Frozen Vegetables Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 21.51 Billion |

| Market Size (2031) | USD 28.29 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Frozen Vegetables Market Analysis by Mordor Intelligence

The Frozen Vegetables market size is expected to grow from USD 20.37 billion in 2025 to USD 21.51 billion in 2026 and is forecast to reach USD 28.29 billion by 2031 at 5.62% CAGR over 2026-2031.

The market's expansion is fueled by increasing demand for convenient meal options, the growth of cold-chain infrastructure, and the rising popularity of plant-based diets. Innovations such as Individual Quick Freezing (IQF) and improved packaging technologies are critical in preserving the quality, flavor, and nutritional content of frozen vegetables. In addition to convenience, frozen vegetables ensure a reliable supply, offer extended shelf life, and contribute significantly to reducing food waste, aligning with global goals for food security and sustainability. Established manufacturers capitalize on vertical integration to achieve scale advantages, while emerging brands focus on direct-to-consumer approaches and sustainability-driven messaging to establish niche positions. Moreover, advancements in energy-efficient refrigeration, isochoric freezing, and AI-powered inventory systems enhance product quality and reduce operational costs, supporting profitability despite volatile energy prices. Regionally, Europe demonstrates mature consumption trends, while the Asia-Pacific region, driven by rapid urbanization, is poised to become the primary growth driver for the frozen vegetable market over the next decade.

Key Report Takeaways

- By vegetable type, peas held 34.72% of the frozen vegetable market share in 2025, while broccoli is forecast to expand at an 8.2% CAGR through 2031.

- By nature, the conventional segment accounted for 67.63% of the frozen vegetable market size in 2025; organic variants are projected to grow at a 6.52% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets led with 31.12% revenue share in 2025, whereas online retail is advancing at an 8.17% CAGR to 2031.

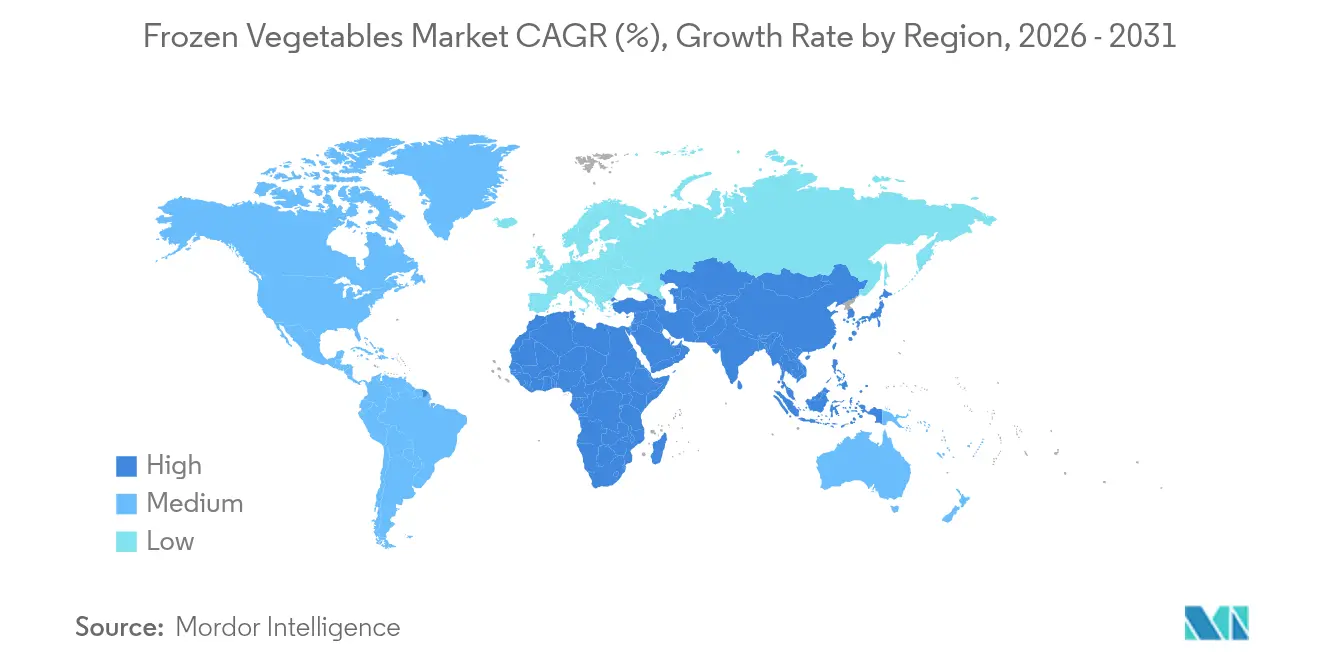

- By geography, Europe dominated with 34.06% of the frozen vegetable market in 2025; Asia-Pacific is poised to deliver a 5.85% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Frozen Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-driven meal preparation | +1.2% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Expansion of modern cold-chain infrastructure | +1.0% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Growing popularity of plant-based, vegetarian, and vegan diets | +0.8% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Long shelf life and reduced food wastage | +0.6% | Global | Long term (≥ 4 years) |

| Expansion of organized retail and e-commerce channels | +0.9% | Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Growing awareness of nutrition retention and safety standards | +0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Convenience-driven meal preparation

Busy households are increasingly focusing on time-saving solutions without compromising nutritional quality, driving changes in frozen vegetable consumption patterns. This shift is driven by urbanization and the demands of dual-income families, resulting in a growing preference for ready-to-cook vegetable options. Conagra Brands' 2025 frozen food report highlights that frozen meals account for 32% of total frozen sales, with younger generations advocating for a broader range of options, including global cuisines and healthier alternatives. The rising adoption of air fryers has further accelerated this trend, demonstrating how frozen vegetables can deliver restaurant-quality results with minimal effort. Deep freezing extends the shelf life of vegetables well beyond that of fresh produce, reducing shopping frequency and minimizing spoilage. The German Frozen Food Institute reported that Germany's sales volume of deep-frozen vegetables reached 522,180 tons in 2024 [1]Source: German Frozen Food Institute, "Sales statistics 2024", tiefkuehlkost.de. Additionally, advanced freezing technologies, such as Individual Quick Freezing (IQF), maintain the texture and nutritional content of vegetables, addressing previous consumer concerns about quality degradation that once limited the adoption of frozen vegetables.

Expansion of modern cold-chain infrastructure

Infrastructure modernization in emerging markets is establishing a strong foundation for the growth of the frozen vegetable market. Governments are increasingly focusing on cold chain development, recognizing its importance in ensuring food security and adding value to agriculture. In China, efforts to diversify the food supply include integrating cold chain logistics to minimize post-harvest losses and improve food distribution efficiency. In the United States, the cold storage market is expanding, driven by the growth of e-commerce and the implementation of automated storage solutions. According to the U.S. Department of Agriculture, the volume of frozen vegetables in U.S. cold storage facilities reached 2,234.26 million pounds in 2024 [2]Source: United States Department of Agriculture, "Cold Storage Summary February 2025", usda.gov. Technological advancements, such as AI-driven predictive analytics and IoT monitoring systems, are enhancing cold chain management by improving operational efficiency and reducing energy consumption. This infrastructure development is enabling market access in previously underserved regions, particularly in the Asia-Pacific, where cold chain investments are supporting agricultural modernization initiatives.

Growing popularity of plant-based, vegetarian, and vegan diets

Health consciousness, environmental sustainability concerns, and ethical considerations are accelerating the adoption of plant-based diets across diverse demographic groups. This trend highlights frozen vegetables as both convenient meal components and effective protein alternatives. In 2023, the India Brand Equity Foundation reported that nearly 30% of India's population follows a vegetarian diet [3]Source: India Brand Equity Foundation, "The Rising Plant-Based Sector in India", ibef.org. Additionally, awareness is growing in India about the health and environmental benefits of plant-based eating. Globally, the move toward plant-rich diets aligns with sustainability objectives and public health campaigns that encourage higher vegetable consumption to address diet-related health issues. Frozen vegetables, with their year-round availability and extended shelf life, enable consistent plant-based meal planning. This helps overcome the seasonality challenges that previously restricted vegetable consumption. In response, food manufacturers are introducing innovative frozen vegetable blends and plant-based meal solutions, catering to flexitarian consumers seeking convenient ways to enhance their plant protein intake.

Long shelf life and reduced food wastage

Frozen vegetables, with their prolonged shelf life, effectively address global food waste challenges while delivering economic advantages to both consumers and retailers by minimizing spoilage and improving inventory management. The frozen food supply chain surpasses fresh alternatives in reducing waste, primarily due to freezing technology that preserves nutritional value and prevents the rapid deterioration commonly seen within days of purchasing fresh produce. Governments are increasingly supporting food waste reduction initiatives, acknowledging the environmental and economic consequences of food loss across the supply chain. Frozen vegetables support portion control and flexible meal planning, making them particularly appealing to smaller households and aging populations that prioritize convenience and cost savings. Additionally, brands investing in sustainable packaging solutions gain a competitive edge, as advanced packaging technologies not only maintain product quality but also significantly extend shelf life.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile energy and refrigerant costs | -0.8% | Global, higher impact in energy-intensive regions | Short term (≤ 2 years) |

| Stringent regulatory restrictions on food safety | -0.4% | Global, varying by regulatory framework | Medium term (2-4 years) |

| Limited consumer awareness | -0.3% | Global | Medium term (2-4 years) |

| Risk of product spoilage and quality degradation | -0.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile energy and refrigerant costs

Frozen vegetable operations grapple with energy cost volatility, which affects cold storage, transportation, and processing expenses, ultimately squeezing profit margins and influencing pricing strategies. Starting January 2029, the U.S. Department of Energy's new energy conservation standards for commercial refrigeration equipment will mandate significant capital investments for compliance, though they may lead to reduced operational costs in the long run. Under the EPA's Significant New Alternatives Policy program, refrigerant regulations impose compliance costs as firms shift to eco-friendly alternatives in retail food refrigeration and cold storage. Companies with vast cold chain networks face planning hurdles due to energy price fluctuations, necessitating advanced hedging strategies and operational agility to stay competitively priced.

Stringent regulatory restrictions on food safety

Food safety agencies are implementing stricter traceability and inspection protocols, driving up compliance costs and operational challenges for frozen vegetable production and distribution. The United States Food and Drug Administration (FDA)'s Food Traceability Rule, effective January 2026, requires detailed record-keeping for frozen vegetables across the supply chain, increasing administrative workloads and necessitating technology upgrades. Farms supplying frozen vegetable processors face additional compliance obligations due to agricultural water standards for produce safety, which include assessment and mitigation measures that vary based on farm size and water source characteristics. In international trade, import inspection fee structures are adding cost pressures. The United States Department of Agriculture has revised regulations to recover inspection service costs through per-pound fees. Additionally, differences in regulatory standards between countries create market access barriers, requiring specialized expertise and significant compliance investments, which disproportionately impact smaller producers with limited resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vegetable Type: Peas continue to headline revenue while broccoli accelerates

Peas generated 34.72% of frozen vegetable market revenue in 2025, driven by their strong household familiarity and the cost efficiency of mechanical harvesting. Western Europe favors pea-based side dishes, while North Americans incorporate peas into mixed-vegetable options for children's menus, supporting baseline volumes. Broccoli, benefiting from its 'superfood' reputation and versatility in stir-fries and microwave steam bags, achieved the highest CAGR at 8.2%. The frozen vegetable market is increasingly targeting health-conscious consumers seeking antioxidant-rich products. Secondary categories, including corn, cauliflower, spinach, mushrooms, and asparagus, are experiencing steady growth due to greater recipe variety and the popularity of premium frozen meal kits. To cater to low-carb diet preferences, product developers are emphasizing riced cauliflower and spiralized zucchini, creating additional revenue opportunities without undermining core product segments.

Demand variations influence sourcing strategies: peas are primarily sourced through contract farming in the temperate regions of Belgium and the U.K. Conversely, broccoli and asparagus sourcing is shifting towards China and Peru to synchronize harvest schedules with processing operations. Risk management teams are expanding grower networks to mitigate regional climate risks. Premium innovations such as value-added glazing, light seasoning, and microwavable pouches are commanding higher price points, helping to counterbalance rising raw material costs. Consequently, the frozen vegetable market demonstrates strong margin resilience despite fluctuations in commodity prices.

By Nature: Conventional holds mass share, organic secures premium growth

In 2025, conventional products accounted for 67.63% of the category's value. This dominance was supported by enhanced agronomic practices, improved yields, and extensive availability across various price points. Their scalability ensures affordability, prompting cafeteria and institutional buyers to prioritize conventional SKUs for their cost-per-serving advantages. On the other hand, organic products are experiencing steady growth, with a 6.52% CAGR projected through 2031. This growth is fueled by consumers, particularly parents concerned about pesticides, seeking cleaner labels. United States Department of Agriculture grants and cost-share incentives are reducing certification barriers, encouraging mid-size growers to convert more acreage. Retailers are enhancing the visibility of organic products by allocating branded freezer sections, emphasizing unique provenance stories and regenerative farming practices, which drive higher spending. As organic supply expands, the price difference with conventional products decreases, fostering broader acceptance while preserving the category's profitability.

Processing facilities are being upgraded to keep organic lines separate, comply with strict residue standards, and prevent cross-contamination. Blockchain traceability solutions are being implemented to ensure organic integrity, which is crucial for exporters targeting markets like the EU and Japan, where certification requirements are stringent. By offering both conventional and organic products, manufacturers are strategically positioned to manage demand fluctuations and meet the needs of diverse consumer budgets.

By Distribution Channel: Omnichannel parity emerges between physical and digital touchpoints

In 2025, supermarkets and hypermarkets accounted for 31.12% of the revenue, driven by expansive freezer aisles, established shopper habits, and attractive in-store promotions. These retailers ensure high-quality cold storage, maintaining product freshness, safety, and nutrient content until the point of sale. Meanwhile, online grocery sales grew at a robust 8.17% CAGR, fueled by pandemic-era adoption and advancements in cold-chain parcel logistics. Urban dark-store models, strategically located near high-density areas, enable delivery within two hours, offering convenience comparable to physical stores. E-commerce platforms utilize AI to anticipate demand surges, pre-position inventory, reduce stockouts, and strengthen consumer confidence.

Online retail is driving growth in the frozen vegetable market by providing brands with data-driven insights into consumer preferences, enabling targeted promotional bundles. In contrast, brick-and-mortar chains are enhancing their relevance by creating experiential zones, such as live cooking demonstrations featuring frozen vegetables. Convenience stores are innovating with micro-freezers stocked with single-serve packs, catering to on-the-go consumers and increasing impulse purchases. A multi-channel strategy is becoming essential: click-and-collect models combine the convenience of e-commerce with in-store foot traffic, while loyalty programs integrate rewards across both digital and physical platforms.

Geography Analysis

Europe maintains 34.06% of the frozen vegetable market revenue in 2025, driven by established consumption patterns, strict safety standards, and a robust refrigerated logistics network. European consumers increasingly prefer convenient, healthy, and sustainable food options. Frozen vegetables meet this demand with their year-round availability and preserved nutritional content. The growing adoption of plant-based diets, vegetarianism, and clean-label products further boosts demand for these nutrient-rich frozen offerings. Belgium leads in exports, primarily shipping IQF peas and mixed vegetables across the European bloc. While Germany, France, and the U.K. exhibit high household penetration rates, future growth hinges on organic, low-salt, and value-added product formats. Rising sustainability expectations are prompting the industry to adopt lighter packaging, driving research and development into recyclable mono-material pouches.

Asia-Pacific is projected to achieve a strong 5.85% CAGR through 2031, leading global market growth. In China, cold-chain modernization is a priority, supported by public-private joint ventures. These efforts enhance rural-to-urban distribution efficiency and strengthen national food security objectives. Domestic processors in China are increasingly competing with European exporters by promoting locally sourced products like broccoli, corn, and spinach, appealing to patriotic consumption trends. In India, states such as Gujarat and Maharashtra are expanding IQF capacity to meet the growing demand from quick-service restaurants in tier-1 and tier-2 cities. Meanwhile, Japan is attracting affluent consumers with premium frozen sushi and bento innovations, offering convenience without compromising traditional flavors.

North America is experiencing steady growth in the frozen vegetable market. Investments in automated cold warehouses, particularly in the Midwest and Gulf Coast, aim to address labor shortages and reduce energy consumption. Canada's compliance with U.S. traceability regulations simplifies cross-border supply chains. At the same time, Mexico is increasing vegetable production through protected agriculture, enhancing input availability. Processors are also diversifying sourcing strategies in response to climate challenges, such as droughts impacting yields in California. This includes a shift toward controlled-environment farms and greenhouse complexes. South America, along with the Middle East and Africa, presents emerging opportunities. In Brazil, the rise of economic supermarket formats is driving domestic frozen vegetable consumption, catering to busy urban professionals. In the United Arab Emirates, the Jebel Ali re-export hub facilitates the distribution of frozen vegetables from Europe and Asia across the Gulf, with food-service channels dominating demand. However, challenges such as cold-chain inefficiencies and power-grid instability persist. Government subsidies and solar-powered warehouses are gradually addressing these issues, unlocking the region's potential.

Competitive Landscape

The frozen vegetable market is moderately fragmented, with major players exercising substantial influence in material procurement and advertising strategies. McCain Foods has significantly expanded its portfolio by acquiring Strong Roots, a move that introduces plant-based SKUs and aligns with its broader sustainability goals. The company has committed to transitioning 100% of its global potato and vegetable acreage to regenerative agricultural practices by 2030, showcasing its dedication to environmental stewardship. Similarly, Bonduelle is strategically redirecting resources into high-margin frozen innovations by forming joint ventures in chilled salads, which allows the company to optimize its capital allocation and focus on growth areas within the frozen vegetable segment.

Key players in the market include McCain Foods Limited, Conagra Brands Inc., Nomad Foods, Bonduelle S.A., and Greenyard NV. These companies compete on various factors such as product offerings, ingredient quality, pricing, functionality, packaging, and marketing strategies to gain a competitive edge. A growing trend is the use of social media platforms and online distribution channels for marketing and branding, aimed at attracting a broader customer base. Technological advancements are reshaping the market: several players are testing isochoric freezing, which promises a 30% reduction in energy consumption compared to blast cooling. Americold and Lineage are exploring AI-driven warehouse orchestration to dynamically allocate pallet locations, reducing travel time and energy usage. Sustainability is becoming a key brand asset, with on-pack QR codes enabling consumers to trace the origin and carbon footprint of each bag of frozen peas.

New entrants are capitalizing on innovative business models, such as e-commerce subscriptions and influencer partnerships, to reduce customer-acquisition costs and build brand loyalty. Venture-backed start-ups are introducing veggie-based frozen meal bowls designed to meet specific dietary needs, including keto and other health-focused protocols, catering to the growing demand for personalized nutrition. The rise of private-label products in retail, particularly among European discount chains, is intensifying price competition. This trend is pressuring established brands to defend their market share by investing in product innovation and loyalty programs. Companies that successfully integrate advanced data analytics, regenerative sourcing practices, and energy-efficient logistics are positioning themselves to gain a competitive edge in this evolving market landscape.

Frozen Vegetables Industry Leaders

-

McCain Foods Limited

-

Nomad Foods

-

Conagra Brands Inc.

-

Bonduelle S.A.

-

Greenyard NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Green Giant introduced twelve new frozen vegetable products, including Crispy Smashed Potatoes, Corn Cob Bites, Veggie Ramen, and Roasting Veggies, catering to consumers looking for convenient and cost-effective meal options.

- April 2024: McCain Foods has strengthened its partnership with Strong Roots, a Dublin-based frozen food producer. Previously, the two brands announced a strategic alliance, with McCain investing to expand its product portfolio and provide vegetable-focused, environmentally sustainable food options to consumers worldwide.

- March 2024: BigBasket, the Indian online grocery retailer, has introduced a new frozen foods brand called Precia. The brand features three primary product categories available nationwide: frozen vegetables, frozen snacks, and frozen sweets.

- June 2023: Nortera has introduced its frozen vegetable brand, Arctic Gardens, to the U.S. market. Notably, 80% of Arctic Gardens' offerings are processed right in North America. The brand features a diverse range of frozen vegetable products that are pre-washed, pre-cut, and ready to cook.

Global Frozen Vegetables Market Report Scope

The frozen vegetables market is segmented by type, distribution channel, and geography. Based on type, the market is segmented into beans, corn, peas, mushroom, cauliflower, asparagus, broccoli, and other types. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, grocery stores, convenience stores, and other distribution channels. Furthermore, the report takes into consideration the market for frozen vegetables in the established and emerging economies across the world, including North America, Europe, Asia-Pacific, South America, and Middle-East and Africa.

| Beans |

| Corn |

| Peas |

| Broccoli |

| Cauliflower |

| Mushroom |

| Asparagus |

| Spinach |

| Other Vegetable Types |

| Organic |

| Conventional |

| Supermarkets / Hypermarkets |

| Convenience Store |

| Specialty Store |

| Online Retail Store |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Vegetable Type | Beans | |

| Corn | ||

| Peas | ||

| Broccoli | ||

| Cauliflower | ||

| Mushroom | ||

| Asparagus | ||

| Spinach | ||

| Other Vegetable Types | ||

| By Nature | Organic | |

| Conventional | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Convenience Store | ||

| Specialty Store | ||

| Online Retail Store | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the frozen vegetable market in 2026?

The frozen vegetable market size stands at USD 21.51 billion in 2026.

What is the forecast CAGR for frozen vegetables through 2031?

The market is projected to advance at a 5.62% CAGR between 2026 and 2031.

Which vegetable type holds the highest revenue share?

Peas lead with a 34.72% share of category revenue in 2025.

Which region is growing the fastest for frozen vegetables?

Asia-Pacific is forecast to post a 5.85% CAGR through 2031 as cold-chain capacity expands.

Page last updated on: