Fruits And Vegetables Processing Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

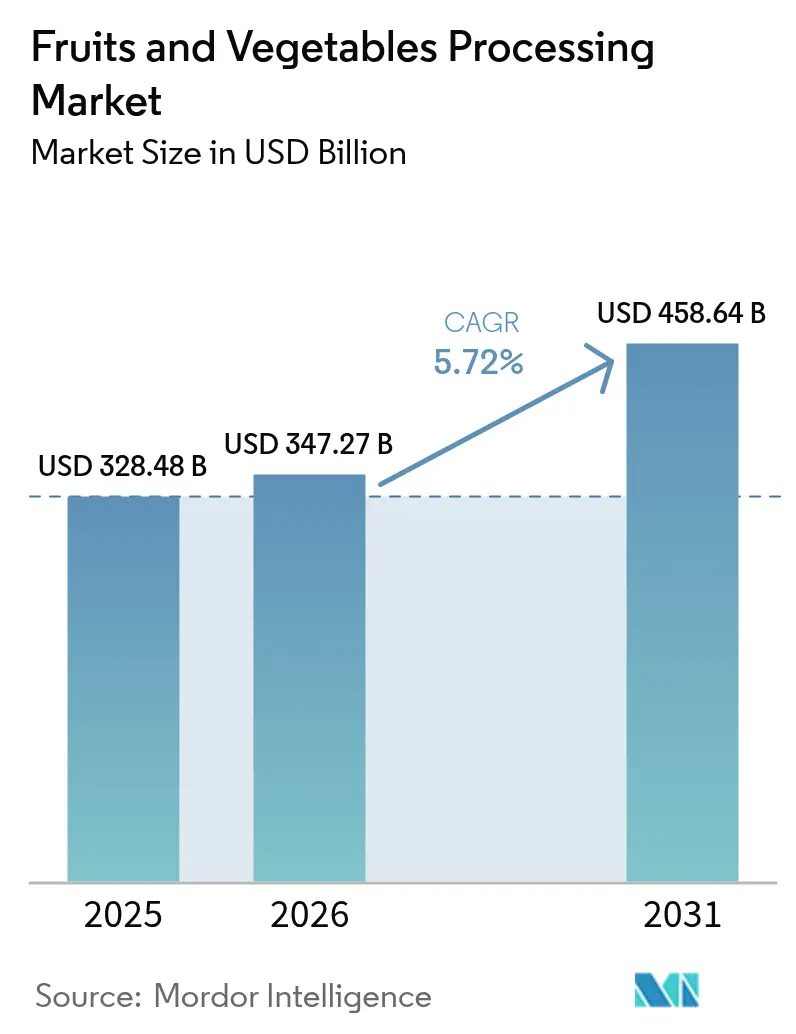

| Market Size (2026) | USD 347.27 Billion |

| Market Size (2031) | USD 458.64 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fruits And Vegetables Processing Market Analysis by Mordor Intelligence

The fruits and vegetables processing market size is projected to be USD 328.48 billion in 2025, USD 347.27 billion in 2026, and reach USD 458.64 billion by 2031, growing at a CAGR of 5.72% from 2026 to 2031. The market is expanding due to factors such as increasing urbanization, rising single-person households, and a growing preference for convenient, time-saving meal options. Stricter regulations on farm-to-fork traceability are driving demand for processed fruits and vegetables that come with reliable safety certifications. The Asia-Pacific region is expected to dominate the market in terms of revenue in 2025, driven by its large population and growing demand for processed food. Meanwhile, the Middle East and Africa are anticipated to witness the fastest growth during the forecast period, as governments in these regions are heavily investing in cold-chain infrastructure to reduce post-harvest losses and improve food supply chains. The market remains moderately consolidated, with key players focusing on innovation and expanding their product offerings to meet evolving consumer needs.

Key Report Takeaways

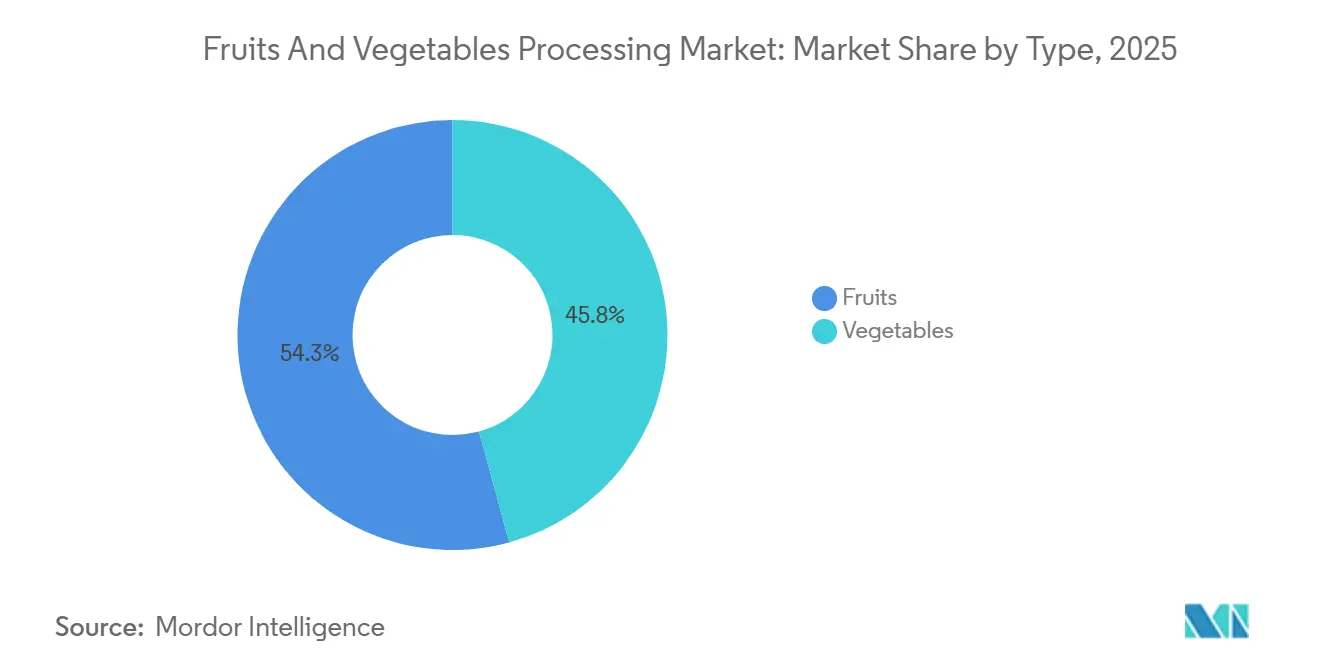

- By product type, fruits commanded 54.25% of the fruits and vegetables processing market share in 2025, while vegetables are projected to advance at a 6.39% CAGR through 2031.

- By form, canned products held a 31.05% slice of the fruits and vegetables processing market size in 2025; frozen offerings are on track for the highest CAGR at 7.12% between 2026 and 2031.

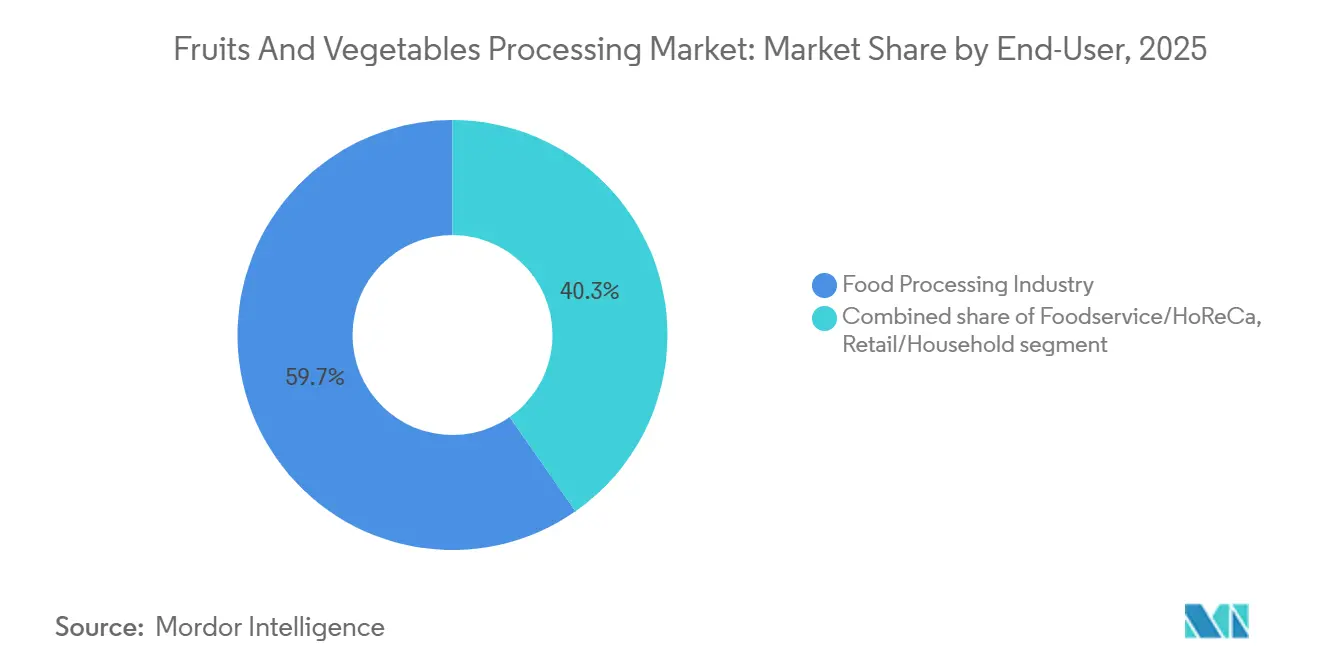

- By end user, the food processing industry accounted for 59.70% of 2025 output, whereas foodservice and HoReCa channels are forecast to post a 7.21% CAGR through 2031.

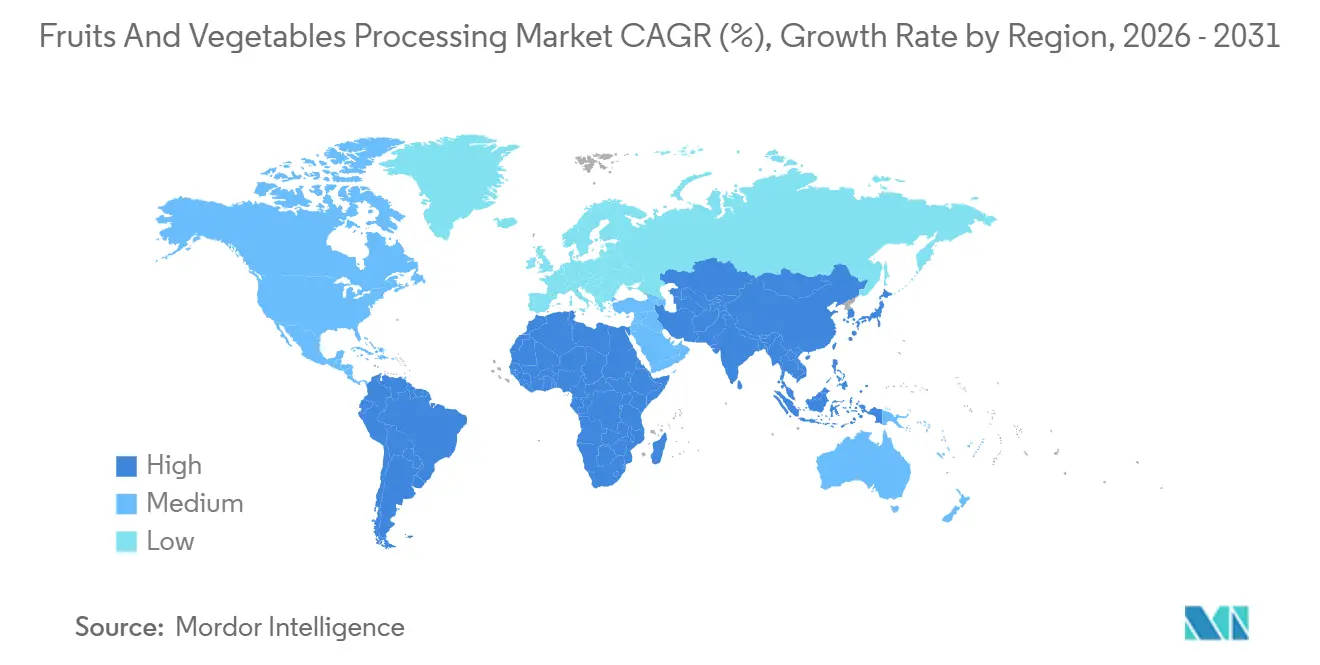

- By geography, Asia-Pacific led with 33.04% revenue in 2025, while the Middle East and Africa region is forecast to expand at an 8.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fruits And Vegetables Processing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for convenient and ready-to-eat fruit and vegetable products | +1.2% | Global, with peaks in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Growing health awareness and preference for nutritious processed products | +1.0% | Global, strongest in North America and Western Europe | Long term (≥ 4 years) |

| Innovation in value-added products such as juices, purees, and snacks | +0.9% | North America, Europe, Asia-Pacific core markets | Medium term (2-4 years) |

| Technological advancements in processing, packaging, and cold chain logistics | +1.1% | Global, early adoption in North America and Europe, spillover to Asia-Pacific and Middle East and Africa | Short term (≤ 2 years) |

| Growing popularity of plant-based diets is boosting demand | +0.8% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Increasing focus on food safety and hygiene standards | +0.7% | Global, regulatory-driven in Europe and North America, emerging in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising consumer demand for convenient and ready-to-eat fruit and vegetable products

The growing demand for convenient, ready-to-eat food products is driving the fruits and vegetables processing market. This trend is largely due to increasingly busy lifestyles and higher workforce participation. For instance, as of May 2024, the employment rate across member countries of the Organisation for Economic Co-operation and Development (OECD) reached 95.1%[1]Source: Organisation for Economic Co-operation and Development, "OECD Employment Outlook 2024", oecd.org. With more people working, there is less time to prepare fresh meals, leading to a greater reliance on pre-cut, frozen, and ready-to-eat fruits and vegetables. Urban households and individuals living alone are particularly drawn to these products because they are portion-controlled and easy to prepare. Furthermore, supermarkets are expanding their ready-meal sections, and online grocery platforms and meal-kit services are incorporating more processed fruits and vegetables into their offerings.

Growing health awareness and preference for nutritious processed products

Health awareness is rising globally, and more people are focusing on increasing their protein intake, driving growth in the fruits and vegetables processing market. Many consumers are looking for foods that are not only convenient but also packed with nutrients, including protein. According to the International Food Information Council (IFIC) Food and Health Survey 2024, 71% of Americans are actively trying to include more protein in their diets[2]Source: International Food Information Council (IFIC), "Food and Health Survey 2024", ific.org. This has led to a growing demand for products enriched with plant-based proteins, such as pea protein, vegetable concentrates, and legume blends. To meet this demand, manufacturers are creating processed fruit and vegetable products that are both nutritious and easy to consume. These products are designed to support balanced diets and offer additional health benefits. As more people prioritize health and convenience, processed fruits and vegetables are becoming key ingredients in a wide range of health-focused food products.

Innovation in value-added products such as juices, purees, and snacks

Growth in the fruits and vegetables processing market is driven by innovations in products such as juices, purees, and fruit- and vegetable-based snacks. New processing techniques, such as cold-pressing and high-pressure processing, are helping manufacturers retain the natural nutrients, flavors, and freshness of these products. This makes premium juices more attractive to health-conscious consumers who prioritize quality and nutrition. There is growing demand for vegetable-based snacks, such as beetroot, kale, and sweet potato chips, as consumers increasingly seek healthier alternatives to traditional snack foods. Furthermore, purees, which were once primarily marketed for infants, are now gaining popularity among adults. These purees are seen as convenient, portion-controlled options that appeal to busy lifestyles. This shift allows manufacturers to expand their product offerings and reach a broader range of consumers, thereby contributing to the market's overall growth.

Growing popularity of plant-based diets is boosting demand

The increasing adoption of plant-based diets is driving significant growth in the fruits and vegetables processing market. Consumers are turning to processed plant-based ingredients as they seek convenient and healthy meal options. According to the World Animal Foundation, as of June 2025, there are approximately 88 million vegans worldwide, underscoring the growing demand for plant-based foods[3]Source: World Animal Foundation, "How Many Vegans Are in the World in 2026? Latest Vegan Stats", worldanimalfoundation.org. Processed fruits and vegetables are essential components of various plant-based products, including ready-to-eat meals, snacks, smoothies, and meat substitutes. This trend is pushing manufacturers to expand their production of frozen, canned, and value-added fruit and vegetable products. By doing so, they aim to meet the increasing global demand for plant-based alternatives while catering to consumer preferences for healthier, more sustainable food choices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment requirements for processing equipment | -0.8% | Global, acute in emerging markets with limited financing | Short term (≤ 2 years) |

| Fluctuations in raw material availability and prices due to seasonality and climate conditions | -1.0% | Global, severe in drought-prone regions (California, Mediterranean, North China) | Medium term (2-4 years) |

| Limited shelf-life perception of certain processed products | -0.4% | North America and Europe, consumer-perception driven | Long term (≥ 4 years) |

| High energy and water consumption in processing operations | -0.6% | Global, most acute in water-scarce regions (Middle East, North Africa, Western United States) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fluctuations in raw material availability and prices due to seasonality and climate conditions

Changes in the availability and prices of raw materials, driven by seasonal patterns and climate variability, pose a significant challenge to the fruits and vegetables processing market. Weather events such as droughts, frost, and irregular rainfall can severely impact crop yields, leading to shortages. As a result, processors often need to depend on more expensive imports or alternative sources to meet demand. This unpredictability makes it harder for companies to plan production efficiently, increases procurement costs, and reduces profit margins. Furthermore, many small and mid-sized processors lack effective risk management strategies, leaving them more vulnerable to these supply and price fluctuations. These challenges collectively hinder consistent market growth.

High capital investment requirements for processing equipment

The high cost of investing in processing equipment is a major challenge for the fruits and vegetables processing market. Setting up new processing facilities or upgrading existing ones requires significant spending on advanced machinery, automation systems, and infrastructure to meet food safety standards. These expenses are particularly difficult for small and medium-sized companies to manage, creating barriers to effective competition. This issue is even more pronounced in emerging economies, where access to financing is often limited. As a result, many businesses face delays in adopting modern processing technologies or expanding their production capacity, which slows down the overall growth of the market. The lack of affordable financing options and the complexity of integrating advanced systems further hinder smaller players' ability to scale their operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vegetables Gain Momentum as Protein Alternatives Expand

The fruits segment led the fruits and vegetables processing market, accounting for 54.25% of the total market share in 2025. This dominance is due to the high demand for processed fruit products like juices, concentrates, canned fruits, frozen fruits, and purees. These products are widely used in industries such as beverages, dairy, bakery, and confectionery. Consumers increasingly prefer convenient, ready-to-consume options, and fruit-based ingredients are becoming more popular in functional and fortified foods. The growing export of tropical and exotic fruit products has further boosted the segment's growth.

The vegetables segment is expected to grow at a CAGR of 6.39% from 2026 to 2031, driven by the rising demand for frozen, canned, and minimally processed vegetables. Consumers are focusing more on healthy eating and convenient meal options, which has increased the popularity of ready-to-cook and ready-to-eat vegetable products. Processed vegetables are also being used more in foodservice, packaged meals, and quick-service restaurants. Moreover, advancements in preservation technologies, such as freezing and drying, are helping to maintain nutritional value and extend shelf life, supporting the segment's long-term growth.

By Form: Frozen Products Accelerate on Cold-Chain Upgrades

Canned products accounted for 31.05% of the fruits and vegetables processing market share in 2025, primarily due to their long shelf life, affordability, and easy availability. These products are popular among households and foodservice providers because they are convenient and can be consumed year-round, regardless of seasonal changes. In addition, canned fruits and vegetables are in high demand in institutional settings and emerging markets where shelf-stable food options are essential. Advances in canning technology have further enhanced the quality of these products by effectively preserving their taste, texture, and nutritional value.

The frozen segment is expected to grow at a CAGR of 7.12% through 2031, driven by rising consumer demand for convenient, minimally processed foods that retain freshness and nutrients. Frozen fruits and vegetables are widely used in ready-to-eat meals, smoothies, and quick-service restaurants due to their longer shelf life and ease of preparation. The growth of urbanization, busy lifestyles, and the expansion of cold chain infrastructure are further boosting the demand for frozen products. Frozen formats are becoming more popular as they better preserve the natural flavor and nutritional content compared to some other processing methods, making them a preferred choice for health-conscious consumers.

By End User: Foodservice and HoReCa Lead Post-Pandemic Recovery

The food processing sector accounted for 59.70% of the fruits and vegetables processing market output in 2025, primarily driven by high demand from packaged food manufacturers. Processed fruits and vegetables are essential ingredients in products like ready meals, soups, sauces, snacks, bakery goods, and beverages. These products are preferred because they have a longer shelf life, maintain consistent quality, and are easy to use in large-scale production. The rising popularity of convenience foods and packaged products continues to strengthen this sector's dominance in the market.

The foodservice and HoReCa (Hotels, Restaurants, and Catering) segment is expected to grow at a CAGR of 7.21% through 2031, driven by the rapid expansion of restaurants, hotels, catering services, and quick-service chains. Urbanization, higher disposable incomes, and changing eating habits are increasing the demand for processed fruits and vegetables in commercial kitchens. These products help save preparation time, reduce food waste, and ensure consistent taste and quality in dishes. Additionally, the growth of global tourism and the rise of organized foodservice chains are further boosting the demand in this segment.

Geography Analysis

Asia-Pacific accounted for 33.04% of the fruits and vegetables processing market revenue in 2025, driven by advancements in post-harvest infrastructure, high agricultural output, and expanding processing capabilities. Countries like India are improving cold storage and transportation systems to reduce food wastage and enhance supply efficiency. Japan’s aging population is increasing the demand for easy-to-consume, single-serve, and fortified processed products. Indonesia is capitalizing on its tropical fruit production to boost exports, while Australia’s strict organic certification standards are helping its exporters target premium global markets. These factors collectively make Asia-Pacific a dominant player in the global processing market.

The Middle East and Africa are expected to experience the fastest growth in the fruits and vegetables processing market, with a CAGR of 8.04% through 2031. This growth is fueled by rising investments in local food processing infrastructure and initiatives to improve food security. Countries like Saudi Arabia and the United Arab Emirates are focusing on domestic processing to reduce dependency on imports. South Africa is strengthening its position in processed fruit exports, while Nigeria is enhancing its processing capacity by connecting farmers directly with processors. These efforts are improving regional self-reliance and creating a more integrated supply chain.

North America and Europe are mature markets but remain important for premium, organic, and value-added processed products. Consumer demand for clean-label, organic, and functional foods is pushing processors to adopt certified sourcing and advanced technologies. Europe is leading in organic product innovation, supported by regulatory goals and the expansion of private-label offerings by retailers. Meanwhile, South American countries like Chile and Brazil play a key role in global supply by exporting processed fruits and vegetables during the off-season in Northern Hemisphere markets. This ensures a steady supply of products worldwide, even during seasonal gaps.

Competitive Landscape

The fruits and vegetables processing market is dominated by a few large multinational companies, making it moderately consolidated. Key players like The Kraft Heinz Company, Conagra Brands Inc., Nestlé S.A., Dole plc, and Del Monte Foods hold strong positions due to their extensive global distribution networks and diverse product offerings. These companies also benefit from well-established brand recognition, which helps them maintain customer loyalty. By managing their supply chains efficiently, from sourcing raw materials to delivering finished products, they ensure consistent availability and remain competitive in both developed and emerging markets.

Alongside these global leaders, regional and local processors play a crucial role in the market. These smaller companies often focus on specialized products tailored to local tastes and preferences. They also emphasize using local crop varieties and maintaining a faster, more responsive supply chain to meet customer demands quickly. By tailoring their offerings to specific regions and keeping prices competitive, these companies effectively serve domestic and nearby markets. This combination of global dominance and regional specialization creates a balanced and moderately consolidated market structure.

Innovation and technology adoption are key factors driving competition in the fruits and vegetables processing market. Leading companies are investing in advanced processing technologies, automation, and improved packaging solutions to enhance product quality, extend shelf life, and boost operational efficiency. Additionally, there is a growing focus on value-added products, such as organic, clean-label, and ready-to-eat options, to meet changing consumer preferences. As more companies adopt these technologies and expand their product portfolios, competition is expected to increase, further shaping the market landscape in the coming years.

Fruits And Vegetables Processing Industry Leaders

-

The Kraft Heinz Company

-

Conagra Brands Inc.

-

Nestlé S.A.

-

Dole plc

-

Del Monte Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MAF RODA Group completed the acquisition of Strauss to strengthen global positioning in the fruit and vegetable processing equipment sector, expanding technological capabilities and market reach across multiple geographic regions.

- January 2025: Superior Foods International was acquired by Peru's Viru Group, the largest producer of canned and frozen fruits and vegetables in Peru, creating enhanced capabilities and expanded offerings in the frozen products market while maintaining independent operations.

- September 2024: Green Giant introduced twelve new veggie-focused frozen products, including three entirely new items: Crispy Smashed Potatoes, Corn Cob Bites, and Veggie Ramen. Additionally, the brand expanded its Green Giant Restaurant Style line with new offerings from Roasting Veggies and Veggies & Rice.

- August 2024: F&S Fresh Foods acquired Calavo Growers' fresh-cut division, Renaissance Food Group, expanding operations across North America with five production facilities in Oregon, California, Texas, and Georgia.

Global Fruits And Vegetables Processing Market Report Scope

Fruit and vegetable processing involves grading and processing raw vegetables and fruits into pieces and paste, which are usually packed in cans. Additionally, to extend shelf life, fruits and vegetables are frozen, chilled, and dried using various processes, such as freeze-drying and sun-drying. The fruits and vegetables processing market is segmented by product type: fruits and vegetables. By form, the market is segmented into fresh, fresh-cut, canned, frozen, dried/dehydrated, and juices/purees. Based on end user, the market is segmented into the food processing industry, foodservice/HoReCa, and retail/household. The report also provides a geographical segmentation of North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, market sizing and forecasts have been prepared on a value basis (USD million).

| Fruits |

| Vegetables |

| Fresh |

| Fresh-Cut |

| Canned |

| Frozen |

| Dried/Dehydrated |

| Juices/Purees |

| Food Processing Industry | |

| Foodservice/HoReCa | |

| Retail/Household | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retailers | |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Fruits | |

| Vegetables | ||

| By Form | Fresh | |

| Fresh-Cut | ||

| Canned | ||

| Frozen | ||

| Dried/Dehydrated | ||

| Juices/Purees | ||

| By End User | Food Processing Industry | |

| Foodservice/HoReCa | ||

| Retail/Household | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retailers | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global demand for processed fruits and vegetables become by 2031?

The fruit and vegetable processing market is projected to reach USD 458.64 billion by 2031, reflecting a 5.72% CAGR from 2026.

Which product form is set to grow the fastest over the next five years?

Frozen products are forecast to register the quickest gains with a 7.12% CAGR as cold-chain networks improve worldwide.

What region shows the highest growth potential?

The Middle East and Africa region is expected to post the strongest growth at an 8.04% CAGR through 2031, driven by food-security investments.

Which region offers the strongest future growth potential?

The Middle East and Africa region is forecast to rise at 8.03% CAGR to 2031.

Why are vegetables gaining share in processed categories?

Rising interest in plant-based protein pushes demand for vegetable purees and blends used in meat substitutes and convenience meals.

Page last updated on: