

| Powdered/Granules |

By Nature

| Conventional |

| Organic |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Freeze-dried Fruits | Strawberry |

| Raspberry | ||

| Pineapple | ||

| Apple | ||

| Mango | ||

| Other Fruits | ||

| Freeze-dried Vegetables | Pea | |

| Corn | ||

| Carrot | ||

| Potato | ||

| Mushroom | ||

| Other Vegetables | ||

| By Form | Whole/Diced | |

| Powdered/Granules | ||

| By Nature | Conventional | |

| Organic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will the freeze-dried fruits and vegetables market be by 2031?

It is projected to reach USD 369.54 billion, expanding at an 8.18% CAGR between 2026 and 2031.

Which segment is growing fastest?

Freeze-dried vegetables are forecast at an 8.71% CAGR, driven by plant-based meal kits and emergency rations.

Why are powders gaining popularity?

Powdered formats dissolve quickly, retain nutrients, and fit functional-beverage formulations that command premium pricing.

How is e-commerce reshaping sales?

Direct-to-consumer subscriptions yield four to five times the margin of supermarket sales and are growing at a 9.73% CAGR.

Page last updated on: