Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

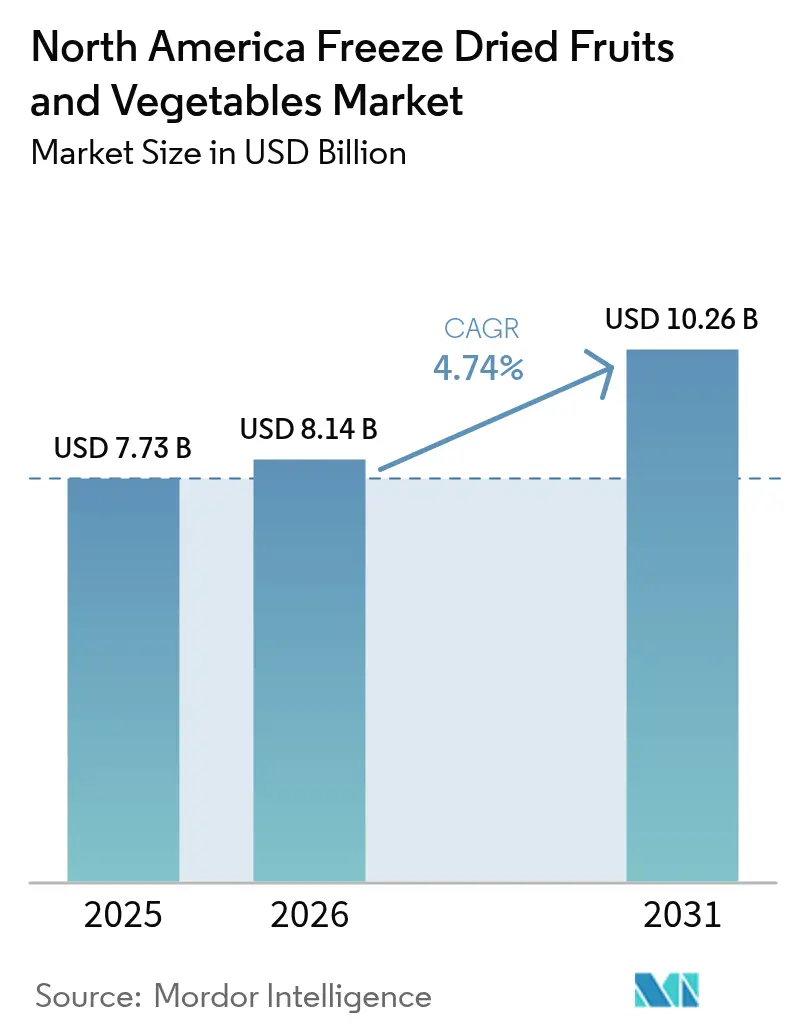

| Base Year Market Size (2025) | USD 7.73 Billion |

| Market Size (2026) | USD 8.14 Billion |

| Market Size (2031) | USD 10.26 Billion |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

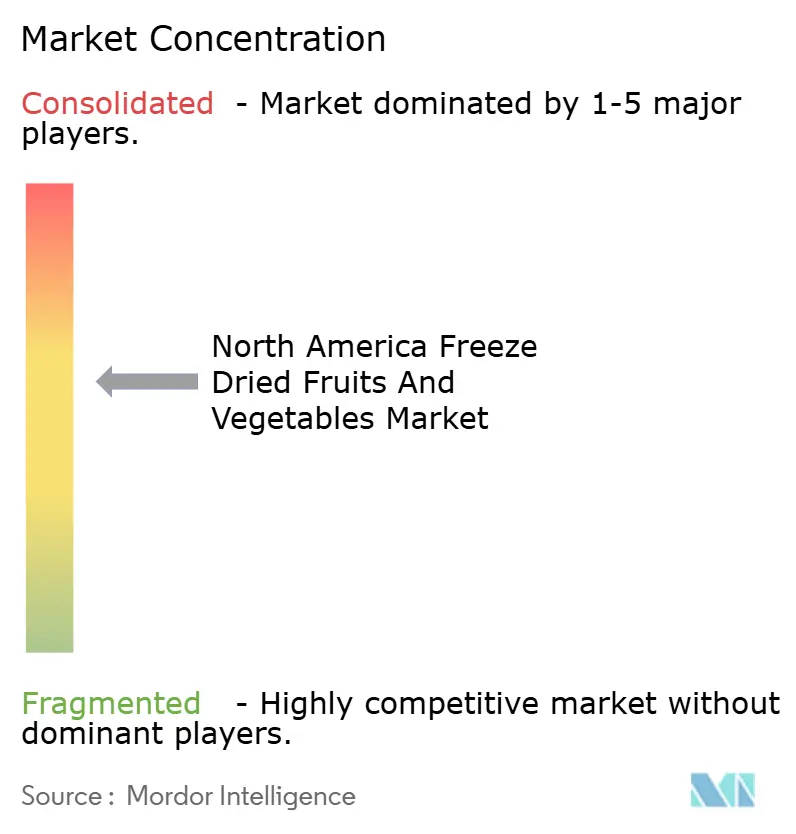

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Freeze Dried Fruits And Vegetables Market Analysis by Mordor Intelligence

The North America freeze-dried fruits and vegetables market size was valued at USD 7.73 billion in 2025 and is projected to reach USD 8.14 billion in 2026 and USD 10.26 billion by 2031, growing at a CAGR of 4.74% from 2026 to 2031. This measured expansion reflects a structural shift in how food processors and consumers value nutrient retention over simple shelf extension. Freeze-drying's ability to preserve up to 97% of original nutrients positions it as the premium preservation method, yet capital intensity and energy consumption, often a few times higher than hot-air drying, constrain adoption among cost-sensitive operators. Manufacturers investing in hybrid freeze-drying technologies that integrate microwave or infrared assistance can reduce energy consumption, potentially unlocking cost parity with conventional drying while preserving freeze-drying's quality advantages. Strategic positioning will hinge on balancing premium positioning against cost discipline, with winners likely emerging from those who master hybrid processing, secure long-term raw-material contracts, and build direct-to-consumer channels that capture full margin stacks.

Key Report Takeaways

- By product type, fruits led with 63.57% of the North America freeze-dried fruits and vegetables market share in 2025, while vegetables are forecast to grow at a 5.41% CAGR through 2031.

- By form, powder and granules accounted for 47.51% of the North American freeze-dried fruits and vegetables market in 2025, and chunks are projected to expand at a 5.47% CAGR over 2026-2031.

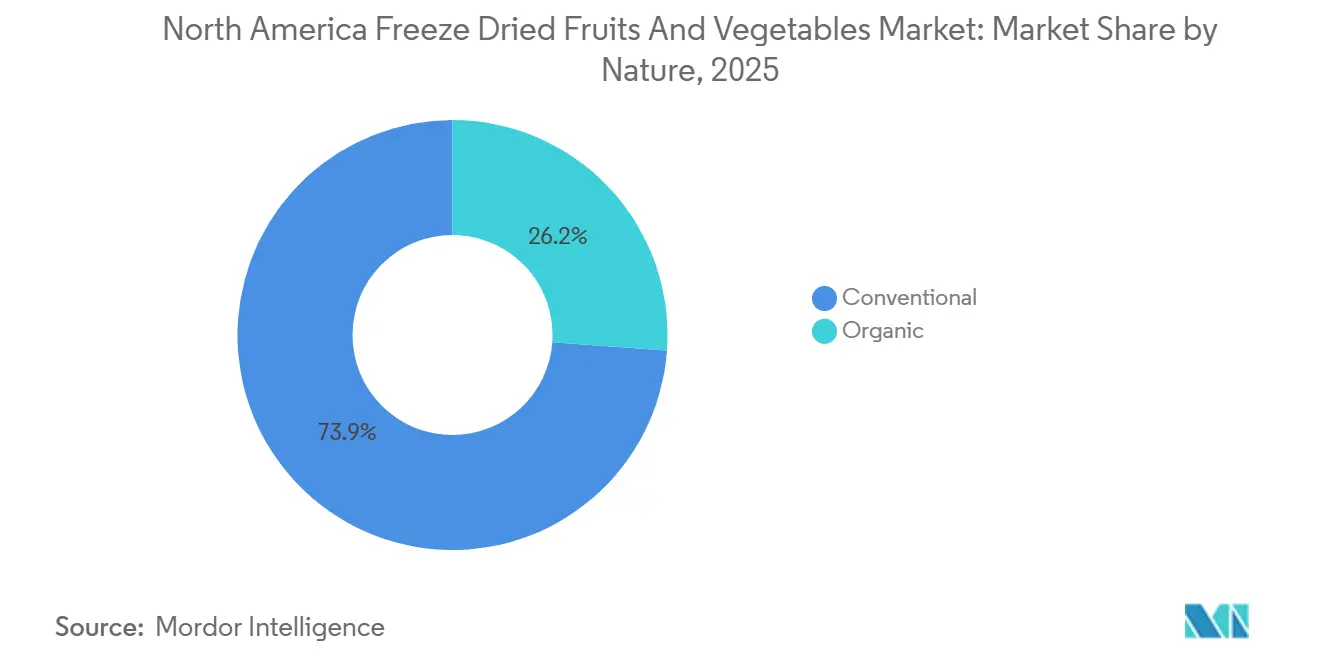

- By nature, conventional variants captured 73.85% share of the North America freeze-dried fruits and vegetables market in 2025; organic products record the fastest projected CAGR of 5.17% through 2031.

- By end-use, the food-processing channel commanded 43.57% share in 2025, whereas retail is advancing at a 5.37% CAGR to 2031.

- By geography, the United States accounted for 78.41% of the North America freeze-dried fruits and vegetables market size in 2025; Mexico represents the fastest-growing geography at a 6.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Freeze Dried Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for nutrient-dense foods with a health focus | +1.2% | North America, with stronger uptake in urban centers | Medium term (2-4 years) |

| Snack consumption rises with busy lifestyles | +0.9% | Global, particularly relevant for remote and disaster-prone regions | Long term (≥ 4 years) |

| Foods increasingly utilize functional ingredients | +1.1% | Europe, concentrated in metropolitan areas | Medium term (2-4 years) |

| Preference for clean-label, natural ingredients | +0.8% | North America, driven by premium retail channels | Medium term (2-4 years) |

| Technological advancements in freeze-drying | +1.0% | North America, accelerated by e-commerce growth | Short term (≤ 2 years) |

| Trends lean towards sustainable, waste-reducing consumption | +0.7% | North America, influenced by Food and Drug Administration natural labeling policies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for nutrient-dense foods with a health focus

Health-conscious consumers are recalibrating purchase decisions around nutrient density rather than calorie reduction alone. Freeze-drying preserves heat-sensitive vitamins (C, B-complex) and bioactive compounds (polyphenols, anthocyanins) that degrade under thermal processing, making it the preferred method for premium wellness products. The sublimation process in freeze-drying preserves a significant portion of original vitamins and minerals, maintaining cellular structure for optimal rehydration. This creates unique differentiation opportunities for manufacturers aiming at health-conscious consumers. Research from Johns Hopkins Center for a Livable Future reveals that many American adults adhere to specific diets [1]Source: Karissa Maeda, “Food Trends for 2025 Focus on Healthful Foods, Viral Trends, and Protein,” jhsph.edu. Brands that transparently communicate nutrient retention data and source from regenerative farms will capture the fastest-growing consumer cohort, millennials and Gen Z shoppers who treat food purchases as health investments.

Snack consumption rises with busy lifestyles

Time scarcity is reshaping eating occasions, with "snackification" replacing traditional meal structures for a growing share of North American consumers. Freeze-drying, which can achieve an extended shelf life without chemical preservatives, not only aligns with clean-label mandates but also addresses concerns about supply chain resilience. The U.S. Fish and Wildlife Service highlighted that Backyard Farms, operating in New Mexico, processes significant quantities from numerous regional farms. This effort not only reduces food waste but also turns climate-damaged crops into marketable products [2]Source: U.S. Fish & Wildlife Service, “Freeze Drying Crops for Increased Climate Change Resilience in New Mexico,” fws.gov. Freeze-dried fruits and vegetables align with this behavior shift because they deliver concentrated nutrition in lightweight, mess-free formats ideal for desk drawers, gym bags, and car consoles. Single-serve freeze-dried snack packs (20-30 grams) are the fastest-growing SKU format. This format innovation addresses a pain point that conventional dried fruits struggle with: stickiness and sugar crystallization that deters on-the-go consumption.

Foods increasingly utilize functional ingredients

Food processors are discovering that freeze-dried fruits and vegetables offer functional benefits beyond flavor and color. When rehydrated during consumption (via milk in cereal, moisture in baked goods), freeze-dried pieces restore texture and release volatile aromatics that mimic fresh produce. This sensory performance is driving adoption in breakfast cereals, where freeze-dried strawberries and blueberries command premium positioning, and in bakery applications where freeze-dried vegetable powders (beet, spinach, carrot) enable natural coloring without artificial additives. For bakery manufacturers navigating clean-label mandates and color stability challenges, freeze-dried vegetable powders offer a dual solution: regulatory compliance and extended shelf life. The margin opportunity is substantial, natural colorants command 3 to 5 times the price of synthetic alternatives, and freeze-dried powders enable "colored by real food" claims that resonate with label-reading consumers.

Preference for clean-label, natural ingredients

As consumers increasingly demand transparency in food processing, freeze-drying emerges as a competitive frontrunner. This method, which avoids chemical additives, effectively preserves the original characteristics of food. The FDA's informal "natural" policy mandates that products should contain "nothing artificial or synthetic" and be "not more than minimally processed." This positions freeze-drying in a favorable light when compared with traditional preservation methods [3]Source: Matthew J. Goodman, “The ‘Natural’ vs. ‘Natural Flavors’ Conflict in Food Labeling,” fdli.org. Additionally, as regulations become stricter regarding natural claims, products relying on synthetic processing aids face greater compliance risks. This shift, however, creates significant opportunities for technologies that genuinely prioritize minimal processing. Private labels in the ready meals and soups market are benefiting from this trend. Suppliers of freeze-dried ingredients, who align with clean-label specifications, are particularly well-positioned to capitalize, especially in premium retail channels [4]Source: Government of Canada, “Sector Trends Analysis – Ready meals and soups in the United States,” canada.ca.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High freeze‑drying production and processing costs | -0.8% | United States and Canada manufacturing centres | Short term (≤ 2 years) |

| Competition from cheaper preservation alternatives | -0.6% | United States, Canada, Mexico price-sensitive retail | Medium term (2-4 years) |

| Supply-chain volatility in fresh produce sourcing | -0.5% | U.S. West Coast, Mexico agricultural regions | Short term (≤ 2 years) |

| Elevated retail prices versus fresh, frozen, or conventional dried options | -0.4% | U.S. mass retail, Mexico emerging middle class | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High freeze‑drying production and processing costs

Freeze-drying's capital intensity and operating expenses create structural barriers to market expansion. Industrial freeze-dryers require vacuum chambers, refrigeration systems, and condensers that cost USD 500,000 to USD 2 million per unit, with installation and commissioning adding 20% to 30%. These economics limit freeze-drying to high-value applications where consumers accept premium pricing. Smaller processors face additional disadvantages: batch-scale equipment (50-100 kg/cycle) operates at higher per-kilogram costs than continuous systems (500+ kg/cycle), and limited access to capital markets restricts technology upgrades. The strategic response for mid-sized players involves co-packing partnerships that amortize fixed costs across multiple brands, or contract manufacturing arrangements with large processors that offer excess capacity during off-peak seasons.

Competition from cheaper preservation alternatives

Freeze-dried products compete not only with fresh produce but also with air-dried, spray-dried, dehydrated, frozen, and canned alternatives that offer acceptable quality at lower price points. Frozen vegetables, which retain 80% to 90% of fresh nutrient content, cost USD 2 to USD 4 per kilogram, an order of magnitude below freeze-dried pricing. This competitive intensity is most acute in foodservice and institutional channels, where procurement managers prioritize cost over marginal quality improvements. The implication for freeze-dried manufacturers is segmentation discipline: focusing on applications where freeze-drying's unique attributes (ambient storage, lightweight, instant rehydration) justify premiums, rather than competing head-to-head in price-sensitive categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Berries Drive Premiumization

Fruits commanded 63.57% market share in 2025, anchored by strawberries, raspberries, and blueberries that deliver intense flavor and visual appeal in snack and ingredient applications. Strawberries are driven by their versatility in cereals, yogurt toppings, and standalone snacks. Vegetables will expand at 5.41% CAGR through 2031, propelled by food processors discovering their utility in soups, ready meals, and plant-based protein formulations where freeze-dried peas, corn, and mushrooms provide texture and umami depth. Peas and corn benefit from mechanical harvesting and year-round greenhouse production that stabilize input costs, while mushrooms command premiums for their savory profiles in Asian-inspired instant noodles and risotto mixes.

Potato freeze-dried products, primarily in powder and granule forms, serve institutional foodservice (instant mashed potatoes) and industrial applications (thickeners, binders) where their bland flavor profile and high starch content provide functional benefits. Carrot freeze-dried powders enable natural orange coloring in pasta, crackers, and baked goods, capturing demand from manufacturers eliminating artificial colorants. The segmentation insight is that vegetables' slower growth masks pockets of rapid expansion in specific applications, manufacturers who identify these niches early can establish category leadership before larger competitors enter. Apple freeze-dried products occupy a middle ground, offering mild flavor that blends into baked goods without overpowering other ingredients.

By Form: Chunks Gain as Snacking Evolves

Powder and granules held 47.51% share in 2025, driven by food processors embedding them into cereals, bakery goods, and beverage mixes, where fine particle size ensures even distribution and rapid rehydration. Chunks and pieces will grow at 5.47% CAGR through 2031, reflecting snack brands' pursuit of texture differentiation and visual appeal that whole or halved freeze-dried fruits deliver. Consumers perceive chunks as "less processed" than powders, creating a halo effect that justifies 15% to 25% price premiums in retail snack categories. Flakes occupy a middle ground, offering faster rehydration than chunks while maintaining more visual integrity than powders, making them ideal for instant oatmeal and soup mixes where appearance matters but rapid preparation is essential.

The form preference varies by application: cereals favor chunks for visual impact and textural contrast, while bakery applications prefer powders for color consistency and moisture management. Beverage applications (smoothie mixes, protein shakes) demand powders for complete dissolution, whereas camping meals and emergency rations favor chunks that rehydrate into recognizable vegetable pieces. Manufacturers investing in variable-cut equipment that produces multiple forms from a single production run can capture margin expansion by serving diverse customer needs without dedicated processing lines. The trend toward "visible ingredients" in packaged foods favors chunks and flakes over powders, suggesting that the 5.47% CAGR for chunks may prove conservative if transparency demands accelerate.

By Nature: Organic Certification Unlocks Premiums

Conventional products captured 73.85% share in 2025, reflecting their cost advantage and established supply chains that ensure year-round availability. Organic variants will accelerate at 5.17% CAGR through 2031, tracking consumer willingness to pay premiums for USDA Organic or Canada Organic certified products. The organic growth trajectory is constrained by supply-side factors: organic berry acreage in the United States grew annually from 2020 to 2024, lagging demand growth, creating persistent supply-demand imbalances that elevate input costs. Processors securing long-term contracts with organic growers, often requiring 3 to 5 year commitments with minimum-price guarantees, can lock in supply and capture margin expansion as retail prices rise faster than input costs.

The organic opportunity is most pronounced in direct-to-consumer channels (e-commerce, subscription boxes) where brand storytelling and transparency justify premium pricing, versus mass-market retail, where price-sensitive consumers trade down to conventional alternatives. Regulatory compliance factors include USDA National Organic Program standards that prohibit synthetic pesticides and require three-year land transition periods, creating barriers to rapid organic acreage expansion. Manufacturers investing in organic supply-chain development today will hold competitive advantages in 2027-2029 when demand is projected to outstrip supply, enabling pricing power and margin expansion.

By End-Use: Retail Channels Accelerate

Food processing commanded 43.57% share in 2025, embedding freeze-dried ingredients into cereals, soups, snacks, ice creams, desserts, and bakery products where they deliver functional benefits (texture, color, flavor) and clean-label positioning. Breakfast cereals represent the largest food-processing sub-segment, with freeze-dried strawberries and blueberries appearing in premium granolas and children's cereals, where visual appeal drives purchase decisions. Soups and snacks leverage freeze-dried vegetables (peas, corn, carrots) for instant rehydration and texture, while ice creams and desserts use freeze-dried fruit pieces for flavor bursts and visual contrast. Bakery and confectionery applications favor freeze-dried powders for natural coloring and moisture management, with beet powder enabling pink hues and spinach powder providing green tones without artificial additives.

Retail will grow fastest at 5.37% CAGR through 2031, reflecting e-commerce penetration that reduces distribution friction for premium-priced freeze-dried snacks, and specialty-store expansion (Whole Foods, Sprouts, natural-foods independents) that provide shelf space for emerging brands. Supermarkets and hypermarkets remain the largest retail sub-channel, offering mass-market reach but demanding slotting fees and promotional support that strain smaller brands' margins. Specialty stores provide a middle path, offering curated assortments and knowledgeable staff that facilitate trial and repeat purchase. The foodservice and HoReCa segment serves restaurants, hotels, and catering operations that value freeze-dried ingredients' extended shelf life and ambient storage, eliminating refrigeration costs and reducing waste from spoilage.

Geography Analysis

The United States held 78.41% market share in 2025, reflecting its mature freeze-drying infrastructure, established supply chains linking agricultural regions to processing hubs, and consumer willingness to pay premiums for convenience and nutrition. California, Oregon, and Washington supply the majority of freeze-dried berries, leveraging proximity to processing facilities in the Pacific Northwest that minimize transportation costs and preserve raw-material quality. The Midwest (Michigan, Wisconsin, Minnesota) provides freeze-dried vegetables, particularly corn and peas, from large-scale farms that achieve economies of scale in mechanical harvesting and post-harvest handling.

Canada represents the second-largest market, with growth driven by health-conscious urban populations in Toronto, Vancouver, and Montreal that mirror U.S. consumption patterns. Canadian processors benefit from lower electricity costs in hydropower-rich provinces (British Columbia, Quebec), reducing freeze-drying's energy burden by 20% to 30% versus U.S. averages. The strategic opportunity in Mexico involves targeting export markets (U.S., Canada) where "Made in North America" positioning satisfies USMCA local-content requirements, while building domestic brands that capture Mexico's emerging premium-snack segment before international competitors establish footholds. Mexico is the growth frontier, expected to expand at 6.03% CAGR through 2031 as nearshoring brings capacity closer to U.S. markets and a rising middle class embraces premium snacks.

Rest of North America (primarily Central American and Caribbean nations) remains nascent, with limited freeze-drying infrastructure and small addressable markets that deter investment. However, these regions offer raw-material sourcing opportunities: Costa Rican pineapple, Guatemalan berries, and Honduran vegetables can supply U.S. and Mexican processors seeking year-round availability and crop diversification. The geographic insight is that North America's freeze-dried market exhibits a core-periphery structure, with the U.S. as the dominant hub, Canada as a high-cost but innovation-oriented satellite, Mexico as the high-growth frontier, and Central America as a raw-material reservoir.

Competitive Landscape

The North American freeze-dried fruits and vegetables market exhibits moderate concentration, where established players command scale advantages in procurement, processing, and distribution, yet regional specialists and organic-focused entrants find profitable niches. White-space opportunities exist in savory freeze-dried snacks (vegetable crisps, seasoned mushroom pieces) that appeal to consumers seeking lower-sugar alternatives to fruit-based products, and in functional ingredient applications (freeze-dried vegetable powders for natural coloring, freeze-dried fruit extracts for flavor systems) where technical expertise and regulatory compliance create barriers to entry.

Technology adoption is reshaping competitive dynamics, with hybrid freeze-drying systems (microwave-assisted, infrared-assisted, ultrasound-assisted) enabling cost reductions that narrow the price gap with conventional drying methods. Early adopters of these technologies will gain advantages in price-sensitive channels (foodservice, private label) where freeze-drying's quality benefits were previously unaffordable. Patent activity in freeze-drying process optimization and equipment design indicates ongoing innovation, with recent filings focusing on energy recovery systems, continuous-feed mechanisms, and multi-stage drying that reduces cycle times.

Compliance with USDA National Organic Program standards, FDA GRAS requirements, and HACCP food-safety protocols creates regulatory moats that protect established players while deterring undercapitalized entrants. The strategic implication is that competitive advantage will increasingly derive from operational excellence (energy efficiency, yield optimization, supply-chain resilience) rather than product differentiation alone, as freeze-drying's quality benefits become table stakes and cost discipline determines profitability. Large processors leverage multi-site operations that enable year-round production by shifting between Northern and Southern Hemisphere raw-material sources, and continuous freeze-dryers that achieve per-kilogram costs below batch-scale equipment.

North America Freeze Dried Fruits And Vegetables Industry Leaders

European Freeze Dry Ltd.

Döhler Group SE

Freeze-Dry Foods Ltd.

Harmony House Foods Inc.

Chaucer Foods Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Glacial Freeze Dry acquired Foodynamics, a Wisconsin‑based freeze‑dry co‑manufacturer, expanding its production capacity and services for freeze‑dried product manufacturers and enabling broader contract manufacturing offerings.

- March 2025: Empire Freezing and Drying secured exclusive licensing rights for Sunkist® freeze‑dried fruit products, including fruit slices and purees, for distribution in U.S. retail stores starting in Q3 2025, expanding freeze‑dried snack offerings in North America.

- April 2024: Thrive Freeze Dry, a manufacturer of freeze-dried products, has entered into a definitive agreement to acquire Paradiesfrucht GmbH ("Paradise" or the "Company"), a global manufacturer of freeze-dried fruits, fruit preparations, yogurts, drops, powders, and granulates.

North America Freeze Dried Fruits And Vegetables Market Report Scope

Freeze-drying is a way to store fresh food so that it lasts longer without preservatives and can be kept on the shelf. The North America Freeze Dried Fruits and Vegetables Market is Segmented by Product Type (Fruits and Vegetables), Form (Powder Granules, Chunks/Pieces, and Flakes), Nature (Organic and Conventional), End-Use (Foodservice/HoReCa, Food Processing, and Retail), and Geography (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

By Product Type

| Fruits | Strawberry |

| Raspberry | |

| Pineapple | |

| Apple | |

| Mango | |

| Others | |

| Vegetables | Pea |

| Corn | |

| Carrot | |

| Potato | |

| Mushroom | |

| Others |

By Form

| Powder/Granules |

| Chunks/Pieces |

| Flakes |

By Nature

| Organic |

| Conventional |

By End-Use

| Foodservice/HoReCa | |

| Food Processing | Breakfast Cereals |

| Soups and Snacks | |

| Ice Creams and Desserts | |

| Bakery and Confectionery | |

| Others | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Others |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Fruits | Strawberry |

| Raspberry | ||

| Pineapple | ||

| Apple | ||

| Mango | ||

| Others | ||

| Vegetables | Pea | |

| Corn | ||

| Carrot | ||

| Potato | ||

| Mushroom | ||

| Others | ||

| By Form | Powder/Granules | |

| Chunks/Pieces | ||

| Flakes | ||

| By Nature | Organic | |

| Conventional | ||

| By End-Use | Foodservice/HoReCa | |

| Food Processing | Breakfast Cereals | |

| Soups and Snacks | ||

| Ice Creams and Desserts | ||

| Bakery and Confectionery | ||

| Others | ||

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

How fast is demand expected to grow after 2026?

The category is anticipated to expand at a 4.74% CAGR between 2026 and 2031.

Which product type currently leads sales?

Fruits, led by strawberries, raspberries, and blueberries, accounted for 63.57% of 2025 revenue.

Why are hybrid freeze-drying systems gaining traction?

Microwave- and infrared-assisted technologies lower energy and cut costs, improving margins.

Which country offers the fastest growth prospects?

Mexico is projected to post a 6.03% CAGR to 2031 thanks to nearshoring and a rising middle class.

Page last updated on: