Premium Spirits Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

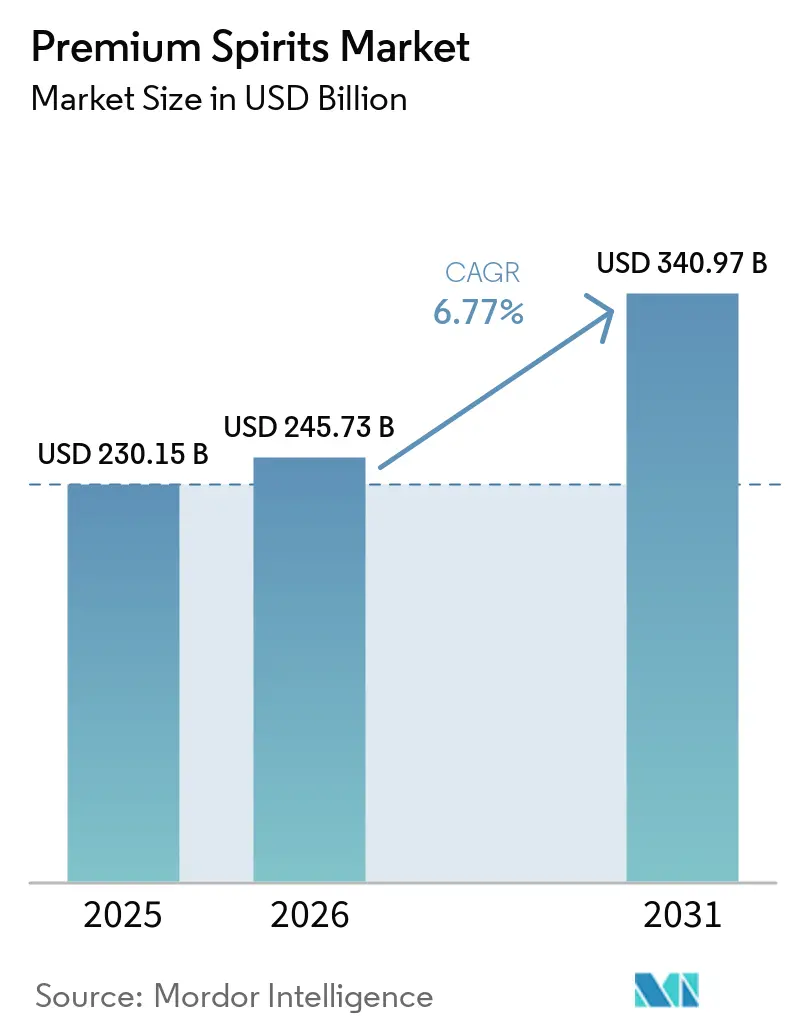

| Market Size (2026) | USD 245.73 Billion |

| Market Size (2031) | USD 340.97 Billion |

| Growth Rate (2026 - 2031) | 6.77% CAGR |

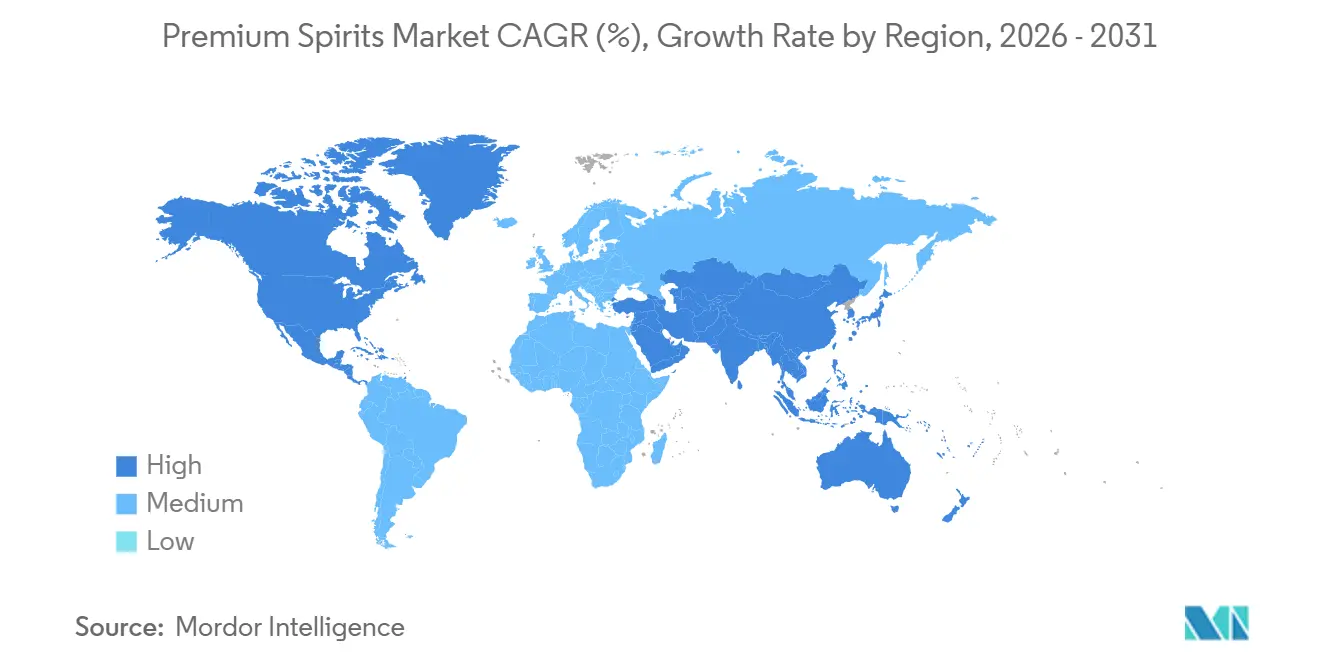

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Premium Spirits Market Analysis by Mordor Intelligence

The premium spirits market size is projected to expand from USD 230.2 billion in 2025 to USD 245.7 billion in 2026 and to USD 341 billion by 2031, registering a CAGR of 6.8% between 2026 and 2031. Despite fluctuations in overall alcohol demand, the premium spirits market is on an upward trajectory. This growth is fueled by consumers' willingness to spend more for curated drinking experiences. Factors such as brand heritage, product authenticity, and heightened visibility in bars bolster this market, allowing brands to command premium prices and maintain value, even amidst softening volumes. Global producers are adapting their strategies, leveraging premium ready-to-drink (RTD) offerings, travel retail avenues, and selective portfolio expansions to attract younger, occasional drinkers to the premium segment. Competitive dynamics are intensifying, with major players honing in on high-growth areas like white spirits, premium whisky, and innovation driven by specific occasions through acquisitions, divestments, and new launches. However, the market grapples with challenges: rising duties, a trend towards moderation, and a maze of distribution regulations. As a result, future successes hinge more on meticulous execution than on the category's overall momentum.

Key Report Takeaways

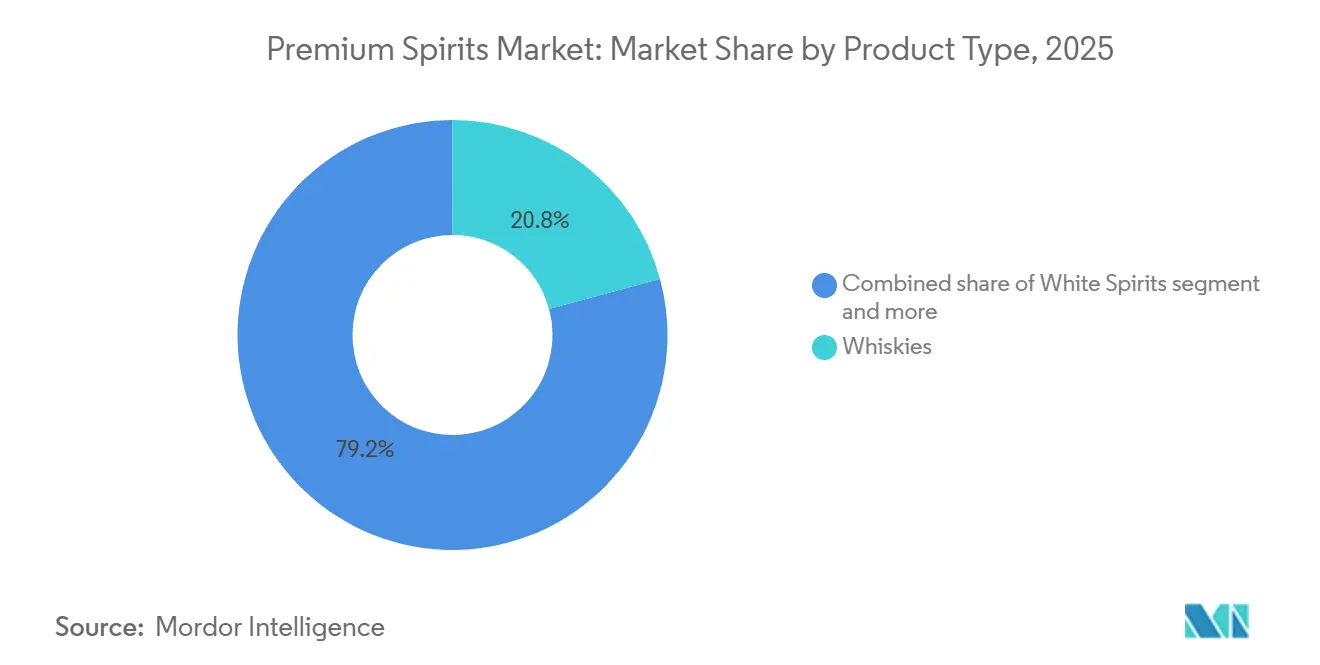

- By product type, whiskies accounted for the largest share of the premium spirits market, at 22.89% in 2025, while white spirits are projected to grow at the fastest CAGR of 4.07% during 2026-2031.

- By end user, men accounted for the largest share of the premium spirits market, at 74.22% in 2025, while women are projected to grow at the fastest CAGR of 4.42% during 2026-2031.

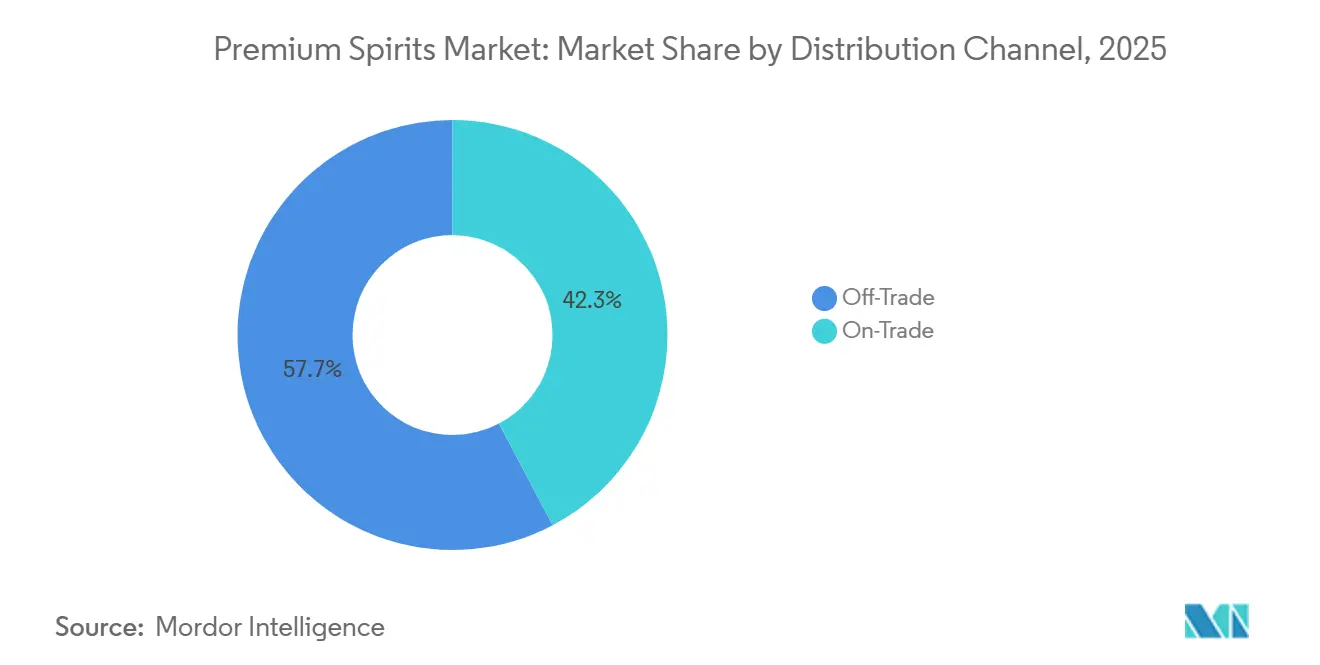

- By distribution channel, off-trade accounted for the largest share of the premium spirits market, at 57.71% in 2025, while on-trade is projected to grow at the fastest CAGR of 4.21% during 2026-2031.

- By geography, North America accounted for the largest share of the premium spirits market, at 36.87% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 6.16% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Premium Spirits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and trading up across core spirits occasions | +1.5% | Global | Medium term (2-4 years) |

| Rising disposable income in emerging urban middle classes | +1.2% | Asia-Pacific and South America | Long term (≥ 4 years) |

| Cocktail culture and premium on-trade recovery | +0.9% | Europe and North America core, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Brand premiumization through heritage, craft, and storytelling | +0.8% | Global, with Europe and North America leading | Medium term (2-4 years) |

| Provenance transparency and traceability as a purchase trigger | +0.6% | North America and Europe | Medium term (2-4 years) |

| Duty-free and travel retail recovery supporting premium mix | +0.7% | Global, with Asia-Pacific and Middle East and Africa core | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumization And Trading Up Across Core Spirits Occasions

Premiumization remains the clearest value driver in the premium spirits market, but it is now happening in a more selective way than it did during the earlier phase of broad-based price-led expansion. Consumers are still trading up, although they are doing it on fewer occasions and with stronger attention to whether a bottle or serve feels worth the extra spend. That behavior is helping categories with stronger quality cues, clear production stories, and visible serving rituals retain momentum even when the wider alcohol category looks softer. It also means the premium spirits market is becoming less tied to total category volumes and more tied to the quality of the purchase occasion itself. Accessible premium price points are therefore in a stronger position than ultra-luxury tiers, because they meet both aspiration and affordability without forcing consumers to abandon premium participation altogether. This shift is reshaping assortment, channel strategy, and new product planning across the premium spirits market, especially for brands that need repeat purchase rather than one-time prestige demand.

Rising Disposable Income In Emerging Urban Middle Classes

Rising incomes in emerging urban markets continue to provide one of the most durable support layers for the premium spirits market, especially where premium alcohol has historically been underpenetrated outside major cities. India stands out in the source draft as the clearest example, with premium and super-premium spirits demand widening beyond metropolitan centers into Tier 2 and Tier 3 cities as spending power, digital retail access, and social acceptance improve. This change matters because it broadens the addressable base for the premium spirits market from a narrow affluent cohort to a larger group of aspirational consumers making step-up purchases more frequently. It also gives multinational and local producers a stronger reason to build regional distribution, premium education, and entry-premium portfolios rather than rely only on top-city premium sales. The opportunity is not limited to one consumer profile, because the source draft also points to younger, more occasion-driven buying behavior and a wider mix of premium preferences across whisky, rum, vodka, and craft-led categories. Over the forecast period, the premium spirits market is likely to benefit most where income gains are matched by better channel reach and clear product positioning rather than by income growth alone.

Cocktail Culture and Premium On-Trade Recovery

Cocktail culture remains a strong commercial driver for the premium spirits market because it helps consumers experience branded premium spirits in a more social and more approachable setting than straight pours or bottle purchases. The on-trade is recovering its importance as a place where premium conversion happens, since premium ingredients, named spirit calls, and experience-led menus raise both consumer willingness to pay and operator interest in higher-value serves. In the source draft, branded ingredient visibility plays a central role, because consumers respond more positively when the spirit brand is clearly part of the drink rather than hidden behind a generic cocktail description. That matters for the premium spirits market because the bar and restaurant channel is not only a direct sales outlet, but also a discovery funnel that influences later off-trade purchases. Premium whisky, tequila, gin, and white spirits benefit especially from this pattern, since mixability, bartender recommendation, and premium menu placement support trial and repeat. As more operators use cocktails to lift ticket size and differentiate venues, the premium spirits market gains a channel that supports both value realization and brand building at the same time.

Brand Premiumization Through Heritage, Craft, And Storytelling

The premium spirits market is increasingly shaped by how well brands translate quality into a credible story around provenance, craft, aging, and maker identity rather than by bottle price alone. In practical terms, this gives producers room to command higher prices with limited structural change to production economics, provided the story feels specific enough to justify the step-up. The source draft shows this through launches that blend heritage with contemporary cultural positioning, which helps established names remain relevant across different age groups without weakening their premium image. This matters in the premium spirits market because consumers are becoming more selective, and selective buyers tend to favor brands that offer a clearer reason to choose them beyond familiarity. Travel retail and gifting channels strengthen this effect, since story-led packaging and limited releases work especially well when the purchase is tied to self-reward or social signaling. Over time, brands with shallow identity or unclear premium credentials are likely to find it harder to defend shelf space, bar listings, and pricing within the premium spirits market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Excise duties and tax-driven shelf price inflation | -0.9% | Europe and North America | Short term (≤ 2 years) |

| Health, moderation, and alcohol reduction trends | -0.7% | Global | Long term (≥ 4 years) |

| Fragmented licensing and route-to-market complexity | -0.4% | Asia-Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Advertising, labeling, and promotion restrictions | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Excise Duties and Tax-Driven Shelf Price Inflation

Higher duties are a significant short-term constraint on the premium spirits market. These duties elevate shelf prices just as consumers are willing to trade up, but only within set spending limits. In the UK, the duty increases over the last three years have surpassed 17%. Despite these tax hikes, spirits duty revenue dropped by GBP 94 million (USD 126.9 million) in the fiscal year 2025-26[1]Source: Scotch Whisky Association, "Spirits sector responds to £94m fall in UK spirits duty revenue", scotch-whisky.org.uk. This decline underscores how pricing pressures can dampen both demand and tax revenues. The impact is particularly severe on the more affordable segment of the premium spirits market. Here, consumers are more sensitive to price changes compared to those at the luxury end. Consequently, brands positioned as 'accessible premium' face a tighter challenge, needing to balance price, perceived value, and sales volume. In markets with intricate local tax systems, the challenge intensifies. Import duties, state levies, and specific markups compound, limiting pricing flexibility. If these fiscal pressures continue, the premium spirits market will increasingly lean towards brands with robust pricing power or those employing a more strategic approach to costs and distribution channels.

Health, Moderation, And Alcohol Reduction Trends

Moderation is increasingly shaping the premium spirits market, influencing not just the quantity consumers drink, but also their choice of alcohol over other beverages. In 2025, U.S. supplier revenue for distilled spirits dipped 2.2% to USD 36.4 billion, indicating that pressure on alcohol demand extends beyond lower-priced segments[2]Source: Distilled Spirits Council of the United States," Distilled Spirits Council Annual Economic Briefing 2025.", distilledspirits.org. The draft attributes this shift to factors like the use of GLP-1, cultural pushes for reduced alcohol consumption, and the rise of alternative formats, all vying for the occasions that traditionally favored spirits. While the premium spirits market remains somewhat shielded by consumers opting for a 'drink-less-but-better' approach, this buffer is eroding as drinking frequency declines. The rising quality of low- and no-alcohol alternatives increases the likelihood that premium-focused consumers will diversify their choices. Looking ahead, the premium spirits market must evolve its brand architecture to embrace moderation, all while preserving its premium identity and profit margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whiskies Hold Leadership While White Spirits Gain Speed

In 2025, whiskies claimed a 22.9% share of the premium spirits market, solidifying their position as the dominant product type globally. This dominance is bolstered by the global appeal of American bourbon, Scotch single malts, Irish whiskey, Japanese whisky, and Indian whisky. These diverse expressions not only deepen the category's geographic reach but also introduce multiple premium entry points. Whisky's versatility, being suitable for both sipping and cocktails, has fortified its demand in both retail and hospitality sectors. In North America, bourbon holds a special significance. Its cultural familiarity, relevance in gifting, and rich brand heritage ensure premium pricing, even amidst selective broader alcohol spending. The whisky segment in the premium spirits market enjoys a diverse range of price points, enabling consumers to gradually trade up rather than making a significant leap in expenditure.

White spirits are projected to lead the premium spirits market with a 4.1% CAGR through 2031. This growth is attributed to gin's evolution into an artisanal category and vodka's resurgence in premium ready-to-drinks (RTDs) and cocktails. White spirits' versatility allows them to seamlessly transition across social occasions, bar formats, and diverse consumer groups, unlike categories that predominantly focus on neat consumption. Notably, larger producers are strategically investing in craft gin assets, signaling a belief in the long-term significance of premium white spirits in their portfolios. Moving forward, while white spirits may not outright displace whisky, they are poised to capture a larger share of premium occasions and adaptable serving formats.

By End User: Men Retain the Core Base While Women Expand the Addressable Pool

In 2025, men accounted for 74.2% of the global value, solidifying their status as the dominant end-user group in the premium spirits market. This dominance stems from longstanding brand-building efforts in whisky, rum, and cognac, where marketing, gifting habits, and heritage imagery have traditionally spotlighted male consumers. However, the premium spirits market is evolving. While men still anchor sales, the market is witnessing a diversification in demand across age, gender, and lifestyle preferences. This evolution underscores the industry's need for a broader portfolio. Companies must stabilize core male demand while tailoring products and messaging to resonate with emerging premium audiences.

Women are projected to grow at a 4.4% CAGR through 2031, positioning them as the fastest-growing end-user group in the premium spirits arena. This shift is significant, indicating an additive demand rather than a mere shift away from male consumers. The growth is attributed to women's increasing engagement with luxury spirits, a heightened interest in premium whisky, and a pronounced appreciation for flavor, presentation, and cultural positioning elements that feel less bound to traditional category norms. This segment of the premium spirits market mirrors a broader trend in premium purchasing behavior, where consumers prioritize authenticity, values, and brand identity alongside traditional category norms. Consequently, the premium spirits market is likely to see a shift in product design, packaging, occasion framing, and communication strategies, moving towards an inclusive premium demand rather than being anchored to a singular historical buyer profile.

By Distribution Channel: Off-Trade Leads Current Value While On-Trade Builds Future Momentum

In 2025, off-trade channels commanded a dominant 57.7% share of the premium spirits market. This dominance is attributed to the advantages offered by liquor stores, specialty retailers, and other off-trade venues. These platforms enable shoppers to compare brands, explore diverse selections, and replenish their premium bottles at leisure. Furthermore, off-trade channels facilitate a smoother transition to premium products. Here, pricing transparency and promotional strategies can nudge consumers towards higher-end purchases, often without the hefty price tag associated with bar or restaurant visits. Specialty retailers, in particular, hold a pivotal position in the premium spirits landscape. They not only offer a wide range but also provide expert advice, cater to gifting needs, and engage consumers who are already inclined towards premium choices. Thus, even as premium occasions evolve, off-trade channels continue to anchor the premium spirits market, driving scale, household penetration, and repeat purchases.

Forecasts predict the on-trade channel will expand at the swiftest rate, boasting a 4.2% CAGR through 2031, solidifying its status as the most strategically vital growth avenue in the premium spirits arena. The significance of on-trade extends beyond mere revenue generation. Establishments like bars, restaurants, and hospitality venues play a crucial role in shaping consumer experiences, influencing trial, brand recognition, and perceived quality elements that packaged retail struggles to emulate. Insights reveal that premium cocktails, curated spirit selections, tasting events, and enhanced presentation not only elevate consumer choices but also influence subsequent off-trade purchases. Thus, the on-trade segment of the premium spirits industry functions dually as a sales avenue and an educational platform, especially for categories where bartender endorsements or cocktail contexts elucidate value. Moving forward, the premium spirits market stands to gain the most from producers who view on-trade and off-trade as interconnected facets of a singular premium journey, rather than isolated channel strategies.

Geography Analysis

In 2025, North America commanded a dominant 36.9% share of the premium spirits market, solidifying its position as the largest regional player. Anchored by the United States, which boasted a staggering USD 36.4 billion in spirits revenue, the region's strength is evident. While premium bourbon and Tennessee whiskey anchor the domestic base, vodka, tequila, and mezcal diversify offerings for various occasions and consumer types. Both Canada and Mexico bolster the regional profile: Canada fuels demand for premium whisky, and Mexico enhances its standing through domestic consumption and a robust export market for premium agave. Despite challenges such as tariff uncertainties and the complexities of imported spirits in supply chains and pricing, North America's scale, brand recognition, and advanced retail infrastructure ensure its leadership in the premium spirits arena.

Asia-Pacific is set to lead the charge, forecasting a robust 6.2% CAGR growth in the premium spirits market through 2031. India stands out as the primary growth driver, witnessing an uptick in both premium and super-premium segments across a broader array of cities and categories. The region's compelling growth narrative is fueled by rising incomes, urbanization, digital accessibility, and an eagerness to explore both imported and domestic premium spirits. While China remains significant, its trajectory appears uneven: domestic baijiu gifting is stabilizing, while select international channels and export activities are on the rise. Meanwhile, nations like Japan, South Korea, Taiwan, and segments of Southeast Asia enrich the narrative, bolstering demand for premium whisky and travel-linked purchases.

Europe, despite a slower expansion pace compared to Asia-Pacific and facing more stringent policy pressures than North America, remains a pivotal player in the premium spirits market. The region's advantages lie in its rich category heritage, robust on-trade demand bolstered by tourism, and the prominence of markets such as the UK, Germany, France, Italy, and Spain. However, the UK faces challenges: repeated duty hikes are straining consumer affordability and limiting volume growth, even as average selling prices hold steady. While South America and the Middle East and Africa currently operate on a smaller scale, they present emerging opportunities, particularly for premium whisky, rum, and travel retail gifting. The Middle East's travel retail hubs are especially noteworthy, with international departures and a penchant for premium gifting elevating the spirits mix[3]Source: Duty Free World Council (DFWC), " Global travel retail report 2025 part one" , dfwc.org. Collectively, the landscape reveals a premium spirits market led by North America's mature demand, buoyed by Asia-Pacific's rising premium adoption, and influenced by Europe's heritage and tourism, alongside select emerging markets.

Competitive Landscape

The premium spirits market has a moderate level of fragmentation, with a handful of global groups dominating and controlling many prominent brands. Meanwhile, numerous craft and regional producers vie for local niches. Diageo, Pernod Ricard, Bacardi, LVMH Moët Hennessy, and Suntory play pivotal roles in the premium spirits landscape. These giants leverage global distribution, brand heritage, and robust financial backing to drive innovation and depth across channels. Concurrently, smaller producers, with their emphasis on local provenance, craft identity, and nimble product development, often set consumer trends, underscoring their commercial relevance. This dynamic creates a dual-speed competitive landscape in the premium spirits arena, where global scale and local authenticity, though distinct in their strengths, both hold significance.

Acquisition-led premium portfolio building stands out as a primary strategic theme. Major producers are increasingly acquiring smaller brands, capitalizing on their inherent craft or local credibility, an asset that's challenging to cultivate from scratch. Highlighting this trend, Diageo's strategic investment in Nao Spirits and Pernod Ricard's foray into British craft distilling underscore how industry stalwarts are leveraging targeted acquisitions to bolster their presence in rapidly evolving subcategories. Additionally, portfolio rationalization emerges as a clear trend, with industry giants divesting from lower-priority assets. This strategic shift allows them to redirect capital towards categories and regions poised for robust long-term premium demand. Consequently, the premium spirits market is witnessing a move away from broad-based portfolio strategies, favoring more discerning decisions centered on category quality, pricing dynamics, and market approach.

Competition in the premium spirits market is increasingly driven by innovation. Established brands are adeptly using product extensions to engage younger, more versatile consumers, all while preserving their core brand equity. A prime illustration is the launch of Rémy V, which adeptly positions a luxury brand within the cocktail space, yet retains its premium essence. Similarly, Chivas Regal's introduction of a new 16-year-old variant leverages its heritage and cultural partnerships to broaden its appeal, without compromising its premium whisky stature. Companies are also adapting to evolving channels, introducing more travel retail exclusives, premium limited editions, and innovations tailored for bars, all aimed at enhancing visibility in high-purchase-intent areas. In summary, the premium spirits market is evolving towards a more disciplined and selective approach, with success increasingly hinging on the alignment of portfolio strategy, premium narrative, and channel execution.

Premium Spirits Industry Leaders

-

Diageo plc

-

Pernod Ricard S.A.

-

Bacardi Limited

-

Brown-Forman Corporation

-

LVMH Moët Hennessy Louis Vuitton SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Diageo unveils Stitzel Reserve 31-Year-Old Bourbon, distilled in 1992 and yielding only 176 bottles, positioned as an ultra-limited single-cask release designed to drive brand equity at the apex of the American whiskey premium spectrum.

- April 2026: Chivas Regal launches its first-ever 16-Year-Old expression, co-created with Formula 1 ambassador Charles Leclerc at a retail price of USD 70, marking the brand's first new permanent age statement in its modern history and targeting a broader, younger, affluent consumer base.

- March 2026: Rémy Cointreau launches Rémy V, a clear white spirit distilled from 100% French grapes and designed to capture cocktail-occasion and younger-consumer demand adjacent to the company's core cognac franchise.

- March 2026: Johnnie Walker launches Black Cask, a new permanent Scotch whisky expression aged exclusively in American white oak ex-bourbon barrels, available at USD 35 per 750 ml in the United States, extending the flagship range into a bourbon-crossover drinking occasion.

Global Premium Spirits Market Report Scope

| Brandy and Cognac |

| Liqueur |

| Rum |

| Tequila and Mezcal |

| Whiskies |

| White Spirits |

| Other Spirit Types |

| Men |

| Women |

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Other Off Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Morocco | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Brandy and Cognac | |

| Liqueur | ||

| Rum | ||

| Tequila and Mezcal | ||

| Whiskies | ||

| White Spirits | ||

| Other Spirit Types | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Other Off Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Morocco | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the premium spirits market by 2031?

The premium spirits market is forecast to reach USD 341 billion by 2031, rising from USD 245.7 billion in 2026 at a 6.8% CAGR.

Which product category leads premium spirits sales today?

Whiskies led product sales with a 22.9% value share in 2025, supported by strong demand across bourbon, Scotch, Irish whiskey, Japanese whisky, and Indian whisky.

Which product type is expanding the fastest through 2031?

White spirits is projected to grow at the fastest pace, with a 4.1% CAGR through 2031, helped by premium gin positioning and vodka’s role in cocktail and RTD formats.

Which region holds the largest share in premium spirits?

North America led with 36.9% share in 2025, supported by the scale of the United States and strong demand for premium whiskey, vodka, and tequila or mezcal.

Page last updated on: